Intraday -RSKWhat You See:

Session Boxes:

As you observe, the larger purple box represents the Asian Session, spanning from around 22:00 to 06:00 UTC. You notice how it captures the overnight market activity.

The smaller, greyish box marks the London Session, from about 08:00 to 12:00 UTC. You can see how the price action changes during this session.

The New York Session is also indicated, with vertical lines possibly marking the open and close, helping you track movements as the U.S. markets come into play.

High and Low Levels:

Horizontal lines are drawn at the high and low of each session. You can use these as potential support or resistance levels, aiding in your decision-making process.

Vertical Lines:

These lines likely correspond to specific key times, such as session opens or closes. You can quickly identify the transition between sessions, which is crucial for your timing.

Color Coding:

Each session is color-coded, making it easier for you to distinguish between them at a glance. The purple, grey, and additional lines offer a clear visual distinction.

How You Use It:

This indicator is your go-to for understanding how different market sessions affect price action. You’ll use it to:

Recognize important price levels within each session.

Identify potential entry and exit points based on session highs and lows.

Observe how the market transitions from one session to another, giving you insight into the best times to trade.

Customization:

You have the flexibility to adjust the settings. You can change session times to suit your trading hours, modify colors to match your chart theme, and even choose which sessions to display or hide based on your focus.

This tool is designed to enhance your analysis, providing you with a structured view of market sessions. With this indicator, you’re well-equipped to navigate the global markets with greater precision and confidence.

Open-source script

Cycles

Candlestick Patterns with SignalsIdentified Patterns:

Bullish Engulfing: Indicates potential upward price movement, marked with green labels and lines.

Bearish Engulfing: Suggests potential downward price movement, marked with red labels and lines.

Hammer: A bullish reversal pattern, marked with blue labels.

Shooting Star: A bearish reversal pattern, marked with orange labels.

Signal Generation:

Long Signal: Triggered when a Bullish Engulfing or Hammer pattern is detected. A dotted green line marks the entry level.

Short Signal: Triggered when a Bearish Engulfing or Shooting Star pattern is detected. A dotted red line marks the entry level.

Visual Elements:

Labels indicating the candlestick pattern names appear at the relevant candles.

Lines connect the previous and current candles for engulfing patterns to highlight their range.

Dotted lines indicate potential entry levels for long or short trades.

SMA Proximity Signal with Trend TableSummary of the Script:

This Pine Script is designed to provide a variety of technical analysis signals based on Simple Moving Averages (SMAs) and market trends across different timeframes. The script combines multiple indicators, such as the SMA crossover, proximity conditions, and trend analysis, along with visual markers and support/resistance lines. Below is a detailed breakdown of the key features:

The script detects crossovers between SMA1 and SMA2 and SMA1 and SMA3, marking them with green circles exactly at the crossover price level (not on the candles).

The crossover events are identified using ta.crossover and ta.crossunder functions.

Additional circles are drawn when other SMAs are in proximity (narrow stage)

Elephant Candle Pattern:

The script identifies "Elephant Candles" based on a large candle body relative to the overall size of the candle, using the condition where the candle body is at least 80% of the total candle size and at least 1.5 times the average candle size.

These candles are marked with an elephant emoji 🐘 at the top of the candle.

Trend Analysis Across Multiple Timeframes:

The script calculates the trend for different timeframes using the SMA20 of each timeframe:

5m, 15m, 1h, 4h, and 1D

It compares the current SMA20 to its previous value to determine whether the trend is Up, Down, or Flat.

Supertrend with Correct Y-axis Scaling OLEG_SLSThe functionality of the script:

1. Supertrend Calculation:

-The trend (Supertrend line) is updated dynamically:

-If the price is above the previous trend, the line follows the upper limit.

-If the price is lower, the line follows the lower boundary.

2. Calculation of the Supertrend for the higher timeframe:

-The function is used to calculate the Supertrend for the hourly, regardless of the current timeframe on the chart.

3. Buy and Sell Signals:

-Buy signal: When the price crosses the Supertrend line up and is above the Supertrend line.

-A sales signal: When the price crosses the Supertrend line down and is below the Supertrend line.

4. Display on the chart

-The Supertrend line is displayed:

-Green if the price is above the Supertrend line.

-Red if the price is below the Supertrend line.

-The Supertrend line for the hourly timeframe is displayed in blue.

5. Alerts

Two types of alerts are created:

-Buy Alert: When there is a buy signal.

-Sell Alert: When there is a sell signal.

Features and recommendations:

-Supertrend works best in trending markets. In a sideways movement, it can give false signals.

-Check the signals on multiple timeframes for confirmation.

-Add additional indicators (for example, RSI or MACD) to filter the signals.

-Test the strategy on historical data before using it in real trading.

_________________________________________________________________________________

Функционал скрипта:

1. Расчет Supertrend:

-Тренд (линия Supertrend) обновляется динамически:

-Если цена выше предыдущего тренда, линия следует за верхней границей.

-Если цена ниже, линия следует за нижней границей.

2. Расчет Supertrend для старшего таймфрейма:

-Используется функция чтобы рассчитать Supertrend для часового,независимо от текущего таймфрейма на графике.

3. Сигналы покупки и продажи:

-Сигнал покупки: Когда цена пересекает линию Supertrend вверх и находится выше линии Supertrend.

-Сигнал продажи: Когда цена пересекает линию Supertrend вниз и находится ниже линии Supertrend.

4. Отображение на графике

-Линия Supertrend отображается:

-Зеленым, если цена выше линии Supertrend.

-Красным, если цена ниже линии Supertrend.

-Линия Supertrend для часового таймфрейма отображается синим цветом.

5. Оповещения

Создаются два типа оповещений:

-Buy Alert: Когда возникает сигнал на покупку.

-Sell Alert: Когда возникает сигнал на продажу.

Особенности и рекомендации:

-Supertrend лучше всего работает в трендовых рынках. В боковом движении может давать ложные сигналы.

-Проверяйте сигналы на нескольких таймфреймах для подтверждения.

-Добавьте дополнительные индикаторы (например, RSI или MACD) для фильтрации сигналов.

-Тестируйте стратегию на исторических данных перед использованием в реальной торговле.

Highest High, Lowest Low, Midpoint for Selected Days [kiyarash]Highest High, Lowest Low, and Midpoint for Selected Days Indicator

This custom TradingView indicator allows you to visualize the highest high, lowest low, and the midpoint (average of the highest high and lowest low) over a custom-defined period. You can choose a starting date and specify how many days ahead you want to track the highest and lowest values. This is useful for identifying key levels in a trend and potential support or resistance zones.

