AQPRO ScalperX📝 INTRODUCTION

AQPRO ScalperX is a trading indicator designed for fast-paced, intraday trading. It uses Donchian channel breakouts, combined with a proprietary filtering system, to catch buy and sell opportunities as close to the beginning as possible without losing quality of the signals.

On top of core signals, ScalperX includes a real-time max profit tracker, a multi-timeframe (MTF) dashboard, support and resistance zones, and risk management visualization tools like automatic rendering of TP and SL lines. The indicator is fully customizable for both its visuals and functional settings.

🎯 PURPOSE OF USAGE

This indicator was initially designed with the idea of trying to make such a tool, that would be able to catch trend reversal in the most safe way. In this particular situation term 'safe way' is very abstract and it is up to interpretation, but we decided that our definition will be 'trading with price breakouts' , meaning that we would like to capitalize on price breaking its previous structure in the direction opposite to the previous one.

You can clearly see on the chart how buy and sell signals are going one after another on the screenshot below:

This ensures that we follow trend consistently and without missing out on potential profits. Just like they say: " let the winners run ".

Even though indicator with similar goals already exist in the open market, we believe that our proprietary algorithms and filters for determining price breakouts can make a big difference to traders, which employ similar strategies on daily basis, by helping them understand where are the potential high-quality breakouts might be. We haven't found indicator with exact same functionality as ours, which means that traders will be able to leverage an actually new tool to generate new price insights.

In short, main goals of this indicator are as follows:

Catching high-quality price breakouts, filtered to reduce the amount of choppy moves and false signals;

Tracking potential profits in real-time, directly on trader's chart;

Organizing data visualization of data pf latest signals from chosen asset from multiple timeframe in one dashboard;

Automated highlighting of key support and resistance zones on the chart, which serve as confirmation for main signals;

⚙️ SETTINGS OVERVIEW

Options for customization of this indicator are straightforward, but let's review them to make things certainly clear:

🔑 ScalperX / Main Settings

Range — defines the "wideness" of the breakout boxes. Higher values create wider breakout zones and impact breakout sensitivity;

Filter — adjusts the spacing between breakout boxes, determining the strictness of signal filtering. Higher values lead to more selective and rarer signals;

Show Max Profit — displays a real-time line and label that updates when a trade achieves a new peak profit, measured in ticks.

⏰ MTF Signal / Main Settings

Show MTF Signals — enables the generation of buy/sell signals from selected higher timeframes, displayed as labels on the current chart;

Timeframe — specifies the higher timeframe to use for MTF signal detection, such as 1 hour (1h) or 4 hours (4h).

🗂️ MTF Dashboard / Main Settings

Show MTF Dashboard — activates a dashboard that tracks entries, TP, SL, and overall trade bias for one selected symbol across four customizable timeframes;

* Dashboard position ( Vertical ) — adjusts whether the dashboard appears on the Top, Middle, or Bottom of the chart;

* Dashboard position ( Horizontal ) — aligns the dashboard Left, Center, or Right within the chart window;

* the name of the parameter is hidden in the settings

🗂️ MTF Dashboard / Ticker

Ticker to Track — Allows you to choose the specific ticker symbol (e.g., BINANCE:BTCUSDT) for MTF tracking.

🗂️ MTF Dashboard / Timeframes

* Timeframe 1 — set the first timeframe for multi-timeframe analysis (e.g., 15 minutes);

* Timeframe 2 — set the second timeframe for multi-timeframe analysis (e.g., 30 minutes);

* Timeframe 3 — set the third timeframe for multi-timeframe analysis (e.g., 1 hour);

* Timeframe 4 — set the fourth timeframe for multi-timeframe analysis (e.g., 4 hours).

* the name of the parameter is hidden in the settings

🛡️ Risk Management / Main Settings

Show TP&SL — displays dynamic lines and labels for the entry, Take Profit (TP), and Stop Loss (SL) of the most recent signal, updated in real-time until a new signal triggers;

Risk-to-Reward Ratio (R:R) — defines the ratio for TP and SL calculation to control your risk and reward on every trade.

📐 Support & Resistance / Main Settings

Show Support & Resistance Zones — enables dynamic zones based on pivot points, colored bullish or bearish based on price context;

History Lookback — defines the number of bars to consider when calculating support and resistance levels. Increasing this results in zones derived from longer-term price structures.

🎨 Visual Settings / ScalperX

Bullish Box — defines the color for bullish breakout boxes;

Bearish Box — defines the color for bearish breakout boxes;

Max Profit — sets the color for the max profit line on the chart.

🎨 Visual Settings / S&R

Support — defines color used for standard support zones;

Resistance — defines color used for standard resistance zones;

Strong Support — defines special color for zones classified as "strong support";

Strong Resistance — defines special color for zones classified as "strong resistance".

🎨 Visual Settings / MTF Dashboard

Bullish — sets the color for bullish trade states in the MTF dashboard;

Bearish — sets the color for bearish trade states in the MTF dashboard.

🔔 Alerts / Main Settings

Buy & Sell — toggles alerts for buy and sell signals detected by the indicator in the current chart timeframe;

MTF Buy & Sell — toggles alerts for buy and sell signals detected across the selected MTF timeframes.

📈 APPLICATION GUIDE

Application flow of this indicator very easy to understand and get used to, because all of the necessary elements — analysis, drawing, alert — are already automated by our algorithms. Let's review how the indicator works.

Let's start with the most basic thing — how will your indicator look when you load it on your chart for the first time:

AQPRO ScalperX consists mainly of 6 logic blocks:

ScalperX signals;

Risk visualization;

Max Profit tracking;

MTF scalper signals;

MTF dashboard;

Support & Resistance zones.

Description of each logic block is provided in the corresponding sections below.

SCALPERX SIGNALS

Signals, generated by our indicator, are shown on the chart as coloured up/down triangle. When a signal appears on the chart, indicator also create a box of length equal to 'Range' parameter from "Main Settings" group of settings. This box is intended to show which area of the price was broken by current candle.

It also important to acknowledge, the breakout itself happens only when price closes beyond broken price area with its close (!) price . Breakouts with highs or lows are not counted. This reduces the amount of low-quality signals and ensures that only the strong breakout will appear on the chart.

VERY IMPORTANT NOTE: all signals are considered valid only on the close of the candle, which triggered the signal, so if you want to enter a trade by any signal, wait for its candle to close and open your trade right on the next candle.

Talking about scalper's settings, we need to shed a light on how the changes in them affect signal's quality.

Parameter 'Range' defines the amount of bars, that will be review prior to current candle to determine wether the price area of this bars is good enough to track and if current candle actually broke this price area.

👍 Rule of thumb : the higher the 'Range' is, the "wider" the boxes. Also the with the increase of this parameter rises the lag of the signals, so be carefully with setting high values to this parameter.

See the visual showcase of signals with different 'Range' parameters on the screenshot below:

The example above features two instancies of ScalperX with two different 'Range' parameter values: 15 (leftchart) and 5 (right chart). You can clearly see, that on left chart here are 2 signals in comparison to 6 signals on right chart. Also signals on the left side have bigger lag and they don't catch the start of the move in comparison to how quickly tops and bottoms are catched with low 'Range' . However, low 'Range' will lead to excessive amount of signals, quality of which during 'whipsaw' markets is not that great.

✉️ Our advice on how to optimally set 'Range' parameter:

Use low values to trade during the times, when there are a lot of clean up and down impulses. This way you will catch reversal opportunities sooner and the quality of the signals will still be great;

Use high values on the 'whipsaw' markets. This will filter out many bad signals, that you would get with low-value 'Range' , and will drastically reduces amount of losing trades.

Talking about the 'Filter' parameter, this particular setting defines the 'strictness' of rules which will be applied to price area validation process. Essentially, the higher this parameter is, the stronger price impulse has to be confirm the breakout. However, changes in this parameter will not impact the "wideness" of boxes at all.

👍 Rule of thumb : the higher the 'Filter' is, the more separated the signal will be. Setting this parameter to high value will lead to increase in lag and big reduction in amount of signals, so be careful this parameter to high values.

