EMA Squeeze RythmHere's a description of this indicator and its purpose:

This indicator is based on the concept of price consolidation and volatility contraction using multiple Exponential Moving Averages (EMAs). It primarily looks for "squeeze" conditions where the EMAs converge, indicating potential market consolidation and subsequent breakout opportunities.

Key Features:

1. Uses 8 EMAs (20-55 period) to measure price compression

2. Measures the distance between fastest (20) and slowest (55) EMAs in ATR units

3. Identifies four distinct states:

- PRE-SQZE: Initial convergence of EMAs

- SQZE: Tighter convergence

- EXT-SQZE: Extreme convergence (highest probability of breakout)

- RELEASE: EMAs begin to expand (potential breakout in progress)

Best Used For:

- Identifying potential breakout setups

- Finding periods of low volatility before explosive moves

- Confirming trend strength using higher timeframe analysis

- Trading mean reversion strategies during squeeze states

- Catching momentum moves during release states

The indicator works well on any timeframe but is particularly effective on 15M to 4H charts for most liquid markets. It includes higher timeframe analysis to help confirm the broader market context.

Cycles

Asset Indexed by Future Interest

Este script em Pine Script calcula e exibe o índice de um ativo em relação à taxa de juros futuros (DI1) em um painel inferior. Ele obtém o preço de fechamento do ativo e a taxa de juros futuros DI1!, e em seguida, calcula o índice do ativo dividindo o preço do ativo pela taxa de juros futuros. Para evitar a divisão por zero, o script realiza uma validação para garantir que o valor da taxa de juros não seja nulo ou zero. O índice calculado é então plotado no painel inferior, em uma linha verde, permitindo que os usuários visualizem a relação entre o preço do ativo e os juros futuros de curto prazo. Esse índice pode ser útil para analisar como a taxa de juros influencia o comportamento do ativo.

This script in Pine Script calculates and displays the ratio of an asset to the future interest rate (DI1) in a lower panel. It obtains the asset's closing price and the future interest rate DI1!, and then calculates the asset index by dividing the asset price by the future interest rate. To avoid division by zero, the script performs validation to ensure that the interest rate value is not null or zero. The calculated index is then plotted in the bottom panel, in a green line, allowing users to visualize the relationship between the asset's price and short-term future interest. This index can be useful for analyzing how the interest rate influences the asset's behavior.

Adjust Asset for Future Interest (Brazil)Este script foi criado para ajustar o preço de um ativo com base na taxa de juros DI11!, que reflete a expectativa do mercado para os juros futuros. O objetivo é mostrar como o valor do ativo seria influenciado se fosse diretamente ajustado pela variação dessa taxa de juros.

Como funciona?

Preço do Ativo

O script começa capturando o preço de fechamento do ativo que está sendo visualizado no gráfico. Esse é o ponto de partida para o cálculo.

Taxa de Juros DI11!

Em seguida, ele busca os valores diários da taxa DI11! no mercado. Esta taxa é uma referência de juros de curto prazo, usada para ajustes financeiros e projeções econômicas.

Fator de Ajuste

Com a taxa de juros DI11!, o script calcula um fator de ajuste simples:

Fator de Ajuste

=

1

+

DI11

100

Fator de Ajuste=1+

100

DI11

Esse fator traduz a taxa percentual em um multiplicador aplicado ao preço do ativo.

Cálculo do Ativo Ajustado

Multiplica o preço do ativo pelo fator de ajuste para obter o valor ajustado do ativo. Este cálculo mostra como o preço seria se fosse diretamente influenciado pela variação da taxa DI11!.

Exibição no Gráfico

O script plota o preço ajustado do ativo como uma linha azul no gráfico, com maior espessura para facilitar a visualização. O resultado é uma curva que reflete o impacto teórico da taxa de juros DI11! sobre o ativo.

Utilidade

Este indicador é útil para entender como as taxas de juros podem influenciar ativos financeiros de forma hipotética. Ele é especialmente interessante para analistas que desejam avaliar a relação entre o mercado de renda variável e as condições de juros no curto prazo.

This script was created to adjust the price of an asset based on the DI11! interest rate, which reflects the market's expectation for future interest rates. The goal is to show how the asset's value would be influenced if it were directly adjusted by the variation of this interest rate.

How does it work?

Asset Price

The script starts by capturing the closing price of the asset that is being viewed on the chart. This is the starting point for the calculation.

DI11! Interest Rate

The script then searches for the daily values of the DI11! rate in the market. This rate is a short-term interest reference, used for financial adjustments and economic projections.

Adjustment Factor

With the DI11! interest rate, the script calculates a simple adjustment factor:

Adjustment Factor

=

1

+

DI11

100

Adjustment Factor=1+

100

DI11

This factor translates the percentage rate into a multiplier applied to the asset's price.

Adjusted Asset Calculation

Multiplies the asset price by the adjustment factor to obtain the adjusted asset value. This calculation shows how the price would be if it were directly influenced by the variation of the DI11! rate.

Display on the Chart

The script plots the adjusted asset price as a blue line on the chart, with greater thickness for easier visualization. The result is a curve that reflects the theoretical impact of the DI11! interest rate on the asset.

Usefulness

This indicator is useful for understanding how interest rates can hypothetically influence financial assets. It is especially interesting for analysts who want to assess the relationship between the equity market and short-term interest rate conditions.

PROWIN STUDY ALTCOIN INDEXPROWIN STUDY ALTCOIN INDEX

This indicator tracks the performance of key altcoin dominance indices (BTC.D, ETH.D, USDT.D, USDC.D, and DAI.D) by analyzing their closing prices. It calculates an Exponential Moving Average (EMA) to highlight the overall trend of the altcoin market. Key horizontal levels representing support (limit up), resistance (limit down), and a central line are drawn to help identify potential price action zones. This indicator is designed for analysis on the others.d asset in a daily timeframe, providing insights into market movements and altcoin dominance shifts.

Percent Movement HighlighterThe Percent Movement Highlighter is a custom TradingView indicator that visually highlights candles based on their percentage movement relative to the previous day's close. The indicator uses two user-defined thresholds:

Positive Threshold: Marks candles that move up by a specified percentage or more.

Negative Threshold: Marks candles that move down by a specified percentage or more.

Features:

Visual Highlights:

Green candles for upward moves exceeding the positive threshold.

Red candles for downward moves exceeding the negative threshold.

Dynamic Counters:

Displays a summary label that counts the number of positive, negative, and neutral candles dynamically as the chart progresses.

User Inputs:

Customizable positive and negative percentage thresholds to suit different trading strategies.

This tool is useful for traders seeking to identify significant price movements and analyze market volatility efficiently.

Pivot Highs/Lows with Bar CountsWhat does the indicator do?

