Hammer + EMA Strategy with Tick-based SL/TPWhat This Script Does:

Detects Hammer (bullish reversal) and Inverted Hammer (bearish reversal) patterns

Requires a simple trend context (using 2 bars back)

Confirms price position relative to EMA 50

Applies tick-based SL and TP

Plots buy/sell signals on chart with emoji labels

Indicators and strategies

Volatility Pulse with Dynamic ExitVolatility Pulse with Dynamic Exit

Overview

This strategy, Volatility Pulse with Dynamic Exit, is designed to capture impulsive price moves following volatility expansions, while ensuring risk is managed dynamically. It avoids trades during low-volatility periods and uses momentum confirmation to enter positions. Additionally, it features a time-based forced exit system to limit overexposure.

How It Works

A position is opened when the current ATR (Average True Range) significantly exceeds its 20-period average, signaling a volatility expansion.

To confirm the move is directional and not random noise, the strategy checks for momentum: the close must be above/below the close of 20 bars ago.

Low volatility zones are filtered out to avoid chop and poor trade entries.

Upon entry, a dynamic stop-loss is set at 1x ATR, while take-profit is set at 2x ATR, offering a 2:1 reward-to-risk ratio.

If the position remains open for more than 42 bars, it is forcefully closed, even if targets are not hit. This prevents long-lasting, stagnant trades.

Key Features

✅ Volatility-based breakout detection

✅ Momentum confirmation filter

✅ Dynamic stop-loss and take-profit based on real-time ATR

✅ Time-based forced exit (42 bars max holding)

✅ Low-volatility environment filter

✅ Realistic settings with 0.05% commission and slippage included

Parameters Explanation

ATR Length (14): Captures recent volatility over ~2 weeks (14 candles).

Momentum Lookback (20): Ensures meaningful price move confirmation.

Volatility Expansion Threshold (0.5x): Strategy activates only when ATR is at least 50% above its average.

Minimum ATR Filter (1.0x): Avoids entries in tight, compressed market ranges.

Max Holding (42 bars): Trades are closed after 42 bars if no exit signal is triggered.

Risk-Reward (2.0x): Aiming for 2x ATR as profit for every 1x ATR risk.

Originality Note

While volatility and momentum have been used separately in many strategies, this script combines both with a time-based dynamic exit system. This exit rule, combined with an ATR-based filter to exclude low-activity periods, gives the system a practical edge in real-world use. It avoids classic rehashes and integrates real trading constraints for better applicability.

Disclaimer

This is a research-focused trading strategy meant for backtesting and educational purposes. Always use proper risk management and perform due diligence before applying to real funds.

magic wand STSM"Magic Wand STSM" Strategy: Trend-Following with Dynamic Risk Management

Overview:

The "Magic Wand STSM" (Supertrend & SMA Momentum) is an automated trading strategy designed to identify and capitalize on sustained trends in the market. It combines a multi-timeframe Supertrend for trend direction and potential reversal signals, along with a 200-period Simple Moving Average (SMA) for overall market bias. A key feature of this strategy is its dynamic position sizing based on a user-defined risk percentage per trade, and a built-in daily and monthly profit/loss tracking system to manage overall exposure and prevent overtrading.

How it Works (Underlying Concepts):

Multi-Timeframe Trend Confirmation (Supertrend):

The strategy uses two Supertrend indicators: one on the current chart timeframe and another on a higher timeframe (e.g., if your chart is 5-minute, the higher timeframe Supertrend might be 15-minute).

Trend Identification: The Supertrend's direction output is crucial. A negative direction indicates a bearish trend (price below Supertrend), while a positive direction indicates a bullish trend (price above Supertrend).

Confirmation: A core principle is that trades are only considered when the Supertrend on both the current and the higher timeframe align in the same direction. This helps to filter out noise and focus on stronger, more confirmed trends. For example, for a long trade, both Supertrends must be indicating a bearish trend (price below Supertrend line, implying an uptrend context where price is expected to stay above/rebound from Supertrend). Similarly, for short trades, both must be indicating a bullish trend (price above Supertrend line, implying a downtrend context where price is expected to stay below/retest Supertrend).

Trend "Readiness": The strategy specifically looks for situations where the Supertrend has been stable for a few bars (checking barssince the last direction change).

Long-Term Market Bias (200 SMA):

A 200-period Simple Moving Average is plotted on the chart.

Filter: For long trades, the price must be above the 200 SMA, confirming an overall bullish bias. For short trades, the price must be below the 200 SMA, confirming an overall bearish bias. This acts as a macro filter, ensuring trades are taken in alignment with the broader market direction.

"Lowest/Highest Value" Pullback Entries:

The strategy employs custom functions (LowestValueAndBar, HighestValueAndBar) to identify specific price action within the recent trend:

For Long Entries: It looks for a "buy ready" condition where the price has found a recent lowest point within a specific number of bars since the Supertrend turned bearish (indicating an uptrend). This suggests a potential pullback or consolidation before continuation. The entry trigger is a close above the open of this identified lowest bar, and also above the current bar's open.

For Short Entries: It looks for a "sell ready" condition where the price has found a recent highest point within a specific number of bars since the Supertrend turned bullish (indicating a downtrend). This suggests a potential rally or consolidation before continuation downwards. The entry trigger is a close below the open of this identified highest bar, and also below the current bar's open.

Candle Confirmation: The strategy also incorporates a check on the candle type at the "lowest/highest value" bar (e.g., closevalue_b < openvalue_b for buy signals, meaning a bearish candle at the low, suggesting a potential reversal before a buy).

Risk Management and Position Sizing:

Dynamic Lot Sizing: The lotsvalue function calculates the appropriate position size based on your Your Equity input, the Risk to Reward ratio, and your risk percentage for your balance % input. This ensures that the capital risked per trade remains consistent as a percentage of your equity, regardless of the instrument's volatility or price. The stop loss distance is directly used in this calculation.

Fixed Risk Reward: All trades are entered with a predefined Risk to Reward ratio (default 2.0). This means for every unit of risk (stop loss distance), the target profit is rr times that distance.

Daily and Monthly Performance Monitoring:

The strategy tracks todaysWins, todaysLosses, and res (daily net result) in real-time.

A "daily profit target" is implemented (day_profit): If the daily net result is very favorable (e.g., res >= 4 with todaysLosses >= 2 or todaysWins + todaysLosses >= 8), the strategy may temporarily halt trading for the remainder of the session to "lock in" profits and prevent overtrading during volatile periods.

