Price Action Trend and Margin EquityThe Price Action Trend and Margin Equity indicator is a multifunctional market analysis tool that combines elements of money management and price pattern analysis. The indicator helps traders identify key price action patterns and determine optimal entry, exit and stop loss levels based on the current trend.

The main components of the indicator:

Money Management:

Allows the trader to set risk management parameters such as the percentage of possible loss on the position, the use of fixed leverage and the total capital.

Calculates the required leverage level to achieve a specified percentage of loss.

Price Action:

Correctly identifies various price patterns such as Pin Bar, Engulfing Bar, PPR Bar and Inside Bar.

Displays these patterns on the chart with the ability to customize candle colors and display styles.

Allows the trader to customize take profit and stop loss points to display them on the chart.

The ability to display patterns only in the direction of the trend.

Trend: (some code taken from ChartPrime)

Uses a trend cloud to visualize the current market direction.

The trend cloud is displayed on the chart and helps traders determine whether the market is in an uptrend or a downtrend.

Alert:

Allows you to set an alert that will be triggered when the pattern is formed.

Example of use:

Let's say a trader uses the indicator to trade the crypto market. He sets the money management parameters, setting the maximum loss per position to 5% and using a fixed leverage of 1:100. The indicator automatically calculates the required position size to meet these parameters ($: on the label). Or displays the leverage (X: on the label) to achieve the required risk.

The trader receives an alert when a Pin Bar is formed. The indicator displays the entry, exit, and stop loss levels based on this pattern. The trader opens a position for the recommended amount in the direction indicated by the indicator and sets the stop loss and take profit at the recommended levels.

General Settings:

Position Loss Percentage: Sets the maximum loss percentage you are willing to take on a single position.

Use Fixed Leverage: Enables or disables the use of fixed leverage.

Fixed Leverage: Sets the fixed leverage level.

Total Equity: Specifies the total equity you are using for trading. (Required for calculation when using fixed leverage)

Turn Patterns On/Off: You can turn on or off the display of various price patterns such as Pin Bar, Outside Bar (Engulfing), Inside Bar, and PPR Bar.

Pattern Colors: Sets the colors for displaying each pattern on the chart.

Candle Color: Allows you to set a neutral color for candles that do not match the price action.

Show Lines: Allows you to turn on or off the display of labels and lines.

Line Length: Sets the length of the stop, entry, and take profit lines.

Label color: One color for all labels (configured below) or the color of the labels in the color of the candle pattern.

Pin entry: Select the entry point for the pin bar: candle head, bar close, or 50% of the candle.

Coefficients for stop and take lines.

Use trend for price action: When enabled, will show price action signals only in the direction of the trend.

Display trend cloud: Enables or disables the display of the trend cloud.

Cloud calculation period: Sets the period for which the maximum and minimum values for the cloud are calculated. The longer the period, the smoother the cloud will be.

Cloud colors: Sets the colors for uptrends and downtrends, as well as the transparency of the cloud.

The logic of the indicator:

Pin Bar is a candle with a long upper or lower shadow and a short body.

Logic: If the length of one shadow is twice the body and the opposite shadow of the candle, it is considered a Pin Bar.

An Inside Bar is a candle that is completely engulfed by the previous candle.

Logic: If the high and low of the current candle are inside the previous candle, it is an Inside Bar.

An Outside Bar or Engulfing is a candle that completely engulfs the previous candle.

Logic: If the high and low of the current candle are outside the previous candle and close outside the previous candle, it is an Outside Bar.

A PPR Bar is a candle that closes above or below the previous candle.

Logic: If the current candle closes above the high of the previous candle or below its low, it is a PPR Bar.

Stop Loss Levels: Calculated based on the specified ratios. If set to 1.0, it shows the correct stop for the pattern by pushing away from the entry point.

Take Profit Levels: Calculated based on the specified ratios.

Create a Label: The label is created at the stop loss level and contains information about the potential leverage and loss.

The formula for calculating the $ value is:

=(Total Capital x (Maximum Loss Percentage on Position/100)) / (Difference between Entry Level and Stop Loss Level × Ratio that sets the stop loss level relative to the length of the candlestick shadow × Fixed Leverage Value) .

Labels contain the following information:

The percentage of price change from the recommended entry point to the stop loss level.

Required Leverage (X: ): The amount of leverage required to achieve the specified loss percentage. (Or a fixed value if selected).

Required Capital ($: ): The amount of capital required to open a position with the specified leverage and loss percentage (only displayed when using fixed leverage).

The trend cloud identifies the maximum and minimum price values for the specified period.

The cloud value is set depending on whether the current price is equal to the high or low values.

If the current closing price is equal to the high value, the cloud is set at the low value, and vice versa.

RU

Индикатор "Price Action Trend and Margin Equity" представляет собой многофункциональный инструмент для анализа рынка, объединяющий в себе элементы управления капиталом и анализа ценовых паттернов. Индикатор помогает трейдерам идентифицировать ключевые прайс экшн паттерны и определять оптимальные уровни входа, выхода и стоп-лосс на основе текущего тренда.

Основные компоненты индикатора:

Управление капиталом:

Позволяет трейдеру задавать параметры управления рисками, такие как процент возможного убытка по позиции, использование фиксированного плеча и общий капитал.

Рассчитывает необходимый уровень плеча для достижения заданного процента убытка.

Price Action:

Правильно идентифицирует различные ценовые паттерны, такие как Pin Bar, Поглащение Бар, PPR Bar и Внутренний Бар.

Отображает эти паттерны на графике с возможностью настройки цветов свечей и стилей отображения.

Позволяет трейдеру настраивать точки тейк профита и стоп лосса для отображения их на графике.

Возможность отображения паттернов только в натправлении тренда.

Trend: (часть кода взята у ChartPrime)

Использует облако тренда для визуализации текущего направления рынка.

Облако тренда отображается на графике и помогает трейдерам определить, находится ли рынок в восходящем или нисходящем тренде.

Оповещение:

Дает возможность установить оповещение которое будет срабатывать при формировании паттерна.

Пример применения:

Предположим, трейдер использует индикатор для торговли на крипто рынке. Он настраивает параметры управления капиталом, устанавливая максимальный убыток по позиции в 5% и используя фиксированное плечо 1:100. Индикатор автоматически рассчитывает необходимый объем позиции для соблюдения этих параметров ($: на лейбле). Или отображает плечо (Х: на лейбле) для достижения необходимого риска.

Трейдер получает оповещение о формировании Pin Bar. Индикатор отображает уровни входа, выхода и стоп-лосс, основанные на этом паттерне. Трейдер открывает позицию на рекомендуемую сумму в направлении, указанном индикатором, и устанавливает стоп-лосс и тейк-профит на рекомендованных уровнях.

Общие настройки:

Процент убытка по позиции: Устанавливает максимальный процент убытка, который вы готовы понести по одной позиции.

Использовать фиксированное плечо: Включает или отключает использование фиксированного плеча.

Уровень фиксированного плеча: Задает уровень фиксированного плеча.

Общий капитал: Указывает общий капитал, который вы используете для торговли. (Необходим для расчета при использовании фиксированного плеча)

Включение/отключение паттернов: Вы можете включить или отключить отображение различных ценовых паттернов, таких как Pin Bar, Outside Bar (Поглощение), Inside Bar и PPR Bar.

Цвета паттернов: Задает цвета для отображения каждого паттерна на графике.

Цвет свечей: Позволяет задать нейтральный цвет для свечей неподходящих под прйс экшн.

Показывать линии: Позволяет включить или отключить отображение лейблов и линий.

Длинна линий: Настройка длинны линий стопа, линии входа и тейк профита.

Цвет лейбла: Один цвет для всех лейблов (настраивается ниже) или цвет лейблов в цвет паттерна свечи.

Вход в пин: Выбор точки входа для пин бара: голова свечи, точка закрытия бара или 50% свечи.

Коэффиценты для стоп и тейк линий.

Использовать тренд для прайс экшна: При включении будет показывать прайс экшн сигналы только в направлении тренда.

Отображение облака тренда: Включает или отключает отображение облака тренда.

Период расчета облака: Устанавливает период, за который рассчитываются максимальные и минимальные значения для облака. Чем больше период, тем более сглаженным будет облако.

