MACD Volume Strategy (BBO + MACD State, Reversal Type)Overview

MACD Volume Strategy (BBO + MACD State, Reversal Type) is a momentum-based reversal system that combines MACD crossover logic with volume filtering to enhance signal accuracy and minimize noise. It aims to identify structural trend shifts and manage risk using predefined parameters.

※This strategy is for educational and research purposes only. All results are based on historical simulations and do not guarantee future performance.

Strategy Objectives

Identify early trend transitions with high probability

Filter entries using volume dynamics to validate momentum

Maintain continuous exposure using a reversal-style model

Apply a consistent 1:1.5 risk-to-reward ratio per trade

Key Features

Integrated MACD and volume oscillator filtering

Zero repainting (all signals confirmed on closed candles)

Automatic position flipping for seamless direction shifts

Stop-loss and take-profit based on recent structural highs/lows

Trading Rules

Long Entry Conditions

MACD crosses above the zero line (BBO Buy arrow)

Volume oscillator is positive (short EMA > long EMA)

MACD is above the signal line

Close any existing short and enter a new long

Short Entry Conditions

MACD crosses below the zero line (BBO Sell arrow)

Volume oscillator is positive

MACD is below the signal line

Close any existing long and enter a new short

Exit Rules

Take Profit (TP) = Entry ± (risk distance × 1.5)

Stop Loss (SL) = Recent swing low (for long) or high (for short)

Early Exit = Triggered when a reversal signal appears (flip logic)

Risk Management Parameters

Pair: ETH/USD

Timeframe: 10-minute

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted for sustainable practice)

Total Trades: 312 (backtest on selected dataset)

※Risk parameters are fully configurable and should be adjusted to suit each trader's personal setup and broker conditions.

Parameters & Configurations

Volume Short Length: 6

Volume Long Length: 12

MACD Fast Length: 11

MACD Slow Length: 21

Signal Smoothing: 10

Oscillator MA Type: SMA

Signal Line MA Type: SMA

Visual Support

Green arrow = Long entry

Red arrow = Short entry

MACD lines, signal line, and histogram

SL/TP markers plotted directly on the chart

Strategic Advantages & Uniqueness

Volume filtering eliminates low-participation, weak signals

Structurally aligned SL/TP based on recent market pivots

No repainting — decisions are made only on closed candles

Always in the market due to the reversal-style framework

Inspirations & Attribution

This strategy is inspired by the excellent work of:

Bitcoinblockchainonline – “BBO_Roxana_Signals MACD + vol”

Leveraging MACD zero-line cross and volume oscillator for intuitive signal generation.

HasanRifat – “MACD Fake Filter ”

Introduced a signal filter using MACD wave height averaging to reduce false positives.

This strategy builds upon those ideas to create a more automated, risk-aware, and technically adaptive system.

Summary

MACD Volume Strategy is a clean, logic-first automated trading system built for precision-seeking traders. It avoids discretionary bias and provides consistent signal logic under backtested historical conditions.

100% mechanical — no discretionary input required

Designed for high-confidence entries

Can be extended with filters, alerts, or trailing stops

※Strategy performance depends on market context. Past performance is not indicative of future results. Use with proper risk management and careful configuration.

Indicators and strategies

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

VWAP StrategyVWAP and volatility filters for structured intraday trades.

How the Strategy Works

1. VWAP Anchored to Session

VWAP is calculated from the start of each trading day.

Standard deviations are used to create bands above/below the VWAP.

2. Entry Triggers: Al Brooks H1/H2 and L1/L2

H1/H2 (Long Entry): Opens below 2nd lower deviation, closes above it.

L1/L2 (Short Entry): Opens above 2nd upper deviation, closes below it.

3. Volatility Filter (ATR)

Skips trades when deviation bands are too tight (< 3 ATRs).

4. Stop Loss

Based on the signal bar’s high/low ± stop buffer.

Longs: signalBarLow - stopBuffer

Shorts: signalBarHigh + stopBuffer

5. Take Profit / Exit Target

Exit logic is customizable per side:

VWAP, Deviation Band, or None

6. Safety Exit

Exits early if X consecutive bars go against the trade.

Longs: X red bars

Shorts: X green bars

Explanation of Strategy Inputs

- Stop Buffer: Distance from signal bar for stop-loss.

- Long/Short Exit Rule: VWAP, Deviation Band, or None

- Long/Short Target Deviation: Standard deviation for target exit.

- Enable Safety Exit: Toggle emergency exit.

- Opposing Bars: Number of opposing candles before safety exit.

- Allow Long/Short Trades: Enable or disable entry side.

- Show VWAP/Entry Bands: Toggle visual aids.

- Highlight Low Vol Zones: Orange shading for low volatility skips.

Tuning Tips

- Stop buffer: Use 1–5 points.

- Target deviation: Start with VWAP. In strong trends use 2nd deviation and turn off the counter-trend entry.

- Safety exit: 3 bars recommended.

- Disable short/long side to focus on one type of reversal.

Backtest Setup Suggestions

- initial_capital = 2000

- default_qty_value = 1 (fixed contracts or percent-of-equity)

GQT GPT - Volume-based Support & Resistance Zones V2搞钱兔,搞钱是为了更好的生活。

Title: GQT GPT - Volume-based Support & Resistance Zones V2

Overview:

This strategy is implemented in PineScript v5 and is designed to identify key support and resistance zones based on volume-driven fractal analysis on a 1-hour timeframe. It computes fractal high points (for resistance) and fractal low points (for support) using volume moving averages and specific price action criteria. These zones are visually represented on the chart with customizable lines and zone fills.

Trading Logic:

• Entry: The strategy initiates a long position when the price crosses into the support zone (i.e., when the price drops into a predetermined support area).

• Exit: The long position is closed when the price enters the resistance zone (i.e., when the price rises into a predetermined resistance area).

• Time Frame: Trading signals are generated solely from the 1-hour chart. The strategy is only active within a specified start and end date.

• Note: Only long trades are executed; short selling is not part of the strategy.

Visualization and Parameters:

• Support/Resistance Zones: The zones are drawn based on calculated fractal values, with options to extend the lines to the right for easier tracking.

• Customization: Users can configure the appearance, such as line style (solid, dotted, dashed), line width, colors, and label positions.

• Volume Filtering: A volume moving average threshold is used to confirm the fractal signals, enhancing the reliability of the support and resistance levels.

• Alerts: The strategy includes alert conditions for when the price enters the support or resistance zones, allowing for timely notifications.

