Retrograde Periods (Multi-Planet)**Retrograde Periods (Multi-Planet) Indicator**

This TradingView script overlays your chart with a dynamic visualization of planetary retrograde periods. Built in Pine Script v6, it computes and displays the retrograde status of eight planets—Mercury, Venus, Mars, Jupiter, Saturn, Uranus, Neptune, and Pluto—using hard-coded retrograde intervals from 2009 to 2026.

**Key Features:**

- Dynamic Background Coloring:

The indicator changes the chart’s background color based on the current retrograde status of the planets. The colors follow a priority order (Mercury > Venus > Mars > Jupiter > Saturn > Uranus > Neptune > Pluto) so that if multiple planets are retrograde simultaneously, the highest-priority planet’s color is displayed.

- Interactive Planet Selection:

User-friendly checkboxes allow you to choose which planets to list in the table’s “Selected” row. Note that while these checkboxes control the display of the planet names in the table, the retrograde calculations remain independent of these selections.

- Real-Time Retrograde Status Table:

A table in the top-right corner displays each planet’s retrograde status in real time. “Yes” is shown in red for a planet in retrograde and “No” in green when it isn’t. This offers an at-a-glance view of the cosmic conditions influencing your charts.

- Astrological & Astronomical Insights:

Whether you’re into sidereal astrology or simply fascinated by celestial mechanics, this script lets you visualize those retrograde cycles. In astrology, retrograde periods are often seen as times for reflection and re-evaluation, while in astronomy they reflect the natural orbital motions seen from our perspective on Earth.

Enhance your trading setup by integrating cosmic cycles into your technical analysis. Happy trading and cosmic exploring!

Cycles

52-Week & 5-Year High/Low with DatesThis indicator is designed to help traders quickly identify key price levels and their historical context by displaying the 52-week high/low and 5-year high/low prices along with their respective dates. It provides a clear visual representation of these levels directly on the chart and in a dashboard table for easy reference.

Key Features

52-Week High/Low:

Displays the highest and lowest prices over the last 252 trading days (approximately 52 weeks).

Includes the exact date when these levels were reached.

5-Year High/Low:

Displays the highest and lowest prices over the last 1260 trading days (approximately 5 years).

Includes the exact date when these levels were reached.

Visual Labels:

High and low levels are marked on the chart with labels that include the price and date.

Dashboard Table:

A table in the top-right corner of the chart summarizes the 52-week and 5-year high/low prices and their dates for quick reference.

Customizable Date Format:

Dates are displayed in the YYYY-MM-DD format for clarity and consistency.

Trading ChecklistTrading Checklist Indicator - Your Trading Plan Companion

A clean and efficient visual checklist to maintain trading discipline and consistency. This indicator helps traders follow their trading plan systematically by providing an easy-to-use checklist of key confirmation points.

Features:

- Visual checklist with clear green/red status indicators

- Clean, non-intrusive interface

- Real-time status updates

- Easy toggle controls for each item

Key Checkpoints:

1. HTF Structure Analysis

2. Order Flow Confirmation

3. SD/OB/FVG (HTF POI) Identification

4. Liquidity Grab Verification

5. Reversal Alignment Check

Final Confirmations:

- Trade Validity Check

- POI & Stop Loss Safety

- Set and Forget Status

How to Use:

1. Add the indicator to your chart

2. Use the Settings panel to toggle each condition

3. Green dots indicate confirmed conditions

4. Red dots show pending confirmations

5. Verify all conditions before executing trades

Note: This indicator helps maintain trading discipline but should be used alongside proper technical and fundamental analysis.

Tags: #TradingChecklist #RiskManagement #TradingPlan #Trading #Technical #Strategy #Discipline

Volume HighlightBar colouring: this indicator is simple but effective, it repaints higher than normal candles a certain colour (by default gold/yellow) it helps to know what are valuable areas to trade around for longs and shorts.

Changing the volume multiplier manually helps you to screen volume relevant to the timeframe you are trading on.

For example, some charts 1min the best filter/setting would be 12-35 multiplier where others like btc 1-4 hourly, the filter/setting might be 8-12.

The key is having only the highest/most relevant 3-4 volume candles showing as they often represent supports and resistances.

Grouped EMAsThis indicator displays grouped EMAs across multiple timeframes (5m, 15m, 30m, and 60m) on a single chart. It allows traders to easily track key EMA levels across different timeframes for better trend analysis and decision-making.

Key Features:

Adjustable EMA Length: Change the EMA period once, and it updates across all timeframes simultaneously.

Multi-Timeframe Support: Displays 365 EMA High and Low for 5-minute, 15-minute, 30-minute, and 60-minute intervals.

Clear Color Coding: Each timeframe is color-coded for quick visual recognition.

How to Use:

Adjust the EMA length using the input option to set your preferred period.

Observe the EMAs across different timeframes to identify support, resistance, and trend directions.

Combine with other indicators or price action strategies for enhanced trading insights.

This tool is ideal for traders looking to simplify multi-timeframe analysis while maintaining flexibility with the EMA period.

Enjoy more informed trading and enhanced trend analysis with Grouped EMAs!

