Advanced Adaptive Grid Trading StrategyThis strategy employs an advanced grid trading approach that dynamically adapts to market conditions, including trend, volatility, and risk management considerations. The strategy aims to capitalize on price fluctuations in both rising (long) and falling (short) markets, as well as during sideways movements. It combines multiple indicators to determine the trend and automatically adjusts grid parameters for more efficient trading.

How it Works:

Trend Analysis:

Short, long, and super long Moving Averages (MA) to determine the trend direction.

RSI (Relative Strength Index) to identify overbought and oversold levels, and to confirm the trend.

MACD (Moving Average Convergence Divergence) to confirm momentum and trend direction.

Momentum indicator.

The strategy uses a weighted scoring system to assess trend strength (strong bullish, moderate bullish, strong bearish, moderate bearish, sideways).

Grid System:

The grid size (the distance between buy and sell levels) changes dynamically based on market volatility, using the ATR (Average True Range) indicator.

Grid density also adapts to the trend: in a strong trend, the grid is denser in the direction of the trend.

Grid levels are shifted depending on the trend direction (upwards in a bear market, downwards in a bull market).

Trading Logic:

The strategy opens long positions if the trend is bullish and the price reaches one of the lower grid levels.

It opens short positions if the trend is bearish and the price reaches one of the upper grid levels.

In a sideways market, it can open positions in both directions.

Risk Management:

Stop Loss for every position.

Take Profit for every position.

Trailing Stop Loss to protect profits.

Maximum daily loss limit.

Maximum number of positions limit.

Time-based exit (if the position is open for too long).

Risk-based position sizing (optional).

Input Options:

The strategy offers numerous settings that allow users to customize its operation:

Timeframe: The chart's timeframe (e.g., 1 minute, 5 minutes, 1 hour, 4 hours, 1 day, 1 week).

Base Grid Size (%): The base size of the grid, expressed as a percentage.

Max Positions: The maximum number of open positions allowed.

Use Volatility Grid: If enabled, the grid size changes dynamically based on the ATR indicator.

ATR Length: The period of the ATR indicator.

ATR Multiplier: The multiplier for the ATR to fine-tune the grid size.

RSI Length: The period of the RSI indicator.

RSI Overbought: The overbought level for the RSI.

RSI Oversold: The oversold level for the RSI.

Short MA Length: The period of the short moving average.

Long MA Length: The period of the long moving average.

Super Long MA Length: The period of the super long moving average.

MACD Fast Length: The fast period of the MACD.

MACD Slow Length: The slow period of the MACD.

MACD Signal Length: The period of the MACD signal line.

Stop Loss (%): The stop loss level, expressed as a percentage.

Take Profit (%): The take profit level, expressed as a percentage.

Use Trailing Stop: If enabled, the strategy uses a trailing stop loss.

Trailing Stop (%): The trailing stop loss level, expressed as a percentage.

Max Loss Per Day (%): The maximum daily loss, expressed as a percentage.

Time Based Exit: If enabled, the strategy exits the position after a certain amount of time.

Max Holding Period (hours): The maximum holding time in hours.

Use Risk Based Position: If enabled, the strategy calculates position size based on risk.

Risk Per Trade (%): The risk per trade, expressed as a percentage.

Max Leverage: The maximum leverage.

Important Notes:

This strategy does not guarantee profits. Cryptocurrency markets are volatile, and trading involves risk.

The strategy's effectiveness depends on market conditions and settings.

It is recommended to thoroughly backtest the strategy under various market conditions before using it live.

Past performance is not indicative of future results.

Indicators and strategies

Multi-Timeframe MACD Strategy ver 1.0Multi-Timeframe MACD Strategy: Enhanced Trend Trading with Customizable Entry and Trailing Stop

This strategy utilizes the Moving Average Convergence Divergence (MACD) indicator across multiple timeframes to identify strong trends, generate precise entry and exit signals, and manage risk with an optional trailing stop loss. By combining the insights of both the current chart's timeframe and a user-defined higher timeframe, this strategy aims to improve trade accuracy, reduce exposure to false signals, and capture larger market moves.

Key Features:

Dual Timeframe Analysis: Calculates and analyzes the MACD on both the current chart's timeframe and a user-selected higher timeframe (e.g., Daily MACD on a 1-hour chart). This provides a broader market context, helping to confirm trends and filter out short-term noise.

Configurable MACD: Fine-tune the MACD calculation with adjustable Fast Length, Slow Length, and Signal Length parameters. Optimize the indicator's sensitivity to match your trading style and the volatility of the asset.

Flexible Entry Options: Choose between three distinct entry types:

Crossover: Enters trades when the MACD line crosses above (long) or below (short) the Signal line.

Zero Cross: Enters trades when the MACD line crosses above (long) or below (short) the zero line.

Both: Combines both Crossover and Zero Cross signals, providing more potential entry opportunities.

Independent Timeframe Control: Display and trade based on the current timeframe MACD, the higher timeframe MACD, or both. This allows you to focus on the information most relevant to your analysis.

Optional Trailing Stop Loss: Implements a configurable trailing stop loss to protect profits and limit potential losses. The trailing stop is adjusted dynamically as the price moves in your favor, based on a user-defined percentage.

No Repainting: Employs lookahead=barmerge.lookahead_off in the request.security() function to prevent data leakage and ensure accurate backtesting and real-time signals.

Clear Visual Signals (Optional): Includes optional plotting of the MACD and Signal lines for both timeframes, with distinct colors for easy visual identification. These plots are for visual confirmation and are not required for the strategy's logic.

Suitable for Various Trading Styles: Adaptable to swing trading, day trading, and trend-following strategies across diverse markets (stocks, forex, cryptocurrencies, etc.).

Fully Customizable: All parameters are adjustable, including timeframes, MACD Settings, Entry signal type and trailing stop settings.

How it Works:

MACD Calculation: The strategy calculates the MACD (using the standard formula) for both the current chart's timeframe and the specified higher timeframe.

Trend Identification: The relationship between the MACD line, Signal line, and zero line is used to determine the current trend for each timeframe.

Entry Signals: Buy/sell signals are generated based on the selected "Entry Type":

Crossover: A long signal is generated when the MACD line crosses above the Signal line, and both timeframes are in agreement (if both are enabled). A short signal is generated when the MACD line crosses below the Signal line, and both timeframes are in agreement.

Zero Cross: A long signal is generated when the MACD line crosses above the zero line, and both timeframes agree. A short signal is generated when the MACD line crosses below the zero line and both timeframes agree.

Both: Combines Crossover and Zero Cross signals.

Trailing Stop Loss (Optional): If enabled, a trailing stop loss is set at a specified percentage below (for long positions) or above (for short positions) the entry price. The stop-loss is automatically adjusted as the price moves favorably.

Exit Signals:

Without Trailing Stop: Positions are closed when the MACD signals reverse according to the selected "Entry Type" (e.g., a long position is closed when the MACD line crosses below the Signal line if using "Crossover" entries).

With Trailing Stop: Positions are closed if the price hits the trailing stop loss.

Backtesting and Optimization: The strategy automatically backtests on the chart's historical data, allowing you to assess its performance and optimize parameters for different assets and timeframes.

Example Use Cases:

Confirming Trend Strength: A trader on a 1-hour chart sees a bullish MACD crossover on the current timeframe. They check the MTF MACD strategy and see that the Daily MACD is also bullish, confirming the strength of the uptrend.

Filtering Noise: A trader using a 15-minute chart wants to avoid false signals from short-term volatility. They use the strategy with a 4-hour higher timeframe to filter out noise and only trade in the direction of the dominant trend.

Dynamic Risk Management: A trader enters a long position and enables the trailing stop loss. As the price rises, the trailing stop is automatically adjusted upwards, protecting profits. The trade is exited either when the MACD reverses or when the price hits the trailing stop.

Disclaimer:

The MACD is a lagging indicator and can produce false signals, especially in ranging markets. This strategy is for educational and informational purposes only and should not be considered financial advice. Backtest and optimize the strategy thoroughly, combine it with other technical analysis tools, and always implement sound risk management practices before using it with real capital. Past performance is not indicative of future results. Conduct your own due diligence and consider your risk tolerance before making any trading decisions.

Multi-Timeframe Parabolic SAR Strategy ver 1.0Multi-Timeframe Parabolic SAR Strategy (MTF PSAR) - Enhanced Trend Trading

This strategy leverages the power of the Parabolic SAR (Stop and Reverse) indicator across multiple timeframes to provide robust trend identification, precise entry/exit signals, and dynamic trailing stop management. By combining the insights of both the current chart's timeframe and a user-defined higher timeframe, this strategy aims to improve trading accuracy, reduce risk, and capture more significant market moves.

Key Features:

Dual Timeframe Analysis: Simultaneously analyzes the Parabolic SAR on the current chart and a higher timeframe (e.g., Daily PSAR on a 1-hour chart). This allows you to align your trades with the dominant trend and filter out noise from lower timeframes.