Цвета облака: Задает цвета для восходящего и нисходящего трендов, а также прозрачность облака.

Логика работы индикатора:

Pin Bar — это свеча с длинной верхней или нижней тенью и коротким телом.

Логика: Если длина одной тени вдвое больше тела и противоположной тени свечи, считается, что это Pin Bar.

Inside Bar — это свеча, полностью поглощенная предыдущей свечой.

Логика: Если максимум и минимум текущей свечи находятся внутри предыдущей свечи, это Inside Bar.

Outside Bar или Поглощение — это свеча, которая полностью поглощает предыдущую свечу.

Логика: Если максимум и минимум текущей свечи выходят за пределы предыдущей свечи и закрывается за пределами предыдущей свечи, это Outside Bar.

PPR Bar — это свеча, которая закрывается выше или ниже предыдущей свечи.

Логика: Если текущая свеча закрывается выше максимума предыдущей свечи или ниже ее минимума, это PPR Bar.

Уровни стоп-лосс: Рассчитываются на основе заданных коэффициентов. При значении 1.0 показывает правильный стоп для паттерна отталкиваясь от точки входа.

Уровки тейк-профита: Рассчитываются на основе заданных коэффициентов.

Создание метки: Метка создается на уровне стоп-лосс и содержит информацию о потенциальном плече и убытке.

Формула для вычисления значения $:

=(Общий капитал x (Максимальный процент убытка по позиции/100)) / (Разница между уровнем входа и уровнем стоп-лосс × Коэффициент, задающий уровень стоп-лосс относительно длины тени свечи × Значение фиксированного плеча).

Метки содержат следующую информацию:

Процент изменения цены от рекомендованной точки входа до уровня стоп-лосс.

Необходимое плечо (Х: ): Уровень плеча, необходимый для достижения заданного процента убытка. (Или фиксированное значение если оно выбрано).

Необходимый капитал ($: ): Сумма капитала, необходимая для открытия позиции с заданным плечом и процентом убытка (отображается только при использовании фиксированного плеча).

Облако тренда определяет максимальные и минимальные значения цены за указанный период.

Значение облака устанавливается в зависимости от того, совпадает ли текущая цена с максимальными или минимальными значениями.

Если текущая цена закрытия равна максимальному значению, облако устанавливается на уровне минимального значения, и наоборот.

Portfolio management

Broad Market MOEX non normalazeBroad Market MOEX - Relative Strength Indicator for MOEX Stocks

This indicator allows you to compare the price dynamics of major Moscow Exchange stocks relative to the selected asset during the trading session.

Features:

• Tracks 10 key MOEX stocks: Sberbank, Rosneft, Lukoil, Gazprom Neft, NOVATEK, Nornickel, Polyus, Tatneft, Surgutneftegas, Severstal

• Shows the percentage price change of each stock relative to the base price at the start of trading (default 9:00 MSK)

• Allows you to customize the base time for reference

• Clearly displays the strength and weakness of individual stocks relative to each other

• Helps identify leaders and laggards during the trading session

How to use:

1. Add the indicator to any MOEX stock chart

2. Adjust the base time if needed (default 9:00)

3. Monitor the relative dynamics of stocks

4. Use for:

- Finding strong/weak stocks

- Identifying sector rotation

- Intraday trading

- Correlation analysis

Color coding of lines helps easily identify each stock on the chart.

The indicator is useful for intraday traders and anyone monitoring the relative strength of stocks on the Moscow Exchange.

Altcoins DCA ScalperIntroduction

The Altcoins DCA Scalper is a Pine Strategy Script designed to automate Altcoins trading through 3Commas integration. It implements a Dollar-Cost Averaging (DCA) strategy that expands upon 3Commas' standard DCA capabilities, helping to manage risk while trading both long and short positions automatically.

This tool aims to assist both beginners exploring automated trading and experienced 3Commas users seeking dynamic DCA automation. The script is specifically designed for the 1-minute timeframe , where it has shown a good balance between performance and risk management. Complete setup typically takes less than 10 minutes, with a detailed guide making configuration straightforward for users of all experience levels.

------------------------------

🔶 What is DCA?

------------------------------

Dollar-cost averaging (DCA) refers to the practice of gradually increasing your position size at lower prices when trading long, or at higher prices when trading short, to achieve a better average entry price if the market moves against the initial entry . Instead of investing all capital at once, which could result in a significant drawdown if the price moves unfavorably, DCA spreads entries across different price levels to help manage potential drawdowns as they occur.

In this script, DCA is implemented through a system that:

🔹 Triggers safety orders only when/if needed (if take profit isn't reached quickly)

🔹 Dynamically adjusts order sizing based on market volatility

🔹 Automatically reduces take profit targets after each DCA order to increase the likelihood of a positive outcome

🔹 Can handle drawdowns depending on market volatility and settings

The images below illustrate two scenarios: one where an entry reaches the take profit directly, without activating DCA orders, and another where DCA is utilized, with the order closing positively after two DCA orders.

Case 1: Order closes in profit after entry

Case 2: Order closes in profit after 2 DCA orders (dynamically placed based on trend and volatility)

This DCA implementation aims to enhance standard 3Commas DCA by adding market-adaptive features while maintaining risk management principles.

------------------------------

🔶 Could this strategy script benefit you?

------------------------------

This script may be helpful if you are:

✅ Looking to automate your trading through 3Commas integration while maintaining full control of your assets

✅ Wanting to enhance 3Commas' standard DCA with market-adaptive features that consider:

Multi-timeframe trend analysis

Real-time volatility assessment

Dynamic safety order sizing and timing

✅ Seeking to minimize chart monitoring through full automation of:

Entry and exit decisions

Safety order management

Risk controls

✅ Interested in comprehensive performance tracking with:

Real-time position metrics

Detailed backtesting capabilities

Risk/reward analysis

Backtesting Metrics (script performance over the backtesting period - which is approx. 15 days on the 1min timeframe with the TradingView Pro Plan):

Current/Open Deal Metrics (the deal is currently under DCA, and waiting for further actions to close):

✅ Looking for trading automation that remains easy to set up and use

Note: While this script provides trading automation, successful trading requires proper education, risk management, and regular performance monitoring. No automated tool can guarantee trading success or profits.

------------------------------

🔶 How it Works

------------------------------

The Altcoins DCA Scalper provides trading automation through:

Market Analysis

* Multi-timeframe trend analysis (1m to 1d) for market direction and entry validation

* Volatility assessment (1h, 4h, 24h) benchmarked against TOTAL3 (excluding Top10 Altcoins and Stablecoins)

* Real-time adjustment of DCA parameters based on:

* Current volatility class (low/medium/high) vs. overall Altcoins market

* Market trend strength

* Price action dynamics

Trading Execution

* Position opening aligned with detected market trends

* "Beast Mode" base order sizing that increases position size during strong trends

* Dynamic take-profit targets that automatically reduce after each safety order to increase the likelihood of positive exits

* Dynamic DCA with safety orders that can:

* Adapt timing based on volatility

* Scale order sizes based on market conditions

* Handle 30-50% drawdowns depending on volatility class

* Execute up to 6 safety orders per position

Risk Management

* Emergency exits during extreme market events:

* "Black Swan" protection for long positions

* "God-Candle" protection for short positions

* Configurable stop-loss with volatility-based placement

* Trend-switch management with automated position reversal

* Position aging controls to prevent capital lock-up

* Leveraged trading protection with a pre-liquidation exit system

Integration & Automation

* Quick setup with two 3Commas bots (typically under 10 minutes)

* Fully automated signal generation and execution through 3Commas

* Detailed performance tracking including:

* Real-time position metrics

* DCA depth analysis

* Win rate and ROE calculations

* Pre-configured settings optimized for most pairs

* Multiple customization options for experienced users

Note: While this strategy employs automation and risk management, trading always carries the risk of loss. No system can guarantee profits, and market conditions significantly impact performance. Always do your own research and monitor your positions closely.