A "monthly stop-out" (monthly_trade) is implemented: If the lres (overall net result from all closed trades) falls below a certain threshold (e.g., -12), the strategy will stop trading for a set period (one week in this case) to protect capital during prolonged drawdowns.

Trade Execution:

Entry Triggers: Trades are entered when all buy/sell conditions (Supertrend alignment, SMA filter, "buy/sell situation" candle confirmation, and risk management checks) are met, and there are no open positions.

Stop Loss and Take Profit:

Stop Loss: The stop loss is dynamically placed at the upTrendValue for long trades and downTrendValue for short trades. These values are derived from the Supertrend indicator, which naturally adjusts to market volatility.

Take Profit: The take profit is calculated based on the entry price, the stop loss, and the Risk to Reward ratio (rr).

Position Locks: lock_long and lock_short variables prevent immediate re-entry into the same direction once a trade is initiated, or after a trend reversal based on Supertrend changes.

Visual Elements:

The 200 SMA is plotted in yellow.

Entry, Stop Loss, and Take Profit lines are plotted in white, red, and green respectively when a trade is active, with shaded areas between them to visually represent risk and reward.

Diamond shapes are plotted at the bottom of the chart (green for potential buy signals, red for potential sell signals) to visually indicate when the buy_sit or sell_sit conditions are met, along with other key filters.

A comprehensive trade statistics table is displayed on the chart, showing daily wins/losses, daily profit, total deals, and overall profit/loss.

A background color indicates the active trading session.

Ideal Usage:

This strategy is best applied to instruments with clear trends and sufficient liquidity. Users should carefully adjust the Your Equity, Risk to Reward, and risk percentage inputs to align with their individual risk tolerance and capital. Experimentation with different ATR Length and Factor values for the Supertrend might be beneficial depending on the asset and timeframe.

SOXL Trend Surge v3.0.2 – Profit-Only RunnerSOXL Trend Surge v3.0.2 – Profit-Only Runner

This is a trend-following strategy built for leveraged ETFs like SOXL, designed to ride high-momentum waves with minimal interference. Unlike most short-term scalping scripts, this model allows trades to develop over multiple days to even several months, capitalizing on the full power of extended directional moves — all without using a stop-loss.

🔍 How It Works

Entry Logic:

Price is above the 200 EMA (long-term trend confirmation)

Supertrend is bullish (momentum confirmation)

ATR is rising (volatility expansion)

Volume is above its 20-bar average (liquidity filter)

Price is outside a small buffer zone from the 200 EMA (to avoid whipsaws)

Trades are restricted to market hours only (9 AM to 2 PM EST)

Cooldown of 15 bars after each exit to prevent overtrading

Exit Strategy:

Takes partial profit at +2× ATR if held for at least 2 bars

Rides the remaining position with a trailing stop at 1.5× ATR

No hard stop-loss — giving space for volatile pullbacks

⚙️ Strategy Settings

Initial Capital: $500

Risk per Trade: 100% of equity (fully allocated per entry)

Commission: 0.1%

Slippage: 1 tick

Recalculate after order is filled

Fill orders on bar close

Timeframe Optimized For: 45-minute chart

These parameters simulate an aggressive, high-volatility trading model meant for forward-testing compounding potential under realistic trading costs.

✅ What Makes This Unique

No stop-loss = fewer premature exits

Partial profit-taking helps lock in early wins

Trailing logic gives room to ride large multi-week moves

Uses strict filters (volume, ATR, EMA bias) to enter only during high-probability windows

Ideal for leveraged ETF swing or position traders looking to hold longer than the typical intraday or 2–3 day strategies

⚠️ Important Note

This is a high-risk, high-reward strategy meant for educational and testing purposes. Without a stop-loss, trades can experience deep drawdowns that may take weeks or even months to recover. Always test thoroughly and adjust position sizing to suit your risk tolerance. Past results do not guarantee future returns. Backtest range: May 8, 2020 – May 23, 2025

Futures Trading Hours RSI StrategyFutures Trading Hours RSI Strategy

A lightweight, session-filtered RSI strategy designed for equity-index futures (e.g. NQ, ES, YM) on a 30-minute chart. It dynamically enters long when RSI crosses above your oversold threshold and short when RSI crosses below your overbought threshold—but only during regular U.S. trading hours (08:30–15:00 CT, Monday–Friday). All positions are set to close at 15:00 CT to avoid overnight risk, and optional background shading highlights your open longs (green) and shorts (red).

⸻

Key Features

• RSI-based entries: configurable length, oversold, and overbought levels

• Session filter: trades only between 08:30–15:00 CT, Monday through Friday

• Automatic exit: closes all positions at or after 15:00 CT each day

• Visual cues: optional background shading for open long/short positions

• Easy customization: adjust length, overSold, overBought, and time offsets

Backtest Performance (NQ Jun 2025, 30 min)

• Total P&L: +$10,230 (+1.02%)

• Profit Factor: 4.61

• Win Rate: 57.1% (4 wins / 7 trades)

• Max Drawdown: $2,215 (0.22%)

(Results shown are for illustrative purposes only; past performance does not guarantee future returns.)

How to Use

1. Add this script to your 30-minute futures chart.

2. Tweak the RSI parameters and time-zone offset to suit your instrument.

3. Enable “background shading” if you’d like a visual reminder of open positions.

4. Run in paper-trade mode to validate performance before going live.

⸻

⚠️ Disclaimer: Trading carries risk. Always backtest and paper-trade before using real capital. Adjust position sizing and risk controls to your own tolerance.