This indicator adds labels to a chart at swing (a.k.a., "pivot") highs and lows. Each label may contain a date, the closing price at the swing, the number of bars since the last swing in the same direction, and the number of bars from the last swing in the opposite direction. A table is also added to the chart that shows the average, min, and max number of bars between swings.

OK, but how do I use it?

Many markets -- especially sideways-moving ones -- commonly cycle between swing highs and lows at regular time intervals. By measuring the number of bars between highs and lows -- both same-sided swings (i.e., H-H and L-L) and opposite-sided swings (i.e., H-L and L-H) -- you can then project the averages of those bar counts from the last high or low swing to make predictions about where the next swing high or low should occur. Note that this indicator does not make the projection for you. You have to determine which swing you want to project from and then use the bar counts from the indicator to draw a line, place a label, etc.

Example: Chart of BTC/USD

The indicator shows pivot highs and lows with bar counts, and it displays a table of stats on those pivots.

If you focus on the center section of the chart, you can see that prices were moving in a sideways channel with very regular highs and lows. This indicator counts the bars between these pivots, and you could have used those counts to predict when the next high or low may have occurred.

The bar counts do not work as well on the more recent section of the chart because there are no regularly time swings.

TASC 2025.01 Linear Predictive Filters█ OVERVIEW

This script implements a suite of tools for identifying and utilizing dominant cycles in time series data, as introduced by John Ehlers in the "Linear Predictive Filters And Instantaneous Frequency" article featured in the January 2025 edition of TASC's Traders' Tips . Dominant cycle information can help traders adapt their indicators and strategies to changing market conditions.

█ CONCEPTS

Conventional technical indicators and strategies often rely on static, unchanging parameters, which may fail to account for the dynamic nature of market data. In his article, John Ehlers applies digital signal processing principles to address this issue, introducing linear predictive filters to identify cyclic information for adapting indicators and strategies to evolving market conditions.

This approach treats market data as a complex series in the time domain. Analyzing the series in the frequency domain reveals information about its cyclic components. To reduce the impact of frequencies outside a range of interest and focus on a specific range of cycles, Ehlers applies second-order highpass and lowpass filters to the price data, which attenuate or remove wavelengths outside the desired range. This band-limited analysis isolates specific parts of the frequency spectrum for various trading styles, e.g., longer wavelengths for position trading or shorter wavelengths for swing trading.

After filtering the series to produce band-limited data, Ehlers applies a linear predictive filter to predict future values a few bars ahead. The filter, calculated based on the techniques proposed by Lloyd Griffiths, adaptively minimizes the error between the latest data point and prediction, successively adjusting its coefficients to align with the band-limited series. The filter's coefficients can then be applied to generate an adaptive estimate of the band-limited data's structure in the frequency domain and identify the dominant cycle.

█ USAGE

This script implements the following tools presented in the article:

Griffiths Predictor

This tool calculates a linear predictive filter to forecast future data points in band-limited price data. The crosses between the prediction and signal lines can provide potential trade signals.

Griffiths Spectrum

This tool calculates a partial frequency spectrum of the band-limited price data derived from the linear predictive filter's coefficients, displaying a color-coded representation of the frequency information in the pane. This mode's display represents the data as a periodogram . The bottom of each plotted bar corresponds to a specific analyzed period (inverse of frequency), and the bar's color represents the presence of that periodic cycle in the time series relative to the one with the highest presence (i.e., the dominant cycle). Warmer, brighter colors indicate a higher presence of the cycle in the series, whereas darker colors indicate a lower presence.

Griffiths Dominant Cycle

This tool compares the cyclic components within the partial spectrum and identifies the frequency with the highest power, i.e., the dominant cycle . Traders can use this dominant cycle information to tune other indicators and strategies, which may help promote better alignment with dynamic market conditions.

Notes on parameters

Bandpass boundaries:

In the article, Ehlers recommends an upper bound of 125 bars or higher to capture longer-term cycles for position trading. He recommends an upper bound of 40 bars and a lower bound of 18 bars for swing trading. If traders use smaller lower bounds, Ehlers advises a minimum of eight bars to minimize the potential effects of aliasing.

Data length:

The Griffiths predictor can use a relatively small data length, as autocorrelation diminishes rapidly with lag. However, for optimal spectrum and dominant cycle calculations, the length must match or exceed the upper bound of the bandpass filter. Ehlers recommends avoiding excessively long lengths to maintain responsiveness to shorter-term cycles.

Adjustable Entry Price Levels by Sobhi v6Adjustable Entry Price Levels", is designed to display customizable price levels on a chart, allowing traders to visualize key price zones relative to a chosen entry price. Here's a detailed breakdown of its functionality:

Purpose

The indicator helps traders create and manage equidistant price levels (both above and below a selected entry price). These levels can assist in planning trades, setting stop-loss and take-profit levels, or identifying key market zones for decision-making.

Features

Entry Price Input:

Users can specify a starting price (Entry Price) to base the levels on.

Adjustable Distance Between Levels:

Levels are spaced at a user-defined interval (Distance), creating equidistant horizontal lines.

Number of Levels:

Users can select how many levels to display above and below the entry price (Number of Levels).

Line Customization:

Style: Choose between Solid, Dotted, or Dashed lines.

Color: Customize the color for upward and downward levels (Line Color Up and Line Color Down).

Thickness: Adjust line thickness (Line Width).

Label Customization:

Visibility: Option to show or hide labels on each level (Show Labels).

Font Size: Set the size of the text for level labels (Label Font Size).

Colors: Separate customization for labels above (Label Color Up) and below (Label Color Down) the entry price.

Extended Line Display:

The lines extend backward (Extend Bars Back) and forward (Extend Bars Forward) to ensure visibility over a larger section of the chart.

Visualization

Upward Levels:

Represented by blue (default) horizontal lines above the entry price.

Labels display the price value of each level in the same color.

Downward Levels:

Represented by red (default) horizontal lines below the entry price.

Labels display the price value of each level in the same color.

Example Use Case

Scenario 1: Support and Resistance Planning

A trader can define a key level (Entry Price) and observe nearby support and resistance zones using the calculated price levels.

Scenario 2: Risk Management

The indicator helps in visualizing stop-loss and take-profit areas equidistant from the entry price.

Scenario 3: Breakout Targets

Traders can use the levels to anticipate potential breakout or breakdown targets.

Customization Options

This indicator is highly customizable, making it versatile for different trading strategies. Traders can tweak:

The visual appearance of the levels (style, color, width).

The number of levels and their spacing.

Whether labels are displayed and their style.

Volume-MACD-RSI Integrated StrategyDescription:

This script integrates three well-known technical analysis tools—Volume, MACD, and RSI—into a single signal meant to help traders identify potential turning points under strong market conditions.

Concept Overview:

Volume Filter: We compare the current bar’s volume to a 20-period volume average and require it to exceed a specified multiplier. This ensures that signals occur only during periods of heightened market participation. The logic is that moves on low volume are less reliable, so we wait for increased activity to confirm potential trend changes.