How to Use:

Set the Starting Date:

In the settings, input the starting date from which you want to begin tracking the price range. This will be the reference point for your analysis.

Choose the Number of Days to Track:

Specify how many days you want to analyze from the selected starting date. For example, if you want to see the highest high and lowest low over the next 3 days, enter "3" in the settings.

Visualizing the Levels:

The indicator will automatically calculate the highest price and the lowest price over the selected period and draw three lines:

Red Line: Represents the Highest High within the selected period.

Green Line: Represents the Lowest Low within the selected period.

Blue Line: Represents the Midpoint, which is the average of the Highest High and Lowest Low.

Interpretation:

Highest High is a key resistance level, indicating the highest price reached within the specified period.

Lowest Low is a key support level, showing the lowest price during the same period.

Midpoint provides a reference for the average price, often acting as a neutral level between support and resistance.

This tool can help traders to quickly assess potential market ranges, identify breakout or breakdown points, and make informed decisions based on recent price action.

How to Apply:

Add the indicator to your chart.

Adjust the settings to choose your desired starting date and the number of days you want to analyze.

Observe the drawn lines for the Highest High, Lowest Low, and Midpoint levels, and use them to assist in your trading decisions.

GMO (Gyroscopic Momentum Oscillator) GMO

Overview

This indicator fuses multiple advanced concepts to give traders a comprehensive view of market momentum, volatility, and potential turning points. It leverages the Gyroscopic Momentum Oscillator (GMO) foundation and layers on IQR-based bands, dynamic ATR-adjusted OB/OS levels, torque filtering, and divergence detection. The outcome is a versatile tool that can assist in identifying both short-term squeezes and long-term reversal zones while detecting subtle shifts in momentum acceleration.

Key Components:

Gyroscopic Momentum Oscillator (GMO) – A physics-inspired metric capturing trend stability and momentum by treating price dynamics as “angle,” “angular velocity,” and “inertia.”

IQR Bands – Highlight statistically typical oscillation ranges, providing insight into short-term squeezes and potential near-term trend shifts.

ATR-Adjusted OB/OS Levels – Dynamic thresholds for overbought/oversold conditions, adapting to volatility, aiding in identifying long-term potential reversal zones.

Torque Filtering & Scaling – Smooths and thresholds torque (the rate of change of momentum) and visually scales it for clarity, indicating sudden force changes that may precede volatility adjustments.

Divergence Detection – Highlights potential reversal cues by comparing oscillator swings against price swings, revealing regular and hidden bullish/bearish divergences.

Conceptual Insights

IQR Bands (Short-Term Squeeze & Trend Direction):

Short-Term Momentum and Squeeze: The IQR (Interquartile Range) bands show where the oscillator tends to “live” statistically. When the GMO line hovers within compressed IQR bands, it can signal a momentum squeeze phase. Exiting these tight ranges often correlates with short-term breakout opportunities.

Trend Reversals: If the oscillator pushes beyond these IQR ranges, it may indicate an emerging short-term trend change. Traders can watch for GMO escaping the IQR “comfort zone” to anticipate a new directional move.

Dynamic OB/OS Levels (Long-Term Reversal Zones):

ATR-Based Adaptive Thresholds: Instead of static overbought/oversold lines, this tool uses ATR to adjust OB/OS boundaries. In calm markets, these lines remain closer to ±90. As volatility rises, they approach ±100, reflecting greater permissible swings.

Long-Term Trend Reversal Potential: If GMO hits these dynamically adjusted OB/OS extremes, it suggests conditions ripe for possible long-term trend reversals. Traders seeking major inflection points may find these adaptive levels more reliable than fixed thresholds.

Torque (Sudden Force & Directional Shifts):

Momentum Acceleration Insight: Torque represents the second derivative of momentum, highlighting how quickly momentum is changing. High positive torque suggests a rapidly strengthening bullish force, while high negative torque warns of sudden bearish pressure.

Early Warning & Stability/Volatility Adjustments: By monitoring torque spikes, traders can anticipate momentum shifts before price fully confirms them. This can signal imminent changes in stability or increased volatility phases.

Indicator Parameters and Usage

GMO-Related Inputs:

lenPivot (Default 100): Length for calculating the pivot line (slow market axis).

lenSmoothAngle (Default 200): Smooths the angle measure, reducing noise.

lenATR (Default 14): ATR period for scaling factor, linking price changes to volatility.

useVolatility (Default true): If true, volatility (ATR) influences inertia, adjusting momentum calculations.

useVolume (Default false): If true, volume affects inertia, adding a liquidity dimension to momentum.

lenVolSmoothing (Default 50): Smooths volume calculations if useVolume is enabled.

lenMomentumSmooth (Default 20): EMA smoothing of GMO for a cleaner oscillator line.

normalizeRange (Default true): Normalizes GMO to a fixed range for consistent interpretation.

lenNorm (Default 100): Length for normalization window, ensuring GMO’s scale adapts to recent extremes.

IQR Bands Settings:

iqrLength (Default 14): Period to compute the oscillator’s statistical IQR.

iqrMult (Default 1.5): Multiplier to define the upper and lower IQR-based bands.

ATR-Adjusted OB/OS Settings:

baseOBLevel (Fixed at 90) and baseOSLevel (Fixed at 90): Base lines for OB/OS.

atrPeriodForOBOS (Default 50): ATR length for adjusting OB/OS thresholds dynamically.

atrScaling (Default 0.2): Controls how strongly volatility affects OB/OS lines.

Torque Filtering & Visualization:

torqueSmoothLength (Default 10): EMA length to smooth raw torque values.

atrPeriodForTorque (Default 14): ATR period to determine torque threshold.

atrTorqueScaling (Default 0.5): Scales ATR for determining torque’s “significant” threshold.

torqueScaleFactor (Default 10.0): Multiplies the torque values for better visual prominence on the chart.

Divergence Inputs:

showDivergences (Default true): Toggles divergence signals.

lbR, lbL (Defaults 5): Pivot lookback periods to identify swing highs and lows.

rangeUpper, rangeLower: Bar constraints to validate potential divergences.

plotBull, plotHiddenBull, plotBear, plotHiddenBear: Toggles for each divergence type.

Visual Elements on the Chart

GMO Line (Blue) & Zero Line (Gray):

GMO line oscillates around zero. Positive territory hints bullish momentum, negative suggests bearish.

IQR Bands (Teal Lines & Yellow Fill):

Upper/lower bands form a statistical “normal range” for GMO. The median line (purple) provides a central reference. Contraction near these bands indicates a short-term squeeze, expansions beyond them can signal emerging short-term trend changes.

