Sentival | QuantEdgeBIntroducing Sentival by QuantEdgeB.

An Adaptive Multi-Factor Indicator for Market Valuation & Trend Strength

____

Overview

The Sentival Valuation System is a medium-term, multi-factor valuation tool designed to assess market conditions using a combination of momentum, mean reversion, and risk-adjusted metrics. It provides traders and investors with a dynamic score reflecting market valuation, ranging from strongly oversold to strongly overbought conditions.

This system leverages a diverse range of technical indicators, including momentum oscillators, volatility measures, risk ratios, and mean-reversion metrics, providing a holistic view of market conditions.

____

1. Key Features

🛠 Multi-Factor Valuation Model

Sentival aggregates nine different indicators, normalizing and rescaling them into a standardized z-score-based valuation system. The final output represents an average of the selected indicators, allowing for flexible customization based on the user’s preference.

📊 Customizable Indicator Selection

Users can enable or disable any of the nine valuation factors, ensuring the system adapts to different market environments, trading styles, and assets.

🔄 Multi-Timeframe Adaptability

Sentival can be used across different time horizons, making it suitable for short-term mean reversion, medium-term traders, or long-term valuation analysis by simply adjusting the timeframe and indicator settings. This flexibility allows traders to adapt Sentival to various market conditions and trading objectives.

🎨 Intuitive Dashboard & Color Coding

- Dynamic Heatmap & Dashboard: Displays valuation strength across multiple factors.

- Gradient-Based Overbought/Oversold Signals: Clear color-coded signals for easy interpretation.

- Background Highlighting: Optional oversold/overbought background zones.

🏆 Statistical & Risk-Based Insights

- Standardized Rescaling & Z-Score Analysis to prevent bias from individual indicators.

- Risk-Adjusted Metrics such as Sharpe, Sortino, and Omega Ratios help assess the overall market risk appetite.

- Trend Following Mode (TF Display): Users can enable the "Trend Following" option to display the trend direction, helping to align valuation signals with the broader market trend.

____

2. How It Works

Sentival is a multi-factor trend and momentum analysis system, designed to track market cycle shifts using a combination of volatility, momentum, risk assessment, and valuation mechanisms. Instead of focusing on one dimension of the market, Sentival integrates multiple methodologies to cross-validate signals and reduce noise. Each indicator in Sentival plays a specific role, ensuring confirmation across different market conditions.

How Each Component Works Together

1️⃣ Chande Momentum Oscillator (CMO)

• A momentum-based measure that determines whether price action is dominated by upward or downward forces.

• Works well in combination with volatility measures to confirm whether a move is sustainable.

2️⃣ Disparity Index

• Measures the distance between price and its moving average, acting as an overextension filter.

• Ensures that trend-following signals are not driven by short-term spikes but sustained trends.

3️⃣ Bollinger Bands % (BB%)

• A volatility measure that indicates how far price is from the statistical mean.

• Helps identify trend exhaustion points where price moves become unstable.

4️⃣ Relative Strength Index (RSI)

• A trend confirmation layer, ensuring that momentum strength aligns with price movement.

• Adds an additional check to prevent false breakouts.

5️⃣ Rate of Change (RoC)

• Captures the speed of price movement, ensuring that the market has enough momentum for trend continuation.

• Works well with risk indicators to filter weaker moves.

6️⃣ Price Z-Score

• A statistical tool to measure how far price is from its long-term equilibrium.

• Helps prevent entering overstretched trends too late.

7️⃣ Risk Ratios (Sharpe, Sortino, Omega)

• This is the risk-adjusted performance component, ensuring that trends have a healthy risk-reward balance.

• Helps determine when a trend has structurally strong backing rather than speculative movement.

8️⃣ Hurst Cycle Analysis

• Measures the persistence of trends by analyzing price fractals.

• Ensures that the market regime is either trending or mean-reverting, improving trade confidence.

9️⃣ Commodity Channel Index (CCI)

• Helps identify strong trend conditions, adding another layer of momentum confirmation.

• Works well with other oscillators to prevent misreading counter-trends.

🔗 Why These Components Work Well Together

• Momentum + Volatility + Risk → Instead of relying on a single category, Sentival merges multiple dimensions of market behavior into a cohesive signal.

• Filters Out False Signals → Combining momentum oscillators, volatility measures, and risk-adjusted metrics ensures high-confidence entries.

