TrendTwisterV1.5 (Forex Ready + Indicators)A Precision Trend-Following TradingView Strategy for Forex**

HullShiftFX is a Pine Script strategy for TradingView that combines the power of the **Hull Moving Average (HMA)** and a **shifted Exponential Moving Average (EMA)** with multi-layered momentum filters including **RSI** and **dual Stochastic Oscillators**.

It’s designed for traders looking to catch high-probability breakouts with tight risk management and visual clarity.

Chart settings:

1. Select "Auto - Fits data to screen"

2. Please Select "Scale Price Chart Only" (To make the chart not squished)

### ✅ Entry Conditions

**Long Position:**

- Price closes above the 12-period Hull Moving Average.

- Price closes above the 5-period EMA shifted forward by 2 bars.

- RSI is above 50.

- Stochastic Oscillator (12,3,3) %K is above 50.

- Stochastic Oscillator (5,3,3) %K is above 50.

- Hull MA crosses above the shifted EMA.

**Short Position:**

- Price closes below the 12-period Hull Moving Average.

- Price closes below the 5-period EMA shifted forward by 2 bars.

- RSI is below 50.

- Stochastic Oscillator (12,3,3) %K is below 50.

- Stochastic Oscillator (5,3,3) %K is below 50.

- Hull MA crosses below the shifted EMA.

---

## 📉 Risk Management

- **Stop Loss:** Set at the low (for long) or high (for short) of the previous 2 candles.

- **Take Profit:** Calculated at a risk/reward ratio of **1.65x** the stop loss distance.

---

## 📊 Indicators Used

- **Hull Moving Average (12)**

- **Exponential Moving Average (5) **

- **Relative Strength Index (14)**

- **Stochastic Oscillators:**

- %K (12,3,3)

- %K (5,3,3)

Indicators and strategies

Donchian Breakout Strategy📈 Donchian Breakout Strategy (Inspired by Way of the Turtle)

This strategy is a modern adaptation of the legendary Turtle Trading system as taught in Way of the Turtle by Curtis Faith — re-engineered for the crypto market’s volatility, 24/7 nature, and frequent fakeouts.

⸻

🐢 Original Inspiration

The original Turtle system, created by Richard Dennis and William Eckhardt, used:

• Breakouts of Donchian Channels (20-day for entry, 10-day for exit)

• Volatility-based position sizing using ATR (N)

• Simple rules, big trend exposure, and pyramiding to grow winners

It was built for futures and commodities, trading daily bars, assuming stable trading hours and regulated markets.

⸻

🚀 What’s Different in This Strategy?

✅ Optimized for Crypto

• Adapts to constant volatility and price manipulation common in crypto

• Adds commission modeling for realistic results (0.045% default)

✅ Improved Entry Filtering

• Uses EMA filter to align with trend direction

• Adds RSI momentum check to avoid early or weak breakouts

• Optional volatility and volume filters to reduce false signals

✅ Smarter Exits

• ATR-based volatility stop loss, not just Donchian reversal

• Avoids pyramiding to reduce risk from sudden reversals

✅ Backtest-Friendly

• Default backtest window starts from 2025-01-01

• Fully configurable: long/short toggle, filter control, stop loss multiplier

⸻

🧪 Use Case

• Best on trending coins with strong directional moves

• Avoids chop via filters, preserving capital

• Can be tuned for aggressive or conservative setups with just a few tweaks

Dkoderweb repainting issue fix strategyHarmonic Pattern Recognition Trading Strategy

This TradingView strategy called "Dkoderweb repainting issue fix strategy" is designed to identify and trade harmonic price patterns with optimized entry and exit points using Fibonacci levels. The strategy implements various popular harmonic patterns including Bat, Butterfly, Gartley, Crab, Shark, ABCD, and their anti-patterns.

Key Features

Pattern Recognition: Identifies 17+ harmonic price patterns including standard and anti-patterns

Fibonacci-Based Entries and Exits: Uses customizable Fibonacci levels for precision entries, take profits, and stop losses

Alternative Timeframe Analysis: Option to use higher timeframes for pattern identification

Heiken Ashi Support: Optional use of Heiken Ashi candles instead of regular candlesticks

Visual Indicators:

Pattern visualization with ZigZag indicator

Buy/sell signal markers

Color-coded background to highlight active trade zones

Customizable Fibonacci level display

How It Works

The strategy uses a ZigZag-based pattern identification system to detect pivot points

When a valid harmonic pattern forms, the strategy calculates the optimal entry window using the specified Fibonacci level (default 0.382)

Entries trigger when price returns to the entry window after pattern completion

Take profit and stop loss levels are automatically set based on customizable Fibonacci ratios

Visual alerts notify you of entries and exits

The strategy tracks active trades and displays them with background color highlights

Customizable Settings

Trade size

Entry window Fibonacci level (default 0.382)

Take profit Fibonacci level (default 0.618)

Stop loss Fibonacci level (default -0.618)

Alert messages for entries and exits

Display options for specific Fibonacci levels

Alternative timeframe selection

This strategy is designed to fix repainting issues that are common in harmonic pattern strategies, ensuring more reliable signals and backtesting results.

Daily Bollinger Band StrategyOverview of the Daily Bollinger Band Strategy

1. Strategy Overview and Features

This strategy is a tool for backtesting a trading method that uses Bollinger Bands. It is *not* a tool for automated trading.

1-1. Main Display Items

The main chart displays the Bollinger Bands and the 200-day moving average.

It also shows the entry and exit points along with the position size (in units of 100 shares).

1-2. Summary of Trading Rules

For long (buy) strategies, the trade enters when the price crosses above the +1σ line of the Bollinger Bands, aiming to ride an upward trend. The position is exited when the price crosses below the middle band.

For short (sell) strategies, the trade enters when the price crosses below the -1σ line of the Bollinger Bands, aiming to ride a downward trend. The position is exited when the price crosses above the middle band.

1-3. Strategic Enhancements

The strategy uses the slope of the 200-day moving average to determine the trend direction and enter trades accordingly. This improves the win rate and payoff ratio.

Additionally, to reduce the probability of ruin, the risk per trade is limited to 1.0% of capital, and position sizing is adjusted using ATR (a volatility indicator).

2. Trading Rules

2-1. Chart Type

Only daily charts are used.

2-2. Indicators Used

(1) Bollinger Bands** (used for entry and exit signals)

- Period: Fixed at 80 days

- Upper and lower bands: Fixed at ±1σ

(2) Moving Average** (used to determine trend direction)

- Period: Fixed at 200 days

- Trend direction is judged based on whether the difference from the previous day is positive (upward) or negative (downward)

2-3. Buy Rules

Setup:

- Price crosses above the +1σ line from below

- Both the middle band and 200-day moving average are upward sloping

Entry:

- Buy at the next day’s market open using a market order

Exit:

- If the price crosses below the middle band, sell at the next day’s open using a market order

2-4. Sell Rules

Setup:

- Price crosses below the -1σ line from above

- Both the middle band and 200-day moving average are downward sloping

Entry:

- Sell at the next day’s market open using a market order

Exit:

- If the price crosses above the middle band, buy back at the next day’s open using a market order

2-5. Risk Management Rules

- Risk per trade: 1.0% of total capital (acceptable loss = capital × 1.0%)

- Position size: Acceptable loss ÷ 2ATR (rounded down to the nearest unit of 100 shares)

2-6. Other Notes

- No brokerage fees

- No pyramiding

- No partial exits

- No reverse positions (no “stop-and-reverse” trades)

3. Strategy Parameters

The following settings can be specified:

3-1. Period Settings

- Start date: Set the start date for the backtest period

- Stop date: Set the end date for the backtest period

3-2. Display of Trend and Signals

- Show trend: When checked, the background color of the bars is light red for an uptrend and light blue for a downtrend

- Show signal: When checked, entry and exit signals are displayed (note: signals are executed at the next day’s open, so there is a one-day lag in the display)

3-3. Capital Management Settings

- Funds: Capital available for trading (in JPY)

- Risk rate: Specify what percentage of the capital to risk per trade

Settings in the “Properties” tab are not used in this strategy.