MACD Momentum Shift:

We incorporate MACD crossovers to determine when momentum is changing direction. MACD is a popular momentum indicator that identifies shifts in trend by comparing short-term and long-term EMAs. A bullish crossover (MACD line crossing above the signal line) may suggest upward momentum is building, while a bearish crossunder can indicate momentum turning downward.

RSI Market Condition Check:

RSI helps us identify overbought or oversold conditions. By requiring that RSI be oversold on buy signals and overbought on sell signals, we attempt to pinpoint entries where price could be at an extreme. The idea is to position entries or exits at junctures where price may be due for a reversal.

How the Script Works Together:

Volume Confirmation: No signals fire unless there’s strong volume. This reduces false positives.

MACD Momentum Check: Once volume confirms market interest, MACD crossover events serve as a trigger to initiate consideration of a trade signal.

RSI Condition: Finally, RSI determines whether the market is at an extreme. This final layer helps ensure we only act on signals that have both momentum shift and a price at an extreme level, potentially increasing the reliability of signals.

Intended Use:

This script can help highlight potential reversal points or trend shifts during active market periods.

Traders can use these signals as a starting point for deeper analysis. For instance, a “BUY” arrow may prompt a trader to investigate the market context, confirm with other methods, or look for patterns that further support a long entry.

The script is best used on markets with reliable volume data, such as stocks or futures, and can be experimented with across different timeframes. Adjusting the RSI thresholds, MACD parameters, and volume multiplier can help tailor it to specific instruments or trading styles.

Chart Setup:

When adding this script to your chart, it should be the only indicator present, so you can clearly see the red “BUY” arrows and green “SELL” arrows at the candle closes where signals occur.

The chart should be kept clean and uncluttered for clarity. No other indicators are necessary since the logic is already integrated into this single script.

4-Year Cycles [jpkxyz]Overview of the Script

I wanted to write a script that encompasses the wide-spread macro fund manager investment thesis: "Crypto is simply and expression of macro." A thesis pioneered by the likes of Raoul Pal (EXPAAM) , Andreesen Horowitz (A16Z) , Joe McCann (ASYMETRIC) , Bob Loukas and many more.

Cycle Theory Background:

The 2007-2008 financial crisis transformed central bank monetary policy by introducing:

- Quantitative Easing (QE): Creating money to buy assets and inject liquidity

- Coordinated global monetary interventions

Proactive 4-year economic cycles characterised by:

- Expansionary periods (low rates, money creation)

- Followed by contraction/normalisation

Central banks now deliberately manipulate liquidity, interest rates, and asset prices to control economic cycles, using monetary policy as a precision tool rather than a blunt instrument.

Cycle Characteristics (based on historical cycles):

- A cycle has 4 seasons (Spring, Summer, Fall, Winter)

- Each season with a cycle lasts 365 days

- The Cycle Low happens towards the beginning of the Spring Season of each new cycle

- This is followed by a run up throughout the Spring and Summer Season

- The Cycle High happens towards the end of the Fall Season

- The Winter season is characterised by price corrections until establishing a new floor in the Spring of the next cycle

Key Functionalities

1. Cycle Tracking

- Divides market history into 4-year cycles (Spring, Summer, Fall, Winter)

- Starts tracking cycles from 2011 (first cycle after the 2007 crisis cycle)

- Identifies and marks cycle boundaries

2. Visualization

- Colors background based on current cycle season

- Draws lines connecting:

- Cycle highs and lows

- Inter-cycle price movements

- Adds labels showing:

- Percentage gains/losses between cycles

- Number of days between significant points

3. Customization Options

- Allows users to customize:

- Colors for each season

- Line and label colors

- Label size

- Background opacity

Detailed Mechanism

Cycle Identification

- Uses a modulo calculation to determine the current season in the 4-year cycle

- Preset boundary years include 2015, 2019, 2023, 2027

- Automatically tracks and marks cycle transitions

Price Analysis

- Tracks highest and lowest prices within each cycle

- Calculates percentage changes:

- Intra-cycle (low to high)

- Inter-cycle (previous high to current high/low)

Visualization Techniques

- Background color changes based on current cycle season

- Dashed and solid lines connect significant price points

- Labels provide quantitative insights about price movements

Unique Aspects

1. Predictive Cycle Framework: Provides a structured way to view market movements beyond traditional technical analysis

2. Seasonal Color Coding: Intuitive visual representation of market cycle stages

3. Comprehensive Price Tracking: Captures both intra-cycle and inter-cycle price dynamics

4. Highly Customizable: Users can adjust visual parameters to suit their preferences

Potential Use Cases

- Technical analysis for long-term investors

- Identifying market cycle patterns

- Understanding historical price movement rhythms

- Educational tool for market cycle theory

Limitations/Considerations

- Based on a predefined 4-year cycle model (Liquidity Cycles)

- Historic Cycle Structures are not an indication for future performance

- May not perfectly represent all market behavior

- Requires visual interpretation

This script is particularly interesting for investors who believe in cyclical market theories and want a visual, data-driven representation of market stages.

Weekly Covered Calls Strategy with IV & Delta LogicWhat Does the Indicator Do?

this is interactive you must use it with your options chain to input data based on the contract you want to trade.

Visualize three strike price levels for covered calls based on:

Aggressive (closest to price, riskier).

Moderate (mid-range, balanced).

Low Delta (farthest, safer).

Incorporate Implied Volatility (IV) from the options chain to make strike predictions more realistic and aligned with market sentiment. Adjust the risk tolerance by modifying Delta inputs and IV values. Risk is defined for example .30 delta means 30% chance of your shares being assigned. If you want to generate steady income with your shares you might want to lower the risk of them being assigned to .05 or 5% etc.

How to Use the Indicator with the Options Chain

Start with the Options Chain:

Look for the following data points from your options chain:

Implied Volatility (IV Mid): Average IV for a particular strike price.

Delta:

~0.30 Delta: Closest strike (Aggressive).

~0.15–0.20 Delta: Mid-range strike (Moderate).

~0.05–0.10 Delta: Far OTM, safer (Low Delta).

Strike Price: Identify strike prices for the desired Deltas.

Open Interest: Check liquidity; higher OI ensures tighter spreads.

Input IV into the Indicator:

Enter the IV Mid value (e.g., 0.70 for 70%) from the options chain into the Implied Volatility field of the indicator.

Adjust Delta Inputs Based on Risk Tolerance:

Aggressive Delta: Increase if you want strikes closer to the current price (riskier, higher premium).

Default: 0.2 (20% chance of shares being assigned).

Moderate Delta: Balanced risk/reward.

Default: 0.12 (12%)

Low Delta: Decrease for safer, farther OTM strikes.

Default: 0.05 (5%)

Visualize the Chart:

Once inputs are updated:

Red Line: Aggressive Strike (closest, riskiest, higher premium).