------------------------------

How to Use

------------------------------

Setting up the Altcoins DCA Scalper is quick and facilitated by the User Interface:

1️⃣ 3Commas/TradingView Setup

* Create two 3Commas accounts if using the FREE plan:

* One account for Long Bot

* One account for Short Bot

* This split allows full functionality while staying within 3Commas' free tier limits

* You do not need two separate accounts if you have a Paid 3Commas subscription

* While a free TradingView account works with the script, it limits you to one trading pair and a 4-day backtesting history. A paid TradingView subscription removes these limitations (such as the "Essential" plan).

2️⃣ Bot Configuration

* Create one Long and one Short DCA Bot in 3Commas

* Follow the setup guide available in the script itself for hassle-free configuration

* Copy Bot IDs and Email Token for script connection

* No complex settings needed - the script manages all DCA parameters by itself

3️⃣ Script Implementation

* Apply the script to your TradingView charts

* Use the built-in backtesting to analyze performance on different pairs

* Focus on USDT.P futures pairs with good volatility

4️⃣ Trading Activation

* Create TradingView alerts for each trading pair you want to activate

* Example: Set an alert for BINANCE: XRPUSDT.P following the in-script guide

* The script automatically manages all aspects:

* Entry and exit decisions

* DCA execution

* Risk management

* Position monitoring

Capital Requirements

* Important: Ensure sufficient capital to cover all activated pairs

* Consider volatility class when allocating capital to specific pairs

Once setup is complete, the script operates fully automatically while you maintain complete control of your funds through 3Commas and your exchange.

Note: While the setup is straightforward, always start with a small number of pairs and monitor performance before expanding. Trade responsibly and never risk more than you can afford to lose.

------------------------------

Explaining the Settings

------------------------------

The Altcoins DCA Scalper offers mulitple customization options during the setup process. All settings include detailed tooltips and default values.

Core Settings Sections:

1️⃣ 3Commas Connection

* Bot IDs and Email Token configuration

* Leverage settings (1x to 5x supported)

* Detailed 3Commas bot setup guide included

* Automatic bot control configuration

2️⃣ Trading Parameters

* Capital allocation per trade

* Timeframe verification

* Alert system setup

* Backtesting period control

* Performance tracking preferences

3️⃣ Advanced Features

🔹 Risk Management Suite

* Emergency exit controls (to strengthen protection against extraordinary market events)

* Customizable stop-loss system

* Trend-based exit management

* Position aging controls

* Liquidation protection features

* Advanced DCA controls

🔹 Performance Analytics

* Real-time position monitoring

* Comprehensive backtesting metrics

* DCA depth analysis

* Win rate calculations

* Capital efficiency tracking

🔹 Technical Optimizations

* Exchange minimum order adjustment

* Trading pair name override capability

* System stability controls

* Error handling mechanisms

🔹 Interface Customization

* Theme selection

* Chart overlay options

* Warning display preferences

* Performance metrics visibility

All settings come pre-configured but can be fully customized based on your trading preferences and risk tolerance. The script includes tooltips and setup guides for each option.

Note: While default settings may be tested, market conditions vary and all trading involves risk. Monitor performance and adjust settings according to your risk management requirements.

------------------------------

Frequently Asked Questions

------------------------------

Here are some common questions you may have, and our answers:

❓ Is this tool only for experts? I'm new to algo trading, can I use it?

No, the Altcoins DCA Scalper could be used by both beginners and experienced traders. The setup process is guided, and the algorithm handles all the calculations in the background.

❓ I'm not familiar with 3Commas. Is that a problem?

While the script is designed to work with 3Commas, a step-by-step guide is provided within the script to help you set up your 3Commas accounts and bots, if needed.

❓ Do I need to constantly monitor the script after it's set up?

No, after the initial setup and configuration, the script operates autonomously. It handles all aspects of trading including entries, exits, DCA management, and risk controls. However, we recommend:

* Checking performance metrics daily

* Reviewing position statistics weekly

* Adjusting pair selection monthly based on performance

* Monitoring overall market conditions that might require adjustments

❓ Can I use it with leverage?

Yes, the script is designed to work with leverage up to 5x on perpetual futures pairs (USDT.P). It includes specific features for leveraged trading:

* Dynamic safety order placement based on distance to liquidation

* Pre-liquidation exit system to minimize exchange fees

* Adjustable take-profit targets optimized for leveraged positions

* Emergency exit system for extreme market movements

* Optional risk controls specific to leverage:

* Automatic exit in the liquidation danger zone

* Position size scaling based on leverage level

* Safety order adjustments for different leverage settings

While leverage can amplify returns, it also increases risk. We recommend starting with lower leverage (2x), or no leverage at all, until familiar with the script's operation.

❓ Does this script guarantee profits?

No, no script or trading strategy can guarantee profits. The Altcoins DCA Scalper provides a framework for implementing an automated DCA strategy, but your success will depend on many different factors and conditions.

❓ Do I need to understand the complex algorithms used in the script?

No, it’s not necessary. The logic is handled by the script, and you do not need to understand every detail to use it effectively. However, a basic knowledge of DCA concepts will be beneficial.

❓ Can I use this script with spot or leveraged trades?

The script is optimized for USDT.P pairs (perpetual futures) with leverage up to 5x. This allows:

* Automatic long/short position management

* Increased capital utilization

* Full DCA functionality without holding the underlying assets

* Enhanced risk management features specific to futures

While spot trading is possible, it requires holding underlying assets for shorts and doesn't access the script's full capabilities.

❓What timeframe should I use?

This script is optimized for the 1-minute timeframe , which is the recommended setting for the best balance between performance, capital efficiency, and risk. While we recommend using the tool on the 1 minute TF, it would work on other timeframes too.

❓ What happens if my internet/computer goes down?

Since the script sends signals from Tradingview to 3Commas (which executes trades on your exchange), your positions and DCA management continue to function even if your TradingView chart is closed or your computer is off. The script only needs to be active to generate new signals.

❓ How are the DCA parameters determined?

The script dynamically adjusts DCA parameters based on:

* The pair's volatility class (compared to the overall altcoin market)

* Current market conditions and volatility

* Position direction (long/short)

* Leverage settings

* Number of safety orders already executed

This allows for adaptive/dynamic DCA compared to static or %-based parameters.

❓ What exchanges are supported?

The script works with any exchange supported by 3Commas for futures trading (approximately 15 different crypto Exchanges). However, it's optimized for Binance Futures (USDT.P pairs) due to its high liquidity and for consistency.

❓ What happens during extreme market conditions?

The script includes some (optional) protective measures that can be activated:

* Emergency exits during sharp and abnormal market moves

* Automatic adjustment of DCA parameters during high volatility

* Position closure on significant trend changes

* Special handling of aged positions

These features aim to protect capital during unusual market conditions.

❓How many pairs can I trade simultaneously?

This depends on your total capital. As a general indication, define the number of pairs to activate based on:

* Total available capital

* Desired position size per pair

* Risk tolerance

* Pairs' volatility class

------------------------------

Final Thoughts

------------------------------

We believe that your trading performance will greatly depend on your selection of appropriate trading pairs for this script (high volatility), and your commitment to regularly monitoring its performance and adjust the settings, rather than on the script alone.

------------------------------

⚠️ Risk Disclaimer

------------------------------

Remember that trading involves risk, and most day traders experience losses. This script is for educational and informational purposes only. Past performance does not guarantee future results. This is not financial advice, and you should always do your own research (DYOR). Trade responsibly with capital you can afford to lose.

The Altcoins DCA Scalper is an independent tool and is not endorsed, connected, or validated by TradingView.

3Commas is a third-party service, and TradingView is not responsible for the 3Commas integration or the performance of 3Commas bots. You are solely responsible for the security and management of your 3Commas account. Do not share your 3Commas access credentials (like login information, Bots-ID, Email Token) with anyone. The Author of the script has no access to such information, and nobody (but you) should.

Dual SD Kijun | QuantEdgeBIntroducing Dual SD Kijun by QuantEdgeB

Dual SD Kijun | QuantEdgeB is a trend-following and volatility-based indicator that enhances the traditional Kijun-Sen with dual Standard Deviation (SD) filtering and a normalized Kijun structure. This system refines trend confirmation and breakout signals by combining price deviation analysis with a dynamic normalization mechanism, providing traders with clear and adaptive entry points.