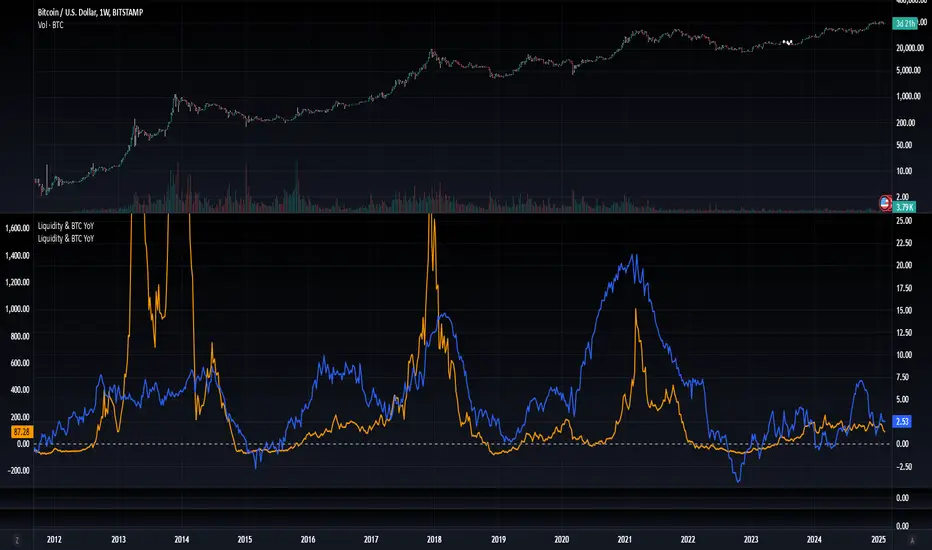

Blockchain Fundamentals: Liquidity & BTC YoYLiquidity & BTC YoY Indicator

Overview:

This indicator calculates the Year-over-Year (YoY) percentage change for two critical metrics: a custom Liquidity Index and Bitcoin's price. The Liquidity Index is derived from a blend of economic and forex data representing the M2 money supply, while the BTC price is obtained from a reliable market source. A dedicated limit(length) function is implemented to handle limited historical data, ensuring that the YoY calculations are available immediately—even when the chart's history is short.

Features Breakdown:

1. Limited Historical Data Workaround

- Functionality: limit(length) The function dynamically adjusts the lookback period when there isn’t enough historical data. This prevents delays in displaying YoY metrics at the beginning of the chart.

2. Liquidity Calculation

- Data Sources: Combines multiple data streams:

USM2, ECONOMICS:CNM2, USDCNY, ECONOMICS:JPM2, USDJPY, ECONOMICS:EUM2, USDEUR

- Formula:

Liquidity Index = USM2 + (CNM2 / USDCNY) + (JPM2 / USDJPY) + (EUM2 / USDEUR)

[b3. Bitcoin Price Calculation

- Data Source: Retrieves Bitcoin's price from BITSTAMP:BTCUSD on the user-selected timeframe for its historical length.

4. Year-over-Year (YoY) Percent Change Calculation

- Methodology:

- The indicator uses a custom function, to autodetect the proper number of bars, based on the selected timeframe.

- It then compares the current value to that from one year ago for both the Liquidity Index and BTC price, calculating the YoY percentage change.

5. Visual Presentation

- Plotting:

- The YoY percentage changes for Liquidity (plotted in blue) and BTC price (plotted in orange) are clearly displayed.

- A horizontal zero line is added for visual alignment, making it easier to compare the two copies of the metric. You add one copy and only display the BTC YoY. Then you add another copy and only display the M2 YoY.

-The zero lines are then used to align the scripts to each other by interposing them. You scale each chart the way you like, then move each copy individually to align both zero lines on top of each other.

This indicator is ideal for analysts and investors looking to monitor macroeconomic liquidity trends alongside Bitcoin's performance, providing immediate insights.

Previous Hour High and Low### **🔷 Previous Hour High & Low Indicator – Description**

#### 📌 **Overview**

The **Previous Hour High & Low Indicator** is designed to help traders identify key levels from the last completed hourly candle. These levels often act as **support and resistance zones**, helping traders make informed decisions about potential breakouts, reversals, and liquidity grabs.

#### 🎯 **How It Works**

- At the start of every new hour, the indicator **locks in** the **high and low** from the **previous fully completed hour**.

- It then **draws horizontal lines** on the chart, marking these levels.

- Works **only on intraday timeframes** (e.g., 1m, 5m, 15m, 30m), ensuring clean and relevant levels.

- Updates dynamically **every new hour** without repainting.

#### 🔑 **Why Is This Useful?**

✔ **Identifies Key Liquidity Zones** – The market often reacts to previous hour highs/lows, making them useful for stop hunts, liquidity grabs, and order block setups.

✔ **Works Well with ICT Concepts** – If you're trading **ICT kill zones**, these levels can help in finding optimal trade entries.

✔ **Helps with Breakout & Rejection Setups** – Traders can watch for price breaking or rejecting these levels for trade confirmation.

✔ **Useful for Scalping & Day Trading** – Works best for short-term traders looking for intraday movements.