Blue Line: Moderate Strike (mid-range).

Green Line: Low Delta Strike (farthest, safer).

Step-by-Step Workflow Example

Open the options chain and note:

Implied Volatility (IV Mid): Example 71.5% → input as 0.715.

Delta for desired strikes:

Aggressive: 0.30 Delta → Closest strike ~ $455.

Moderate: 0.15 Delta → Mid-range strike ~ $470.

Low Delta: 0.05 Delta → Farther strike ~ $505.

Open the indicator and adjust:

IV Mid: Enter 0.715.

Aggressive Delta: Leave at 0.12 (or adjust to bring strikes closer).

Moderate Delta: Leave at 0.18.

Low Delta: Adjust to 0.25 for safer, farther strikes.

View the chart:

Compare the indicator's strikes (red, blue, green) with actual options chain strikes.

Use the visualization to: Validate the risk/reward for each strike.

Align strikes with technical trends, support/resistance.

Adjusting Inputs Based on Risk Tolerance

Higher Risk: Increase Aggressive Delta (e.g., 0.15) for closer strikes.

Use higher IV values for volatile stocks.

Moderate Risk: Use default values (0.12–0.18 Delta).

Balance premiums and probability.

Lower Risk: Increase Low Delta (e.g., 0.30) for farther, safer strikes.

Focus on higher IV stocks with good open interest.

Key Benefits

Simplifies Strike Selection: Visualizes the three risk levels directly on the chart.

Aligns with Market Sentiment: Incorporates IV for realistic forecasts.

Customizable for Risk: Adjust inputs to match personal risk tolerance.

By combining the options chain (IV, Delta, and liquidity) with the technical chart, you get a powerful, visually intuitive tool for covered call strategies.

Momentum Matrix (BTC-COIN)The Momentum Matrix (BTC-COIN) indicator analyzes the momentum relationship between Coinbase stock ( NASDAQ:COIN ) and Bitcoin ( CRYPTOCAP:BTC ). By combining RSI, correlation, and dominance metrics, it identifies bullish and bearish macro trends to align trades with market momentum.

How It Works

Price Inputs: Pulls weekly price data for CRYPTOCAP:BTC and NASDAQ:COIN for macro analysis.

Metrics Calculated:

• RSI Divergence: Measures momentum differences between CRYPTOCAP:BTC and $COIN.

• Price Ratio: Tracks the $COIN/ CRYPTOCAP:BTC relationship relative to its long-term average (SMA).

• Correlation: Analyzes price co-movement between CRYPTOCAP:BTC and $COIN.

• Dominance Impact: Incorporates CRYPTOCAP:BTC dominance for broader crypto trends.

Composite Momentum Score: Combines these metrics into a smoothed macro momentum value.

Thresholds for Trend Detection: Upper and lower thresholds dynamically adapt to market conditions.

Signals and Visualization:

• Buy Signal: Momentum exceeds the upper threshold, indicating bullish trends.

• Sell Signal: Momentum falls below the lower threshold, indicating bearish trends.

• Background Colors: Green (bullish), Red (bearish).

Strengths

Integrates multiple metrics for robust macro analysis.

Dynamic thresholds adapt to market conditions.

Effective for identifying macro momentum shifts.

Limitations

Lag in high volatility due to smoothing.

Less effective in choppy, sideways markets.

Assumes CRYPTOCAP:BTC dominance drives NASDAQ:COIN momentum, which may not always hold true.

Improvements

Multi-Timeframe Analysis: Add daily or monthly data for precision.

Volume Filters: Include volume thresholds for signal validation.

Additional Metrics: Consider MACD or Stochastics for further confirmation.

Complementary Tools

Volume Indicators: OBV or cumulative delta for confirmation.

Trend-Following Systems: Pair with moving averages for timing.

Market Breadth Metrics: Combine with CRYPTOCAP:BTC dominance trends for context.

Weekly Covered Calls StrategyWhat Does This Indicator Do?

This indicator is a tool to help you pick strike prices for your weekly covered call options strategy. It does two things:

Plots two suggested strike prices on your chart:

Aggressive Strike (red label): A strike price closer to the current price, offering higher premiums but with a higher chance of assignment.

Moderate Strike (blue label): A strike price further from the current price, offering lower premiums but with a lower chance of assignment.

Uses technical analysis (volatility) to calculate these strike prices dynamically. It adjusts them based on the market's volatility and your chosen risk settings.

How It Works:

The indicator uses the following inputs to determine the strike prices:

ATR (Average True Range):

This measures the stock's volatility (how much the stock moves up or down over a given period).

A higher ATR = more volatile stock = wider range for strike prices.

Delta Adjustments:

The default settings use Delta values of 0.12 (Aggressive) and 0.18 (Moderate).

Delta is a concept in options trading that estimates the likelihood of the option being "in the money" (ITM) by expiration.

A 0.12 Delta = 12% chance of assignment (Aggressive)

A 0.18 Delta = 18% chance of assignment (Moderate)

Volatility Factor:

This multiplies the ATR by a factor (default is 1.5) to estimate the expected price move and adjust strike prices accordingly.

How to Use the Indicator:

Step 1: Understand the Labels

Red Label (Aggressive Strike):

Closer to the current stock price.

You’ll collect higher premiums because the strike price is riskier (closer to being ITM).

Best for traders comfortable with a higher risk of assignment.

Blue Label (Moderate Strike):

Further from the current stock price.

You’ll collect lower premiums because the strike price is safer (further from being ITM).

Best for traders looking to avoid assignment and collect safer weekly income.

Step 2: Match It to the Options Chain

Open your options chain (like the one you see in Fidelity, TOS, or TradingView).

Look for the strike prices closest to the red (aggressive) and blue (moderate) labels plotted by the indicator.

Compare the premiums (the amount you collect for selling the call) and decide:

If you want higher income: Go with the Aggressive Strike.

If you want safety: Go with the Moderate Strike.

Step 3: Manage Your Risk and Income

Avoid Assignment:

If you do not want your shares to be called away, choose strike prices further from the current price (e.g., moderate strike).

Maximize Premiums:

If you’re okay with a chance of your shares being called away, choose the closer aggressive strike for higher premium income.

Weekly Income Goal:

Use this strategy consistently each week to collect premium income while holding your shares.

Step 4: Adjust for Your Risk Tolerance

You can adjust the Delta values (0.12 for Aggressive and 0.18 for Moderate) to suit your risk tolerance:

Lower Delta (e.g., 0.08–0.10): Safer, fewer chances of assignment, lower premiums.

Higher Delta (e.g., 0.20–0.25): Riskier, higher chances of assignment, higher premiums.

Technical Analysis Summary (What the Indicator Uses):

The indicator uses ATR (Average True Range) to measure volatility and estimate how far the price might move.

It then multiplies ATR by a Volatility Factor to calculate the strike prices.

Using the Delta Adjustment settings, it adjusts these strike prices to give you a balance between risk and reward.

Putting It All Together:

Look at the Chart: The indicator will show two lines and labels for strike prices.

Check the Options Chain: Find the closest strike prices and compare premiums.

Decide Your Strategy:

Want higher premium income? Choose the Aggressive Strike (red label).

Want lower risk of assignment? Choose the Moderate Strike (blue label).

Collect Weekly Income: Sell the call option and repeat this process weekly to generate consistent income.

Happy trading, and may your premiums roll in while your shares stay safe! 🎯📊

20/50 SMA Cross 200 SMAThis Pine Script code is designed to identify and visualize crossovers of two shorter-term Simple Moving Averages (SMAs), a 20-period SMA and a 50-period SMA, with a longer-term 200-period SMA on a price chart. It also includes alerts for these crossover events. Here's a breakdown:

**Purpose:**

The core idea behind this script is to detect potential trend changes. Crossovers of shorter-term moving averages over a longer-term moving average are often interpreted as bullish signals, while crossovers below are considered bearish.

**Key Components:**

1. **Moving Average Calculation:**

* `sma20 = ta.sma(close, 20)`: Calculates the 20-period SMA of the closing price.

* `sma50 = ta.sma(close, 50)`: Calculates the 50-period SMA of the closing price.

* `sma200 = ta.sma(close, 200)`: Calculates the 200-period SMA of the closing price.

2. **Crossover Detection:**

* `crossUp20 = ta.crossover(sma20, sma200)`: Returns `true` when the 20-period SMA crosses above the 200-period SMA.

* `crossDown20 = ta.crossunder(sma20, sma200)`: Returns `true` when the 20-period SMA crosses below the 200-period SMA.

* Similar logic applies for `crossUp50` and `crossDown50` with the 50-period SMA.

3. **Recent Crossover Tracking (Crucial Improvement):**

* `lookback = 7`: Defines a lookback period of 7 bars.

* `var bool hasCrossedUp20 = false`, etc.: Declares `var` (persistent) boolean variables to track if a crossover has occurred *within* the last 7 bars. This is the most important correction from previous versions.

* The logic using `ta.barssince()` is the key:

* If a crossover happens (`crossUp20` is true), the corresponding `hasCrossedUp20` is set to `true`.

* If no crossover happens on the current bar, it checks if a crossover happened within the last 7 bars using `ta.barssince(crossUp20) <= lookback`. If so, it keeps `hasCrossedUp20` as `true`. After 7 bars, it becomes `false`.

4. **Plotting Crossovers:**

* `plotshape(...)`: Plots circles on the chart to visually mark the crossovers.

* Green circles below the bars for bullish crossovers (20 and 50).

* Red circles above the bars for bearish crossovers (20 and 50).

* Different shades of green/red (green/lime, red/maroon) distinguish between 20 and 50 SMA crossovers.

5. **Plotting Moving Averages (Optional but Helpful):**

* `plot(sma20, color=color.blue, linewidth=1)`: Plots the 20-period SMA in blue.

* Similar logic for the 50-period SMA (orange) and 200-period SMA (gray).

6. **Alerts:**

* `alertcondition(...)`: Triggers alerts when crossovers occur. This is essential for real-time trading signals.

**How it Works (in Simple Terms):**

The script continuously calculates the 20, 50, and 200 SMAs. It then monitors for instances where the 20 or 50 SMA crosses the 200 SMA. When such a crossover happens, a colored circle is plotted on the chart, and an alert is triggered. The key improvement is that it remembers if a crossover occurred in the last 7 bars and continues to display the circle during that period.

**Use Case:**

Traders use this type of indicator to identify potential entry and exit points in the market. A bullish crossover (shorter SMA crossing above the longer SMA) might be a signal to buy, while a bearish crossover might be a signal to sell.

**Key Improvements over Previous Versions:**

* **Correct Lookback Implementation:** The use of `ta.barssince()` and `var` variables is the correct and efficient way to check for crossovers within a lookback period. This fixes the major flaw in earlier versions.

* **Clear Visualizations:** The use of `plotshape` with distinct colors makes it easy to distinguish between 20 and 50 SMA crossovers.

* **Alerts:** The inclusion of alerts makes the script much more practical for real-time trading.

This improved version provides a robust and useful tool for identifying and tracking SMA crossovers.

Weighted Fourier Transform: Spectral Gating & Main Frequency🙏🏻 This drop has 2 purposes:

1) to inform every1 who'd ever see it that Weighted Fourier Tranform does exist, while being available nowhere online, not even in papers, yet there's nothing incredibly complicated about it, and it can/should be used in certain cases;

2) to show TradingView users how they can use it now in dem endevours, to show em what spectral filtering is, and what can they do with all of it in diy mode.

... so we gonna have 2 sections in the description

Section 1: Weighted Fourier Transform

It's quite easy to include weights in Fourier analysis: you just premultiply each datapoint by its corresponding weight -> feed to direct Fourier Transform, and then divide by weights after inverse Fourier transform. Alternatevely, in direct transform you just multiply contributions of each data point to the real and imaginary parts of the Fourier transform by corresponding weights (in accumulation phase), and in inverse transform you divide by weights instead during the accumulation phase. Everything else stays the same just like in non-weighted version.

If you're from the first target group let's say, you prolly know a thing or deux about how to code & about Fourier Transform, so you can just check lines of code to see the implementation of Weighted Discrete version of Fourier Transform, and port it to to any technology you desire. Pine Script is a developing technology that is incredibly comfortable in use for quant-related tasks and anything involving time series in general. While also using Python for research and C++ for development, every time I can do what I want in Pine Script, I reach for it and never touch matlab, python, R, or anything else.

Weighted version allows you to explicetly include order/time information into the operation, which is essential with every time series, although not widely used in mainstream just as many other obvious and right things. If you think deeply, you'll understand that you can apply a usual non-weighted Fourier to any 2d+ data you can (even if none of these dimensions represent time), because this is a geometric tool in essence. By applying linearly decaying weights inside Fourier transform, you're explicetly saying, "one of these dimensions is Time, and weights represent the order". And obviously you can combine multiple weightings, eg time and another characteristic of each datum, allows you to include another non-spatial dimension in your model.

By doing that, on properly processed (not only stationary but Also centered around zero data), you can get some interesting results that you won't be able to recreate without weights:

^^ A sine wave, centered around zero, period of 16. Gray line made by: DWFT (direct weighted Fourier transform) -> spectral gating -> IWFT (inverse weighted Fourier transform) -> plotting the last value of gated reconstructed data, all applied to expanding window. Look how precisely it follows the original data (the sine wave) with no lag at all. This can't be done by using non-weighted version of Fourier transform.

^^ spectral filtering applied to the whole dataset, calculated on the latest data update

And you should never forget about Fast Fourier Transform, tho it needs recursion...

