Machine Learning Key Levels [AlgoAlpha]🟠 OVERVIEW

This script plots Machine Learning Key Levels on your chart by detecting historical pivot points and grouping them using agglomerative clustering to highlight price levels with the most past reactions. It combines a pivot detection, hierarchical clustering logic, and an optional silhouette method to automatically select the optimal number of key levels, giving you an adaptive way to visualize price zones where activity concentrated over time.

🟠 CONCEPTS

Agglomerative clustering is a bottom-up method that starts by treating each pivot as its own cluster, then repeatedly merges the two closest clusters based on the average distance between their members until only the desired number of clusters remain. This process creates a hierarchy of groupings that can flexibly describe patterns in how price reacts around certain levels. This offers an advantage over K-means clustering, since the number of clusters does not need to be predefined. In this script, it uses an average linkage approach, where distance between clusters is computed as the average pairwise distance of all contained points.

The script finds pivot highs and lows over a set lookback period and saves them in a buffer controlled by the Pivot Memory setting. When there are at least two pivots, it groups them using agglomerative clustering: it starts with each pivot as its own group and keeps merging the closest pairs based on their average distance until the desired number of clusters is left. This number can be fixed or chosen automatically with the silhouette method, which checks how well each point fits in its cluster compared to others (higher scores mean cleaner separation). Once clustering finishes, the script takes the average price of each cluster to create key levels, sorts them, and draws horizontal lines with labels and colors showing their strength. A metrics table can also display details about the clusters to help you understand how the levels were calculated.

🟠 FEATURES

Agglomerative clustering engine with average linkage to merge pivots into level groups.

Dynamic lines showing each cluster’s price level for clarity.

Labels indicating level strength either as percent of all pivots or raw counts.

A metrics table displaying pivot count, cluster count, silhouette score, and average pivots per cluster.

Optional silhouette-based auto-selection of cluster count to adaptively find the best fit.

🟠 USAGE

Add the indicator to any chart. Choose how far back to detect pivots using Pivot Length and set Pivot Memory to control how many are kept for clustering (more pivots give smoother levels but can slow performance). If you want the script to pick the number of levels automatically, enable Auto No. Levels ; otherwise, set Number of Levels . The colored horizontal lines represent the calculated key levels, and circles show where pivots occurred colored by which cluster they belong to. The labels beside each level indicate its strength, so you can see which levels are supported by more pivots. If Show Metrics Table is enabled, you will see statistics about the clustering in the corner you selected. Use this tool to spot areas where price often reacts and to plan entries or exits around levels that have been significant over time. Adjust settings to better match volatility and history depth of your instrument.

Volatility

ZF RSI PLOT1. How RSI Is Calculated

RSI is typically computed over 14 periods (days, hours, etc.) using the formula:

RSI=100−1001+RS

RSI=100−1+RS100

where

RS=Average Gain over N periodsAverage Loss over N periods

RS=Average Loss over N periodsAverage Gain over N periods

2. Overbought (> 70)

Definition: An RSI reading above 70 suggests that the instrument has experienced relatively large gains and may be “overbought.”

Interpretation:

Potential Reversal: Prices may have risen too far, too fast, and could be due for a pullback or consolidation.

Exit/Take Profits: Traders often trim long positions or tighten stops as RSI climbs above 70.

Confirmation Needed:

Bearish “RSI divergence” (price makes a higher high while RSI makes a lower high).

Price action signals (e.g., bearish candlestick patterns).

Volume drying up on advances.

3. Oversold (< 30)

Definition: An RSI reading below 30 suggests that the instrument has experienced relatively large losses and may be “oversold.”

Interpretation:

Potential Bounce: Prices may have fallen too far, too fast, and could be due for a rebound or consolidation.

Buying Opportunity: Traders often look to initiate or add to long positions as RSI drops below 30.

Confirmation Needed:

Bullish “RSI divergence” (price makes a lower low while RSI makes a higher low).

Price action signals (e.g., hammer candlesticks, support levels).

Volume picking up on declines.

4. Divergences

Bullish Divergence: Price ↓ makes a lower low, RSI ↑ makes a higher low ⇒ possible trend change to the upside.

Bearish Divergence: Price ↑ makes a higher high, RSI ↓ makes a lower high ⇒ possible trend change to the downside.

5. Adjustments & Variations

Stronger Trends: Use 80/20 thresholds to avoid early signals in very strong up- or down-trends.

Shorter/Longer Periods: Adjust the look-back period (e.g., 9 for more sensitivity, 21 for smoother signals) depending on your time frame.

6. Limitations & Best Practices

Can Stay Extreme: In strong trends, RSI may remain overbought/oversold for extended periods—don’t trade it in isolation.

Combine with Other Tools: Use trend filters (moving averages, ADX), support/resistance, and volume to confirm entries.

Risk Management: Always set stops and manage position size; RSI signals can fail.

7. Putting It All Together

Identify Trend: Is the market in an uptrend, downtrend, or range?

Watch RSI Extremes: Note when RSI crosses above 70 or below 30.

Seek Confirmation: Look for divergences, candlestick/pricing signals, and supporting volume.

Execute & Manage: Enter with clear stop-loss levels, consider scaling, and lock in profits appropriately.

By understanding both the raw threshold signals and the nuances—like divergences and trend-context—you can harness RSI’s simplicity while mitigating its pitfalls.

Momentum Regression [BackQuant]Momentum Regression

The Momentum Regression is an advanced statistical indicator built to empower quants, strategists, and technically inclined traders with a robust visual and quantitative framework for analyzing momentum effects in financial markets. Unlike traditional momentum indicators that rely on raw price movements or moving averages, this tool leverages a volatility-adjusted linear regression model (y ~ x) to uncover and validate momentum behavior over a user-defined lookback window.

Purpose & Design Philosophy

Momentum is a core anomaly in quantitative finance — an effect where assets that have performed well (or poorly) continue to do so over short to medium-term horizons. However, this effect can be noisy, regime-dependent, and sometimes spurious.

The Momentum Regression is designed as a pre-strategy analytical tool to help you filter and verify whether statistically meaningful and tradable momentum exists in a given asset. Its architecture includes:

Volatility normalization to account for differences in scale and distribution.

Regression analysis to model the relationship between past and present standardized returns.

Deviation bands to highlight overbought/oversold zones around the predicted trendline.

Statistical summary tables to assess the reliability of the detected momentum.

Core Concepts and Calculations

The model uses the following:

Independent variable (x): The volatility-adjusted return over the chosen momentum period.

Dependent variable (y): The 1-bar lagged log return, also adjusted for volatility.

A simple linear regression is performed over a large lookback window (default: 1000 bars), which reveals the slope and intercept of the momentum line. These values are then used to construct:

A predicted momentum trendline across time.