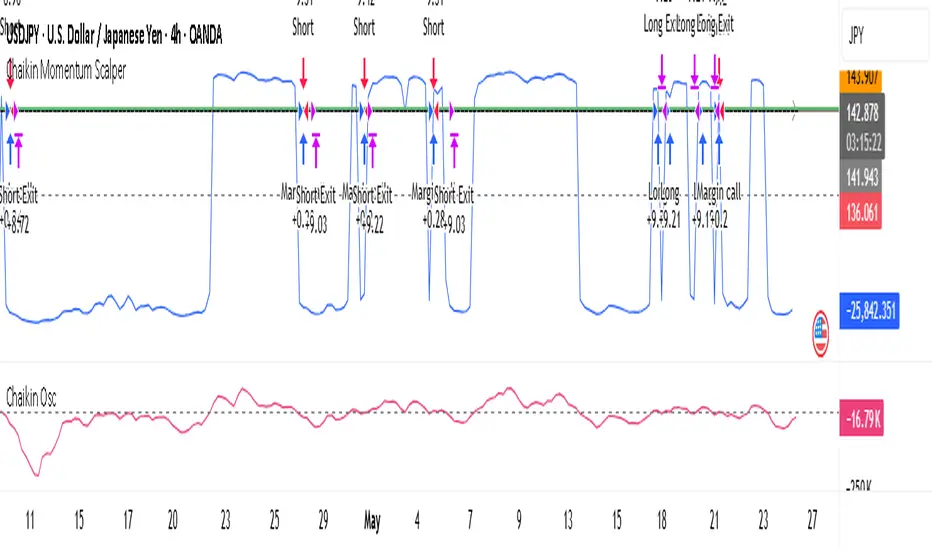

Chaikin Momentum Scalper🎯 Overview

The Chaikin Momentum Scalper is a powerful trading strategy designed to identify momentum shifts in the market and ride the trend for maximum profits. This strategy is ideal for trading the USD/JPY currency pair on a 15-minute chart, making it perfect for high-frequency trading (HFT). Whether you’re starting with a small account of $1,000 or managing a larger portfolio, this strategy can scale to suit your needs.

________________________________________

🔑 How the Strategy Works

Here’s how the Chaikin Momentum Scalper identifies trade opportunities:

1️⃣ Momentum Detection

The core of this strategy is the Chaikin Oscillator, a tool that measures the flow of money into or out of a market. It helps us understand whether buyers (bulls) or sellers (bears) are in control.

• When the indicator crosses above zero, it signals that buying momentum is picking up – a buying opportunity.

• When the indicator crosses below zero, it signals that selling momentum is increasing – a selling opportunity.

2️⃣ Trend Confirmation

We don’t just jump into trades based on momentum alone. We also use a 200-period simple moving average (SMA) to confirm the overall trend.

• If the price is above the SMA, it confirms an uptrend, so we look for buy trades.

• If the price is below the SMA, it confirms a downtrend, so we look for sell trades.

This way, we align our trades with the broader market direction for higher success rates.

3️⃣ Volatility & Risk Management

We use a tool called the Average True Range (ATR) to measure market volatility. This helps us:

• Set a stop-loss (where we’ll exit the trade if the market moves against us) at a safe distance from our entry point.

• Set a take-profit (where we’ll lock in profits) at a target that’s larger than the stop-loss, ensuring a good reward-to-risk ratio.

This approach adapts to the market’s behavior, tightening stops in calmer conditions and widening them when volatility increases.

________________________________________

📈 Why This Strategy Works

✅ It combines momentum and trend-following principles, increasing the chances of trading in the right direction.

✅ It dynamically adjusts risk levels based on market volatility, keeping losses small and profits big.

✅ It’s scalable – perfect for both small accounts (like $1,000) and larger, corporate-sized portfolios.

✅ It has been deep-backtested on USD/JPY 15-minute charts, proving its consistency across different market conditions.

________________________________________

📝 Important Notes

📌 This strategy is best used for USD/JPY on a 15-minute chart, making it great for high-frequency trading while you continue to build and refine your trading system.

📌 It’s designed to work on both small ($1,000+) and large accounts, so it can grow with you as your capital increases.

📌 While it has passed deep backtesting on this pair and timeframe, remember that no strategy is perfect. It’s crucial to test it yourself, start with a demo account, and apply proper risk management before trading real money.

🌟 Final Thoughts

The Chaikin Momentum Scalper is a solid, adaptable trading approach combining momentum, trend direction, and volatility awareness. If you’re looking for a strategy to kick-start your trading journey—or to add to your existing system—it offers a strong foundation.

Grid Tendence V1The “Grid Tendence V1” strategy is based on the classic Grid strategy, only in this case the entries and exits are made in favor of the trend, which allows to take advantage of large movements to maximize profits, since it is also possible to enter and exit with the balance with a controlled risk, because precisely the distance between each Grid works as a natural and adaptable stop loss and take profit. This fact helps to avoid overlapping entries and exits that would result from using stop loss and take profit as limit orders.

In this version of the script the entries and exits are always at market, and based on the percentage change of the price, not on the profit or loss of the current position.

The user will notice that the strategy setup is based on a controlled risk, risking 5% on each trade, a fairly standard commission and a modest initial capital, all this in order to protect the user of the strategy from unexpected or unrealistic results.

However, it is always recommended to optimize the parameters so that the strategy is effective for each asset and for each time frame.

LANZ Strategy 3.0 [Backtest]🔷 LANZ Strategy 3.0 — Asian Range Fibonacci Scalping Strategy

LANZ Strategy 3.0 is a precision-engineered backtesting tool tailored for intraday traders who rely on the Asian session range to determine directional bias. This strategy implements dynamic Fibonacci projections and strict time-window validation to simulate a clean and disciplined trading environment.

🧠 Core Components:

Asian Range Bias Definition: Direction is established between 01:15–02:15 a.m. NY time based on the candle’s close in relation to the midpoint of the Asian session range (18:00–01:15 NY).

Limit Order Execution: Only one trade is placed daily, using a limit order at the Asian range high (for sells) or low (for buys), between 01:15–08:00 a.m. NY.

Fibonacci-Based TP/SL:

Original Mode: TP = 2.25x range, SL = 0.75x range.

Optimized Mode: TP = 1.95x range, SL = 0.65x range.

No Trade After 08:00 NY: If the limit order is not executed before 08:00 a.m. NY, it is canceled.

Fallback Logic at 02:15 NY: If the market direction misaligns with the setup at 02:15 a.m., the system re-evaluates and can re-issue the order.

End-of-Day Closure: All positions are closed at 15:45 NY if still open.

📊 Backtest-Ready Design:

Entries and exits are executed using strategy.entry() and strategy.exit() functions.

Position size is fixed via capital risk allocation ($100 per trade by default).

Only one position can be active at a time, ensuring controlled risk.

📝 Notes:

This strategy is ideal for assets sensitive to the Asian/London session overlap, such as Forex pairs and indices.

Easily switch between Fibonacci versions using a single dropdown input.

Fully deterministic: all entries are based on pre-defined conditions and time constraints.

👤 Credits:

Strategy developed by rau_u_lanz using Pine Script v6. Built for traders who favor clean sessions, directional clarity, and consistent execution using time-based logic and Fibonacci projections.