Key Features:

1. Kijun-Sen with Standard Deviation (SD) Filtering 📏

- The indicator builds upon the Kijun-Sen concept by calculating the midpoint of the highest and lowest price over a given period.

- Two Kijun calculations:

1️⃣ Primary Kijun (Shorter Length)

2️⃣ Normalized Kijun (Longer Length)

- The Kijun acts as the base trend filter, smoothing price action while adapting to volatility.

2. Standard Deviation Weighted Bands (SD Kijun) 📊

- Volatility-adjusted trend confirmation using SD bands around the Kijun-Sen.

- Helps detect trend acceleration and potential reversals based on price deviation.

3. Normalized Kijun for Trend Validation 🔄

- A dynamic normalization function scales the Kijun-Sen relative to price.

- Short EMA smoothing reduces noise for more accurate signals.

- Long EMA smoothing smooths the normalized deviations, refining trend confirmation.

4. Dual Signal Confirmation (SD + Normalized Kijun) ✅❌

- Long Signals (🔵): Price must break above the upper SD filter while the normalized Kijun confirms trend strength.

- Short Signals (🔴):Price must drop below the lower SD filter while the normalized Kijun confirms bearish conditions.

- The dual confirmation reduces false breakouts and ensures stronger trend validation.

___

How It Works:

1. Kijun Calculation :

- Computes the midpoint of the highest and lowest prices over a defined period.

- Uses two Kijun-Sen lengths to separate short-term and normalized trends.

2. Standard Deviation Filtering :

- Calculates the price deviation around the Kijun to determine potential breakout points.

- Price must close above/below SD thresholds to trigger a potential trend continuation.

3. Normalization Process :

- The normalized Kijun is divided by price, helping scale deviations across assets.

- Two smoothing factors (Short & Long) refine the normalized Kijun structure.

- Ensures signals remain consistent across different market conditions.

4. Final Signal Production :

- Bullish Confirmation (🔵): Price closes above the upper SD band and the normalized Kijun confirms strength.

- Bearish Confirmation (🔴): Price closes below the lower SD band and the normalized Kijun signals weakness.

___

Use Cases:

✅ For Trend Trading & Breakout Confirmation

- The SD bands help filter strong breakouts, ensuring valid long and short signals.

- If SD bands expand, it signals increased volatility and potential momentum shifts.

- Works best when paired with momentum indicators (e.g., ADX, RSI) to confirm trend strength.

✅ For Trend Validation with Normalized Kijun

- The normalized Kijun acts as an additional filter to ensure price movements are sustainable.

- If both SD and Normalized Kijun confirm a trend, the probability of a strong continuation increases.

✅ For Detecting Market Reversals

- If price fails to break SD bands or the normalized Kijun diverges, it may indicate a weak trend or potential trend exhaustion.

- Helps traders avoid false breakouts and focus on high-probability setups.

__

Customization Options:

1. Kijun Lengths 🏗️

- Primary Kijun Length (Default: 24)

- Normalized Kijun Length (Default: 34)

2. Standard Deviation Settings 📊

- SD Length (Default: 40)

- Long SD Weight (Default: 0.98)

- Short SD Weight (Default: 1.02)

3. Normalization Smoothing 🔄

- Short Normalized Smoothing (Default: 1)

- Long Normalized Smoothing (Default: 1)

4. Color Modes & Visual Enhancements 🎨

- Default, Solar, Warm, Cool, Classic ,X

___

Conclusion:

The Dual SD Kijun | QuantEdgeB provides a powerful and adaptive trend confirmation system by combining standard deviation filtering with a normalized Kijun mechanism. By ensuring dual validation, traders can filter out weak signals and focus on stronger trends. Whether used for breakout confirmation or trend validation, this indicator offers precise, data-driven signals for improved market decision-making. 🚀📈

🔹 Disclaimer: Past performance is not indicative of future results. No trading indicator can guarantee success in financial markets.

🔹 Strategic Consideration: As always, backtesting and strategic adjustments are essential to fully optimize this indicator for real-world trading. Traders should consider risk management practices and adapt settings to their specific market conditions and trading style.

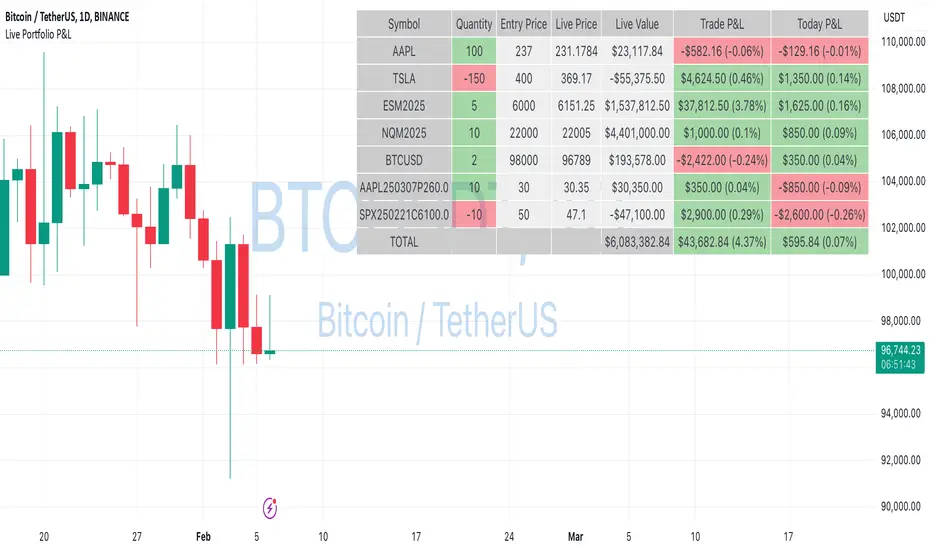

Live Portfolio P<his script calculates live P&L (Profit & Loss) for up to 40 instruments — stocks, ETFs, options, futures, and Forex pairs supported by TradingView. Instead of juggling numerous inputs, you paste your portfolio in CSV format into a single text field, and the script handles the rest. It parses each position and displays a comprehensive table showing the symbol, current price, position value, total P&L, and today’s P&L—all updated in real time.

Key Features

CSV Portfolio Input – Effortlessly import all your positions at once without filling in multiple fields. You can export the position from your broker, save it in the required format, and paste it into this script.

Supports Various Asset Classes – Works with any instrument that TradingView provides data for, including futures, options, and Forex.

Up to 40 Instruments – Track a broad and diverse set of holdings in one place.

Real-Time Updates – Get immediate feedback on live price changes, total value, and current P&L.

Today’s P&L – Monitor your daily performance to gauge short-term trends.

CSV is consumed in the following format:

Symbol (supported TradingView instruments)

Entry Price

Quantity (negative for short position)

Lot Size (for futures/options, it might not be one)

For example:

AAPL,237,100,1

TSLA,400,-150,1

ESM2025,6000,5,50

Planned Enhancements

Multi-Currency Support – Automatically convert and display your positions’ values in different currencies.

Advanced Metrics – Get deeper insights with calculations for drawdown, Sharpe ratio, and more.

Risk Management Tools – Set stop-loss and take-profit levels and receive alerts when thresholds are hit.

Option Greeks & Margin Calculations – Manage complex option strategies and track margin requirements.

Questions for You

What additional features would you like to see?

Are there any specific metrics or analytics you’d find especially valuable?

How might this script fit into your current trading workflow?

Feel free to share your thoughts and suggestions. Your feedback will help shape future updates and make this tool even more helpful for traders like you!

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Altcoins Screener [SwissAlgo]Introduction: The Altcoins Screener at a Glance

The Altcoins Screener is a cryptocurrency analysis tool designed to provide an overview of potential trading opportunities across multiple crypto coins/tokens and categories. By combining technical analysis, price action assessment, and social metrics (via LunarCrush data), it presents market information and trading signals for a broad range of altcoins (approx. 300 USDT.P pairs of 9 crypto categories).

The screener is designed to consolidate market information onto a single chart , aiming to streamline the analysis of market conditions. It provides a consolidated market overview, which can simplify the assessment of market conditions, compared to monitoring individual charts with several layered indicators.