See the visual showcase of signals with different 'Filter' parameters on the screenshot below:

The example above features two instancies of ScalperX with two different 'Filter' parameter values: 20 (left chart) and 2.5 (right chart). You can clear see, that low 'Filter' generated 6 signals, while higher one generated only 4 signals. However if you look closer, you will see that 2 signals, that existing in the yellow dashed area on the right chart, don't exist in the same area on the left chart. This is because high value of this parameter requires price impulse to be very strong in order for the indicator to mark this breakout as a valid one. What is more important is that these 2 'missing' signals were actually bad and, technically, we actually cut our losses in this case with high value of 'Filter' . You can see that the leftmost sell signal on the left chart eventually closed in a nice profit, in comparison to the same trade being closed in a loss on the right chart because of the 2 signals that we were talking about above.

It is important to note, that setting 'Filter' to low values will not affect performance this much as it low value of 'Range' do, because the indicator already works on low values of this parameter by default and the signals on average are already good enough for trading.

✉️ Our advice on how to optimally set 'Filter' parameter:

Use low values to trade on the markets with clean up and down impulses. This way you avoid excessive filtering and leave a room for good signals to come right at you;

Use high values to trade on 'whipsaw' markets. Higher values of this parameter on these markets have same effect as high 'Range' parameter: filtering false signals and leaving room for actually strong price impulses, which you will later capitalize on.

RISK VISUALIZATION (TP&SL)

Rendering Take-Profits and Stop-Losses in our indicator works quite simple: for each new trade indicator creates new pairs of lines and labels for TP and SL, while lines & labels from previous trade are erased for aesthetics purposes. Each label shows price coordinates, so that each trader would be able to grap the numbers in seconds.

See the visual showcase of TP & SL visualization on the screenshot below:

Also, whenever TP or SL of the current trade is reached, drawing of both TP and SL stops. When the TP is reached, additional '✅' emoji on the TP price is shown as confirmation of Take-Profit.

However, while TP or SL has not been reached, TP&SL labels and lines will be prolonged until one of them will be reached or new signals will come.

See the visual showcase of TP & SL stopping being visualized & TP on the screenshot below:

MAX PROFIT TRACKING

This mechanic is not particularly a new one in field of trading, but people usually forgot that it can be a useful indicator of state of the market:

when lines and labels of Max Profit are far from entry points on consistent basis , it usually means that indicator's signals actually can catch a beginning of good price moves, which enables trader to capitalize on them;

when lines and labels of Max Profit are close to entry points on consistent basis , it means that either market is choppy or the indicator can't catch trading opportunities in time. To 'fix' this you can try to reconfigure scalper's parameters, which were described above.

Principles of Max Profit in this indicator are of industry-standard: when price updates its extremum and 'generates' more profit than it previously did, Max Profit label and line change their position to this extremum. Max Profit label displays the maximum potential amount of profit that a trader could have got during this trade in pips (!) .

See the visual showcase of Max Profit work on the screenshot below:

MTF SCALPER SIGNALS

The principles of these signals are exactly the same as principles for classic Scalper signals. Refer to 'Scalper Signals' section above to rehearse the knowledge.

Logic behind these signals is very simple:

We take classic Scalper signals;

We request the data about these latest signals from specific other timeframe ( user can choose it in the settings );

If such signals appeared, we display it on the chart as a big label with timeframe value inside of it. In comparison to classic signals, no additional boxes are created . TP&SL functionality doesn't cover MTF signals, so don't expect to see TP&SL lines and labels for MTF signals.

See the visual showcase of MTF Scalper signals on the screenshot below:

MTF DASHBOARD

The functionality of the dashboard is pretty simple, but it makes the dashboard itself a very powerful tool in a hands of experienced trader.

Let's review structure of MTF dashboard on the screenshot below:

The important feature of MTF dashboard is that its tracks latest trade's data from a particular ticker and its four timeframes, all of which any trader chooses in the settings. This means, that you can be on asset ABC , but track the data from asset XYZ . This allows for a quick scan of sentiment from different assets and their timeframes, which gives traders a clue on what is the trend on these assets both on lower and higher timeframes at the same moment and saves a lot of time from jumping from one asset & timeframe to another.

To see that this is exactly the case with our indicator, see the screenshot below:

Needless to say, that you can track current asset in the dashboard as well. This will have the same benefits, described in the paragraph above.

You can also customize colours for bullish and bearish patterns for MTF Dashboard in the settings.

SUPPORT & RESISTANCE ZONES

Support & resistance (S&R) zones are a great tool for confirming Scalper signals in complex situations. Using these zones to determine whether or a particular entry opportunity is good is a practice of professional traders, which we specifically added to our indicator for the reason of improving the quality of Scalper signals in long run.

The mechanics behind these zones is based on pivot points, the lookback for which you can customize in the parameter called 'History Lookback (Bars)' in "Support & Resistance / Main Settings" group of settings. Increasing this parameter will lead to a appearance of more 'global' zones, but they will appear much rarer, rather then zones, generated with low values of this parameter.

The quality of these zones doesn't change much when changing this parameter — it only changes the frequency of the zones on the chart. Zones, generated from high values of this parameter are more suitable for long-term trading, while zones, generated from low value of this parameter, are more suitable for short-term trading.

It also important to mention that any zone on the chart is considered active only until the moment its farther border ( top border for resistance zones and bottom border for support zones) is reached by price's high or low .

Take a look on the screenshot below to see which zones does the indicator draw:

Let's review the zones themselves now:

Classic Support/Resistance Zone — a standard zone, which on average has amedium success rate to reverse the price when collided with it;

High-buyer-volume/High-seller-volume Support/Resistance Zone — a stronger zone, which on average has much better success rate to reverse the price when collided with it. Classic zone is marked as high-volume only if the up/down volume near the pivot point of this zone is greater than a certain threshold ( not changeable );

Extreme Support/Resistance Zone — a zone, which appeared beyond price's least-possible-to-cross levels, and has to the highest success rate of reversing the price on encounter across the zones, mentioned previously. Classic zone, which appeared beyond certain price levels, calculated with our proprietary risk system, is considered extreme. Classic zone doesn't need to be high-volume to become an Extreme Zone!

High-buyer-volume/High-seller-volume Extreme Support/Resistance Zone — an Extreme Zone, which has also passed up/down volume evolution process, mentioned in the point 2 .

Trading with the zones, mentioned above, with highest-on-paper success rate — especially Extreme Zones — does NOT guarantee you a price reversal when the price will reach this zone. However, by conducting our own extensive research with this indicator, we have found that using these zone will actually help you increase your success rate on average, because using these zones as confirmation systems filter out quite a number of false signals on average.

It is also important to mention, that opacity (same as 'transparency') of S&R zones depends on the volume of around zone's pivot point:

if volume is high , zone has 'brighter' (less opacity) colour;

if volume is low , zone has 'darker' (more opacity) colour.

Let's review examples of Scalper signal, which 1) where filtered out by our S&R zones and 2) where confirmed by our S&R zones. See the screenshot below:

The example above clearly shows the importance of having an S&R zone confirming the signal. This kind of 'team work' between of Scalper signals and S&R zones results in filtering lots of bad signals and confirmation of truly strong ones.

🔔 ALERTS

This indicator employs alerts for an event when new signal occurs on the current timeframe or on MTF timeframe. While creating the alert below 'Condition' field choose 'any alert() function call'.

When this alert is triggered, it will generate this kind of message:

// Alerts for current timeframe

string msg_template = "EXCHANGE:ASSET, TIMEFRAME: BUY_OR_SELL"

string msg_example = "BINANCE:BTCUSDT, 15m: Buy"

// Alerts for MTF timeframe

string msg_template_mtf = "MTF / EXCHANGE:ASSET, TIMEFRAME: BUY_OR_SELL"

string msg_example_mtf = "MTF / BINANCE:BTCUSDT, 1h: Buy"

📌 NOTES

This indicators works best on assets with high liquidity; most suitable timeframes range from 1m to 4h (depends on your trading style) ;

Seriously consider using S&R zones as confirmation to main Scalper signals or any of your own signals. Confirmation process may filter out a lot of signals, but your PNL History will say "thank you" to you in the long-run and you will see yourself how good confirmed signals actually do work;

Don't forget to look at MTF dashboard from time to time to see global sentiment. This will help you time your entry moments better and will improve your performance in the long run;

This indicator can serve both as primary source of signals and as confirmation tool, but we advise to try to combine it with your own strategy frst to see if it will improve your performance.