#### ⚙ **Customization Options**

- The high and low levels are color-coded:

🔵 **Previous Hour High (Blue)** → Acts as potential resistance or breakout point.

🔴 **Previous Hour Low (Red)** → Acts as potential support or breakdown level.

#### 📊 **Best Timeframes to Use This On**

- **1-minute, 5-minute, 15-minute, 30-minute charts** → Most effective for intraday trading.

- Avoid using on **hourly or higher timeframes**, as these levels become less relevant.

---

🚀 **This indicator is perfect for traders looking to track short-term price reactions at key levels.** Let me know if you want to add alerts, zone shading, or any other enhancements! 🔥

Multi-Asset Ratio (20 vs 5) - LuchapThis indicator calculates and displays the ratio between the sum of the prices of several base assets and the sum of the prices of several quote assets. You can select up to 20 base assets and 5 quote assets, and enable or disable each asset individually to refine your analysis. This ratio allows you to quickly evaluate the relative performance of different groups of assets.

SNR Quarter Pointsfor btmm swingers

this is qp /quater point find in trading view

Here's a description for your TradingView Pine Script indicator:

---

**Support & Resistance (SNR) Lines Indicator**

This TradingView indicator automatically draws Support and Resistance (SNR) lines on the chart at every 250-pip level, starting from 0.0000. The indicator aims to help traders identify key price levels where the market is likely to experience reversal or consolidation. By plotting lines at regular intervals, the script provides a clear visual representation of potential support and resistance zones, aiding traders in making more informed trading decisions. The levels are dynamically adjusted based on market price movement, ensuring they stay relevant for active trading.

---

Let me know if you’d like to tweak it further!

Master Litecoin Dominance Network Value ModelUse this indicator on the LTC.D (Litecoin daily) chart to get a comprehensive view of Litecoin's network value relative to Bitcoin. It analyzes on-chain metrics and market data to help assess Litecoin's intrinsic worth and market trends.

Fibonacci Cycle Finder🟩 Fibonacci Cycle Finder is an indicator designed to explore Fibonacci-based waves and cycles through visualization and experimentation, introducing a trigonometric approach to market structure analysis. Unlike traditional Fibonacci tools that rely on static horizontal levels, this indicator incorporates the dynamic nature of market cycles, using adjustable wavelength, phase, and amplitude settings to visualize the rhythm of price movements. By applying a sine function, it provides a structured way to examine Fibonacci relationships in a non-linear context.

Fibonacci Cycle Finder unifies Fibonacci principles with a wave-based method by employing adjustable parameters to align each wave with real-time price action. By default, the wave begins with minimal curvature, preserving the structural familiarity of horizontal Fibonacci retracements. By adjusting the input parameters, the wave can subtly transition from a horizontal line to a more pronounced cycle,visualizing cyclical structures within price movement. This projective structure extends potential cyclical outlines on the chart, opening deeper exploration of how Fibonacci relationships may emerge over time.

Fibonacci Cycle Finder further underscores a non-linear representation of price by illustrating how wave-based logic can uncover shifts that are missed by static retracement tools. Rather than imposing immediate oscillatory behavior, the indicator encourages a progressive approach, where the parameters may be incrementally modified to align wave structures with observed price action. This refinement process deepens the exploration of Fibonacci relationships, offering a systematic way to experiment with non-linear price dynamics. In doing so, it revisits fundamental Fibonacci concepts, demonstrating their broader adaptability beyond fixed horizontal retracements.

🌀 THEORY & CONCEPT 🌀

What if Fibonacci relationships could be visualized as dynamic waves rather than confined to fixed horizontal levels? Fibonacci Cycle Finder introduces a trigonometric approach to market structure analysis, offering a different perspective on Fibonacci-based cycles. This tool provides a way to visualize market fluctuations through cyclical wave motion, opening the door to further exploration of Fibonacci’s role in non-linear price behavior.

Traditional Fibonacci tools, such as retracements and extensions, have long been used to identify potential support and resistance levels. While valuable for analyzing price trends, these tools assume linear price movement and rely on static horizontal levels. However, market fluctuations often exhibit cyclical tendencies , where price follows natural wave-like structures rather than strictly adhering to fixed retracement points. Although Fibonacci-based tools such as arcs, fans, and time zones attempt to address these patterns, they primarily apply geometric projections. The Fibonacci Cycle Finder takes a different approach by mapping Fibonacci ratios along structured wave cycles, aligning these relationships with the natural curvature of market movement rather than forcing them onto rigid price levels.

Rather than replacing traditional Fibonacci methods, the Fibonacci Cycle Finder supplements existing Fibonacci theory by introducing an exploratory approach to price structure analysis. It encourages traders to experiment with how Fibonacci ratios interact with cyclical price structures, offering an additional layer of insight beyond static retracements and extensions. This approach allows Fibonacci levels to be examined beyond their traditional static form, providing deeper insights into market fluctuations.

📊 FIBONACCI WAVE IMPLEMENTATION 📊

The Fibonacci Cycle Finder uses two user-defined swing points, A and B, as the foundation for projecting these Fibonacci waves. It first establishes standard horizontal levels that correspond to traditional Fibonacci retracements, ensuring a baseline reference before wave adjustments are applied. By default, the wave is intentionally subtle— Wavelength is set to 1 , Amplitude is set to 1 , and Phase is set to 0 . In other words, the wave starts as “stretched out.” This allows a slow, measured start, encouraging users to refine parameters incrementally rather than producing abrupt oscillations. As these parameters are increased, the wave takes on more distinct sine and cosine characteristics, offering a flexible approach to exploring Fibonacci-based cyclicity within price action.

Three parameters control the shape of the Fibonacci wave:

1️⃣ Wavelength Controls the horizontal spacing of the wave along the time axis, determining the length of one full cycle from peak to peak (or trough to trough). In this indicator, Wavelength acts as a scaling input that adjusts how far the wave extends across time, rather than a strict mathematical “wavelength.” Lower values further stretch the wave, increasing the spacing between oscillations, while higher values compress it into a more frequent cycle. Each full cycle is divided into four quarter-cycle segments, a deliberate design choice to minimize curvature by default. This allows for subtle oscillations and smoother transitions, preventing excessive distortion while maintaining flexibility in wave projections. The wavelength is calculated relative to the A-B swing, ensuring that its scale adapts dynamically to the selected price range.

2️⃣ Amplitude Defines the vertical displacement of the wave relative to the baseline Fibonacci level. Higher values increase the height of oscillations, while lower values reduce the height, Negative values will invert the wave’s initial direction. The amplitude is dynamically applied in relation to the A-B swing direction, ensuring that an upward swing results in upward oscillations and a downward swing results in downward oscillations.

3️⃣ Phase Shifts the wave’s starting position along its cycle, adjusting alignment relative to the swing points. A phase of 0 aligns with a sine wave, where the cycle starts at zero and rises. A phase of 25 aligns with a cosine wave, starting at a peak and descending. A phase of 50 inverts the sine wave, beginning at zero but falling first, while a phase of 75 aligns with an inverted cosine , starting at a trough and rising. Intermediate values between these phases create gradual shifts in wave positioning, allowing for finer alignment with observed market structures.

By fine-tuning these parameters, users can adapt Fibonacci waves to better reflect observed market behaviors. The wave structure integrates with price movements rather than simply overlaying static levels, allowing for a more dynamic representation of cyclical price tendencies. This indicator serves as an exploratory tool for understanding potential market rhythms, encouraging traders to test and visualize how Fibonacci principles extend beyond their traditional applications.

🖼️ CHART EXAMPLES 🖼️

Following this downtrend, price interacts with curved Fibonacci levels, highlighting resistance at the 0.236 and 0.382 levels, where price stalls before pulling back. Support emerges at the 0.5, 0.618, and 0.786 levels, where price finds stability and rebounds

In this Fibonacci retracement, price initially finds support at the 1.0 level, following the natural curvature of the cycle. Resistance forms at 0.786, leading to a pullback before price breaks through and tests 0.618 as resistance. Once 0.618 is breached, price moves upward to test 0.5, illustrating how Fibonacci-based cycles may align with evolving market structure beyond static, horizontal retracements.

Following this uptrend, price retraces downward and interacts with the Fibonacci levels, demonstrating both support and resistance at key levels such as 0.236, 0.382, 0.5, and 0.618.

With only the 0.5 and 1.0 levels enabled, this chart remains uncluttered while still highlighting key price interactions. The short cycle length results in a mild curvature, aligning smoothly with market movement. Price finds resistance at the 0.5 level while showing strong support at 1.0, which follows the natural flow of the market. Keeping the focus on fewer levels helps maintain clarity while still capturing how price reacts within the cycle.

🛠️ CONFIGURATION AND SETTINGS 🛠️

Wave Parameters

Wavelength : Stretches or compresses the wave along the time axis, determining the length of one full cycle. Higher values extend the wave across more bars, while lower values compress it into a shorter time frame.

Amplitude : Expands or contracts the wave along the price axis, determining the height of oscillations relative to Fibonacci levels. Higher values increase the vertical range, while negative values invert the wave’s initial direction.

Phase : Offsets the wave along the time axis, adjusting where the cycle begins. Higher values shift the starting position forward within the wave pattern.

Fibonacci Levels

Levels : Enable or disable specific Fibonacci levels (0.0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0) to focus on relevant price zones.

Color : Modify level colors for enhanced visual clarity.

Visibility

Trend Line/Color : Toggle and customize the trend line connecting swing points A and B.

Setup Lines : Show or hide lines linking Fibonacci levels to projected waves.

A/B Labels Visibility : Control the visibility of swing point labels.

Left/Right Labels : Manage the display of Fibonacci level labels on both sides of the chart.

Fill % : Adjust shading intensity between Fibonacci levels (0% = no fill, 100% = maximum fill).

A and B Points (Time/Price):

These user-defined anchor points serve as the basis for Fibonacci wave calculations and can be manually set. A and B points can also be adjusted directly on the chart, with automatic synchronization to the settings panel, allowing for seamless modifications without needing to manually input values.

⚠️ DISCLAIMER ⚠️

The Fibonacci Cycle Finder is a visual analysis tool designed to illustrate Fibonacci relationships and serve as a supplement to traditional Fibonacci tools. While the indicator employs mathematical and geometric principles, no guarantee is made that its calculations will align with other Fibonacci tools or proprietary methods. Like all technical and visual indicators, the Fibonacci levels generated by this tool may appear to visually align with key price zones in hindsight. However, these levels are not intended as standalone signals for trading decisions. This indicator is intended for educational and analytical purposes, complementing other tools and methods of market analysis.

🧠 BEYOND THE CODE 🧠

Fibonacci Cycle Finder is the latest indicator in the Fibonacci Geometry Series. Building on the concepts of the Fibonacci Time-Price Zones and the Fibonacci 3-D indicators, this tool introduces a trigonometric approach to market structure analysis.

The Fibonacci Cycle Finder indicator, like other xxattaxx indicators , is designed to encourage both education and community engagement. Your feedback and insights are invaluable to refining and enhancing the Fibonacci Cycle Finder indicator. We look forward to the creative applications, observations, and discussions this tool inspires within the trading community.

Volume Alert with Adaptive Trend - MissouriTimElevate your market analysis with our "Volume Alert with Adaptive Trend" indicator. This powerful tool combines real-time volume spike notifications with a sophisticated adaptive trend channel, providing traders with both immediate and long-term market insights. Customize your trading experience with adjustable volume alert thresholds and trend visualization options.

Features Summary

Volume Alert Features:

Volume Spike Detection:

Alerts you when volume exceeds a user-defined multiplier of the 20-period Simple Moving Average (SMA) of volume, helping identify potential market interest or significant price movements.

Visual Notification:

A "Volume Alert" label appears on the chart in a striking purple color (#7300E6) with white text, making high volume bars easily noticeable.

Customizable Sensitivity:

The volume spike threshold is adjustable, allowing you to set how sensitive the alert should be to volume changes, tailored to your trading strategy.

Alerts:

An alert condition is set to notify you when a volume spike occurs, ensuring you don't miss potential trading opportunities.

Adaptive Trend Features

Adaptive Channel:

Visualizes market trends through a dynamic channel that adjusts to price movements, offering insights into trend direction, strength, and potential reversal points.

Lookback Period:

Choose between short-term or long-term trend analysis with a toggle that adjusts the calculation period for the trend channel.

Channel Customization:

Fine-tune the trend channel with options for deviation multiplier, line styles, colors, transparency, and extension preferences to match your visual trading preferences.

Non-Repainting:

The trend lines are updated only on the current bar, ensuring the integrity of historical data for backtesting and strategy development.

Integrated Utility

Combination of Tools: This indicator marries the immediacy of volume alerts with the strategic depth of trend analysis, offering a comprehensive view of market dynamics.

User Customization: With inputs for both volume alerts and trend visualization, the indicator can be tailored to suit various trading styles, from scalping to swing trading.

This indicator ensures you're always in tune with market movements, providing crucial information at a glance to inform your trading decisions.

Timeframe Display + Countdown📘 Help Guide: Timeframe Display + Countdown + Alert

🔹 Overview

This indicator displays:

✅ The selected timeframe (e.g., 5min, 1H, 4H)

✅ A countdown timer showing minutes and seconds until the current candle closes

✅ An optional alert that plays a sound when 1 minute remains before the new candle starts

⚙️ How to Use

1️⃣ Add the Indicator

• Open TradingView

• Click on Pine Script Editor

• Copy and paste the script

• Click Add to Chart

2️⃣ Customize Settings

• Text Color: Choose a color for the displayed text

• Text Size: Adjust the font size (8–24)

• Transparency: Set how transparent the text is (0%–100%)

• Position: Choose where the text appears (Top Left, Top Right, Bottom Left, Bottom Right)

• Enable Audible Alert: Turn ON/OFF the alert when 1 minute remains

3️⃣ Set Up an Audible Alert in TradingView

🚨 Important: Pine Script cannot play sounds directly; you must set up a manual alert in TradingView.

Steps:

1. Click “Alerts” (🔔 icon in TradingView)

2. Click “Create Alert” (+ button)

3. In “Condition”, select this indicator (Timeframe Display + Countdown)

4. Under “Options”, choose:

• Trigger: “Once Per Bar”

• Expiration: Set a valid time range

• Alert Actions: Check “Play Sound” and choose a sound

5. Click “Create” ✅

🛠️ How It Works

• Countdown Timer:

• Updates in real time, displaying MM:SS until the candle closes

• Resets when a new candle starts

• Alert Trigger:

• When 1:00 minute remains, an alert is sent

• If properly configured in TradingView, it plays a sound

Highs&Lows by HourHighs & Lows by Hour

Description:

Highs & Lows by Hour is a TradingView indicator that helps traders identify the most frequent hours at which daily high and low price points occur. By analyzing historical price data directly from the TradingView chart, this tool provides valuable insights into market timing, allowing traders to optimize their strategies around key price movements.