Key Features:

🔹 Multi-category analysis covering 300 crypto pairs of 9 categories on a single chart (Layer 1 & Top Coins, Layer2 & Scaling, Defi & Landing, Gaming & Metaverse, AI & Data, Exchanges & Trading, NFT & Social, Memes & Community, Other, User's Custom Portfolio).

🔹 Technical analysis with trade signals (Long/Short) based on an aggregated view of technical and social data points

🔹 Social sentiment integration through LunarCrush metrics (GalaxyScore, AltRank, Social Sentiment)

🔹 Real-time market scanning provides automated alerts when market conditions for specified coins/tokens potentially change.

🔹 Custom watchlist support for personalized monitoring (users can define a custom category containing a set of specific cryptocurrencies, i.e. own portfolio).

The screener presents data in a table format, using color-coded indicators to aid visual analysis. Detailed technical information is also provided. The assessments/trade signals provided by this indicator should be considered as one input among many when forming your trading strategy.

--------------------------------------

What It Does

The Altcoins Screener is a cryptocurrency analysis tool that offers:

Data Display and Analysis (Technical/Social):

🔹 Technical Metrics

* Technical Raw Data : Displays raw values for a range of technical indicators, including RSI, Stochastic RSI, DMI/ADX, RVI, ATR, OBV, and Hull Moving Averages (including their recent trends and potential significance).

Detailed view of key technical indicators, for further analysis and evaluation:

* Technical Analysis (Summary) : Provides a summarized interpretation of technical conditions based on aggregated parameters:

* Price Action

* Trend

* Momentum

* Volatility

* Volume

Summarized view of confluences for potential long/short bias:

🔹 Social Metrics (LunarCrush) : Presents data from LunarCrush®, including Galaxy Score®, AltRank®, and Social Sentiment® (including their recent trends and potential significance).

Lunarcrush data for the top 10 coins for each crypto category:

🔹 PVSRA (Price Volume & Market Makers Activity) Candles : Shows special candles highlighting potential market maker activity and volume anomalies, helping identify possible manipulation zones (including imbalance zones, i.e. price areas that market makers may revisit)

--------------------------------------

Key Features:

Automated trade signals (Long/Short) are generated based on algorithmic calculations and signal confidence levels across technical and social data points. These signals are intended to be used as one component of a broader trading strategy.

Custom sensitivity settings allow users to adjust the analysis timeframe (options: 1D, 2D, or 1W). Higher timeframes may provide a broader perspective, while the 2D setting is the default configuration.

Multi-category analysis covering a selection of approximately 300 crypto pairs across 9 predefined crypto categories.

Custom symbol selection: Users can define a custom list of up to 10 symbols for focused monitoring.

Automated Alerts to track potential trend changes across crypto categories (Long to Short to Neutral, or vice versa)

Visual Interface:

Organized table display with color-coded indicators to aid interpretation.

Clear and efficient format for scanning market information.

--------------------------------------

Target Audience

🔹 The screener is designed for cryptocurrency traders who:

Need to efficiently monitor multiple USDT perpetual futures markets

Use technical analysis in their trading decisions

Want to track sector-wide movements across crypto categories

🔹 Suitable for different trading styles:

Scalpers requiring quick market assessment

Swing traders analyzing multi-day trends

Position traders monitoring longer-term setups

The color-coded interface makes it accessible for intermediate traders while providing detailed metrics for advanced users. A basic understanding of technical analysis and crypto trading is recommended.

--------------------------------------

How It Works

The Altcoins Screener evaluates cryptocurrencies through a multi-layered analysis:

🔹 Core Analysis Components

Each parameter combines multiple indicators for comprehensive evaluation:

Price Action

EMA crossovers and momentum

Support/resistance zones

Candlestick patterns

Trend

Hull Moving Average system

DMI/ADX trend strength

Multi-timeframe confirmation

Momentum

RSI/Stochastic RSI readings

MACD convergence/divergence

Oscillator confirmations

Volatility

RVI/ATR measurements

Bollinger Bands behavior

Historical volatility trends

Volume

OBV trend analysis

Volume/price correlations

Volume profile assessment

🔹 Signal Generation Process

1. Real-time data collection across timeframes

2. Weighted indicator calculations

3. Parameter aggregation and analysis

4. Signal strength determination

5. Color-coding and alert generation

--------------------------------------

How to Use

🔹 Initial Setup:

Add the indicator to a chart (use the 1D timeframe)

Select your preferred crypto category or create a custom list

Choose between Technical Analysis or Technical Metrics view

Set data sensitivity based on your trading style

🔹 Using the Technical Analysis View:

Monitor color-coded dots for quick market assessment

Green: bullish conditions

Red: bearish conditions

Gray: neutral conditions

Check the "Trade Signal" column for potential Long/Short entries signaled by confluences among technical and/or social data points

🔹 Using the Technical Metrics View:

Review detailed numerical values

Monitor slopes (↑↓ arrows) for the most recent trend direction of each data point

Watch for pivotal points (highlighted cells): these are data points that suggest potential trend reversals

Focus on the confluence of multiple indicators

The technical metrics view corroborates the conclusions shown in the Technical Analysis View, providing more details about some critical data points.

🔹 Alert Configuration:

Enable Technical Alerts for signal notifications (which coin/token seems most suited for Long or Short trades, and which coin/token is in a neutral/uncertain state for trading = "No Trade")

Configure alert conditions based on trading style

Set timeframe-appropriate sensitivity

Monitor alert messages for trade signals

Instructions on how to set alerts are provided in the script (enable "Signals Setup Instructions" in User Interface to get a step-by-step guide about setting up alerts)

Best Practices:

Confirm signals across multiple timeframes

Use appropriate sensitivity for your trading style

Monitor multiple categories for sector rotation

Combine signals with your trading strategy

Verify signals with price action confirmation and deep dive into the charts of your potential targets

--------------------------------------

About the Settings

🔹 Crypto Category Selection

Layer 1 & Major: Top market cap coins (BTC, ETH, XRP,...), established protocols

Layer 2 & Scaling: ETH L2s, scaling solutions

DeFi & Lending: Decentralized finance protocols

Gaming & Metaverse: Gaming and virtual world tokens

AI & Data: Artificial intelligence and data projects

Exchange & Trading: Exchange tokens, trading protocols

NFT & Social: NFT platforms, social tokens

Memes & Community: Community-driven tokens

Others & Misc: Other categories

Custom Category: User-defined list (up to 10 symbols)

Data Type Options

Technical Analysis: Color-coded summary view

Technical Metrics: Detailed numerical values of some key technical data points

Sensitivity Settings

Higher: Shorter timeframe, more frequent signals

Default: Balanced timeframe, standard signals

Lower: Longer timeframe, stronger signals

Alert Settings

Technical Alerts: Trade signal notifications

Data Timeframe: Minimum 1D required

Theme: Dark/Light mode options

Note: All analysis is performed on USDT Perpetual Futures pairs from Binance

--------------------------------------

FAQ

Q: Does the screener work on other exchanges besides Binance?

A: No, it's designed specifically for Binance USDT Perpetual Futures pairs. Binance offers the highest liquidity and trading volume in the crypto derivatives market, making it ideal for technical analysis. The extensive range of trading pairs and reliable data streams help ensure more accurate signals and analysis. Using a single high-liquidity exchange also helps avoid inconsistencies that could arise from aggregating data across multiple platforms with varying liquidity levels.

Q: What's the minimum timeframe required?

A: The screener requires a minimum 1D (daily) timeframe. This requirement ensures that the technical analysis has sufficient data points for reliable signal generation. Lower timeframes can produce more noise and false signals, while daily timeframes help filter out market noise and identify stronger trends.

Q: Why are some social metrics showing "NaN"?

A: "NaN" (Not a Number) appears when cryptocurrencies don't have associated LunarCrush data. This typically occurs with newer tokens or those with lower market caps. The technical analysis remains fully functional regardless of social metric availability, as these are complementary data points.

Q: How often are signals updated?

A: Signals update with each new candle on the selected timeframe (1D, 2D, or 1W). For example, on the default 2D setting, signals are recalculated every two days as new candles form. This helps reduce noise while maintaining timely analysis of market conditions.

Q: Can I add spot trading pairs?