🏁 AFTERWORD

AQPRO ScalperX was designed to help traders identify high-quality price breakouts and generate market insights based on them, which include signal generation. Main feature of this indicator is Scalper algorithm, which generate price-breakout-based signals directly on your chart.

Alongside these signals you can leverage 1) MTF Dashboard to track latest trade's data from chosen asset and its four timeframes, 2) risk visualization functionality (TP&SL) to improve understanding of current market risks and 3) Support & Resistance zones, which serve as a great confirmation tool for Scalper signals, but can also work with any other signal generation tool to enhance its performance.

ℹ️ If you have questions about this or any other our indicator, please leave it in the comments.

Volatility

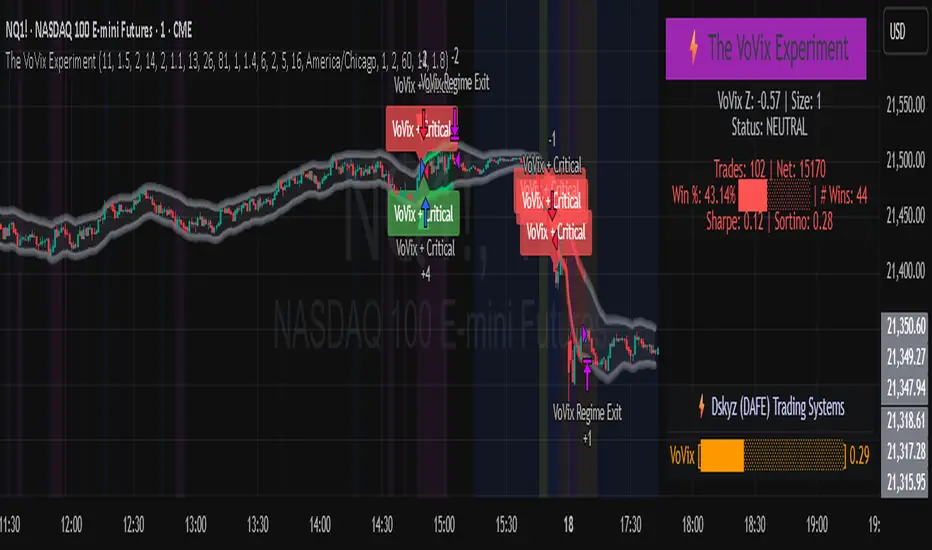

The VoVix Experiment The VoVix Experiment

The VoVix Experiment is a next-generation, regime-aware, volatility-adaptive trading strategy for futures, indices, and more. It combines a proprietary VoVix (volatility-of-volatility) anomaly detector with price structure clustering and critical point logic, only trading when multiple independent signals align. The system is designed for robustness, transparency, and real-world execution.

Logic:

VoVix Regime Engine: Detects pre-move volatility anomalies using a fast/slow ATR ratio, normalized by Z-score. Only trades when a true regime spike is detected, not just random volatility.

Cluster & Critical Point Filters: Price structure and volatility clustering must confirm the VoVix signal, reducing false positives and whipsaws.

Adaptive Sizing: Position size scales up for “super-spikes” and down for normal events, always within user-defined min/max.

Session Control: Trades only during user-defined hours and days, avoiding illiquid or high-risk periods.

Visuals: Aurora Flux Bands (From another Original of Mine (Options Flux Flow): glow and change color on signals, with a live dashboard, regime heatmap, and VoVix progression bar for instant insight.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 15 min (but works on all timeframes)

Order size: Adaptive, 1–2 contracts

Session: 5:00–15:00 America/Chicago (default, fully adjustable)

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for MNQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Forward Testing: (This is no guarantee. I've provided these results to show that executions perform as intended. Test were done on Tradovate)

ALL TRADES

Gross P/L: $12,907.50

# of Trades: 64

# of Contracts: 186

Avg. Trade Time: 1h 55min 52sec

Longest Trade Time: 55h 46min 53sec

% Profitable Trades: 59.38%

Expectancy: $201.68

Trade Fees & Comm.: $(330.95)

Total P/L: $12,576.55

Winning Trades: 59.38%

Breakeven Trades: 3.12%

Losing Trades: 37.50%

Link: www.dropbox.com

Inputs & Tooltips

VoVix Regime Execution: Enable/disable the core VoVix anomaly detector.

Volatility Clustering: Require price/volatility clusters to confirm VoVix signals.

Critical Point Detector: Require price to be at a statistically significant distance from the mean (regime break).

VoVix Fast ATR Length: Short ATR for fast volatility detection (lower = more sensitive).

VoVix Slow ATR Length: Long ATR for baseline regime (higher = more stable).

VoVix Z-Score Window: Lookback for Z-score normalization (higher = smoother, lower = more reactive).

VoVix Entry Z-Score: Minimum Z-score for a VoVix spike to trigger a trade.

VoVix Exit Z-Score: Z-score below which the regime is considered decayed (exit).

VoVix Local Max Window: Bars to check for local maximum in VoVix (higher = stricter).

VoVix Super-Spike Z-Score: Z-score for “super” regime events (scales up position size).

Min/Max Contracts: Adaptive position sizing range.

Session Start/End Hour: Only trade between these hours (exchange time).

Allow Weekend Trading: Enable/disable trading on weekends.

Session Timezone: Timezone for session filter (e.g., America/Chicago for CME).

Show Trade Labels: Show/hide entry/exit labels on chart.

Flux Glow Opacity: Opacity of Aurora Flux Bands (0–100).

Flux Band EMA Length: EMA period for band center.

Flux Band ATR Multiplier: Width of bands (higher = wider).

Compliance & Transparency

* No hidden logic, no repainting, no pyramiding.

* All signals, sizing, and exits are fully explained and visible.

* Backtest settings are stricter than most real accounts.

* All visuals are directly tied to the strategy logic.

* This is not a mashup or cosmetic overlay; every component is original and justified.

Disclaimer

Trading is risky. This script is for educational and research purposes only. Do not trade with money you cannot afford to lose. Past performance is not indicative of future results. Always test in simulation before live trading.

Proprietary Logic & Originality Statement

This script, “The VoVix Experiment,” is the result of original research and development. All core logic, algorithms, and visualizations—including the VoVix regime detection engine, adaptive execution, volatility/divergence bands, and dashboard—are proprietary and unique to this project.

1. VoVix Regime Logic

The concept of “volatility of volatility” (VoVix) is an original quant idea, not a standard indicator. The implementation here (fast/slow ATR ratio, Z-score normalization, local max logic, super-spike scaling) is custom and not found in public TradingView scripts.

2. Cluster & Critical Point Logic

Volatility clustering and “critical point” detection (using price distance from a rolling mean and standard deviation) are general quant concepts, but the way they are combined and filtered here is unique to this script. The specific logic for “clustered chop” and “critical point” is not a copy of any public indicator.

3. Adaptive Sizing

The adaptive sizing logic (scaling contracts based on regime strength) is custom and not a standard TradingView feature or public script.

4. Time Block/Session Control

The session filter is a common feature in many strategies, but the implementation here (with timezone and weekend control) is written from scratch.

5. Aurora Flux Bands (From another Original of Mine (Options Flux Flow)

The “glowing” bands are inspired by the idea of volatility bands (like Bollinger Bands or Keltner Channels), but the visual effect, color logic, and integration with regime signals are original to this script.

6. Dashboard, Watermark, and Metrics

The dashboard, real-time Sharpe/Sortino, and VoVix progression bar are all custom code, not copied from any public script.

What is “standard” or “common quant practice”?

Using ATR, EMA, and Z-score are standard quant tools, but the way they are combined, filtered, and visualized here is unique. The structure and logic of this script are original and not a mashup of public code.

This script is 100% original work. All logic, visuals, and execution are custom-coded for this project. No code or logic is directly copied from any public or private script.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Dskyz (DAFE) GENESIS Dskyz (DAFE) GENESIS: Adaptive Quant, Real Regime Power

Let’s be honest: Most published strategies on TradingView look nearly identical—copy-paste “open-source quant,” generic “adaptive” buzzwords, the same shallow explanations. I’ve even fallen into this trap with my own previously posted strategies. Not this time.

What Makes This Unique

GENESIS is not a black-box mashup or a pre-built template. It’s the culmination of DAFE’s own adaptive, multi-factor, regime-aware quant engine—built to outperform, survive, and visualize live edge in anything from NQ/MNQ to stocks and crypto.