SpeedBullish Strategy Confirm V6.2SpeedBullish Strategy Confirm V6.2

SpeedBullish V6.2 is an advanced price-action + indicator-based strategy designed to confirm trend strength and signal entries with high precision. This version builds on the W/M pattern structure and adds dynamic filtering with EMA, MACD Histogram, RSI, ATR, and Volume.

✅ Signal Conditions

🔹 Buy Signal:

Price above EMA10 or EMA15

MACD Histogram crosses above 0

RSI > 50

(Optional) Higher low via Pivot Low

(Optional) ATR > ATR SMA * Multiplier

(Optional) Volume > SMA * Multiplier

🔻 Sell Signal:

Price below EMA10 or EMA15

MACD Histogram crosses below 0

RSI < 50

(Optional) Lower high via Pivot High

(Optional) Confirmed high volatility and volume

⚙️ Strategy Features

MACD Histogram for momentum shift detection

RSI filtering for momentum confirmation

EMA10/15 for trend direction

ATR-based volatility filter

Volume confirmation filter

Dynamic TP/SL + Trailing Stop

Webhook Integration for MT5 auto-trade

Visual signal markers + background highlight

🔔 Alerts

Alerts are sent in JSON format via alert() with the current symbol, action (buy/sell), and price. Webhook endpoint and secret key are configurable.

📈 How to Use

Attach the strategy to any symbol and timeframe

Customize filters and confirmations to fit your market conditions

Enable webhook alerts for integration with your MT5 Expert Advisor or trading bot

Backtest and optimize before live deployment

Bias Ratio-ETH-3H @CTTC5108Most of the code of this strategy should be my own original.

This Ethereum 3-hour time cycle strategy can be traced back to February 24, 2023. Although the profit and winning rate are not high, it is still relatively stable.

This strategy uses the deviation rate to enter the market. Invest 10% of the principal each time.

The limit start time adopts a rolling design (should be original).

Real-time retracement and maximum retracement are accurately calculated (should be original).

Adopt segmented stop profit (optional) design.

Open source for learning and other use.

Range Filter Strategy with ATR TP/SLHow This Strategy Works:

Range Filter:

Calculates a smoothed average (SMA) of price

Creates upper and lower bands based on standard deviation

When price crosses above upper band, it signals a potential uptrend

When price crosses below lower band, it signals a potential downtrend

ATR-Based Risk Management:

Uses Average True Range (ATR) to set dynamic take profit and stop loss levels

Take profit is set at entry price + (ATR × multiplier) for long positions

Stop loss is set at entry price - (ATR × multiplier) for long positions

The opposite applies for short positions

Input Parameters:

Adjustable range filter length and multiplier

Customizable ATR length and TP/SL multipliers

All parameters can be optimized in TradingView's strategy tester

You can adjust the input parameters to fit your trading style and the specific market you're trading. The ATR-based exits help adapt to current market volatility.

Range Filter + ATR Strategy (Low Drawdown)Key Features for Low Drawdown:

Range Filter: Identifies trends while filtering out market noise

ATR-based Position Sizing: Adjusts position size based on volatility to risk a fixed percentage of capital

Trailing Stops: Uses ATR-based trailing stops to lock in profits and limit losses

Conservative Risk Parameters: Defaults to 1% risk per trade (adjustable)

Trend Confirmation: Requires two consecutive closes above/below the range filter

How to Use:

The strategy enters long when price is above the upper range filter for two consecutive bars

Enters short when price is below the lower range filter for two consecutive bars

Uses ATR to size positions appropriately for current volatility

Implements trailing stops based on ATR to protect profits

Optimization Tips:

Adjust the Range Filter period based on your timeframe

Modify the risk percentage (1% is conservative)

Tweak the ATR multiple for trailing stops (1.5 is moderate)

Consider adding a time-based exit if drawdown is still too high

ORB 5M + VWAP + Braid Filter + TP 2R o Niveles PreviosORB 5-Minute Breakout Strategy Summary

Strategy Name:

ORB 5M + VWAP + Braid Filter + TP 2R or Previous Levels

Timeframe:

5-minute chart

Trading Window:

9:35 AM to 11:00 AM (New York time)

✅ Entry Conditions:

Opening Range: Defined from 9:30 to 9:35 AM (first 5-minute candle).

Breakout Entry:

Long trade: Price breaks above the opening range high.

Short trade: Price breaks below the opening range low.

Confirmation Filters (All must be met):

Strong candle (green for long, red for short).

VWAP in the direction of the trade.

Braid Filter by Mango2Juice supports the breakout direction (green for long, red for short).

📉 Stop Loss:

Placed at the opposite side of the opening range.

🎯 Take Profit (TP):

+2R (Risk-to-Reward Ratio of 2:1),

or

Closest of the following: previous day’s high/low or premarket levels.

⚙️ Additional Rules:

Only valid signals between 9:35 and 11:00 AM.

Only one trade per breakout direction per day.

Filter out "trap candles" (very small or indecisive candles).

Avoid trading after 11:00 AM.

📊 Performance Goals:

Maintain a high Profit Factor (above 3 ideally).

Focus on tickers with good historical performance under this strategy (e.g., AMZN, PLTR, CVNA).

Momentum Long + Short Strategy (BTC 3H)Momentum Long + Short Strategy (BTC 3H)

🔍 How It Works, Step by Step

Detect the Trend (📈/📉)

Calculate two moving averages (100-period and 500-period), either EMA or SMA.

For longs, we require MA100 > MA500 (uptrend).

For shorts, we block entries if MA100 exceeds MA500 by more than a set percentage (to avoid fading a powerful uptrend).

Apply Momentum Filters (⚡️)

RSI Filter: Measures recent strength—only allow longs when RSI crosses above its smoothed average, and shorts when RSI dips below the oversold threshold.

ADX Filter: Gauges trend strength—ensures we only enter when a meaningful trend exists (optional).

ATR Filter: Confirms volatility—avoids choppy, low-volatility conditions by requiring ATR to exceed its smoothed value (optional).

Confirm Entry Conditions (✅)

Long Entry:

Price is above both MAs

Trend alignment & optional filters pass ✅

Short Entry:

Price is below both MAs and below the lower Bollinger Band

RSI is sufficiently oversold

Trend-blocker & ATR filter pass ✅

Position Sizing & Risk (💰)

Each trade uses 100 % of account equity by default.

One pyramid addition allowed, so you can scale in if the move continues.

Commission and slippage assumptions built in for realistic backtests.

Stops & Exits (🛑)

Long Stop-Loss: e.g. 3 % below entry.

Long Auto-Exit: If price falls back under the 500-period MA.

