Thunderbird BoSThe Thunderbird BoS script is meticulously crafted for those who thrive on higher timeframes (daily, weekly, monthly) and aim to capture the significant moves and trends in the market.

What does the Thunderbird BoS script do?

Breakouts are pivotal moments in investing, and the Thunderbird BoS script is your ally in identifying them. Here's how:

Breakout Detection: The script springs into action when there's a breakout of a specific Donchian setting, producing a signal.

Visual Aids: It doesn't just stop at signals. The script visually displays entry, stop, and compound levels right on your chart. This feature is especially handy when you hover over a bar, as it allows you to see levels from past signals, no matter how far back in time.

Trend Confirmation: The script is adept at producing entry signals in both confirmed bull and bear trends.

Filtering the Noise: Using the Donchian logic, the script confirms end-of-day entry points in a long-term trend and efficiently filters out fake breakouts and entry points in a sideways market.

How does BoS work?

The BoS is a product of meticulous calculations:

Breakout Signal: Upon detecting a breakout signal, the entry-level is determined. For a bullish breakout, it's calculated a specific % above the high, and for a bearish breakout, a specific % below.

Stop Calculation: Using the Average True Range (ATR) over a number of specific days, the stop loss is set below the entry for long positions and above for short positions.

Compound Levels: The compound level is also determined using an ATR formula above the entry for long positions and below for short ones.

What's the ideal timeframe for this script?

The Thunderbird BoS script is tailor-made for the daily timeframe. This ensures that breakout signals are derived from a comprehensive view of the market's movements.

What sets the Thunderbird BoS script apart?

The uniqueness of the Thunderbird BoS script lies in its:

Historical Insight: The ability to view levels from past signals by simply hovering over a bar. This feature aids in analysing entry levels from any point in the past and is displayed seamlessly in the data window.

Precision for Daily Timeframe: The script is specifically coded for the daily timeframe to:

Pinpoint the onset of potential long-term trends.

Confirm entry points at the end of the trading day, effectively filtering out intraday distractions.

Minimise the chances of fake breakouts in a trend.

Continuously generate entry points as the trend evolves, facilitating compounding.

Efficiently filter out breakouts in a sideways market.

In essence, the Thunderbird BoS script is an investor's tool for focusing on the quality of potential positions when investing in long-term market trends. It's not just about identifying trends; it's about making informed decisions based on them.

Portfolio management

Thunderbird PoCWhat kind of traders/investors are we?

We are trend followers. Our scripts are designed to be used on the higher timeframes (daily/weekly/monthly) to catch significant moves/trends in the market. While many are aware of the power of trend following, not all have the tools to execute it effectively. Our scripts are tailored to pinpoint and capitalise on long-term market trends.

What does this script do?

The Thunderbird PoC is a tool for investors looking to capitalise on breakout opportunities. When a breakout of the Donchian occurs, the script produces a signal. This signal is then used to display the entry, stop, and compound levels in the data window. One of its standout features is its ability to show levels for the bar where the mouse is hovering. This allows investors to analyse entry levels from past signals retrospectively. All this information is also conveniently displayed in the data window.

How is the PoC produced?

The PoC is meticulously calculated using a formula the encapsulates ATR. Upon a breakout signal, an entry-level is determined. For a bullish breakout, the entry is set a fixed % leve above the high, and for a bearish breakout, at a fixed % level below. The stop loss level is then calculated by using the ATR formula below the entry for long positions and above for short positions. The compound level is also set using an ATR formula above the entry for long positions and below for short ones.

What is the best timeframe to use the script?

The Thunderbird PoC is optimised for the daily timeframe. This is where the breakout signals are most effective and reliable. By focusing on the daily timeframe, investors can capture significant market movements and avoid the noise of shorter timeframes.

What makes this script unique?

The Thunderbird PoC stands out in its ability to provide investors with a retrospective view of the market. By allowing users to see the levels for the bar where the mouse is, it offers a unique perspective on past signals, enabling investors to learn and adapt from historical data. This feature, combined with its detailed display in the data window, makes it an invaluable tool for those looking to use trend-following techniques.

This tool removes the need of manually having to calculate the entry, stop loss, compound and risk-free levels yourself.

This script has been coded specifically for the daily timeframe to:

Highlight the start of potential long-term trends.

Confirm entry points at the end of the trading day, absorbing intraday noise.

Reduce fake breakouts in a trend.

Continue to create entry points as the trend develops to allow for compounding.

Filter out breakouts in a sideways market.

This entry signal script helps investors focus on the quality of a potential position when investing in long-term market trends.

Portfolio HeatThe "Portfolio Heat" indicator offers a visual representation of potential risk exposure for a portfolio across up to eight different symbols. It dynamically calculates three risk metrics based on current price, the number of shares owned, your designated stop loss, and total account size.

Open Dollar Risk – the total dollar amount you will lose if your stop loss is hit.

Open % of Portfolio Risk – the risk as a percentage of your total account size.

Starting Capital Risk – the dollar amount risked based on the difference between the entry price and stop price.

These metrics adjust in real-time, allowing you to monitor and manage risk more effectively.

Open portfolio heat refers to how much you would lose if all your currently held stock positions hit their stop-losses, whether those stop-losses are below what you paid for them - referred to as your “cost basis” - at your cost basis (breakeven) or above your cost basis (in the money). Admittedly, it’s a pretty bad day when all your stops are hit at once, but as traders we need to prepare for the worst. To visualize what “open heat” looks like on a single stock position, please note the chart below:

In the example above you can see that if you were to purchase 100 shares of this stock at a cost-basis of $18/share, and your stop-loss is placed at $15, if the current price of the stock is at $20 and the stock price drops to hit your stop-loss, it would result in a $500 total drawdown in your portfolio. Keep in mind this is just one stock position. Hypothetically, if you were even holding two stocks that had the above open heat, with a $10,000 account size, you could experience a 10% drawdown quite fast if the market corrects.

The “Portfolio Heat” indicator is fully customizable allowing traders to select the number of positions in the portfolio, colors and a detailed or a summary view of risk.

Note if entering a short position, you will enter the number of shares owned as a negative number.

Curved Management (Zeiierman)█ Overview

The Curved Management (Zeiierman) is a trade management indicator tailored for traders looking to visualize their entry, stop loss, and take profit levels. Unique in its design, this indicator doesn't just display lines; it offers rounded or curved visualizations, setting it apart from conventional tools.

█ How It Works

At its core, this indicator leverages the power of the Average True Range (ATR), a metric for volatility, to establish logical stop-loss levels based on recent price action. By incorporating the ATR, the tool dynamically adapts to the market's changing volatility. What sets it apart is the unique curved visualization. Instead of the usual straight lines representing entry/sl levels, users can choose between rounded and straight edges for their take profit and stop loss levels. This aesthetic tweak gives the chart a cleaner look and offers a more intuitive understanding of risk management.

█ How to Apply the Indicator

Upon initially loading the indicator, a label appears that reads, "Set the 'xy' time and price for 'Curved Management (Zeiierman).'" This prompts you to click on the chart at your entry point. After selecting your entry point on the chart, the indicator will load. Ensure you adjust the trend direction in the settings panel based on whether you took a long or short position.