A: No, the screener is optimized for Binance USDT perpetual futures pairs for data consistency and analysis purposes. While spot and perpetual prices typically align closely due to arbitrage, using a single data source (Binance) and contract type (USDT perpetual) ensures uniform data quality and analysis across all pairs. This standardization helps maintain reliable technical analysis and signal generation.

Q: How many coins can I add to my custom list?

A: Users can add up to 10 custom symbols to their watchlist. This limit is designed to maintain optimal performance while allowing focused monitoring of specific assets. The custom list complements the predefined categories that cover over 300 pairs.

Q: What determines signal confidence levels?

A: Signal confidence is calculated through a weighted algorithm that considers multiple factors: trend strength (Hull MA, DMI/ADX), momentum indicators (RSI, SRSI), volatility measurements (RVI, ATR, BB), volume analysis (OBV, volume trends), and price action patterns. Higher confidence levels indicate stronger alignment across these factors.

Q: Are signals guaranteed to work?

A: No. Signals are analytical tools based on historical and current market data, not guaranteed predictions. They should be used as one component of a comprehensive trading strategy that includes proper risk management, position sizing, and additional confirmation factors. Past performance does not guarantee future results.

Q: Why does the screener need higher timeframes?

A: Higher timeframes (1D minimum) provide several benefits: reduced market noise, more reliable technical signals, better trend identification, and lower likelihood of false signals. They also align better with institutional trading patterns and allow for a more thorough analysis of market conditions across multiple indicators.

--------------------------------------

Conclusion

The Altcoins Screener is a comprehensive crypto market analysis tool that:

Scans 300+ cryptocurrencies across 9 sectors on a single chart

Combines technical indicators and social metrics for signal generation

Identifies potential trading opportunities through color-coded visuals

Saves time by eliminating the need to monitor multiple charts

The tool is suited for:

Market overview and sector rotation analysis

Quick assessment of market conditions

Technical and social sentiment tracking

Systematic trading approach with alerts

Use this screener with caution and as a complement to any other tool you use to define your trading strategy.

--------------------------------------

Disclaimer

This indicator is for informational and educational purposes only:

Not financial advice: This indicator should not be considered investment advice.

No guarantee of accuracy: The indicator's calculations and signals are based on specific algorithms and data sources, but accuracy cannot be guaranteed. Market conditions can change rapidly.

Past performance is not predictive: Past performance of the indicator's signals or any specific asset is not indicative of future results.

Substantial risk of loss: Trading cryptocurrencies involves a substantial risk of loss. You can lose money trading these assets.

User responsibility: Users are solely responsible for their own trading decisions and should exercise caution.

Independent research required: Always conduct thorough independent research (DYOR) before making any trading decisions.

Technical analysis is one of many tools: Technical analysis, including the output of this indicator, is just one tool among many and should not be relied upon exclusively.

Risk management is essential: Use proper risk management techniques, including position sizing and stop-loss orders.

Comprehensive strategy: Use this tool as part of a comprehensive trading strategy, not as a standalone solution.

No liability for trading results: The Author assumes no responsibility or liability for any trading results or losses incurred as a result of using this indicator.

No TradingView affiliation: SwissAlgo is an independent entity and is not affiliated with or endorsed by TradingView.

LunarCrush data: The indicator utilizes publicly available data from LunarCrush. LunarCrush data and trademarks are the property of LunarCrush.

Consult a financial advisor: Consult with a qualified financial advisor before making any investment decisions.

By using this indicator, you acknowledge and agree to these terms. If you do not agree with these terms, please refrain from using this indicator.

Position Tracker 1.0Position Tracker 1.0 allows users to input their position using USD, quantity, or a DCA approach while setting take profit (TP) and stop loss (SL) levels based on either fixed dollar values or percentages. The indicator provides optional markers for TP/SL crossings and an entry label showing key trade details. A live tracker can be enabled for real-time P&L updates, and all visual elements are customizable for clarity and preference.

Instructions for Position Tracker 1.0

1. Input Method & Position Details:

* Choose between USD, Quantity, or DCA.

* Enter your entry price, entry time, investment amount, or quantity as needed.

2. TP & SL Setup:

* For each TP (up to 5) and the SL, select whether to use a fixed dollar target or a percentage

target relative to your entry price.

* Enter the corresponding price (if using Dollar) or percentage (if using Percentage).

* For TPs, specify the percentage of your position to sell when the level is hit.

3. Marker & Display Options:

* Toggle the TP and SL crossing markers on or off.

* Adjust which details (Price, Diff, Sell for TP; Price, Diff, Loss for SL) are shown on the labels.

* The entry label always shows the Avg. Cost and can optionally include the quantity, invested

amount, and live tracker (real-time P&L).

4. Visual Customization:

* Change text size, marker size, and colors for profit, loss, TP, and SL lines as desired.

Binance Pseudo Funding FeeThe indicator calculates the Funding Fee for Binance based on the Premium Index provided by TradingView. The calculation formula can be found here: Binance Funding Rate Introduction . This is NOT the official rate visible on binance.com and used for settlements, but rather an estimated rate, which is inherently INACCURATE . The accuracy of the calculation heavily depends on the timeframe, with almost perfect results on minute-based timeframes.

For the most accurate calculations, you need to visit Binance Funding History and fill in the corresponding Interval , Interest Rate , and Funding Cap/Floor settings for the specific symbol in the indicator's settings. I understand this is not convenient, but for now, this is how it works.

The blue bars indicate the settlement time. Funding can be smoothed using moving averages. Both the funding rate and the moving averages are displayed using plot and are labeled, so you can set alerts on them.

Gold Pro StrategyHere’s the strategy description in a chat format:

---

**Gold (XAU/USD) Trend-Following Strategy**

This **trend-following strategy** is designed for trading gold (XAU/USD) by combining moving averages, MACD momentum indicators, and RSI filters to capture sustained trends while managing volatility risks. The strategy uses volatility-adjusted stops to protect gains and prevent overexposure during erratic price movements. The aim is to take advantage of trending markets by confirming momentum and ensuring entries are not made at extreme levels.

---

**Key Components**

1. **Trend Identification**

- **50 vs 200 EMA Crossover**

- **Bullish Trend:** 50 EMA crosses above 200 EMA, and the price closes above the 200 EMA

- **Bearish Trend:** 50 EMA crosses below 200 EMA, and the price closes below the 200 EMA

2. **Momentum Confirmation**

- **MACD (12,26,9)**

- **Buy Signal:** MACD line crosses above the signal line

- **Sell Signal:** MACD line crosses below the signal line

- **RSI (14 Period)**

- **Bullish Zone:** RSI between 50-70 to avoid overbought conditions

- **Bearish Zone:** RSI between 30-50 to avoid oversold conditions

3. **Entry Criteria**

- **Long Entry:** Bullish trend, MACD bullish crossover, and RSI between 50-70

- **Short Entry:** Bearish trend, MACD bearish crossover, and RSI between 30-50

4. **Exit & Risk Management**

- **ATR Trailing Stops (14 Period):**

- Initial Stop: 3x ATR from entry price

- Trailing Stop: Adjusts to lock in profits as price moves favorably

- **Position Sizing:** 100% of equity per trade (high-risk strategy)

---

**Key Logic Flow**

1. **Trend Filter:** Use the 50/200 EMA relationship to define the market's direction

2. **Momentum Confirmation:** Confirm trend momentum with MACD crossovers

3. **RSI Validation:** Ensure RSI is within non-extreme ranges before entering trades

4. **Volatility-Based Risk Management:** Use ATR stops to manage market volatility

---

**Visual Cues**

- **Blue Line:** 50 EMA

- **Red Line:** 200 EMA

- **Green Triangles:** Long entry signals

- **Red Triangles:** Short entry signals

---

**Strengths**

- **Clear Trend Focus:** Avoids counter-trend trades

- **RSI Filter:** Prevents entering overbought or oversold conditions

- **ATR Stops:** Adapts to gold’s inherent volatility

- **Simple Rules:** Easy to follow with minimal inputs

---

**Weaknesses & Risks**

- **Infrequent Signals:** 50/200 EMA crossovers are rare

- **Potential Missed Opportunities:** Strict RSI criteria may miss some valid trends