Dynamic OB/OS (Red & Green Lines):

Red line near +90 to +100: Overbought zone (dynamic).

Green line near -90 to -100: Oversold zone (dynamic).

Movement into these zones may mark significant, longer-term reversal potential.

Torque Histogram (Colored Bars):

Plotted below GMO. Green bars = torque above positive threshold (bullish acceleration).

Red bars = torque below negative threshold (bearish acceleration).

Gray bars = neutral range.

This provides early warnings of momentum shifts before price responds fully.

Precession (Orange Line):

Scaled for visibility, adds context to long-term angular shifts in the oscillator.

Divergence Signals (Shapes):

Circles and offset lines highlight regular or hidden bullish/bearish divergences, offering potential reversal signals.

Practical Interpretation & Strategy

Short-Term Opportunities (IQR Focus):

If GMO compresses within IQR bands, the market might be “winding up.” A break above/below these bands can signal a short-term trade opportunity.

Long-Term Reversal Zones (Dynamic OB/OS):

When GMO approaches these dynamically adjusted extremes, conditions may be ripe for a major trend shift. This is particularly useful for swing or position traders looking for significant turnarounds.

Monitoring Torque for Acceleration Cues:

Torque spikes can precede price action, serving as an early catalyst signal. If torque turns strongly positive, anticipate bullish acceleration; strongly negative torque may warn of upcoming bearish pressure.

Confirm with Divergences:

Divergences between price and GMO reinforce potential reversal or continuation signals identified by IQR, OB/OS, or torque. Use them to increase confidence in setups.

Tips and Best Practices

Combine with Price & Volume Action:

While the indicator is powerful, always confirm signals with actual price structure, volume patterns, or other trend-following tools.

Adjust Lengths & Periods as Needed:

Shorter lengths = more responsiveness but more noise. Longer lengths = smoother signals but greater lag. Tune parameters to match your trading style and timeframe.

Use ATR and Volume Settings Wisely:

If markets are highly volatile, consider useVolatility to refine momentum readings. If liquidity is key, enable useVolume.

Scaling Torque:

If torque bars are hard to read, increase torqueScaleFactor further. The scaling doesn’t affect logic—only visibility.

Conclusion

The “GMO + IQR Bands + ATR-Adjusted OB/OS + Torque Filtering (Scaled)” indicator presents a holistic framework for understanding market momentum across multiple timescales and conditions. By interpreting short-term squeezes via IQR bands, long-term reversal zones via adaptive OB/OS, and subtle acceleration changes through torque, traders can gain advanced insights into when to anticipate breakouts, manage risk around potential reversals, and fine-tune timing for entries and exits.

This integrated approach helps navigate complex market dynamics, making it a valuable addition to any technical analysis toolkit.

Master Litecoin Network Value Model BandThe "Master Litecoin Network Value Model Band" is a TradingView Pine Script indicator designed to analyze and visualize Litecoin's valuation dynamics in comparison to Bitcoin, leveraging a range of on-chain and market metrics. The script creates bands to highlight overvalued or undervalued conditions for Litecoin relative to multiple network and market factors.

Key Features:

Data Integration:

Incorporates on-chain data such as total addresses, new addresses, active addresses, transactions, volume, hodlers, and block sizes for both Litecoin and Bitcoin.

Uses market metrics like price, supply, and retail involvement to model Litecoin's network value.

Value Models:

Constructs individual models based on specific metrics (e.g., new addresses, transaction volume, median volume) to evaluate Litecoin's network valuation against Bitcoin.

Normalizes these models by adjusting for relative supply and Bitcoin's USD price.

Average and Median Models:

Calculates an Average Value Model by combining multiple metric-based models.

Provides a smoothed Median Value Model for more stable trends over time.

Dynamic Bands:

Identifies the maximum and minimum values among the various models to establish upper and lower bands for Litecoin's valuation.

Compares Litecoin's USD price to these bands, categorizing it as overvalued (above the upper band), undervalued (below the lower band), or fairly valued (within the bands).

Visual Representation:

Plots the upper and lower bounds (maxValue and minValue) along with Litecoin's price (ltcusd).

Highlights price movements with color-coded fills:

White fill: Litecoin price exceeds the maximum band.

Blue fill: Litecoin price is between the maximum and minimum bands.

Black fill: Litecoin price falls below the minimum band.

Purpose:

This indicator provides traders and analysts with a comprehensive tool to:

Assess Litecoin's market position relative to its network fundamentals.

Identify potential buy or sell zones based on deviation from fair valuation bands.

Track Litecoin's value trends in relation to Bitcoin as a benchmark.

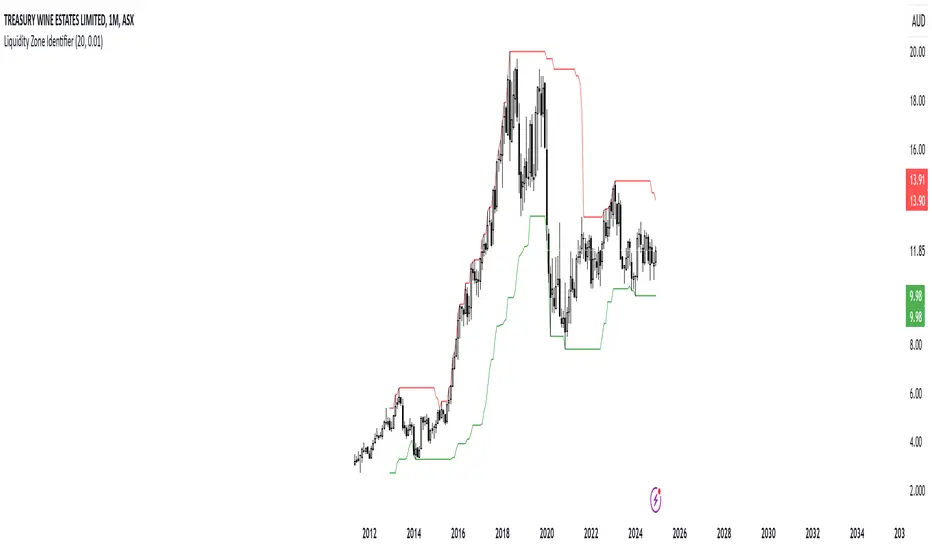

RShar Liquidity Zone Identifier Description of the Liquidity Zone Identifier Indicator

The **Liquidity Zone Identifier** is a TradingView indicator designed to highlight key liquidity zones on a price chart. Liquidity zones represent areas where the price is likely to encounter significant resistance or support, making them critical for technical analysis and trading decisions.