4. Backtest Results (Example)

Here are the backtest results conducted by the author:

- Target Stocks: All components of the Nikkei 225

- Test Period: January 4, 2000 – December 30, 2024

- Data Points: 12,886

- Win Rate: 33.45%

- Net Profit: ¥82,132,380

- Payoff Ratio: 2.450

- Expected Value: ¥6,373.8

- Risk Rate: 1.0%

- Probability of Ruin: 0.00%

---

デイリー・ボリンジャーバンド・ストラテジーの概要

1. ストラテジーの概要と特徴

このストラテジーは、ボリンジャーバンドを使ったトレード手法のバックテストを行うツールです。自動売買を行うツールではありません。

1-1. 主な表示項目

メインチャートにボリンジャーバンドと 200日移動平均線を表示します。

また、エントリーと手仕舞いのタイミングと数量(100株単位)も表示されます。

1-2. トレードルールの概要

買い戦略の場合、ボリンジャーバンドの +1σ 超えでエントリーして上昇トレンドに乗り、ミドルバンドを割ったら決済します。

売り戦略の場合、ボリンジャーバンドの -1σ 割りでエントリーして下降トレンドに乗り、ミドルバンドを上抜けたら決済します。

1-3. ストラテジーの工夫点

200日移動平均線の傾きを見てトレンド方向にエントリーをしています。こうして勝率とペイオフレシオの成績を向上しています。

また、破産確率を抑えるために、リスク資金比率を 1.0% にして、ATR(ボラティリティ指標) を使って注文数を調整しています。

2. 売買ルール

2-1. 使用するチャート

日足チャートに限定します

2-2. 使用する指標

(1) ボリンジャーバンド(仕掛けと手仕舞いのシグナルに使用)

期間は80日に固定

上下バンドは ±1σ に固定

(2) 移動平均線(トレンドの方向を見るために使用)

期間は200日に固定

移動平均の値の前日との差がプラスのとき上向き、マイナスのとき下向きと判断

2-3. 買いのルール

セットアップ:ボリンジャーバンドの +1σ を価格が下から上に交差 かつ ミドルバンドと 200日移動平均線が上向き

仕掛け:翌日の寄り付きに成行で買う

手仕舞い:ボリンジャーバンドのミドルバンドを価格が上から下に交差したら、翌日の寄り付きに成行で売る

2-4. 売りのルール

セットアップ:ボリンジャーバンドの -1σ を価格が上から下に交差 かつ ミドルバンドと 200日移動平均線が下向き

仕掛け:翌日の寄り付きに成行で売る

手仕舞い:ボリンジャーバンドのミドルバンドを価格が下から上に交差したら、翌日の寄り付きに成行で買い戻す

2-5. 資金管理のルール

リスク資金比率:資産の 1.0%(許容損失 = 資産 × 1.0%)

注文数:許容損失 ÷ 2ATR(単元株数未満は切り捨て)

2-6. その他

仲介手数料:なし

ピラミッディング:なし

分割決済:なし

ドテン:しない

3. ストラテジーのパラメーター

次の項目が指定できます。

3-1. 期間の設定

Staer date : バックテストの検証期間の開始日を指定します

Stop date : バックテストの検証期間の終了日を指定します

3-2. トレンドとシグナルの表示

Show trend : チェックを入れると、バーの背景色が、トレンドが上昇のときは薄い赤で、下落のときは薄い青で表示されます

Show signal : チェックを入れると、エントリーと手仕舞いのシグナルを表示します(シグナルの出た翌日の寄り付きに売買をするので表示に1日のずれがあります)

3-3. 資金管理用の設定

Funds : トレード用の資金(円)

Risk rate : 許容損失を資金の何%にするかで指定します

「プロパティタブ」で設定する値は、このストラテジーでは有効ではありません。

4. バックテストの結果(例)

作者がバックテストを実施した結果をお知らせします。

対象銘柄:日経225構成銘柄すべて

対象期間:2000年1月4日~2024年12月30日

データ件数:12,886

勝率:33.45%

純利益:82,132,380

ペイオフレシオ:2.450

期待値:6,373.8

リスク資金比率:1.0%

破産確率:0.00%

NY First Candle Break and RetestStrategy Overview

Session and Time Parameters:

The strategy focuses on the New York trading session, starting at 9:30 AM and lasting for a predefined session length, typically 3 to 4 hours. This timing captures the most active market hours, providing ample trading opportunities.

Strategy Parameters:

Utilizes the Average True Range (ATR) to set dynamic stop-loss levels, ensuring risk is managed according to market volatility.

Employs a reward-to-risk ratio to determine take profit levels, aiming for a balanced approach between potential gains and losses.

Strategy Settings:

Incorporates simple moving averages (EMA) and the Volume Weighted Average Price (VWAP) to identify trend direction and price levels.

Volume confirmation is used to validate breakouts, ensuring trades are based on significant market activity.

Trade Management:

Features a trailing stop mechanism to lock in profits as the trade moves in favor, with multiple take profit levels to secure gains incrementally.

The strategy is designed to handle both long and short positions, adapting to market conditions.

Alert Settings:

Provides alerts for key events such as session start, breakout, retest, and entry signals, helping traders stay informed and act promptly.

Visual cues on the chart highlight entry and exit points, making it easier for beginners to follow the strategy.

This strategy is particularly suited for the current volatile market environment, where simplicity and clear guidelines can help beginner traders navigate the complexities of trading. It emphasizes risk management and uses straightforward indicators to make informed trading decisions.

I put together this Trading View scalping strategy for futures markets with some help from Claude AI. Shoutout to everyone who gave me advice along the way—I really appreciate it! I’m sure there’s room for improvement, so feel free to share your thoughts… just go easy on me. :)

Dskyz Adaptive Futures Elite (DAFE)Dskyz Adaptive Futures Edge (DAFE)

imgur.com

A Dynamic Futures Trading Strategy

DAFE adapts to market volatility and price action using technical indicators and advanced risk management. It’s built for high-stakes futures trading (e.g., MNQ, BTCUSDT.P), offering modular logic for scalpers and swing traders alike.

Key Features

Adaptive Moving Averages

Dynamic Logic: Fast and slow SMAs adjust lengths via ATR, reacting to momentum shifts and smoothing in calm markets.

Signals: Long entry on fast SMA crossing above slow SMA with price confirmation; short on cross below.

RSI Filtering (Optional)

Momentum Check: Confirms entries with RSI crossovers (e.g., above oversold for longs). Toggle on/off with custom levels.

Fine-Tuning: Adjustable lookback and thresholds (e.g., 60/40) for precision.

Candlestick Pattern Recognition

Eng|Enhanced Detection: Identifies strong bullish/bearish engulfing patterns, validated by volume and range strength (vs. 10-period SMA).

Conflict Avoidance: Skips trades if both patterns appear in the lookback window, reducing whipsaws.

Multi-Timeframe Trend Filter

15-Minute Alignment: Syncs intrabar trades with 15-minute SMA trends; optional for flexibility.

Dollar-Cost Averaging (DCA) New!

Scaling: Adds up to a set number of entries (e.g., 4) on pullbacks/rallies, spaced by ATR multiples.

Control: Caps exposure and resets on exit, enhancing trend-following potential.

Trade Execution & Risk Management

Entry Rules: Prioritizes moving averages or patterns (user choice), with volume, volatility, and time filters.

Stops & Trails:

Initial Stop: ATR-based (2–3.5x, volatility-adjusted).

Trailing Stop: Locks profits with configurable ATR offset and multiplier.

Discipline

Cooldown: Pauses post-exit (e.g., 0–5 minutes).

Min Hold: Ensures trades last a set number of bars (e.g., 2–10).

Visualization & Tools

Charts: Overlays MAs, stops, and signals; trend shaded in background.

Dashboard: Shows position, P&L, win rate, and more in real-time.

Debugging: Logs signal details for optimization.

Input Parameters

Parameter Purpose Suggested Use

Use RSI Filter - Toggle RSI confirmation *Disable 4 price-only

trading

RSI Length - RSI period (e.g., 14) *7–14 for sensitivity

RSI Overbought/Oversold - Adjust for market type *Set levels (e.g., 60/40)

Use Candlestick Patterns - Enables engulfing signals *Disable for MA focus

Pattern Lookback - Pattern window (e.g., 19) *10–20 bars for balance

Use 15m Trend Filter - Align with 15-min trend *Enable for trend trades

Fast/Slow MA Length - Base MA lengths (e.g., 9/19) *10–25 / 30–60 per

timeframe

Volatility Threshold - Filters volatile spikes *Max ATR/close (e.g., 1%)

Min Volume - Entry volume threshold *Avoid illiquid periods

(e.g., 10)

ATR Length - ATR period (e.g., 14) *Standard volatility

measure

Trailing Stop ATR Offset - Trail distance (e.g., 0.5) *0.5–1.5 for tightness

Trailing Stop ATR Multi - Trail multiplier (e.g., 1.0) *1–3 for trend room

Cooldown Minutes - Post-exit pause (e.g., 0–5) *Prevents overtrading

Min Bars to Hold - Min trade duration (e.g., 2) *5–10 for intraday

Trading Hours - Active window (e.g., 9–16) *Focus on key sessions

Use DCA - Toggle DCA *Enable for scaling

Max DCA Entries - Cap entries (e.g., 4) *Limit risk exposure

DCA ATR Multiplier Entry spacing (e.g., 1.0) *1–2 for wider gaps

Compliance

Realistic Testing: Fixed quantities, capital, and slippage for accurate backtests.

Transparency: All logic is user-visible and adjustable.

Risk Controls: Cooldowns, stops, and hold periods ensure stability.

Flexibility: Adapts to various futures and timeframes.