█ How to Use

Use the tool to manage your active position.

Long Entry

Short Entry

█ Settings

The indicator comes packed with various settings allowing customization:

Trade Direction

Decide the direction of the trade (long/short).

Reward multiplier

Sets the ratio for take profit relative to stop loss. Increasing this value will set your take profit further from the entry, and decreasing it will bring it closer.

Risk multiplier

Multiplier for calculating stop loss based on the ATR value. Increasing this makes your stop loss further from the entry, while decreasing brings it closer.

█ Related Free Scripts

Trade & Risk Management Tool

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Risk Reward Optimiser [ChartPrime]█ CONCEPTS

In modern day strategy optimization there are few options when it comes to optimizing a risk reward ratio. Users frequently need to experiment and go through countless permutations in order to tweak, adjust and find optimal in their data.

Therefore we have created the Risk Reward Optimizer.

The Risk Reward Optimizer is a technical tool designed to provide traders with comprehensive insights into their trading strategies.

It offers a range of features and functionalities aimed at enhancing traders' decision-making process.

With a focus on comprehensive data, it is there to help traders quickly and efficiently locate Risk Reward optimums for inbuilt of custom strategies.

█ Internal and external Signals:

The script can optimize risk to reward ratio for any type of signals

You can utilize the following :

🔸Internal signals ➞ We have included a number of common indicators into the optimizer such as:

▫️ Aroon

▫️ AO (Awesome Oscillator)

▫️ RSI (Relative Strength Index)

▫️ MACD (Moving Average Convergence Divergence)

▫️ SuperTrend

▫️ Stochastic RSI

▫️ Stochastic

▫️ Moving averages

All these indicators have 3 conditions to generate signals :

Crossover

High Than

Less Than

🔸External signal

▫️ by incorporating your own indicators into the analysis. This flexibility enables you to tailor your strategy to your preferences.

◽️ How to link your signal with the optimizer:

In order to be able to analysis your signal we need to read it and to do so we would need to PLOT your signal with a defined value

plot( YOUR LONG Condition ? 100 : 0 , display = display.data_window)

█ Customizable Risk to Reward Ratios:

This tool allows you to test seven different customizable risk to reward ratios , helping you determine the most suitable risk-reward balance for your trading strategy. This data-driven approach takes the guesswork out of setting stop-loss and take-profit levels.

█ Comprehensive Data Analysis:

The tool provides a table displaying key metrics, including:

Total trades

Wins

Losses

Profit factor

Win rate

Profit and loss (PNL)

This data is essential for refining your trading strategy.

🔸 It includes a tooltip for each risk to reward ratio which gives data for the:

Most Profitable Trade USD value

Most Profitable Trade % value

Most Profitable Trade Bar Index

Most Profitable Trade Time (When it occurred)

Position and size is adjustable

█ Visual insights with histograms:

Visualize your trading performance with histograms displaying each risk to reward ratio trade space, showing total trades, wins, losses, and the ratio of profitable trades.

This visual representation helps you understand the strengths and weaknesses of your strategy.

It offers tooltips for each RR ratio with the average win and loss percentages for further analysis.

█ Dynamic Highlighting:

A drop-down menu allows you to highlight the maximum values of critical metrics such as:

Profit factor

Win rate

PNL

for quick identification of successful setups.

█ Stop Loss Flexibility:

You can adjust stop-loss levels using three different calculation methods:

ATR

Pivot

VWAP

This allows you to align risk-reward ratios with your preferred risk tolerance.

█ Chart Integration:

Visualize your trades directly on your price chart, with each trade displayed in a distinct color for easy tracking.

When your take-profit (TP) level is reached , the tool labels the corresponding risk-reward ratio for that specific TP, simplifying trade management.

█ Detailed Tooltips:

Tooltips provide deeper insights into your trading performance. They include information about the most profitable trade, such as the time it occurred, the bar index, and the percentage gain. Histogram tooltips also offer average win and loss percentages for further analysis.

█ Settings:

█ Code:

In summary, the Risk Reward Optimizer is a data-driven tool that offers traders the ability to optimize their risk-reward ratios, refine their strategies, and gain a deeper understanding of their trading performance. Whether you're a day trader, swing trader, or investor, this tool can help you make informed decisions and improve your trading outcomes.

S&P Sector PerformanceS&P Sector Performance calculate and display the logarithmic returns of SPX and each S&P Sector for a predefined timeframe or for a custom date.

IU SIP CALCULATORHow This Indicator Script Works:

1. This indicator script calculate the monthly SIP returns of any market over any user defined period.

2. SIP stands for Systematic Investment Plan. It is a way to invest in any asset by regularly investing a fixed amount of money at regular intervals for example Monthly, Weekly, Quarterly etc.

3. This indicator Calculate the following

# Average buy price

# Total quantity hold

# Yearly returns

# Monthly returns

# Total invested amount

# Total profits in amount

# Total portfolio value

# Total returns in per percentage term.

4. This script takes monthly SIP amount, starting month, starting year, ending year, ending month from the user and store the value for calculations.

5. After that it store the open price of every month into an array then it average the array and compare that price with the last month close price.

6. on the bases of this it performs all of the calculations.

7. The script plot every calculation into an table from.

8. It requires monthly chart timeframe for working.

9. The table is editable user can change the color and transparency.

How User Can Benefit From The Script:

1. User can get the past monthly SIP returns of any market he wants to invest this will give him an overview about what to expect from the market.

2. Once user understand the expected returns from the market he can adjust his investment strategy.

3. This help the user to Analyse various stocks and their past performance.

4. User can also short list the best performed stocks.

5. Over all this script will give complete SIP vision of any market.

Bonsai BX (Backtester)In today's trading landscape, traders need precision and deep analytical tools to navigate the sea of strategies. The Bonsai Backtester is one such tool, meticulously designed to evaluate multiple trading strategies in an integrated manner.

═════════════════════════════════════════════════════════════════════════

🌳 Bonsai BX 🌳 Universal Strategy Testing

📘 Overview

A product of collaboration with the Bonsai community, this backtester is both a reflection of collective insights and a means to provide traders with data-driven insights on TradingView.

📌 Current Backtest

• Dataset: BTCUSD daily candles from Coinbase, starting from March 2015.

• Source Signals: The Bonsai indicator signals are employed for both long and short entries. These are directly visible on the publication chart.

• Trading Assumptions:

• Initial Capital: $1,000

• Maximum Position Size: 10% of equity per trade

• Stop Loss: 10% per position

• Commission: 0.1%

• Slippage: 100 ticks (1.00)

🛠 Key Features

The Bonsai BX is equipped with a range of features aimed at providing traders with a more comprehensive analysis environment:

Features on Chart

• External Indicator Adaptability: Easily incorporate signals from both built-in and custom TradingView indicators.

• Snapshot Table: Delivers on-the-spot insights into crucial strategy performance metrics, including equity, open profit, position size, and entry price. While these details are available in TradingView's 'Performance Summary' panel, we've integrated them directly onto the chart for a more streamlined and accessible viewing experience.

• Trade Labels: Visualize profit metrics for individual trades directly on the chart, allowing for a more immediate grasp of trade outcomes.