Upper and lower deviation bands , representing ±n standard deviations of the regression residuals (errors).

These visual elements help traders judge how far current returns deviate from the modeled momentum trend, similar to Bollinger Bands but derived from a regression model rather than a moving average.

Key Metrics Provided

On each update, the indicator dynamically displays:

Momentum Slope (β₁): Indicates trend direction and strength. A higher absolute value implies a stronger effect.

Intercept (β₀): The predicted return when x = 0.

Pearson’s R: Correlation coefficient between x and y.

R² (Coefficient of Determination): Indicates how well the regression line explains the variance in y.

Standard Error of Residuals: Measures dispersion around the trendline.

t-Statistic of β₁: Used to evaluate statistical significance of the momentum slope.

These statistics are presented in a top-right summary table for immediate interpretation. A bottom-right signal table also summarizes key takeaways with visual indicators.

Features and Inputs

✅ Volatility-Adjusted Momentum : Reduces distortions from noisy price spikes.

✅ Custom Lookback Control : Set the number of bars to analyze regression.

✅ Extendable Trendlines : For continuous visualization into the future.

✅ Deviation Bands : Optional ±σ multipliers to detect abnormal price action.

✅ Contextual Tables : Help determine strength, direction, and significance of momentum.

✅ Separate Pane Design : Cleanly isolates statistical momentum from price chart.

How It Helps Traders

📉 Quantitative Strategy Validation:

Use the regression results to confirm whether a momentum-based strategy is worth pursuing on a specific asset or timeframe.

🔍 Regime Detection:

Track when momentum breaks down or reverses. Slope changes, drops in R², or weak t-stats can signal regime shifts.

📊 Trade Filtering:

Avoid false positives by entering trades only when momentum is both statistically significant and directionally favorable.

📈 Backtest Preparation:

Before running costly simulations, use this tool to pre-screen assets for exploitable return structures.

When to Use It

Before building or deploying a momentum strategy : Test if momentum exists and is statistically reliable.

During market transitions : Detect early signs of fading strength or reversal.

As part of an edge-stacking framework : Combine with other filters such as volatility compression, volume surges, or macro filters.

Conclusion

The Momentum Regression indicator offers a powerful fusion of statistical analysis and visual interpretation. By combining volatility-adjusted returns with real-time linear regression modeling, it helps quantify and qualify one of the most studied and traded anomalies in finance: momentum.

BB + RSI & Volume FilterThis script overlays three sets of technical filters on your price chart and generates signals when conditions align:

Bollinger Bands

Calculates upper, middle, and lower bands using either SMA or EMA.

Buy signal when price crosses up through the lower band.

Sell signal when price crosses down through the upper band.

Volume Filter

Computes a simple moving average of volume.

Ensures breakout moves have sufficient volume by requiring current volume > SMA(volume) × multiplier.

RSI Filter

Computes RSI on the chosen source.

Buy when RSI crosses above the oversold threshold.

Sell when RSI crosses below the overbought threshold.

Only plots RSI signals that pass the volume filter.

You get:

Bollinger entry/exit shapes (labeled “BB ↑/↓”).

RSI entry/exit shapes (labeled “RSI”) only when volume confirms the move.

Alerts for each signal type.

This combination reduces false breakouts by requiring both volatility (Bollinger) or momentum (RSI) and volume confirmation

Rolling Log Returns [BackQuant]Rolling Log Returns

The Rolling Log Returns indicator is a versatile tool designed to help traders, quants, and data-driven analysts evaluate the dynamics of price changes using logarithmic return analysis. Widely adopted in quantitative finance, log returns offer several mathematical and statistical advantages over simple returns, making them ideal for backtesting, portfolio optimization, volatility modeling, and risk management.

What Are Log Returns?

In quantitative finance, logarithmic returns are defined as:

ln(Pₜ / Pₜ₋₁)

or for rolling periods:

ln(Pₜ / Pₜ₋ₙ)

where P represents price and n is the rolling lookback window.

Log returns are preferred because:

They are time additive : returns over multiple periods can be summed.

They allow for easier statistical modeling , especially when assuming normally distributed returns.

They behave symmetrically for gains and losses, unlike arithmetic returns.

They normalize percentage changes, making cross-asset or cross-timeframe comparisons more consistent.

Indicator Overview

The Rolling Log Returns indicator computes log returns either on a standard (1-period) basis or using a rolling lookback period , allowing users to adapt it to short-term trading or long-term trend analysis.

It also supports a comparison series , enabling traders to compare the return structure of the main charted asset to another instrument (e.g., SPY, BTC, etc.).

Core Features

✅ Return Modes :

Normal Log Returns : Measures ln(price / price ), ideal for day-to-day return analysis.

Rolling Log Returns : Measures ln(price / price ), highlighting price drift over longer horizons.

✅ Comparison Support :

Compare log returns of the primary instrument to another symbol (like an index or ETF).

Useful for relative performance and market regime analysis .

✅ Moving Averages of Returns :

Smooth noisy return series with customizable MA types: SMA, EMA, WMA, RMA, and Linear Regression.

Applicable to both primary and comparison series.

✅ Conditional Coloring :

Returns > 0 are colored green ; returns < 0 are red .

Comparison series gets its own unique color scheme.

✅ Extreme Return Detection :

Highlight unusually large price moves using upper/lower thresholds.

Visually flags abnormal volatility events such as earnings surprises or macroeconomic shocks.

Quantitative Use Cases

🔍 Return Distribution Analysis :

Gain insight into the statistical properties of asset returns (e.g., skewness, kurtosis, tail behavior).

📉 Risk Management :

Use historical return outliers to define drawdown expectations, stress tests, or VaR simulations.

🔁 Strategy Backtesting :

Apply rolling log returns to momentum or mean-reversion models where compounding and consistent scaling matter.

📊 Market Regime Detection :

Identify periods of consistent overperformance/underperformance relative to a benchmark asset.

📈 Signal Engineering :

Incorporate return deltas, moving average crossover of returns, or threshold-based triggers into machine learning pipelines or rule-based systems.

Recommended Settings

Use Normal mode for high-frequency trading signals.

Use Rolling mode for swing or trend-following strategies.

Compare vs. a broad market index (e.g., SPY or QQQ ) to extract relative strength insights.

Set upper and lower thresholds around ±5% for spotting major volatility days.

Conclusion

The Rolling Log Returns indicator transforms raw price action into a statistically sound return series—equipping traders with a professional-grade lens into market behavior. Whether you're conducting exploratory data analysis, building factor models, or visually scanning for outliers, this indicator integrates seamlessly into a modern quant's toolbox.