Summary

DAFE excels in volatile futures markets with adaptive logic, DCA scaling, and robust risk tools. Currently in prop account testing, it’s a powerful framework for precision trading.

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

Fibonacci Counter-Trend TradingOverview:

The Fibonacci Counter-Trend Trading strategy is designed to capitalize on price reversals by utilizing Fibonacci levels calculated from the standard deviation of price movements. This strategy opens a sell order when the closing price crosses above a specified upper Fibonacci level and a buy order when the closing price crosses below a specified lower Fibonacci level. By leveraging the principles of Fibonacci retracement and volatility, this strategy aims to identify potential reversal points in the market.

How It Works:

Fibonacci Levels Calculation:

The strategy calculates upper and lower Fibonacci levels based on the standard deviation of the price over a specified moving average length. These levels are derived from the Fibonacci sequence, which is widely used in technical analysis to identify potential support and resistance levels.

The upper levels are calculated by adding specific Fibonacci ratios (0.236, 0.382, 0.5, 0.618, 0.764, and 1.0) multiplied by the standard deviation to the basis (the volume-weighted moving average).

The lower levels are calculated by subtracting the same Fibonacci ratios multiplied by the standard deviation from the basis.

Trade Entry Rules:

Sell Order: A sell order is triggered when the closing price crosses above the selected upper Fibonacci level. This indicates a potential reversal point where the price may start to decline.

Buy Order: A buy order is initiated when the closing price crosses below the selected lower Fibonacci level. This suggests a potential reversal point where the price may begin to rise.

Trade Management:

The strategy includes stop-losses based on the Fibonacci levels to protect against adverse price movements.

How to Use:

Users can customize the moving average length and the multiplier for the standard deviation to suit their trading preferences and market conditions.

The strategy can be applied to various financial instruments, including stocks, forex, and cryptocurrencies, making it versatile for different trading environments.

Pros:

The Fibonacci Counter-Trend Trading strategy combines the mathematical principles of the Fibonacci sequence with the statistical measure of standard deviation, providing a unique approach to identifying potential market reversals.

This strategy is particularly useful in volatile markets where price swings can lead to significant trading opportunities.

The use of Fibonacci levels can help traders identify key support and resistance areas, enhancing decision-making.

Cons:

The strategy may generate false signals in choppy or sideways markets, leading to potential losses if the price does not reverse as anticipated.

Relying solely on Fibonacci levels without considering other technical indicators or market conditions may result in missed opportunities or increased risk.

The effectiveness of the strategy can vary depending on the chosen parameters (e.g., moving average length and standard deviation multiplier), requiring users to spend time optimizing these settings for different market conditions.

As with any counter-trend strategy, there is a risk of significant drawdowns during strong trending markets, where the price continues to move in one direction without reversing.

By understanding the mechanics of the Fibonacci Counter-Trend Trading strategy, along with its pros and cons, traders can effectively implement it in their trading routines and potentially enhance their trading performance.

BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

[SM-042] EMA 5-8-13 with ADX FilterWhat is the strategy?

The strategy combines three exponential moving averages (EMAs) — 5, 8, and 13 periods — with an optional ADX (Average Directional Index) filter. It is designed to enter long or short positions based on EMA crossovers and to exit positions when the price crosses a specific EMA. The ADX filter, if enabled, adds a condition that only allows trades when the ADX value is above a certain threshold, indicating trend strength.

Who is it for?

This strategy is for traders leveraging EMAs and trend strength indicators to make trade decisions. It can be used by anyone looking for a simple trend-following strategy, with the flexibility to adjust for trend strength using the ADX filter.

When is it used?

- **Long trades**: When the 5-period EMA crosses above the 8-period EMA, with an optional ADX condition (if enabled) that requires the ADX value to be above a specified threshold.

- **Short trades**: When the 5-period EMA crosses below the 8-period EMA, with the ADX filter again optional.

- **Exits**: The strategy exits a long position when the price falls below the 13-period EMA and exits a short position when the price rises above the 13-period EMA.

Where is it applied?

This strategy is applied on a chart with any asset on TradingView, with the EMAs and ADX plotted for visual reference. The strategy uses `strategy.entry` to open positions and `strategy.close` to close them based on the set conditions.

Why is it useful?

This strategy helps traders identify trending conditions and filter out potential false signals by using both EMAs (to capture short-term price movements) and the ADX (to confirm the strength of the trend). The ADX filter can be turned off if not desired, making the strategy flexible for both trending and range-bound markets.

How does it work?

- **EMA Crossover**: The strategy enters a long position when the 5-period EMA crosses above the 8-period EMA, and enters a short position when the 5-period EMA crosses below the 8-period EMA.

- **ADX Filter**: If enabled, the strategy checks whether the ADX value is above a set threshold (default is 20) before allowing a trade.

- **Exit Conditions**: Long positions are closed when the price falls below the 13-period EMA, and short positions are closed when the price rises above the 13-period EMA.

- **Plotting**: The strategy plots the three EMAs and the ADX value on the chart for visualization. It also displays a horizontal line at the ADX threshold.

This setup allows for clear decision-making based on the interaction between different time-frame EMAs and trend strength as indicated by ADX.

Follow Line Strategy Version 2.5 (React HTF)Follow Line Strategy v2.5 (React HTF) - TradingView Script Usage

This strategy utilizes a "Follow Line" concept based on Bollinger Bands and ATR to identify potential trading opportunities. It includes advanced features like optional working hours filtering, higher timeframe (HTF) trend confirmation, and improved trend-following entry/exit logic. Version 2.5 introduces reactivity to HTF trend changes for more adaptive trading.

Key Features:

Follow Line: The core of the strategy. It dynamically adjusts based on price breakouts beyond Bollinger Bands, using either the low/high or ATR-adjusted levels.

Bollinger Bands: Uses a standard Bollinger Bands setup to identify overbought/oversold conditions.

ATR Filter: Optionally uses the Average True Range (ATR) to adjust the Follow Line offset, providing a more dynamic and volatility-adjusted entry point.

Optional Trading Session Filter: Allows you to restrict trading to specific hours of the day.

Higher Timeframe (HTF) Confirmation: A significant feature that allows you to confirm trade signals with the trend on a higher timeframe. This can help to filter out false signals and improve the overall win rate.

HTF Selection Method: Choose between Auto and Manual HTF selection:

Auto: The script automatically determines the appropriate HTF based on the current chart timeframe (e.g., 1min -> 15min, 5min -> 4h, 1h -> 1D, Daily -> Monthly).

Manual: Allows you to select a specific HTF using the Manual Higher Timeframe input.

Trend-Following Entries/Exits: The strategy aims to enter trades in the direction of the established trend, using the Follow Line to define the trend.

Reactive HTF Trend Changes: v2.5 exits positions not only based on the trade timeframe (TTF) trend changing, but also when the higher timeframe trend reverses against the position. This makes the strategy more responsive to larger market movements.

Alerts: Provides buy and sell alerts for convenient trading signal notifications.

Visualizations: Plots the Follow Line for both the trade timeframe and the higher timeframe (optional), making it easy to understand the strategy's logic.

How to Use:

Add to Chart: Add the "Follow Line Strategy Version 2.5 (React HTF)" script to your TradingView chart.

Configure Settings: Customize the strategy's settings to match your trading style and preferences. Here's a breakdown of the key settings:

Indicator Settings:

ATR Period: The period used to calculate the ATR. A smaller period is more sensitive to recent price changes.

Bollinger Bands Period: The period used for the Bollinger Bands calculation. A longer period results in smoother bands.

Bollinger Bands Deviation: The number of standard deviations from the moving average that the Bollinger Bands are plotted. Higher deviations create wider bands.

Use ATR for Follow Line Offset?: Enable to use ATR to calculate the Follow Line offset. Disable to use the simple high/low.

Show Trade Signals on Chart?: Enable to show BUY/SELL labels on the chart.

Time Filter:

Use Trading Session Filter?: Enable to restrict trading to specific hours of the day.

Trading Session: The trading session to use (e.g., 0930-1600 for regular US stock market hours). Use 0000-2400 for all hours.

Higher Timeframe Confirmation:

Enable HTF Confirmation?: Enable to use the HTF trend to filter trade signals. If enabled, only trades in the direction of the HTF trend will be taken.

HTF Selection Method: Choose between "Auto" and "Manual" HTF selection.

Manual Higher Timeframe: If "Manual" is selected, choose the specific HTF (e.g., 240 for 4 hours, D for daily).

Show HTF Follow Line?: Enable to plot the HTF Follow Line on the chart.

Understanding the Signals:

Buy Signal: The price breaks above the upper Bollinger Band, and the HTF (if enabled) confirms the uptrend.

Sell Signal: The price breaks below the lower Bollinger Band, and the HTF (if enabled) confirms the downtrend.

Exit Long: The trade timeframe trend changes to downtrend or the higher timeframe trend changes to downtrend.

Exit Short: The trade timeframe trend changes to uptrend or the higher timeframe trend changes to uptrend.