Short Stop-Loss: e.g. 3 % above entry.

Short Take-Profit: e.g. 4 % below entry.

🎨 Why It’s Powerful & Customizable

Modular Filters: Turn on/off RSI, ADX, ATR filters to suit different market regimes.

Adjustable Thresholds: Fine-tune stop-loss %, take-profit %, RSI lengths, MA gaps and more.

Multi-Timeframe Potential: Although coded for 3 h BTC, you can adapt it to stocks, forex or other cryptos—just recalibrate!

Backtest Fine-Tuned: Default settings were optimized via backtesting on historical BTC data—but they’re not guarantees of future performance.

⚠️ Warning & Disclaimer

This strategy is for educational purposes only and designed for a toy fund. Crypto markets are highly volatile—you can lose 100 % of your capital. It is not a predictive “holy grail” but a rules-based framework using past data. The parameters have been fine-tuned on historical data and are not valid for future trades without fresh calibration. Always practice with paper-trading first, use proper risk management, and do your own research before risking real money. 🚨🔒

Good luck exploring and experimenting! 🚀📊

Volume and Volatility Ratio Indicator-WODI策略名称

交易量与波动率比例策略-WODI

一、用户自定义参数

vol_length:交易量均线长度,计算基础交易量活跃度。

index_short_length / index_long_length:指数短期与长期均线长度,用于捕捉中短期与中长期趋势。

index_magnification:敏感度放大倍数,调整指数均线的灵敏度。

index_threshold_magnification:阈值放大因子,用于动态过滤噪音。

lookback_bars:形态检测回溯K线根数,用于捕捉反转模式。

fib_tp_ratio / fib_sl_ratio:斐波那契止盈与止损比率,分别对应黄金分割(0.618/0.382 等)级别。

enable_reversal:反转信号开关,开启后将原有做空信号反向为做多信号,用于单边趋势加仓。

二、核心计算逻辑

交易量百分比

使用 ta.sma 计算 vol_ma,并得到 vol_percent = volume / vol_ma * 100。

价格波动率

volatility = (high – low) / close * 100。

构建复合指数

volatility_index = vol_percent * volatility,并分别计算其短期与长期均线(乘以 index_magnification)。

动态阈值

index_threshold = index_long_ma * index_threshold_magnification,过滤常规波动。

三、信号生成与策略执行

做多/做空信号

当短期指数均线自下而上突破长期均线,且 volatility_index 突破 index_threshold 时,发出做多信号。

当短期指数均线自上而下跌破长期均线,且 volatility_index 跌破 index_threshold 时,发出做空信号。

反转信号模式(可选)

若 enable_reversal = true,则所有做空信号反向为做多,用于在强趋势行情中加仓。

止盈止损管理

进场后自动设置斐波那契止盈位(基于入场价 × fib_tp_ratio)和止损位(入场价 × fib_sl_ratio)。

支持多级止盈:可依次以 0.382、0.618 等黄金分割比率分批平仓。

四、图表展示

策略信号标记:图上用箭头标明每次做多/做空(或反转加仓)信号。

斐波那契区间:在K线图中显示止盈/止损水平线。

复合指数与阈值线:与原版相同,在独立窗口绘制短、长期指数均线、指数曲线及阈值。

量能柱状:高于均线时染色,反转模式时额外高亮。

Strategy Name

Volume and Volatility Ratio Strategy – WODI

1. User-Defined Parameters

vol_length: Length for volume SMA.

index_short_length / index_long_length: Short and long MA lengths for the composite index.

index_magnification: Sensitivity multiplier for index MAs.

index_threshold_magnification: Threshold multiplier to filter noise.

lookback_bars: Number of bars to look back for pattern detection.

fib_tp_ratio / fib_sl_ratio: Fibonacci take-profit and stop-loss ratios (e.g. 0.618, 0.382).

enable_reversal: Toggle for reversal mode; flips short signals to long for trend-following add-on entries.

2. Core Calculation

Volume Percentage:

vol_ma = ta.sma(volume, vol_length)

vol_percent = volume / vol_ma * 100

Volatility:

volatility = (high – low) / close * 100

Composite Index:

volatility_index = vol_percent * volatility

Short/long MAs applied and scaled by index_magnification.

Dynamic Threshold:

index_threshold = index_long_ma * index_threshold_magnification.

3. Signal Generation & Execution

Long/Short Entries:

Long when short MA crosses above long MA and volatility_index > index_threshold.

Short when short MA crosses below long MA and volatility_index < index_threshold.

Reversal Mode (optional):

If enable_reversal is on, invert all short entries to long to scale into trending moves.

Fibonacci Take-Profit & Stop-Loss:

Automatically set TP/SL levels at entry price × respective Fibonacci ratios.

Supports multi-stage exits at 0.382, 0.618, etc.

4. Visualization

Signal Arrows: Marks every long/short or reversal-add signal on the chart.

Fibonacci Zones: Plots TP/SL lines on the price panel.

Index & Threshold: Same as v1.0, with MAs, index curve, and threshold in a separate sub-window.

Volume Bars: Colored when above vol_ma; extra highlight if a reversal-add signal triggers

Big Mover Catcher BTC 4h🧠 Big Mover Catcher (BTC 4H Strategy) — Educational Tool

⚠️ Disclaimer: I am not a financial advisor. This script is for educational and testing purposes only. Cryptocurrency trading is highly volatile and involves significant risk. You can lose all of your invested capital.

📌 Overview

The Big Mover Catcher strategy is a work-in-progress trading system designed for Bitcoin (BTC) on the 4-hour chart. It aims to identify strong breakout moves by combining multiple technical indicators and conditions, allowing for high customization and filter-based confirmations.

This script is part of a personal project to learn Pine Script and backtesting on TradingView. It is currently in the testing and research phase.

🎯 Strategy Objective

Catch large, high-momentum breakout moves in the BTC market using:

Bollinger Band breakouts for entry signals

Momentum, volatility, and trend filters for trade confirmation

🧰 Features & Filters

The script provides a flexible set of filters that can be turned ON/OFF and adjusted directly from the settings panel:

✅ Entry Conditions

Price must break above or below Bollinger Bands

All selected filters must align before entry

🧪 Available Filters:

Relative Strength Index (RSI) with EMA/SMA smoothing

Average Directional Index (ADX) with EMA/SMA smoothing

Average True Range (ATR) with EMA/SMA smoothing

MACD Signal above or below zero

EMA 350 trend filter

ATR / ADX / RSI Threshold toggles for added control

🔥 Additional Feature:

Force Take Profit: Optionally closes the trade immediately if a candle closes with more than a defined % movement (default: 5%). This can help lock in quick profits during high volatility moves.