Configurable PSAR: Fine-tune the PSAR calculation with adjustable Start, Increment, and Maximum values to optimize sensitivity for your trading style and the asset's volatility.

Independent Timeframe Control: Choose to display and trade based on either or both the current timeframe PSAR and the higher timeframe PSAR. Focus on the most relevant information for your analysis.

Clear Visual Signals: Distinct colors for the current and higher timeframe PSAR dots provide a clear visual representation of potential entry and exit points.

Multiple Entry Strategies: The strategy offers flexible entry conditions, allowing you to trade based on:

Confirmation: Both current and higher timeframe PSAR signals agree and the current timeframe PSAR has just flipped direction. (Most conservative)

Current Timeframe Only: Trades based solely on the current timeframe PSAR, ideal for when the higher timeframe is less relevant or disabled.

Higher Timeframe Only: Trades based solely on the higher timeframe PSAR.

Dynamic Trailing Stop (PSAR-Based): Implements a trailing stop-loss based on the current timeframe's Parabolic SAR. This helps protect profits by automatically adjusting the stop-loss as the price moves in your favor. Exits are triggered when either the current or HTF PSAR flips.

No Repainting: Uses lookahead=barmerge.lookahead_off in the security() function to ensure that the higher timeframe data is accessed without any data leakage, preventing repainting issues.

Fully Configurable: All parameters (PSAR settings, higher timeframe, visibility, colors) are adjustable through the strategy's settings panel, allowing for extensive customization and optimization.

Suitable for Various Trading Styles: Applicable to swing trading, day trading, and trend-following strategies across various markets (stocks, forex, cryptocurrencies, etc.).

How it Works:

PSAR Calculation: The strategy calculates the standard Parabolic SAR for both the current chart's timeframe and the selected higher timeframe.

Trend Identification: The direction of the PSAR (dots below price = uptrend, dots above price = downtrend) determines the current trend for each timeframe.

Entry Signals: The strategy generates buy/sell signals based on the chosen entry strategy (Confirmation, Current Timeframe Only, or Higher Timeframe Only). The Confirmation strategy offers the highest probability signals by requiring agreement between both timeframes.

Trailing Stop Exit: Once a position is entered, the strategy uses the current timeframe PSAR as a dynamic trailing stop. The stop-loss is automatically adjusted as the PSAR dots move, helping to lock in profits and limit losses. The strategy exits when either the Current or HTF PSAR changes direction.

Backtesting and Optimization: The strategy automatically backtests on the chart's historical data, allowing you to evaluate its performance and optimize the settings for different assets and timeframes.

Example Use Cases:

Trend Confirmation: A trader on a 1-hour chart observes a bullish PSAR flip on the current timeframe. They check the MTF PSAR strategy and see that the Daily PSAR is also bullish, confirming the strength of the uptrend and providing a high-probability long entry signal.

Filtering Noise: A trader on a 5-minute chart wants to avoid whipsaws caused by short-term price fluctuations. They use the strategy with a 1-hour higher timeframe to filter out noise and only trade in the direction of the dominant trend.

Dynamic Risk Management: A trader enters a long position and uses the current timeframe PSAR as a trailing stop. As the price rises, the PSAR dots move upwards, automatically raising the stop-loss and protecting profits. The trade is exited when the current (or HTF) PSAR flips to bearish.

Disclaimer:

The Parabolic SAR is a lagging indicator and can produce false signals, particularly in ranging or choppy markets. This strategy is intended for educational and informational purposes only and should not be considered financial advice. It is essential to backtest and optimize the strategy thoroughly, use it in conjunction with other technical analysis tools, and implement sound risk management practices before using it with real capital. Past performance is not indicative of future results. Always conduct your own due diligence and consider your risk tolerance before making any trading decisions.

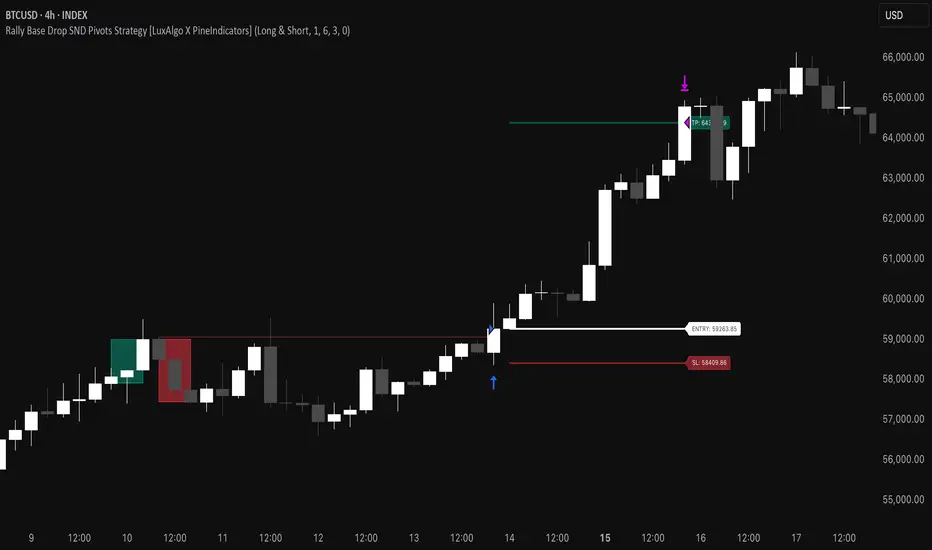

Rally Base Drop SND Pivots Strategy [LuxAlgo X PineIndicators]This strategy is based on the Rally Base Drop (RBD) SND Pivots indicator developed by LuxAlgo. Full credit for the concept and original indicator goes to LuxAlgo.

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand trading system that detects pivot points based on Rally, Base, and Drop (RBD) candles. This strategy automatically identifies key market structure levels, allowing traders to:

Identify pivot-based supply and demand (SND) zones.

Use fixed criteria for trend continuation or reversals.

Filter out market noise by requiring structured price formations.

Enter trades based on breakouts of key SND pivot levels.

How the Rally Base Drop SND Pivots Strategy Works

1. Pivot Point Detection Using RBD Candles

The strategy follows a rigid market structure methodology, where pivots are detected only when:

A Rally (R) consists of multiple consecutive bullish candles.

A Drop (D) consists of multiple consecutive bearish candles.

A Base (B) is identified as a transition between Rallies and Drops, acting as a pivot point.

The pivot level is confirmed when the formation is complete.

Unlike traditional fractal-based pivots, RBD Pivots enforce stricter structural rules, ensuring that each pivot:

Has a well-defined bullish or bearish price movement.

Reduces false signals caused by single-bar fluctuations.

Provides clear supply and demand levels based on structured price movements.

These pivot levels are drawn on the chart using color-coded boxes:

Green zones represent bullish pivot levels (Rally Base formations).

Red zones represent bearish pivot levels (Drop Base formations).

Once a pivot is confirmed, the high or low of the base candle is used as the reference level for future trades.

2. Trade Entry Conditions

The strategy allows traders to select from three trading modes:

Long Only – Only takes long trades when bullish pivot breakouts occur.

Short Only – Only takes short trades when bearish pivot breakouts occur.

Long & Short – Trades in both directions based on pivot breakouts.

Trade entry signals are triggered when price breaks through a confirmed pivot level:

Long Entry:

A bullish pivot level is formed.

Price breaks above the bullish pivot level.

The strategy enters a long position.

Short Entry:

A bearish pivot level is formed.

Price breaks below the bearish pivot level.

The strategy enters a short position.

The strategy includes an optional mode to reverse long and short conditions, allowing traders to experiment with contrarian entries.

3. Exit Conditions Using ATR-Based Risk Management

This strategy uses the Average True Range (ATR) to calculate dynamic stop-loss and take-profit levels:

Stop-Loss (SL): Placed 1 ATR below entry for long trades and 1 ATR above entry for short trades.

Take-Profit (TP): Set using a Risk-Reward Ratio (RR) multiplier (default = 6x ATR).

When a trade is opened:

The entry price is recorded.

ATR is calculated at the time of entry to determine stop-loss and take-profit levels.

Trades exit automatically when either SL or TP is reached.

If reverse conditions mode is enabled, stop-loss and take-profit placements are flipped.

Visualization & Dynamic Support/Resistance Levels

1. Pivot Boxes for Market Structure

Each pivot is marked with a colored box:

Green boxes indicate bullish demand zones.

Red boxes indicate bearish supply zones.

These boxes remain on the chart to act as dynamic support and resistance levels, helping traders identify key price reaction zones.

2. Horizontal Entry, Stop-Loss, and Take-Profit Lines

When a trade is active, the strategy plots:

White line → Entry price.

Red line → Stop-loss level.

Green line → Take-profit level.

Labels display the exact entry, SL, and TP values, updating dynamically as price moves.

Customization Options

This strategy offers multiple adjustable settings to optimize performance for different market conditions:

Trade Mode Selection → Choose between Long Only, Short Only, or Long & Short.