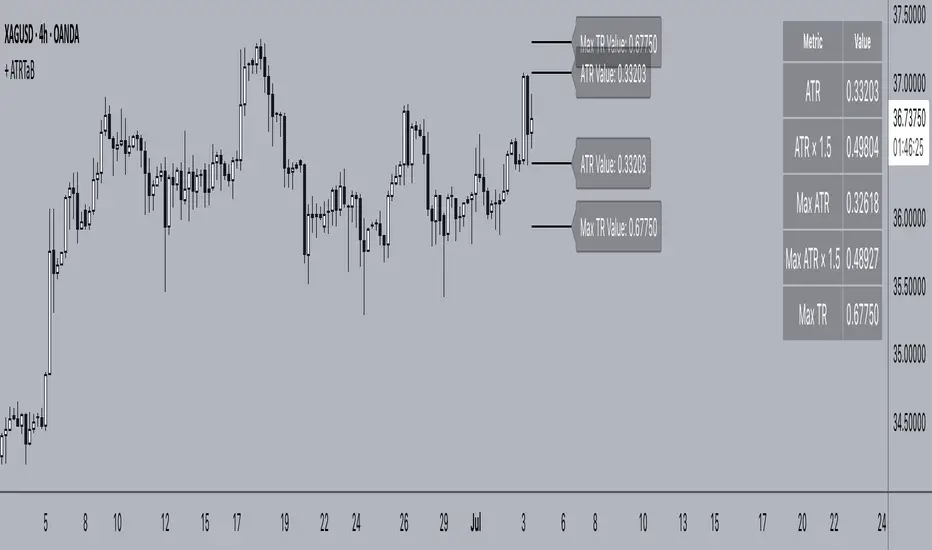

+ ATR Table and BracketsHi, all. I'm back with a new indicator—one I firmly believe could be one of the most valuable indicators you keep in your indicator toolshed—based around true range.

This is a simple, streamlined indicator utilizing true range and average true range that will help any trader with stoploss, trailing stoploss, and take-profit placement—things that I know many traders use average true range for. It could also be useful for trade entries as well, depending on the trader's style.

Typically, most traders (or at least what I've seen recommended across websites, video tutorials on YouTube, etc.) are taught to simply take the ATR number and use that, and possibly some sort of multiplier, as your stoploss and take-profit. This is fine, but I thought that it might be possible to dive a bit deeper into these values. Because an average is a combination of values, some higher, some lower, and we often see ATR spikes during periods of high volatility, I thought wouldn't it be useful to know what value those ATR spikes are, and how do they relate to the ATR? Then I thought to myself, well, what about the most volatile candle within that ATR (the candle with the greatest true range)? Couldn't knowing that value be useful to a trader? So then the idea of a table displaying these values, along with the ATR and the ATR times some multiplier number, would be a useful, simple way to display this information. That's what we have here.

The table is made up of two columns, one with the name of the metric being measured, and the other with its value. That's it. Simple.

As nice as this was, I thought an additional, great, and perhaps better, way to visualize this information would be in the form of brackets extending from the current bar. These are simply lines/labels plotted at the price values of the ATR, ATR times X, highest ATR, highest ATR times X, and highest TR value. These labels supply the actual values of the ATR, etc., but may also display the price if you should choose (both of these values are toggleable in the 'Inputs' section of the indicator.). Additionally, you can choose to display none of these labels, or all five if you wish (leaves the chart a bit cluttered, as shown in the image below), though I suspect you'll determine your preferences for which information you'd like to see and which not.

Chart with all five lines/labels displayed. I adjusted the ATRX value to 3 just to make the screenshot as legible as possible. Default is set to 1.5. As you can see, the label doesn't show the multiplier number, but the table does.

Here's a screenshot of the labels showing the price in addition to the value of the ATR, set to "Previous Closing Price," (see next paragraph for what that means) and highest TR. Personally, I don't see the value in the displaying the price, but I thought some people might want that. It's not available in the table as of now, but perhaps if I get enough requests for it I will add it.

That's basically it, but one last detail I need to go over is the dropdown box labeled "Bar Value ATR Levels are Oriented To." Firstly, this has no effect on Highest ATR, Highest ATRX, and Highest TR levels. Those are based on the ATR up to the last closed candle, meaning they aren't including the value of the currently open candle (this would be useless). However, knowing that different traders trade different ways it seemed to me prudent to allow for traders to select which opening or closing value the trader wishes to have the ATR brackets based on. For example, as someone who has consumed much No Nonsense Forex content I know that traders are urged to enter their trades in the last fifteen minutes of the trading day because the ATR is unlikely to change significantly in that period (ATR being the centerpiece of NNFX money management), so one of three selections here is to plot the brackets based on the ATR's inclusion of this value (this of course means the brackets will move while the candle is still open). The other options are to set the brackets to the current opening price, or the previous closing price. Depending on what you're trading many times these prices are virtually identical, but sometimes price gaps (stocks in particular), so, wanting your brackets placed relative to the previous close as opposed to the current open might be preferable for some traders.

And that's it. I really hope you guys like this indicator. I haven't seen anything closely similar to it on TradingView, and I think it will be something you all will find incredibly handy.

Please enjoy!

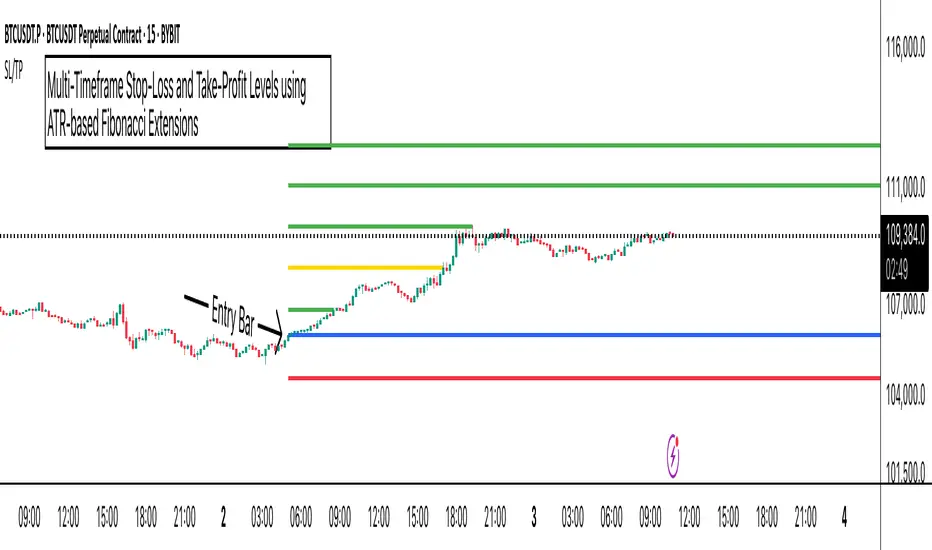

ATR Stop-Loss with Fibonacci Take-Profit [jpkxyz]ATR Stop-Loss with Fibonacci Take-Profit Indicator

This comprehensive indicator combines Average True Range (ATR) volatility analysis with Fibonacci extensions to create dynamic stop-loss and take-profit levels. It's designed to help traders set precise risk management levels and profit targets based on market volatility and mathematical ratios.

Two Operating Modes

Default Mode (Rolling Levels)

In default mode, the indicator continuously plots evolving stop-loss and take-profit levels based on real-time price action. These levels update dynamically as new bars form, creating rolling horizontal lines across the chart. I use this mode primarily to plot the rolling ATR-Level which I use to trail my Stop-Loss into profit.

Characteristics:

Levels recalculate with each new bar

All selected Fibonacci levels display simultaneously

Uses plot() functions with trackprice=true for price tracking

Custom Anchor Mode (Fixed Levels)

This is the primary mode for precision trading. You select a specific timestamp (typically your entry bar), and the indicator locks all calculations to that exact moment, creating fixed horizontal lines that represent your actual trade levels.

Characteristics:

Entry line (blue) marks your anchor point

Stop-loss calculated using ATR from the anchor bar

Fibonacci levels projected from entry-to-stop distance

Lines terminate when price breaks through them

Includes comprehensive alert system

Core Calculation Logic

ATR Stop-Loss Calculation:

Stop Loss = Entry Price ± (ATR × Multiplier)

Long positions: SL = Entry - (ATR × Multiplier)

Short positions: SL = Entry + (ATR × Multiplier)

ATR uses your chosen smoothing method (RMA, SMA, EMA, or WMA)

Default multiplier is 1.5, adjustable to your risk tolerance

Fibonacci Take-Profit Projection:

The distance from entry to stop-loss becomes the base unit (1.0) for Fibonacci extensions:

TP Level = Entry + (Entry-to-SL Distance × Fibonacci Ratio)

Available Fibonacci Levels:

Conservative: 0.618, 1.0, 1.618

Extended: 2.618, 3.618, 4.618

Complete range: 0.0 to 4.764 (23 levels total)

Multi-Timeframe Functionality

One of the indicator's most powerful features is timeframe flexibility. You can analyze on one timeframe while using stop-loss and take-profit calculations from another.

Best Practices:

Identify your entry point on execution timeframe

Enable "Custom Anchor" mode

Set anchor timestamp to your entry bar

Select appropriate analysis timeframe

Choose relevant Fibonacci levels

Enable alerts for automated notifications

Example Scenario:

Analyse trend on 4-hour chart

Execute entry on 5-minute chart for precision

Set custom anchor to your 5-minute entry bar

Configure timeframe setting to "4h" for swing-level targets

Select appropriate Fibonacci Extension levels

Result: Precise entry with larger timeframe risk management

Visual Intelligence System

Line Behaviour in Custom Anchor Mode:

Active levels: Lines extend to the right edge

Hit levels: Lines terminate at the breaking bar

Entry line: Always visible in blue

Stop-loss: Red line, terminates when hit

Take-profits: Green lines (1.618 level in gold for emphasis)

Customisation Options:

Line width (1-4 pixels)

Show/hide individual Fibonacci levels

ATR length and smoothing method

ATR multiplier for stop-loss distance

RSI-BBGun-v6.1RSI BB Gun – Operator's Guide

“Eyes on target. Wait for the right moment. Then strike.”

________________________________________

🎯 Mission Objective

RSI BB Gun identifies extreme market conditions using RSI and Bollinger Bands, then overlays trend and volatility intelligence so you know when the setup is real.

The ❌ is your target acquisition signal—price just moved from an extreme zone back into play. Now you’ve got a clean radar lock.

________________________________________

📡 How to Operate

🟣 Step 1: Watch for the ❌'s (Black X = RSI & Bollinger Band Extremes Encountered)

• The Purple X means price and RSI are both stretched—and just snapped back into range.

• The target is now in the cross hairs and potentially ready for engagement.

🟥 Step 2: Confirm the Trend

• The thick ribbon tells you if the trend is with you:

o 🟢 Green = Uptrend. Focus on long setups.

o 🔴 Red = Downtrend. Focus on puts or short plays.

• Align with trend. Only engage when the field favors your position.

🔺 Step 3: Evaluate Signal Context

• Green Triangles = price just crossed below lower Bollinger Band (oversold).

• Red Triangles = price crossed above upper Band (overbought).

• Horizontal Lines Disappeared = The bar after the green or red horizontal line disappears means its time. We patiently wait for this as it means the momentum may be changing.

• These are your early indicators—they scout the setup on the GO / NO GO DECISION.

• ❌ + triangle + trend = clean shot.

________________________________________

☁️ Avoid These Situations

• ❌ in a choppy/no-trend zone = false alarm. Don’t engage.

• Repeated black ❌s without a purple ❌confirmation = low conviction. Let it go.

________________________________________

________________________________________

🪖 Operator's Mindset

“You don’t chase trades. You stalk them. When the ❌ flashes, the system has found a target. What you do next is up to your discipline, your tools, and your plan.”

________________________________________

Note: This is a free version. Upcoming paid version includes multi-timeframes working together. Multiple strategies. Volatility meter. Make money and master the BB Gun so that you can elevate to the Snipers weapon.

🔒 Want More Firepower?

Upgraded version coming soon. Unlocks next-gen targeting tools:

• Multi-timeframe RSI intelligence in a live dashboard

• Precision-timed combo signals based on layered volatility + RSI logic

• Advanced trend filters, trade zone overlays, and sniper-level entry indicators

• Ideal for swing traders and options strategists who want clarity under pressure

💥 Budget-friendly. No subscription. Upgrade when you're ready to go Pro.

Tip: Make 4+ trades mastering this setup. Then use a small portion of the trades to gain more features. Always be in a position you cannot lose.