⚙️ Customizable Inputs

You can configure:

Stop loss percentage

All indicator lengths

Smoothing types (EMA/SMA)

Threshold activation toggles

Individual filter ON/OFF switches

This makes the strategy highly adaptable for educational exploration and optimization.

📊 Best Used For

Learning Pine Script and strategy structure

Testing filter combinations for BTC on the 4H timeframe

Understanding how different indicators interact in live markets

⚠️ Note: ❌ Short trades are currently disabled by default, as short-side logic is still under development.

❗ Final Reminder

This script is not financial advice. It is an educational tool. Use it to learn and explore trading logic. Trading cryptocurrencies carries high risk — only invest what you can afford to lose.

LANZ Strategy 2.0 [Backtest]🔷 LANZ Strategy 2.0 — Structural Breakout Logic with Dynamic Swing Protection

LANZ Strategy 2.0 is a precision-focused backtesting system built for intraday traders who rely on structural confirmations before the London session to guide directional bias. This tool uses smart swing detection, risk-defined position sizing, and strict time-based execution to simulate real trading conditions with clarity and control.

🧠 Core Components:

Structural Confirmation (Trend & BoS): Detects trend direction and break of structure (BoS) using a three-swing logic, aligning trade entries with valid structural movement.

Time-Based Execution: Trades are triggered exclusively at 02:00 a.m. New York time, ensuring disciplined and repeatable intraday testing.

Swing-Based SL Models: Traders can select between three stop-loss protection types:

First Swing: Most recent structural level

Second Swing: Prior level

Full Coverage: All recent swing levels + configurable pip buffer

Dynamic TP Calculation: Take-Profit is projected as a risk-based multiple (RR), fully adjustable via input.

Capital-Based Risk Management: Risk is defined as a percentage of a fixed account size (e.g., $100 per trade from $10,000), and lot size is automatically calculated based on SL distance.

Fallback Entry Logic: If structural breakout is present but trend is not confirmed, a secondary entry is triggered.

End-of-Session Management: Any open trades are automatically closed at 11:45 a.m. NY time, with optional manual labeling or review.

📊 Visual Features (Optional in Indicator Version):

(Note: Visuals apply to the indicator version of LANZ 2.0, not this backtest script)

Swing level labels (1st, 2nd) and dynamic SL/TP lines.

Real-time session coloring for clarity: Pre-London, Entry Window, and NY Close.

Outcome labels: +RR, -RR, or net % at close.

Auto-cleanup of previous drawings for a clean chart per session.

⚙️ How It Works:

Detects last trend and BoS using swing logic before 02:00 a.m. NY.

At 02:00 a.m., evaluates directional bias and executes BUY or SELL if confirmed.

Applies selected SL logic (1st, 2nd, or full swing protection).

Sets TP based on the RR multiplier.

Closes the trade either on SL, TP, or at 11:45 a.m. NY manually.

🔔 Alerts:

Time-of-day alert at 02:00 a.m. NY to monitor execution.

Can be extended to cover SL/TP triggers or new BoS events.

📝 Notes:

Designed for backtesting precision and discretionary decision-making.

Ideal for Forex pairs, indices, or assets active during the London session.

Fully customizable: session timing, swing logic, SL buffer, and RR.

👤 Credits:

Strategy built by @rau_u_lanz using Pine Script v6, combining structural logic, capital-based risk control, and London-session timing in a backtest-ready framework for traders who demand accuracy and structure.

EMA Pullback Speed Strategy 📌 **Overview**

The **EMA Pullback Speed Strategy** is a trend-following approach that combines **price momentum** and **Exponential Moving Averages (EMA)**.

It aims to identify high-probability entry points during brief pullbacks within ongoing uptrends or downtrends.

The strategy evaluates **speed of price movement**, **relative position to dynamic EMA**, and **candlestick patterns** to determine ideal timing for entries.

One of the key concepts is checking whether the price has **“not pulled back too much”**, helping focus only on situations where the trend is likely to continue.

⚠️ This strategy is designed for educational and research purposes only. It does not guarantee future profits.

🧭 **Purpose**

This strategy addresses the common issue of **"jumping in too late during trends and taking unnecessary losses."**

By waiting for a healthy pullback and confirming signs of **trend resumption**, traders can enter with greater confidence and reduce false entries.

🎯 **Strategy Objectives**

* Enter in the direction of the prevailing trend to increase win rate

* Filter out false signals using pullback depth, speed, and candlestick confirmations

* Predefine Take-Profit (TP) and Stop-Loss (SL) levels for safer, rule-based trading

✨ **Key Features**

* **Dynamic EMA**: Reacts faster when price moves quickly, slower when market is calm – adapting to current momentum

* **Pullback Filter**: Avoids trades when price pulls back too far (e.g., more than 5%), indicating a trend may be weakening

* **Speed Check**: Measures how strongly the price returns to the trend using candlestick body speed (open-to-close range in ticks)

📊 **Trading Rules**

**■ Long Entry Conditions:**

* Current price is above the dynamic EMA (indicating uptrend)

* Price has pulled back toward the EMA (a "buy the dip" situation)

* Pullback depth is within the threshold (not excessive)

* Candlesticks show consecutive bullish closes and break the previous high

* Price speed is strong (positive movement with momentum)

**■ Short Entry Conditions:**

* Current price is below the dynamic EMA (indicating downtrend)

* Price has pulled back up toward the EMA (a "sell the rally" setup)

* Pullback is within range (not too deep)

* Candlesticks show consecutive bearish closes and break the previous low

* Price speed is negative (downward momentum confirmed)

**■ Exit Conditions (TP/SL):**

* **Take-Profit (TP):** Fixed 1.5% target above/below entry price

* **Stop-Loss (SL):** Based on recent price volatility, calculated using ATR × 4

💰 **Risk Management Parameters**

* Symbol & Timeframe: BTCUSD on 1-hour chart (H1)

* Test Capital: \$3000 (simulated account)

* Commission: 0.02%

* Slippage: 2 ticks (minimal execution lag)

* Max risk per trade: 5% of account balance

* Backtest Period: Aug 30, 2023 – May 9, 2025

* Profit Factor (PF): 1.965 (Net profit ÷ Net loss, including spreads & fees)

⚙️ **Trading Parameters & Indicator Settings**

* Maximum EMA Length: 50

* Accelerator Multiplier: 3.0

* Pullback Threshold: 5.0%

* ATR Period: 14

* ATR Multiplier (SL distance): 4.0

* Fixed TP: 1.5%

* Short-term EMA: 21

* Long-term EMA: 50

* Long Speed Threshold: ≥ 1000.0 (ticks)

* Short Speed Threshold: ≤ -1000.0 (ticks)

⚠️Adjustments are based on BTCUSD.