⸻

搞钱兔,搞钱是为了更好的生活。

标题: GQT GPT - 基于成交量的支撑与阻力区间 V2

概述:

本策略使用 PineScript v5 实现,旨在基于成交量驱动的分形分析,在1小时级别的图表上识别关键支撑与阻力区间。策略通过成交量移动平均线和特定的价格行为标准计算分形高点(阻力)和分形低点(支撑),并以自定义的线条和区间填充形式直观地显示在图表上。

交易逻辑:

• 进场条件: 当价格进入支撑区间(即价格跌入预设支撑区域)时,策略在没有持仓的情况下发出做多信号。

• 离场条件: 当价格进入阻力区间(即价格上升至预设阻力区域)时,持有多头头寸则会被平仓。

• 时间范围: 策略的信号仅基于1小时级别的图表,并且仅在指定的开始日期与结束日期之间生效。

• 备注: 本策略仅执行多头交易,不进行空头操作。

可视化与参数设置:

• 支撑/阻力区间: 根据计算得出的分形值绘制支撑与阻力线,可选择将线条延伸至右侧,便于后续观察。

• 自定义选项: 用户可以调整线条样式(实线、点线、虚线)、线宽、颜色及标签位置,以满足个性化需求。

• 成交量过滤: 策略使用成交量移动平均阈值来确认分形信号,提高支撑和阻力区间的有效性。

• 警报功能: 当价格进入支撑或阻力区间时,策略会触发警报条件,方便用户及时关注市场变化。

⸻

Smart Money Pivot Strategy [Jason Kasei]This strategy is designed to identify key pivot points (Pivot High and Pivot Low) in the market and leverage the "Smart Money" concept to capture price breakout opportunities. It supports both long and short trades, offering customizable stop-loss (SL) and take-profit (TP) settings, while visually plotting pivot points and breakout signals on the chart.

Core Features

Pivot Point Detection:

Utilizes ta.pivothigh and ta.pivotlow functions to detect the highest (Pivot High) and lowest (Pivot Low) points within a specified period (default: 20 bars).

Trading Signals:

Long Signal: Triggered when the price breaks above a previous Pivot High, indicating a potential uptrend.

Short Signal: Triggered when the price breaks below a previous Pivot Low, indicating a potential downtrend.

How It Works

Detects Pivot High (PH) and Pivot Low (PL) over the specified period and records their price and time.

Triggers a long entry when the price breaks above a Pivot High and a short entry when it falls below a Pivot Low.

Sets exit conditions automatically based on predefined SL and TP percentages after entry.

Plots breakout points and levels on the chart for analysis.

Considerations

The strategy relies on accurate pivot point detection; adjust the period parameter based on market volatility.

In highly volatile markets, consider widening the stop loss to avoid frequent triggering.

Combine with other indicators or analysis methods to validate signals and avoid blind trading.

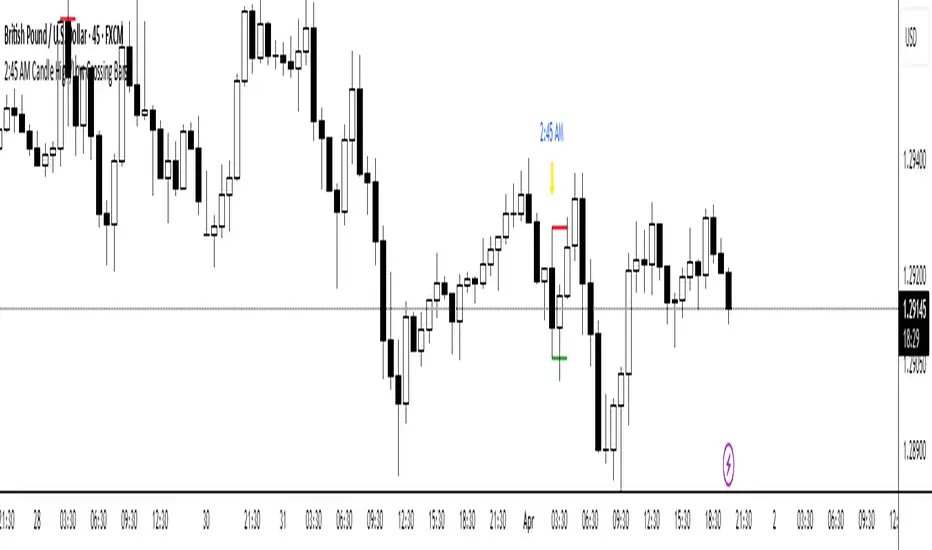

2:45 AM Candle High/Low Crossing Bars2:45 AM Candle High/Low Crossing Bars is an indicator that focuses on the trading view 2:45am NY TIME high and low indicating green for buy and red bars for sell, with the 2:45am new york time highlight/ If the next candle sweeps the low we buy while if it sweeps the high we sell, all time zoon must be the new York UTC time.

Supertrend + MACD CrossoverKey Elements of the Template:

Supertrend Settings:

supertrendFactor: Adjustable to control the sensitivity of the Supertrend.

supertrendATRLength: ATR length used for Supertrend calculation.

MACD Settings:

macdFastLength, macdSlowLength, macdSignalSmoothing: These settings allow you to fine-tune the MACD for better results.

Risk Management:

Stop-Loss: The stop-loss is based on the ATR (Average True Range), a volatility-based indicator.

Take-Profit: The take-profit is based on the risk-reward ratio (set to 3x by default).

Both stop-loss and take-profit are dynamic, based on ATR, which adjusts according to market volatility.

Buy and Sell Signals:

Buy Signal: Supertrend is bullish, and MACD line crosses above the Signal line.

Sell Signal: Supertrend is bearish, and MACD line crosses below the Signal line.

Visual Elements:

The Supertrend line is plotted in green (bullish) and red (bearish).

Buy and Sell signals are shown with green and red triangles on the chart.

Next Steps for Optimization:

Backtesting:

Run backtests on BTC in the 5-minute timeframe and adjust parameters (Supertrend factor, MACD settings, risk-reward ratio) to find the optimal configuration for the 60% win ratio.

Fine-Tuning Parameters:

Adjust supertrendFactor and macdFastLength to find more optimal values based on BTC's market behavior.

Tweak the risk-reward ratio to maximize profitability while maintaining a good win ratio.

Evaluate Market Conditions:

The performance of the strategy can vary based on market volatility. It may be helpful to evaluate performance in different market conditions or pair it with a filter like RSI or volume.

Let me know if you'd like further tweaks or explanations!

Triangular Hull Moving Average [BigBeluga X PineIndicators]This strategy is based on the original Triangular Hull Moving Average (THMA) + Volatility indicator by BigBeluga. Full credit for the concept and design goes to BigBeluga.

The strategy blends smoothed trend-following logic using a Triangular Hull Moving Average with dynamic volatility overlays, providing actionable trade signals with responsive visual feedback. It's designed for traders who want a non-lagging trend filter while also monitoring market volatility in real time.

How the Strategy Works

1. Triangular Hull Moving Average (THMA) Core

At its core, the strategy uses a Triangular Hull Moving Average (THMA) — a variation of the traditional Hull Moving Average with triple-smoothing logic:

It combines multiple weighted moving averages (WMAs) to create a faster and smoother trend line.

This reduces lag without compromising trend accuracy.

The THMA reacts more responsively to price movements than classic MAs.

THMA Formula:

thma(_src, _length) =>

ta.wma(ta.wma(_src,_length / 3) * 3 - ta.wma(_src, _length / 2) - ta.wma(_src, _length), _length)

This logic filters out short-term noise while still being sensitive to genuine trend shifts.

2. Volatility-Enhanced Candle Plotting

An optional volatility mode overlays the chart with custom candles that incorporate volatility bands:

Wicks expand and contract dynamically based on market volatility.

The volatility value is computed using a HMA of high-low range over a user-defined length.

The candle bodies reflect THMA values, while the wicks reflect the current volatility spread.

This feature allows traders to visually gauge the strength of price moves and anticipate possible breakouts or slowdowns.

3. Trend Reversal Signal Detection

The strategy identifies trend reversals when the THMA line crosses over/under its own past value:

A bullish signal is triggered when THMA crosses above its value from two bars ago.

A bearish signal is triggered when THMA crosses below its value from two bars ago.