True multi-factor core: Volume/price imbalances, trend shifts, volatility compression/expansion, and RSI all interlock for signal creation.

Adaptive regime logic: Trades only in healthy, actionable conditions—no “one-size-fits-all” signals.

Momentum normalization: Uses rolling, percentile-based fast/slow EMA differentials, ALWAYS normalized, ALWAYS relevant—no “is it working?” ambiguity.

Position sizing that adapts: Not fixed-lot, not naive—not a loophole for revenge trading.

No hidden DCA or pyramiding—what you see is what you trade.

Dashboard and visual system: Directly connected to internal logic. If it’s shown, it’s used—and nothing cosmetic is presented on your chart that isn’t quantifiable.

📊 Inputs and What They Mean (Read Carefully)

Maximum Raw Score: How many distinct factors can contribute to regime/trade confidence (default 4). If you extend the quant logic, increase this.

RSI Length / Min RSI for Shorts / Max RSI for Longs: Fine-tunes how “overbought/oversold” matters; increase the length for smoother swings, tighten floors/ceilings for more extreme signals.

⚡ Regime & Momentum Gates

Min Normed Momentum/Score (Conf): Raise to demand only the strongest trends—your filter to avoid algorithmic chop.

🕒 Volatility & Session

ATR Lookback, ATR Low/High Percentile: These control your system’s awareness of when the market is dead or ultra-volatile. All sizing and filter logic adapts in real time.

Trading Session (hours): Easy filter for when entries are allowed; default is regular trading hours—no surprise overnight fills.

📊 Sizing & Risk

Max Dollar Risk / Base-Max Contracts: All sizing is adaptive, based on live regime and volatility state—never static or “just 1 contract.” Control your max exposures and real $ risk. ATR will effect losses in high volatility times.

🔄 Exits & Scaling

Stop/Trail/Scale multipliers: You choose how dynamic/flexible risk controls and profit-taking need to be. ATR-based, so everything auto-adjusts to the current market mode.

Visuals That Actually Matter

Dashboard (Top Right): Shows only live, relevant stats: scoring, status, position size, win %, win streak, total wins—all from actual trade engine state (not “simulated”).

Watermark (Bottom Right): Momentum bar visual is always-on, regime-aware, reflecting live regime confidence and momentum normalization. If the bar is empty, you’re truly in no-momentum. If it glows lime, you’re riding the strongest possible edge.

*No cosmetics, no hidden code distractions.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Why It Wins

While others put out “AI-powered” strategies with little logic or soul, GENESIS is ruthlessly practical. It is built around what keeps traders alive:

- Context-aware signals, not just patterns

- Tight, transparent risk

- Inputs that adapt, not confuse

- Visuals that clarify, not distract

- Code that runs clean, efficient, and with minimal overfitting risk (try it on QQQ, AMD, SOL, etc. out of the box)

Disclaimer (for TradingView compliance):

Trading is risky. Futures, stocks, and crypto can result in significant losses. Do not trade with funds you cannot afford to lose. This is for educational and informational purposes only. Use in simulation/backtest mode before live trading. No past performance is indicative of future results. Always understand your risk and ownership of your trades.

This will not be my last—my goal is to keep raising the bar until DAFE is a brand or I’m forced to take this private.

Use with discipline, use with clarity, and always trade smarter.

— Dskyz , powered by DAFE Trading Systems.

REVELATIONS (VoVix - PoC) REVELATIONS (VoVix - POC): True Regime Detection Before the Move

Let’s not sugarcoat it: Most strategies on TradingView are recycled—RSI, MACD, OBV, CCI, Stochastics. They all lag. No matter how many overlays you stack, every one of these “standard” indicators fires after the move is underway. The retail crowd almost always gets in late. That’s never been enough for my team, for DAFE, or for anyone who’s traded enough to know the real edge vanishes by the time the masses react.

How is this different?

REVELATIONS (VoVix - POC) was engineered from raw principle, structured to detect pre-move regime change—before standard technicals even light up. We built, tested, and refined VoVix to answer one hard question:

What if you could see the spike before the trend?

Here’s what sets this system apart, line-by-line:

o True volatility-of-volatility mathematics: It’s not just "ATR of ATR" or noise smoothing. VoVix uses normalized, multi-timeframe v-vol spikes, instantly detecting orderbook stress and "outlier" market events—before the chart shows them as trends.

o Purist regime clustering: Every trade is enabled only during coordinated, multi-filter regime stress. No more signals in meaningless chop.

o Nonlinear entry logic: No trade is ever sent just for a “good enough” condition. Every entry fires only if every requirement is aligned—local extremes, super-spike threshold, regime index, higher timeframe, all must trigger in sync.

o Adaptive position size: Your contracts scale up with event strength. Tiny size during nominal moves, max leverage during true regime breaks—never guesswork, never static exposure.

o All exits governed by regime decay logic: Trades are closed not just on price targets but at the precise moment the market regime exhausts—the hardest part of systemic trading, now solved.

How this destroys the lag:

Standard indicators (RSI, MACD, OBV, CCI, and even most “momentum” overlays) simply tell you what already happened. VoVix triggers as price structure transitions—anyone running these generic scripts will trade behind the move while VoVix gets in as stress emerges. Real alpha comes from anticipation, not confirmation.

The visuals only show what matters:

Top right, you get a live, live quant dashboard—regime index, current position size, real-time performance (Sharpe, Sortino, win rate, and wins). Bottom right: a VoVix "engine bar" that adapts live with regime stress. Everything you see is a direct function of logic driving this edge—no cosmetics, no fake momentum.

Inputs/Signals—explained carefully for clarity:

o ATR Fast Length & ATR Slow Length:

These are the heart of VoVix’s regime sensing. Fast ATR reacts to sharp volatility; Slow ATR is stability baseline. Lower Fast = reacts to every twitch; higher Slow = requires more persistent, “real” regime shifts.

Tip: If you want more signals or faster markets, lower ATR Fast. To eliminate noise, raise ATR Slow.

o ATR StdDev Window: Smoothing for volatility-of-volatility normalization. Lower = more jumpy, higher = only the cleanest spikes trigger.

Tip: Shorten for “jumpy” assets, raise for indices/futures.

o Base Spike Threshold: Think of this as your “minimum event strength.” If the current move isn’t volatile enough (normalized), no signal.

Tip: Higher = only biggest moves matter. Lower for more signals but more potential noise.

o Super Spike Multiplier: The “are you sure?” test—entry only when the current spike is this multiple above local average.

Tip: Raise for ultra-selective/swing-trading; lower for more active style.

Regime & MultiTF:

o Regime Window (Bars):

How many bars to scan for regime cluster “events.” Short for turbo markets, long for big swings/trends only.

o Regime Event Count: Only trade when this many spikes occur within the Regime Window—filters for real stress, not isolated ticks.

Tip: Raise to only ever trade during true breakouts/crashes.

o Local Window for Extremes:

How many bars to check that a spike is a local max.

Tip: Raise to demand only true, “clearest” local regime events; lower for early triggers.

o HTF Confirm:

Higher timeframe regime confirmation (like 45m on an intraday chart). Ensures any event you act on is visible in the broader context.

Tip: Use higher timeframes for only major moves; lower for scalping or fast regimes.

Adaptive Sizing:

o Max Contracts (Adaptive): The largest size your system will ever scale to, even on extreme event.

Tip: Lower for small accounts/conservative risk; raise on big accounts or when you're willing to go big only on outlier events.

o Min Contracts (Adaptive): The “toe-in-the-water.” Smallest possible trade.

Tip: Set as low as your broker/exchange allows for safety, or higher if you want to always have meaningful skin in the game.

Trade Management:

o Stop %: Tightness of your stop-loss relative to entry. Lower for tighter/safer, higher for more breathing room at cost of greater drawdown.

o Take Profit %: How much you'll hold out for on a win. Lower = more scalps. Higher = only run with the best.

o Decay Exit Sensitivity Buffer: Regime index must dip this far below the trading threshold before you exit for “regime decay.”

Tip: 0 = exit as soon as stress fails, higher = exits only on stronger confirmation regime is over.

o Bars Decay Must Persist to Exit: How long must decay be present before system closes—set higher to avoid quick fades and whipsaws.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Tip: Set to 1 for instant regime exit; raise for extra confirmation (less whipsaw risk, exits held longer).