Alerts:

The script includes alert conditions for buy and sell signals. To set up alerts, click the "Alerts" button in TradingView and select the desired alert condition from the script. The alert message provides the ticker and interval.

Backtesting and Optimization:

Use TradingView's Strategy Tester to backtest the strategy on different assets and timeframes.

Experiment with different settings to optimize the strategy for your specific trading style and risk tolerance. Pay close attention to the ATR Period, Bollinger Bands settings, and the HTF confirmation options.

Tips and Considerations:

HTF Confirmation: The HTF confirmation can significantly improve the strategy's performance by filtering out false signals. However, it can also reduce the number of trades.

Risk Management: Always use proper risk management techniques, such as stop-loss orders and position sizing, when trading any strategy.

Market Conditions: The strategy may perform differently in different market conditions. It's important to backtest and optimize the strategy for the specific markets you are trading.

Customization: Feel free to modify the script to suit your specific needs. For example, you could add additional filters or entry/exit conditions.

Pyramiding: The pyramiding = 0 setting prevents multiple entries in the same direction, ensuring the strategy doesn't compound losses. You can adjust this value if you prefer to pyramid into winning positions, but be cautious.

Lookahead: The lookahead = barmerge.lookahead_off setting ensures that the HTF data is calculated based on the current bar's closed data, preventing potential future peeking bias.

Trend Determination: The logic for determining the HTF trend and reacting to changes is critical. Carefully review the f_calculateHTFData function and the conditions for exiting positions to ensure you understand how the strategy responds to different market scenarios.

Disclaimer:

This script is for informational and educational purposes only. It is not financial advice, and you should not trade based solely on the signals generated by this script. Always do your own research and consult with a qualified financial advisor before making any trading decisions. The author is not responsible for any losses incurred as a result of using this script.

Scalping 15min: EMA + MACD + RSI + ATR-based SL/TP📈 Strategy: 15-Minute Scalping — EMA + MACD + RSI + ATR-based SL/TP

This scalping strategy is designed for 15-minute charts and combines trend-following and momentum confirmation with dynamic stop loss and take profit levels based on volatility.

🔧 Indicators Used:

EMA 50 — identifies the main trend

MACD Histogram — confirms momentum direction

RSI (14) — filters overbought/oversold conditions

ATR (14) — dynamically sets SL and TP based on market volatility

📊 Entry Conditions:

Long Entry:

Price is above EMA 50

MACD histogram is positive

RSI is above 50 but below 70

Short Entry:

Price is below EMA 50

MACD histogram is negative

RSI is below 50 but above 30

🛑 Risk Management:

Stop Loss: 1×ATR (user-configurable)

Take Profit: 2×ATR (user-configurable)

These values can be adjusted in the script inputs depending on your risk/reward preference or market conditions.

⚠️ Notes:

Strategy is optimized for scalping fast-moving pairs (e.g. crypto, forex).

Works best in trending markets.

Use backtesting and forward testing before live trading.

50 EMA Crossover With Monthly DCARecommended Chart Interval = 1W

Overview:

This strategy combines trend-following principles with dollar-cost averaging (DCA), aiming to efficiently deploy capital while minimizing market timing risk.

How It Works:

When the Long Condition is Not Met (i.e., Price < 50 EMA):

- If the price is below the 50 EMA, a fixed DCA amount is added to a cash reserve every month.

- This ensures that capital is consistently accumulated, even when the strategy isn't in a long position.

When the Long Condition is Met (i.e., Price > 50 EMA):

- A long position is opened when the price is above the 50 EMA.

- At this point, the entire capital, including the accumulated cash reserve, is deployed into the market.

- While the strategy is long, a DCA buy order is placed every month using the set DCA amount, continuously investing as the market conditions allow.

Exit Strategy:

If the price falls below the 50 EMA, the strategy closes all positions, and the cash reserve accumulation process begins again.

Key Benefits:

✔ Systematic Investing: Ensures consistent capital deployment while following trend signals.

✔ Cash Efficiency: Accumulates uninvested funds when conditions aren’t met and deploys them at optimal moments.

✔ Risk Management: Exits when the price trend weakens, protecting capital.

Conclusion:

This method allows for efficient capital growth by combining a trend-following approach with disciplined DCA, ensuring risk is managed while capital is deployed systematically at optimal points in the market. 🚀

Trailing Monster StrategyTrailing Monster Strategy

This is an experimental trend-following strategy that incorporates a custom adaptive moving average (PKAMA), RSI-based momentum filtering, and dynamic trailing stop-loss logic. It is designed for educational and research purposes only, and may require further optimization or risk management considerations prior to live deployment.

Strategy Logic

The strategy attempts to participate in sustained price trends by combining:

- A Power Kaufman Adaptive Moving Average (PKAMA) for dynamic trend detection,

- RSI and Simple Moving Average (SMA) filters for market condition confirmation,

- A delayed trailing stop-loss to manage exits once a trade is in profit.

Entry Conditions

Long Entry:

- RSI exceeds the overbought threshold (default: 70),

- Price is trading above the 200-period SMA,

- PKAMA slope is positive (indicating upward momentum),

- A minimum number of bars have passed since the last entry.

Short Entry:

- RSI falls below the oversold threshold (default: 30),

- Price is trading below the 200-period SMA,

- PKAMA slope is negative (indicating downward momentum),

-A minimum number of bars have passed since the last entry.

Exit Conditions

- A trailing stop-loss is applied once the position has been open for a user-defined number of bars.

- The trailing distance is calculated as a fixed percentage of the average entry price.

Technical Notes

This script implements a custom version of the Power Kaufman Adaptive Moving Average (PKAMA), conceptually inspired by alexgrover’s public implementation on TradingView .

Unlike traditional moving averages, PKAMA dynamically adjusts its responsiveness based on recent market volatility, allowing it to better capture trend changes in fast-moving assets like altcoins.

Disclaimer

This strategy is provided for educational purposes only.

It is not financial advice, and no guarantee of profitability is implied.

Always conduct thorough backtesting and forward testing before using any strategy in a live environment.

Adjust inputs based on your individual risk tolerance, asset class, and trading style.

Feedback is encouraged. You are welcome to fork and modify this script to suit your own preferences and market approach.

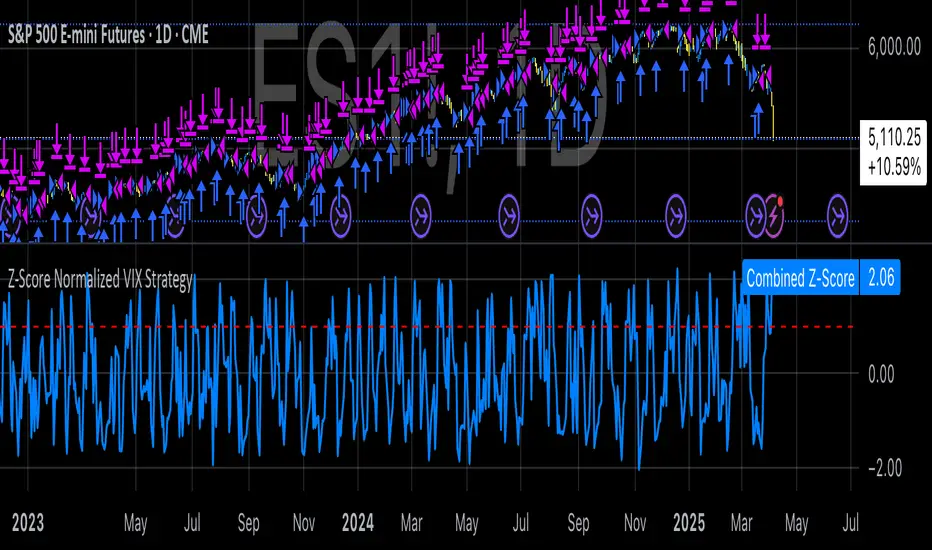

Z-Score Normalized VIX StrategyThis strategy leverages the concept of the Z-score applied to multiple VIX-based volatility indices, specifically designed to capture market reversals based on the normalization of volatility. The strategy takes advantage of VIX-related indicators to measure extreme levels of market fear or greed and adjusts its position accordingly.

1. Overview of the Z-Score Methodology

The Z-score is a statistical measure that describes the position of a value relative to the mean of a distribution in terms of standard deviations. In this strategy, the Z-score is calculated for various volatility indices to assess how far their values are from their historical averages, thus normalizing volatility levels. The Z-score is calculated as follows:

Z = \frac{X - \mu}{\sigma}

Where:

• X is the current value of the volatility index.

• \mu is the mean of the index over a specified period.

• \sigma is the standard deviation of the index over the same period.

This measure tells us how many standard deviations the current value of the index is away from its average, indicating whether the market is experiencing unusually high or low volatility (fear or calm).