These shifts are marked on the chart with triangle-shaped signals for clear visibility.

This logic helps detect momentum shifts early and enables reactive trade entries.

Trade Entry & Exit Logic

Trade Modes Supported

Users can choose between:

Only Long – Enters long trades only.

Only Short – Enters short trades only.

Long & Short – Enables both directions.

Entry Conditions

Long Entry:

Triggered when a bullish crossover is detected.

Active only if the strategy mode allows long trades.

Short Entry:

Triggered when a bearish crossover is detected.

Active only if the strategy mode allows short trades.

Exit Conditions

In Only Long mode, the strategy closes long positions when a bearish signal appears.

In Only Short mode, the strategy closes short positions when a bullish signal appears.

In Long & Short mode, the strategy does not auto-close positions — instead, it opens new positions on each confirmed signal.

Dashboard Visualization

In the bottom-right corner of the chart, a live dashboard displays:

The current trend direction (🢁 for bullish, 🢃 for bearish).

The current volatility level as a percentage.

This helps traders quickly assess market status and adjust their decisions accordingly.

Customization Options

THMA Length: Adjust how smooth or reactive the trend detection should be.

Volatility Toggle & Length: Enable or disable volatility visualization and set sensitivity.

Color Settings: Choose colors for up/down trend visualization.

Trade Direction Mode: Limit the strategy to long, short, or both types of trades.

Use Cases & Strategy Strengths

1. Trend Following

Use the THMA-based candles and triangle signals to enter with momentum. The indicator adapts quickly, reducing lag and improving trade timing.

2. Volatility Monitoring

Visualize the strength of the trend with volatility wicks. Use expanding bands to confirm breakouts and contracting ones to detect weakening moves.

3. Signal Confirmation

Combine this tool with other indicators or use the trend shift triangles as confirmations for manual entries.

Conclusion

The THMA + Volatility Strategy is a non-repainting trend-following system that integrates:

Triangular Hull MA for advanced trend detection.

Real-time volatility visualization.

Clear entry signals based on trend reversals.

Configurable trade direction settings.

It is ideal for traders who:

Prefer smoothed price analysis.

Want to follow trends with precision.

Value visual volatility feedback for breakout detection.

Full credit for the original concept and indicator goes to BigBeluga.

Litecoin Trailing-Stop StrategyAltcoins Trailing-Stop Strategy

This strategy is based on a momentum breakout approach using PKAMA (Powered Kaufman Adaptive Moving Average) as a trend filter, and a delayed trailing stop mechanism to manage risk effectively.

It has been designed and fine-tuned Altcoins, which historically shows consistent volatility patterns and clean trend structures, especially on intraday timeframes like 15m and 30m.

Strategy Logic:

Entry Conditions:

Long when PKAMA indicates an upward move

Short when PKAMA detects a downward trend

Minimum spacing of 30 bars between trades to avoid overtrading

Trailing Stop:

Activated only after a customizable delay (delayBars)

User can set trailing stop % and delay independently

Helps avoid premature exits due to short-term volatility

Customizable Parameters:

This strategy uses a custom implementation of PKAMA (Powered Kaufman Adaptive Moving Average), inspired by the work of alexgrover

PKAMA is a volatility-aware moving average that adjusts dynamically to market conditions, making it ideal for altcoins where trend strength and direction change frequently.

This script is for educational and experimental purposes only. It is not financial advice. Please test thoroughly before using it in live conditions, and always adapt parameters to your specific asset and time frame.

Feedback is welcome! Feel free to clone and adapt it for your own trading style.

Cycle Biologique Strategy // (\_/)

// ( •.•)

// (")_(")

//@fr33domz

Experimental Research: Cycle Biologique Strategy

Overview

The "Cycle Biologique Strategy" is an experimental trading algorithm designed to leverage periodic cycles in price movements by utilizing a sinusoidal function. This strategy aims to identify potential buy and sell signals based on the behavior of a custom-defined biological cycle.

Key Parameters

Cycle Length: This parameter defines the duration of the cycle, set by default to 30 periods. The user can adjust this value to optimize the strategy for different asset classes or market conditions.

Amplitude: The amplitude of the cycle influences the scale of the sinusoidal wave, allowing for customization in the sensitivity of buy and sell signals.

Offset: The offset parameter introduces phase shifts to the cycle, adjustable within a range of -360 to 360 degrees. This flexibility allows the strategy to align with various market rhythms.

Methodology

The core of the strategy lies in the calculation of a periodic cycle using a sinusoidal function.

Trading Signals

Buy Signal: A buy signal is generated when the cycle value crosses above zero, indicating a potential upward momentum.

Sell Signal: Conversely, a sell signal is triggered when the cycle value crosses below zero, suggesting a potential downtrend.

Execution

The strategy executes trades based on these signals:

Upon receiving a buy signal, the algorithm enters a long position.

When a sell signal occurs, the strategy closes the long position.

Visualization

To enhance user experience, the periodic cycle is plotted visually on the chart in blue, allowing traders to observe the cyclical nature of the strategy and its alignment with market movements.

Multi-EMA Crossover StrategyMulti-EMA Crossover Strategy

This strategy uses multiple exponential moving average (EMA) crossovers to identify bullish trends and execute long trades. The approach involves progressively stronger signals as different EMA pairs cross, indicating increasing bullish momentum. Each crossover triggers a long entry, and the intensity of bullish sentiment is reflected in the color of the bars on the chart. Conversely, bearish trends are represented by red bars.

Strategy Logic:

First Long Entry: When the 1-day EMA crosses above the 5-day EMA, it signals initial bullish momentum.

Second Long Entry: When the 3-day EMA crosses above the 10-day EMA, it confirms stronger bullish sentiment.

Third Long Entry: When the 5-day EMA crosses above the 20-day EMA, it indicates further trend strength.

Fourth Long Entry: When the 10-day EMA crosses above the 40-day EMA, it suggests robust long-term bullish momentum.

The bar colors reflect these conditions:

More blue bars indicate stronger bullish sentiment as more short-term EMAs are above their longer-term counterparts.

Red bars represent bearish conditions when short-term EMAs are below longer-term ones.

Example: Bitcoin Trading on a Daily Timeframe

Bullish Scenario:

Imagine Bitcoin is trading at $30,000 on March 31, 2025:

First Signal: The 1-day EMA crosses above the 5-day EMA at $30,000. This suggests initial upward momentum, prompting a small long entry.

Second Signal: A few days later, the 3-day EMA crosses above the 10-day EMA at $31,000. This confirms strengthening bullish sentiment; another long position is added.

Third Signal: The 5-day EMA crosses above the 20-day EMA at $32,500, indicating further upward trend development; a third long entry is executed.

Fourth Signal: Finally, the 10-day EMA crosses above the 40-day EMA at $34,000. This signals robust long-term bullish momentum; a fourth long position is entered.

Bearish Scenario:

Suppose Bitcoin reverses from $34,000 to $28,000:

The 1-day EMA crosses below the 5-day EMA at $33,500.

The 3-day EMA dips below the 10-day EMA at $32,000.

The 5-day EMA falls below the 20-day EMA at $30,000.

The final bearish signal occurs when the 10-day EMA drops below the 40-day EMA at $28,000.

The bars turn increasingly red as bearish conditions strengthen.

Advantages of This Strategy:

Progressive Confirmation: Multiple crossovers provide layered confirmation of trend strength.