________________________________________

Bottom line: Tune the sensitivity, selectivity, and risk of REVELATIONS by these inputs. Raise thresholds and windows for only the best, most powerful signals (institutional style); lower for activity (scalpers, fast cryptos, signals in constant motion). Sizing is always adaptive—never static or martingale. Exits are always based on both price and regime health. Every input is there for your control, not to sell “complexity.” Use with discipline, and make it your own.

This strategy is not just a technical achievement: It’s a statement about trading smarter, not just more.

* I went back through the code to make sure no the strategy would not suffer from repainting, forward looking, or any frowned upon loopholes.

Disclaimer:

Trading is risky and carries the risk of substantial loss. Do not use funds you aren’t prepared to lose. This is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

Expect more: We’ll keep pushing the standard, keep evolving the bar until “quant” actually means something in the public code space.

Use with clarity, use with discipline, and always trade your edge.

— Dskyz , for DAFE Trading Systems

Deviation over Deviation (DoD) (DAFE) Deviation over Deviation (DoD)

Let’s call it out: The vast majority of “volatility” tools on TradingView are just new wrappers on old math—ATR, bands, and basic deviation, all chasing the same tired after-the-fact moves. They’re built to describe the aftermath, not the ignition. If you’re still relying on these, you’re trading in the rearview mirror while the real edge is already gone. That’s not our game, and it shouldn’t be yours.

Deviation over Deviation (DoD) is built for one purpose:

To expose the hidden regime shifts—the moments when volatility itself becomes volatile, when the market’s “normal” deviation is no longer normal, and when the next move is about to erupt. This isn’t just another overlay. This is a quant-grade anomaly detector, engineered to show you the probability surface before the crowd even knows it’s changed.

What sets this apart:

Deviation over Deviation (DoD):

Not just “how much did price move,” but “how unusual is the current volatility compared to its own history?” This is the Z-score of Z-scores—a true rarity detector for market stress, lull, or impending breakout.

VoVix Integration:

Select VoVix as your source and you’re not just tracking price, but the volatility of volatility—the same math that powers institutional regime models. This is the edge that front-runs the move, not follows it.

Multi-Timeframe Comparative Engine:

Instantly compare current and higher timeframe DoD Z-scores. See when the micro and macro regimes align—or when they’re about to collide.

Professional, Adaptive Dashboard:

No cosmetic fluff, always showing you the real quant state: current DoD Z, HTF DoD Z, and regime warnings. Every color, every plot, every signal is a direct function of the logic—no distractions, no lag.

How this destroys the lag:

Standard deviation, ATR, and “volatility bands” are always late. They tell you what just happened. DoD and VoVix show you when the nature of volatility itself is changing—when the market is about to leave the old regime behind. This is the difference between trading the past and trading the future.

Inputs/Signals—explained for clarity:

Deviation Lookback & DoD Lookback:

Control the sensitivity and selectivity of the regime detector. Shorter = more signals, longer = only the rarest events.

Source Selection:

Choose from price, volume, volatility, or VoVix. Each source gives you a different lens on market stress. VoVix is for those who want to see the “regime quake” before the aftershocks.

HTF (Comparative Timeframe):

Set your higher timeframe for macro regime confirmation. When both DoD Z-scores align, you’re seeing a true market inflection.

VoVix Parameters:

Fine-tune the volatility-of-volatility engine for your market. Lower ATR Fast = more responsive; higher ATR Slow = more selective. Adjust for your asset, your timeframe, your edge.

Bottom line:

This isn’t just another “volatility” script. This is a regime anomaly detector, built for traders who want to anticipate, not react. Every input is there for a reason. Every plot is a direct readout of the quant logic. Use it to filter your entries, to time your exits, or to simply see the market’s hidden structure in real time.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*Updated the Dashboard/Metrics Display for better visibility

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

(DAFE) DEVMA - Crossover (Deviation Moving Average) (DAFE) DEVMA - Crossover (Deviation Moving Average)

Let’s keep pushing the edge. After the breakthrough of Deviation over Deviation (DoD)—which gave traders a true lens into volatility’s hidden regime shifts—many asked: “What’s next?” The answer is DEVMA: a crossover engine built not on price, but on the heartbeat of the market itself.

Why is this different?

DEVMA isn’t just a moving average crossover. It’s a regime detector that tracks the expansion and contraction of deviation—giving you a real-time readout of when the market’s energy is about to shift. This is the next step for anyone who wants to anticipate volatility, not just react to it.

What sets DEVMA apart:

Volatility-First Logic:Both fast and slow lines are moving averages of deviation, not price. You’re tracking the market’s “energy,” not just its direction. This is the quant edge that most scripts miss.

Regime-Colored Lines:

The fast and slow DEVMA lines change color in real time—green/aqua for expansion, maroon/orange for contraction—so you can see regime shifts at a glance.

Quant-Pro Visuals:

Subtle glow, clean cross markers, and a minimalist dashboard keep your focus on what matters: the regime, not the noise.

Static Regime Thresholds:

Reference lines at 1.5 and 0.5 (custom colors) give you instant context for “normal” vs. “extreme” volatility states.

No Price Chasing:

This isn’t about following price. It’s about anticipating the next volatility regime—before the crowd even knows what’s coming.

How this builds on DoD:

DoD showed you when volatility itself was about to change. DEVMA takes that insight and turns it into a crossover engine—so you can see, filter, and act on regime shifts in real time. If DoD was the radar, DEVMA is the navigation system.

Inputs/Signals—explained for clarity:

Deviation Lookback:

Controls the sensitivity of the regime detector. Shorter = more signals, longer = only the rarest events.

Fast/Slow DEVMA Lengths:

Fine-tune how quickly the regime lines react. Fast for scalping, slow for swing trading.

Source Selection:

Choose from price, volume, volatility, or VoVix. Each source gives you a different lens on market stress. VoVix is for those who want to see the “regime quake” before the aftershocks.

VoVix Parameters:

Fine-tune the volatility-of-volatility engine for your market. Lower ATR Fast = more responsive; higher ATR Slow = more selective.

Bottom line:

DEVMA is for those who want to see the market’s heartbeat, not just its shadow. Use it to filter your trades, time your entries, or simply understand the market’s true rhythm. Every input is there for a reason. Every plot is a direct readout of the quant logic. Use with discipline, and make it your own.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*Updated the Dashboard/Metrics Display for better visibility

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Harmony in Havoc - The Entropy of VoVix Harmony in Havoc – The Entropy of VoVix

There are moments in the market when chaos and order are not opposites, but partners in a dance.

Harmony in Havoc is not just an indicator—it’s a window into that dance.

Most tools try to tame the market by smoothing it, boxing it in, or chasing after what’s already happened. This script does the opposite: it listens for the music beneath the noise, the rare moments when volatility and unpredictability align, and the market’s next movement is about to begin.

What is Harmony in Havoc?

VoVix Spike:

The pulse of volatility-of-volatility. Not just how much the market is moving, but how violently its own heartbeat is changing.

Entropy:

A real-time measure of surprise. When entropy is high, the market is not just moving—it’s breaking its own patterns, rewriting its own rules.

Progression Bar & Status:

The yellow bar is your visual gauge of tension. As it fills, the market is winding up.

Wait: The world is calm.

Get ready!: The storm is building.

Take Action!!: The probability of a regime eruption is at its peak.

Yellow Background:

When the background glows, the market is at its most unstable—this is not a buy or sell signal, but a quant alert.

How does it work?

Every tick, Harmony in Havoc measures the distance between the market’s current volatility and its own unpredictability. When the VoVix spike approaches or exceeds the entropy threshold, the system knows:

“This is the moment when the improbable becomes possible.”

Why is this different?

It doesn’t tell you what to do.

It doesn’t chase price.

It doesn’t care about trends, bands, or the past.

Instead, it gives you a quantitative sense of anticipation—a way to see when the market is most likely to break from its own history, and when the edge is at its sharpest.

How to use it:

Watch for the yellow background and “Take Action!!” status.

Use it as a regime filter, a volatility dashboard, or a warning system for your own strategies.

Tune the inputs for your asset and timeframe—make it your own.

Inputs—explained for you:

VoVix Fast/Slow ATR & Stdev:

Control how sensitive the system is to volatility shocks. Lower = more signals, higher = only the rarest events.

Entropy Window & Bins:

Control how “surprised” the entropy engine is by current volatility. Shorter window = more responsive, more bins = finer detail.