This indicator is specifically designed for the one-hour (H1) timeframe . It does not display any data on other timeframes , as it relies on analyzing daily highs and lows within hourly periods.

This indicator processes the available data based on the number of historical bars loaded in the TradingView chart. The number of analyzed bars depends on the TradingView subscription plan , which determines how much historical data is accessible.

Key Features:

Works exclusively on the H1 timeframe , ensuring accurate analysis of daily highs and lows

Hourly highs and lows analysis to identify the most frequent hours when the market reaches its daily high and low

Sorted by frequency, displaying the most significant trading hours in descending order based on their recurrence

Customizable table and colors to fit the chart theme and trading style

Useful for scalpers, day traders, and swing traders to anticipate potential price reversals and breakouts

How It Works:

The indicator scans historical price data directly from the TradingView chart to detect the hour at which daily highs and daily lows occur.

It counts the frequency of highs and lows for each hour of the trading day based on the number of available bars in the TradingView chart.

The recorded data is displayed in a structured table, sorted by frequency from highest to lowest.

Users can customize colors to enhance readability and seamlessly integrate the indicator into their analysis.

Why Use This Indicator?

Identify key market patterns by recognizing the most critical hours when price extremes tend to form

Improve timing for trades by aligning entries and exits with high-probability time windows

Enhance market awareness by understanding when market volatility is likely to peak based on historical trends

Important Notes:

This indicator works only on the one-hour (H1) timeframe . It will not display any data on other timeframes

Works well on Forex, stocks, crypto, and futures , especially for intraday traders

The indicator analyzes only the historical bars available on the TradingView chart, which varies depending on the TradingView subscription plan (Free, Pro, Pro+, Premium)

This indicator does not generate buy or sell signals but serves as a data-driven tool for market analysis

How to Use:

Apply the Highs & Lows by Hour indicator to a one-hour (H1) chart on TradingView

Review the table displaying the most frequent hours for daily highs and lows

Adjust colors and settings for better visualization

Use the data to refine trading decisions and align strategy with historical price behavior

Killzone Highlights with Volume [odnac]

Description:

This indicator seamlessly integrates volume analysis with kill zone highlights across different market sessions.

The indicator dynamically displays trading volume and visually emphasizes key trading sessions in various time zones, including Asia, Europe, and New York (both AM and PM sessions).

Users have the flexibility to customize the colors of bullish and bearish volume bars, as well as the transparency and color of the kill zone highlights, allowing for tailored visual analysis of trading periods.

Features:

Bullish and Bearish Volume Colors:

Displays the volume of trades with user-defined colors for bullish (up) and bearish (down) candles.

Killzone Highlights:

Highlights the kill zones for Asia, Europe, New York AM, and New York PM sessions with user-defined colors and transparency.

Customization Options:

Allows users to adjust the colors, transparency, and time settings for each kill zone.

Weekend Handling:

Option to hide kill zone highlights during weekends.

Timeframe Limitation:

Users can set the maximum timeframe for which the kill zone highlights will be displayed.

Usage:

This indicator is designed for traders who want to gain insights into market activity during key trading sessions.

By combining volume data with visually distinct kill zone highlights, it helps traders make informed decisions based on the most active trading periods.

Ideal for intraday traders looking to leverage session-based strategies for more effective trading decisions.

Blockchain Fundamentals: Global LiquidityGlobal Liquidity Indicator Overview

This indicator provides a comprehensive technical analysis of liquidity trends by deriving a Global Liquidity metric from multiple data sources. It applies a suite of technical indicators directly on this liquidity measure, rather than on price data. When this metric is expanding Bitcoin and crypto tends to bullish conditions.

Features:

1. Global Liquidity Calculation

Data Integration: Combines multiple market data sources using a ratio-based formula to produce a unique liquidity measure.

Custom Metric: This liquidity metric serves as the foundational input for further technical analysis.

2. Timeframe Customization

User-Selected Period: Users can select the data timeframe (default is 2 months) to ensure consistency and flexibility in analysis.

3. Additional Technical Indicators

RSI, Momentum, ROC, MACD, and Stochastic:

Each indicator is computed using the Global Liquidity series rather than price.

User-selectable toggles allow for enabling or disabling each individual indicator as desired.

4. Enhanced MACD Visualization

Dynamic Histogram Coloring:

The MACD histogram color adjusts dynamically: brighter hues indicate rising histogram values while darker hues indicate falling values.

When the histogram is above zero, green is used; when below zero, red is applied, offering immediate visual insight into momentum shifts.

Conclusion

This indicator is an enlightening tool for understanding liquidity dynamics, aiding in macroeconomic analysis and investment decision-making by highlighting shifts in liquidity conditions and market momentum.

VWAP + KCVolume Weighted Average Price (VWAP) is a technical analysis tool used to measure the average price weighted by volume. VWAP is typically used with intraday charts as a way to determine the general direction of intraday prices. It's similar to a moving average in that when price is above VWAP, prices are rising and when price is below VWAP, prices are falling. VWAP is primarily used by technical analysts to identify market trend.