Pivot Length → Defines the number of required Rally & Drop candles for a pivot.

ATR Exit Multiplier → Adjusts stop-loss distance based on ATR.

Risk-Reward Ratio (RR) → Modifies take-profit level relative to risk.

Historical Lookback → Limits how far back pivot zones are displayed.

Color Settings → Customize pivot box colors for bullish and bearish setups.

Considerations & Limitations

Pivot Breakouts Do Not Guarantee Reversals. Some pivot breaks may lead to continuation moves instead of trend reversals.

Not Optimized for Low Volatility Conditions. This strategy works best in trending markets with strong momentum.

ATR-Based Stop-Loss & Take-Profit May Require Optimization. Different assets may require different ATR multipliers and RR settings.

Market Noise May Still Influence Pivots. While this method filters some noise, fake breakouts can still occur.

Conclusion

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand system that combines:

Pivot-based market structure analysis (using Rally, Base, and Drop candles).

Breakout-based trade entries at confirmed SND levels.

ATR-based dynamic risk management for stop-loss and take-profit calculation.

This strategy helps traders:

Identify high-probability supply and demand levels.

Trade based on structured market pivots.

Use a systematic approach to price action analysis.

Automatically manage risk with ATR-based exits.

The strict pivot detection rules and built-in breakout validation make this strategy ideal for traders looking to:

Trade based on market structure.

Use defined support & resistance levels.

Reduce noise compared to traditional fractals.

Implement a structured supply & demand trading model.

This strategy is fully customizable, allowing traders to adjust parameters to fit their market and trading style.

Full credit for the original concept and indicator goes to LuxAlgo.

IU BBB(Big Body Bar) StrategyDESCRIPTION

The IU BBB (Big Body Bar) Strategy is a price action-based trading strategy that identifies high-momentum candles with significantly larger body sizes compared to the average. It enters trades when a strong bullish or bearish move occurs and manages risk using an ATR-based trailing stop-loss system.

USER INPUTS:

- Big Body Threshold – Defines how many times larger the candle body should be compared to the average body ( default is 4 ).

- ATR Length – The period for the Average True Range (ATR) used in the trailing stop-loss calculation ( default is 14 ).

- ATR Factor – Multiplier for ATR to determine the trailing stop distance ( default is 2 ).

LONG CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is higher than the opening price (bullish candle).

SHORT CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is lower than the opening price (bearish candle).

LONG EXIT:

- ATR-based trailing stop-loss dynamically adjusts, locking in profits as the price moves higher.

SHORT EXIT:

- ATR-based trailing stop-loss dynamically adjusts, securing profits as the price moves lower.

WHY IT IS UNIQUE:

- Unlike traditional momentum strategies, this system adapts to volatility by filtering trades based on relative candle size.

- It incorporates an ATR-based trailing stop-loss, ensuring risk management and profit protection.

- The strategy avoids choppy market conditions by only trading when significant momentum is present.

HOW USERS CAN BENEFIT FROM IT:

- Catch Strong Price Moves – The strategy helps traders enter trades when the market shows decisive momentum.

- Effective Risk Management – The ATR-based trailing stop ensures that winning trades remain profitable.

- Works Across Markets – Can be applied to stocks, forex, crypto, and indices with proper optimization.

- Fully Customizable – Users can adjust sensitivity settings to match their trading style and time frame.

Liquidity Sweep Filter Strategy [AlgoAlpha X PineIndicators]This strategy is based on the Liquidity Sweep Filter developed by AlgoAlpha. Full credit for the concept and original indicator goes to AlgoAlpha.

The Liquidity Sweep Filter Strategy is a non-repainting trading system designed to identify liquidity sweeps, trend shifts, and high-impact price levels. It incorporates volume-based liquidation analysis, trend confirmation, and dynamic support/resistance detection to optimize trade entries and exits.

This strategy helps traders:

Detect liquidity sweeps where major market participants trigger stop losses and liquidations.

Identify trend shifts using a volatility-based moving average system.

Analyze volume distribution with a built-in volume profile visualization.

Filter noise by differentiating between major and minor liquidity sweeps.

How the Liquidity Sweep Filter Strategy Works

1. Trend Detection Using Volatility-Based Filtering

The strategy applies a volatility-adjusted moving average system to determine trend direction:

A central trend line is calculated using an EMA smoothed over a user-defined length.

Upper and lower deviation bands are created based on the average price deviation over multiple periods.

If price closes above the upper band, the strategy signals an uptrend.

If price closes below the lower band, the strategy signals a downtrend.

This approach ensures that trend shifts are confirmed only when price significantly moves beyond normal market fluctuations.

2. Liquidity Sweep Detection

Liquidity sweeps occur when price temporarily breaks key levels, triggering stop-loss liquidations or margin call events. The strategy tracks swing highs and lows, marking potential liquidity grabs:

Bearish Liquidity Sweeps – Price breaks a recent high, then reverses downward.

Bullish Liquidity Sweeps – Price breaks a recent low, then reverses upward.

Volume Integration – The strategy analyzes trading volume at each sweep to differentiate between major and minor sweeps.

Key levels where liquidity sweeps occur are plotted as color-coded horizontal lines:

Red lines indicate bearish liquidity sweeps.

Green lines indicate bullish liquidity sweeps.

Labels are displayed at each sweep, showing the volume of liquidated positions at that level.

3. Volume Profile Analysis

The strategy includes an optional volume profile visualization, displaying how trading volume is distributed across different price levels.

Features of the volume profile:

Point of Control (POC) – The price level with the highest traded volume is marked as a key area of interest.

Bounding Box – The profile is enclosed within a transparent box, helping traders visualize the price range of high trading activity.

Customizable Resolution & Scale – Traders can adjust the granularity of the profile to match their preferred time frame.

The volume profile helps identify zones of strong support and resistance, making it easier to anticipate price reactions at key levels.

Trade Entry & Exit Conditions

The strategy allows traders to configure trade direction:

Long Only – Only takes long trades.

Short Only – Only takes short trades.

Long & Short – Trades in both directions.

Entry Conditions

Long Entry:

A bullish trend shift is confirmed.

A bullish liquidity sweep occurs (price sweeps below a key level and reverses).

The trade direction setting allows long trades.

Short Entry:

A bearish trend shift is confirmed.

A bearish liquidity sweep occurs (price sweeps above a key level and reverses).

The trade direction setting allows short trades.

Exit Conditions

Closing a Long Position:

A bearish trend shift occurs.

The position is liquidated at a predefined liquidity sweep level.

Closing a Short Position:

A bullish trend shift occurs.

The position is liquidated at a predefined liquidity sweep level.

Customization Options

The strategy offers multiple adjustable settings:

Trade Mode: Choose between Long Only, Short Only, or Long & Short.

Trend Calculation Length & Multiplier: Adjust how trend signals are calculated.

Liquidity Sweep Sensitivity: Customize how aggressively the strategy identifies sweeps.

Volume Profile Display: Enable or disable the volume profile visualization.

Bounding Box & Scaling: Control the size and position of the volume profile.

Color Customization: Adjust colors for bullish and bearish signals.

Considerations & Limitations

Liquidity sweeps do not always result in reversals. Some price sweeps may continue in the same direction.

Works best in volatile markets. In low-volatility environments, liquidity sweeps may be less reliable.

Trend confirmation adds a slight delay. The strategy ensures valid signals, but this may result in slightly later entries.

Large volume imbalances may distort the volume profile. Adjusting the scale settings can help improve visualization.

Conclusion

The Liquidity Sweep Filter Strategy is a volume-integrated trading system that combines liquidity sweeps, trend analysis, and volume profile data to optimize trade execution.

By identifying key price levels where liquidations occur, this strategy provides valuable insight into market behavior, helping traders make better-informed trading decisions.

Key use cases for this strategy:

Liquidity-Based Trading – Capturing moves triggered by stop hunts and liquidations.

Volume Analysis – Using volume profile data to confirm high-activity price zones.

Trend Following – Entering trades based on confirmed trend shifts.

Support & Resistance Trading – Using liquidity sweep levels as dynamic price zones.

This strategy is fully customizable, allowing traders to adapt it to different market conditions, timeframes, and risk preferences.

Full credit for the original concept and indicator goes to AlgoAlpha.

Market Trend Levels Non-Repainting [BigBeluga X PineIndicators]This strategy is based on the Market Trend Levels Detector developed by BigBeluga. Full credit for the concept and original indicator goes to BigBeluga.

The Market Trend Levels Detector Strategy is a non-repainting trend-following strategy that identifies market trend shifts using two Exponential Moving Averages (EMA). It also detects key price levels and allows traders to apply multiple filters to refine trade entries and exits.

This strategy is designed for trend trading and enables traders to:

Identify trend direction based on EMA crossovers.

Detect significant market levels using labeled trend lines.

Use multiple filter conditions to improve trade accuracy.

Avoid false signals through non-repainting calculations.

How the Market Trend Levels Detector Strategy Works

1. Core Trend Detection Using EMA Crossovers

The strategy detects trend shifts using two EMAs:

Fast EMA (default: 12 periods) – Reacts quickly to price movements.

Slow EMA (default: 25 periods) – Provides a smoother trend confirmation.

A bullish crossover (Fast EMA crosses above Slow EMA) signals an uptrend , while a bearish crossover (Fast EMA crosses below Slow EMA) signals a downtrend .

2. Market Level Detection & Visualization

Each time an EMA crossover occurs, a trend level line is drawn:

Bullish crossover → A green line is drawn at the low of the crossover candle.

Bearish crossover → A purple line is drawn at the high of the crossover candle.

Lines can be extended to act as support and resistance zones for future price action.

Additionally, a small label (●) appears at each crossover to mark the event on the chart.

3. Trade Entry & Exit Conditions

The strategy allows users to choose between three trading modes:

Long Only – Only enters long trades.

Short Only – Only enters short trades.

Long & Short – Trades in both directions.

Entry Conditions

Long Entry:

A bullish EMA crossover occurs.

The trade direction setting allows long trades.

Filter conditions (if enabled) confirm a valid long signal.

Short Entry:

A bearish EMA crossover occurs.

The trade direction setting allows short trades.

Filter conditions (if enabled) confirm a valid short signal.

Exit Conditions

Long Exit:

A bearish EMA crossover occurs.

Exit filters (if enabled) indicate an invalid long position.

Short Exit:

A bullish EMA crossover occurs.

Exit filters (if enabled) indicate an invalid short position.

Additional Trade Filters

To improve trade accuracy, the strategy allows traders to apply up to 7 additional filters:

RSI Filter: Only trades when RSI confirms a valid trend.

MACD Filter: Ensures MACD histogram supports the trade direction.

Stochastic Filter: Requires %K line to be above/below threshold values.

Bollinger Bands Filter: Confirms price position relative to the middle BB line.

ADX Filter: Ensures the trend strength is above a set threshold.

CCI Filter: Requires CCI to indicate momentum in the right direction.

Williams %R Filter: Ensures price momentum supports the trade.

Filters can be enabled or disabled individually based on trader preference.

Dynamic Level Extension Feature

The strategy provides an optional feature to extend trend lines until price interacts with them again:

Bullish support lines extend until price revisits them.

Bearish resistance lines extend until price revisits them.

If price breaks a line, the line turns into a dotted style , indicating it has been breached.

This helps traders identify key levels where trend shifts previously occurred, providing useful support and resistance insights.

Customization Options

The strategy includes several adjustable settings :

Trade Direction: Choose between Long Only, Short Only, or Long & Short.

Trend Lengths: Adjust the Fast & Slow EMA lengths.

Market Level Extension: Decide whether to extend support/resistance lines.

Filters for Trade Confirmation: Enable/disable individual filters.

Color Settings: Customize line colors for bullish and bearish trend shifts.

Maximum Displayed Lines: Limit the number of drawn support/resistance lines.

Considerations & Limitations

Trend Lag: As with any EMA-based strategy, signals may be slightly delayed compared to price action.

Sideways Markets: This strategy works best in trending conditions; frequent crossovers in sideways markets can produce false signals.

Filter Usage: Enabling multiple filters may reduce trade frequency, but can also improve trade quality.

Line Overlap: If many crossovers occur in a short period, the chart may become cluttered with multiple trend levels. Adjusting the "Display Last" setting can help.

Conclusion

The Market Trend Levels Detector Strategy is a non-repainting trend-following system that combines EMA crossovers, market level detection, and customizable filters to improve trade accuracy.

By identifying trend shifts and key price levels, this strategy can be used for:

Trend Confirmation – Using EMA crossovers and filters to confirm trend direction.

Support & Resistance Trading – Identifying dynamic levels where price reacts.

Momentum-Based Trading – Combining EMA crossovers with additional momentum filters.

This strategy is fully customizable and can be adapted to different trading styles, timeframes, and market conditions.

Full credit for the original concept and indicator goes to BigBeluga.

RSI, Volume, MACD, EMA ComboRSI + Volume + MACD + EMA Trading System

This script combines four powerful indicators—Relative Strength Index (RSI), Volume, Moving Average Convergence Divergence (MACD), and Exponential Moving Average (EMA)—to create a comprehensive trading strategy for better trend confirmation and trade entries.

How It Works

RSI (Relative Strength Index)

Helps identify overbought and oversold conditions.

Used to confirm momentum strength before taking a trade.

Volume

Confirms the strength of price movements.

Avoids false signals by ensuring there is sufficient trading activity.

MACD (Moving Average Convergence Divergence)

Confirms trend direction and momentum shifts.

Provides buy/sell signals through MACD line crossovers.

EMA (Exponential Moving Average)

Acts as a dynamic support and resistance level.

Helps filter out trades that go against the overall trend.

Trading Logic

Buy Signal:

RSI is above 50 (bullish momentum).

MACD shows a bullish crossover.

The price is above the EMA (trend confirmation).

Volume is increasing (strong participation).

Sell Signal:

RSI is below 50 (bearish momentum).

MACD shows a bearish crossover.

The price is below the EMA (downtrend confirmation).

Volume is increasing (intense selling pressure).

Backtesting & Risk Management

The strategy is optimized for scalping on the 1-minute timeframe (adjustable for other timeframes).

Default settings use realistic commission and slippage to simulate actual trading conditions.

A stop-loss and take-profit system is integrated to manage risk effectively.

This script is designed to help traders filter out false signals, improve trend confirmation, and increase trade accuracy by combining multiple indicators in a structured way.

Gradient Trend Filter STRATEGY [ChartPrime/PineIndicators]This strategy is based on the Gradient Trend Filter indicator developed by ChartPrime. Full credit for the concept and indicator goes to ChartPrime.

The Gradient Trend Filter Strategy is designed to execute trades based on the trend analysis and filtering system provided by the Gradient Trend Filter indicator. It integrates a noise-filtered trend detection system with a color-gradient visualization, helping traders identify trend strength, momentum shifts, and potential reversals.

How the Gradient Trend Filter Strategy Works

1. Noise Filtering for Smoother Trends

To reduce false signals caused by market noise, the strategy applies a three-stage smoothing function to the source price. This function ensures that trend shifts are detected more accurately, minimizing unnecessary trade entries and exits.

The filter is based on an Exponential Moving Average (EMA)-style smoothing technique.

It processes price data in three successive passes, refining the trend signal before generating trade entries.

This filtering technique helps eliminate minor fluctuations and highlights the true underlying trend.

2. Multi-Layered Trend Bands & Color-Based Trend Visualization

The Gradient Trend Filter constructs multiple trend bands around the filtered trend line, acting as dynamic support and resistance zones.

The mid-line changes color based on the trend direction:

Green for uptrends

Red for downtrends

A gradient cloud is formed around the trend line, dynamically shifting colors to provide early warning signals of trend reversals.

The outer bands function as potential support and resistance, helping traders determine stop-loss and take-profit zones.

Visualization elements used in this strategy:

Trend Filter Line → Changes color between green (bullish) and red (bearish).

Trend Cloud → Dynamically adjusts color based on trend strength.

Orange Markers → Appear when a trend shift is confirmed.

Trade Entry & Exit Conditions

This strategy automatically enters trades based on confirmed trend shifts detected by the Gradient Trend Filter.

1. Trade Entry Rules

Long Entry:

A bullish trend shift is detected (trend direction changes to green).

The filtered trend value crosses above zero, confirming upward momentum.

The strategy enters a long position.

Short Entry:

A bearish trend shift is detected (trend direction changes to red).

The filtered trend value crosses below zero, confirming downward momentum.

The strategy enters a short position.

2. Trade Exit Rules

Closing a Long Position:

If a bearish trend shift occurs, the strategy closes the long position.

Closing a Short Position:

If a bullish trend shift occurs, the strategy closes the short position.

The trend shift markers (orange diamonds) act as a confirmation signal, reinforcing the validity of trade entries and exits.

Customization Options

This strategy allows traders to adjust key parameters for flexibility in different market conditions:

Trade Direction: Choose between Long Only, Short Only, or Long & Short .

Trend Length: Modify the length of the smoothing function to adapt to different timeframes.

Line Width & Colors: Customize the visual appearance of trend lines and cloud colors.

Performance Table: Enable or disable the equity performance table that tracks historical trade results.

Performance Tracking & Reporting

A built-in performance table is included to monitor monthly and yearly trading performance.

The table calculates monthly percentage returns, displaying them in a structured format.

Color-coded values highlight profitable months (blue) and losing months (red).

Tracks yearly cumulative performance to assess long-term strategy effectiveness.

Traders can use this feature to evaluate historical performance trends and optimize their strategy settings accordingly.

How to Use This Strategy

Identify Trend Strength & Reversals:

Use the trend line and cloud color changes to assess trend strength and detect potential reversals.

Monitor Momentum Shifts:

Pay attention to gradient cloud color shifts, as they often appear before the trend line changes color.