• Long & Short Behaviors: Modify long behaviors to either open new long positions while closing short ones, or simply to close short positions. Conversely, for short behaviors, opt to either initiate new short positions while closing any active long ones or simply close long positions.

• Multiple Signals Integration: The tool can currently handle up to three different external signals for long and short trades.

• Condition-based Initiation: Define whether longs and shorts are triggered when 'All Conditions Met' or just 'Any Single Condition Met'. This flexibility allows for a more nuanced trading approach. For example, if you're using a trade signal alongside the RSI, you can specify that a long position should only open when the trade signal is active and the RSI is below 30 at the same time. This lets you combine multiple signals or conditions for more precise trade initiation.

• TP & SL Customization:

• Single TP: Set a specific Take Profit percentage.

• SL: Define a Stop Loss percentage and choose between a standard or trailing stop.

• Trail From: Specify the starting point of the trailing stop, be it the breakeven point or a certain percentage.

• Interface Theme: Users can select between light and dark themes for their interface.

Performance and Trailing

🎛 Using Bonsai BX

1. Add it to your TradingView chart.

2. Adjust script parameters and settings. Integrate external indicator signals as needed.

3. Activate the backtester to refine trading strategies.

Backtester Settings Menu

🪝 Webhook (Beta)

The Webhook functionality, now in beta, augments the Bonsai BX utility. This feature offers a more intuitive method for users to direct webhooks to trading bots, exchanges, and brokers. It simplifies the process by eliminating the need to adjust JSON structures or other payload formats, making alert automation more accessible.

📜 Feedback & Community

The feedback from the Bonsai community has been instrumental in the tool's development and will continue to shape its evolution. As part of our commitment to adaptive, smart trading, this script will continually be updated to meet the ever-changing requirements of traders.

❗️ Disclaimer

Backtesting tools, including the Bonsai BX , simulate trading strategies based on historical data. The following key points should be kept in mind:

1. Past Performance is Not Predictive: While backtesting can offer insights, it's essential to understand that past performance does not guarantee or predict future results. Historical data might not account for future market changes or unforeseen events.

2. External Influences: Market outcomes can be significantly influenced by various external factors like geopolitical events, economic announcements, and sudden shifts in market sentiment. Such factors are often not considered in backtesting simulations.

3. Market Dynamics: Elements like market volatility, liquidity constraints, and slippage can drastically alter expected outcomes. These dynamics might not always be accurately represented in backtest simulations.

4. Limitations of Simulated Trades: Backtesting operates under the assumption that historical trends and patterns will replicate. However, market conditions evolve, and what worked in the past might not necessarily be viable in the future.

5. Informed Decisions: Always base your trading decisions on a mix of comprehensive research, current market analysis, and risk assessment. Relying solely on backtested results can lead to misconstrued perceptions and potential pitfalls.

Trading involves risks, and it's crucial to be fully informed and cautious before making any investment decisions. Always consider seeking advice from financial experts or professionals when in doubt.

Abz US Real ratesThis indicator shows Fed Funds Rate vs US inflation. It also shows the US 10 year bond yield and provides a color indication that aims to indicate if this is a period where owning TLT is a good idea or not. It is not investment advice and it is only aiming to indicate whether the trend is supportive or not for long dated US bonds in comparison with short dated treasury bills and versus inflation.

Recessions: Recessions are indicated by a grey background.

Yield inversion: Periods where the Fed Funds Rate is above the US 10 year bond yield are shown as a maroon background and frequently are macro indicators of an upcoming recession. Like other macro signals, this can't be relied upon as a timing tool.

This is intended to be used as an indictor on a long term chart. Minimum would be weekly but could be even more valid to focus on a chart with monthly candles.

Forex & Stock Daily WatchList And Screener [M]Hi, this is a watchlist and screener indicator for Forex and Stocks.

This indicator is designed for traders who trade in the forex markets and monitor developments in indices and other currency pairs.

It includes information on 14 indices such as the volatility index, Baltic dry index, etc. You can customize the indices as you wish. The indices table contains the index's price (or points), daily change, stochastic value, and trend direction.

The second table is designed for trading forex and stock currency pairs.

In this table, you will find information such as price, volume, change, stochastic, RSI, trend direction, and MACD result for all traded pairs. You can customize all the currency pairs in this table as you wish, and you can also tailor the oscillator settings to your preferences.

In the settings section, you can use checkboxes to hide the pairs in both tables.

The "Customize" section in the settings allows you to personalize the table appearances according to your preferences.

S__Trader's Portfolio ManagementThis custom TradingView script is a powerful tool designed to help investors effectively manage their portfolios. This script allows you to monitor, analyze, and optimize your portfolio performance using moving averages in technical analysis. This script is for the traders who want to manage his portfolio by moving averages which is powered by using 4 of them together.

Timeframe is based on Daily as default but you can prefer to see weekly, monthly or else depends on your trading character

This script uses 4 customizable moving averages to decide cash/stocks ratio. Each moving average has %25 power of decide. If price is above the moving average, each moving average adds %25 to stock total percentage, else below they add %25 to cash. So you can decide your cash stock ratio by that moving averages.

For example if price is above all of that moving averages, script table shows you %100 total for stocks but if price is above for example 2 of that moving averages, script table shows you %50 for stocks and get remaining %50 cash.

For example if price is above only 1 of that moving averages, script table shows %25 for that stocks and that means %75 cash.

If price is below all that moving averages, script table shows %0, means that sell all stocks and stay cash %100

You can choose to plot moving averages or not

Or you can choose just track them by line

You can hide table also and decide table size and place at graph

By using this script, you can monitor your portfolio's performance, manage risk, and optimize your investment strategies. However, please remember that this script is just a tool and should not be used as a sole decision-making tool for investments. Always use it in conjunction with risk management and other analytical methods.

Hopefully, this script will help you enhance your investment process. Best of luck!

Position calculator [krazke]This indicator will help you calculate your position. This will automatically calculate potential liquidation price and select leverage for your stop loss and risk size.

How to use it:

1. Select position direction. (long checkmark - selected if it's long)

2. Select entry. If you want to use custom entry price select checkmark and set value. (Current price is default entry)

3. Enter stop loss.

4. Enter risk.

5. Enter max leverage for current ticker.

P.S. Liquidation price is not 100% correct but it almost.

Equity Trade Risk ManagerEquity Trade Risk Manager is a simple indicator that helps you protect your portfolio by going into each trade risk first !

Equity Trade Risk Manager does this by calculating your ideal position size or ideal stop loss based on your account size, purchase price and risk tolerance. This ensures you are never risking more than your predetermined amount on each trade.

Unlike most position size calculators, that will only tell traders how many shares to purchase, Equity Trade Risk Manger allows the trader to choose whether they want to calculate the ideal number of shares to purchase or where to set the trades stop loss based on the number of shares owned. Not only that, but knowing traders need to act fast, the indicator also gives the option to quickly use the current price and low of the day as an entry and stop. Lastly, your stop loss will be plotted onto the chart for a visual aid.

Features:

Dynamic Risk Settings:

Account Customization: Input your account size to get metrics tailored to you.