🆚 Why This Beats Standard RSI/BB Tools

Mission Feature Basic Indicators RSI Ribbon Lite

Trend Confirmation ❌ ✅ Ribbon Overlay

Multi-Timeframe Awareness ❌ ✅ 5-Timeframe RSI Grid

Volatility Confirmation ❌ ✅ Weighted ATR Scoring

Combo Signal Alerts ❌ ✅ ❌ Reentry Combo Alerts

TradingView Alerts ❌ ✅ Built-In Radar Ping

#rsi #bb #bollingerbands #hull ma #trend

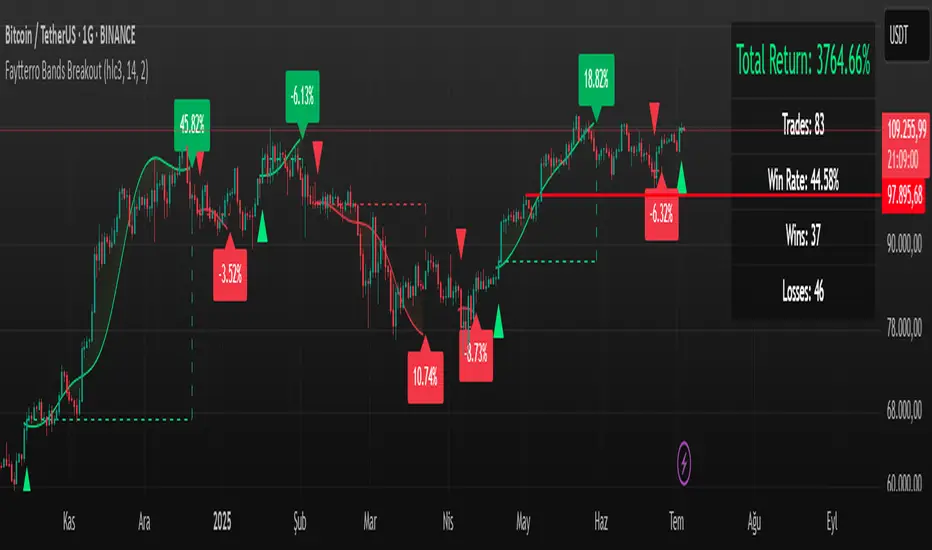

Faytterro Bands Breakout📌 Faytterro Bands Breakout 📌

This indicator was created as a strategy showcase for another script: Faytterro Bands

It’s meant to demonstrate a simple breakout strategy based on Faytterro Bands logic and includes performance tracking.

❓ What Is It?

This script is a visual breakout strategy based on a custom moving average and dynamic deviation bands, similar in concept to Bollinger Bands but with unique smoothing (centered regression) and performance features.

🔍 What Does It Do?

Detects breakouts above or below the Faytterro Band.

Plots visual trade entries and exits.

Labels each trade with percentage return.

Draws profit/loss lines for every trade.

Shows cumulative performance (compounded return).

Displays key metrics in the top-right corner:

Total Return

Win Rate

Total Trades

Number of Wins / Losses

🛠 How Does It Work?

Bullish Breakout: When price crosses above the upper band and stays above the midline.

Bearish Breakout: When price crosses below the lower band and stays below the midline.

Each trade is held until breakout invalidation, not a fixed TP/SL.

Trades are compounded, i.e., profits stack up realistically over time.

📈 Best Use Cases:

For traders who want to experiment with breakout strategies.

For visual learners who want to study past breakouts with performance metrics.

As a template to develop your own logic on top of Faytterro Bands.

⚠ Notes:

This is a strategy-like visual indicator, not an automated backtest.

It doesn't use strategy.* commands, so you can still use alerts and visuals.

You can tweak the logic to create your own backtest-ready strategy.

Unlike the original Faytterro Bands, this script does not repaint and is fully stable on closed candles.

RSI-Adaptive T3 + Squeeze Momentum Strategy✅ Strategy Guide: RSI-Adaptive T3 + Squeeze Momentum Strategy

📌 Overview

The RSI-Adaptive T3 + Squeeze Momentum Strategy is a dynamic trend-following strategy based on an RSI-responsive T3 moving average and Squeeze Momentum detection .

It adapts in real-time to market volatility to enhance entry precision and optimize risk.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main objective of this strategy is to catch the early phase of a trend and generate consistent entry signals.

Designed to be intuitive and accessible for traders from beginner to advanced levels.

✨ Key Features

RSI-Responsive T3: T3 length dynamically adjusts according to RSI values for adaptive trend detection

Squeeze Momentum: Combines Bollinger Bands and Keltner Channels to identify trend buildup phases

Visual Triggers: Entry signals are generated from T3 crossovers and momentum strength after squeeze release

📊 Trading Rules

Long Entry:

When T3 crosses upward, momentum is positive, and the squeeze has just been released.

Short Entry:

When T3 crosses downward, momentum is negative, and the squeeze has just been released.

Exit (Reversal):

When the opposite condition to the entry is triggered, the position is reversed.

💰 Risk Management Parameters

Pair & Timeframe: BTC/USD (30-minute chart)

Capital (simulated): $30,00

Order size: `$100` per trade (realistic, low-risk sizing)

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 5%

Number of Trades (backtest period): 181

📊 Performance Overview

Symbol: BTC/USD

Timeframe: 30-minute chart

Date Range: January 1, 2024 – July 3, 2025

Win Rate: 47.8%

Profit Factor: 2.01

Net Profit: 173.16 (units not specified)

Max Drawdown: 5.77% or 24.91 (0.79%)

⚙️ Indicator Parameters

Indicator Name: RSI-Adaptive T3 + Squeeze Momentum

RSI Length: 14

T3 Min Length: 5

T3 Max Length: 50

T3 Volume Factor: 0.7

BB Length: 27 (Multiplier: 2.0)

KC Length: 20 (Multiplier: 1.5, TrueRange enabled)

🖼 Visual Support

T3 slope direction, squeeze status, and momentum bars are visually plotted on the chart,

providing high clarity for quick trend analysis and execution.

🔧 Strategy Improvements & Uniqueness

Inspired by the RSI Adaptive T3 by ChartPrime and Squeeze Momentum Indicator by LazyBear ,

this strategy fuses both into a hybrid trend-reversal and momentum breakout detection system .

Compared to traditional trend-following methods, it excels at capturing early trend signals with greater sensitivity .

✅ Summary

The RSI-Adaptive T3 + Squeeze Momentum Strategy combines momentum detection with volatility-responsive risk management.

With a strong balance between visual clarity and practicality, it serves as a powerful tool for traders seeking high repeatability.

⚠️ This strategy is based on historical data and does not guarantee future profits.

Always use appropriate risk management when applying it.

Market Maker Trap Reversal V1Market Maker Trap Reversal V1 is a lightweight, precision-focused tool designed to detect the same liquidity manipulation tactics used by institutional players and market makers.

This script identifies key liquidity sweeps of prior swing highs/lows and confirms trap reversals when price closes back inside the swept range — a signature move of smart money designed to trap retail breakout traders.

Built for disciplined execution, this tool includes:

✅ Sweep detection using custom swing lookbacks

✅ Convincing trap confirmation (strong candle body)

✅ Optional NY session filter for optimal timing

✅ Clean long/short alerts for seamless automation

✅ No indicators — just raw price action and intent

Use this strategy to mirror market maker logic, avoid false breakouts, and trade with real conviction around liquidity events.