This can indicate early momentum weakening or strengthening.

Act on Trend Shift Markers:

Use orange diamonds as confirmation signals for trend shifts and trade entry/exit points.

Utilize Cloud Bands as Support/Resistance:

The outer bands of the cloud serve as dynamic support and resistance, helping with stop-loss and take-profit placement.

Considerations & Limitations

Trend Lag: Since the strategy applies a smoothing function, entries may be slightly delayed compared to raw price action.

Volatile Market Conditions: In high-volatility markets, trend shifts may occur more frequently, leading to higher trade frequency.

Optimized for Trend Trading: This strategy is best suited for trending markets and may produce false signals in sideways (ranging) conditions.

Conclusion

The Gradient Trend Filter Strategy is a trend-following system based on the Gradient Trend Filter indicator by ChartPrime. It integrates noise filtering, trend visualization, and gradient-based color shifts to help traders identify strong market trends and potential reversals.

By combining trend filtering with a multi-layered cloud system, the strategy provides clear trade signals while minimizing noise. Traders can use this strategy for long-term trend trading, momentum shifts, and support/resistance-based decision-making.

This strategy is a fully automated system that allows traders to execute long, short, or both directions, with customizable settings to adapt to different market conditions.

Credit for the original concept and indicator goes to ChartPrime.

Simple APF Strategy Backtesting [The Quant Science]Simple backtesting strategy for the quantitative indicator Autocorrelation Price Forecasting. This is a Buy & Sell strategy that operates exclusively with long orders. It opens long positions and generates profit based on the future price forecast provided by the indicator. It's particularly suitable for trend-following trading strategies or directional markets with an established trend.

Main functions

1. Cycle Detection: Utilize autocorrelation to identify repetitive market behaviors and cycles.

2. Forecasting for Backtesting: Simulate trades and assess the profitability of various strategies based on future price predictions.

Logic

The strategy works as follow:

Entry Condition: Go long if the hypothetical gain exceeds the threshold gain (configurable by user interface).

Position Management: Sets a take-profit level based on the future price.

Position Sizing: Automatically calculates the order size as a percentage of the equity.

No Stop-Loss: this strategy doesn't includes any stop loss.

Example Use Case

A trader analyzes a dayli period using 7 historical bars for autocorrelation.

Sets a threshold gain of 20 points using a 5% of the equity for each trade.

Evaluates the effectiveness of a long-only strategy in this period to assess its profitability and risk-adjusted performance.

User Interface

Length: Set the length of the data used in the autocorrelation price forecasting model.

Thresold Gain: Minimum value to be considered for opening trades based on future price forecast.

Order Size: percentage size of the equity used for each single trade.

Strategy Limit

This strategy does not use a stop loss. If the price continues to drop and the future price forecast is incorrect, the trader may incur a loss or have their capital locked in the losing trade.

Disclaimer!

This is a simple template. Use the code as a starting point rather than a finished solution. The script does not include important parameters, so use it solely for educational purposes or as a boilerplate.

GRIM309 CallPut StrategyThis draws the 5, 10, 20, 50 and 200 EMA lines.

It creates suggestions of when to open and close call positions (GREEN) as well as open and close put positions (RED) it has a early warning system, and in case there is a spike between the last 5 positions it will signal close the position, this is optional (isWarning)

There is also a cooldown period, when set at 2 it means wait a position before initiating another, I did not like the position closing and then opening directly afterwards, you could cooldown for 3 and skip 2 candles or more etc. Set to 1 then it will open/close without cooling down.

Additionally the very bottom shows wether it is in an uptrend or downtrend currently (Yellow triangle)

Pure Price Action StrategyTest Price Action Strategy from Lux Pure Price Action Indicator

How This Strategy Works:

Recognizing Trends & Reversals:

Break of Structure (BOS): A bullish signal indicating a trend continuation.

Market Structure Shift (MSS): A bearish signal indicating a potential reversal.

Analyzing Market Momentum:

It uses recent highs and lows to confirm whether the price is making higher highs (bullish) or lower lows (bearish).

Customizing Visualization Styles:

Buy signals (BUY Signal) are plotted as green upward arrows.

Sell signals (SELL Signal) are plotted as red downward arrows.

Stop-Loss (SL) & Take-Profit (TP): Configurable via percentage input.

IU Gap Fill StrategyThe IU Gap Fill Strategy is designed to capitalize on price gaps that occur between trading sessions. It identifies gaps based on a user-defined percentage threshold and executes trades when the price fills the gap within a day. This strategy is ideal for traders looking to take advantage of market inefficiencies that arise due to overnight or session-based price movements. An ATR-based trailing stop-loss is incorporated to dynamically manage risk and lock in profits.

USER INPUTS

Percentage Difference for Valid Gap - Defines the minimum gap size in percentage terms for a valid trade setup. ( Default is 0.2 )

ATR Length - Sets the lookback period for the Average True Range (ATR) calculation. (default is 14 )

ATR Factor - Determines the multiplier for the trailing stop-loss, helping in risk management. ( Default is 2.00 )

LONG CONDITION

A gap-up occurs, meaning the current session opens above the previous session’s close.

The price initially dips below the previous session's close but then recovers and closes above it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

SHORT CONDITION

A gap-down occurs, meaning the current session opens below the previous session’s close.

The price initially moves above the previous session’s close but then closes below it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

LONG EXIT

An ATR-based trailing stop-loss is set below the entry price and dynamically adjusts upwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

SHORT EXIT

An ATR-based trailing stop-loss is set above the entry price and dynamically adjusts downwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

WHY IT IS UNIQUE

Precision in Identifying Gaps - The strategy focuses on real price gaps rather than minor fluctuations.

Dynamic Risk Management - Uses ATR-based trailing stop-loss to secure profits while allowing the trade to run.

Versatility - Works on stocks, indices, forex, and any market that experiences session-based gaps.

Optimized Entry Conditions - Ensures entries are taken only when the price attempts to fill the gap, reducing false signals.

HOW USERS CAN BENEFIT FROM IT

Enhance Trade Timing - Captures high-probability trade setups based on market inefficiencies caused by gaps.

Minimize Risk - The ATR trailing stop-loss helps protect gains and limit losses.

Works in Different Market Conditions - Whether markets are trending or consolidating, the strategy adapts to potential gap fill opportunities.

Fully Customizable - Users can fine-tune gap percentage, ATR settings, and stop-loss parameters to match their trading style.

Fibonacci-Only Strategy V2Fibonacci-Only Strategy V2

This strategy combines Fibonacci retracement levels with pattern recognition and statistical confirmation to identify high-probability trading opportunities across multiple timeframes.

Core Strategy Components:

Fibonacci Levels: Uses key Fibonacci retracement levels (19% and 82.56%) to identify potential reversal zones

Pattern Recognition: Analyzes recent price patterns to find similar historical formations

Statistical Confirmation: Incorporates statistical analysis to validate entry signals

Risk Management: Includes customizable stop loss (fixed or ATR-based) and trailing stop features

Entry Signals:

Long entries occur when price touches or breaks the 19% Fibonacci level with bullish confirmation

Short entries require Fibonacci level interaction, bearish confirmation, and statistical validation

All signals are visually displayed with color-coded markers and dashboard

Trading Method:

When a triangle signal appears, open a position on the next candle

Alternatively, after seeing a signal on a higher timeframe, you can switch to a lower timeframe to find a more precise entry point

Entry signals are clearly marked with visual indicators for easy identification

Risk Management Features:

Adjustable stop loss (percentage-based or ATR-based)

Optional trailing stops for protecting profits

Multiple take-profit levels for strategic position exit

Customization Options:

Timeframe selection (1m to Daily)

Pattern length and similarity threshold adjustment

Statistical period and weight configuration

Risk parameters including stop loss and trailing stop settings

This strategy is particularly well-suited for cryptocurrency markets due to their tendency to respect Fibonacci levels and technical patterns. Crypto's volatility is effectively managed through the customizable stop-loss and trailing-stop mechanisms, making it an ideal tool for traders in digital asset markets.

For optimal performance, this strategy works best on higher timeframes (30m, 1h and above) and is not recommended for low timeframe scalping. The Fibonacci pattern recognition requires sufficient price movement to generate reliable signals, which is more consistently available in medium to higher timeframes.

Users should avoid trading during sideways market conditions, as the strategy performs best during trending markets with clear directional movement. The statistical confirmation component helps filter out some sideways market signals, but it's recommended to manually avoid ranging markets for best results.

Optimized Auto-Detect Strategy (MA, ATR, Trend, RSI) Overview

This script is designed for traders seeking a trend-following approach that adapts to different currency pairs (e.g., EURUSD, NZDUSD, XAUUSD). It combines moving average crossovers with ATR-based stops, optional trend filters, and RSI filters to help reduce false signals and capture larger moves.

Key Features

1. Auto-Detect Logic

- Automatically applies different moving average periods and ATR multipliers based on the symbol (e.g., XAUUSD, EURUSD, NZDUSD).