Calculation Choices: Decide if you want the tool to calculate the number of shares you should buy or where to set your stop-loss.

Custom Risk Parameters: Use preset risk percentages or set your own to match your comfort level.

Price Point Flexibility:

Enter your entry and stop price or opt to use the current price and the low of the day.

Interactive Display Settings:

Customizable Interface: Adjust table positions, text size, and color schemes to match your trading dashboard aesthetic.

On-Chart Stop-Loss Indication: Visualize your stop loss on the chart itself.

Get a snapshot of your dollar risk, position size, shares to buy, and stop-loss.

Trade Warehouse (SPOT trades)Hello there!

Let's imagine You are trading SPOT, buy more and more every new dump, but bear market is not going to stop... and your first trade was 3 YEARS AGO!!!

Can't believe it is true.

The problem is - exchanges allow You to see only new trades last 6 months(Binance). But I want to see all of them! How do I know AVG Price?

This script is my solution. Just use it to track and store your trade, so You can see AVG without uploading old trades everytime and using calculator.

Script description:

Here You can see the "Trade" type of variable. Python script using Pandas converts trades from .csv file into string type that You can input as trade(price, pair, amount, date..). After it uppends to the trades_array and pushed into the loop.

If trade date is more than current cundle - it pushes new trade to other arrays such a "pair", "avg_tot" etc. to comput it later.

If trade was buy - it increase invested capital and owned amount, opposite for sell and recomputs AVG price.

Since script has at least 1 trade it starts to plot AVG price.

There are 2 AVG price:

1. For total invested counting(You can get negative value if traded successful)

2. Current AVG price since last 0 currency amount(there is dust value to set how many usd we take as dust)

Table represents all assets statistics

Just upload your trades only 1 time, use script to convert it into pine code, and use as indicator. This script allow You to see ALL trades from oldest to the newest.

github.com/Arivadis/...w_Tradings_warehouse

If this script helped You - press Star (on GitHub) Like (on TradingView)

Warning -

Does not include free/earn/withdraw/deposit counting. Only Buy and Sell =>

This script has no idea about your side currency deposits, so if You got Your BTC or EUR or .. from another wallet and sold later - it can break your statistical data. Add this transfer manually(see examples inside script).

Use my github manual to get this script workin.

Installing takes around 3 minutes and contains 3-5 steps

Risk Management and Positionsize - MACD exampleMastering Risk Management

Risk management is the cornerstone of successful trading, and it's often the difference between turning a profit and suffering a loss. In light of its importance, I share a risk management tool which you can use for your trading strategies. The script not only assists in position sizing but also comes with built-in technical features that help in market timing. Let's delve into the nitty-gritty details.

Input Parameter: MarginFactor

One of the key features of the script is the MarginFactor input parameter. This element lets you control the portion of your equity used for placing each trade. A MarginFactor of -0.5 means 50% of your total equity will be deployed in placing the position size. Although Tradingview has a built-in option to adjust position sizing in a same way, I personally prefer to have the logic in my pinecode script. The main reason is userexperience in managing and testing different settings for different charts, timeframes and instruments (with the same strategy).

Stoploss and MarginFactor

If your strategy has a 4% stop-loss, you can choose to use only 50% of your equity by setting the MarginFactor to -0.5. In this case, you are effectively risking only 2% of your total capital per trade, which aligns well with the widely-accepted rule of thumb suggesting a 1-2% risk per trade. Similar if your stoploss is only 1% you can choose to change the MarginFactor to 1, resulting in a positionsize of 200% of your equity. The total risk would be again 2% per trade if your stoploss is set to 1%.

Max Drawdown and MarginFactor

Your MarginFactor setting can also be aligned with the maximum drawdown of your strategy, seen during a backtested period of 2-3 years. For example, if the max drawdown is 15%, you could calibrate your MarginFactor accordingly to limit your risk exposure.

Option to Toggle Number of Contracts

The script offers the option to toggle between using a percentage of equity for position sizing or specifying a fixed number of contracts. Utilizing a percentage of equity might yield unrealistic backtest results, especially over longer periods. This occurs because as the capital grows, the absolute position size also increases, potentially inflating the accumulated returns generated by the backtester. On the other hand, setting a fixed number of contracts as your position size offers a more stable and realistic ROI over the backtested period, as it removes the compounding effect on position sizes.

Key Features Strategy

MACD High Time Frame Entry and Exit Logic

The strategy employs a high time frame MACD (Moving Average Convergence Divergence) to make entry and exit decisions. You can easily adjust the timeframe settings and MACD settings in the inputsection to trade on lower timeframes. For more information on the HTF MACD with dynamic smoothing see:

Moving Average High Time Frame Filter

To reduce market 'noise', the strategy incorporates a high time frame moving average filter. This ensures that the trades are aligned with the dominant market trend (trading the trend). In the inputsection traders can easily switch between different type of moving averages. For more information about this HTF filter see:

Dynamic Smoothing

The script includes a feature for dynamic smoothing. The script contains The timeframeToMinutes(tf) function to convert any given time frame into its equivalent in minutes. For example, a daily (D) time frame is converted into 1440 minutes, a weekly (W) into 10,080 minutes, and so forth. Next the smoothing factor is calculated by dividing the minutes of the higher time frame by those of the current time frame. Finally, the script applies a Simple Moving Average (SMA) over the MACD, SIGNAL, and HIST values, MA filter using the dynamically calculated smoothing factor.

User Convenience: One of the major benefits is that traders don't need to manually adjust the smoothing factor when switching between different time frames. The script does this dynamically.

Visual Consistency: Dynamic smoothing helps traders to more accurately visualize and interpret HTF indicators when trading on lower time frames.

Time Frame Restriction: It's crucial to note that the operational time frame should always be lower than the time frame selected in the input sections for dynamic smoothing to function as intended.

By incorporating this dynamic smoothing logic, the script offers traders a nuanced yet straightforward way to adapt High Time Frame indicators for lower time frame trading, enhancing both adaptability and user experience.

Limitations: Exit Strategy

It's crucial to note that the script comes with a simplified exit strategy, devoid of features like a stop-loss, trailing stop-loss or multiple take profits. This means that while the script focuses on entries and risk management, it might result in higher losses if market conditions unexpectedly turn unfavorable.

Conclusion

Effective risk management is pivotal for trading success, and this TradingView script is designed to give you a better idea how to implement positions sizing with your preferred strategy. However, it's essential to note that this tool should not be considered financial advice. Always perform your due diligence and consult with financial advisors before making any trading decisions.

Feel free to use this risk management tool as building block in your trading scripts, Happy Trading!

MarketSmith VolumesThe 'MarketSmith Volumes' is to be used with the 'MarketSmith Indicator' and 'EPS & Sales' in order to mimic fully MarketSmith Graphs with the maximum number of indicators allowed by a free Tradingview Plan: 3

This indicator is no more than a simple volume indicator where all parameters are already adjusted to resemble MarketSmith graphical volumes.

Also you will find integrated:

High Volumes Bars Peak :

They allow us to see peak volumes at a glance.