2. VIX Indices Used in the Strategy

The strategy utilizes four commonly referenced volatility indices:

• VIX (CBOE Volatility Index): Measures the market’s expectations of 30-day volatility based on S&P 500 options.

• VIX3M (3-Month VIX): Reflects expectations of volatility over the next three months.

• VIX9D (9-Day VIX): Reflects shorter-term volatility expectations.

• VVIX (VIX of VIX): Measures the volatility of the VIX itself, indicating the level of uncertainty in the volatility index.

These indices provide a comprehensive view of the current volatility landscape across different time horizons.

3. Strategy Logic

The strategy follows a long entry condition and an exit condition based on the combined Z-score of the selected volatility indices:

• Long Entry Condition: The strategy enters a long position when the combined Z-score of the selected VIX indices falls below a user-defined threshold, indicating an abnormally low level of volatility (suggesting a potential market bottom and a bullish reversal). The threshold is set as a negative value (e.g., -1), where a more negative Z-score implies greater deviation below the mean.

• Exit Condition: The strategy exits the long position when the combined Z-score exceeds the threshold (i.e., when the market volatility increases above the threshold, indicating a shift in market sentiment and reduced likelihood of continued upward momentum).

4. User Inputs

• Z-Score Lookback Period: The user can adjust the lookback period for calculating the Z-score (e.g., 6 periods).

• Z-Score Threshold: A customizable threshold value to define when the market has reached an extreme volatility level, triggering entries and exits.

The strategy also allows users to select which VIX indices to use, with checkboxes to enable or disable each index in the calculation of the combined Z-score.

5. Trade Execution Parameters

• Initial Capital: The strategy assumes an initial capital of $20,000.

• Pyramiding: The strategy does not allow pyramiding (multiple positions in the same direction).

• Commission and Slippage: The commission is set at $0.05 per contract, and slippage is set at 1 tick.

6. Statistical Basis of the Z-Score Approach

The Z-score methodology is a standard technique in statistics and finance, commonly used in risk management and for identifying outliers or unusual events. According to Dumas, Fleming, and Whaley (1998), volatility indices like the VIX serve as a useful proxy for market sentiment, particularly during periods of high uncertainty. By calculating the Z-score, we normalize volatility and quantify the degree to which the current volatility deviates from historical norms, allowing for systematic entry and exit based on these deviations.

7. Implications of the Strategy

This strategy aims to exploit market conditions where volatility has deviated significantly from its historical mean. When the Z-score falls below the threshold, it suggests that the market has become excessively calm, potentially indicating an overreaction to past market events. Entering long positions under such conditions could capture market reversals as fear subsides and volatility normalizes. Conversely, when the Z-score rises above the threshold, it signals increased volatility, which could be indicative of a bearish shift in the market, prompting an exit from the position.

By applying this Z-score normalized approach, the strategy seeks to achieve more consistent entry and exit points by reducing reliance on subjective interpretation of market conditions.

8. Scientific Sources

• Dumas, B., Fleming, J., & Whaley, R. (1998). “Implied Volatility Functions: Empirical Tests”. The Journal of Finance, 53(6), 2059-2106. This paper discusses the use of volatility indices and their empirical behavior, providing context for volatility-based strategies.

• Black, F., & Scholes, M. (1973). “The Pricing of Options and Corporate Liabilities”. Journal of Political Economy, 81(3), 637-654. The original Black-Scholes model, which forms the basis for many volatility-related strategies.

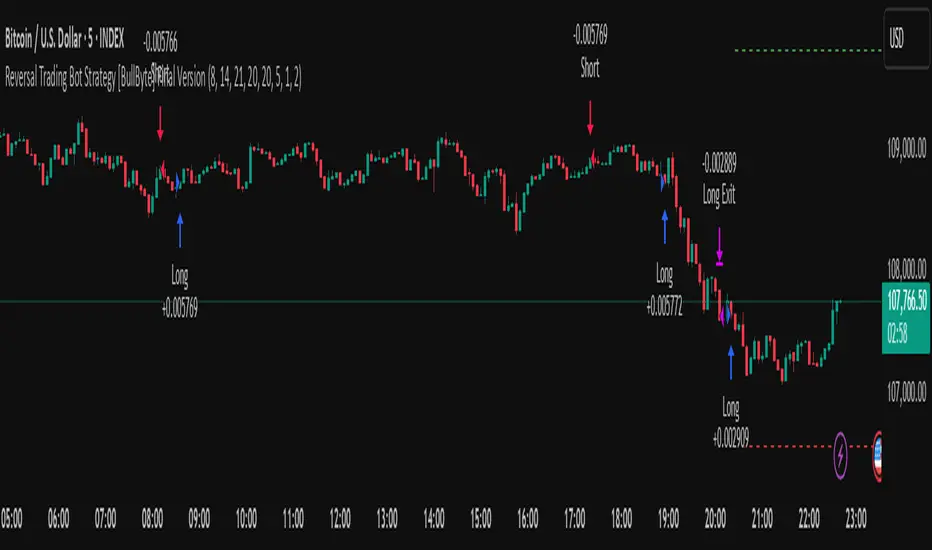

Reversal Trading Bot Strategy[BullByte]Overview :

The indicator Reversal Trading Bot Strategy is crafted to capture potential market reversal points by combining momentum, volatility, and trend alignment filters. It uses a blend of technical indicators to identify both bullish and bearish reversal setups, ensuring that multiple market conditions are met before entering a trade.

Core Components :

Technical Indicators Used :

RSI (Relative Strength Index) :

Purpose : Detects divergence conditions by comparing recent lows/highs in price with the RSI.

Parameter : Length of 8.

Bollinger Bands (BB) :

Purpose : Measures volatility and identifies price levels that are statistically extreme.

Parameter : Length of 20 and a 2-standard deviation multiplier.

ADX (Average Directional Index) & DMI (Directional Movement Index) :

Purpose : Quantifies the strength of the trend. The ADX threshold is set at 20, and additional filters check for the alignment of the directional indicators (DI+ and DI–).

ATR (Average True Range) :

Purpose : Provides a volatility measure used to set stop levels and determine risk through trailing stops.

Volume SMA (Simple Moving Average of Volume ):

Purpose : Helps confirm strength by comparing the current volume against a 20-period average, with an optional filter to ensure volume is at least twice the SMA.

User-Defined Toggle Filters :

Volume Filter : Confirms that the volume is above average (or twice the SMA) before taking trades.

ADX Trend Alignment Filter : Checks that the ADX’s directional indicators support the trade direction.

BB Close Confirmation : Optionally refines the entry by requiring price to be beyond the upper or lower Bollinger Band rather than just above or below.

RSI Divergence Exit : Allows the script to close positions if RSI divergence is detected.

BB Mean Reversion Exit : Closes positions if the price reverts to the Bollinger Bands’ middle line.

Risk/Reward Filter : Ensures that the potential reward is at least twice the risk by comparing the distance to the Bollinger Band with the ATR.

Candle Movement Filter : Optional filter to require a minimum percentage move in the candle to confirm momentum.

ADX Trend Exit : Closes positions if the ADX falls below the threshold and the directional indicators reverse.

Entry Conditions :

Bullish Entry :

RSI Divergence : Checks if the current close is lower than a previous low while the RSI is above the previous low, suggesting bullish divergence.

Bollinger Confirmation : Requires that the price is above the lower (or upper if confirmation is toggled) Bollinger Band.

Volume & Trend Filters : Combines volume condition, ADX strength, and an optional candle momentum condition.

Risk/Reward Check : Validates that the trade meets a favorable risk-to-reward ratio.

Bearish Entry :

Uses a mirror logic of the bullish entry by checking for bearish divergence, ensuring the price is below the appropriate Bollinger level, and confirming volume, trend strength, candle pattern, and risk/reward criteria.

Trade Execution and Exit Strateg y:

Trade Execution :

Upon meeting the entry conditions, the strategy initiates a long or short position.

Stop Loss & Trailing Stops :

A stop-loss is dynamically set using the ATR value, and trailing stops are implemented as a percentage of the close price.

Exit Conditions :

Additional exit filters can trigger early closures based on RSI divergence, mean reversion (via the middle Bollinger Band), or a weakening trend as signaled by ADX falling below its threshold.

This multi-layered exit strategy is designed to lock in gains or minimize losses if the market begins to reverse unexpectedly.

How the Strategy Works in Different Market Conditions :

Trending Markets :

The ADX filter ensures that trades are only taken when the trend is strong. When the market is trending, the directional movement indicators help confirm the momentum, making the reversal signal more reliable.

Ranging Markets :

In choppy markets, the Bollinger Bands expand and contract, while the RSI divergence can highlight potential turning points. The optional filters can be adjusted to avoid false signals in low-volume or low-volatility conditions.

Volatility Management :

With ATR-based stop-losses and a risk/reward filter, the strategy adapts to current market volatility, ensuring that risk is managed consistently.