Show/Hide Controls:

Toggle the VoVix spike, entropy line, and their glows to customize your visual experience.

Bottom line:

This is not a buy or sell script.

This is a quant regime detector for those who want to feel the market’s tension—to sense when harmony and havoc are about to collide.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*I've only tested this on 1 and 5 min frames.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

3 days ago

Release Notes

* Now mobile friendly. I've added a toggle to switch the dashboard on/off, and added a mobile information line that shows the same information on the dashboard. This is to allow the script to stay visually in balance and this also has a toggle.

* Background color added that coresponds with Buy or Sell areas.

Big Money TrackerOI-Anchored VWAP: Big Money Position Tracker

Understanding VWAP in Big Money Trading

Volume Weighted Average Price (VWAP) is the benchmark most widely used by institutions to assess their execution quality and market timing. It represents the average price a security has traded at throughout the day, weighted by volume.

Why Institutions Care About VWAP:

Portfolio managers often mandate trades to be executed at or better than VWAP

Large orders are broken down and executed around VWAP to minimize market impact

Trading desks use VWAP as a neutral price to assess if they're buying too high or selling too low

Algorithmic trading systems use VWAP as a key reference for order execution

The OI-VWAP Edge

This indicator takes Big Money VWAP trading to the next level by anchoring VWAP calculations to significant Open Interest (OI) changes. This helps identify not just where institutions are trading, but where they're establishing significant positions in the crypto markets.

Key Features:

Dynamic OI-based VWAP anchoring that identifies where large positions are established

Previous VWAP level tracking to monitor historical Big Money interest points

Smart sweep detection system for both current and previous VWAP levels

Standard deviation bands for volatility context

What Makes This Indicator Unique:

Uses aggregated Open Interest data from major exchanges (Binance, BitMEX, Bybit, Kraken)

Automatically detects significant OI increases to anchor VWAP levels

Tracks both current and previous Big Money reference prices

Identifies potential stop runs and liquidity sweeps

Trading Applications:

The indicator helps identify where large positions are established and how they might influence price action:

Defense Zones: When price approaches a VWAP level with high OI, institutions often defend their positions

Liquidation Levels: Previous VWAP levels can become liquidation targets for trapped positions

Stop Runs: Sweep detection helps identify when large players might be hunting stops or creating liquidity

Mean Reversion: SD bands help identify potential reversal zones around Big Money average prices

Best Practices:

Look for price reaction at current VWAP when OI is increasing

Monitor sweeps of previous VWAP levels for potential reversals

Use SD bands to gauge volatility expansion/contraction around Big Money positions

Pay attention to failed sweeps as they often indicate strong position defense

Trading Scenarios:

// Bullish Position Defense:

// 1. High OI increase creates new VWAP (Big Money entry)

// 2. Price tests VWAP from above (retest of entry)

// 3. Failed bearish sweeps = shorts trapped

// 4. Strong defense + trapped shorts = potential squeeze

// Bearish Liquidation:

// 1. Previous VWAP level above current price

// 2. High OI trapped at higher prices

// 3. Price sweeps above then fails = more trapped longs

// 4. Break below = potential cascading liquidations

G-Bot v3Overview:

G-Bot is an invite-only Pine Script tailored for traders seeking a precise, automated breakout strategy. This closed-source script integrates with 3Commas via API to execute trades seamlessly, combining classic indicators with proprietary logic to identify high-probability breakouts. G-Bot stands out by filtering market noise through a unique confluence of signals, offering adaptive risk management, and employing advanced alert deduplication to ensure reliable automation. Its purpose-built design delivers actionable signals for traders prioritizing consistency and efficiency in trending markets.

What It Does and How It Works:

G-Bot generates trade signals by evaluating four key market dimensions—trend, price action, momentum, and volume—on each 60-minute bar. The script’s core components and their roles are:

Trend Detection (EMAs): Confirms trend direction by checking if the 5-period EMA is above (bullish) or below (bearish) the 6-period EMA, with the price positioned accordingly (above the 5-period EMA for longs, below for shorts). The tight EMA pairing is optimized for the 60-minute timeframe to capture sustained trends while minimizing lag.

Price Action Trigger (Swing Highs/Lows): Identifies breakouts when the price crosses above the previous swing high (for longs) or below the previous swing low (for shorts), using a period lookback to focus on recent price pivots. This ensures entries align with significant market moves.

Momentum Filter (RSI): Validates breakouts by requiring RSI to fall within moderated ranges. These ranges avoid overbought/oversold extremes, prioritizing entries with balanced momentum to enhance trade reliability.

Volume Confirmation (3-period SMA): Requires volume to exceed its 3-period SMA, confirming that breakouts are driven by strong market participation, reducing the risk of false moves.

Risk Management (14-period ATR): Calculates stop-loss distances (ATR) and trailing stops (ATR and ATR-point offset) to align trades with current volatility, protecting capital and locking in profits.

These components work together to create a disciplined system: the EMAs establish trend context, swing breaks confirm price momentum, RSI filters for optimal entry timing, and volume ensures market conviction. This confluence minimizes false signals, a critical advantage for hourly breakout trading.

Why It’s Original and Valuable:

G-Bot’s value lies in its meticulous integration of standard indicators into a non-standard, automation-focused system. Its unique features include:

Curated Signal Confluence: Unlike generic breakout scripts that rely on single-indicator triggers (e.g., EMA crossovers), G-Bot requires simultaneous alignment of trend, price action, momentum, and volume. This multi-layered approach, reduces noise and prioritizes high-conviction setups, addressing a common flaw in simpler strategies.

Proprietary Alert Deduplication: G-Bot employs a custom mechanism to prevent redundant alerts, using a 1-second minimum gap and bar-index tracking. This ensures signals are actionable and compatible with 3Commas’ high-frequency automation, a feature not found in typical Pine Scripts.

Adaptive Position Sizing: The script calculates trade sizes based on user inputs (1-5% equity risk, max USD cap, equity threshold) and ATR-derived stop distances, ensuring positions reflect both account size and market conditions. This dynamic approach enhances risk control beyond static sizing methods.

3Commas API Optimization: G-Bot generates JSON-formatted alerts with precise position sizing and exit instructions, enabling seamless integration with 3Commas bots. This level of automation, paired with detailed Telegram alerts for monitoring, streamlines the trading process.

Visual Clarity: On-chart visuals—green triangles for long entries, red triangles for shorts, orange/teal lines for swing levels, yellow circles for price crosses—provide immediate insight into signal triggers, allowing traders to validate setups without accessing the code.

G-Bot is not a repackaging of public code but a specialized tool that transforms familiar indicators into a robust, automated breakout system. Its originality lies in the synergy of its components, proprietary alert handling, and trader-centric automation, justifying its invite-only status.

How to Use:

Setup: Apply G-Bot to BITGET’s BTCUSDT.P chart on a 60-minute timeframe.

3Commas Configuration: Enter your 3Commas API Secret Key and Bot UUID in the script’s input settings to enable webhook integration.

Risk Parameters: Adjust Risk % (1-5%), Max Risk ($), and Equity Threshold ($) to align position sizing with your account and risk tolerance.

Webhook Setup: Configure 3Commas to receive JSON alerts for automated trade execution. Optionally, connect Telegram for detailed signal notifications.

Monitoring: Use on-chart visuals to track signals:

Green triangles (below bars) mark long entries; red triangles (above bars) mark shorts.

Orange lines show swing highs; teal lines show swing lows.

Yellow circles indicate price crosses; purple crosses highlight volume confirmation.

Testing: Backtest G-Bot in a demo environment to validate performance and ensure compatibility with your trading strategy.

Setup Notes : G-Bot is a single, self-contained script for BTCUSDT.P on 60-minute charts, with all features accessible via user inputs. No additional scripts or passwords are required, ensuring compliance with TradingView’s single-publication rule.

Disclaimer: Trading involves significant risks, and past performance is not indicative of future results. Thoroughly test G-Bot in a demo environment before deploying it in live markets.

Full setup support will be provided

SuperTrend: Silent Shadow 🕶️ SuperTrend: Silent Shadow — Operate in trend. Vanish in noise.

Overview

SuperTrend: Silent Shadow is an enhanced trend-following system designed for traders who demand clarity in volatile markets and silence during indecision.