Visual Feedback: Bar colors help traders quickly assess market sentiment and adjust positions accordingly.

Flexibility: Suitable for trending markets like Bitcoin during strong rallies or downturns.

Limitations:

Lagging Signals: EMAs are lagging indicators and may react slowly to sudden price changes.

False Breakouts: Crossovers in choppy markets can lead to whipsaws or false signals.

This strategy works best in trending markets and should be combined with additional risk management techniques, e.g., stop loss or optimal position sizes (Kelly Criterion).

02 SMC + BB Breakout (Improved)This strategy combines Smart Money Concepts (SMC) with Bollinger Band breakouts to identify potential trading opportunities. SMC focuses on identifying key price levels and market structure shifts, while Bollinger Bands help pinpoint overbought/oversold conditions and potential breakout points. The strategy also incorporates higher timeframe trend confirmation to filter out trades that go against the prevailing trend.

Key Components:

Bollinger Bands:

Calculated using a Simple Moving Average (SMA) of the closing price and a standard deviation multiplier.

The strategy uses the upper and lower bands to identify potential breakout points.

The SMA (basis) acts as a centerline and potential support/resistance level.

The fill between the upper and lower bands can be toggled by the user.

Higher Timeframe Trend Confirmation:

The strategy allows for optional confirmation of the current trend using a higher timeframe (e.g., daily).

It calculates the SMA of the higher timeframe's closing prices.

A bullish trend is confirmed if the higher timeframe's closing price is above its SMA.

This helps filter out trades that go against the prevailing long-term trend.

Smart Money Concepts (SMC):

Order Blocks:

Simplified as recent price clusters, identified by the highest high and lowest low over a specified lookback period.

These levels are considered potential areas of support or resistance.

Liquidity Zones (Swing Highs/Lows):

Identified by recent swing highs and lows, indicating areas where liquidity may be present.

The Swing highs and lows are calculated based on user defined lookback periods.

Market Structure Shift (MSS):

Identifies potential changes in market structure.

A bullish MSS occurs when the closing price breaks above a previous swing high.

A bearish MSS occurs when the closing price breaks below a previous swing low.

The swing high and low values used for the MSS are calculated based on the user defined swing length.

Entry Conditions:

Long Entry:

The closing price crosses above the upper Bollinger Band.

If higher timeframe confirmation is enabled, the higher timeframe trend must be bullish.

A bullish MSS must have occurred.

Short Entry:

The closing price crosses below the lower Bollinger Band.

If higher timeframe confirmation is enabled, the higher timeframe trend must be bearish.

A bearish MSS must have occurred.

Exit Conditions:

Long Exit:

The closing price crosses below the Bollinger Band basis.

Or the Closing price falls below 99% of the order block low.

Short Exit:

The closing price crosses above the Bollinger Band basis.

Or the closing price rises above 101% of the order block high.

Position Sizing:

The strategy calculates the position size based on a fixed percentage (5%) of the strategy's equity.

This helps manage risk by limiting the potential loss per trade.

Visualizations:

Bollinger Bands (upper, lower, and basis) are plotted on the chart.

SMC elements (order blocks, swing highs/lows) are plotted as lines, with user-adjustable visibility.

Entry and exit signals are plotted as shapes on the chart.

The Bollinger band fill opacity is adjustable by the user.

Trading Logic:

The strategy aims to capitalize on Bollinger Band breakouts that are confirmed by SMC signals and higher timeframe trend. It looks for breakouts that align with potential market structure shifts and key price levels (order blocks, swing highs/lows). The higher timeframe filter helps avoid trades that go against the overall trend.

In essence, the strategy attempts to identify high-probability breakout trades by combining momentum (Bollinger Bands) with structural analysis (SMC) and trend confirmation.

Key User-Adjustable Parameters:

Bollinger Bands Length

Standard Deviation Multiplier

Higher Timeframe

Higher Timeframe Confirmation (on/off)

SMC Elements Visibility (on/off)

Order block lookback length.

Swing lookback length.

Bollinger band fill opacity.

This detailed description should provide a comprehensive understanding of the strategy's logic and components.

***DISCLAIMER: This strategy is for educational purposes only. It is not financial advice. Past performance is not indicative of future results. Use at your own risk. Always perform thorough backtesting and forward testing before using any strategy in live trading.***

Strategy Stats [presentTrading]Hello! it's another weekend. This tool is a strategy performance analysis tool. Looking at the TradingView community, it seems few creators focus on this aspect. I've intentionally created a shared version. Welcome to share your idea or question on this.

█ Introduction and How it is Different

Strategy Stats is a comprehensive performance analytics framework designed specifically for trading strategies. Unlike standard strategy backtesting tools that simply show cumulative profits, this analytics suite provides real-time, multi-timeframe statistical analysis of your trading performance.

Multi-timeframe analysis: Automatically tracks performance metrics across the most recent time periods (last 7 days, 30 days, 90 days, 1 year, and 4 years)

Advanced statistical measures: Goes beyond basic metrics to include Information Coefficient (IC) and Sortino Ratio

Real-time feedback: Updates performance statistics with each new trade

Visual analytics: Color-coded performance table provides instant visual feedback on strategy health

Integrated risk management: Implements sophisticated take profit mechanisms with 3-step ATR and percentage-based exits

BTCUSD Performance

The table in the upper right corner is a comprehensive performance dashboard showing trading strategy statistics.

Note: While this presentation uses Vegas SuperTrend as the underlying strategy, this is merely an example. The Stats framework can be applied to any trading strategy. The Vegas SuperTrend implementation is included solely to demonstrate how the analytics module integrates with a trading strategy.

⚠️ Timeframe Limitations

Important: TradingView's backtesting engine has a maximum storage limit of 10,000 bars. When using this strategy stats framework on smaller timeframes such as 1-hour or 2-hour charts, you may encounter errors if your backtesting period is too long.

Recommended Timeframe Usage:

Ideal for: 4H, 6H, 8H, Daily charts and above

May cause errors on: 1H, 2H charts spanning multiple years

Not recommended for: Timeframes below 1H with long history

█ Strategy, How it Works: Detailed Explanation

The Strategy Stats framework consists of three primary components: statistical data collection, performance analysis, and visualization.

🔶 Statistical Data Collection

The system maintains several critical data arrays:

equityHistory: Tracks equity curve over time

tradeHistory: Records profit/loss of each trade

predictionSignals: Stores trade direction signals (1 for long, -1 for short)

actualReturns: Records corresponding actual returns from each trade

For each closed trade, the system captures:

float tradePnL = strategy.closedtrades.profit(tradeIndex)

float tradeReturn = strategy.closedtrades.profit_percent(tradeIndex)

int tradeType = entryPrice < exitPrice ? 1 : -1 // Direction

🔶 Performance Metrics Calculation

The framework calculates several key performance metrics:

Information Coefficient (IC):

The correlation between prediction signals and actual returns, measuring forecast skill.

IC = Correlation(predictionSignals, actualReturns)

Where Correlation is the Pearson correlation coefficient:

Correlation(X,Y) = (nΣXY - ΣXY) / √

Sortino Ratio:

Measures risk-adjusted return focusing only on downside risk:

Sortino = (Avg_Return - Risk_Free_Rate) / Downside_Deviation

Where Downside Deviation is:

Downside_Deviation = √

R_i represents individual returns, T is the target return (typically the risk-free rate), and n is the number of observations.

Maximum Drawdown:

Tracks the largest percentage drop from peak to trough:

DD = (Peak_Equity - Trough_Equity) / Peak_Equity * 100

🔶 Time Period Calculation

The system automatically determines the appropriate number of bars to analyze for each timeframe based on the current chart timeframe:

bars_7d = math.max(1, math.round(7 * barsPerDay))

bars_30d = math.max(1, math.round(30 * barsPerDay))

bars_90d = math.max(1, math.round(90 * barsPerDay))

bars_365d = math.max(1, math.round(365 * barsPerDay))

bars_4y = math.max(1, math.round(365 * 4 * barsPerDay))

Where barsPerDay is calculated based on the chart timeframe:

barsPerDay = timeframe.isintraday ?

24 * 60 / math.max(1, (timeframe.in_seconds() / 60)) :

timeframe.isdaily ? 1 :

timeframe.isweekly ? 1/7 :

timeframe.ismonthly ? 1/30 : 0.01

🔶 Visual Representation

The system presents performance data in a color-coded table with intuitive visual indicators:

Green: Excellent performance

Lime: Good performance

Gray: Neutral performance

Orange: Mediocre performance

Red: Poor performance

█ Trade Direction

The Strategy Stats framework supports three trading directions:

Long Only: Only takes long positions when entry conditions are met

Short Only: Only takes short positions when entry conditions are met

Both: Takes both long and short positions depending on market conditions

█ Usage

To effectively use the Strategy Stats framework:

Apply to existing strategies: Add the performance tracking code to any strategy to gain advanced analytics

Monitor multiple timeframes: Use the multi-timeframe analysis to identify performance trends

Evaluate strategy health: Review IC and Sortino ratios to assess predictive power and risk-adjusted returns

Optimize parameters: Use performance data to refine strategy parameters

Compare strategies: Apply the framework to multiple strategies to identify the most effective approach

For best results, allow the strategy to generate sufficient trade history for meaningful statistical analysis (at least 20-30 trades).

█ Default Settings

The default settings have been carefully calibrated for cryptocurrency markets:

Performance Tracking:

Time periods: 7D, 30D, 90D, 1Y, 4Y

Statistical measures: Return, Win%, MaxDD, IC, Sortino Ratio

IC color thresholds: >0.3 (green), >0.1 (lime), <-0.1 (orange), <-0.3 (red)

Sortino color thresholds: >1.0 (green), >0.5 (lime), <0 (red)

Multi-Step Take Profit:

ATR multipliers: 2.618, 5.0, 10.0

Percentage levels: 3%, 8%, 17%

Short multiplier: 1.5x (makes short take profits more aggressive)

Stop loss: 20%

RSI Pro+ (Bear market, financial crisis and so on EditionIn markets defined by volatility, fear, and uncertainty – the battlegrounds of bear markets and financial crises – you need tools forged in resilience. Introducing RSI Pro+, a strategy built upon a legendary indicator born in 1978, yet engineered with modern visual clarity to remain devastatingly effective even in the chaotic financial landscapes of 3078.

This isn't about complex algorithms predicting the unpredictable. It's about harnessing the raw, time-tested power of the Relative Strength Index (RSI) to identify potential exhaustion points and capitalize on oversold conditions. RSI Pro+ cuts through the noise, providing clear, actionable signals when markets might be poised for a relief bounce or reversal.

Core Technology (The 1978 Engine):

RSI Crossover Entry: The strategy initiates a LONG position when the RSI (default period 11) crosses above a user-defined low threshold (default 30). This classic technique aims to enter when selling pressure may be waning, offering potential entry points during sharp downturns or periods of consolidation after a fall.

Modern Enhancements (The 3078 Cockpit):

RSI Pro+ isn't just about the signal; it's about providing a professional-grade visual experience directly on your chart:

Entry Bar Highlight: A subtle background flash on the chart signals the exact bar where the RSI crossover condition is met, alerting you to potential entry opportunities.

Trade Bar Coloring: Once a trade is active, the price bars are subtly colored, giving you immediate visual confirmation that the strategy is live in the market.

Entry Price Line: A clear, persistent line marks your exact average entry price for the duration of the trade, serving as a crucial visual anchor.

Take Profit Line: Your calculated Take Profit target is plotted as a distinct line, keeping your objective clearly in sight.

Custom Entry Marker: A precise shape (▲) appears below the bar where the trade entry was actually executed, pinpointing the start of the position.

On-Chart Info Table (HUD): A clean, customizable Heads-Up Display appears when a trade is active, showing vital information at a glance:

Entry Price: Your position's average cost basis.

TP Target: The calculated price level for your Take Profit exit.

Current PnL%: Real-time Profit/Loss percentage for the open trade.

Full Customization: Nearly every aspect is configurable via the settings menu:

RSI Period & Crossover Level

Take Profit Percentage

Toggle ALL visual enhancements on/off individually

Position the Info Table wherever you prefer on the chart.

How to Use RSI Pro+:

Add to Chart: Apply the "RSI Pro+ (Bear market...)" strategy to your TradingView chart. Ensure any previous versions are removed.

Access Settings: Click the cogwheel icon (⚙️) next to the strategy name on your chart.

Configure Inputs (Crucial Step):

RSI Crossover Level: This is key. The default (30) targets standard oversold conditions. In severe downturns, you might experiment with lower levels (e.g., 25, 20) or higher ones (e.g., 40) depending on the asset and timeframe. Observe where RSI(11) typically bottoms out on your chart.

Take Profit Percentage (%): Define your desired profit target per trade (e.g., enter 0.5 for 0.5%, 1.0 for 1%). The default is a very small 0.11%.

RSI Period: While default is 11, you can adjust this (e.g., the standard 14).

Visual Enhancements: Enable or disable the visual features (background highlights, bar coloring, lines, markers, table) according to your preference using the checkboxes. Adjust table position.

Observe & Backtest: Watch how the strategy behaves on your chosen asset and timeframe. Use TradingView's Strategy Tester to analyze historical performance based on your settings. No strategy works perfectly everywhere; testing is essential.

Important Considerations:

Risk Management: This specific script version focuses on a Take Profit exit. It does not include an explicit Stop Loss. You MUST manage risk through appropriate position sizing, potentially adding a Stop Loss manually, or by modifying the script.

Oversold ≠ Reversal: An RSI crossover is an indicator of potential exhaustion, not a guarantee of a price reversal.

Fixed TP: A fixed percentage TP ensures small wins but may exit before larger potential moves.

Backtesting Limitations: Past performance does not guarantee future results.

RSI Pro+ strips away complexity to focus on a robust, time-honored principle, enhanced with modern visuals for the discerning trader navigating today's (and tomorrow's) challenging markets

PowerZone Trading StrategyExplanation of the PowerZone Trading Strategy for Your Users

The PowerZone Trading Strategy is an automated trading strategy that detects strong price movements (called "PowerZones") and generates signals to enter a long (buy) or short (sell) position, complete with predefined take profit and stop loss levels. Here’s how it works, step by step:

1. What is a PowerZone?

A "PowerZone" (PZ) is a zone on the chart where the price has shown a significant and consistent movement over a specific number of candles (bars). There are two types:

Bullish PowerZone (Bullish PZ): Occurs when the price rises consistently over several candles after an initial bearish candle.

Bearish PowerZone (Bearish PZ): Occurs when the price falls consistently over several candles after an initial bullish candle.

The code analyzes:

A set number of candles (e.g., 5, adjustable via "Periods").

A minimum percentage move (adjustable via "Min % Move for PowerZone") to qualify as a strong zone.

Whether to use the full candle range (highs and lows) or just open/close prices (toggle with "Use Full Range ").

2. How Does It Detect PowerZones?

Bullish PowerZone:

Looks for an initial bearish candle (close below open).

Checks that the next candles (e.g., 5) are all bullish (close above open).

Ensures the total price movement exceeds the minimum percentage set.

Defines a range: from the high (or open) to the low of the initial candle.

Bearish PowerZone:

Looks for an initial bullish candle (close above open).

Checks that the next candles are all bearish (close below open).

Ensures the total price movement exceeds the minimum percentage.

Defines a range: from the high to the low (or close) of the initial candle.

These zones are drawn on the chart with lines: green or white for bullish, red or blue for bearish, depending on the color scheme ("DARK" or "BRIGHT").

3. When Does It Enter a Trade?

The strategy waits for a breakout from the PowerZone range to enter a trade:

Buy (Long): When the price breaks above the high of a Bullish PowerZone.

Sell (Short): When the price breaks below the low of a Bearish PowerZone.

The position size is set to 100% of available equity (adjustable in the code).

4. Take Profit and Stop Loss

Take Profit (TP): Calculated as a multiple (adjustable via "Take Profit Factor," default 1.5) of the PowerZone height. For example:

For a buy, TP = Entry price + (PZ height × 1.5).

For a sell, TP = Entry price - (PZ height × 1.5).

Stop Loss (SL): Calculated as a multiple (adjustable via "Stop Loss Factor," default 1.0) of the PZ height, placed below the range for buys or above for sells.

5. Visualization on the Chart

PowerZones are displayed with lines on the chart (you can hide them with "Show Bullish Channel" or "Show Bearish Channel").

An optional info panel ("Show Info Panel") displays key levels: PZ high and low, TP, and SL.

You can also enable brief documentation on the chart ("Show Documentation") explaining the basic rules.

6. Alerts

The code generates automatic alerts in TradingView:

For a bullish breakout: "Bullish PowerZone Breakout - LONG!"

For a bearish breakdown: "Bearish PowerZone Breakdown - SHORT!"

7. Customization

You can tweak:

The number of candles to detect a PZ ("Periods").

The minimum percentage move ("Min % Move").

Whether to use highs/lows or just open/close ("Use Full Range").

The TP and SL factors.

The color scheme and what elements to display on the chart.

Practical Example

Imagine you set "Periods = 5" and "Min % Move = 2%":

An initial bearish candle appears, followed by 5 consecutive bullish candles.

The total move exceeds 2%.

A Bullish PowerZone is drawn with a high and low.

If the price breaks above the high, you enter a long position with a TP 1.5 times the PZ height and an SL equal to the height below.

The system executes the trade and exits automatically at TP or SL.

Conclusion

This strategy is great for capturing strong price movements after consolidation or momentum zones. It’s automated, visual, and customizable, making it useful for both beginner and advanced traders. Try it out and adjust it to fit your trading style!

External Signals Strategy TesterExternal Signals Strategy Tester

This strategy is designed to help you backtest external buy/sell signals coming from another indicator on your chart. It is a flexible and powerful tool that allows you to simulate real trading based on signals generated by any indicator, using input.source connections.

🔧 How It Works

Instead of generating signals internally, this strategy listens to two external input sources:

One for buy signals

One for sell signals

These sources can be connected to the plots from another indicator (for example, custom indicators, signal lines, or logic-based plots).

To use this:

Add your indicator to the chart (it must be visible on the same pane as this strategy).

Open the settings of the strategy.

In the fields Buy Signal and Sell Signal, select the appropriate plot (line, value, etc.) from the indicator that represents the buy/sell logic.

The strategy will open positions when the selected buy signal crosses above 0, and sell signal crosses above 0.

This logic can be easily adapted by modifying the crossover rule inside the script if your signal style is different.

⚙️ Features Included

✅ Configurable trade direction:

You can choose whether to allow long trades, short trades, or both.

✅ Optional close on opposite signal:

When enabled, the strategy will exit the current position if an opposite signal appears.

✅ Optional full position reversal:

When enabled, the strategy will close the current position and immediately open an opposite one on the reverse signal.

✅ Risk Management Tools:

You can define:

Take Profit (TP): Position will be closed once the specified profit (in %) is reached.

Stop Loss (SL): Position will be closed if the price drops to the specified loss level (in %).

BreakEven (BE): Once the specified profit threshold is reached, the strategy will move the stop-loss to the entry price.

📌 If any of these values (TP, SL, BE) are set to 0, the feature is disabled and will not be applied.

🧪 Best Use Cases

Backtesting signals from custom indicators, without rewriting the logic into a strategy.

Comparing the performance of different signal sources.

Testing external indicators with optional position management logic.

Validating strategies using external filters, oscillators, or trend signals.

📌 Final Notes

You can visualize where the strategy detected buy/sell signals using green/red markers on the chart.

All parameters are customizable through the strategy settings panel.

This strategy does not repaint, and it processes signals in real-time only (no lookahead bias).

Long Term Profitable Swing | AbbasA Story of a Profitable Swing Trading Strategy

Imagine you're sailing across the ocean, looking for the perfect wave to ride. Swing trading is quite similar—you're navigating the stock market, searching for the ideal moments to enter and exit trades. This strategy, created by Abbas, helps you find those waves and ride them effectively to profitable outcomes.

🌊 Finding the Perfect Wave (Entry)

Our journey begins with two simple signs that tell us a great trading opportunity is forming:

- Moving Averages: We use two lines that follow price trends—the faster one (EMA 16) reacts quickly to recent price moves, and the slower one (EMA 30) gives us a longer-term perspective. When the faster line crosses above the slower line, it's like a clear signal saying, "Hey! The wave is rising, and prices might move higher!"

- RSI Momentum: Next, we check a tool called the RSI, which measures momentum (how strongly prices are moving). If the RSI number is above 50, it means there's enough strength behind this rising wave to carry us forward.

When both signals appear together, that's our green light. It's time to jump on our surfboard and start riding this promising wave.

⚓ Safely Riding the Wave (Risk Management)

While we're riding this wave, we want to ensure we're safe from sudden surprises. To do this, we use something called the Average True Range (ATR), which measures how volatile (or bumpy) the price movements are:

- Stop-Loss: To avoid falling too hard, we set a safety line (stop-loss) 8 times the ATR below our entry price. This helps ensure we exit if the wave suddenly turns against us, protecting us from heavy losses.

- Take Profit: We also set a goal to exit the trade at 11 times the ATR above our entry. This way, we capture significant profits when the wave reaches a nice high point.

🌟 Multiple Rides, Bigger Adventures

This strategy allows us to take multiple positions simultaneously—like riding several waves at once, up to 5. Each trade we make uses only 10% of our trading capital, keeping risks manageable and giving us multiple opportunities to win big.

🗺️ Easy to Follow Settings

Here are the basic settings we use:

- Fast EMA**: 16

- Slow EMA**: 30

- RSI Length**: 9

- RSI Threshold**: 50

- ATR Length**: 21

- ATR Stop-Loss Multiplier**: 8

- ATR Take-Profit Multiplier**: 11

These settings are flexible—you can adjust them to better suit different markets or your personal trading style.

🎉 Riding the Waves of Success

This simple yet powerful swing trading approach helps you confidently enter trades, clearly know when to exit, and effectively manage your risk. It’s a reliable way to ride market waves, capture profits, and minimize losses.

Happy trading, and may you find many profitable waves to ride! 🌊✨

Please test, and take into account that it depends on taking multiple longs within the swing, and you only get to invest 25/30% of your equity.

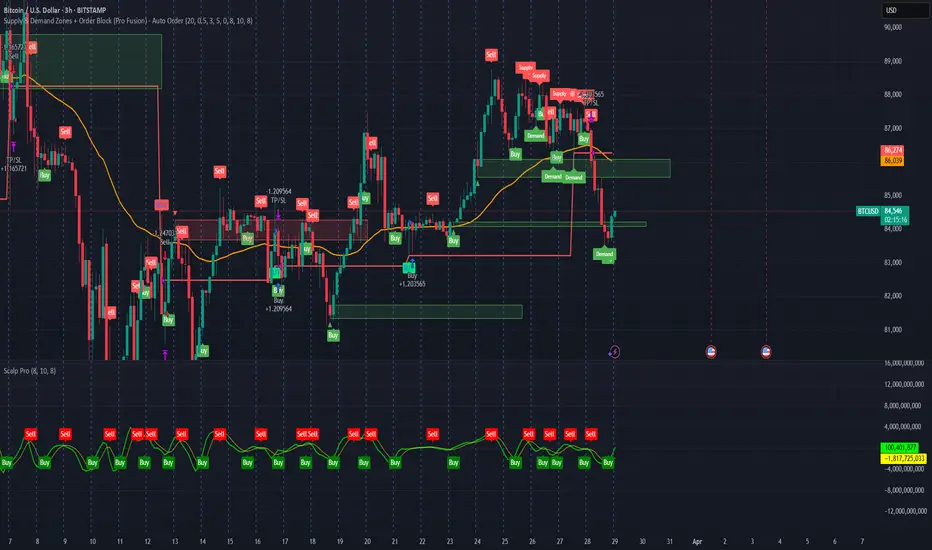

Supply & Demand Zones + Order Block (Pro Fusion) - Auto Order Strategy Title:

Smart Supply & Demand Zones + Order Block Auto Strategy with ScalpPro (Buy-Focused)

📄 Strategy Description:

This strategy combines the power of Supply & Demand Zone analysis, Order Block detection, and an enhanced Scalp Pro momentum filter, specifically designed for automated decision-making based on high-volume breakouts.

✅ Key Features:

Auto Entry (Buy Only) Based on Breakouts

Automatically enters a Buy position when the price breaks out of a valid demand zone, confirmed by EMA 50 trend and volume spike.

Order Block Logic

Identifies bullish and bearish order blocks using consecutive candle structures and significant price movement.

Dynamic Stop Loss & Trailing Stop

Implements a trailing stop once price moves in profit, along with static initial stop loss for risk management.

Clear Visual Labels & Alerts

Displays BUY/SELL, Demand/Supply, and Order Block labels directly on the chart. Alerts trigger on valid breakout signals.

Scalp Pro Momentum Filter (Optimized)

Uses a modified MACD-style momentum indicator to confirm trend strength and filter out weak signals.

EMA 10/55/200 - LONG ONLY MTF (4h with 1D & 1W confirmation)Title: EMA 10/55/200 - Long Only Multi-Timeframe Strategy (4h with 1D & 1W confirmation)

Description:

This strategy is designed for trend-following long entries using a combination of exponential moving averages (EMAs) on the 4-hour chart, confirmed by higher timeframe trends from the daily (1D) and weekly (1W) charts.

🔍 How It Works

🔹 Entry Conditions (4h chart):

EMA 10 crosses above EMA 55 and price is above EMA 55

OR

EMA 55 crosses above EMA 200

OR

EMA 10 crosses above EMA 500

These entries indicate short-term momentum aligning with medium/long-term trend strength.

🔹 Confirmation (multi-timeframe alignment):

Daily (1D): EMA 55 is above EMA 200

Weekly (1W): EMA 55 is above EMA 200

This ensures that we only enter long trades when the higher timeframes support an uptrend, reducing false signals during sideways or bearish markets.

🛑 Exit Conditions

Bearish crossover of EMA 10 below EMA 200 or EMA 500

Stop Loss: 5% below entry price

⚙️ Backtest Settings

Capital allocation per trade: 10% of equity

Commission: 0.1%

Slippage: 2 ticks

These are realistic conditions for crypto, forex, and stocks.

📈 Best Used On

Timeframe: 4h

Instruments: Trending markets like BTC/ETH, FX majors, or growth stocks

Works best in volatile or trending environments

⚠️ Disclaimer

This is a backtest tool and educational resource. Always validate on demo accounts before applying to real capital. Do your own due diligence.

Dow Theory Trend StrategyDow Theory Trend Strategy (Pine Script)

Overview

This Pine Script implements a trading strategy based on the core principles of Dow Theory. It visually identifies trends (uptrend, downtrend) by analyzing pivot highs and lows and executes trades when the trend direction changes. This script is an improved version that features refined trend determination logic and strategy implementation.

Core Concept: Dow Theory

The script uses a fundamental Dow Theory concept for trend identification:

Uptrend: Characterized by a series of Higher Highs (HH) and Higher Lows (HL).

Downtrend: Characterized by a series of Lower Highs (LH) and Lower Lows (LL).

How it Works

Pivot Point Detection:

It uses the built-in ta.pivothigh() and ta.pivotlow() functions to identify significant swing points (potential highs and lows) in the price action.

The pivotLookback input determines the number of bars to the left and right required to confirm a pivot. Note that this introduces a natural lag (equal to pivotLookback bars) before a pivot is confirmed.

Improved Trend Determination:

The script stores the last two confirmed pivot highs and the last two confirmed pivot lows.

An Uptrend (trendDirection = 1) is confirmed only when the latest pivot high is higher than the previous one (HH) AND the latest pivot low is higher than the previous one (HL).

A Downtrend (trendDirection = -1) is confirmed only when the latest pivot high is lower than the previous one (LH) AND the latest pivot low is lower than the previous one (LL).

Key Improvement: If neither a clear uptrend nor a clear downtrend is confirmed based on the latest pivots, the script maintains the previous trend state (trendDirection := trendDirection ). This differs from simpler implementations that might switch to a neutral/range state (e.g., trendDirection = 0) more frequently. This approach aims for smoother trend following, acknowledging that trends often persist through periods without immediate new HH/HL or LH/LL confirmations.

Trend Change Detection:

The script monitors changes in the trendDirection variable.

changedToUp becomes true when the trend shifts to an Uptrend (from Downtrend or initial state).

changedToDown becomes true when the trend shifts to a Downtrend (from Uptrend or initial state).

Visualizations

Background Color: The chart background is colored to reflect the currently identified trend:

Blue: Uptrend (trendDirection == 1)

Red: Downtrend (trendDirection == -1)

Gray: Initial state or undetermined (trendDirection == 0)

Pivot Points (Optional): Small triangles (shape.triangledown/shape.triangleup) can be displayed above pivot highs and below pivot lows if showPivotPoints is enabled.