- Makes it easy to switch charts without manually adjusting parameters each time.

2. ATR-Based Stop

- Uses the Average True Range (ATR) to set dynamic stop-loss levels, adapting to each market’s volatility.

3. Optional Trend Filter

- Filters out trades if price is below the 200 SMA for longs (and above for shorts), aiming to avoid choppy, range-bound markets.

4. Optional RSI Filter

- Only enters long if RSI is above a certain threshold (e.g., 50), or short if below another threshold, reducing entries during low momentum.

5. Partial Exit & Trailing/Break-Even

- Locks in partial profit at a chosen R:R (e.g., 1:1), then either trails the remaining position or moves the stop to break-even.

- This helps capture additional gains if the trend extends beyond the initial target.

6. Customizable Parameters

- You can toggle on/off each filter (Trend, RSI) and adjust the ATR multiplier, MA periods, partial exit levels, etc.

- Allows easy optimization for different pairs or timeframes.

How to Use

1. Add to Chart: Click “Add to chart” in the Pine Editor.

2. Configure Inputs: In the script’s settings, toggle the filters you want (Trend Filter, RSI Filter, etc.) and set your desired ATR multiplier, RSI thresholds, partial exit ratio, etc.

3. Strategy Tester: Check the performance under the “Strategy Tester” tab. Adjust parameters if needed.

4. Realistic Settings: Consider adding spreads/commissions in the “Properties” tab for more accurate backtests, especially if you trade pairs with higher spreads (like XAUUSD).

Disclaimer

No Guarantee: This script does not guarantee profits. Markets are unpredictable, and results may vary with market conditions.

For Educational Purposes: Always do your own research and forward testing. Past performance does not indicate future results.

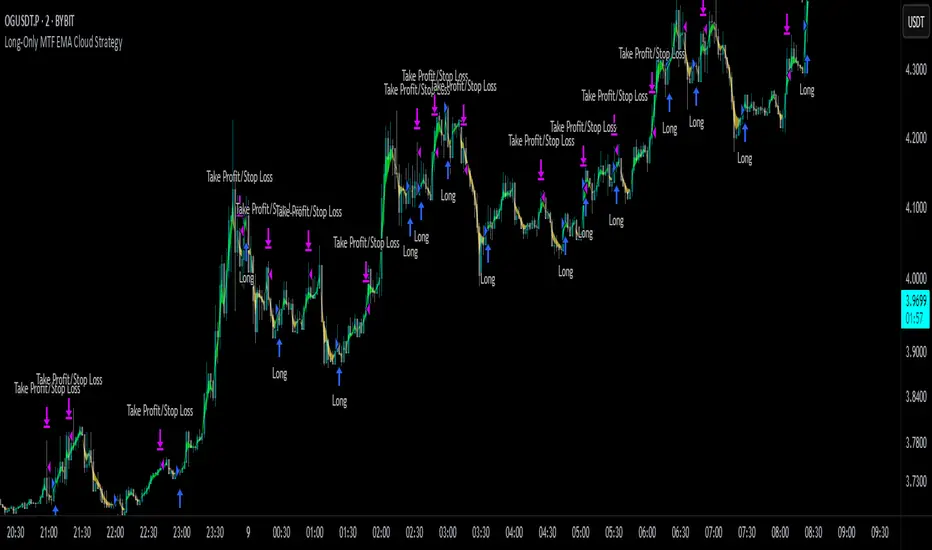

Long-Only MTF EMA Cloud StrategyOverview:

The Long-Only EMA Cloud Strategy is a powerful trend-following strategy designed to help traders identify and capitalize on bullish market conditions. By utilizing an Exponential Moving Average (EMA) Cloud, this strategy provides clear and reliable signals for entering long positions when the market trend is favorable. The EMA cloud acts as a visual representation of the trend, making it easier for traders to make informed decisions. This strategy is ideal for traders who prefer to trade in the direction of the trend and focus exclusively on long positions.

Key Features:

EMA Cloud:

The strategy uses two EMAs (short and long) to create a dynamic cloud.

The cloud is bullish when the short EMA is above the long EMA, indicating a strong upward trend.

The cloud is bearish when the short EMA is below the long EMA, indicating a downward trend or consolidation.

Long Entry Signals:

A long position is opened when the EMA cloud turns bullish, which occurs when the short EMA crosses above the long EMA.

This crossover signals a potential shift in market sentiment from bearish to bullish, providing an opportunity to enter a long trade.

Adjustable Timeframe:

The EMA cloud can be calculated on the same timeframe as the chart or on a higher/lower timeframe for multi-timeframe analysis.

This flexibility allows traders to adapt the strategy to their preferred trading style and time horizon.

Risk Management:

The strategy includes adjustable stop loss and take profit levels to help traders manage risk and lock in profits.

Stop loss and take profit levels are calculated as a percentage of the entry price, ensuring consistency across different assets and market conditions.

Alerts:

Built-in alerts notify you when a long entry signal is generated, ensuring you never miss a trading opportunity.

Alerts can be customized to suit your preferences, providing real-time notifications for potential trades.

Visualization:

The EMA cloud is plotted on the chart, providing a clear visual representation of the trend.

Buy signals are marked with a green label below the price bar, making it easy to identify entry points.

How to Use:

Add the Script:

Add the script to your chart in TradingView.

Set EMA Lengths:

Adjust the Short EMA Length and Long EMA Length in the settings to suit your trading style.

For example, you might use a shorter EMA (e.g., 21) for more responsive signals or a longer EMA (e.g., 50) for smoother signals.

Choose EMA Cloud Resolution:

Select the EMA Cloud Resolution (timeframe) for the cloud calculation.

You can choose the same timeframe as the chart or a different timeframe (higher or lower) for multi-timeframe analysis.

Adjust Risk Management:

Set the Stop Loss (%) and Take Profit (%) levels according to your risk tolerance and trading goals.

For example, you might use a 1% stop loss and a 2% take profit for a 1:2 risk-reward ratio.

Enable Alerts:

Enable alerts to receive notifications for long entry signals.

Alerts can be configured to send notifications via email, SMS, or other preferred methods.

Monitor and Trade:

Monitor the chart for buy signals and execute trades accordingly.

Use the EMA cloud as a visual guide to confirm the trend direction before entering a trade.

Ideal For:

Trend-Following Traders: This strategy is perfect for traders who prefer to trade in the direction of the trend and capitalize on sustained price movements.

Long-Only Traders: If you prefer to focus exclusively on long positions, this strategy provides a clear and systematic approach to identifying bullish opportunities.

Multi-Timeframe Analysts: The adjustable EMA cloud resolution allows you to analyze trends across different timeframes, making it suitable for both short-term and long-term traders.

Risk-Averse Traders: The inclusion of stop loss and take profit levels helps manage risk and protect your capital.

MACD Crossover Strategy MACD Crossover Strategy:

This strategy is based on the Moving Average Convergence Divergence (MACD) indicator, a popular tool used in technical analysis to identify potential trend changes and momentum in price movements. The strategy focuses on MACD crossovers within a specific "important zone" to generate trading signals.

Key Components:

1. MACD Calculation: The strategy uses customizable parameters for fast length (default 12), slow length (default 26), and signal length (default 9) to calculate the MACD line and signal line.

2. Important Zone: Defined by upper and lower thresholds (default 0.5 and -0.5), this zone helps filter out potentially less significant crossovers.

3. Entry Conditions:

- Long (Buy) Entry: When the MACD line crosses above the signal line within the important zone.

- Short (Sell) Entry: When the MACD line crosses below the signal line within the important zone.

4. Exit Conditions: The strategy closes positions on opposite crossover signals. Long positions are closed on bearish crossovers, and short positions on bullish crossovers.

5. Visualization:

- MACD line (blue) and signal line (orange) are plotted.

- The zero line, upper threshold, and lower threshold are displayed for reference.

- Buy signals are represented by green triangles at the bottom of the chart.

- Sell signals are shown as red triangles at the top of the chart.

This strategy aims to capture trend changes while filtering out potentially false signals that occur when the MACD is at extreme values. By focusing on crossovers within the important zone, the strategy attempts to identify more reliable trading opportunities.

Traders can adjust the MACD parameters and the important zone thresholds to fine-tune the strategy for different assets or timeframes. As with any trading strategy, it's crucial to thoroughly backtest and consider risk management before using it in live trading.

Dual SuperTrend w VIX Filter - Strategy [presentTrading]Hey everyone! Haven't been here for a long time. Been so busy again in the past 2 months. I recently started working on analyzing the combination of trend strategy and VIX, but didn't get outstanding results after a few tries. Sharing this tool with all of you in case you have better insights.

█ Introduction and How it is Different

The Dual SuperTrend with VIX Filter Strategy combines traditional trend following with market volatility analysis. Unlike conventional SuperTrend strategies that focus solely on price action, this experimental system incorporates VIX (Volatility Index) as an adaptive filter to create a more context-aware trading approach. By analyzing where current volatility stands relative to historical norms, the strategy adjusts to different market environments rather than applying uniform logic across all conditions.

BTCUSD 6hr Long Short Performance

█ Strategy, How it Works: Detailed Explanation

🔶 Dual SuperTrend Core

The strategy uses two SuperTrend indicators with different sensitivity settings:

- SuperTrend 1: Length = 13, Multiplier = 3.5

- SuperTrend 2: Length = 8, Multiplier = 5.0

The SuperTrend calculation follows this process:

1. ATR = Average of max(High-Low, |High-PreviousClose|, |Low-PreviousClose|) over 'length' periods

2. UpperBand = (High+Low)/2 - (Multiplier * ATR)

3. LowerBand = (High+Low)/2 + (Multiplier * ATR)

Trend direction is determined by:

- If Close > previous LowerBand, Trend = Bullish (1)

- If Close < previous UpperBand, Trend = Bearish (-1)

- Otherwise, Trend = previous Trend

🔶 VIX Analysis Framework

The core innovation lies in the VIX analysis system:

1. Statistical Analysis:

- VIX Mean = SMA(VIX, 252)

- VIX Standard Deviation = StdDev(VIX, 252)

- VIX Z-Score = (Current VIX - VIX Mean) / VIX StdDev

2. **Volatility Bands:

- Upper Band 1 = VIX Mean + (2 * VIX StdDev)

- Upper Band 2 = VIX Mean + (3 * VIX StdDev)

- Lower Band 1 = VIX Mean - (2 * VIX StdDev)

- Lower Band 2 = VIX Mean - (3 * VIX StdDev)

3. Volatility Regimes:

- "Very Low Volatility": VIX < Lower Band 1

- "Low Volatility": Lower Band 1 ≤ VIX < Mean

- "Normal Volatility": Mean ≤ VIX < Upper Band 1

- "High Volatility": Upper Band 1 ≤ VIX < Upper Band 2

- "Extreme Volatility": VIX ≥ Upper Band 2

4. VIX Trend Detection:

- VIX EMA = EMA(VIX, 10)

- VIX Rising = VIX > VIX EMA

- VIX Falling = VIX < VIX EMA

Local performance:

🔶 Entry Logic Integration

The strategy combines trend signals with volatility filtering:

Long Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bullish (trend = 1)

- AND selected VIX filter condition must be satisfied

Short Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bearish (trend = -1)

- AND selected VIX filter condition must be satisfied

Available VIX filter rules include:

- "Below Mean + SD": VIX < Lower Band 1

- "Below Mean": VIX < VIX Mean

- "Above Mean": VIX > VIX Mean

- "Above Mean + SD": VIX > Upper Band 1

- "Falling VIX": VIX < VIX EMA

- "Rising VIX": VIX > VIX EMA

- "Any": No VIX filtering

█ Trade Direction

The strategy allows testing in three modes:

1. **Long Only:** Test volatility effects on uptrends only

2. **Short Only:** Examine volatility's impact on downtrends only

3. **Both (Default):** Compare how volatility affects both trend directions

This enables comparative analysis of how volatility regimes impact bullish versus bearish markets differently.

█ Usage

Use this strategy as an experimental framework:

1. Form a hypothesis about how volatility affects trend reliability

2. Configure VIX filters to test your specific hypothesis

3. Analyze performance across different volatility regimes

4. Compare results between uptrends and downtrends

5. Refine your volatility filtering approach based on results

6. Share your findings with the trading community

This framework allows you to investigate questions like:

- Are uptrends more reliable during rising or falling volatility?

- Do downtrends perform better when volatility is above or below its historical average?

- Should different volatility filters be applied to long vs. short positions?

█ Default Settings

The default settings serve as a starting point for exploration:

SuperTrend Parameters:

- SuperTrend 1 (Length=13, Multiplier=3.5): More responsive to trend changes

- SuperTrend 2 (Length=8, Multiplier=5.0): More selective filter requiring stronger trends

VIX Analysis Settings:

- Lookback Period = 252: Establishes a full market cycle for volatility context

- Standard Deviation Bands = 2 and 3 SD: Creates statistically significant regime boundaries

- VIX Trend Period = 10: Balances responsiveness with noise reduction

Default VIX Filter Selection:

- Long Entry: "Above Mean" - Tests if uptrends perform better during above-average volatility

- Short Entry: "Rising VIX" - Tests if downtrends accelerate when volatility is increasing

Feel Free to share your insight below!!!

Supertrend TP SL (PRO)2. Main Components:

Supertrend Indicator:

Theoretical basis: The Supertrend indicator is based on two main concepts: Average True Range (ATR) and Factor. ATR measures the extent of price fluctuations in a given period of time, while Factor determines the sensitivity of the indicator to price changes.

Mechanism of operation: The indicator calculates two possible lines: one line representing the potential support level and another line representing the potential resistance level. The selection of the appropriate line depends on the current price direction. When the price is above the line, the indicator is considered to be in an uptrend, and vice versa.

Customizable inputs:

atrPeriod: Allows the trader to specify the time period for calculating the ATR. Shorter periods make the indicator more sensitive to price changes, while longer periods reduce its sensitivity.

factor: Allows the adjustment of the factor. Higher values make the indicator less likely to give false signals, but they may also delay entry signals.

Risk Management:

Take Profit and Stop Loss Orders:

TPPoints: Specifies the distance between the entry price and the take profit level. This distance is expressed in points, and is converted to an actual price value using syminfo.mintick (the smallest possible price movement of the traded asset).

SLPoints: Specifies the distance between the entry price and the stop loss level.

Importance: These orders allow the trader to specify the maximum loss he is willing to take and the profit target he is aiming to achieve, which helps in effective risk management.

Activate/Disable Trades:

isLongEnabled: Allows buy trades to be enabled or disabled, which allows the trader to trade in one direction only (for example, only trade in the uptrend during a bull market).

isShortEnabled: Allows sell trades to be enabled or disabled.

isTakeProfitEnabled: Allows take profit orders to be enabled or disabled. The trader may wish to disable them if he prefers to manage his trades manually.

isStopLossEnabled: Allows you to enable or disable stop loss orders. Although disabling them may seem tempting in some cases, it is a very risky move.

Visual Customization:

Line Style and Width:

lineStyle: Allows the trader to choose the style of lines used to draw TP and SL levels (Solid, Dashed, Dotted).

lineWidth: Sets the thickness of the lines.

Label Size:

labelSize: Allows you to set the size of the labels that display TP and SL levels (Small, Normal, Large).

Colors:

bullColor, bearColor, tpColor, slColor: Allows the trader to customize the colors of the different elements on the chart, making visual analysis easier.

3. Strategy Logic:

Determining Entry Signals: The strategy relies on the Supertrend indicator to determine entry signals. When the Supertrend trend changes from bearish to bullish, a buy trade is triggered (if isLongEnabled is enabled). When the trend changes from bullish to bearish, a sell trade is triggered (if isShortEnabled is enabled).

Order Execution: Once the entry signal is triggered, the strategy automatically places buy or sell orders.

Trade Management: After opening a trade, the strategy monitors the price and automatically triggers Take Profit and Stop Loss orders if the price reaches the specified levels.

Visualization: The strategy displays useful information on the chart, such as TP and SL lines, entry and exit signals, which helps the trader understand the strategy’s behavior and evaluate its performance.

4. Advanced Tips:

Optimizing Settings: The strategy’s performance can be improved by adjusting different input values. For example, the trader can experiment with different values for atrPeriod and factor to improve the accuracy of Supertrend signals.

Combining Indicators: This strategy can be combined with other indicators to improve the accuracy of entry signals. For example, the Relative Strength Index (RSI) can be used to confirm Supertrend signals.

Time Analysis: The strategy’s performance can be analyzed over different time periods to evaluate its effectiveness in various market conditions.

Strategy Testing: Before using the strategy in real trading, it should be tested on historical data (Backtesting) to evaluate its performance and determine the optimal settings.

5. Associated Risks:

False Signals: The Supertrend indicator may sometimes give false signals, especially in volatile markets.

Losses: Even with the use of stop loss orders, the trader may be exposed to significant losses.

Over-optimization: Over-optimization of settings on historical data may lead to misleading results. The trader should be careful about generalizing the results to future data.

Over-reliance on automation: The automated strategy should not be relied upon completely. The trader should monitor the trades and make appropriate decisions when necessary.

6. Disclaimer:

I am not a licensed financial advisor. This strategy is provided for educational and illustrative purposes only and should not be considered as investment advice. Trading in financial markets involves significant risks and you may lose your invested capital. Before making any investment decisions, consult a qualified financial advisor and conduct your own research. You alone are responsible for your trading decisions and their results. By using this strategy, you acknowledge and agree that I am not responsible for any losses or damages you may incur.