Key Features:

1. **Dynamic Resistance and Support Levels**:

- The indicator calculates the highest high and lowest low over a user-defined period (`length`) to identify potential resistance and support levels.

- Sensitivity can be adjusted using the `zoneSensitivity` parameter, which defines a percentage buffer around these levels to expand the zones.

2. **Visual Representation**:

- Resistance zones are highlighted in **red**, indicating areas where the price may face selling pressure.

- Support zones are highlighted in **green**, representing areas where the price may find buying interest.

- The zones are displayed as shaded regions using the `fill` function, making them visually distinct and easy to interpret.

3. **Customizable Inputs**:

- **Zone Length** (`length`): Determines the number of candles considered for calculating highs and lows.

- **Zone Sensitivity** (`zoneSensitivity`): Sets the percentage margin around the calculated levels to define the liquidity zones.

- **Zone Colors**: Users can customize the colors for resistance and support zones to suit their preferences.

- **Toggle Fill**: The `showFill` option allows users to enable or disable shaded zone visualization.

4. **Alerts for Trading Opportunities**:

- Alerts are triggered when:

- The price enters the **resistance zone** (current high is greater than or equal to the resistance zone).

- The price enters the **support zone** (current low is less than or equal to the support zone).

- These alerts help traders stay informed of critical market movements without constantly monitoring the chart.

#### How It Works:

1. **Calculation of Zones**:

- The highest high and lowest low over the specified `length` are calculated to define the primary levels.

- A buffer zone is added around these levels based on the `zoneSensitivity` percentage, creating a margin of interaction for price movements.

2. **Plotting the Zones**:

- The top and bottom boundaries of the resistance and support zones are plotted as lines.

- The area between these boundaries is shaded using the `fill` function to enhance visualization.

3. **Alerts for Key Events**:

- Traders are notified when price action interacts with the zones, enabling quick decision-making.

#### Use Case:

The Liquidity Zone Identifier is ideal for:

- Identifying areas of potential price reversal or consolidation.

- Spotting high-probability trading setups near resistance and support zones.

- Complementing other technical indicators in a trading strategy.

By effectively highlighting critical price levels, this indicator provides traders with a powerful tool to navigate the markets with greater precision.

Financial Conditions Composite Z-Score1. Inputs and Data Sources

The script pulls data for the following financial metrics using TradingView's request.security function:

CBOE:VIX (Volatility Index): A measure of market volatility.

MOVE Index: A measure of bond market volatility (or Treasury volatility).

BAMLH0A0HYM2 (High-Yield Spread): The spread between high-yield corporate bonds and Treasury yields.

BAMLC0A0CM (Credit Spread): The spread for investment-grade corporate bonds.

Each of these metrics represents a key aspect of financial conditions:

VIX: Equity market risk.

MOVE: Bond market risk.

High-Yield Spread and Credit Spread: Perception of risk in corporate debt.

2. Z-Score Calculation

A z-score standardizes each metric to show how far it deviates from its average over a specified period (lookback = 160, or 160 days):

Positive z-scores indicate the metric is higher than average.

Negative z-scores indicate the metric is lower than average.

The formula for the z-score:

Z-Score = Metric − Mean

Standard Deviation Z-Score = Standard Deviation Metric−Mean

3. Combined Z-Score

The script combines the four individual z-scores into a single Composite Z-Score, equally weighted across the metrics:

Combined Z-Score = (Z VIX + Z MOVE + Z High-Yield Spread + Z Credit Spread) / 4

This Combined Z-Score provides an overall measure of financial conditions:

Positive combined z-scores indicate tighter or riskier financial conditions.

Negative combined z-scores indicate looser or less risky financial conditions.

4. Visual Elements on the Chart

A. Colorful Lines: Individual Z-Scores

Each of the four metrics is plotted as a separate line:

Red: Z-score of the VIX.

Green: Z-score of the MOVE index.

Orange: Z-score of the high-yield spread.

Purple: Z-score of the credit spread.

These lines show how each metric contributes to the overall financial conditions. For example:

A rising red line means increasing equity market volatility (risk).

A rising green line means increasing bond market volatility (risk).

B. Blue Line: Combined Z-Score

The blue line represents the Combined Z-Score. It aggregates the individual z-scores into a single measure:

A rising blue line suggests financial conditions are tightening (greater risk across markets).

A falling blue line suggests financial conditions are loosening (lower risk across markets).

C. Red and Green Background: Z-Score Regions

Red Background: When the Combined Z-Score is positive (>0), it indicates riskier or tighter financial conditions.

Green Background: When the Combined Z-Score is negative (<0), it indicates less risky or looser financial conditions.

This background coloring helps visually distinguish periods of riskier financial conditions from less risky ones.

5. Purpose of the Visualization

This indicator provides a comprehensive view of financial conditions across multiple asset classes:

Traders can use it to gauge the level of systemic market stress.

Investors can use it to assess when risk is elevated (positive z-scores) or subdued (negative z-scores).

It helps in decision-making for strategies that depend on market volatility or risk appetite.

Summary of What You See:

Colorful Lines (Red, Green, Orange, Purple): Individual z-scores for each metric (VIX, MOVE, high-yield spread, credit spread).

Blue Line: The aggregated Combined Z-Score that summarizes financial conditions.

Red and Green Background:

Red: Tight or risky financial conditions (Combined Z-Score > 0).

Green: Loose or low-risk financial conditions (Combined Z-Score < 0).

This visualization provides a multi-dimensional view of financial conditions at a glance, helping to identify periods of high or low risk in the markets.

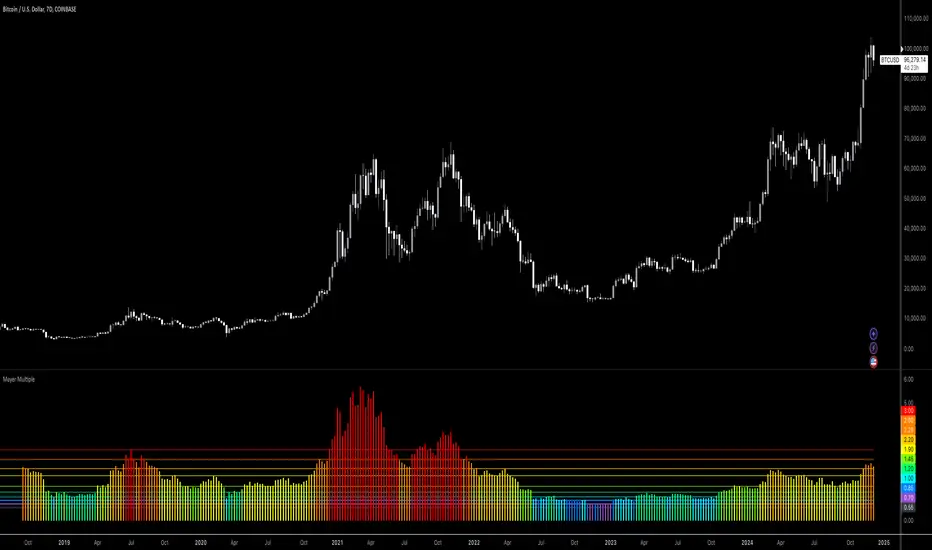

Bitcoin: Mayer MultipleMayer Multiple Indicator

The Mayer Multiple is a powerful tool designed to help traders assess market conditions and identify optimal buying or selling opportunities. It calculates the ratio between the current price and its 200-day simple moving average (SMA), visualizing key thresholds that indicate value zones, caution areas, and overheated markets.

Key Features:

Dynamic Market Zones: Clearly marked levels like "Smash Buy," "Boost DCA," and "Extreme Euphoria" to guide your trading decisions.

Customizable Input: Adjust the SMA length to fit your strategy.

Color-Coded Signals: Intuitive visualization of market sentiment for quick analysis.

Comprehensive Thresholds: Historical insights into price behavior with plotted reference levels based on probabilities.

This indicator is ideal for traders aiming to enhance their long-term strategies and improve decision-making in volatile markets. Use it to gain an edge in identifying potential turning points and managing risk effectively.

Trend Condition [TradersPro]

OVERVIEW

The Trend Condition Indicator measures the strength of the bullish or bearish trend by using a ribbon pattern of exponential moving averages and scoring system. Trend cycles naturally expand and contract as a normal part of the cycle. It is the rhythm of the market. Perpetual expansion and contraction of trend.

As trend cycles develop the indicator shows a compression of the averages. These compression zones are key locations as trends typically expand from there. The expansion of trend can be up or down.

As the trend advances the ribbon effect of the indicator can be seen as each average expands with the price action. Once they have “fanned” the probability of the current trend slowing is high.

This can be used to recognize a powerful trend may be concluding. Traders can tighten stops, exit positions or utilize other prudent strategies.

CONCEPTS

Each line will display green if it is higher than the prior period and red if it is lower than the prior period. If the average is green it is considered bullish and will score one point in the bullish display. Red lines are considered bearish and will score one point in the bearish display.

The indicator can then be used at a quick glance to see the number of averages that are bullish and the number that are bearish.

A trader may use these on any tradable instrument. They can be helpful in stock portfolio management when used with an index like the S&P 500 to determine the strength of the current market trend. This may affect trade decisions like possession size, stop location and other risk factors.

Tomas' Financial Conditions Z Score"The indicator is a composite z-score comprised of the following four components (equally-weighted):

Credit spreads - ICE BofA High Yield Option Adjusted Spread (BAMLH0A0HYM2) and ICE BofA Corporate Index Option Adjusted Spread (BAMLC0A0CM)

Volatility indexes - VIX (S&P 500 implied volatility) and MOVE (US Treasury bond implied volatility)

I've got it set to a 160-day lookback period, which I think is roughly the best setting after some tinkering.

When the z-score is above zero, it throws a red signal - and when the z-score is below zero, it throws a green signal.

This indicator is a follow-on from the "traffic light financial conditions indicator" that I wrote a thread about a couple of months ago.

I moved on from that previous indicator because it is based on the Federal Reserve's NFCI, which is regularly revised, but I didn't take that into account at the time.

So not a great real-time indicator, if the signal can be subsequently revised in the opposite direction weeks later.

This new indicator is based on real-time market data, so there's no revisions, and it also updates daily, as opposed to weekly for the NFCI"

Options Betting Range - Extended# Options Betting Range - Extended

**Options Betting Range - Extended** is a versatile TradingView indicator designed to assist traders in identifying and visualizing optimal options trading ranges for multiple symbols. By leveraging predefined prediction and execution dates along with specific high and low price points, this indicator dynamically draws trendlines to highlight potential options betting zones, enhancing your trading strategy and decision-making process.

## **Key Features**

- **Multi-Symbol Support:** Automatically adapts to popular symbols such as SPY, IWM, QQQ, DIA, TLT, and GOOG, providing tailored options betting ranges for each.

- **Dynamic Trendlines:** Draws both dashed and solid trendlines based on user-defined prediction and execution dates, clearly marking high and low price boundaries.

- **Customizable Parameters:** Easily configure prediction and execution dates, high and low prices, and timezones to suit your specific trading requirements.

- **Single Execution:** Ensures that each trendline is drawn only once per specified prediction date, preventing clutter and maintaining chart clarity.

- **Clear Visual Indicators:** Utilizes color-coded labels to denote high (green) and low (red) price points, making it easy to identify critical trading levels at a glance.

## **How It Works**

1. **Initialization:**

- Upon adding the indicator to your chart, it initializes with predefined symbols and their corresponding high and low price points for two trendlines each.

2. **Configuration:**

- **Trendline 1:**

- **Prediction Date:** Set the year, month, and day when the trendline should be predicted.

- **Execution Date:** Define the year, month, and day when the trendline will be executed.

- **Timezone:** Choose the appropriate timezone to ensure accurate date matching.

- **Trendline 2:**

- Similarly, configure the prediction and execution dates along with the timezone.

3. **Trendline Drawing:**

- On reaching the specified prediction date, the indicator draws dashed trendlines representing the high and low price ranges.

- Solid trendlines are then drawn to solidify the high and low price boundaries.

- Labels are added to clearly mark the high and low price points on the chart.

4. **Visualization:**

- The trendlines and labels provide a visual framework for potential options trading ranges, allowing traders to make informed decisions based on these predefined levels.

## **How to Use**

1. **Add the Indicator:**

- Open your TradingView chart and apply the **Options Betting Range - Extended** indicator.

2. **Select a Symbol:**

- Ensure that the chart is set to one of the supported symbols (e.g., SPY, IWM, QQQ, DIA, TLT, GOOG) to activate the corresponding trendline configurations.

3. **Configure Trendline Parameters:**

- Access the indicator settings to input your desired prediction and execution dates, high and low prices, and select the appropriate timezone for each trendline.

4. **Monitor Trendlines:**

- As the chart progresses to the specified prediction dates, observe the dynamically drawn trendlines and labels indicating the options betting ranges.

5. **Make Informed Trades:**

- Utilize the visual cues provided by the trendlines to identify optimal entry and exit points for your options trading strategies.

## **Benefits**

- **Enhanced Strategy Visualization:** Clearly outlines potential trading ranges, aiding in the formulation and execution of precise options strategies.