10-Week Average Volume :

When viewing a weekly chart, this line represents a 10-week moving average volume level. It allows you to see if the current Volume Bar of the week is above or under the average volume traded in the past 10 Weeks.

50-Day Average Volume :

When viewing a daily chart, this line represents a 50-day moving average volume level. Whether or not volume is above or below the average for a certain period could have a significant impact on your stock chart analysis.

TradePlannerTradePlanner is trade planning tool which helps to map out your trade plan by displaying an entry line, a stop line, and multiple target lines (up to 5 targets) right on the chart. Each line can be configured to display the distance from the entry in terms of both number of ticks as well as the profit/loss in currency terms. An on-screen table quantifies and summarizes the entire trade plan information plus it calculates and displays the maximum lot size given the specified amount of risk you want to take per trade, which is totally customizable, all of which takes the guesswork out of trade planning.

MarketSmith IndicatorThis script provides you with several indicators that will enable you to mimic MarketSmith charts, even with a free TradingView plan.

You can use this script with my ' EPS & Sales ' indicator.

MarketSmith-style bars

The script offers an original approach to managing candlesticks within the code, making them almost identical to those on MarketSmith.

For a perfect display, select ' Bars ' on your chart and set the opacity of your candles to 100% to display only the candles proposed by this indicator.

If you don't want them, you can simply disable them in the ' Style ' tab by unchecking 'MarketSmith Bars' and 'Chars'.

These candles are designed to be used with a fix chart. (No beautiful result with zooming in or out.)

Normally, the display will still be correct by right-clicking, and ' Reset Chart '.

Simple customizable moving averages

With automatic distinction of the weekly time unit. You can choose to display them or not, select the calculation method and modify their length via the panel.

The RS Rating indicator

I've integrated the RS Rating indicator into this script, as the RS Rating is a fundamental component of this layout.

High and valley points

These points are used by MarketSmith to detect bases, patterns, cup & handle.

Designed for US Market only you won't be able to screen correctly the India market for example.

External Indicator Analysis Overlay | Buy/Sell | HTF Heikin-AshiThis chart overlay offers multiple candlestick display options. The Regular (Japanese) and the Heikin-Ashi candles are well known. The Mari-Ashi (or Renko) option is something special as it should be timeframe independent, so that sideways action should be represented in one candle. That is difficult to realize as an overlay on the normal candlestick structure, but perhaps the chosen implementation is useful nonetheless. The Velocity option is experimental and is designed to show if the price has accelerated too much in a trend direction. In this case, the highs and lows do not reflect the actual highs and lows, but indicate the overshooting velocity. The opening of the candle also depends on the inherent velocity, but the close of the candle is always the actual close. Anyway, it doesn't look very useful, but the option is there.

All options can be applied to higher timeframes. A usable setting is obtained by disabling only the body of the TradingView candles in regular mode and enabling this overlay.

A large part of this overlay consists of buy/sell indication settings. For activation it is necessary to select an external source. For example the “Relative Bi-Directional Volatility Range”, specifically the Trend Shift Signal (TSS). This signal switches from 0 to 1, if the trend becomes bullish or from 0 to -1, if the trend becomes bearish. It will be automatically detected without specifying the Indication Type. Alternatively, the Volatility Moving Average (VMA) would meet the requirements for the Indication Type “Buy = positive | Sell = negative”. The Moving Average Convergence Divergence (MACD) also fulfills these conditions. Another example is to use any Moving Average with the Indication Type “Buy = rising | Sell = falling”. In the chart above the Hull Moving Average (HMA) is used. In addition, it is possible to reverse the signal, so that positive signals become negative and vice versa. The signals will be labeled as Buy or Sell on the chart.

The user can analyze whether the provided signals are good or bad indications for going long or short or simply for rebalancing a portfolio. Therefore, it is possible to set a starting point for the analysis and choose a weighting for the investments from 0% to 100% of the portfolio. To avoid sleepless nights, a very reliable (and conservative) setting seems to be Rebalancing with 50% (very similar to the well-known 60/40 portfolio). The calculation results are shown in a table.

As a small addition there is the possibility to label the peaks by setting the distance between the highs/lows. This will make the quality of the buy and sell signals even more clear.

Symbol Searcher [EmuMoon]Introducing the EmuMoon 'Symbol Searcher'. Your go-to tool for quickly comparing and discovering the best coins/symbols to trade.

With this nifty tool, you can easily search and compare 40+ different coins/symbols simultaneously to find the most volatile ones, while also identifying coins that are already correlated to the ones you're trading. That way, you can diversify your portfolio and avoid putting all your eggs in one basket.🧺🐣

The Symbol Searcher lets you sort by volatility, correlation and weighted combinations of both. You can even input your own coins/symbols to see how they stack up. It's a fun way to explore the crypto/trading market and find new opportunities.

You can also add the 'Symbol Searcher' to the chart multiple times to display even more symbols. This works excellent with the other DCA Tools that are Advanced!

Features

The EmuMoon 'Symbol Searcher' has a number of features, including:

• Optimal Coin Selection - The 'Top Picks' Table automatically populates with coins/symbols exhibiting the most desirable values that are well suited to trading.

• 'Sort By' Drop-Down - Explore a wide range of sorting options to discover coins/symbols that align with your target goals and preferences.

• Lookback Duration - Small or broad, you can specify the quantity of bars/candles that are used when performing internal calculations.

• Customisable View - Choose the Quantity of Pairs to Compare and also separately choose the Quantity of Pairs to Display.

• Real-Time Data - Receive up-to-the-minute data on coins/symbols, pick any time frame interval to make informed and timely choices.

• Quick & Easy - You can search, compare and analyse a wide range of coins with speed and convenience and no complex setup.

• Default Pairs - Carefully selected from Binance USDT Spot, the top 40 pairs with a 'Maximum Supply' based on the highest statistics at the time of creating. Add your own at any time.

• Connectivity - Use on the go, on any device. Settings menu and display tables have been optimized to look great on Mobile as well as PC, Browser, App, Laptop, Mobile, Tablet etc.

• Fast Loading - Streamlined array/table structure means enhanced script compile times, significantly improving script compiling times and timeout errors.

Settings

• Show Main Table - Show or hide the main coin selection table.

• Display X Pairs - Choose how many pairs to display.

• Compare X Pairs - Choose how many pairs to compare.

• Lookback - Choose the quantity of bars/candles to be used for the Correlation and Volatility calculations.

• Sort By - Choose how the main table is sorted.

• Show Top Picks Table - Show or hide the Top Picks Table.

• + Corr X Vol - Choose the quantity of High Correlation + High Volatility coins to show on the Top Picks Table.

• - Corr X Vol - Choose the quantity of Low Correlation + High Volatility coins to show on the Top Picks Table.

• o Corr X Vol - Choose the quantity of Neutral Correlation + High Volatility coins to show on the Top Picks Table.

• Symbol Input 1 - To check for correlation, the script utilizes coin slot number 1 as a reference, comparing it against all the coins numbered 2~40.

• Symbol Inputs 2~40 - Customize the coin inputs (2~40) according to your preference.

• Table Position - Adjust location of table plotted on chart. You can also add the 'Symbol Searcher' to the chart multiple times to display even more symbols. 🎉

• Info & Help - Some great information about the script and its features

• Text Size - Whether you are on PC, App, or Tablet, you can adjust the view to fit your device.