**Coded with the help of Zero"

Adaptive Squeeze Momentum +OVERVIEW

Adaptive Squeeze Momentum+ is an enhanced, auto-adaptive momentum indicator inspired by the classic Squeeze Momentum concept. This script dynamically adjusts its parameters to any timeframe without requiring manual inputs, making it a versatile tool for intraday traders and long-term investors alike.

CONCEPTS

The indicator combines Bollinger Bands (BB) and Keltner Channels (KC) to identify volatility compression ("squeeze") and expansion phases. When BB contracts within KC, a squeeze is detected, signaling reduced volatility and potential for a breakout. Additionally, a linear regression momentum calculation helps assess the strength and direction of price moves.

FEATURES

Auto-Adaptation:

Automatically adjusts BB/KC lengths and multipliers based on the chart timeframe (from 1 minute to 1 month).

Dynamic Squeeze Detection:

Clear visual encoding of squeeze status:

- Gray cross: neutral

- Blue cross: squeeze active

- Yellow cross: squeeze released

Momentum Histogram:

Colored area chart shows positive and negative momentum with slope-based coloring.

Clean Visualization:

Minimalist plots focused on actionable signals.

USAGE

Identify Squeeze Phases:

When the blue cross appears, the market is in a volatility squeeze, potentially preceding a breakout.

Monitor Momentum Direction:

The area plot shows the magnitude and direction of price momentum.

Confirm Entries and Exits:

Combine squeeze releases (yellow) with positive momentum for potential long entries or negative momentum for shorts.

Adaptable to Any Market:

Works seamlessly across cryptocurrencies, stocks, forex, and indices on all timeframes.

ALIP FX Smart Scalper – Precision for 1-Min TradersALIP FX Smart Scalper – Precision for 1-Min Traders

Looking for a powerful and clean scalping tool built for the 1-minute chart?

This indicator is engineered for serious scalpers who demand high accuracy, zero repaint, and trend-aligned signals.

✅ Key Features:

🔹 Trend-based filtering (EMA logic)

🔹 RSI + ATR + Slope conditions

🔹 No repaint – signals appear only on closed candles

🔹 Buy & Sell alerts with label and audio

🔹 Works best on BTC, NAS100, Gold (1m/5m TF)

💡 Why It Works:

The ALIP FX Smart Scalper ignores weak noise signals and only highlights clean trend-following opportunities.

Perfect for traders who want fast decisions with logic, not luck.

📌 Live test it now on TradingView

🔗

📥 More tools & education: t.me

🔻 Powered by: ALIP FX

"Success Elevated. Trade Smarter."

#ALIPFX #ScalpingIndicator #NoRepaint #TradingTools #SmartScalper #BTCUSD #NASDAQ100 #Gold

SQZMOM Breakout Strategy📌 SQZMOM Breakout Strategy – Optimized for 15-Minute Intraday Trading

SQZMOM Breakout Strategy is a momentum and volatility-based algorithmic trading system, primarily built around the Squeeze Momentum (SQZMOM) indicator. It is specifically optimized for 15-minute timeframes to exploit intraday breakouts and trend continuations.

📊 Key Features:

✅ Breakout signals based on the Squeeze Momentum indicator

✅ Trend filter using 200-period WMA (visual only, not affecting entries)

✅ RSI filter to avoid trades in overbought/oversold zones

✅ Volume and ATR filters to confirm breakout quality

✅ Position sizing dynamically scales from 5% to 20% based on signal strength

✅ Trailing Stop Loss based on user-adjustable ATR multiple (default: 2.0 ATR)

✅ No fixed Take Profit: trades ride the trend using trailing stops

⚙️ Configurable Inputs:

Bollinger Band & Keltner Channel parameters

RSI thresholds (fixed at 40 to avoid early entries against momentum)

Trailing Stop distance defined by ATR Multiplier for Trailing Stop

All parameters are user-tunable for further optimization

🟢 When Does It Enter a Trade?

Long Entry:

SQZMOM fires bullish breakout + momentum increases + price above WMA200 + sufficient volume & ATR + RSI > 40

Short Entry:

SQZMOM fires bearish breakout + momentum decreases + price below WMA200 + sufficient volume & ATR + RSI < 40

Signal entries are deferred until all filters (especially RSI) align — no crossover logic is used

🎯 Trade Management:

Position Sizing: Adjusted according to momentum strength (val), from 5% to 20%

Exit Strategy: Trailing Stop only, no hard TP — lets profits run

TP/SL logic: Trailing SL moves dynamically with price, distance = ATR × multiplier

📚 Scientific & Practical Foundations:

The model is inspired by John Carter’s “TTM Squeeze” principle: volatility contraction followed by explosive momentum

Position sizing and ATR-based trailing logic follow Ernie Chan’s adaptive risk framework in Algorithmic Trading (2013)

RSI as a trend-quality gate is consistent with classic momentum confirmation rules

Victor Osimhen Galatasaray⚽ Victor Osimhen Strategy – Ride the Momentum, Rule the Market!

Hello dear trader! 👋

We’re proud to introduce a strategy designed for crypto markets, built to be fast, smart, and resilient — just like its namesake:

📈 The Victor Osimhen Strategy ⚽

Much like the unstoppable striker himself, this strategy:

Kicks off early

Strikes at the right moment

Knows exactly when to exit the field

🧠 What Powers the Strategy?

Victor Osimhen is based on three proven elements:

WaveTrend – A powerful momentum signal for entry

Volatility Stop (VStop) – A trend direction filter

Advanced Trailing Stop – A smart exit that adapts to price action

With full Multi-Timeframe (MTF) support, it tracks the bigger picture while reacting to finer movements:

For example: While viewing the 4H chart, it listens to signals from the 2H timeframe, offering early and more accurate entries/exits.

🪙 Why Does It Work Better in Crypto?

✅ It’s built for the high volatility and 24/7 nature of crypto markets

✅ It reacts fast to momentum shifts

✅ It filters out noise using trend confirmation

✅ And it adapts dynamically with its advanced trailing exit logic

🎁 A Friendly Request

If this strategy brings you profits — and if you feel like sharing the joy —

we’d be truly happy if you considered donating a portion to Galatasaray Sports Club 💛❤️

(Of course, this is entirely voluntary and from the heart!)

🔒 Final Reminder

This strategy isn’t magic — but when used with discipline, patience, and risk control, it can be a game-changer.

Please test it in demo mode first, and only go live when you're ready.

🏁 Good Luck!

With the Victor Osimhen Strategy, you're now equipped to:

✅ Catch early momentum

✅ Stay aligned with the trend

✅ Protect your profits with style

Wishing you strong signals and solid trades!