It combines classic Supertrend logic with a proprietary ShadowTrail engine and an adaptive Silence Protocol to filter noise and highlight only the cleanest signals.

Key Features

✅ Core Supertrend Logic

Built on Average True Range (ATR), this trend engine identifies directional bias with visual clarity. Lines adjust dynamically with price action and flip when meaningful reversals occur.

✅ ShadowTrail: Stepped Counter-Barrier

ShadowTrail doesn’t predict reversals — it reinforces structure.

When price is trending, ShadowTrail forms a stepped ceiling in downtrends and a stepped floor in uptrends. This visual containment zone helps define the edges of price behavior and offers a clear visual anchor for stop-loss placement and trade containment.

✅ Silence Protocol: Adaptive Noise Filtering

During low-volatility zones, the system enters “stealth mode”:

• Trend lines turn white to indicate reduced signal quality

• Fill disappears to reduce distraction

This helps avoid choppy entries and keeps your focus sharp when the market isn’t.

✅ Visual Support & Stop-Loss Utility

When trendlines flatten or pause, they naturally highlight price memory zones. These flat sections often align with:

• Logical stop-loss levels

• Prior support/resistance areas

• Zones of reduced volatility where price recharges or rejects

✅ Custom Styling

Full control over line colors, width, transparency, fill visibility, and silence behavior. Tailor it to your strategy and visual preferences.

How to Use

• Use Supertrend color to determine bias — flips mark momentum shifts

• ShadowTrail mirrors the primary trend as a structural ceiling/floor

• Use flat segments of both lines to identify consolidation zones or place stops

• White lines = low-quality signal → stand by

• Combine with RSI, volume, divergence, or your favorite tools for confirmation

Recommended For:

• Traders seeking clearer trend signals

• Avoiding false entries in sideways or silent markets

• Identifying key support/resistance visually

• Structuring stops around real market containment levels

• Scalping, swing, or position trading with adaptive clarity

Built by Sherlock Macgyver

Forged for precision. Designed for silence.

When the market speaks, you listen.

When it doesn’t — you wait in the shadows.

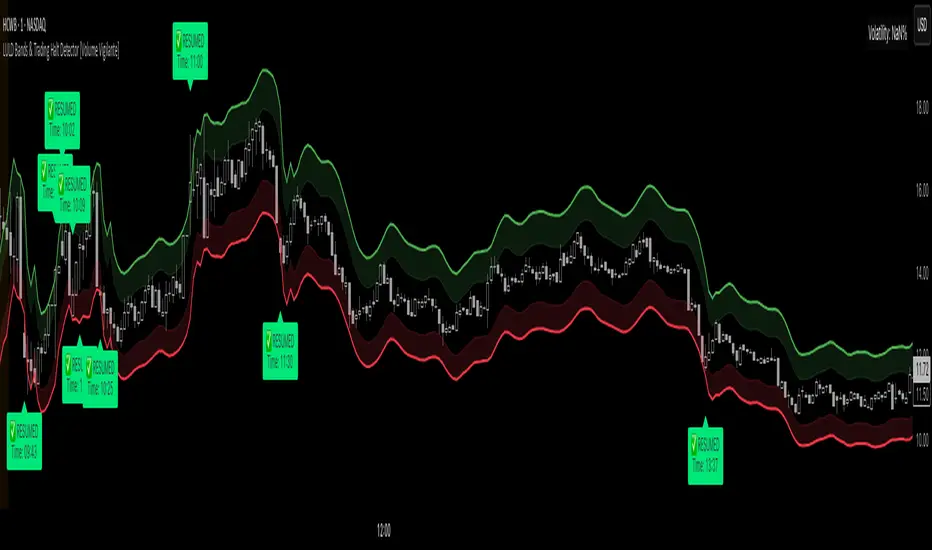

LULD Bands & Trading Halt Detector [Volume Vigilante]📖 LULD Bands & Trading Halt Detector

This advanced tool visualizes official Limit Up / Limit Down (LULD) price bands and detects regulatory trading halts and resumptions based on SEC and NASDAQ rules. It is engineered for high accuracy by anchoring all calculations to the 1-minute timeframe, ensuring reliable signals across any chart resolution.

📌 What Does This Script Do?

- Draws real-time LULD price band estimations and optional buffer (caution) zones directly on the chart.

- Detects trading halt resumptions by monitoring time gaps between candles and other regulatory criteria. (Note: Due to Pine Script limitations, halts cannot be detected in real-time, only resumptions after they occur.)

- Triggers real-time alerts for:

- Trading Resumptions (Limit Up & Limit Down)

- LULD Zone Entries (Caution Zone)

- Band Breaches (Limit Up and Limit Down)

- Plots historical halt resumption markers to analyse past events.

📐 How It Works:

- Implements official SEC/NASDAQ LULD rules for Tier 1 and Tier 2 securities.

- Applies special band adjustments for the final 25 minutes of trading (after 3:35 PM ET).

- Anchors all logic to the 1-minute timeframe for precise calculations, even on higher timeframe charts.

- Includes adjustable volume and volatility filters to eliminate false signals (ghost halts) on low-- liquidity assets, especially Tier 2 securities when TradingView fails to print candles.

⚙️ How to Use It:

1.) Apply the script to any asset or timeframe.

2.) Adjust Volume and Volatility Filters to reduce noise. (Recommended: 500,000+ volume, 10%+ volatility.)

3.) Enable or disable visual components like bands, buffer zones, and halt resumption labels.

4.) Configure alerts directly from the script settings panel.

5.) Apply alerts to individual assets via "Add Alert On..." or to entire watchlists using "Add Alert on the List."

🧩 What Makes This Script Unique?

- True 1-Minute Anchored Calculations: Ensures alerts and visuals match official trading halt criteria regardless of chart timeframe.

- Customisable Buffered Zones: Visualise proximity to regulatory price limits and avoid volatility traps.

- Combines halt resumption detection, limit up/down band visualisation, and real-time alerts into one clean, modular tool.

📚 Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Use at your own discretion and consult a licensed financial advisor before making trading decisions based on it.

Official Resources:

- NASDAQ LULD Regulations (FAQ):

www.nasdaqtrader.com

Current Nasdaq Trading Halts:

www.nasdaqtrader.com

ATR ComboA Collection of three ATRs.

The whole idea of this indicator is to easily visualise the relationship of volatility to the current price action.

The default settings are:

5 Moving Average (Pink)

50 Moving Average (Blue)

1000 Moving Average (Yellow)

Using the default settings, the Yellow line represents the larger-scale volatility average.

the Blue line represents more recent volatility and the Pink lien represents the very recent average.

Using this indicator is possible in a number of ways:

If volatility is high and directional, you will see a sharp increase in the Pink line.

If volatility is high and choppy, the Pink line will be well above the Blue line and will oscillate up and down.

If volatility is starting to cool down, the Pink line will approach the Blue and Yellow lines.

Disparity Index with Volatility ZonesDisparity Index with Volatility Zones

is a momentum oscillator that measures the percentage difference between the current price and its simple moving average (SMA). This allows traders to identify overbought/oversold conditions, assess momentum strength, and detect potential trend reversals or continuations.

🔍 Core Concept:

The Disparity Index (DI) is calculated as:

DI = 100 × (Price − SMA) / SMA

A positive DI indicates the price is trading above its moving average (potential bullish sentiment), while a negative DI suggests the price is below the average (potential bearish sentiment).

This version of the Disparity Index introduces a dual-zone volatility framework, offering deeper insight into the market's current state.

🧠 What Makes This Version Unique?

1. High Volatility Zones

When DI crosses above +1.0% or below –1.0%, it often indicates the start or continuation of a strong trend.

Sustained readings beyond these thresholds typically align with trending phases, offering opportunities for momentum-based entries.

A reversal back within ±1.0% after exceeding these levels can suggest a shift in momentum — similar to how RSI exits the overbought/oversold zones before reversals.

These thresholds act as dynamic markers for breakout confirmation and potential trend exhaustion.

2. Low Volatility Zones

DI values between –0.5% and +0.5% define the low-volatility zone, shaded for visual clarity.

This area typically indicates market indecision, sideways price action, or consolidation.

Trading within this range may favor range-bound or mean-reversion strategies, as trend momentum is likely limited.

The logic is similar to interpreting a flat ADX, tight Bollinger Bands, or contracting Keltner Channels — all suggesting consolidation.