Section 2: About use cases for quant trading, about this particular implementaion in Pine Script 6 (currently the latest version as of Friday 13, December 2k24).

Given the current state of things, we have certain limits on matrix size on TradingView (and we need big dope matrixes to calculate polynomial regression -> detrend & center our data before Fourier), and recursion is not yet available in Pine Script, so the script works on short datasets only, and requires some time.

A note on detrending. For quality results, Fourier Transform should be applied to not only stationary but also centered around zero data. The rightest way to do detrending of time series

is to fit Cumulative Weighted Moving Polynomial Regression (known as WLSMA in some narrow circles xD) and calculate the deltas between datapoint at time t and this wonderful fit at time t. That's exactly what you see on the main chart of script description: notice the distances between chart and WLSMA, now look lower and see how it matches the distances between zero and purple line in WFT study. Using residuals of one regression fit of the whole dataset makes less sense in time series context, we break some 'time' and order rules in a way, tho not many understand/cares abouit it in mainstream quant industry.

Two ways of using the script:

Spectral Gating aka Spectral filtering. Frequency domain filtering is quite responsive and for a greater computational cost does not introduce a lag the way it works with time-domain filtering. Works this way: direct Fourier transform your data to get frequency & phase info -> compute power spectrum out of it -> zero out all dem freqs that ain't hit your threshold -> inverse Fourier tranform what's left -> repeat at each datapoint plotting the very first value of reconstructed array*. With this you can watch for zero crossings to make appropriate trading decisions.

^^ plot Freq pass to use the script this way, use Level setting to control the intensity of gating. These 3 only available values: -1, 0 and 1, are the general & natural ones.

* if you turn on labels in script's style settings, you see the gray dots perfectly fitting your data. They get recalculated (for the whole dataset) at each update. You call it repainting, this is for analytical & aesthetic purposes. Included for demonstration only.

Finding main/dominant frequency & period. You can use it to set up Length for your other studies, and for analytical purposes simply to understand the periodicity of your data.

^^ plot main frequency/main period to use the script this way. On the screenshot, you can see the script applied to sine wave of period 16, notice how many datapoints it took the algo to figure out the signal's period quite good in expanding window mode

Now what's the next step? You can try applying signal windowing techniques to make it all less data-driven but your ego-driven, make a weighted periodogram or autocorrelogram (check Wiener-Khinchin Theorem ), and maybe whole shiny spectrogram?

... you decide, choice is yours,

The butterfly reflect the doors ...

∞

LRI Momentum Cycles [AlgoAlpha]Discover the LRI Momentum Cycles indicator by AlgoAlpha, a cutting-edge tool designed to identify market momentum shifts using trend normalization and linear regression analysis. This advanced indicator helps traders detect bullish and bearish cycles with enhanced accuracy, making it ideal for swing traders and intraday enthusiasts alike.

Key Features :

🎨 Customizable Appearance : Set personalized colors for bullish and bearish trends to match your charting style.

🔧 Dynamic Trend Analysis : Tracks market momentum using a unique trend normalization algorithm.

📊 Linear Regression Insight : Calculates real-time trend direction using linear regression for better precision.

🔔 Alert Notifications : Receive alerts when the market switches from bearish to bullish or vice versa.

How to Use :

🛠 Add the Indicator : Favorite and apply the indicator to your TradingView chart. Adjust the lookback period, linear regression source, and regression length to fit your strategy.

📊 Market Analysis : Watch for color changes on the trend line. Green signals bullish momentum, while red indicates bearish cycles. Use these shifts to time entries and exits.

🔔 Set Alerts : Enable notifications for momentum shifts, ensuring you never miss critical market moves.

How It Works :

The LRI Momentum Cycles indicator calculates trend direction by applying linear regression on a user-defined price source over a specified period. It compares historical trend values, detecting bullish or bearish momentum through a dynamic scoring system. This score is normalized to ensure consistent readings, regardless of market conditions. The indicator visually represents trends using gradient-colored plots and fills to highlight changes in momentum. Alerts trigger when the momentum state changes, providing actionable trading signals.

Drawdown from All-Time High (Line)This Pine Script is a **Drawdown Indicator from All-Time High** for TradingView. It calculates and plots the percentage drawdown from the highest price the asset has ever reached (the all-time high). Here's a breakdown of what this script does:

### Description:

- **Drawdown Calculation**:

- The drawdown is calculated as the difference between the current price (`close`) and the all-time high, divided by the all-time high, and multiplied by 100 to express it as a percentage.

- If the current price is higher than the previous all-time high, the all-time high is updated to the current price.

- **All-Time High Tracking**:

- The script tracks the highest price (`allTimeHigh`) that the asset has ever reached. Each time a new high is reached, the `allTimeHigh` value is updated.

- **Line Plot**:

- The drawdown percentage is then plotted as a line on the chart, with a color of **blue** for easy visualization.

- The line shows how much the price has dropped relative to its all-time high.

- **Zero Line**:

- A horizontal line is added at the **0%** level to act as a reference point, which is helpful to identify when the asset has fully recovered to its all-time high.

### Key Features:

- **Track Drawdown**: The indicator helps visualize how far the current price has fallen from its highest point, which is useful for understanding the depth of losses (drawdowns) during a period.

- **Update All-Time High**: The indicator automatically updates the all-time high whenever a new high is detected.

- **Visual Reference**: The 0% horizontal line provides a clear indication of when the asset is at its all-time high, and the drawdown is at 0%.

### How it Works:

- If the current price surpasses the all-time high, the script will reset the all-time high to the new price.

- The drawdown percentage is calculated from the current price relative to this all-time high, and it is displayed as a line on the chart.

### Visuals:

- **Drawdown Line**: Plots the percentage of the drawdown, which is the drop from the all-time high.

- **Zero Line**: A dotted horizontal line at 0% marks the level of the all-time high.

This indicator is valuable for understanding the extent of price corrections and potential recoveries relative to the historical peak of the asset. It is especially useful for traders and investors who want to assess the risk of drawdowns in relation to the highest price achieved by the asset.

Log Regression OscillatorThe Log Regression Oscillator transforms the logarithmic regression curves into an easy-to-interpret oscillator that displays potential cycle tops/bottoms.

🔶 USAGE

Calculating the logarithmic regression of long-term swings can help show future tops/bottoms. The relationship between previous swing points is calculated and projected further. The calculated levels are directly associated with swing points, which means every swing point will change the calculation. Importantly, all levels will be updated through all bars when a new swing is detected.

The "Log Regression Oscillator" transforms the calculated levels, where the top level is regarded as 100 and the bottom level as 0. The price values are displayed in between and calculated as a ratio between the top and bottom, resulting in a clear view of where the price is situated.

The main picture contains the Logarithmic Regression Alternative on the chart to compare with this published script.

Included are the levels 30 and 70. In the example of Bitcoin, previous cycles showed a similar pattern: the bullish parabolic was halfway when the oscillator passed the 30-level, and the top was very near when passing the 70-level.

🔹 Proactive

A "Proactive" option is included, which ensures immediate calculations of tentative unconfirmed swings.

Instead of waiting 300 bars for confirmation, the "Proactive" mode will display a gray-white dot (not confirmed swing) and add the unconfirmed Swing value to the calculation.

The above example shows that the "Calculated Values" of the potential future top and bottom are adjusted, including the provisional swing.

When the swing is confirmed, the calculations are again adjusted, showing a red dot (confirmed top swing) or a green dot (confirmed bottom swing).

🔹 Dashboard

When less than two swings are available (top/bottom), this will be shown in the dashboard.

The user can lower the "Threshold" value or switch to a lower timeframe.

🔹 Notes

Logarithmic regression is typically used to model situations where growth or decay accelerates rapidly at first and then slows over time, meaning some symbols/tickers will fit better than others.

Since the logarithmic regression depends on swing values, each new value will change the calculation. A well-fitted model could not fit anymore in the future.

Users have to check the validity of swings; for example, if the direction of swings is downwards, then the dataset is not fitted for logarithmic regression.

In the example above, the "Threshold" is lowered. However, the calculated levels are unreliable due to the swings, which do not fit the model well.

Here, the combination of downward bottom swings and price accelerates slower at first and faster recently, resulting in a non-fit for the logarithmic regression model.

Note the price value (white line) is bound to a limit of 150 (upwards) and -150 (down)

In short, logarithmic regression is best used when there are enough tops/bottoms, and all tops are around 100, and all bottoms around 0.

Also, note that this indicator has been developed for a daily (or higher) timeframe chart.

🔶 DETAILS

In mathematics, the dot product or scalar product is an algebraic operation that takes two equal-length sequences of numbers (arrays) and returns a single number, the sum of the products of the corresponding entries of the two sequences of numbers.

The usual way is to loop through both arrays and sum the products.

In this case, the two arrays are transformed into a matrix, wherein in one matrix, a single column is filled with the first array values, and in the second matrix, a single row is filled with the second array values.

After this, the function matrix.mult() returns a new matrix resulting from the product between the matrices m1 and m2.

Then, the matrix.eigenvalues() function transforms this matrix into an array, where the array.sum() function finally returns the sum of the array's elements, which is the dot product.

dot(x, y)=>

if x.size() > 1 and y.size() > 1

m1 = matrix.new()

m2 = matrix.new()

m1.add_col(m1.columns(), y)

m2.add_row(m2.rows (), x)

m1.mult (m2)

.eigenvalues()

.sum()

🔶 SETTINGS

Threshold: Period used for the swing detection, with higher values returning longer-term Swing Levels.

Proactive: Tentative Swings are included with this setting enabled.

Style: Color Settings

Dashboard: Toggle, "Location" and "Text Size"

ATT + Key Levels with SessionsKey Features:

ATT Turning Point Numbers:

This input allows the user to define specific numbers (e.g., "3,11,17,29,41,47,53,59") that mark turning points in price action, which are checked using the bar_index modulo 60. If the current bar index matches one of these turning points, it triggers potential buy or sell signals.

RSI (Relative Strength Index):

The RSI is calculated based on a user-defined period (rsi_period), typically 14, and used to indicate overbought or oversold conditions. The script defines overbought (70) and oversold (30) levels, which are used to filter buy or sell signals.

Session Times:

The script includes predefined session times for major trading markets:

New York: From 9:30 AM EST to 4:00 PM EST.

London: From 8:00 AM GMT to 4:30 PM GMT.

Asia: From 12:00 AM GMT to 9:00 AM GMT.

These session times are used to restrict the buy and sell signals to specific market sessions.

Key Levels:

The script calculates and plots key market levels for the current day and week:

Daily High and Low: The highest and lowest prices of the current day.

Weekly High and Low: The highest and lowest prices of the current week.

These levels are plotted with different colors for visual reference.

Signal Logic:

Buy Signal: Triggered when the current bar is a turning point (according to the ATT model), the RSI is below the oversold threshold, and the current time is within the active session times (New York, London, or Asia).

Sell Signal: Triggered when the current bar is a turning point, the RSI is above the overbought threshold, and the current time is within the active session times.

Signal Limitations:

A user-defined limit (max_signals_per_session) controls the maximum number of signals that can be plotted within each session. This prevents excessive signal generation.

Plotting and Background Highlights:

Buy and Sell Signals: The script plots shapes (labels) above or below the bars to indicate buy or sell signals when the conditions are met.

Background Highlight: The background color is highlighted in yellow when the current bar matches one of the defined ATT turning points.

In Summary:

The indicator combines multiple technical factors to generate trading signals:

Turning points in price action (based on custom ATT numbers),

RSI levels (overbought/oversold),

Market session times (New York, London, Asia),

Key price levels (daily and weekly highs and lows).

This combination helps traders identify potential buying and selling opportunities while considering broader market dynamics and limiting the number of signals during each session.

AuriumFlowAURIUM (GOLD-Weighted Average with Fractal Dynamics)

Aurium is a cutting-edge indicator that blends volume-weighted moving averages (VWMA), fractal geometry, and Fibonacci-inspired calculations to deliver a precise and holistic view of market trends. By dynamically adjusting to price and volume, Aurium uncovers key levels of confluence for trend reversals and continuations, making it a powerful tool for traders.

Key Features:

Dynamic Trendline (GOLD):

The central trendline is a weighted moving average based on price and volume, tuned using Fibonacci-based fast (34) and slow (144) exponential moving average lengths. This ensures the trendline adapts seamlessly to the flow of market dynamics.

Formula:

GOLD = VWMA(34) * Volume Factor + VWMA(144) * (1 - Volume Factor)

Fractal Highs and Lows:

Detects pivotal market points using a fractal lookback period (default 5, odd-numbered). Fractals identify local highs and lows over a defined window, capturing the structure of market cycles.

Trend Background Highlighting:

Bullish Zone: Price above the GOLD line with a green background.

Bearish Zone: Price below the GOLD line with a red background.

Buy and Sell Alerts:

Generates actionable signals when fractals align with GOLD. Bullish fractals confirm continuation or reversal in an uptrend, while bearish fractals validate a downtrend.

The Math Behind Aurium:

Volume-Weighted Adjustments:

By integrating volume into the calculation, Aurium dynamically emphasizes price levels with greater participation, giving traders insight into zones of institutional interest.

Formula:

VWMA = EMA(Close * Volume) / EMA(Volume)

Fractal Calculations:

Fractals are identified as local maxima (highs) or minima (lows) based on the surrounding bars, leveraging the natural symmetry in price behavior.

Fibonacci Relationships:

The 34 and 144 EMA lengths are Fibonacci numbers, offering a natural alignment with price cycles and market rhythms.