Omori Law Recovery PhasesWhat is the Omori Law?

Originally a seismological model, the Omori Law describes how earthquake aftershocks decay over time. It follows a power law relationship: the frequency of aftershocks decreases roughly proportionally to 1/(t+c)^p, where:

t = time since the main shock

c = time offset constant

p = power law exponent (typically around 1.0)

Application to the markets

Financial markets experience "aftershocks" similar to earthquakes:

Market Crashes as Main Shocks: Major market declines (crashes) represent the initial shock event.

Volatility Decay: After a crash, market volatility typically declines following a power law pattern rather than a linear or exponential one.

Behavioral Components: The decay pattern reflects collective market psychology - initial panic gives way to uncertainty, then stabilization, and finally normalization.

The Four Recovery Phases

The Omori decay pattern in markets can be divided into distinct phases:

Acute Phase: Immediately after the crash, characterized by extreme volatility, panic selling, and sharp reversals. Trading is hazardous.

Reaction Phase: Volatility begins decreasing, but markets test previous levels. False rallies and retests of lows are common.

Repair Phase: Structure returns to the market. Volatility approaches normal levels, and traditional technical analysis becomes more reliable.

Recovery Phase: The final stage where market behavior normalizes completely. The impact of the original shock has fully decayed.

Why It Matters for Traders

Understanding where the market stands in this recovery cycle provides valuable context:

Risk Management: Adjust position sizing based on the current phase

Strategy Selection: Different strategies work in different phases

Psychological Preparation: Know what to expect based on the phase

Time Horizon Guidance: Each phase suggests appropriate time frames for trading

Unified ATR LevelsThis is a unified ATR-based band plotting indicator.

It allows you to display:

Default ATR (on current timeframe)

Preset ATR (mapped to higher timeframe logic)

User-defined ATR (on any custom timeframe)

✳️ Features:

Configurable multipliers, colors, and line widths

Smart label positioning (left, middle, right)

Clean visuals with adjustable label size

Ideal for multi-timeframe analysis and volatility zones

📌 All feedback welcome!

Tags:

volatility, ATR, multi-timeframe, support-and-resistance, custom-indicator

Price Extension from 8 EMAOverview

This indicator can be used to see how far away the price is from the 8 EMA. It compares this to the Average Daily Range % to see if the stock may be overextended. The "Extension Multiplier" represents how far the stock is extended away from the 8 EMA.

Core Concept

This indicator is best used for breakout trades that are trying to make sure they are not chasing the stock.

How to Use This Indicator

This tool is primarily intended for analyzing daily charts of individual stocks and is often used by breakout traders to evaluate potential entry areas.

If the stock is far away from the 8 EMA, it is likely not ready to break out. If it is close to the 8ema, it could be ready to move higher.

This indicator can also be used in the opposite way. For example, shorting or puts.

Understanding the colors

Green (Not Extended): Indicates the price is close to the 8 EMA. This often corresponds to periods of consolidation.

Yellow (Slightly Extended): The price is beginning to move away from the 8 EMA.

Orange (Extended): The price has moved a considerable distance from the 8 EMA.

Red (Very Extended): The price is at an extreme distance from the 8 EMA, historically increasing the likelihood of a pullback or consolidation.

Settings

Info Row Position: Adjusts the vertical position of the display table on the chart. Useful when using other indicators.

ADR Length: Sets the lookback period for calculating the Average Daily Range. Or the average range % for different timeframes.

Timeframe: Determines the timeframe for the EMA and ADR calculation (the default is Daily).

Bollinger Band + RSI Strategy ScannerVrushaNilansh Indicator for 15min. Trading Based on Bollinger Bands+RSI

Volatility Flow X – MACD + Ichimoku Hybrid Trail🌥️ Volatility Flow X – Hybrid Ichimoku Cloud Explained

This strategy combines Ichimoku’s cloud structure with real-time price position.

Unlike standard Ichimoku coloring, the cloud here reflects both trend direction and price behavior.

🔍 What the Cloud Colors Mean

🟢 Green Cloud

Senkou A > Senkou B

Price is above the cloud

→ Indicates strong uptrend; suitable for long entries

🔴 Red Cloud

Senkou A < Senkou B

Price is below the cloud

→ Indicates strong downtrend; suitable for short entries

⚪ Gray Cloud

Price contradicts trend, or price is inside the cloud

→ Represents indecision, low momentum; best to avoid entries

⚙️ Technical Features

Ichimoku Components: Tenkan-sen, Kijun-sen, Senkou Span A & B, Chikou Span

Cloud Transparency: 30%

MACD Filter: Optional momentum confirmation (customizable)

Trailing Stop: Optional dynamic trailing stop after trigger level

Directional Control: Long and short trailing rules can be set independently

📚 References

Ichimoku Charts – Nicole Elliott

Algorithmic Trading – Ernie Chan

TradingView Pine Script and hybrid trend models

⚠️ Disclaimer

This strategy is for educational and backtesting purposes only.

It is not financial advice. Always test thoroughly before applying to real trades.

ATRWhat the Indicator Shows:

A compact table with four cells is displayed in the bottom-left corner of the chart:

| ATR | % | Level | Lvl+ATR |

Explanation of the Columns:

ATR — The averaged daily range (volatility) calculated with filtering of abnormal bars (extremely large or small daily candles are ignored).

% — The percentage of the daily ATR that the price has already covered today (the difference between the daily Open and Close relative to ATR).

Level — A custom user-defined level set through the indicator settings.

Lvl+ATR — The sum of the daily ATR and the user-defined level. This can be used, for example, as a target or stop-loss reference.

Color Highlighting of the "%" Cell:

The background color of the "%" ATR cell changes depending on the value:

✅ If the value is less than 10% — the cell is green (market is calm, small movement).

➖ If the value is between 10% and 50% — no highlighting (average movement, no signal).

🟡 If the value is between 50% and 70% — the cell is yellow (movement is increasing, be alert).

🔴 If the value is above 70% — the cell is red (the market is actively moving, high volatility).

Key Features:

✔ All ATR calculations and percentage progress are performed strictly based on daily data, regardless of the chart's current timeframe.

✔ The indicator is ideal for intraday traders who want to monitor daily volatility levels.

✔ The table always displays up-to-date information for quick decision-making.

✔ Filtering of abnormal bars makes ATR more stable and objective.

What is Adaptive ATR in this Indicator:

Instead of the classic ATR, which simply averages the true range, this indicator uses a custom algorithm:

✅ It analyzes daily bars over the past 100 days.

✅ Calculates the range High - Low for each bar.

✅ If the bar's range deviates too much from the average (more than 1.8 times higher or lower), the bar is considered abnormal and ignored.