Recommendation on using this Strategy with a Trading Bot :

This strategy is well-suited for high-frequency trading (HFT) due to its ability to quickly identify reversal setups and execute trades dynamically with automated stop-loss and trailing exits. By integrating this script with a TradingView webhook-based bot or an API-driven execution system, traders can automate trade entries and exits in real-time, reducing manual execution delays and capitalizing on fast market movements.

Disclaimer :

This script is provided for educational and informational purposes only. It is not intended as investment advice. Trading involves significant risk, and you should always conduct your own research and analysis before making any trading decisions. The author is not responsible for any losses incurred while using this script.

EMA 34 Crossover with Break Even Stop LossEMA 34 Crossover with Break Even Stop Loss Strategy

This trading strategy is based on the 34-period Exponential Moving Average (EMA) and aims to enter long positions when the price crosses above the EMA 34. The strategy is designed to manage risk effectively with a dynamic stop loss and take-profit mechanism.

Key Features:

EMA 34 Crossover:

The strategy generates a long entry signal when the closing price of the current bar crosses above the 34-period EMA, with the condition that the previous closing price was below the EMA. This crossover indicates a potential upward trend.

Risk Management:

Upon entering a trade, the strategy sets a stop loss at the low of the previous bar. This helps in controlling the downside risk.

A take profit level is set at a 10:1 risk-to-reward ratio, meaning the potential profit is ten times the amount risked on the trade.

Break-even Stop Loss:

As the price moves in favor of the trade and reaches a 3:1 risk-to-reward ratio, the strategy moves the stop loss to the entry price (break-even). This ensures that no loss will be incurred if the market reverses, effectively protecting profits.

Exit Conditions:

The strategy exits the trade when either the stop loss is hit (if the price drops below the stop loss level) or the take profit target is reached (if the price rises to the take profit level).

If the price reaches the break-even level (entry price), the stop loss is adjusted to lock in profits and prevent any loss.

Visualization:

The stop loss and take profit levels are plotted on the chart for easy visualization, helping traders track the status of their trade.

Trade Management Summary:

Long Entry: When price crosses above the 34-period EMA.

Stop Loss: Set to the low of the previous candle.

Take Profit: Set to a 10:1 risk-to-reward ratio.

Break-even: Stop loss is moved to entry price when a 3:1 risk-to-reward ratio is reached.

Exit: The trade is closed either when the stop loss or take profit levels are hit.

This strategy is designed to minimize losses by employing a dynamic stop loss and to maximize gains by setting a favorable risk-to-reward ratio, making it suitable for traders who prefer a structured, automated approach to risk management and trend-following.

BTC Trading RobotOverview

This Pine Script strategy is designed for trading Bitcoin (BTC) by placing pending orders (BuyStop and SellStop) based on local price extremes. The script also implements a trailing stop mechanism to protect profits once a position becomes sufficiently profitable.

________________________________________

Inputs and Parameter Setup

1. Trading Profile:

o The strategy is set up specifically for BTC trading.

o The systemType input is set to 1, which means the strategy will calculate trade parameters using the BTC-specific inputs.

2. Common Trading Inputs:

o Risk Parameters: Although RiskPercent is defined, its actual use (e.g., for position sizing) isn’t implemented in this version.

o Trading Hours Filter:

SHInput and EHInput let you restrict trading to a specific hour range. If these are set (non-zero), orders will only be placed during the allowed hours.

3. BTC-Specific Inputs:

o Take Profit (TP) and Stop Loss (SL) Percentages:

TPasPctBTC and SLasPctBTC are used to determine the TP and SL levels as a percentage of the current price.

o Trailing Stop Parameters:

TSLasPctofTPBTC and TSLTgrasPctofTPBTC determine when and by how much a trailing stop is applied, again as percentages of the TP.

4. Other Parameters:

o BarsN is used to define the window (number of bars) over which the local high and low are calculated.

o OrderDistPoints acts as a buffer to prevent the entry orders from being triggered too early.

________________________________________

Trade Parameter Calculation

• Price Reference:

o The strategy uses the current closing price as the reference for calculations.

• Calculation of TP and SL Levels:

o If the systemType is set to BTC (value 1), then:

Take Profit Points (Tppoints) are calculated by multiplying the current price by TPasPctBTC.

Stop Loss Points (Slpoints) are calculated similarly using SLasPctBTC.

A buffer (OrderDistPoints) is set to half of the take profit points.

Trailing Stop Levels:

TslPoints is calculated as a fraction of the TP (using TSLTgrasPctofTPBTC).

TslTriggerPoints is similarly determined, which sets the profit level at which the trailing stop will start to activate.

________________________________________

Time Filtering

• Session Control:

o The current hour is compared against SHInput (start hour) and EHInput (end hour).

o If the current time falls outside the allowed window, the script will not place any new orders.

________________________________________

Entry Orders

• Local Price Extremes:

o The strategy calculates a local high and local low using a window of BarsN * 2 + 1 bars.

• Placing Stop Orders:

o BuyStop Order:

A long entry is triggered if the current price is less than the local high minus the order distance buffer.

The BuyStop order is set to trigger at the level of the local high.

o SellStop Order:

A short entry is triggered if the current price is greater than the local low plus the order distance buffer.

The SellStop order is set to trigger at the level of the local low.

Note: Orders are only placed if there is no current open position and if the session conditions are met.

________________________________________

Trailing Stop Logic

Once a position is open, the strategy monitors profit levels to protect gains:

• For Long Positions:

o The script calculates the profit as the difference between the current price and the average entry price.

o If this profit exceeds the TslTriggerPoints threshold, a trailing stop is applied by placing an exit order.

o The stop price is set at a distance below the current price, while a limit (profit target) is also defined.

• For Short Positions:

o The profit is calculated as the difference between the average entry price and the current price.

o A similar trailing stop exit is applied if the profit exceeds the trigger threshold.

________________________________________

Summary

In essence, this strategy works by:

• Defining entry levels based on recent local highs and lows.

• Placing pending stop orders to enter the market when those levels are breached.

• Filtering orders by time, ensuring trades are only taken during specified hours.

• Implementing a trailing stop mechanism to secure profits once the trade moves favorably.

This approach is designed to automate BTC trading based on price action and dynamic risk management, although further enhancements (like dynamic position sizing based on RiskPercent) could be added for a more complete risk management system.

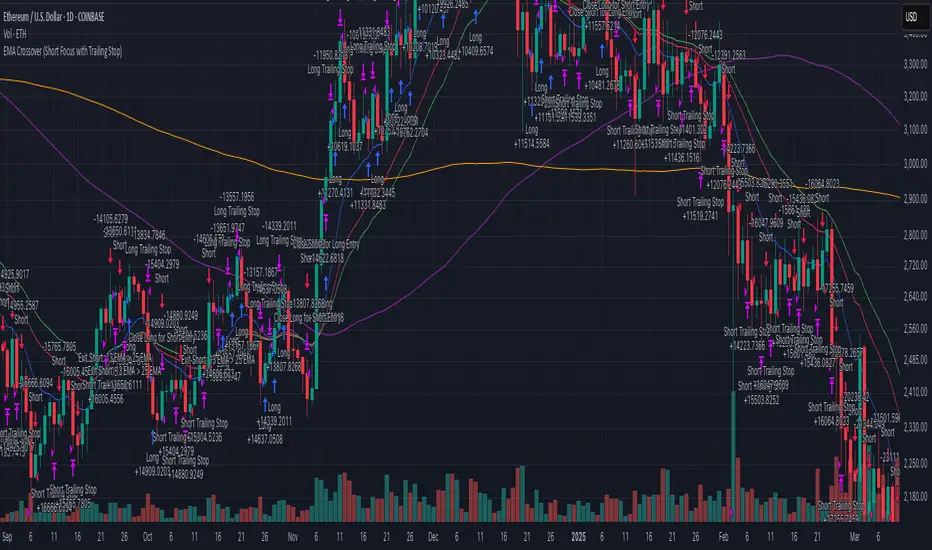

EMA Crossover (Short Focus with Trailing Stop)This strategy utilizes a combination of Exponential Moving Averages (EMA) and Simple Moving Averages (SMA) to generate entry and exit signals for both long and short positions. The core of the strategy is based on the 13-period EMA (short EMA) crossing the 33-period EMA (long EMA) for entering long trades, while a 13-period EMA crossing the 25-period EMA (mid EMA) generates short trade signals. The 100-period SMA and 200-period SMA serve as additional trend indicators to provide context for the market conditions. The strategy aims to capitalize on trend reversals and momentum shifts in the market.

The strategy is designed to execute trades swiftly with an emphasis on entering positions when conditions align in real time. For long entries, the strategy initiates a buy when the 13 EMA is greater than the 33 EMA, indicating a bullish trend. For short entries, the 13 EMA crossing below the 33 EMA signals a bearish trend, prompting a short position. Importantly, the code includes built-in exit conditions for both long and short positions. Long positions are exited when the 13 EMA falls below the 33 EMA, while short positions are closed when the 13 EMA crosses above the 25 EMA.

A key feature of the strategy is the use of trailing stops for both long and short positions. This dynamic exit method adjusts the stop level as the market moves in favor of the trade, locking in profits while reducing the risk of losses. The trailing stop for long positions is based on the high price of the current bar, while the trailing stop for short positions is set using the low price, providing more flexibility in managing risk. This trailing stop mechanism helps to capture profits from favorable market moves while ensuring that positions are exited if the market moves against them.

This strategy works best on the daily timeframe and is optimized for major cryptocurrency pairs. The daily chart allows for the EMAs to provide more reliable signals, as the strategy is designed to capture broader trends rather than short-term market fluctuations. Using it on major crypto pairs increases its effectiveness as these assets tend to have strong and sustained trends, providing better opportunities for the strategy to perform well.

Adaptive Fibonacci Pullback System -FibonacciFluxAdaptive Fibonacci Pullback System (AFPS) - FibonacciFlux

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0). Original concepts by FibonacciFlux.

Abstract

The Adaptive Fibonacci Pullback System (AFPS) presents a sophisticated, institutional-grade algorithmic strategy engineered for high-probability trend pullback entries. Developed by FibonacciFlux, AFPS uniquely integrates a proprietary Multi-Fibonacci Supertrend engine (0.618, 1.618, 2.618 ratios) for harmonic volatility assessment, an Adaptive Moving Average (AMA) Channel providing dynamic market context, and a synergistic Multi-Timeframe (MTF) filter suite (RSI, MACD, Volume). This strategy transcends simple indicator combinations through its strict, multi-stage confluence validation logic. Historical simulations suggest that specific MTF filter configurations can yield exceptional performance metrics, potentially achieving Profit Factors exceeding 2.6 , indicative of institutional-level potential, while maintaining controlled risk under realistic trading parameters (managed equity risk, commission, slippage).

4 hourly MTF filtering

1. Introduction: Elevating Pullback Trading with Adaptive Confluence

Traditional pullback strategies often struggle with noise, false signals, and adapting to changing market dynamics. AFPS addresses these challenges by introducing a novel framework grounded in Fibonacci principles and adaptive logic. Instead of relying on static levels or single confirmations, AFPS seeks high-probability pullback entries within established trends by validating signals through a rigorous confluence of:

Harmonic Volatility Context: Understanding the trend's stability and potential turning points using the unique Multi-Fibonacci Supertrend.

Adaptive Market Structure: Assessing the prevailing trend regime via the AMA Channel.

Multi-Dimensional Confirmation: Filtering signals with lower-timeframe Momentum (RSI), Trend Alignment (MACD), and Market Conviction (Volume) using the MTF suite.

The objective is to achieve superior signal quality and adaptability, moving beyond conventional pullback methodologies.

2. Core Methodology: Synergistic Integration

AFPS's effectiveness stems from the engineered synergy between its core components:

2.1. Multi-Fibonacci Supertrend Engine: Utilizes specific Fibonacci ratios (0.618, 1.618, 2.618) applied to ATR, creating a multi-layered volatility envelope potentially resonant with market harmonics. The averaged and EMA-smoothed result (`smoothed_supertrend`) provides a robust, dynamic trend baseline and context filter.

// Key Components: Multi-Fibonacci Supertrend & Smoothing

average_supertrend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_supertrend = ta.ema(average_supertrend, st_smooth_length)

2.2. Adaptive Moving Average (AMA) Channel: Provides dynamic market context. The `ama_midline` serves as a key filter in the entry logic, confirming the broader trend bias relative to adaptive price action. Extended Fibonacci levels derived from the channel width offer potential dynamic S/R zones.

// Key Component: AMA Midline

ama_midline = (ama_high_band + ama_low_band) / 2

2.3. Multi-Timeframe (MTF) Filter Suite: An optional but powerful validation layer (RSI, MACD, Volume) assessed on a lower timeframe. Acts as a **validation cascade** – signals must pass all enabled filters simultaneously.

2.4. High-Confluence Entry Logic: The core innovation. A pullback entry requires a specific sequence and validation:

Price interaction with `average_supertrend` and recovery above/below `smoothed_supertrend`.

Price confirmation relative to the `ama_midline`.

Simultaneous validation by all enabled MTF filters.

// Simplified Long Entry Logic Example (incorporates key elements)

long_entry_condition = enable_long_positions and

(low < average_supertrend and close > smoothed_supertrend) and // Pullback & Recovery

(close > ama_midline and close > ama_midline) and // AMA Confirmation

(rsi_filter_long_ok and macd_filter_long_ok and volume_filter_ok) // MTF Validation

This strict, multi-stage confluence significantly elevates signal quality compared to simpler pullback approaches.

1hourly filtering

3. Realistic Implementation and Performance Potential

AFPS is designed for practical application, incorporating realistic defaults and highlighting performance potential with crucial context:

3.1. Realistic Default Strategy Settings:

The script includes responsible default parameters:

strategy('Adaptive Fibonacci Pullback System - FibonacciFlux', shorttitle = "AFPS", ...,

initial_capital = 10000, // Accessible capital

default_qty_type = strategy.percent_of_equity, // Equity-based risk

default_qty_value = 4, // Default 4% equity risk per initial trade

commission_type = strategy.commission.percent,

commission_value = 0.03, // Realistic commission

slippage = 2, // Realistic slippage

pyramiding = 2 // Limited pyramiding allowed

)

Note: The default 4% risk (`default_qty_value = 4`) requires careful user assessment and adjustment based on individual risk tolerance.

3.2. Historical Performance Insights & Institutional Potential:

Backtesting provides insights into historical behavior under specific conditions (always specify Asset/Timeframe/Dates when sharing results):

Default Performance Example: With defaults, historical tests might show characteristics like Overall PF ~1.38, Max DD ~1.16%, with potential Long/Short performance variance (e.g., Long PF 1.6+, Short PF < 1).

Optimized MTF Filter Performance: Crucially, historical simulations demonstrate that meticulous configuration of the MTF filters (particularly RSI and potentially others depending on market) can significantly enhance performance. Under specific, optimized MTF filter settings combined with appropriate risk management (e.g., 7.5% risk), historical tests have indicated the potential to achieve **Profit Factors exceeding 2.6**, alongside controlled drawdowns (e.g., ~1.32%). This level of performance, if consistently achievable (which requires ongoing adaptation), aligns with metrics often sought in institutional trading environments.

Disclaimer Reminder: These results are strictly historical simulations. Past performance does not guarantee future results. Achieving high performance requires careful parameter tuning, adaptation to changing markets, and robust risk management.

3.3. Emphasizing Risk Management:

Effective use of AFPS mandates active risk management. Utilize the built-in Stop Loss, Take Profit, and Trailing Stop features. The `pyramiding = 2` setting requires particularly diligent oversight. Do not rely solely on default settings.

4. Conclusion: Advancing Trend Pullback Strategies

The Adaptive Fibonacci Pullback System (AFPS) offers a sophisticated, theoretically grounded, and highly adaptable framework for identifying and executing high-probability trend pullback trades. Its unique blend of Fibonacci resonance, adaptive context, and multi-dimensional MTF filtering represents a significant advancement over conventional methods. While requiring thoughtful implementation and risk management, AFPS provides discerning traders with a powerful tool potentially capable of achieving institutional-level performance characteristics under optimized conditions.

Acknowledgments

Developed by FibonacciFlux. Inspired by principles of Fibonacci analysis, adaptive averaging, and multi-timeframe confirmation techniques explored within the trading community.

Disclaimer

Trading involves substantial risk. AFPS is an analytical tool, not a guarantee of profit. Past performance is not indicative of future results. Market conditions change. Users are solely responsible for their decisions and risk management. Thorough testing is essential. Deploy at your own considered risk.

LUX CLARA - EMA + VWAP (No ATR Filter) - v6EMA STRAT SHOUT OUTOUTLIERSSSSS

Overview:

an intraday strategy built around two core principles:

Trend Confirmation using the 50 EMA (Exponential Moving Average) in relation to the VWAP (Volume-Weighted Average Price).

Entry Signals triggered by the 8 EMA crossing the 50 EMA in the direction of that confirmed trend.

Key Logic:

Bullish Trend if the 50 EMA is above VWAP. Only long entries are allowed when the 8 EMA crosses above the 50 EMA during that bullish phase.

Bearish Trend if the 50 EMA is below VWAP. Only short entries are allowed when the 8 EMA crosses below the 50 EMA during that bearish phase.

Intraday Focus: Trades are restricted to a user-defined session window (default 7:30 AM–11:30 AM), aligning entries/exits with peak intraday liquidity.

Exit Rule: Positions close automatically when the 8 EMA crosses back in the opposite direction of the entry.

Why It Works:

EMA + VWAP helps detect both immediate momentum (EMAs) and overall institutional bias (VWAP).

By confining trades to a set intraday window, the strategy aims to capture morning volatility while avoiding choppy afternoon or overnight sessions.