Usage

While statistics provide valuable insights, they should not be solely relied upon as an indicator of future results. This script serves as a tool traders can utilise to help gain an overview of the market landscape, and quickly compare and identify potential opportunities, enhancing their decision-making process. To use the indicator, simply input your chosen coins/symbols or use the defaults, select the quantity you want to compare, choose a sorting option, you can also generate a Top Picks list based on the highest performing values by using the +/-/o Corr X Vol quantity selections.

Broadview Algorithmic StudioWelcome! This is the writeup for the Broadview Algorithmic Studio.

There are many unique features in this script.

- Broadview Underpriced & Overpriced

- Broadview Blackout Bollinger Bands

- Trailing Take Profit Suite

- Algorithmic Weights

- VSA Score

- Pip Change Log

- Activation Panel

- Weight Scanner

There are 116 primary inputs that allow users to algorithmically output unique DCA signal-sets. There are 85 inputs that allow users to control individual lengths, levels, thresholds, and multiplicative weights of the script. You will not find any other script with this many inputs, properly strung together for you to produce unlimited strategies for any market. The entire premise for the Broadview Algorithmic Studio is for users to be able to have extensive-cutting-edge features that allow them to produce more strategies, having control over every element that outputs a signal set. The number of unique strategies you can output with this script is VAST, and each continues to follow a safe DCA methodology.

This script is ready for use with 3Commas, interactive brokers, and other means of automation. It provides detailed information on Base Orders and Safety Orders, giving the number, cumulative spending, position average, and remaining balance for each SO in the series. Using this script we will explore the depths of strategic volume scaling, and the algorithms we use to determine spending.

Let me first start by saying the number of safe DCA-friendly signal-sets this script can output is absolutely staggering.

Let's limit the scope just to the Broadview Underpriced & Overpriced and Broadview Dominance indicators.

Each band of the Dominance Suite can be controlled individually with unique lengths, levels, and weights. This means the Dominance Suite can establish Bearish or Bullish dominance, in any market condition, and give it a unique overloading weight. The Broadview Underpriced & Overpriced indicator finally gives us the ability to establish these "market conditions" first with cycles. Of all the cycles this indicator establishes, the two primary are Underpriced & Overpriced. We determine this using a composite Overbought & Oversold with an Exponential Moving Average. So the script can now know, what cycle it is in, who is dominant during that cycle, and exactly how much weight in volume scaling the order should have.

Brand new is the ability for indicators of this level to be able to talk together in a single script. The Broadview Underpriced & Overpriced indicator and the Broadview Dominance indicator can inform one another across multiple vectors, create a unique market snapshot, and give that snapshot a unique weight every bar. The unique weight is compiled in the volume scaling math, thus giving us an automated-strategic-safe and quite efficient volume scaling for every order. In our coming updates we will explore this synergy to its very deepest layers. These indicators can be laced together in many ways, called vectors.

Only in the Algorithmic Studio do we explore these depths and yield those findings, features, and inputs to the user.

Let me take a quick break to explain another area-of-opportunity for our research and development.

The VSA Score is something we've tried before, but until the creation of the Broadview Blackout Bollinger Bands Auto Indicator it was not possible. The concept we want to explore is "Positional Honing". Over time we want users and the script itself to be able to understand the difference between a script-config that produces a high number of Hits, from a configuration that produces a high number of "Misses". The Volume Scaling Accuracy Score uses the BBB Auto Indicator as a heavily reliable, non-repainting, method of determining what the very-best signals for increased volume-scaling are.

Increased volume scaling is denoted by the near-white highlighter line running vertically. This line will either fall inside the BBB Auto Indicator bands (which are hidden), or, they will fall below and outside the BBB Auto bands. If increased spending happens inside the bands it's a "Miss". If increased spending happens below and outside the bands, it's a Hit. Oftentimes misses are actually pretty good spots for extra spending, which helps lower your position average, but Hits are always better. The Hits that the BBB Auto Indicator provides are extremely good.

Let's talk about the Trailing Take Profit Suite. This suite allows us to set a trailing take profit which is a feature that lets one maximize their profits. If the trailing take profit is engaged, then when the regular take profit is hit, it will trigger, denoted in red vertical lines, and the trailing take profit will look for a specified rate of change before it actually takes profit. This usually helps traders in those times when their regular take profit was set too low, allowing them to maximize their profits with a Trailing Take Profit.

For the moment, let's think about our scores. In the dashboard you'll notice a score beginning the Pip Change Log, the VSA Score, and the Activation Panel.

These scores use a new kind of logistic correlation formula where 4 digits are given to activation, rather than 1. This is to allow room for a future concept in AI we call "Deadzones" or you can think of it as impedance. This is not a bias in logistic regression. It's an entirely different concept. A neuron, which a perceptron attempts to mimic, has a bias.. but it also has a sort of electrical resistance. This is because a neuron is individually-alive entity. So a perceptron, as it were, would need to have both a bias and a natural resistance, or deadzone.

It is a lot of fun to watch the scores and how they react during playback. They tend to smooth trends but are also quite quick to correct to accuracy. In the future we will add the deadzones and biases to the scores. This should help both users and the script produce better signal sets. The Pip Change Log is an indicator that measures Rate of Change in Pips. This is one that I am particularly excited to study, as I am a huge fan of ROC. The Activation Panel shows these scores for 4 primary indicators: On Balance Volume, Relative Strength Index, Average Directional Index, and Average True Range.

Having the Pip Change Log, VSA Score, and Activation Panel up on the dashboard with their logistic correlation scores allows traders to study markets and setups quite intimately. The weight scanner at the bottom allows users to track the cumulative applied multiplicative weights during playback. The massive number of inputs, connected vectors of indicators, input-weights, lengths, levels, and thresholds sets up all the algorithmic infrastructure for powerusers to explore every idea and strategy output they could imagine. Also with the connected vector infrastructure we can deepen our indicators in a way where, "How they talk to each other.", comes first in every development conversation.

The Algorithmic Studio is for the Power-user.

These are not basic equations coming together to determine spending. This is a massive multi-layered-perceptron with everything from Trailing-Take-Profits to strategic-automatic algorithmic downscaling. The Broadview Algorithmic Studio gives a home to the poweruser who wants access to everything in a trading and investing AI, right up until the backpropagation. The Broadview Algorithmic Studio, gives users the ability to sit in the chair of the would-be AI.

Thank you.