- **Time-Saving Automation:** Automatically draws trendlines based on your configurations, reducing the need for manual chart analysis.

- **Improved Decision-Making:** Provides objective price levels for trading, minimizing emotional bias and enhancing analytical precision.

## **Important Considerations**

- **Timezone Accuracy:** Ensure that the timezones selected in the indicator settings align with your chart's timezone to maintain accurate date matching.

- **Chart Timeframe:** The prediction dates should correspond to the timeframe of your chart (e.g., daily, hourly) to ensure that trendlines are triggered correctly.

- **Visible Price Range:** Verify that the high and low prices set for trendlines are within the visible range of your chart to ensure that all trendlines and labels are clearly visible.

## **Conclusion**

**Options Betting Range - Extended** is a powerful tool for traders seeking to automate and visualize their options trading ranges across multiple symbols. By providing clear, customizable trendlines based on specific prediction and execution dates, this indicator enhances your ability to identify and act upon strategic trading opportunities with confidence.

---

Square Numbers Horizontal LinesTrading with square numbers is a unique approach to technical analysis, where square numbers (1, 4, 9, 16, 25, etc.) are used to guide the identification of potential levels of support, resistance, and price targets. These numbers are often considered in a more mathematical or geometric context, and they can be applied in trading strategies, chart patterns, and psychological market analysis.

Vietnamese Lunar New Year DatesVisualize Vietnamese Lunar New Year dates on your chart with this indicator!

This script plots vertical red lines for Lunar New Year from 2000 to 2030, along with blue and green lines marking the start of December (previous year) and January (current year) for context. Perfect for analyzing market patterns around this significant holiday.

Customize further to suit your trading style!"

Intraday Trend CandlesThe Intraday Trend Candles (ITC) indicator is a Pine Script-based tool designed for traders seeking to visualize market trends effectively. Using a combination of the Look Back Period, a multiplier for true range, and linearly weighted moving averages (LWMA), this indicator calculates dynamic trend limits that adapt to price movements. It identifies key trend shifts by comparing the current price to these dynamic thresholds, resulting in a visually intuitive display of market bias directly on the chart. The indicator is particularly well-suited for intraday trading, as it provides responsive insights tailored to short-term price action.

The ITC plots color-coded candles, highlighting bullish trends in blue and bearish trends in yellow, with gray indicating indecision or trend continuation. This color-coded approach makes it easy to identify reversals and trend dynamics at a glance. Additionally, a trend line is plotted to enhance clarity, signaling whether the price is favoring the upper or lower threshold of the calculated range. With built-in alerts for trend reversals, traders can stay informed about critical market shifts without constantly monitoring the chart. This combination of visual cues and alerts makes the ITC a versatile and powerful tool for traders focusing on momentum and trend-following strategies.

Normalised ATR - Configurable Session Volatility AnalysisThis indicator analyzes price volatility across different trading sessions throughout the day. Here are its key features:

1. **Configurable Time Periods**

- Users can set specific date ranges for analysis

- Supports up to 12 customizable trading sessions

- Adjustable session durations (1-8 hours each)

2. **Volatility Measurements**

- Offers two calculation methods:

* Normalized Range: (High-Low)/Midpoint Price × 100 (as percentage)

* Absolute Range: Simple High-Low difference

- Tracks key statistics for each session:

* Maximum range

* Minimum range

* Average range

* 25% quartile range

3. **Statistical Analysis**

- Calculates 5th and 95th percentiles across all sessions

- Provides visual reference lines for these percentiles

- Shows detailed statistics in a color-coded table

4. **Visual Display**

- Clear tabular display of session statistics

- Color-coded for easy reading

- Plot of daily ranges with percentile bounds

- Session times displayed in UTC

This tool is particularly useful for:

- Understanding market volatility patterns across different trading sessions

- Identifying optimal trading hours

- Planning trading strategies based on historical volatility patterns

- Comparing volatility across different market periods

2-Year MA Multiplier [UAlgo]The 2-Year MA Multiplier is a technical analysis tool designed to assist traders and investors in identifying potential overbought and oversold conditions in the market. By plotting the 2-year moving average (MA) of an asset's closing price alongside an upper band set at five times this moving average, the indicator provides visual cues to assess long-term price trends and significant market movements.

🔶 Key Features

2-Year Moving Average (MA): Calculates the simple moving average of the asset's closing price over a 730-day period, representing approximately two years.

Visual Indicators: Plots the 2-year MA in forest green and the upper band in firebrick red for clear differentiation.

Fills the area between the 2-year MA and the upper band to highlight the normal trading range.

Uses color-coded fills to indicate overbought (tomato red) and oversold (cornflower blue) conditions based on the asset's closing price relative to the bands.

🔶 Idea

The concept behind the 2-Year MA Multiplier is rooted in the cyclical nature of markets, particularly in assets like Bitcoin. By analyzing long-term price movements, the indicator aims to identify periods of significant deviation from the norm, which may signal potential buying or selling opportunities.

2-year MA smooths out short-term volatility, providing a clearer view of the asset's long-term trend. This timeframe is substantial enough to capture major market cycles, making it a reliable baseline for analysis.

Multiplying the 2-year MA by five establishes an upper boundary that has historically correlated with market tops. When the asset's price exceeds this upper band, it may indicate overbought conditions, suggesting a potential for price correction. Conversely, when the price falls below the 2-year MA, it may signal oversold conditions, presenting potential buying opportunities.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Blue Sniper V.1Overview

This Pine Script indicator is designed to generate Buy and Sell signals based on proximity to the 50 EMA, stochastic oscillator levels, retracement conditions, and EMA slopes. It is tailored for trending market conditions, making it ideal for identifying high-probability entry points during strong bullish or bearish trends.

Key Features:

Filters out signals in non-trending conditions.

Focuses on retracements near the 50 EMA for precise entries.

Supports alert notifications for Buy and Sell signals.

Includes a cooldown mechanism to prevent signal spamming.

Allows time-based filtering to restrict signals to a specific trading window.

How It Works

Trending Market Conditions

The indicator is most effective when the market exhibits a clear trend. It uses two exponential moving averages (50 EMA and 200 EMA) to determine the overall market trend:

Bullish Trend: 50 EMA is above the 200 EMA, and both EMAs have upward slopes.

Bearish Trend: 50 EMA is below the 200 EMA, and both EMAs have downward slopes.

Buy and Sell Conditions

Buy Signal:

The market is in a bullish trend.

Stochastic oscillator is in the oversold zone.

Price retraces upwards, breaking away from the recent low by more than 1.5 ATR.

Price is near the 50 EMA (within the defined proximity percentage).