- **Aggressive Position Sizing:** 100% equity allocation can lead to large drawdowns

- **No Profit Targets:** Relies on trailing stops rather than defined exit targets

---

**Performance Profile**

| Metric | Expected Range |

|----------------------|---------------------|

| Annual Trades | 4-8 |

| Win Rate | 55-65% |

| Max Drawdown | 25-35% |

| Profit Factor | 1.8-2.5 |

---

**Optimization Recommendations**

1. **Increase Trade Frequency**

Adjust the EMAs to shorter periods:

- `emaFastLen = input.int(30, "Fast EMA")`

- `emaSlowLen = input.int(150, "Slow EMA")`

2. **Relax RSI Filters**

Adjust the RSI range to:

- `rsiBullish = rsi > 45 and rsi < 75`

- `rsiBearish = rsi < 55 and rsi > 25`

3. **Add Profit Targets**

Introduce a profit target at 1.5% above entry:

```pine

strategy.exit("Long Exit", "Long",

stop=longStopPrice,

profit=close*1.015, // 1.5% target

trail_offset=trailOffset)

```

4. **Reduce Position Sizing**

Risk a smaller percentage per trade:

- `default_qty_value=25`

---

**Best Use Case**

This strategy excels in **strong trending markets** such as gold rallies during economic or geopolitical crises. However, during sideways or choppy market conditions, the strategy might require manual intervention to avoid false signals. Additionally, integrating fundamental analysis—like monitoring USD weakness or geopolitical risks—can enhance its effectiveness.

---

This strategy offers a balanced approach for trading gold, combining trend-following principles with risk management tailored to the volatility of the market.

Jay Stock Vs S&P Sector Performance

This indicator facilitates stock comparison with an S&P sector while also identifying sector trends and potential trend beginnings, continuations, and conclusions by integrating moving averages with trend lines.

Its unique trend curves also assist in pinpointing key support and resistance levels for the sector. The sector grouping and market cap are calculated within the indicator using a curated list of stocks.

Multi-timeframe plots provide valuable insights by displaying short-term and long-term trends on the same chart, making it suitable for both intraday and swing trading analysis.

Multiple sector charts and trends can be visualized at the same time by adding multiple instances of same indicator to compare different sectors for portfolio rebalancing between sectors.

Another distinctive and essential feature is performance lines, which allow for visualizing S&P sector performance relative to the SPX market and stock performance relative to the S&P sector. Using the performance lines, one can identify top-performing sectors and then pinpoint the best stocks within those sectors.

How to read multi-timeframe charts?

The first timeframe, such as daily, is represented by a red EMA8 line (labeled DE) and a corresponding thin trend line (labeled DT). The second timeframe, such as weekly, uses a green EMA8 line (labeled WE) and a medium trend line (labeled WT). The third timeframe, such as monthly, is depicted with a blue EMA8 line (labeled ME) and a thick trend line (labeled MT).

As the timeframe increases, the true range increases and hence trend curve thickness increases.

How do EMA and Trend Line Work Together?

In the Electronic Tech sector daily chart screenshot below, trend initiation is highlighted with a green circle, trend continuation is marked by arrow, and trend completion is indicated with a red circle. A total of two trends are identified on the chart.

When the EMA crosses above the corresponding trend line, it signals the start of a trend, while a cross below the trend line marks its end. The period between the trend start and end represents trend continuation.

How do Trend Lines Serve as Support or Resistance?

In the Electronics Sector daily chart screenshot below, the monthly green trend line serves as support when the price declines toward it, while the red trend line acts as resistance when the price rises from below.

Green circles on the chart highlight instances where the monthly trend provided support, while red circles indicate points where the weekly trend acted as resistance.

How Multi-Timeframe Trends Assist in Stock Analysis?

In the Transportation sector daily chart screenshot below, the monthly trend is rising, and the weekly trend is also moving upward, indicating a favorable outlook for both long-term (monthly) and medium-term (weekly) trends. While, the daily chart suggests a up trend starting.

How to use performance lines to pick outperforming sectors and stocks?

In the screenshot below, the sector candles and trendlines have been disabled in the settings for better clarity, while the performance lines remain enabled. The chart displays META's performance lines, comparing its performance against the Technology Services sector.

The upward movement of the red lines indicates that META is performing well relative to its sector, while the rising blue lines suggest that the sector itself is gaining strength. This trend signals a potential improvement in both the sector’s overall performance and META’s standing within it.

Inputs and customization:

The combination of ema and trend plots will be plotted for 4 different time frames all at once. The first three timeframes(60, 240, D, W, M, etc) can be chosen in the settings while the fourth one is for current chart timeframe.

One can manually select the sector for comparison in the settings or choose to have it automatically selected for most of S&P 500 stocks. At what price to plot the sector chart can be set in the settings.

The sector candles, trend lines, performance lines and labels, can all be shown or hidden by adjusting settings.

How is Trend Line and EMA calculated?

The Trend line is calculated using an arithmetic equation based on the last 8 data points, which are themselves a combination of weighted moving averages of varying lengths. A 14-period true range of the price is calculated and plotted as a buffer zone around the trend lines.

Trend curves appear green when the price is above the trend line and red when it is below. Trend lines are labeled using the timeframe followed by 'T' (e.g., DT, WT, MT).

The EMA represents the weighted moving average of the most recent eight candles and is labeled with the timeframe followed by 'E' (e.g., DE, WE, ME).

How is sector data(representational) Calculated ?

The representational sector data (market cap) is calculated by summing each stock's price, weighted by its market cap percentage within the selected group, and then scaling the result to display at the desired price point on the chart.

The sector plot data shown here is the representation(not actual) of total market value of a few chosen stocks (list shown on chart) in the S&P 500. Large-cap stocks are excluded from the calculation to mitigate bias. Therefore, the displayed chart offers an approximate representation of the sector movement.

How is performance Calculated ?

The stock vs. sector performance, shown in red, is calculated as the stock's market cap movement divided by the sector's market cap movement. If the stock is doing much better than the rest of its sector group, this line will go up. Similarly, sector Vs SPX performance, shown in blue, is calculated as sector movement divide by SPX movement. When a sector outperforms the broader(SPX) market, the blue line trends upward.

Pro Tip: For optimal visibility, apply this indicator to a separate pane below the stock chart.

Caution: This indicator is intended solely for educational and analytical purposes, assisting traders in studying stock movements relative to their sector group. Stocks selected for sector market cap calculations are curated and hence these plots should only be taken for comparison study purposes. Exercise caution when using it for investment decisions.

Sharpe and Sortino Ratios with Date RangeThis indicator calculates the Sharpe and Sortino ratios using a chart symbol's periodic price returns.

I added the ability to calculate SORTINO and Sharpe based on CUSTOM DATES within the option menu.

It builds on the script here: by adding this feature.

A little about the Sortino Ratio.

www.nasdaq.com

I want equity market returns, but I don’t want equity market volatility. This is the sentiment many investors naturally feel. This sentiment often grows stronger as one approaches or is in the phase where they desire distributions from their savings to improve lifestyle. This is why there is a need for active management in the investment arena. The desire to control downside volatility, but also participate in the upside growth is a very fundamental human desire. The Sortino Ratio measures how well a particular investment meets this fundamental human desire.

There is the old adage, “volatility is the price you pay for returns.” However, what if we could measure the historical performance of an investment and see if it has given above average returns compared to the downside volatility. This is a simple division problem. It will tell us if the volatility “price we are paying for returns” is good. We can then compare that to other investments to see how they compare.

Let us take the return and subtract the risk-free interest rate and then simply divide that by the downside movement from the average. A basic division problem yielding a number that measures a very basic human desire: How well did this investment do compared to the downside risk it experienced.

In the world of financial analysis and investment management, ratios are abundant. There are many ratios that are truly important to a particular analysis. However, the sheer abundance of ratios that are available often overwhelms the casual investor, leading them to disregard ratios altogether. I would argue for those investors that desire a way to rank an investment by its ability to satisfy this very fundamental human desire, the Sortino Ratio is the number they need to consider.