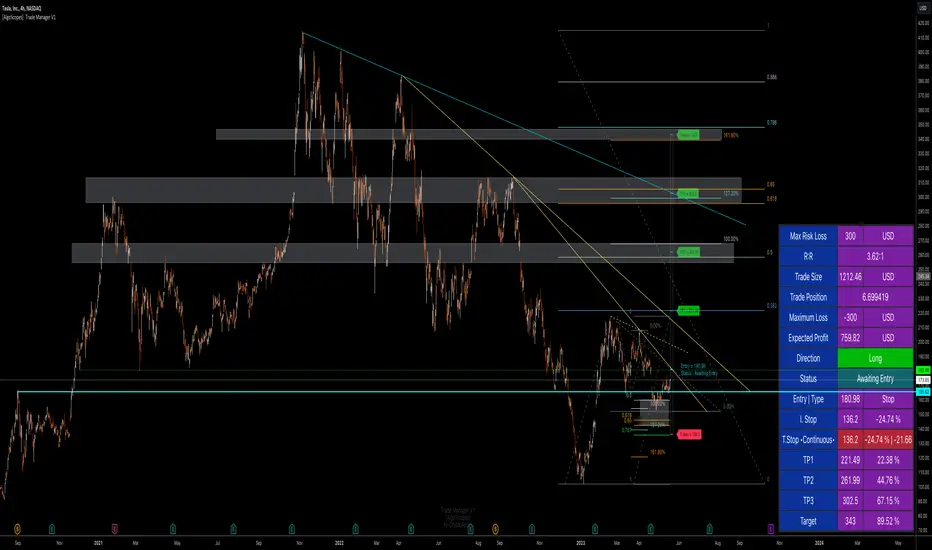

Trade Manager & Position Size Tool & PnL Tracker [AlgoScopes] V1Position size tool, leverage calculator, trade tracker, money management, trade presentation, risk reward management, margin position, live profit and loss, that's all in this one Trade Manager indicator.

The idea for this indicator comes from two years ago when I was helping a friend who, at the request of 15-20 members from our telegram group, wanted to create a paid group and share our ideas for trade with them (it started as an experiment for just a month or two and ended with 15 months with over 500 trading ideas and signals, with a complete TA chart). If I had time to create this indicator back then for members, it would have been much easier for them to be able to understand and follow the trade idea that was presented through a classic chart, with all the things that a TA must have:

Entry (as well as the reason for entry),

Stop (where the idea for the trade is no longer valid),

Target (with the reason why it is the target for that trade),

Take profits (taking part of the profit on the way to the target).

The majority of members still did not understand how much position to trade, what is the possible profit or loss, if the margin trade is how much leverage to use, in one word “money management”. The most important rule that every trader must follow is "Plan your trade and trade your plan". Learn money management and you are halfway there to becoming a successful trader. It is only after all that, you learn to use some of the "holy grail" indicators. When you have mastered those first two rules, find and master your favorite indicator or trading style (the most important thing is to stick to those two rules). The margin | leverage is also included in the script, for which there are so many dilemmas, arguments and discussions. (that many who still do not understand margin, would trade that it is not passionate if it is controlled). Too much for an introduction, especially since this indicator has so much to explain.

Most importantly, this is an invite-only indicator, and there are so many free indicators on tradingview that can also serve you very well. As far as I know, all exchanges have a calculator tool to calculate the possible profit and loss for each trade you plan to take.

*This indicator is not recommended for scalping on a 1min chart because the script, as you will see, is very complex, so the loading time is longer than with simpler indicators.

💠 ABOUT THE SCRIPT

This script is made to help manage trade. In this one indicator you have the possibility to do technical analysis, calculation for trade (four types: account size risk, trade investment, maximum to lose or position size), monitor 'PnL' (profit and loss in real time) do the calculation in the second, maybe local currency, and set an alert (from entry to any other change in trade). As the script is made for general use, some slight differences are possible for real time 'PnL' or 'ROI'. Always do a test before you start trading with larger amounts. The script is recommended for intra day trading and above. The script is not recommended for scalping on the 1min chart

💎 PROCESS TO ADD SCRIPT TO CHART

Possible trade on break example trade

As this script is invite-only, to add it to the chart you need to click on Indicators and find it under the 'Invite-Only' section. When you add the script to the chart (as it is interactive), you will be asked to do 4 steps.

🔸 'SET TRADE TIME'

Click on the chart where the last vertical bar is.

If you are already in the trade, then find the bar|time where the trade started

(you want to follow trade or trade presentation)

🔸 1) 'SET ENTRY'

Click on the horizontal level where you want to place the Entry

🔸 2) 'SET STOP'

Click on the horizontal level where you want to set the Stop

🔸 3) 'SET TARGET

Click on the horizontal level where you want to place the Target

💎 CONFIRM INPUTS

After you have done those 4 steps, a popup will appear with the relevant inputs for the trade.

You will see that some inputs are already filled (done in those 4 steps before, Entry, Stop and Target). You can correct them if you want (you will sometimes notice a longer 'space decimal' for the trade ticker, but this will not affect the calculator or other parts of the script). You can do the rest of the inputs for trade or finish it later when the script is loaded on the chart (it is recommended to fill in 'Trade Type' and 'Amount'. Don't forget to click on the "Apply" button to load the script on the chart.

💎 INDICATOR LOADED ON CHART

• When the indicator is loaded on the chart (regardless of whether it is a new trade or a trade that has already started), the following items are displayed by default:

🔸 ' Trade Table ' shows all relevant information for the trade

🔸 ' Trade Box ' with lines for Entry, Stop and Target (Take Profits if enabled)

🔸 ' Trade Box Labels ' with relevant data

• The Entry label is also the trade status label, and if the trade is not active, by default it is the Entry color

If the trade is active or when a new trade reached Entry, several new things are noticeable:

• Entry|Status label as well as status row in table will change color as well as 'Entry Reached' text

• Several extra columns relative to trade will be added to the Entry|Status label

• 3 new columns will also appear on the Trade Table (Live PnL, Live min PnL and Live ROI)

• If Trail Stop is enabled, the label will change the text to T.Stop and change color depending on whether it is in loss or profit.

• If Trail Stop is enabled, inside Trade Box trail line it will follow price action inside the box, while the label will always be fixed at the initial level

• A vertical colored line will appear on the right side of the Trade Box (depending on whether the trade is in profit or loss) which shows as in the Trade Table like Live PnL

⚪ SETTINGS

💎 Trade Account Setup

🔸 ‘Trade Type’

• 'Account Capital' or portfolio (with combination '% Capital Risk')

• 'Investment' (how much you want to invest in the trade)

• 'Risk To Lose' (how much you want to risk losing)

• 'Position Size' (exact position size, units|share for trade)

🔸 ‘Account Type’

• If the account is in another currency or you want to see possible profit | loss in local currency

• Around 150 world and local currencies supported by ICE exchange

🔸 ‘Amount’

• Amount for ‘Trade Type’

🔸 ‘% Capital Risk’

• Only for ‘Account Capital’ trade type

(i.e. 10.000 account capital with ‘% Capital Risk’ 4 is 10.000 x 4% = maximum loss 400)

🔸 ‘Leverage’

• Enable|Disable for margin trade i size of leverage (maximum 125x)

(be sure to study how and when to use margin trade through the tutorial, because margin trade can be very dangerous. If you have not perfected margin trade, there is a great possibility of losing most or even all of your account capital).