✅ Only "normal" bars are included in the calculation.

✅ The average range of these normal bars is the adaptive ATR.

Detailed Algorithm of the getAdaptiveATR() Function:

The function takes the number of bars to include in the calculation (for example, 5):

The average of the last 5 normal bars is calculated.

pinescript

Копировать

Редактировать

adaptiveATR = getAdaptiveATR(5)

Step-by-Step Process:

An empty array ranges is created to store the ranges.

Daily bars with indices from 1 to 100 are iterated over.

For each bar:

🔹 The daily High and Low with the required offset are loaded via request.security().

🔹 The range High - Low is calculated.

🔹 The temporary average range of the current array is calculated.

🔹 The bar is checked for abnormality (too large or too small).

🔹 If the bar is normal or it's the first bar — its range is added to the array.

Once the array accumulates the required number of bars (count), their average is calculated — this is the adaptive ATR.

If it's not possible to accumulate the required number of bars — na is returned.

Что показывает индикатор:

На графике внизу слева отображается компактная таблица из четырех ячеек:

ATR % Уровень Ур+ATR

Пояснения к столбцам:

ATR — усреднённый дневной диапазон (волатильность), рассчитанный с фильтрацией аномальных баров (слишком большие или маленькие дневные свечи игнорируются).

% — процент дневного ATR, который уже "прошла" цена на текущий день (разница между открытием и закрытием относительно ATR).

Уровень — пользовательский уровень, который задаётся вручную через настройки индикатора.

Ур+ATR — сумма уровня и дневного ATR. Может использоваться, например, как ориентир для целей или стопов.

Цветовая подсветка ячейки "%":

Цвет фона ячейки с процентом ATR меняется в зависимости от значения:

✅ Если значение меньше 10% — ячейка зелёная (рынок пока спокоен, маленькое движение).

➖ Если значение от 10% до 50% — фон не подсвечивается (среднее движение, нет сигнала).

🟡 Если значение от 50% до 70% — ячейка жёлтая (движение усиливается, повышенное внимание).

🔴 Если значение выше 70% — ячейка красная (рынок активно движется, высокая волатильность).

Особенности работы:

✔ Все расчёты ATR и процентного прохождения производятся исключительно по дневным данным, независимо от текущего таймфрейма графика.

✔ Индикатор подходит для трейдеров, которые торгуют внутри дня, но хотят ориентироваться на дневные уровни волатильности.

✔ В таблице всегда отображается актуальная информация для принятия быстрых торговых решений.

✔ Фильтрация аномальных баров делает ATR более устойчивым и объективным.

Что такое адаптивный ATR в этом индикаторе

Вместо классического ATR, который просто усредняет истинный диапазон, здесь используется собственный алгоритм:

✅ Он берет дневные бары за последние 100 дней.

✅ Для каждого из них рассчитывает диапазон High - Low.

✅ Если диапазон бара слишком сильно отличается от среднего (более чем в 1.8 раза больше или меньше), бар считается аномальным и игнорируется.

✅ Только нормальные бары попадают в расчёт.

✅ В итоге считается среднее из диапазонов этих нормальных баров — это и есть адаптивный ATR.

Подробный алгоритм функции getAdaptiveATR()

Функция принимает количество баров для расчёта (например, 5):

Считается 5 последних нормальных баров

pinescript

Копировать

Редактировать

adaptiveATR = getAdaptiveATR(5)

Пошагово:

Создаётся пустой массив ranges для хранения диапазонов.

Перебираются дневные бары с индексами от 1 до 100.

Для каждого бара:

🔹 Через request.security() подгружаются дневные High и Low с нужным смещением.

🔹 Считается диапазон High - Low.

🔹 Считается временное среднее диапазона по текущему массиву.

🔹 Проверяется, не является ли бар аномальным (слишком большой или маленький).

🔹 Если бар нормальный или это самый первый бар — его диапазон добавляется в массив.

Как только массив набирает заданное количество баров (count), берётся их среднее значение — это и есть адаптивный ATR.

Если не удалось набрать нужное количество баров — возвращается na.

Volatility Flow X | Dual Trend Strategy [VWMA+SMA+ADX]📌 Strategy Title

Volatility Flow X | Dual Trend Strategy

🧾 Description

🚀 Strategy Overview

Volatility Flow X is a dual-directional trading strategy that combines Volume-Weighted MA (VWMA) for momentum, Simple MA (SMA) for trend direction, ADX for trend strength filtering, and ATR-based volatility cloud for dynamic support/resistance zones.

It is designed specifically for high-volatility assets like BTC/USD on intraday timeframes such as 15 min, 30 min, and 1 hour — offering both breakout and trend-following opportunities.

🔬 Technical Components and Sources

1. VWMA (Volume-Weighted Moving Average)

Captures volume-weighted momentum shifts.

📚 Kirkpatrick & Dahlquist (2010) — “Technical Analysis”

2. SMA (Simple Moving Average)

Used as a baseline trend direction validator.

📚 Ernie Chan — “Algorithmic Trading” (2013)

3. ADX (Average Directional Index)

Filters out low-conviction signals based on trend strength.

📚 J. Welles Wilder (1978) — ADX in directional movement systems

4. ATR Cloud (Volatility Envelope)

Creates upper and lower dynamic bands using ATR to visualize trend pressure.

📚 Zunino et al. (2017) — Fractal volatility behavior in Bitcoin markets

🧠 Key Features

✅ 3 configurable Long signal modes

✅ 3 configurable Short signal modes

✅ Manually switchable signals for flexibility

✅ Auto-calculated TP/SL using ATR and risk/reward ratio

✅ ADX filter to avoid choppy trends

✅ Visual cloud overlay for support/resistance

✅ Suitable for scalping and short-term swing trading

⚙️ Recommended Settings (for BTC/USDT – 30min)

VWMA Length = 18

SMA Length = 50

ATR Length = 14, Multiplier = 2.5

Risk-Reward Ratio = 1.5

ADX Length = 14, Threshold = 18, Lookback = 4

⚠️ Disclaimer

This strategy is not financial advice. Please backtest and understand the risks before using it in live markets.

Shavarie's Sniper LineShavarie’s Sniper Line is a precision confirmation tool built for high-quality entries — not noisy signals.

It activates only when all 3 conditions agree:

🔁 Momentum bend detection

💧 Money Flow Index (MFI) pressure

🔺 Delta volume strength (emulated from price/volume flow)

When all conditions align, the Sniper Line shifts to:

+1 for potential buy zone

-1 for potential sell zone

0 when neutral — no action

Best used in combination with supply/demand zones, Heikin Ashi, or larger trend structures. Built for traders who value patience, precision, and massive R:R setups.