Customization:

Users can adjust EMA lengths, session times, or incorporate stops/targets for additional risk management.

It can be tested on various symbols and intraday timeframes to gauge performance and robustness.

TrendSync Pro (SMC)📊 TrendSync Pro (SMC) – Advanced Trend-Following Strategy with HTF Alignment

Created by Shubham Singh

🔍 Strategy Overview

TrendSync Pro (SMC) is a precision-based smart trend-following strategy inspired by Smart Money Concepts (SMC). It combines: Real-time pivot-based trendline detection

Higher Time Frame (HTF) filtering to align trades with dominant trend

Risk management via adjustable Stop Loss (SL) and Take Profit (TP)

Directional control — trade only bullish, bearish, or both setups

Realistic backtesting using commissions and slippage

Pre-optimized profiles for scalpers, intraday, swing, and long-term traders

🧠 How It Works:

🔧 Strategy Settings Image:

beeimg.com

The strategy dynamically identifies trend direction by using swing high/low pivots. When a new pivot forms: It draws a trendline from the last significant pivot

Detects whether the trend is up (based on pivot lows) or down (based on pivot highs)

Waits for price to break above/below the trendline

Confirms with HTF price direction (HTF close > previous HTF close = bullish)

Only then it triggers a long or short trade

It exits either at TP, SL, or a manual trendline break

🛠️ Adjustable Parameters:

Trend Period: Length for pivot detection (affects sensitivity of trendlines)

HTF Timeframe: Aligns lower timeframe entries with higher timeframe direction

SL% and TP%: Customize your risk-reward profile

Commission & Slippage: Make backtests more realistic

Trade Direction: Choose to trade: Long only, Short only, or Both

🎛️ Trade Direction Control:

In settings, you can choose: Bullish Only: Executes only long entries

Bearish Only: Executes only short entries

Both: Executes both long and short entries when conditions are met

This allows you to align trades with your own market bias or external analysis.

📈 Entry Logic: Long Entry:

• Price crosses above trendline

• HTF is bullish (HTF close > previous close)

• Latest pivot is a low (trend is considered up)

Short Entry:

• Price crosses below trendline

• HTF is bearish (HTF close < previous close)

• Latest pivot is a high (trend is considered down)

📉 Exit Logic: Hit Take Profit or Stop Loss

Manual trendline invalidation: If price crosses opposite of the trend direction

⏰ Best Timeframes & Recommended Settings:

Scalping (1m to 5m):

HTF = 15m | Trend Period = 7

SL = 0.5% | TP = 1% to 2%

Intraday (15m to 30m):

HTF = 1H | Trend Period = 10–14

SL = 0.75% | TP = 2% to 3%

6 Hour Trading (30m to 1H):

HTF = 4H | Trend Period = 20

SL = 1% | TP = 4% to 6%

Swing Trading (4H to 1D):

HTF = 1D | Trend Period = 35

SL = 2% | TP = 8% to 12%

Long-Term Investing (1D+):

HTF = 1W | Trend Period = 50

SL = 3% | TP = 15%+

Note: These are recommended base settings. Adjust based on volatility, asset class, or personal trading style.

📸 Testing Note:

beeimg.com

TradingView limits test length to 20k bars (~40 trades on smaller timeframes). To show long-term results: Test on higher timeframes (e.g., 1H, 4H, 1D)

Share images of backtest result in description

Host longer test result screenshots on Imgur or any public drive

📍 Asset Behavior Insight:

This strategy works on multiple assets, including BTC, ETH, etc.

Performance varies by trend strength:

Sometimes BTC performs better than ETH

Other times ETH gives better results

That’s normal as both assets follow different volatility and trend behavior

It’s a trend-following setup. Longer and clearer the trend → better the results.

✅ Best Practices: Avoid ranging markets

Use proper SL/TP for each timeframe

Use directional filter if you already have a directional bias

Always forward test before going live

⚠️ Trading Disclaimer:

This script is for educational and backtesting purposes only. Trading involves risk. Always use risk management and never invest more than you can afford to lose.

Smart Grid Scalping (Pullback) Strategy[BullByte]The Smart Grid Scalping (Pullback) Strategy is a high-frequency trading strategy designed for short-term traders who seek to capitalize on market pullbacks. This strategy utilizes a dynamic ATR-based grid system to define optimal entry points, ensuring precise trade execution. It integrates volatility filtering and an RSI-based confirmation mechanism to enhance signal accuracy and reduce false entries.

This strategy is specifically optimized for scalping by dynamically adjusting trade levels based on current market conditions. The grid-based system helps capture retracement opportunities while maintaining strict trade management through predefined profit targets and trailing stop-loss mechanisms.

Key Features :

1. ATR-Based Grid System :

- Uses a 10-period ATR to dynamically calculate grid levels for entry points.

- Prevents chasing trades by ensuring price has reached key levels before executing entries.

2. No Trade Zone Protection :

- Avoids low-volatility zones where price action is indecisive.

- Ensures only high-momentum trades are executed to improve success rate.

3. RSI-Based Entry Confirmation :

- Long trades are triggered when RSI is below 30 (oversold) and price is in the lower grid zone.

- Short trades are triggered when RSI is above 70 (overbought) and price is in the upper grid zone.

4. Automated Trade Execution :

- Long Entry: Triggered when price drops below the first grid level with sufficient volatility.

- Short Entry: Triggered when price exceeds the highest grid level with sufficient volatility.

5. Take Profit & Trailing Stop :

- Profit target set at a customizable percentage (default 0.2%).

- Adaptive trailing stop mechanism using ATR to lock in profits while minimizing premature exits.

6. Visual Trade Annotations :

- Clearly labeled "LONG" and "SHORT" markers appear at trade entries for better visualization.

- Grid levels are plotted dynamically to aid decision-making.

Strategy Logic :

- The script first calculates the ATR-based grid levels and ensures price action has sufficient volatility before allowing trades.

- An additional RSI filter is used to ensure trades are taken at ideal market conditions.

- Once a trade is executed, the script implements a trailing stop and predefined take profit to maximize gains while reducing risks.

---

Disclaimer :

Risk Warning :

This strategy is provided for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Users are advised to conduct their own due diligence and risk management before using this strategy in live trading.

The developer and publisher of this script are not responsible for any financial losses incurred by the use of this strategy. Market conditions, slippage, and execution quality can affect real-world trading outcomes.

Use this script at your own discretion and always trade responsibly.

Uptrick X PineIndicators: Z-Score Flow StrategyThis strategy is based on the Z-Score Flow Indicator developed by Uptrick. Full credit for the original concept and logic goes to Uptrick.

The Z-Score Flow Strategy combines statistical mean-reversion logic with trend filtering, RSI confirmation, and multi-mode trade execution, offering a flexible and structured approach to trading both reversals and trend continuations.

Core Concepts Behind Z-Score Flow

1. Z-Score Mean Reversion Logic

The Z-score measures how far current price deviates from its statistical mean, in standard deviations.

A high positive Z-score (e.g. > 2) suggests price is overbought and may revert downward.

A low negative Z-score (e.g. < -2) suggests price is oversold and may revert upward.

The strategy uses Z-score thresholds to trigger signals when price deviates far enough from its mean.

2. Trend Filtering with EMA

To prevent counter-trend entries, the strategy includes a trend filter based on a 50-period EMA:

Only allows long entries if price is below EMA (mean-reversion in downtrends).

Only allows short entries if price is above EMA (mean-reversion in uptrends).

3. RSI Confirmation and Lockout System

An RSI smoothing mechanism helps confirm signals and avoid whipsaws:

RSI must be below 30 and rising to allow buys.

RSI must be above 70 and falling to allow sells.

Once a signal occurs, it is "locked out" until RSI re-enters the neutral zone (30–70).

This avoids multiple signals in overextended zones and reduces overtrading.

Entry Signal Logic

A buy or sell is triggered when:

Z-score crosses below (buy) or above (sell) the threshold.

RSI smoothed condition is met (oversold and rising / overbought and falling).

The trend condition (EMA filter) aligns.

A cooldown period has passed since the last opposite trade.

This layered approach helps ensure signal quality and timing precision.

Trade Modes

The strategy includes three distinct trade modes to adapt to various market behaviors:

1. Standard Mode

Trades are opened using the Z-score + RSI + trend filter logic.

Each signal must pass all layered conditions.

2. Zero Cross Mode

Trades are based on the Z-score crossing zero.

This mode is useful in trend continuation setups, rather than mean reversion.

3. Trend Reversal Mode

Trades occur when the mean slope direction changes, i.e., basis line changes color.

Helps capture early trend shifts with less lag.

Each mode can be customized for long-only, short-only, or long & short execution.

Visual Components

1. Z-Score Mean Line

The basis (mean) line is colored based on slope direction.

Green = bullish slope, Purple = bearish slope, Gray = flat.

A wide shadow band underneath reflects current trend momentum.