⚠️Forex and other currency pairs require separate adjustments.

🔧 **Strategy Improvements & Uniqueness**

Unlike basic moving average crossovers or RSI triggers, this strategy emphasizes **"momentum-supported pullbacks"**.

By combining dynamic EMA, speed checks, and candlestick signals, it captures trades **as if surfing the wave of a trend.**

Its built-in filters help **avoid overextended pullbacks**, which often signal the trend is ending – making it more robust than traditional trend-following systems.

✅ **Summary**

The **EMA Pullback Speed Strategy** is easy to understand, rule-based, and highly reproducible – ideal for both beginners and intermediate traders.

Because it shows **clear visual entry/exit points** on the chart, it’s also a great tool for practicing discretionary trading decisions.

⚠️ Past performance is not a guarantee of future results.

Always respect your Stop-Loss levels and manage your position size according to your risk tolerance.

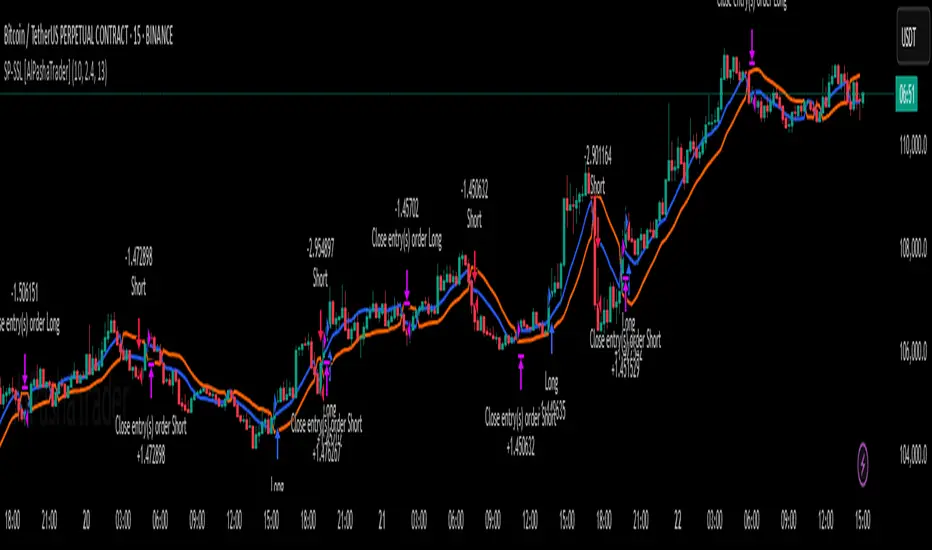

Supertrend - SSL Strategy with Toggle [AlPashaTrader]📈 Overview of the Supertrend - SSL Strategy with Toggle Indicator

This strategy combines two powerful technical tools—Supertrend and SSL Channel—to deliver precise and reliable trading signals, designed for traders who value confirmation and risk management. 🎯

⚙️ How This Indicator Was Created

The strategy was meticulously crafted to harness the complementary strengths of:

Supertrend Indicator: A trend-following tool based on Average True Range (ATR) and a multiplier factor, it detects bullish or bearish trends by calculating dynamic support and resistance levels. 📊

SSL Channel: A channel indicator built using two Simple Moving Averages (SMA) of the highs and lows over a set period. It cleverly determines trend direction by comparing price action relative to these moving averages. 🔄

These two indicators are merged into one cohesive strategy with an optional toggle feature allowing the trader to choose whether to require confirmation from both indicators before taking a position or to act on signals from either. 🎚️

The script includes user-friendly controls for:

Defining a custom trading date range 📅, useful for backtesting or restricting trading to specific market conditions.

Setting the ATR length and multiplier for Supertrend sensitivity ⚙️.

Adjusting the SSL channel period for responsiveness to price changes ⏱️.

Choosing whether to require dual confirmation (both Supertrend and SSL signals) for more conservative trading or a single indicator trigger for a more aggressive approach 🛡️ vs ⚔️.

🔍 How This Indicator Works

Signal Generation:

Supertrend analyzes market volatility and trend direction, signaling a potential buy when the trend turns bullish 📈 and a sell when bearish 📉.

SSL Channel tracks price relative to its high and low moving averages to identify uptrends and downtrends. A crossover of the SSL Up and SSL Down lines generates buy or sell signals 🔔.

Confirmation Logic:

When confirmation is enabled, the strategy waits for agreement between both indicators before entering a trade ✅, reducing false signals.

When confirmation is disabled, it trades based on signals from either indicator ⚡, allowing more frequent entries but potentially higher risk.

Entry and Exit Rules:

Entry occurs when the indicator(s) signal a new trend direction 🚀 for long, or decline for short.

Exit happens when opposing signals appear 🛑, closing existing positions to lock in profits or cut losses.

Visual Aids:

The SSL Channel lines are plotted directly on the chart with distinct colors to intuitively show trend shifts 🎨.

The system respects the specified date range ⏳, ensuring trades only occur within user-defined periods.

🎯 How to Use This Strategy Effectively

Set Your Preferences: Adjust ATR length, factor, and SSL period to your style. More sensitive? Decrease lengths. Smoother? Increase them ⚙️.

Choose Confirmation Mode: Use the toggle depending on your risk appetite:

Confirmation ON ✅: For conservative traders wanting high-probability setups.

Confirmation OFF ⚡: For aggressive traders who want more signals.

Apply Date Filters: Focus your trading or backtesting on specific periods 📅.

Monitor Entry/Exit Signals: Watch crossovers and Supertrend changes closely 👀.

Risk Management: The strategy uses position sizing as a percentage of equity (default 15%) 💰. Adjust accordingly.

Combine with Other Tools: Enhance results by combining this with volume, price action, or fundamentals 🔧.

📝 Summary

This Supertrend - SSL Strategy with Toggle is a dynamic and flexible trading tool blending volatility-based trend detection with moving-average channel insights. It empowers traders to customize confirmation strictness, control trading periods, and efficiently capture trending opportunities while managing risk smartly.