Sell Signal:

The market is in a bearish trend.

Stochastic oscillator is in the overbought zone.

Price retraces downwards, breaking away from the recent high by more than 1.5 ATR.

Price is near the 50 EMA.

Outputs

Signals:

Buy Signal: Green "BUY" label below the price bar.

Sell Signal: Red "SELL" label above the price bar.

Alerts:

Alerts are triggered for Buy and Sell signals if conditions are met within the specified time window (if enabled).

EMA Visualization:

50 EMA (blue line).

200 EMA (red line).

Limitations

Not Suitable for Non-Trending Markets: This script is designed for trending conditions. Sideways or choppy markets may produce false signals.

Proximity Tolerance: Adjust the proximityPercent to prevent signals from triggering too frequently during minor oscillations around the 50 EMA.

No Guarantee of Accuracy: As with any technical indicator, it should be used in conjunction with other tools and analysis.

Enhanced Reversal DetectorEnhanced Reversal Detector - Script Description

Overview:

The Enhanced Reversal Detector is a highly refined indicator designed to identify precise trend reversals in financial markets. It improves upon the original reversal detection logic by incorporating additional filters for trend confirmation (using EMA), volume spikes, and candle patterns. These enhancements significantly increase the reliability and accuracy of reversal signals, making it an excellent tool for both short-term and long-term traders.

Key Features

Candle Lookback Logic:

The indicator evaluates historical price action over a user-defined lookback period to detect potential reversal zones.

Bullish reversal conditions are met when price consistently tests lows, and bearish reversal conditions are met when price tests highs.

Trend Confirmation (EMA Filter):

To ensure that reversal signals align with the broader market trend, the indicator incorporates an Exponential Moving Average (EMA) filter.

Bullish signals are only triggered when the price is above the EMA, while bearish signals are only triggered when the price is below the EMA.

Volume Spike Filter:

The indicator checks for significant increases in trading volume to confirm that the reversal is supported by strong market activity.

Volume spikes are calculated as trading volume exceeding a multiple of the 20-bar average volume (default: 1.5x).

Confirmation Period:

Users can define a confirmation window within which reversal signals must be validated.

This reduces false positives and ensures only strong reversals are considered.

Non-Repainting Mode:

Offers a non-repainting option, where signals are based on confirmed conditions from previous bars, ensuring reliability for backtesting.

Visual and Alert Features:

Clear visual markers on the chart indicate bullish (green triangle) and bearish (red triangle) reversal points.

Alert notifications can be enabled for both bullish and bearish reversals, keeping traders informed in real-time.

Inputs

Candle Lookback: Number of candles to evaluate for reversal conditions.

Confirm Within: Number of candles within which a reversal must be validated.

Non-Repainting Mode: Option to enable or disable repainting for signals.

EMA Length: The length of the Exponential Moving Average used for trend confirmation.

Volume Spike Multiplier: Multiplier for identifying significant increases in trading volume.

How It Works

Reversal Detection:

Bullish signals are triggered when:

Price consistently tests recent lows (lookback period).

Price closes above the EMA.

A significant volume spike occurs.

Bearish signals are triggered under opposite conditions (price testing highs, closing below EMA, and volume spike).

Signal Filtering:

Incorporates EMA and volume-based filters to eliminate false positives and focus on high-confidence reversal signals.

Alert Notifications:

Alerts notify users of bullish or bearish reversal opportunities as soon as they are detected.

Use Cases

Scalping and Day Trading:

Ideal for identifying reversals on lower timeframes (e.g., 1-minute or 5-minute charts).

Swing Trading:

Works effectively on higher timeframes (e.g., 1-hour or daily charts) for capturing significant

trend reversals.

Volatile Markets:

Particularly useful in high-volatility markets like cryptocurrencies or forex.

Customization Tips

Adjust the lookback period to fine-tune the sensitivity of the reversal detection.

Increase the volume spike multiplier for markets with irregular trading volumes to focus on significant moves.

Experiment with the EMA length to align signals with your trading strategy's preferred trend duration.

Conclusion

The Enhanced Reversal Detector combines advanced price action analysis, trend confirmation, and market participation filters to deliver high-accuracy reversal signals. With its customizable settings and robust filtering mechanisms, this indicator is an invaluable tool for identifying profitable trading opportunities while minimizing noise and false signals.

LIT - ConfirmationsOverview

The LIT - Confirmations Indicator is a dynamic checklist tool designed for traders who uses LIT Strategy (Liquidity Inducement Theory) following liquidity and smart money concepts as benefit. This tool allows users to document and track essential trading confirmations directly on their TradingView charts, offering a structured and visual approach to market analysis.

What Makes This Unique?

Unlike other open-source tools, the LIT - Confirmations Indicator introduces a fully interactive and customizable table directly on the chart. This table provides real-time feedback with clear ✅ (checked) and ❌ (unchecked) visual indicators for each confirmation. The user can position the table on the chart according to their preference, ensuring it integrates seamlessly into their trading workflow without obscuring critical chart data.

How It Works

1. Predefined Confirmations

The indicator includes a set of commonly used trading confirmations:

Identify Liquidity: Mark areas where liquidity might pool.

Inducement: Confirm the presence of inducements before market reversals.

Relevant Break of Structure (BOS): Validate critical structural changes.

Mitigation after RBoS: Check for mitigation following a BOS.

Smart Money Trap (SMT): Identify traps often utilized by smart money.

Timing: Ensure trades are entered during high-probability time windows.

Mitigation to the Leftside: Confirm whether price action aligns with prior mitigations.

Set Targets: Define and document logical take-profit or stop-loss levels.

2.Interactive Table Display

A table is dynamically created on the chart, showing all confirmations with their current state (checked or unchecked).

Users can choose the position of the table (top, middle, or bottom and left, center, or right) and customize its background color for better visibility.

3. Customization

All confirmations are toggled through the input settings, allowing traders to adapt the indicator to their unique strategies.

The display can be easily adjusted to match the trader’s preferences without cluttering the chart.

How to Use

1. Add the indicator to your chart.

2. Open the settings panel to activate the relevant confirmations for your analysis.

3. Use the Display Settings section to adjust the table's position and background color.

4. View the table on your chart to track selected confirmations in real-time.

Who Is This For?

This indicator is ideal for traders who:

Use Liquidity Inducent Theory strategy in their analysis.

Prefer a structured and systematic trading approach.

Need an on-chart tool to document confirmations without relying on external notes or tools.

Why Closed Source?

The logic behind the interactive table and confirmation system is specifically tailored to LIT practitioners and is not publicly available in existing open-source scripts. The closed-source nature of this script protects its unique implementation, ensuring the integrity and exclusivity of the tool.