Ideal For:

Traders seeking a precise and intuitive indicator for aligning with trends and detecting reversals.

Strategies inspired by Bill Williams, with added volume and fractal-based insights.

Short-term scalpers and long-term trend-followers alike.

Unlock deeper market insights and trade with precision using Aurium!

Enhanced RSIEnhanced RSI with Phases, Divergences & Volume Control:

This advanced RSI indicator expands on the traditional Relative Strength Index by introducing dynamic exhaustion phase detection, automatic divergence identification, and volume-based control evaluation. It provides traders with actionable insights into trend momentum, potential reversals, and market dominance.

Key Features:

Dynamic Exhaustion Phases:

Identifies real phases of the RSI based on slope and momentum:

Acceleration: Momentum increasing rapidly (green phase).

Deceleration: Momentum weakening (red phase).

Plateau: Momentum flattening (yellow phase).

Neutral: No significant momentum shift detected.

Phases are displayed dynamically in a box on the chart.

Automatic Divergence Detection:

Bullish Divergence: Identified when price makes a lower low while RSI makes a higher low.

Bearish Divergence: Identified when price makes a higher high while RSI makes a lower high.

Divergences are marked directly on the RSI chart with labeled circles.

Volume-Based Control Evaluation:

Analyzes price action relative to volume to determine market dominance:

Bulls in Control: Closing price is higher than the opening price.

Bears in Control: Closing price is lower than the opening price.

Neutral: No significant dominance (closing equals opening).

Volume status is displayed alongside the RSI phase in the chart’s top-left box.

Custom RSI Plot:

Includes overbought (70), oversold (30), and neutral (50) levels for easier interpretation of market conditions.

RSI plotted in blue for clarity.

How to Use:

Add to Chart:

Apply this indicator to any chart in TradingView.

Interpret the RSI Phase Box:

Use the RSI phase (Acceleration, Deceleration, Plateau, Neutral) to identify trend momentum.

Combine the phase with the volume status (Bulls or Bears in Control) to confirm market sentiment.

Identify Divergences:

Look for Bullish Divergence (potential upward reversal) or Bearish Divergence (potential downward reversal) marked directly on the RSI chart.

Adjust Settings:

Customize the RSI period, phase sensitivity, and divergence lookback period to fit your trading style.

Disclaimer:

This indicator is a tool to assist with technical analysis. It is not a financial advice or a guarantee of market performance. Always combine this indicator with other methods or strategies for better results.

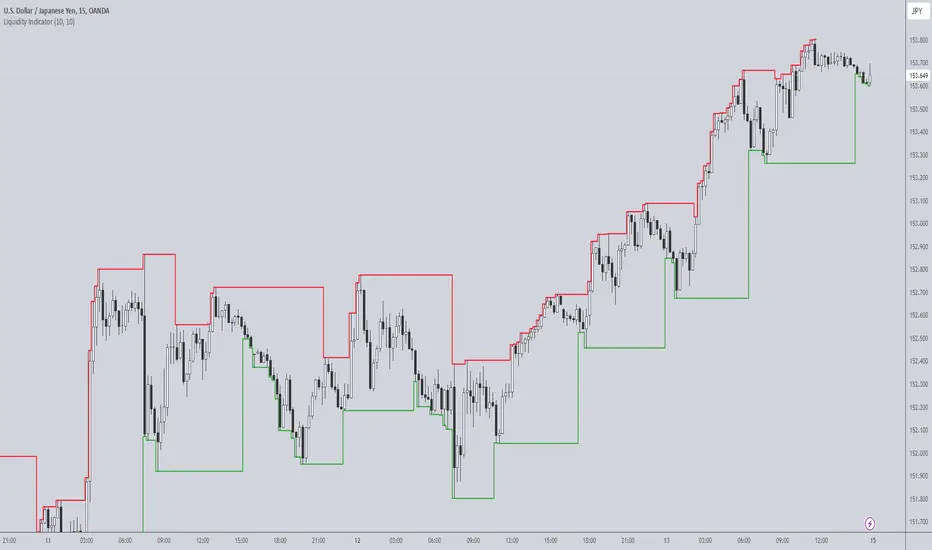

Liquidity IndicatorThe Liquidity Indicator helps identify key price levels where liquidity may be concentrated by highlighting local highs and local lows on the chart. These levels are calculated using a lookback period to determine the highest and lowest points in the recent price action.

Local Highs: Displayed as red lines, these indicate recent peaks where price has experienced rejection or a possible reversal point.

Local Lows: Displayed as green lines, these represent recent troughs where price may find support or experience a bounce.

This indicator is useful for spotting potential areas of interest for price reversal or continuation, as high liquidity zones may lead to more significant price movements.

Key Features:

Adjustable lookback period to define the scope for identifying local highs and lows.

Continuous plotting without any time restrictions, providing real-time insights into liquidity conditions.

Alerts available for when a local high or local low is detected, enabling timely market analysis.

Use Case:

This indicator can be used in conjunction with other technical analysis tools or strategies to help identify significant price levels where liquidity could impact price action. It is suitable for both intraday and swing traders looking for key price zones where potential reversals or continuations might occur.

Crypto$ure EMA with 4H Trend TableThe Crypto AMEX:URE EMA indicator provides a clear, multi-timeframe confirmation setup to help you align your shorter-term trades with the broader market trend.

Key Features:

4-Hour EMA Trend Insight:

A table, displayed at the top-right corner of your chart, shows the current 4-hour EMA value and whether the 4-hour trend is Bullish, Bearish, or Neutral. This gives you a reliable, higher-timeframe perspective, making it easier to understand the general market direction.

Lower Timeframe Signals (e.g., 25m or 15m):

On your chosen chart timeframe, the indicator plots two EMAs (Fast and Slow).

A Buy Signal (an up arrow) appears when the Fast EMA crosses above the Slow EMA, indicating potential upward momentum.

A Sell Signal (a down arrow) appears when the Fast EMA crosses below the Slow EMA, indicating potential downward momentum.

Manual Confirmation for Better Accuracy:

While the Buy/Sell signals come directly from the shorter timeframe, you can use the 4-hour trend information from the table to confirm or filter these signals. For example, if the 4-hour trend is Bullish, the Buy signals on the shorter timeframe may carry more weight. If it’s Bearish, then the Sell signals might be more reliable.

How to Use:

Add the Crypto AMEX:URE EMA indicator to your chart.

Check the top-right table to see the current 4-hour EMA trend.

Watch for Buy (up arrow) or Sell (down arrow) signals on your current timeframe.

For added confidence, consider taking Buy signals only when the 4-hour trend is Bullish and Sell signals when the 4-hour trend is Bearish.

Note:

This indicator does not generate trading orders. Instead, it provides actionable insights to help guide your discretionary decision-making. Always consider additional market context, risk management practices, and personal trading rules before acting on any signal.