💎 TRADE ENTRY & TARGET & STOP & T.STOP & DATE | TIME

🔸 ‘Trade Date & Time’

🔸 ‘Entry’

🔸 ‘Stop’

🔸 ‘Target’

• (all was set in the previous step but can be correct/adjusted if needed)

🔸 ‘Market Entry’

• Enabled will move Entry on that bar close

🔸 ‘Liquidation’ (enabled by default)

• Show ‘Warning’ if trade Stop is close or invalid (trade will hit liquidation before reached Stop level)

🔸 ‘Trailing Type’ (4 trailing stop type)

• ‘Disabled’ (Stop will stay the entire time at the initial stop level)

• ‘Continuous’ (I.Stop follow price by distance or percent when price reached Trail start level)

• ‘Stepped’ (I.Stop moves to previous level when price reached Trail start level)

• ‘Breakeven’ (I.Stop moves to Entry when price reached Trail start level)*

* (least one Take Profit enabled)

🔸 ‘Trailing Active’ (Entry, TP1, TP2 and TP3)

• Trailing stop starts level if ‘Trailing Type’ is enabled

🔸 ‘Trailing by’ (distance or percent)

• ‘Distance’ (T.Stop will follow price action by distance)

• ‘Percent’ (T.Stop will follow price action by percent)

(this is a good example to see the difference between trailing by initial distance and initial percentage)

🔸 ‘T.Stop Distance & Percent’ (initial distance and percent for table trade only)

• Useful for bot or exchange

🔸 ‘Stop, T.Stop, Target and TP’s in PIP’s’

• Distance in PIP’s

💎 TAKE PROFIT

🔸 ‘Split Target’ (enabled by default to three take profits (TP) with auto split)

🔸 ‘Number of Take Profits’ (up to three take profits)

🔸 ‘Type’ (auto or manual)

• For manual type fill all prices to preferred level. TP percent (TP1%, TP2% and TP3% ) and Target% is how much profit you want to take on a specific level.

• PLEASE NOTE sum of all enabled ‘TP’ and targets = 100 (e.g. two TP and sets TP1% to 25 and TP2% to 35, then Target% should be 40% i.e. 25 + 35 + 40 = 100)

💎 TRADE BOX & LINES

🔸 ‘Target Line’ (color for target line and trade table ‘direction’)

🔸 ‘Stop Line’ (color for initial line and trail line)

🔸 ‘Entry Line’ (color for entry line and label & table status)

🔸 ‘To Trade Time’ (‘trade box’ left vertical line)

• By default is set to trade date and time

• Unchecked will be moved to the last bar (live time)

🔸 ‘Extended Left’ (extend Entry, Stop, Target and TP’s lines to left)

• To check for possible support|resistance

🔸 ‘Size’ (Entry, Stop, Target and TP’s lines size)

🔸 ‘PnL Box Size’ (line size for vertical box lines)

🔸 ‘Offset’ (right vertical line offset from last bar)

🔸 ‘PnL Box Color’ (right vertical line and trail fill color)

• Color changes for profit & loss

🔸 ‘Box Line Color’ (box base color)

💎 LABELS

🔸 ‘Stop & Target Labels’ (enable|disable stop and target labels)

• By default is set to small (tiny, small, normal, large, huge and auto option)

• Disabled will move all information on Entry|Status label

🔸 ‘Offset’ (label offset from trade box)

🔸 ‘Target Label’ (label color for target and all enabled tp’s)

🔸 ‘Stop Label’ (label color for initial stop and enabled trailing stop)

🔸 ‘Label Text’ (color for label text)

🔸 ‘Status Label Color’ (label table entry|status color when trade is not active)

🔸 ‘PnL’ (entry|status color for profit and loss)

🔸 ‘Size’ (by default set to normal, option tiny, small, normal, large, huge and auto)

🔸 ‘Risk to Reward’ (show risk to reward on labels)

🔸 ‘Extra Info’ (by default disabled, show extra related info for trade on labels)

• Useful if Trade Table disabled

🔸 ‘Close Trade Stats’ (by default disabled, show all info when trade is closed)

• By default is white text color for close trade stats label

💎 ALERTS

🔸 ‘Failed Trade’ (alert if price reached Stop before is active, reached Entry)

• Useful if trade need adjustment but it can also be left as it is

and alert is just warning

🔸 ‘New & Update Alert’ (alert when price reached Entry or change status to enabled Take Profits)

🔸 ‘Trade Closure Alert’ (alert when trade closed, reached Stop, Target or enabled Trail Stop)

• Alert can be in modified or default preset jSon format as well as in plain text format

• Place holders for creating alerts are :

{type}, {symbol}, {exchange}, {ticker}, {base}, {quote}, {timeframe}, {price}, {direction}, {entry}, {stop}, {tstop}, {tp1}, {tp2}, {tp3}, {target}, {tstopstatus}, {status}, {result}

* {type} placeholder is set to ‘Trade Active’, ‘Trade Update’ and ‘Trade Closed’

💎 TABLE DISPLAY

🔸 ‘Trade Table’ (enable|disable trade table)

🔸 ‘Position’ (by default set to bottom right with option bottom, middle and top with left, center and right)

🔸 ‘Size’ (by default set to normal, option tiny, small, normal, large, huge and auto)

🔸 ‘Full Table’ (by default enabled, disabled show small table without some info*)

* check picture for reference

🔸 ‘Presentation’ (by default disabled, hide all info related to PnL in trade currency)

• Useful if trade shared for presentation, hidden trade fiat|currency info)

🔸 ‘Header’ (color for trade table first row)

🔸 ‘Stats’ (color for trade table statistics row)

🔸 ‘Text’ (color for trade table text)

🔸 ‘Error’ (color for all errors if is made when trade is setup)

• Color for errors is for trade table and trade labels

🔸 ‘Fiat Price’ (by default enabled, show info for second fiat*

* if trade is in crypto and ‘quoted’ currency is not stable coin, like ETHBTC, or ‘Account Type’ is set to different currency

🔸 ‘Live Fiat Price’ (if ‘quoted’ currency enabled will show live exchange conversion)

🔸 ‘All Errors’ (enabled by default, show all error if trade setup is wrong)

• When error shows on trade, disabled this to see what|where is error

• Check below for more details

🔸 ‘Tool Tip (chart)’ (enabled show all tooltip on chart)

• Check below for more details

• When you are familiar with indicator, disable popup tooltip

💎 TOOLTIP

All possible tooltips have been added for easier understanding, especially for traders who are just learning how to place a trade. (when you perfect this indicator, you can turn off the tooltip in settings, and you can also normally use the lite version of this indicator, which does not contain all these futures)

🔸 ' Settings Tooltips’

🔸 ‘Chart Tooltips’

🔸 ‘Table Tooltips’

🔴 ERRORS

When you setup trade, not only a novice in trading, but also experienced traders can make a mistake and for this reason all possible errors are included in the indicator which will be shown on the chart by changing the color of the labels as well as on the trade table and in most of the cases and error text.

If the tooltip is enabled in the settings, you can see the reason for the error as well as the solution.

Here are some examples of possible errors.

Stay safe

PLAN YOUR TRADE AND TRADE YOUR PLAN

VWCE * DXY valuationVWCE is priced in EUR, but it is calculated in USD. It is always good to know VWCE´s "real" valuation. As sometimes the price of VWCE may seem expensive, but the underlying DXY can indicate otherwise. Helpful to get an impression of the real value of VWCE for EUR-based traders and to know where the world market is standing.