2. المكونات الرئيسية:

مؤشر Supertrend:

الأساس النظري: يعتمد مؤشر Supertrend على مفهومين رئيسيين هما: متوسط المدى الحقيقي (Average True Range - ATR) ومعامل الضرب (Factor). ATR يقيس مدى تقلبات الأسعار في فترة زمنية محددة، بينما Factor يحدد مدى حساسية المؤشر لتغيرات الأسعار.

آلية العمل: يقوم المؤشر بحساب خطين محتملين: خط يمثل مستوى الدعم المحتمل وخط آخر يمثل مستوى المقاومة المحتمل. يعتمد اختيار الخط المناسب على اتجاه السعر الحالي. عندما يكون السعر أعلى من الخط، يعتبر المؤشر في اتجاه صاعد، والعكس صحيح.

المدخلات القابلة للتخصيص:

atrPeriod: يتيح للمتداول تحديد الفترة الزمنية لحساب ATR. الفترات الأقصر تجعل المؤشر أكثر حساسية لتغيرات الأسعار، بينما الفترات الأطول تقلل من حساسيته.

factor: يسمح بتعديل معامل الضرب. القيم الأعلى تجعل المؤشر أقل عرضة لإعطاء إشارات خاطئة، ولكنها قد تؤخر أيضًا إشارات الدخول.

إدارة المخاطر:

أوامر جني الأرباح وإيقاف الخسارة:

TPPoints: يحدد المسافة بين سعر الدخول ومستوى جني الأرباح. يتم التعبير عن هذه المسافة بالنقاط (Points)، ويتم تحويلها إلى قيمة سعرية فعلية باستخدام syminfo.mintick (أصغر حركة سعرية ممكنة للأصل المتداول).

SLPoints: يحدد المسافة بين سعر الدخول ومستوى إيقاف الخسارة.

الأهمية: تتيح هذه الأوامر للمتداول تحديد الحد الأقصى للخسارة التي يرغب في تحملها والهدف الربحي الذي يسعى لتحقيقه، مما يساعد على إدارة المخاطر بشكل فعال.

تفعيل/تعطيل الصفقات:

isLongEnabled: يسمح بتفعيل أو تعطيل صفقات الشراء، مما يمكن المتداول من التداول في اتجاه واحد فقط (على سبيل المثال، التداول فقط في الاتجاه الصاعد خلال سوق صاعدة).

isShortEnabled: يسمح بتفعيل أو تعطيل صفقات البيع.

isTakeProfitEnabled: يسمح بتفعيل أو تعطيل أوامر جني الأرباح. قد يرغب المتداول في تعطيلها إذا كان يفضل إدارة صفقاته يدويًا.

isStopLossEnabled: يسمح بتفعيل أو تعطيل أوامر إيقاف الخسارة. على الرغم من أن تعطيلها قد يبدو مغريًا في بعض الحالات، إلا أنه يعتبر خطوة محفوفة بالمخاطر للغاية.

التخصيص المرئي:

نمط وعرض الخطوط:

lineStyle: يتيح للمتداول اختيار نمط الخطوط المستخدمة لرسم مستويات TP و SL (Solid, Dashed, Dotted).

lineWidth: يحدد سمك الخطوط.

حجم الملصقات:

labelSize: يسمح بتحديد حجم الملصقات التي تعرض مستويات TP و SL (Small, Normal, Large).

الألوان:

bullColor, bearColor, tpColor, slColor: تتيح للمتداول تخصيص ألوان العناصر المختلفة على الرسم البياني، مما يسهل عملية التحليل البصري.

3. منطق عمل الاستراتيجية:

تحديد إشارات الدخول: تعتمد الاستراتيجية على مؤشر Supertrend لتحديد إشارات الدخول. عندما يتغير اتجاه Supertrend من هابط إلى صاعد، يتم تفعيل صفقة شراء (إذا كانت isLongEnabled مفعلة). وعندما يتغير الاتجاه من صاعد إلى هابط، يتم تفعيل صفقة بيع (إذا كانت isShortEnabled مفعلة).

تنفيذ الأوامر: بمجرد تفعيل إشارة الدخول، تقوم الاستراتيجية بوضع أوامر الشراء أو البيع تلقائيًا.

إدارة الصفقات: بعد فتح الصفقة، تقوم الاستراتيجية بمراقبة السعر وتفعيل أوامر جني الأرباح وإيقاف الخسارة تلقائيًا في حالة وصول السعر إلى المستويات المحددة.

التمثيل المرئي: تعرض الاستراتيجية معلومات مفيدة على الرسم البياني، مثل خطوط TP و SL وإشارات الدخول والخروج، مما يساعد المتداول على فهم سلوك الاستراتيجية وتقييم أدائها.

4. نصائح متقدمة:

تحسين الإعدادات: يمكن تحسين أداء الاستراتيجية من خلال تعديل قيم المدخلات المختلفة. على سبيل المثال، يمكن للمتداول تجربة قيم مختلفة لـ atrPeriod و factor لتحسين دقة إشارات Supertrend.

الجمع بين المؤشرات: يمكن دمج هذه الاستراتيجية مع مؤشرات أخرى لتحسين دقة إشارات الدخول. على سبيل المثال، يمكن استخدام مؤشر القوة النسبية (RSI) لتأكيد إشارات Supertrend.

التحليل الزمني: يمكن تحليل أداء الاستراتيجية على مدى فترات زمنية مختلفة لتقييم مدى فعاليتها في ظروف السوق المتنوعة.

اختبار الاستراتيجية: قبل استخدام الاستراتيجية في التداول الحقيقي، يجب اختبارها على بيانات تاريخية (Backtesting) لتقييم أدائها وتحديد الإعدادات المثلى.

5. المخاطر المرتبطة:

الإشارات الخاطئة: قد يعطي مؤشر Supertrend إشارات خاطئة في بعض الأحيان، خاصة في الأسواق المتقلبة.

الخسائر: حتى مع استخدام أوامر إيقاف الخسارة، قد يتعرض المتداول لخسائر كبيرة.

التحسين المفرط: قد يؤدي التحسين المفرط للإعدادات على بيانات تاريخية إلى نتائج مضللة. يجب أن يكون المتداول حذرًا بشأن تعميم النتائج على البيانات المستقبلية.

الاعتماد الزائد على الأتمتة: يجب عدم الاعتماد بشكل كامل على الاستراتيجية الآلية. يجب على المتداول مراقبة الصفقات واتخاذ القرارات المناسبة عند الضرورة.

6. إخلاء المسؤولية:

أنا لست مستشارًا ماليًا مرخصًا. هذه الاستراتيجية مقدمة لأغراض تعليمية وتوضيحية فقط، ولا ينبغي اعتبارها نصيحة استثمارية. التداول في الأسواق المالية ينطوي على مخاطر كبيرة، وقد تخسر رأس المال المستثمر. قبل اتخاذ أي قرارات استثمارية، استشر مستشارًا ماليًا مؤهلاً وقم بإجراء بحثك الخاص. أنت وحدك المسؤول عن قراراتك التجارية ونتائجها. باستخدام هذه الاستراتيجية، فإنك تقر وتوافق على أنني لست مسؤولاً عن أي خسائر أو أضرار قد تتكبدها.

Sniper Trade Pro (ES 15-Min) - Topstep Optimized🔹 Overview

Sniper Trade Pro is an advanced algorithmic trading strategy designed specifically for E-mini S&P 500 (ES) Futures on the 15-minute timeframe. This strategy is optimized for Topstep 50K evaluations, incorporating strict risk management to comply with their max $1,000 daily loss limit while maintaining a high probability of success.

It uses a multi-confirmation approach, integrating:

✅ Money Flow Divergence (MFD) → To track liquidity imbalances and institutional accumulation/distribution.

✅ Trend Confirmation (EMA + VWAP) → To identify strong trend direction and avoid choppy markets.

✅ ADX Strength Filter → To ensure entries only occur in trending conditions, avoiding weak setups.

✅ Break-Even & Dynamic Stop-Losses → To reduce drawdowns and protect profits dynamically.

This script automatically generates Buy and Sell signals and provides built-in risk management for automated trading execution through TradingView Webhooks.

🔹 How Does This Strategy Work?

📌 1. Trend Confirmation (EMA + VWAP)

The strategy uses:

✔ 9-EMA & 21-EMA: Fast-moving averages to detect short-term momentum.

✔ VWAP (Volume-Weighted Average Price): Ensures trades align with institutional volume flow.

How it works:

Bullish Condition: 9-EMA above 21-EMA AND price above VWAP → Confirms buy trend.

Bearish Condition: 9-EMA below 21-EMA AND price below VWAP → Confirms sell trend.

📌 2. Liquidity & Money Flow Divergence (MFD)

This indicator measures liquidity shifts by tracking momentum changes in price and volume.

✔ MFD Calculation:

Uses Exponential Moving Average (EMA) of Momentum (MOM) to detect changes in buying/selling pressure.

If MFD is above its moving average, it signals liquidity inflows → bullish strength.

If MFD is below its moving average, it signals liquidity outflows → bearish weakness.

Why is this important?

Detects when Smart Money is accumulating or distributing before major moves.