Disclaimer

This indicator does not provide trading signals or strategies. It is a tool to document user-defined confirmations and should be used in conjunction with a thorough understanding of market behavior and risk management practices.

Logarithmic Regression AlternativeLogarithmic regression is typically used to model situations where growth or decay accelerates rapidly at first and then slows over time. Bitcoin is a good example.

𝑦 = 𝑎 + 𝑏 * ln(𝑥)

With this logarithmic regression (log reg) formula 𝑦 (price) is calculated with constants 𝑎 and 𝑏, where 𝑥 is the bar_index .

Instead of using the sum of log x/y values, together with the dot product of log x/y and the sum of the square of log x-values, to calculate a and b, I wanted to see if it was possible to calculate a and b differently.

In this script, the log reg is calculated with several different assumed a & b values, after which the log reg level is compared to each Swing. The log reg, where all swings on average are closest to the level, produces the final 𝑎 & 𝑏 values used to display the levels.

🔶 USAGE

The script shows the calculated logarithmic regression value from historical swings, provided there are enough swings, the price pattern fits the log reg model, and previous swings are close to the calculated Top/Bottom levels.

When the price approaches one of the calculated Top or Bottom levels, these levels could act as potential cycle Top or Bottom.

Since the logarithmic regression depends on swing values, each new value will change the calculation. A well-fitted model could not fit anymore in the future.

Swings are based on Weekly bars. A Top Swing, for example, with Swing setting 30, is the highest value in 60 weeks. Thirty bars at the left and right of the Swing will be lower than the Top Swing. This means that a confirmation is triggered 30 weeks after the Swing. The period will be automatically multiplied by 7 on the daily chart, where 30 becomes 210 bars.

Please note that the goal of this script is not to show swings rapidly; it is meant to show the potential next cycle's Top/Bottom levels.

🔹 Multiple Levels

The script includes the option to display 3 Top/Bottom levels, which uses different values for the swing calculations.

Top: 'high', 'maximum open/close' or 'close'

Bottom: 'low', 'minimum open/close' or 'close'

These levels can be adjusted up/down with a percentage.

Lastly, an "Average" is included for each set, which will only be visible when "AVG" is enabled, together with both Top and Bottom levels.

🔹 Notes

Users have to check the validity of swings; the above example only uses 1 Top Swing for its calculations, making the Top level unreliable.

Here, 1 of the Bottom Swings is pretty far from the bottom level, changing the swing settings can give a more reliable bottom level where all swings are close to that level.

Note the display was set at "Logarithmic", it can just as well be shown as "Regular"

In the example below, the price evolution does not fit the logarithmic regression model, where growth should accelerate rapidly at first and then slows over time.

Please note that this script can only be used on a daily timeframe or higher; using it at a lower timeframe will show a warning. Also, it doesn't work with bar-replay.

🔶 DETAILS

The code gathers data from historical swings. At the last bar, all swings are calculated with different a and b values. The a and b values which results in the smallest difference between all swings and Top/Bottom levels become the final a and b values.

The ranges of a and b are between -20.000 to +20.000, which means a and b will have the values -20.000, -19.999, -19.998, -19.997, -19.996, ... -> +20.000.

As you can imagine, the number of calculations is enormous. Therefore, the calculation is split into parts, first very roughly and then very fine.

The first calculations are done between -20 and +20 (-20, -19, -18, ...), resulting in, for example, 4.

The next set of calculations is performed only around the previous result, in this case between 3 (4-1) and 5 (4+1), resulting in, for example, 3.9. The next set goes even more in detail, for example, between 3.8 (3.9-0.1) and 4.0 (3.9 + 0.1), and so on.

1) -20 -> +20 , then loop with step 1 (result (example): 4 )

2) 4 - 1 -> 4 +1 , then loop with step 0.1 (result (example): 3.9 )

3) 3.9 - 0.1 -> 3.9 +0.1 , then loop with step 0.01 (result (example): 3.93 )

4) 3.93 - 0.01 -> 3.93 +0.01, then loop with step 0.001 (result (example): 3.928)

This ensures complicated calculations with less effort.

These calculations are done at the last bar, where the levels are displayed, which means you can see different results when a new swing is found.

Also, note that this indicator has been developed for a daily (or higher) timeframe chart.

🔶 SETTINGS

Three sets

High/Low

• color setting

• Swing Length settings for 'High' & 'Low'

• % adjustment for 'High' & 'Low'

• AVG: shows average (when both 'High' and 'Low' are enabled)

Max/Min (maximum open/close, minimum open/close)

• color setting

• Swing Length settings for 'Max' & 'Min'

• % adjustment for 'Max' & 'Min'

• AVG: shows average (when both 'Max' and 'Min' are enabled)

Close H/Close L (close Top/Bottom level)

• color setting

• Swing Length settings for 'Close H' & 'Close L'

• % adjustment for 'Close H' & 'Close L'

• AVG: shows average (when both 'Close H' and 'Close L' are enabled)

Show Dashboard, including Top/Bottom levels of the desired source and calculated a and b values.

Show Swings + Dot size

Kalman Filter Oscillator v4The Kalman Filter Oscillator v4 is an advanced tool designed to help traders and investors identify trends more effectively while reducing the impact of market noise. As the latest iteration in its development, this version integrates improvements that make it more adaptive and precise, catering to the challenges of today’s financial markets.

This indicator operates on the principle of the Kalman filter, a well-regarded mathematical approach used for estimating the state of a dynamic system. By filtering out random fluctuations, it smooths price data to provide clearer insights into underlying trends. Unlike traditional methods such as moving averages, which often lag and can miss rapid shifts, the Kalman Filter Oscillator is reactive in real time, making it particularly suited for dynamic markets.

Version v4 builds on earlier versions by offering a refined combination of short-term and long-term trend analysis. Through adjustable parameters, traders can balance sensitivity to immediate price changes with a broader perspective of the market direction. Additionally, the oscillator incorporates a unique feature that tracks a price’s position relative to its recent highs and lows, which enhances its ability to pinpoint potential turning points or key market conditions.

The indicator’s value lies in its adaptability and practicality. Traders can use it to confirm trends, identify overbought or oversold conditions, or smooth out erratic price movements, reducing the likelihood of false signals. By presenting information in a clear and actionable format, it allows users to make better-informed decisions with greater confidence.

As of late 2024, the Kalman Filter Oscillator v4 represents a sophisticated yet user-friendly advancement in trend analysis. While not a one-size-fits-all solution, it serves as a valuable component in a trader’s toolkit, complementing other strategies and enhancing overall market understanding.