Disappointing in the marketplace for research, the Sortino Ratio is not featured prominently. It is much easier to find the inflows a particular ETF has experienced than the Sortino Ratio. Inflows are important. They measure how much people are investing into an ETF. However, they are mostly only important to the fund manager, not the investor. What investors care about is the Risk-Adjusted Return. This is the Sortino Ratio.

Rolling CAGRRolling CAGR (Compound Annual Growth Rate) Indicator

This indicator calculates and plots the rolling Compound Annual Growth Rate (CAGR) for any selected data source. CAGR represents the mean annual growth rate of an investment over a specified time period, taking into account the effect of compounding.

Features:

• Customizable data source (default: close price)

• Adjustable time period in years

• Configurable trading days per year (252 for stocks, 365 for crypto)

• Results displayed as percentage values

• Works on daily timeframes

Input Parameters:

• Data Source: Select the price or indicator data to analyze

• Number of Years: Set the lookback period for CAGR calculation

• Trading Days in a Year: Adjust based on market type (252 for stocks, 365 for crypto)

Usage:

Perfect for analyzing long-term growth rates and comparing investment performance across different periods. The indicator provides a rolling view of compound growth, helping traders and investors understand the sustained growth rate of an asset over their chosen timeframe.

Note: This indicator is designed for daily timeframes as CAGR calculations are most meaningful over longer periods.

Formula Used:

CAGR = (End Value / Start Value)^(1/number of years) - 1

Contracts CalculatorThe Contracts Calculator is a simple yet powerful tool for traders who want to efficiently calculate their position size and the number of contracts to trade based on their account balance, chosen leverage, and the percentage they wish to invest. This indicator helps traders manage their risk and make informed trading decisions.

Key Features:

Account Balance (USD): Input your account balance in USD.

Percentage of Account Balance (%): Choose the percentage of your balance you want to invest.

Leverage (min. 1): Set your desired leverage (minimum value is 1).

Current Price (Live): The indicator fetches the current market price in real-time.

Calculations:

Investment Amount (without leverage): The amount you want to invest is calculated as a percentage of your total account balance.

Investment Amount (with leverage): The script then applies the leverage to increase your investment amount.

Position Size and Contracts: Based on the leveraged amount and the current market price, it calculates the number of contracts you can trade.

Output:

A user-friendly table displays the following:

Account Balance (USD)

Percentage of Balance to Invest

Leverage Applied

Position Size (USD)

Number of Contracts to Trade

This indicator is ideal for traders who want to quickly calculate their position size and manage their risk in an easy-to-read format. Simply input your details and let the Contracts Calculator do the rest!

It is designed for efficient risk management and provides clear, actionable insights for day trading and other short-term trading strategies.

Version: Alpha 0.02

Crypto Market Confidence Period | viResearchCrypto Market Confidence Period | viResearch

Conceptual Foundation and Innovation

The "Crypto Market Confidence Period" indicator from viResearch offers traders a precise way to evaluate market conditions and identify safe investment periods in the crypto market. This tool combines market performance metrics across different assets and uses a dynamic approach to pinpoint periods of market confidence. By assessing historical performance and relative asset strength, the indicator classifies periods as either "safe" or "unsafe" for investment, helping traders make data-driven decisions. It is particularly useful for those looking to understand the cyclical nature of market trends and determine the optimal time for entering or exiting the market.

Technical Composition and Calculation

The "Crypto Market Confidence Period" indicator utilizes key market performance data, including price changes and historical trends, to evaluate the overall market climate. The core calculation involves comparing the system equity over a specified period (based on peak and nadir values) to determine periods of market confidence. The indicator calculates the highest and lowest points in system equity over a user-defined period, marking these as safe and unsafe periods. If the system equity reaches its highest value (peak), it indicates a "Safe Period" for investment, while a drop to its lowest value (nadir) signals an "Unsafe Period." These periods help traders assess when the market is more likely to experience mean reversion or continued trends.

Practical Applications

The "Crypto Market Confidence Period" indicator is designed to provide traders with a clear understanding of market conditions, specifically identifying safe and unsafe investment periods. By tracking system equity and evaluating market highs and lows, this tool can help traders make informed decisions about when to enter or exit trades. The key applications include:

Determining Mean Reversion Periods: The indicator highlights when the market is moving away from its average, signaling a potential mean reversion period. Traders can use this information to anticipate a reversal in market direction.

Identifying Trending Periods: When the market remains consistently in a "Safe Period," it may indicate that a trend is in motion, and the likelihood of continued price movement is higher. Traders can focus on trend-following strategies during these periods.

Advantages and Strategic Value

The "Crypto Market Confidence Period" indicator offers significant value by helping traders identify periods where market behavior is more predictable. This tool enhances trading strategies by distinguishing between periods of market stability (safe) and volatility (unsafe). Traders can use these insights to reduce risk during unsafe periods and capitalize on trends during safe periods.

Alerts and Visual Cues

The indicator includes alert conditions for both safe and unsafe periods. Alerts are triggered when the market enters a "Safe Period" or an "Unsafe Period," allowing traders to take action based on the market's current state. Additionally, the indicator provides visual cues, such as background color changes, to help traders quickly identify the market's condition and make timely decisions.

Summary and Usage Tips

The "Crypto Market Confidence Period" indicator is an invaluable tool for traders looking to manage risk and optimize their investment timing in the crypto market. By providing insights into market confidence, this indicator helps identify when the market is likely to revert to its mean or when a trend is likely to continue. Traders can use this tool to guide their decision-making, making it a versatile addition to any trading strategy.

Position Size Calculator (MOEX Futures)Описание на русском языке

Этот скрипт для TradingView создан специально для трейдеров, работающих с фьючерсами на Московской бирже. Его основная цель – помочь трейдерам быстро и точно рассчитывать параметры позиции, такие как количество контрактов, риск на сделку, общий размер маржи, а также цены стоп-лосса и тейк-профита.

Функционал:

Расчет цены контракта: учитывает цену актива (в пунктах) и стоимость одного пункта.

Риск на сделку: определяется как процент от общего капитала.

Размер позиции: рассчитывается на основе риска на сделку и стоп-лосса.

Количество контрактов: округляется до целого числа вниз.

Общий размер маржи: определяется исходя из количества контрактов и маржи на один контракт.

Цены стоп-лосса и тейк-профита: вычисляются как для лонг-, так и для шорт-позиций.

Интерактивная таблица: статично отображается в правом верхнем углу графика и обновляется автоматически при изменении входных данных.

Скрипт заточен исключительно под специфику фьючерсов Московской биржи и позволяет трейдерам оптимизировать расчёты, минимизировать ошибки и экономить время.

Description in English

This TradingView script is specifically designed for traders working with futures on the Moscow Exchange. Its primary purpose is to help traders quickly and accurately calculate position parameters, such as the number of contracts, risk per trade, total margin size, and stop-loss and take-profit prices.

Features:

Contract price calculation: Takes into account the asset price (in points) and the price per point.

Risk per trade: Defined as a percentage of the total capital.

Position size: Calculated based on the risk per trade and stop-loss percentage.

Number of contracts: Rounded down to the nearest whole number.

Total margin size: Determined based on the number of contracts and margin per contract.

Stop-loss and take-profit prices: Calculated for both long and short positions.

Interactive table: Statically displayed in the top-right corner of the chart and dynamically updated when input parameters change.

This script is tailored exclusively to the specifics of futures trading on the Moscow Exchange, enabling traders to optimize calculations, minimize errors, and save time.

[Helper] Trade Journal TableThis indicator serves as a starting point for creating a customized trade journal that meets individual requirements. It provides a basic structure for visualizing trade data in table form which can be adapt to specific needs. The trade data must be maintained directly within the script using the Pine Editor.

Basic Structure:

The example table consists of six columns: Date, Entry Price, Exit Price, Profit/Loss (color-coded), Strategy, and Notes. It is displayed centrally on the chart and dynamically adjusts to the number of recorded trades.

Example Data:

To demonstrate its functionality, the indicator includes predefined example trades, which should be replaced with actual trading data. Additional information, such as strategies and notes, can be added to improve trade documentation.

Precision Trade Zone By KittisakThis indicator is designed for Money Management calculations, helping to facilitate risk management in trading, determining suitable leverage based on acceptable risk, and adjusting the Stop Loss level to align with the calculated leverage.