⚙️ Features:

Customizable moving average length and input source

Adjustable thresholds for overbought/oversold and low-volatility zones

Optional visual fill between low-volatility bounds

Clean and minimal chart footprint (non-essential plots hidden by default)

📈 How to Use:

1. Trend Confirmation:

A break above +1.0% can be used as a bullish continuation signal.

A break below –1.0% may confirm bearish strength.

Long periods above/below these thresholds support trend-following entries.

2. Reversal Detection:

If DI returns below +1.0% after exceeding it, bullish momentum may be fading.

If DI rises above –1.0% after falling below, bearish pressure may be weakening.

These shifts resemble overbought/oversold transitions in oscillators like RSI or Stochastic, and can be paired with divergence, volume, or price structure analysis for higher reliability.

3. Sideways Market Detection:

DI values within ±0.5% indicate low volatility or a non-trending environment.

Traders may avoid breakout entries during these periods or apply range-trading tactics instead.

Observing transitions out of the low-volatility zone can help anticipate breakouts.

4. Combine with Other Indicators:

DI signals can be enhanced using tools like MACD, Volume Oscillators, or Moving Averages.

For example, a DI breakout beyond ±1.0% supported by a MACD crossover or volume spike can help validate trend initiation.

This indicator is especially powerful when paired with Bollinger Bands:

A simultaneous price breakout from the Bollinger Band and DI moving beyond ±1.0% can help identify early trend inflection points.

This combination supports entering positions early in a developing trend, improving the efficiency of trend-following strategies and enhancing decision-making precision.

It also helps filter false breakouts when DI fails to confirm the move outside the band.

This indicator is designed for educational and analytical purposes and works across all timeframes and asset classes.

It is particularly useful for traders seeking a clear framework to identify momentum strength, filter sideways markets, and improve entry timing within a larger trading system.

Volume candle intraday 90% valid - with alertThe candle with the highest volume of the day and that creates a new daily high or low.

- Only usable on M15 timeframes;

- You can set a range of bars (from the beginning of the day) to ignore;

- "90% valid" means a candle with volume greater than 90% of the last candle with the highest volume of the day (in the script you can change the percentage of valid volumes to define the candle volume, replacing all the "90" with the desired percentage);

- Long volumes are compared to longs and short volumes are compared to shorts;

- Script created with ChatGpt;

The psychology behind this pattern is the following: on the daily high/low, a lot of volumes will enter in a short time, either by absorption: buyers or sellers enter en masse following the trend when it is too late; or by exhaustion: buyers or sellers who entered en masse and late have no more strength to continue pushing the price, they cause a volume peak to buy/sell as much as they could, then their enemies take over forming a high/low).

Happy trading everyone! :)

###################################################################################

La candela con il volume più alto della giornata e che crea un nuovo massimo o minimo giornaliero.

- Utilizzabile solo su timeframe M15;

- Si può impostare un range di barre(da inizio giornata) da ignorare;

- "90% valida" sta per candela con volume superiore del 90% dell'ultima candela con volume più alto della giornata(nello script si può cambiare percentuale di volumi validi per definire candela volume, sostituendo tutti i "90" con la percentuale desiderata);

- I volumi long vengono confrontati con i long e i volumi short con gli short;

- Script creato con ChatGpt;

La psicologia dietro questo pattern è la seguente: sul massimo/minimo giornaliero entreranno tanti volumi in breve tempo, sia per assorbimento: buyers o sellers entrano in massa seguendo il trend quando è troppo tardi; sia per esaurimento: buyers o sellers entrati in massa e in ritardo non hanno più forza per continuare a spingere il prezzo, causano un picco volumetrico per comprare/vendere più che potevano, quindi i loro nemici prendono il sopravvento formando un massimo/minimo).

Buon trading a tutti! :)

VOID Directional Spike MarkerThis indicator highlights significant directional moves on the $VOID chart (NYSE USI:UVOL − DERIBIT:DVOL ) using simple visual cues:

🔼 Green up arrows when the candle closes significantly higher than it opens

🔽 Red down arrows when the candle closes significantly lower than it opens

Threshold is fully customizable (default: 15,000,000)

Ideal for spotting explosive internal shifts on the 5-minute chart during key market moments

Alerts included for both up and down spikes

Use this to track aggressive buying or selling pressure across NYSE internals and time your entries on NQ, ES, or YM with stronger conviction.

Zen FDAX Session📝 Description

OVERVIEW

The Zen FDAX Session indicator highlights periods outside the regular trading hours of the FDAX (DAX Futures) on the Xetra exchange. It shades the chart background during non-trading hours, aiding traders in distinguishing active market periods from inactive ones.

FUNCTIONALITY

Customizable Trading Hours: Users can define the session's start and end times in UTC, allowing flexibility to match personal trading schedules or account for daylight saving changes.

Visual Clarity: The indicator applies a subtle background color to non-trading hours, ensuring clear demarcation without obscuring price data.

Time Zone Awareness: Designed with UTC inputs to maintain consistency across different user time zones.

USAGE

Add the Indicator: Apply the "Zen FDAX Session" indicator to your chart.

Set Trading Hours: Input your desired session start and end times in UTC.

Interpret the Shading: Areas with shaded backgrounds represent times outside your defined trading session.

Note: This indicator does not generate buy/sell signals but serves as a visual aid to identify trading sessions.

Bollinger Bands x3 with Fill + HMA + Dynamic Width Colors📄 Description for TradingView Publication:

This is an enhanced and flexible version of the classic Bollinger Bands indicator, designed for traders who want deeper insight into market volatility and price structure.

🔹 Key Features:

✅ Triple Bollinger Bands

Displays 3 standard deviation bands: ±1σ, ±2σ, and ±3σ

Customize each deviation level independently

✅ Dynamic Band Width Coloring

Band lines change color when the distance between upper and lower bands narrows

Helps identify volatility contractions and potential squeeze setups

✅ Dynamic Fill Coloring

Fill between bands also changes color when the bands narrow

Visually highlights transitions from high to low volatility conditions

✅ Multiple Moving Average Options

Choose from:

Simple Moving Average (SMA)

Exponential Moving Average (EMA)

Smoothed Moving Average (SMMA / RMA)

Weighted Moving Average (WMA)

Volume-Weighted Moving Average (VWMA)

Hull Moving Average (HMA) for a smoother, more responsive central tendency

✅ Customization Options

Show/hide each band individually

Adjust standard deviation multipliers

Toggle fills between bands

Customize fill colors for normal and narrowing conditions

Offset option to shift all plots forward or backward

💡 Use Case Tips:

When all bands begin narrowing, it could signal an upcoming volatility expansion or breakout.

Use the ±3σ bands to gauge extreme price behavior, and ±1σ for short-term mean reversion.

Combine with price action, momentum, or volume for breakout confirmation.

🧰 Recommended For:

Volatility traders

Mean reversion strategies

Breakout traders

Trend confirmation and structure analysis

Enhanced Volume Trend Indicator with BB SqueezeEnhanced Volume Trend Indicator with BB Squeeze: Comprehensive Explanation

The visualization system allows traders to quickly scan multiple securities to identify high-probability setups without detailed analysis of each chart. The progression from squeeze to breakout, supported by volume trend confirmation, offers a systematic approach to identifying trading opportunities.

The script combines multiple technical analysis approaches into a comprehensive dashboard that helps traders make informed decisions by identifying high-probability setups while filtering out noise through its sophisticated confirmation requirements. It combines multiple technical analysis approaches into an integrated visual system that helps traders identify potential trading opportunities while filtering out false signals.

Core Features

1. Volume Analysis Dashboard

The indicator displays various volume-related metrics in customizable tables:

AVOL (After Hours + Pre-Market Volume): Shows extended hours volume as a percentage of the 21-day average volume with color coding for buying/selling pressure. Green indicates buying pressure and red indicates selling pressure.

Volume Metrics: Includes regular volume (VOL), dollar volume ($VOL), relative volume compared to 21-day average (RVOL), and relative volume compared to 90-day average (RVOL90D).

Pre-Market Data: Optional display of pre-market volume (PVOL), pre-market dollar volume (P$VOL), pre-market relative volume (PRVOL), and pre-market price change percentage (PCHG%).

2. Enhanced Volume Trend (VTR) Analysis

The Volume Trend indicator uses adaptive analysis to evaluate buying and selling pressure, combining multiple factors: