HMA Crossover + ATR + Curvature (Long & Short)📏 Hull Moving Averages (Trend Filters)

- fastHMA = ta.hma(close, fastLength)

- slowHMA = ta.hma(close, slowLength)

These two HMAs act as dynamic trend indicators:

- A bullish crossover of fast over slow HMA signals a potential long setup.

- A bearish crossunder triggers short interest.

⚡️ Curvature (Acceleration Filter)

- curv = ta.change(ta.change(fastHMA))

This calculates the second-order change (akin to the second derivative) of the fast HMA — effectively the acceleration of the trend. It serves as a filter:

- For long entries: curv > curvThresh (positive acceleration)

- For short entries: curv < -curvThresh (negative acceleration)

It helps eliminate weak or stagnating moves by requiring momentum behind the crossover.

📈 Volatility-Based Risk Management (ATR)

- atr = ta.atr(atrLength)

- stopLoss = atr * atrMult

- trailStop = atr * trailMult

These define your:

- Initial stop loss: scaled to recent volatility using ATR and atrMult.

- Trailing stop: also ATR-scaled, to lock in gains dynamically as price moves favorably.

💰 Position Sizing via Risk Percent

- capital = strategy.equity

- riskCapital = capital * (riskPercent / 100)

- qty = riskCapital / stopLoss

This dynamically calculates the position size (qty) such that if the stop loss is hit, the loss does not exceed the predefined percentage of account equity. It’s a volatility-adjusted position sizing method, keeping your risk consistent regardless of market conditions.

📌 Execution Logic

- Long Entry: on bullish HMA crossover with rising curvature.

- Short Entry: on bearish crossover with falling curvature.

- Exits: use ATR-based trailing stops.

- Position is closed when trend conditions reverse (e.g., bearish crossover exits the long).

This framework gives you:

- Trend-following logic (via HMAs)

- Momentum confirmation (via curvature)

- Volatility-aware execution and exits (via ATR)

- Risk-controlled dynamic sizing

Want to get surgical and test what happens if we use curvature on the difference between HMAs instead? That might give some cool insights into trend strength transitions.

Indicators and strategies

⚡ HMA PowerPlay Strategy ⚡The ⚡ HMA PowerPlay Strategy ⚡ is a highly filtered momentum-based strategy that combines trend-following and volatility breakout logic. It is designed for precision entries during strong directional moves.

**Key Features:**

- Dual HMA filtering (short-term and long-term)

- Strong bullish/bearish candle detection

- ATR-based dynamic stop loss and R-multiple targets

- Volume confirmation filter

- RSI + MACD oscillator conditions for additional confirmation

- Entry checklist panel for transparent signal breakdown

- Oscillator and price panel for deeper context

- Supports both long and short signals

Ideal for traders who want visual clarity, data-backed entries, and structured position management.

Developed and optimized by IMSHAHROKH.

SG Multi Entry/Exit IndicatorThis strategy is based on an entry and an exit indicator that can be selected from a range of indicators.

The entry / exit indicators are standard Stochastic, MACD, RSI and MA indicators.

The graphs for each indicator are normalised to between 0 and 100 and displayed on above the other with buy and sell indicators.

The Strategy can be enabled / disabled via the inputs as can the date range as can whether to put a dummy sell signal in for the last trading day to give an accurate Mark to Market performance.

Liquidity Sweep Strategy v2 - Fixed Close LabelsThe Liquidity Sweep Strategy v2 is designed to detect stop-loss hunting behavior, commonly seen in institutional trading. It capitalizes on false breakouts beyond recent swing highs or lows (liquidity zones), which are followed by sharp reversals.

This strategy is particularly effective during high-volume liquidity grabs when markets trigger stop-loss clusters and then reverse direction — a phenomenon often referred to as a liquidity sweep or stop hunt

CNCRADIO talked GPT into Watching the YouTube!Referred GPT to the youtube channel and produced PINE script with no errors first try, followed some prompts and this is the result.

Ichimoku + RSI + VWMA Strategy Suite (w/ ATR SLTP)Ichimoku + RSI + VWMA indikatörleri kullanılarak üretilen seçmeli stratejiler.

SMA3 / EMA10 + MACD (9-10pm COL) | SL 10 pips, TP 10 pipsmedias movil de 3 periodos mas una ema de 10 + macd cruces, el tp y sl no se usan de la estrategia se usa minimo o maximo q marque el zigzag de 6 periodos.

3-period simple moving average plus a 10-period EMA and MACD crossovers. Take profit and stop loss are not fixed; instead, they are based on the most recent low or high marked by a 6-period ZigZag indicator."

Multi-Confluence Swing Hunter V1# Multi-Confluence Swing Hunter V1 - Complete Description

Overview

The Multi-Confluence Swing Hunter V1 is a sophisticated low timeframe scalping strategy specifically optimized for MSTR (MicroStrategy) trading. This strategy employs a comprehensive point-based scoring system that combines optimized technical indicators, price action analysis, and reversal pattern recognition to generate precise trading signals on lower timeframes.

Performance Highlight:

In backtesting on MSTR 5-minute charts, this strategy has demonstrated over 200% profit performance, showcasing its effectiveness in capturing rapid price movements and volatility patterns unique to MicroStrategy's trading behavior.

The strategy's parameters have been fine-tuned for MSTR's unique volatility characteristics, though they can be optimized for other high-volatility instruments as well.