By integrating proven indicators in a user-friendly, visually intuitive package, this strategy stands as a sophisticated tool suitable for various markets and trading styles. 🚀📊

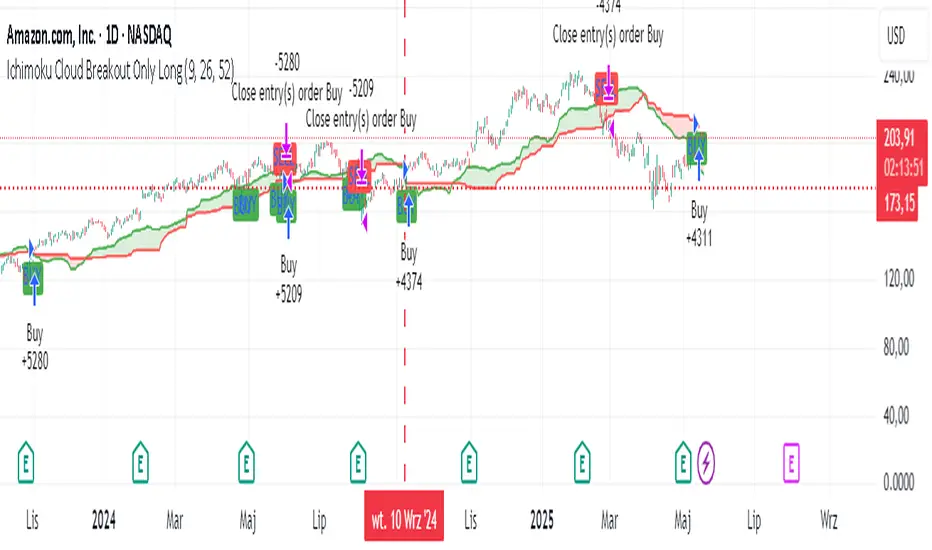

Ichimoku Cloud Breakout Only LongThis is a very simple trading strategy based exclusively on the Ichimoku Cloud. There are no additional indicators or complex rules involved. The key condition is that we only open long positions when the price is clearly above the cloud — indicating a bullish trend.

For optimal results, the recommended timeframes are 1D (daily) or 1W (weekly) charts. These higher timeframes help filter out market noise and provide more reliable trend signals.

We do not short the market under any circumstances. The focus is purely on riding upward momentum when the price breaks out or stays above the cloud.

This strategy works best when applied to growth stocks with strong upward trends and good fundamentals — such as Google (GOOGL), Tesla (TSLA), Apple (AAPL), or NVIDIA (NVDA).

AltCoin Index Correlation🧠 AltCoin Index Correlation — Strategy Overview

AltCoin Index Correlation is a dynamic EMA-based trading strategy designed primarily for altcoins, but also adaptable to stocks and indices, thanks to its flexible reference index system.

🧭 Strategy Philosophy

The core idea behind this strategy is simple yet powerful:

Price action becomes more meaningful when it aligns with broader market context.

This script analyzes the correlation between the asset’s trend and a reference index trend, using dual EMA (Exponential Moving Average) crossovers for both.

When both the altcoin and the reference index (e.g. Altcoin Dominance, BTC Dominance, Total Market Cap, or even indices like the NASDAQ 100 or S&P 500) are aligned in trend direction, the script considers it a high-confidence setup.

It also includes:

Optional inverse correlation logic (for contrarian setups)

Custom leverage settings (e.g., 1x, 1.8x, etc.)

A dynamic scale-out mechanism during weakening trends

Date filtering for controlled backtests

A live performance dashboard with equity, PnL, win rate, drawdown, APR, and more

⚙️ Default Settings & Backtest Results

Timeframe tested: 1H

Test date: May 20, 2025

Sample: 100 high-cap altcoins

Reference index: CRYPTOCAP:OTHERS.D (Altcoin Dominance)

Leverage: 1.8x (180% of capital used)

📊 With default settings:

Win rate: ~80%

Higher profits, due to increased exposure

Best suited for confident trend followers with higher risk tolerance

📉 With fixed capital or 1x leverage:

Win rate improves to ~90%

Lower returns, but greater capital preservation

Ideal for conservative or risk-managed trading styles

🔄 Versatility

While tailored for altcoins, this strategy supports traditional markets as well:

Easily switch the reference index to OANDA:NAS100USD or S&P 500 for stock correlation trading

Adjust EMA lengths and leverage to match the asset class and volatility profile

🧩 Suggested Use

Best used on trending markets (not sideways)

Ideal for 1H timeframes, but adjustable

Suitable for traders who want a rules-based, macro-aware entry/exit system

Try it out, customize it to your style, try different settings and share your results with the community!

Feedback is welcome — and improvements are always in progress.

🚀 ### Check my profile for other juicy hints and original strategies. ### 🚀

Liquidity Grab Strategy (Volume Trap)🧠 Strategy Logic:

Liquidity Grab Detection:

The script looks for a sharp drop in price (bearish engulfing or breakdown candle).

However, volume remains flat (within 5% of the 20-period moving average), suggesting the move is manipulated, not genuine.

Fair Value Gap Confirmation (FVG):

It confirms that a Fair Value Gap exists — a gap between recent candle bodies that price is likely to retrace into.

This gap represents a high-probability entry zone.

Trade Setup:

A limit BUY order is placed at the base of the FVG.

Stop Loss (SL) is placed below the gap.

Take Profit (TP) is placed at the most recent swing high.

📈 How to Use It:

Add the strategy to your TradingView chart (1–5 min or 15 min works well for intraday setups).

Look for green BUY labels and plotted lines:

💚 Green = Entry price

🔴 Red = Stop loss

🔵 Blue = Take profit

The script will automatically simulate entries when conditions are met and exit either at TP or SL.

Use TradingView’s Strategy Tester to review:

Win rate

Net profit

Risk-adjusted performance

Trend Revisit Pullback Strategy (Final Working Box)📈 Trend Revisit Pullback Strategy

This TradingView Pine Script strategy identifies strong trend breakouts and accounts for natural pullbacks by:

Entering long or short on strong 1-bar breakouts

Allowing for pullback averaging if price retraces after entry

Expecting a revisit to the original entry price within 15 bars

Automatically exiting at break-even or using a custom TP/SL

Drawing a visual trade zone (entry → SL → revisit window) for easy reference

Optional labels and color-coded boxes to track each trade’s lifecycle

Ideal for trend traders who anticipate a pullback and prefer to manage risk with break-even exits or reward-to-risk parameters.