Trend Change Signals (Optional): Labels ("▲ UP" / "▼ DOWN") can be displayed when a trend change is confirmed (changedToUp / changedToDown) if showTrendChange is enabled. These visually mark the potential entry points for the strategy.

Strategy Logic

Entry Conditions:

Enters a long position (strategy.long) using strategy.entry("L", ...) when changedToUp becomes true.

Enters a short position (strategy.short) using strategy.entry("S", ...) when changedToDown becomes true.

Position Management: The script uses strategy.entry(), which automatically handles position reversal. If the strategy is long and a short signal occurs, strategy.entry() will close the long position and open a new short one (and vice-versa).

Inputs

pivotLookback: The number of bars on each side to confirm a pivot high/low. Higher values mean pivots are confirmed later but may be more significant.

showPivotPoints: Toggle visibility of pivot point markers.

showTrendChange: Toggle visibility of the trend change labels ("▲ UP" / "▼ DOWN").

Key Improvements from Original

Smoother Trend Logic: The trend state persists unless a confirmed reversal pattern (opposite HH/HL or LH/LL) occurs, reducing potential whipsaws in choppy markets compared to logic that frequently resets to neutral.

Strategy Implementation: Converted from a pure indicator to a strategy capable of executing backtests and potentially live trades based on the Dow Theory trend changes.

Disclaimer

Dow Theory signals are inherently lagging due to the nature of pivot confirmation.

The effectiveness of the strategy depends heavily on the market conditions and the chosen pivotLookback setting.

This script serves as a basic template. Always perform thorough backtesting and implement proper risk management (e.g., stop-loss, take-profit, position sizing) before considering any live trading.

Arbitrage Spot-Futures Don++Strategy: Spot-Futures Arbitrage Don++

This strategy has been designed to detect and exploit arbitrage opportunities between the Spot and Futures markets of the same trading pair (e.g. BTC/USDT). The aim is to take advantage of price differences (spreads) between the two markets, while minimizing risk through dynamic position management.

[Operating principle

The strategy is based on calculating the spread between Spot and Futures prices. When this spread exceeds a certain threshold (positive or negative), reverse positions are opened simultaneously on both markets:

- i] Long Spot + Short Futures when the spread is positive.

- i] Short Spot + Long Futures when the spread is negative.

Positions are closed when the spread returns to a value close to zero or after a user-defined maximum duration.

[Strategy strengths

1. Adaptive thresholds :

- Entry/exit thresholds can be dynamic (based on moving averages and standard deviations) or fixed, offering greater flexibility to adapt to market conditions.

2. Robust data management :

- The script checks the validity of data before executing calculations, thus avoiding errors linked to missing or invalid data.

3. Risk limitation :

- A position size based on a percentage of available capital (default 10%) limits exposure.

- A time filter limits the maximum duration of positions to avoid losses due to persistent spreads.

4. Clear visualization :

- Charts include horizontal lines for entry/exit thresholds, as well as visual indicators for spread and Spot/Futures prices.

5. Alerts and logs :

- Alerts are triggered on entries and exits to inform the user in real time.

[Points for improvement or completion

Although this strategy is functional and robust, it still has a few limitations that could be addressed in future versions:

1. [Limited historical data :

- TradingView does not retrieve real-time data for multiple symbols simultaneously. This can limit the accuracy of calculations, especially under conditions of high volatility.

2. [Lack of liquidity management :

- The script does not take into account the volumes available on the order books. In conditions of low liquidity, it may be difficult to execute orders at the desired prices.

3. [Non-dynamic transaction costs :

- Transaction costs (exchange fees, slippage) are set manually. A dynamic integration of these costs via an external API would be more realistic.

4. User-dependency for symbols :

- Users must manually specify Spot and Futures symbols. Automatic symbol validation would be useful to avoid configuration errors.

5. Lack of advanced backtesting :

- Backtesting is based solely on historical data available on TradingView. An implementation with third-party data (via an API) would enable the strategy to be tested under more realistic conditions.

6. [Parameter optimization :

- Certain parameters (such as analysis period or spread thresholds) could be optimized for each specific trading pair.

[How can I contribute?

If you'd like to help improve this strategy, here are a few ideas:

1. Add additional filters:

- For example, a filter based on volume or volatility to avoid false signals.

2. Integrate dynamic costs:

- Use an external API to retrieve actual costs and adjust thresholds accordingly.

3. Improve position management:

- Implement hedging or scalping mechanisms to maximize profits.

4. Test on other pairs:

- Evaluate the strategy's performance on other assets (ETH, SOL, etc.) and adjust parameters accordingly.

5. Publish backtesting results :

- Share detailed analyses of the strategy's performance under different market conditions.

[Conclusion

This Spot-Futures arbitrage strategy is a powerful tool for exploiting price differentials between markets. Although it is already functional, it can still be improved to meet more complex trading scenarios. Feel free to test, modify and share your ideas to make this strategy even more effective!

[Thank you for contributing to this open-source community!

If you have any questions or suggestions, please feel free to comment or contact me directly.

Adaptive KDJ (MTF)Hey guys,

this is an adaptive MTF KDJ oscillator.

Pick up to 3 different timeframes, choose a weighting if you want and enjoy the beautiful signals it will show you.

The length of every timeframe is adaptive and based of the timeframe's ATR.

The plot shows the smoothed average of the 3 KDJ values.

Large triangles show KDJ crossings.

Small triangles show anticipations of possible crossings.

I found out it works best with 1m, 5m, 15m and weighting=1 for forex scalping in 1m.

Use other indicators for confluence.

Buy on 5% dip strategy with time adjustment

This script is a strategy called "Buy on 5% Dip Strategy with Time Adjustment 📉💡," which detects a 5% drop in price and triggers a buy signal 🔔. It also automatically closes the position once the set profit target is reached 💰, and it has additional logic to close the position if the loss exceeds 14% after holding for 230 days ⏳.

Strategy Explanation

Buy Condition: A buy signal is triggered when the price drops 5% from the highest price reached 🔻.

Take Profit: The position is closed when the price hits a 1.22x target from the average entry price 📈.

Forced Sell Condition: If the position is held for more than 230 days and the loss exceeds 14%, the position is automatically closed 🚫.

Leverage & Capital Allocation: Leverage is adjustable ⚖️, and you can set the percentage of capital allocated to each trade 💸.

Time Limits: The strategy allows you to set a start and end time ⏰ for trading, making the strategy active only within that specific period.

Code Credits and References

Credits: This script utilizes ideas and code from @QuantNomad and jangdokang for the profit table and algorithm concepts 🔧.

Sources:

Monthly Performance Table Script by QuantNomad:

ZenAndTheArtOfTrading's Script:

Strategy Performance

This strategy provides risk management through take profit and forced sell conditions and includes a performance table 📊 to track monthly and yearly results. You can compare backtest results with real-time performance to evaluate the strategy's effectiveness.

The performance numbers shown in the backtest reflect what would have happened if you had used this strategy since the launch date of the SOXL (the Direxion Daily Semiconductor Bull 3x Shares ETF) 📅. These results are not hypothetical but based on actual performance from the day of the ETF’s launch 📈.

Caution ⚠️

No Guarantee of Future Results: The results are based on historical performance from the launch of the SOXL ETF, but past performance does not guarantee future results. It’s important to approach with caution when applying it to live trading 🔍.

Risk Management: Leverage and capital allocation settings are crucial for managing risk ⚠️. Make sure to adjust these according to your risk tolerance ⚖️.