## Key Innovation & Originality

This strategy introduces a unique **dual scoring system** approach:

- **Entry Scoring**: Identifies swing bottoms using 13+ different technical criteria

- **Exit Scoring**: Identifies swing tops using inverse criteria for optimal exit timing

Unlike traditional strategies that rely on simple indicator crossovers, this system quantifies market conditions through a weighted scoring mechanism, providing objective, data-driven entry and exit decisions.

## Technical Foundation

### Optimized Indicator Parameters

The strategy utilizes extensively backtested parameters specifically optimized for MSTR's volatility patterns:

**MACD Configuration (3,10,3)**:

- Fast EMA: 3 periods (vs standard 12)

- Slow EMA: 10 periods (vs standard 26)

- Signal Line: 3 periods (vs standard 9)

- **Rationale**: These faster parameters provide earlier signal detection while maintaining reliability, particularly effective for MSTR's rapid price movements and high-frequency volatility

**RSI Configuration (21-period)**:

- Length: 21 periods (vs standard 14)

- Oversold: 30 level

- Extreme Oversold: 25 level

- **Rationale**: The 21-period RSI reduces false signals while still capturing oversold conditions effectively in MSTR's volatile environment

**Parameter Adaptability**: While optimized for MSTR, these parameters can be adjusted for other high-volatility instruments. Faster-moving stocks may benefit from even shorter MACD periods, while less volatile assets might require longer periods for optimal performance.

### Scoring System Methodology

**Entry Score Components (Minimum 13 points required)**:

1. **RSI Signals** (max 5 points):

- RSI < 30: +2 points

- RSI < 25: +2 points

- RSI turning up: +1 point

2. **MACD Signals** (max 8 points):

- MACD below zero: +1 point

- MACD turning up: +2 points

- MACD histogram improving: +2 points

- MACD bullish divergence: +3 points

3. **Price Action** (max 4 points):

- Long lower wick (>50%): +2 points

- Small body (<30%): +1 point

- Bullish close: +1 point

4. **Pattern Recognition** (max 8 points):

- RSI bullish divergence: +4 points

- Quick recovery pattern: +2 points

- Reversal confirmation: +4 points

**Exit Score Components (Minimum 13 points required)**:

Uses inverse criteria to identify swing tops with similar weighting system.

## Risk Management Features

### Position Sizing & Risk Control

- **Single Position Strategy**: 100% equity allocation per trade

- **No Overlapping Positions**: Ensures focused risk management

- **Configurable Risk/Reward**: Default 5:1 ratio optimized for volatile assets

### Stop Loss & Take Profit Logic

- **Dynamic Stop Loss**: Based on recent swing lows with configurable buffer

- **Risk-Based Take Profit**: Calculated using risk/reward ratio

- **Clean Exit Logic**: Prevents conflicting signals

## Default Settings Optimization

### Key Parameters (Optimized for MSTR/Bitcoin-style volatility):

- **Minimum Entry Score**: 13 (ensures high-conviction entries)

- **Minimum Exit Score**: 13 (prevents premature exits)

- **Risk/Reward Ratio**: 5.0 (accounts for volatility)

- **Lower Wick Threshold**: 50% (identifies true hammer patterns)

- **Divergence Lookback**: 8 bars (optimal for swing timeframes)

### Why These Defaults Work for MSTR:

1. **Higher Score Thresholds**: MSTR's volatility requires more confirmation

2. **5:1 Risk/Reward**: Compensates for wider stops needed in volatile markets

3. **Faster MACD**: Captures momentum shifts quickly in fast-moving stocks

4. **21-period RSI**: Reduces noise while maintaining sensitivity

## Visual Features

### Score Display System

- **Green Labels**: Entry scores ≥10 points (below bars)

- **Red Labels**: Exit scores ≥10 points (above bars)

- **Large Triangles**: Actual trade entries/exits

- **Small Triangles**: Reversal pattern confirmations

### Chart Cleanliness

- Indicators plotted in separate panes (MACD, RSI)

- TP/SL levels shown only during active positions

- Clear trade markers distinguish signals from actual trades

## Backtesting Specifications

### Realistic Trading Conditions

- **Commission**: 0.1% per trade

- **Slippage**: 3 points

- **Initial Capital**: $1,000

- **Account Type**: Cash (no margin)

### Sample Size Considerations

- Strategy designed for 100+ trade sample sizes

- Recommended timeframes: 4H, 1D for swing trading

- Optimal for trending/volatile markets

## Strategy Limitations & Considerations

### Market Conditions

- **Best Performance**: Trending markets with clear swings

- **Reduced Effectiveness**: Highly choppy, sideways markets

- **Volatility Dependency**: Optimized for moderate to high volatility assets

### Risk Warnings

- **High Allocation**: 100% position sizing increases risk

- **No Diversification**: Single position strategy

- **Backtesting Limitation**: Past performance doesn't guarantee future results

## Usage Guidelines

### Recommended Assets & Timeframes

- **Primary Target**: MSTR (MicroStrategy) - 5min to 15min timeframes

- **Secondary Targets**: High-volatility stocks (TSLA, NVDA, COIN, etc.)