The Keltner Channels (KC) indicator is a banded indicator similar to Bollinger Bands and Moving Average Envelopes. They consist of an Upper Envelope above a Middle Line as well as a Lower Envelope below the Middle Line. The Middle Line is a moving average of price over a user-defined time period. Either a simple moving average or an exponential moving average are typically used. The Upper and Lower Envelopes are set a (user-defined multiple) of a range away from the Middle Line. This can be a multiple of the daily high/low range, or more commonly a multiple of the Average True Range.

ORB with 100 EMAORB Trading Strategy for FX Pairs on the 30-Minute Time Frame

Overview

This Opening Range Breakout (ORB) strategy is designed for trading FX pairs on the 30-minute time frame. The strategy is structured to take advantage of price momentum while aligning trades with the overall trend using the 100-period Exponential Moving Average (100EMA). The primary objective is to enter trades when price breaks and closes above or below the Opening Range (OR), with additional confirmation from a retest of the OR level if the initial entry is missed.

Strategy Rules

1. Defining the Opening Range (OR)

- The OR is determined by the high and low of the first 30-minute candle after market open.

- This range acts as the key level for breakout trading.

2. Trend Confirmation Using the 100EMA

- The 100EMA serves as a filter to determine trade direction:

- Buy Setup: Only take buy trades when the OR is above the 100EMA.

- Sell Setup: Only take sell trades when the OR is below the 100EMA.

3. Entry Criteria

- Buy Trade: Enter a long position when a candle breaks and closes above the OR high, confirming the breakout.

- Sell Trade: Enter a short position when a candle breaks and closes below the OR low, confirming the breakout.

- Retest Entry: If the initial entry is missed, wait for a price retest of the OR level for a secondary entry opportunity.

4. Risk-to-Reward Ratio (R2R)

- The goal is to target a 1:1 Risk-to-Reward (R2R) ratio.

- Stop-loss placement:

- Buy Trade: Place stop-loss just below the OR low.

- Sell Trade: Place stop-loss just above the OR high.

- Take profit at a distance equal to the stop-loss for a 1:1 R2R.

5. Risk Management

- Risk per trade should be based on personal risk tolerance.

- Adjust lot sizes accordingly to maintain a controlled risk percentage of account balance.

- Avoid over-leveraging, and consider moving stop-loss to breakeven if the price moves favourably.

Additional Considerations

- Avoid trading during major news events that may cause high volatility and unpredictable price movements.

- Monitor market conditions to ensure breakout confirmation with strong momentum rather than false breakouts.

- Use additional confluences such as candlestick patterns, support/resistance zones, or volume analysis for stronger trade validation.

This ORB strategy is designed to provide structured trade opportunities by combining breakout momentum with trend confirmation via the 100EMA. The strategy is straightforward, allowing traders to capitalise on clear breakout movements while implementing effective risk management practices. While the 1:1 R2R target provides a balanced approach, traders should always adapt their risk tolerance and market conditions to optimise trade performance.

By following these rules and maintaining discipline, traders can use this strategy effectively across various FX pairs on the 30-minute time frame.

Shifted Buy PressureDifferentiated Buy Pressure Indicator Documentation

Overview: The Differentiated Buy Pressure indicator is a custom Pine Script™ indicator designed to measure and visualize buy and sell pressure in the market. It calculates buy pressure based on a combination of volume, range, and gap, and provides a differentiated buy pressure which is shifted by 90°, offering predictive insights.

Inputs:

Window Size: The window size for average calculation (default: 20).

Show Overlay: Option to show the price overlay (default: false).

Overlay Boost Factor: Boosting factor for overlaying the price (default: 0.01).

Calculations:

Relative Range: Calculated as (high - low) / close.

Average Range: Simple moving average of the relative range over the specified window.

Average Volume: Simple moving average of the volume over the specified window.

Relative Gap: Calculated as open / close .

Average Gap: Simple moving average of the relative gap over the specified window.

Buy Pressure: Calculated using the formula: buy_pressure = -math.log(relative_range / avg_range * volume / avg_volume * relative_gap / avg_gap)

Differentiated Buy Pressure: Calculated as the difference between the current and previous buy pressure: diff_buy_pressure = buy_pressure - buy_pressure

Plots:

Zero Line: A horizontal line at zero for reference.

Buy Pressure: Plotted in blue, representing the calculated buy pressure.

Differentiated Buy Pressure: Plotted in red, representing the differentiated buy pressure.

Overlay: Optionally plots the price overlay boosted by the differentiated buy pressure.

Labels:

Labels are created to display the buy pressure and differentiated buy pressure values on the chart.

Usage: This indicator helps traders visualize the buy and sell pressure in the market. Positive values indicate buy pressure, while negative values indicate sell pressure. The differentiated buy pressure, shifted by 90°, provides predictive insights into future market movements.

This documentation provides a comprehensive overview of the Differentiated Buy Pressure indicator, explaining its purpose, inputs, calculations, and usage.

OmniPulse (Fixed Version)OmniPulse (Fixed Version) – Description

OmniPulse is a multi-indicator framework designed to combine three core oscillators—RSI, Stochastic, and Momentum—at various lookback lengths, then refine their signals using placeholder features such as machine learning forecasting, adaptive cycle detection, and neural network filtering. While some of these advanced features are not natively supported in Pine Script, they are represented here in simplified forms to illustrate how a more sophisticated system could be structured.