- **Crypto Markets**: Bitcoin, Ethereum (with parameter adjustments)

- **Timeframe Optimization**: 1min-15min for scalping, 30min-1H for swing scalping

### Timeframe Recommendations

- **Primary Scalping**: 5-minute and 15-minute charts

- **Active Monitoring**: 1-minute for precise entries

- **Swing Scalping**: 30-minute to 1-hour timeframes

- **Avoid**: Sub-1-minute (excessive noise) and above 4-hour (reduces scalping opportunities)

## Technical Requirements

- **Pine Script Version**: v6

- **Overlay**: Yes (plots on price chart)

- **Additional Panes**: MACD and RSI indicators

- **Real-time Compatibility**: Confirmed bar signals only

## Customization Options

All parameters are fully customizable through inputs:

- Indicator lengths and levels

- Scoring thresholds

- Risk management settings

- Visual display preferences

- Date range filtering

## Conclusion

This scalping strategy represents a comprehensive approach to low timeframe trading that combines multiple technical analysis methods into a cohesive, quantified system specifically optimized for MSTR's unique volatility characteristics. The optimized parameters and scoring methodology provide a systematic way to identify high-probability scalping setups while managing risk effectively in fast-moving markets.

The strategy's strength lies in its objective, multi-criteria approach that removes emotional decision-making from scalping while maintaining the flexibility to adapt to different instruments through parameter optimization. While designed for MSTR, the underlying methodology can be fine-tuned for other high-volatility assets across various markets.

**Important Disclaimer**: This strategy is designed for experienced scalpers and is optimized for MSTR trading. The high-frequency nature of scalping involves significant risk. Past performance does not guarantee future results. Always conduct your own analysis, consider your risk tolerance, and be aware of commission/slippage costs that can significantly impact scalping profitability.

TMNT3 [v5, Code Copilot] with PyramidCore Principles

Trend-Following Breakouts

Enters on clean price breakouts above the prior N-day high (System 1: 20 days; System 2: 55 days).

Exits on reversals through the prior M-day low (System 1: 10 days; System 2: 20 days).

Volatility-Based Stops

Uses the Average True Range (ATR) to set a dynamic stop-loss at

Stop = Entry Price ± (ATR×Multiplier)

Stop= Entry Price-(ATR×Multiplier)

Adapts to changing market noise—wider stops in volatile conditions, tighter in calm markets.

System 1 vs. System 2 Toggle

System 1 (20/10) for shorter, faster swing opportunities.

System 2 (55/20) for catching longer, more powerful trends.

Pyramiding into Winners

Scales into a position in fixed “units” (each risking a constant % of equity).

Adds an extra unit each time price extends by a set fraction of ATR (default 0.5× ATR), up to a configurable maximum (default 5 units).

Only increases exposure when the trend proves itself—managing risk while maximizing returns.

Strict Risk Management

Each unit carries its own ATR-based stop, ensuring no single leg blows out the account.

Default risk per unit is a small, fixed percentage of total equity (e.g. 1% per unit).

Visual Aids & Confirmation

Overlaid entry/exit channels and trend/exit lines for immediate context.

Optional on-chart labels and background shading to highlight active trade regimes.

Why It Works

Objectivity & Discipline: Rules-based entries, exits, and sizing remove emotional guesswork.

Adaptive to Market Conditions: ATR stops and pyramiding adapt to both calm and turbulent phases.

Scalable: Toggle between short and long breakout horizons to suit different assets or timeframes.

Volatility Index Percentile Risk STOCK StrategyVolatility-Index Percentile Risk STOCK Strategy

──────────────────────────────────────────────

PURPOSE

• Go long equities only when implied volatility (from any VIX-style index) is in its quietest percentile band.

• Scale stop-loss distance automatically with live volatility so risk stays proportional across timeframes and market regimes.

HOW IT WORKS

1. Pull the closing price of a user-selected volatility index (default: CBOE VIX, Nasdaq VXN, etc.).

2. Compute its 1-year (252-bar) percentile.

– If percentile < “Enter” threshold → open / maintain long.

– If percentile > “Exit” threshold → flatten.

3. Set the stop-loss every bar at:

SL % = (current VIX value) ÷ Risk Divisor

(e.g., VIX = 20 and divisor = 57 → 0.35 % SL below entry).

This keeps risk tighter when volatility is high and looser when it’s calm.

USER INPUTS

• VIX-style Index — symbol of any volatility index

• Look-back — length for percentile (default 252)

• Enter Long < Percentile — calm-market trigger (default 15 %)

• Exit Long > Percentile — fear trigger (default 60 %)

• Risk Divisor (SL) — higher number = tighter stop; start with 57 on 30-min charts

• Show Debug Plots — optional visibility of percentile & SL%

RECOMMENDED BACK-TEST SETTINGS

• Timeframe: 30 min – Daily on liquid stocks/ETFs highly correlated to the chosen VIX.

• Initial capital: 100 000 | Order size: 10 % of equity

• Commission: 0.03 % | Slippage: 5 ticks

• Enable *Bar Magnifier* and *Fill on bar close* for realistic execution.

ADDITIONAL INFORMATION

• **Self-calibrating risk** – no static ATR or fixed %, adapts instantly to changing volatility.

• **Percentile filter** – regime-aware entry logic that avoids false calm periods signalled by raw VIX levels.

• **Timeframe-agnostic** – works from intraday to weekly; √T-style divisor lets you fine-tune stops quickly ,together with the percentiles and days length.

• Zero look-ahead.

CAVEATS

• Long-only; no built-in profit target. Add one if your plan requires fixed R:R exits.

• Works best on indices/stocks that move with the selected vol index.

• Back-test results are educational; past performance never guarantees future returns.

LICENSE & CREDITS

Released under the Mozilla Public License 2.0.

Inspired by academic research on volatility risk premia and mean-reversion.

DISCLAIMER

This script is for informational and educational purposes only. It is **not** financial advice. Use at your own risk.

KST Strategy [Skyrexio]Overview

KST Strategy leverages Know Sure Thing (KST) indicator in conjunction with the Williams Alligator and Moving average to obtain the high probability setups. KST is used for for having the high probability to enter in the direction of a current trend when momentum is rising, Alligator is used as a short term trend filter, while Moving average approximates the long term trend and allows trades only in its direction. Also strategy has the additional optional filter on Choppiness Index which does not allow trades if market is choppy, above the user-specified threshold. Strategy has the user specified take profit and stop-loss numbers, but multiplied by Average True Range (ATR) value on the moment when trade is open. The strategy opens only long trades.

Unique Features

ATR based stop-loss and take profit. Instead of fixed take profit and stop-loss percentage strategy utilizes user chosen numbers multiplied by ATR for its calculation.

Configurable Trading Periods. Users can tailor the strategy to specific market windows, adapting to different market conditions.

Optional Choppiness Index filter. Strategy allows to choose if it will use the filter trades with Choppiness Index and set up its threshold.

Methodology

The strategy opens long trade when the following price met the conditions:

Close price is above the Alligator's jaw line

Close price is above the filtering Moving average

KST line of Know Sure Thing indicator shall cross over its signal line (details in justification of methodology)

If the Choppiness Index filter is enabled its value shall be less than user defined threshold

When the long trade is executed algorithm defines the stop-loss level as the low minus user defined number, multiplied by ATR at the trade open candle. Also it defines take profit with close price plus user defined number, multiplied by ATR at the trade open candle. While trade is in progress, if high price on any candle above the calculated take profit level or low price is below the calculated stop loss level, trade is closed.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.5, number of ATRs to calculate stop-loss level)

ATR Take Profit (by default = 3.5, number of ATRs to calculate take profit level)

Filter MA Type (by default = Least Squares MA, type of moving average which is used for filter MA)

Filter MA Length (by default = 200, length for filter MA calculation)

Enable Choppiness Index Filter (by default = true, setting to choose the optional filtering using Choppiness index)

Choppiness Index Threshold (by default = 50, Choppiness Index threshold, its value shall be below it to allow trades execution)

Choppiness Index Length (by default = 14, length used in Choppiness index calculation)

KST ROC Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #2 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #3 (by default = 20, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #4 (by default = 30, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #2 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #3 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #4 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST Signal Line Length (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is KST, Williams Alligator, Moving Average, ATR and Choppiness Index.

The KST (Know Sure Thing) is a momentum oscillator developed by Martin Pring. It combines multiple Rate of Change (ROC) values, smoothed over different timeframes, to identify trend direction and momentum strength. First of all, what is ROC? ROC (Rate of Change) is a momentum indicator that measures the percentage change in price between the current price and the price a set number of periods ago.

ROC = 100 * (Current Price - Price N Periods Ago) / Price N Periods Ago

In our case N is the KST ROC Length inputs from settings, here we will calculate 4 different ROCs to obtain KST value:

KST = ROC1_smooth × 1 + ROC2_smooth × 2 + ROC3_smooth × 3 + ROC4_smooth × 4

ROC1 = ROC(close, KST ROC Length #1), smoothed by KST SMA Length #1,

ROC2 = ROC(close, KST ROC Length #2), smoothed by KST SMA Length #2,

ROC3 = ROC(close, KST ROC Length #3), smoothed by KST SMA Length #3,

ROC4 = ROC(close, KST ROC Length #4), smoothed by KST SMA Length #4

Also for this indicator the signal line is calculated:

Signal = SMA(KST, KST Signal Line Length)

When the KST line rises, it indicates increasing momentum and suggests that an upward trend may be developing. Conversely, when the KST line declines, it reflects weakening momentum and a potential downward trend. A crossover of the KST line above its signal line is considered a buy signal, while a crossover below the signal line is viewed as a sell signal. If the KST stays above zero, it indicates overall bullish momentum; if it remains below zero, it points to bearish momentum. The KST indicator smooths momentum across multiple timeframes, helping to reduce noise and provide clearer signals for medium- to long-term trends.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

The next indicator is Moving Average. It has a lot of different types which can be chosen to filter trades and the Least Squares MA is used by default settings. Let's briefly explain what is it.

The Least Squares Moving Average (LSMA) — also known as Linear Regression Moving Average — is a trend-following indicator that uses the least squares method to fit a straight line to the price data over a given period, then plots the value of that line at the most recent point. It draws the best-fitting straight line through the past N prices (using linear regression), and then takes the endpoint of that line as the value of the moving average for that bar. The LSMA aims to reduce lag and highlight the current trend more accurately than traditional moving averages like SMA or EMA.

Key Features:

It reacts faster to price changes than most moving averages.

It is smoother and less noisy than short-term EMAs.

It can be used to identify trend direction, momentum, and potential reversal points.

ATR (Average True Range) is a volatility indicator that measures how much an asset typically moves during a given period. It was introduced by J. Welles Wilder and is widely used to assess market volatility, not direction.

To calculate it first of all we need to get True Range (TR), this is the greatest value among:

High - Low

abs(High - Previous Close)

abs(Low - Previous Close)

ATR = MA(TR, n) , where n is number of periods for moving average, in our case equals 14.

ATR shows how much an asset moves on average per candle/bar. A higher ATR means more volatility; a lower ATR means a calmer market.

The Choppiness Index is a technical indicator that quantifies whether the market is trending or choppy (sideways). It doesn't indicate trend direction — only the strength or weakness of a trend. Higher Choppiness Index usually approximates the sideways market, while its low value tells us that there is a high probability of a trend.

Choppiness Index = 100 × log10(ΣATR(n) / (MaxHigh(n) - MinLow(n))) / log10(n)

where:

ΣATR(n) = sum of the Average True Range over n periods

MaxHigh(n) = highest high over n periods

MinLow(n) = lowest low over n periods

log10 = base-10 logarithm

Now let's understand how these indicators work in conjunction and why they were chosen for this strategy. KST indicator approximates current momentum, when it is rising and KST line crosses over the signal line there is high probability that short term trend is reversing to the upside and strategy allows to take part in this potential move. Alligator's jaw (blue) line is used as an approximation of a short term trend, taking trades only above it we want to avoid trading against trend to increase probability that long trade is going to be winning.

Almost the same for Moving Average, but it approximates the long term trend, this is just the additional filter. If we trade in the direction of the long term trend we increase probability that higher risk to reward trade will hit the take profit. Choppiness index is the optional filter, but if it turned on it is used for approximating if now market is in sideways or in trend. On the range bounded market the potential moves are restricted. We want to decrease probability opening trades in such condition avoiding trades if this index is above threshold value.

When trade is open script sets the stop loss and take profit targets. ATR approximates the current volatility, so we can make a decision when to exit a trade based on current market condition, it can increase the probability that strategy will avoid the excessive stop loss hits, but anyway user can setup how many ATRs to use as a stop loss and take profit target. As was said in the Methodology stop loss level is obtained by subtracting number of ATRs from trade opening candle low, while take profit by adding to this candle's close.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2025.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 60%

Maximum Single Position Loss: -5.53%

Maximum Single Profit: +8.35%

Net Profit: +5175.20 USDT (+51.75%)

Total Trades: 120 (56.67% win rate)

Profit Factor: 1.747

Maximum Accumulated Loss: 1039.89 USDT (-9.1%)

Average Profit per Trade: 43.13 USDT (+0.6%)

Average Trade Duration: 27 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 1h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrexio commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation.

MARSdx BTCUSD Strategy🔍 Strategy Overview

The MARSdx Strategy is a hybrid trend-following and momentum-based system designed specifically for Bitcoin trading(works also on other Crypto like ETHUSD). It combines four technical indicators—SMA, EMA, RSI, and ADX—to filter high-probability long entries during strong bullish phases.

✅ Entry Conditions

Price above SMA(50) → confirms long-term bullish trend

Price above EMA(7) → confirms short-term momentum

RSI(2) > ADX(2) → confirms strong bullish pressure

Only when all three conditions are met, a long position is opened.

❌ Exit Condition

RSI(2) < ADX(2) → momentum weakens, exit position

📊 Indicators Used

SMA (Simple Moving Average) – identifies overall trend

EMA (Exponential Moving Average) – captures short-term momentum

RSI (Relative Strength Index) – gauges strength of price movement

ADX (Average Directional Index) – filters based on trend strength

⚙️ Inputs

SMA Length: Default 50

EMA Length: Default 7

RSI Length: Default 2

ADX Length: Default 2

You can tweak these parameters to suit other timeframes or crypto assets.

⚠️ This strategy only takes long trades. It does not use any stop-loss or profit target logic and should be combined with sound risk management.

Ticker Pulse Meter + Fear EKG StrategyDescription

The Ticker Pulse Meter + Fear EKG Strategy is a technical analysis tool designed to identify potential entry and exit points for long positions based on price action relative to historical ranges. It combines two proprietary indicators: the Ticker Pulse Meter (TPM), which measures price positioning within short- and long-term ranges, and the Fear EKG, a VIX-inspired oscillator that detects extreme market conditions. The strategy is non-repainting, ensuring signals are generated only on confirmed bars to avoid false positives. Visual enhancements, such as optional moving averages and Bollinger Bands, provide additional context but are not core to the strategy's logic. This script is suitable for traders seeking a systematic approach to capturing momentum and mean-reversion opportunities.

How It Works

The strategy evaluates price action using two key metrics:

Ticker Pulse Meter (TPM): Measures the current price's position within short- and long-term price ranges to identify momentum or overextension.

Fear EKG: Detects extreme selling pressure (akin to "irrational selling") by analyzing price behavior relative to historical lows, inspired by volatility-based oscillators.

Entry signals are generated when specific conditions align, indicating potential buying opportunities. Exits are triggered based on predefined thresholds or partial position closures to manage risk. The strategy supports customizable lookback periods, thresholds, and exit percentages, allowing flexibility across different markets and timeframes. Visual cues, such as entry/exit dots and a position table, enhance usability, while optional overlays like moving averages and Bollinger Bands provide additional chart context.

Calculation Overview

Price Range Calculations:

Short-Term Range: Uses the lowest low (min_price_short) and highest high (max_price_short) over a user-defined short lookback period (lookback_short, default 50 bars).

Long-Term Range: Uses the lowest low (min_price_long) and highest high (max_price_long) over a user-defined long lookback period (lookback_long, default 200 bars).

Percentage Metrics:

pct_above_short: Percentage of the current close above the short-term range.

pct_above_long: Percentage of the current close above the long-term range.

Combined metrics (pct_above_long_above_short, pct_below_long_below_short) normalize price action for signal generation.

Signal Generation:

Long Entry (TPM): Triggered when pct_above_long_above_short crosses above a user-defined threshold (entryThresholdhigh, default 20) and pct_below_long_below_short is below a low threshold (entryThresholdlow, default 40).

Long Entry (Fear EKG): Triggered when pct_below_long_below_short crosses under an extreme threshold (orangeEntryThreshold, default 95), indicating potential oversold conditions.

Long Exit: Triggered when pct_above_long_above_short crosses under a profit-taking level (profitTake, default 95). Partial exits are supported via a user-defined percentage (exitAmt, default 50%).

Non-Repainting Logic: Signals are calculated using data from the previous bar ( ) and only plotted on confirmed bars (barstate.isconfirmed), ensuring reliability.

Visual Enhancements:

Optional moving averages (SMA, EMA, WMA, VWMA, or SMMA) and Bollinger Bands can be enabled for trend context.

A position table displays real-time metrics, including open positions, Fear EKG, and Ticker Pulse values.

Background highlights mark periods of high selling pressure.

Entry Rules

Long Entry:

TPM Signal: Occurs when the price shows strength relative to both short- and long-term ranges, as defined by pct_above_long_above_short crossing above entryThresholdhigh and pct_below_long_below_short below entryThresholdlow.

Fear EKG Signal: Triggered by extreme selling pressure, when pct_below_long_below_short crosses under orangeEntryThreshold. This signal is optional and can be toggled via enable_yellow_signals.

Entries are executed only on confirmed bars to prevent repainting.

Exit Rules

Long Exit: Triggered when pct_above_long_above_short crosses under profitTake.

Partial exits are supported, with the strategy closing a user-defined percentage of the position (exitAmt) up to four times per position (exit_count limit).

Exits can be disabled or adjusted via enable_short_signal and exitPercentage settings.

Inputs

Backtest Start Date: Defines the start of the backtesting period (default: Jan 1, 2017).

Lookback Periods: Short (lookback_short, default 50) and long (lookback_long, default 200) periods for range calculations.

Resolution: Timeframe for price data (default: Daily).

Entry/Exit Thresholds:

entryThresholdhigh (default 20): Threshold for TPM entry.

entryThresholdlow (default 40): Secondary condition for TPM entry.

orangeEntryThreshold (default 95): Threshold for Fear EKG entry.

profitTake (default 95): Exit threshold.

exitAmt (default 50%): Percentage of position to exit.

Visual Options: Toggle for moving averages and Bollinger Bands, with customizable types and lengths.

Notes

The strategy is designed to work across various timeframes and assets, with data sourced from user-selected resolutions (i_res).

Alerts are included for long entry and exit signals, facilitating integration with TradingView's alert system.

The script avoids repainting by using confirmed bar data and shifted calculations ( ).

Visual elements (e.g., SMA, Bollinger Bands) are inspired by standard Pine Script practices and are optional, not integral to the core logic.

Usage

Apply the script to a chart, adjust input settings to suit your trading style, and use the visual cues (entry/exit dots, position table) to monitor signals. Enable alerts for real-time notifications.

Designed to work best on Daily timeframe.

LANZ Strategy 1.0 [Backtest]🔷 LANZ Strategy 1.0 — Time-Based Session Trading with Smart Reversal Logic and Risk-Controlled Limit Orders

This backtest version of LANZ Strategy 1.0 brings precision to session-based trading by using directional confirmation, pre-defined risk parameters, and limit orders that execute overnight. Designed for the 1-hour timeframe, it allows traders to evaluate the system with configurable SL, TP, and risk settings in a fully automated environment.

🧠 Core Strategy Logic:

1. Directional Confirmation at 18:00 NY:

At 18:00 NY, the system compares the 08:00 open vs the 18:00 close:

If the direction matches the previous day, the signal is reversed.

If the direction differs, the current day's trend is kept.

This logic is designed to avoid momentum exhaustion and capture corrective reversals.

2. Entry Level Definition:

Based on the confirmed direction:

For BUY, the Low of the day is used as Entry Point (EP).

For SELL, the High of the day becomes EP.

The system plots a Stop Loss and Take Profit based on user-defined pip inputs (default: SL = 18 pips, TP = 54 pips → RR 1:3).

3. Time-Limited Entry Execution (LIMIT Orders):

Orders are sent after 18:00 NY and can be triggered anytime between 18:00 and 08:00 NY.

If EP is not touched before 08:00, the order is automatically cancelled.

4. Manual Close Feature:

If the trade is still open at the configured hour (default 09:00 NY), the system closes all positions, simulating realistic intraday exit scenarios.

5. Lot Size Calculation Based on Risk:

Lot size is dynamically calculated using the account size, risk percentage, and SL distance.

This ensures consistent risk exposure regardless of market volatility.

⚙️ Step-by-Step Flow:

08:00 NY → Captures the open of the day.

18:00 NY → Confirms direction and defines EP, SL, and TP.

After 18:00 NY → If conditions are met, a LIMIT order is placed at EP.

Between 18:00–08:00 NY → If price touches EP, the trade is executed.

At 08:00 NY → If EP wasn’t touched, the order is cancelled.

At Configured Manual Close Time (default 09:00 NY) → All open positions are force-closed if still active.

🧪 Backtest Settings:

Timeframe: 1-hour only

Order Type: strategy.entry() with limit=

SL/TP Configurable: Yes, in pips

Risk Input: % of capital per trade

Manual Close Time: Fully adjustable (default 09:00 NY)

👨💻 Credits:

Developed by LANZ

Strategy logic and trading concept built with clarity and precision.

Code structure and documentation by Kairos, your AI trading assistant.

Designed for high-confidence execution and clean backtesting performance.

Z Score 主图策略 — v1.02Hello Traders,

Here is my new year gift for the community, Digergence for Many Indicators v4. I tried to make it modular and readable as much as I can. Thanks to Pine Team for improving Pine Platform all the time!

How it works?

- On each candle it checks divergences between current and any of last 16 Pivot Points for the indicators.

- it search divergence on choisen indicators => RSI , MACD , MACD Histogram, Stochastic , CCI , Momentum, OBV, VWMACD, CMF and any External Indicator!

- it checks following divergences for 16 pivot points that is in last 100 bars for each Indicator.

--> Regular Positive Digergences

--> Regular Negative Digergences

--> Hidden Positive Digergences

--> Hidden Negative Digergences

- for positive divergences first it checks if closing price is higher than last closing price and indicator value is higher than perious value, then start searching divergence

- for negative divergences first it checks if closing price is lower than last closing price and indicator value is lower than perious value, then start searching divergence

Some Options:

Pivot Period: you set Pivot Period as you wish. you can see Pivot Points using "Show Pivot Points" option

Source for Pivot Points: you can use Close or High/Low as source

Divergence Type: you can choose Divergence type to be shown => "Regular", "Hidden", "Regular/Hidden"

Show Indicator Names: you have different options to show indicator names => "Full", "First Letter", "Don't Show"

Show Divergence Number: option to see number of indicators which has Divergence

Show Only Last Divergence: if you enable this option then it shows only last Positive and Negative Divergences

you can include any External Indicator to see if there is divergence

- enable "Check External Indicator"

- and then choose External indicator name in the list, "External Indicator"

- External indicator name is shown as Extrn

- related external indicator must be added before enabling this option

Coloring, line width and line style options for different type of divergences.

Following Alerts added:

- Positive Regular Divergence Detected

- Negative Regular Divergence Detected

- Positive Hidden Divergence Detected

- Negative Hidden Divergence Detected

Now lets see some examples:

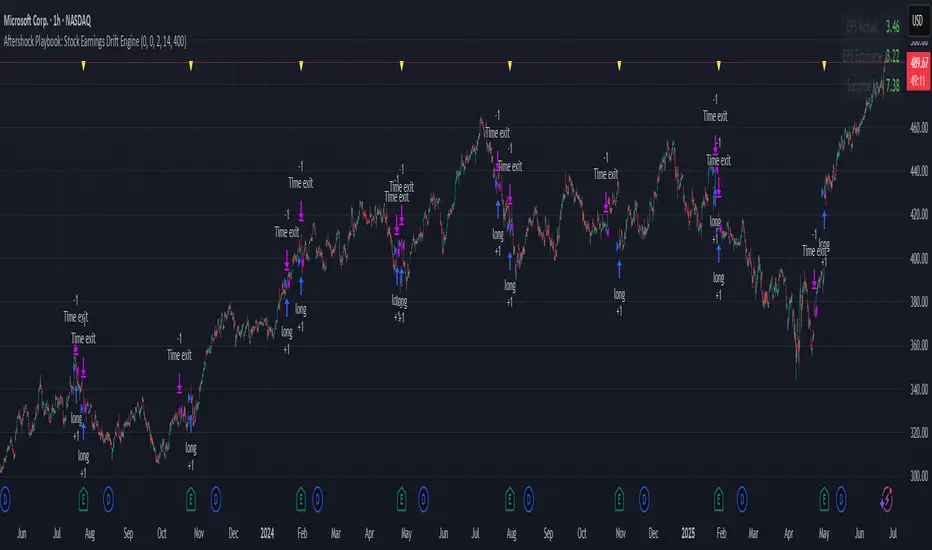

Aftershock Playbook: Stock Earnings Drift EngineStrategy type

Event-driven post-earnings momentum engine (long/short) built for single-stock charts or ADRs that publish quarterly results.

What it does

Detects the exact earnings bar (request.earnings, lookahead_off).

Scores the surprise and launches a position on that candle’s close.

Tracks PnL: if the first leg closes green, the engine automatically re-enters on the very next bar, milking residual drift.

Blocks mid-cycle trades after a loss until the next earnings release—keeping the risk contained to one cycle.

Think of it as a sniper that fires on the earnings pop, reloads once if the shot lands, then goes silent until the next report.

Core signal inputs

Component Default Purpose

EPS Surprise % +0 % / –5 % Minimum positive / negative shock to trigger longs/shorts.

Reverse signals? Off Quick flip for mean-reversion experiments.

Time Risk Mgt. Off Optional hard exit after 45 calendar days (auto-scaled to any TF).

Risk engine

ATR-based stop (ATR × 2 by default, editable).

Bar time stop (15-min → Daily: Have to select the bar value ).

No pyramiding beyond the built-in “double-tap”.

All positions sized as % of equity via Strategy Properties.

Visual aids

Yellow triangle marks the earnings bar.

Diagnostics table (top-right) shows last Actual, Estimate, and Surprise %.

Status-line tool-tips on every input.

Default inputs

Setting Value

Positive surprise ≥ 0 %

Negative surprise ≤ –5 %

ATR stop × 2

ATR length 50

Hold horizon 350 ( 1h timeframe chart bars)

Back-test properties

Initial capital 10 000

Order size 5 % of equity

Pyramiding 1 (internal re-entry only)

Commission 0.03 %

Slippage 5 ticks

Fills Bar magnifier ✔ · On bar close ✔ · Standard OHLC ✔

How to use

Add the script to any earnings-driven stock (AAPL, MSFT, TSLA…).

Turn on Time Risk Management if you want stricter risk management

Back-test different ATR multipliers to fit the stock’s volatility.

Sync commission & slippage with your broker before forward-testing.

Important notes

Works on every timeframe from 15 min to 1 D. Sweet spot around 30min/1h

All request.earnings() & request.security() calls use lookahead_off—zero repaint.

The “double-tap” re-entry occurs once per winning cycle to avoid drift-chasing loops.

Historical stats ≠ future performance. Size positions responsibly.

Out of the Noise Intraday Strategy with VWAP [YuL]This is my (naive) implementation of "Beat the Market An Effective Intraday Momentum Strategy for S&P500 ETF (SPY)" paper by Carlo Zarattini, Andrew Aziz, Andrea Barbon, so the credit goes to them.

It is supposed to run on SPY on 30-minute timeframe, there may be issues on other timeframes.

I've used settings that were used by the authors in the original paper to keep it close to the publication, but I understand that they are very aggressive and probably shouldn't be used like that.

Results are good, but not as good as they are stated in the paper (unsurprisingly?): returns are smaller and Sharpe is very low (which is actually weird given the returns and drawdown ratio), there are also margin calls if you enable margin check (and you should).

I have my own ideas of improvements which I will probably implement separately to keep this clean.

Grid Bot v6 StrategyGrid Bot v6 Strategy

Adaptive parabolic grid that turns market structure into a step-by-step trading plan

Idea of strategy and source code of base indicator provided by my subscriber @Sergio_Nov

1. Core concept

Grid Bot v6 draws a dynamic parabola from a user-defined time/price anchor and builds a 10-level grid around it (five lines above, five below).

Each level is colour-coded:

Green – preferred buy area

Red – preferred sell area

Yellow – overlap of buy-and-sell zones (balance)

Grey – neutral zone

Orders are fired when price touches or reverses from a grid line and the signal is confirmed by current market sentiment. If sentiment contradicts the signal, the order is tagged secondary and uses a reduced lot size.

2. How the logic works

Parabola – the function f_parabola computes the curve from Accel, Curve and Sensitivity. Zero values give a flat horizontal grid; non-zero values create an accelerating or decelerating trendline.

Grid spacing – controlled by Intervals (percentage of price). Lines are recalculated every bar, so the grid “breathes” with the market.

Triggers – choose which part of the candle must reach the level (Wick, Close, Midpoint, SWMA).

Confirmation – decide whether a simple touch is enough or a full reversal is required (Touch vs Reverse).

Sentiment filter – by default the slope of the parabola (up = long bias, down = short bias). You can override it to Long, Short or Neutral.

Order types – four independent sizes: Main Buy, Secondary Buy, Main Sell, Secondary Sell. Pyramiding up to 100 entries is allowed.

Visuals – the script plots actual and projected grid lines (100 bars ahead), the SWMA trigger and the parabola itself. Trade symbols: ▲ ▼ △ ▽.

3. User inputs

Strategy Settings

Main Buy Lot / Secondary Buy Lot

Main Sell Lot / Secondary Sell Lot

Grid Settings

Accel – tilt of the curve (positive for uptrend, negative for downtrend)

Curve – concavity; higher absolute value = stronger bend

Intervals – distance between grid lines (in %)

Sensitivity – how fast the parabola adapts; higher = more reactive

Buy Zones / Sell Zones – number of active lines below/above the curve

Trigger – Wick, Close, Midpoint, SWMA

Confirm – Touch or Reverse

Sentiment – Slope, Long, Short, Neutral

Show Signals / Show Selector – toggle on-chart markers and SWMA line

Chart Settings – individual colours for active grid, projection, parabola and SWMA.

Time/Price Anchor

B_Time – starting bar (e.g. a recent swing high/low)

B_Price – price at that bar

Tip: drop the anchor on a clear pivot, then tune Accel and Curve so the parabola hugs the trend.

4. Quick-start guide

Open your favourite symbol and timeframe (works best on volatile markets from 5-minute to 4-hour).

Set B_Time / B_Price to the last significant extreme.

Adjust Accel and Curve:

Uptrend – positive Accel, negative Curve for a concave support.

Range – both zero for a flat ladder.

Choose Intervals: smaller values = more frequent trades.

Limit Buy Zones and Sell Zones if you prefer a tighter grid.

Run a back-test, check P/L, max drawdown and trade count.

Fine-tune: lower Sensitivity if the curve outruns price; switch Trigger to SWMA to filter noise.

5. Pros and cons

Strengths

Adaptive levels that keep up with trend acceleration.

Clear colour coding plus forward projection for better context.

Sentiment filter reduces counter-trend exposures.

Weaknesses

Many parameters – each asset/timeframe needs its own calibration.

In narrow ranges frequent fills can accumulate fees.

pyramiding = 100 grows exposure quickly; monitor margin closely.

6. Risk disclaimer

This script is for educational and research purposes only. Historical performance does not guarantee future results. Before going live:

Forward-test bar-by-bar;

Check that your broker supports similar order handling;

Apply sound position sizing and, where appropriate, stop-losses or hedging.

XAUT Box with RSI Div(Dynamic Adjustment + MA + Short + English)Strategy Overview: Box Range with RSI Divergence (Dynamic Adjustment - OKX Signal Format)

This Pine Script strategy, "XAUT Box with RSI Div (Dynamic Adjustment + MA + Short + English )", is designed for trading within a box range while leveraging RSI divergences and moving average trends. It is optimized for use with OKX signal credentials and integrates TradingView alerts for automated trading.

Optimal Configuration

Take-Profit: 18% return rate.

Initial Margin: $50.

Total Margin: $800 USDT.

Expected Monthly Return: 10%+.

[Myth Busting] [ORB] Casper SMC - 16 JunJust showcase of YouTube strategy claimed to be profitable and fool proof. Not on every asset and not long-term though