Key Components:

Multi-Length Oscillator Arrays

RSI (calcrsi() function)

Stochastic (placeholder via ta.sma() on a typical price average)

Momentum (ta.roc())

These are calculated for multiple lengths defined by the rsiLengths, stochLengths, and momentumLengths arrays.

Dual-Threshold Convergence

Compares each oscillator’s value to user-defined upper/lower thresholds (threshold1, threshold2) to identify bullish or bearish conditions.

Summarizes results in a convergence score.

Placeholder Machine Learning Forecast

Demonstrates a simple averaging of oscillator values as a “forecast” when toggled on.

Adaptive Cycle Detection (Placeholder)

Introduces a static cycle period (e.g., 20.0) as a placeholder for more advanced transforms.

Neural Network Filter (Placeholder)

Averages convergence, forecast, and cyclePeriod into a single filteredSignal.

Signal Plotting

Plots the filtered signal on the chart.

Highlights potential bullish or bearish extremes with shape markers based on percentile thresholds.

Practical Use & Extension:

Real Multi-Timeframe Analysis: Replace placeholders with request.security() for each timeframe.

Advanced Forecasting: Incorporate custom or external machine learning models.

Genuine Cycle Detection: Implement more sophisticated logic or user-defined cycle detection tools.

Neural Network Heuristics: Expand the placeholder step into a deeper filtering or weighting system.

Overall, OmniPulse serves as an adaptable blueprint for traders and developers, showcasing how multiple indicators and advanced concepts might be combined into a cohesive, signal-generating framework.

Month of Year Performance█ OVERVIEW

The Month of Year Performance indicator is designed to visualize and compare the cumulative percentage change for each month of the year. By aggregating monthly returns, it helps uncover seasonal trends and potential anomalies in financial markets.

In financial analysis, a calendar based anomaly refers to recurring patterns or tendencies associated with specific time periods, such as days of the week. By calculating the cumulative percentage change for each month (January through December) and displaying the results both graphically and in a summary table, this indicator helps identify whether certain months

consistently outperform others.

█ FEATURES

Customisable time window via Time Settings.

Calculates cumulative percentage change for each month (January to December) separately.

Built-in error check to ensure the indicator is applied on a Monthly timeframe.

Distinct visual representation for each month using unique colours.

Customisable table settings including location and font size.

Displays a performance summary table with metrics such as performance, average return, % positive, and count.

█ HOW TO USE

Add the indicator to a chart set to a Monthly timeframe.

Select your desired Start Time and End Time in the Time Settings.

Toggle the performance table on or off in the Table Settings.

Adjust the table’s location and font size as needed.

View the cumulative monthly performance plotted in distinct colours.

Colour Scheme:

January: Blue

February: Red

March: Green

April: Orange

May: Purple

June: Fuchsia

July: Teal

August: Yellow

September: Navy

October: Lime

November: Maroon

December: Aqua

Jerusalem Session Weekday MarkingJerusalem Session Weekday Marking

This indicator applies a background color to each trading day based on the Jerusalem time zone (Asia/Jerusalem). It's a simple, no-frills tool for traders operating in markets that follow a Sunday-Thursday business week.

How It Works:

Monday to Thursday → Red background (Regular trading days)

Friday to Sunday → Green background (Weekend/non-standard trading days)

Background coloring applies to the entire day (not just session hours).

Why Use This?

Designed for traders focusing on Middle Eastern, Israeli, and Forex markets.

Helps differentiate trading days at a glance in a market where Friday-Saturday weekends are standard.

Works automatically with Jerusalem timezone, no manual adjustments needed.

🚀 Simple, effective, and useful for traders who care about local trading schedules. 🚀

Day of Week Performance█ OVERVIEW

The Day of Week Performance indicator is designed to visualise and compare the cumulative percentage change for each day of the week. This indicator explores one of the many calendar based anomalies in financial markets.

In financial analysis, a calendar based anomaly refers to recurring patterns or tendencies associated with specific time periods, such as days of the week. By calculating the cumulative percentage change for each day (Monday through Friday) and displaying the results both graphically and in a summary table, this indicator helps identify whether certain days consistently outperform others.

█ FEATURES

Customisable time window via Time Settings.

Calculates cumulative percentage change for each day (Monday to Friday) separately.

Option to use Sunday instead of Friday for CFDs and Futures analysis.

Distinct visual representation for each day using unique colours.

Customisable table settings including position and font size.

Built-in error checks to ensure the indicator is applied on a Daily timeframe.

█ HOW TO USE

Add the indicator to a chart set to a Daily timeframe.

Select your desired Start Time and End Time in the Time Settings.

Toggle the performance table on or off in the Table Settings.

Adjust the table’s location and font size as needed.

Use the "Use Sunday instead of Friday" option if your market requires it.

View the cumulative performance plotted in distinct colours.

Colour Scheme:

Monday: Blue

Tuesday: Red

Wednesday: Green

Thursday: Orange

Friday: Purple