• Adaptability Across Market Regimes → Whether the market is trending, consolidating, or volatile, the system adjusts dynamically.

• Cross-Validation for Trend Strength → If multiple components align, it increases certainty that a trend is real and sustainable.

____

3. Sentival Scanner - table breakdown

The dashboard-style table generated is designed to give traders a holistic market view at a glance. It processes a variety of technical signals and distills them into readable labels, visual strength bars, and actionable trend states. Here's a breakdown of what each section means:

1. Direction

This section analyzes whether the average Z-score (a composite of several indicators) is increasing, decreasing, or neutral over time. It does this using a smoothed trend of the Z-score, comparing recent values to older ones.

2. Momentum

Momentum is derived from the rate of change (RoC) of the average Z-score. It evaluates how strong the current move is. If momentum is above a certain positive threshold, it’s considered positive, if below a negative threshold, it’s negative, otherwise it’s neutral.

3. Impulse

Impulse reflects the velocity of momentum — in other words, is the market speeding up or slowing down? High positive values suggest strong acceleration (strong impulse), while negative values show deceleration or stalling.

4. Drive

This metric combines momentum and velocity to create a descriptive phrase that captures the market’s behavior. For example:

• “Strong Upside” means strong momentum with acceleration.

• “Fading Downside” means bearish momentum losing steam.

• “Neutral” appears when momentum is indecisive.

5. Deviation Distance

This represents how far the market price is from fair value in terms of standard deviation units (σ). It’s calculated using Z-scores and classified as:

• +1σ, +2σ, etc., for overvalued regions.

• −1σ, −2σ, etc., for undervalued areas.

• “At Fair Value” if close to the mean.

6. Bull and Bear Strength Bars

The system computes both bullish and bearish strength, using distance from fair value, the rate of change, and the velocity. These strengths are displayed as progress bars, giving a quick visual cue of conviction. The table labels them as:

• “Bull Conviction” if there's a long bias.

• “Bull Potential” if bullish but undecided.

• “Bear Conviction” or “Bear Potential” for short-side equivalents.

7. Trend Signal

This is a simple label that tells you if the scanner recommends a Long, Short, or Cash (neutral) stance based on threshold logic. It is based on whether the average Z-score crosses above a long threshold or below a short one.

8. Stage

The “Stage” label summarizes the valuation environment based on the composite Z-score:

• Strong Undervalued

• Moderately Undervalued

• Fair Value

• Overvalued, etc.

This stage helps traders know whether they are operating in cheap or expensive territory statistically.

Summary

Overall, this table merges advanced technical signals like momentum, volatility, valuation, and risk into a digestible format that updates dynamically with each bar. The goal is to provide traders with a 360° perspective on market conditions, tailored for both trend-following and mean-reversion strategies.

___________

4. Sentival Valuation Score & Interpretation

🔹 Sentival Score Ranges

- 📉 Strongly Oversold (-2 and below) → Market is extremely undervalued; potential reversal.

- 📉 Moderately Oversold (-1.5 to -2) → Discounted market conditions, buying interest may emerge.

- 📉 Slightly Oversold (-0.5 to -1.5) → Possible accumulation phase.

- ⚖ Fair Value (-0.5 to +0.5) → Market trading at equilibrium.

- 📈 Slightly Overbought (+0.5 to +1.5) → Initial signs of market strength.

- 📈 Moderately Overbought (+1.5 to +2) → Market heating up, caution warranted, selling interest may emerge.

- 📈 Strongly Overbought (+2 and above) → Extreme valuation, increased risk of correction.

This classification helps traders gauge overall market sentiment and make better allocation decisions.

Note: Past valuations and buy/sell signals generated by Sentival do not guarantee future performance. Market conditions can change, and proper risk management should always be applied.

____

5. Use Cases & Applications

🔹 📊 Market Rotation & Asset Allocation

- Used as a valuation model to determine if a market or asset is undervalued or overvalued.

- Rotational strategies can benefit from the valuation score by switching exposure between assets.

🔹 📈 Medium-Term Trend Identification

- Detects overbought and oversold conditions while filtering out short-term noise.

- Can be combined with other trend-following indicators for confluence-based strategies.

🔹 🔄 Mean Reversion & Momentum Trading

- Provides statistical validation for momentum breakouts or mean reversion signals.

- Useful for long-short trading strategies, determining optimal entry & exit points.

____

Conclusion

Sentival is a powerful universal valuation system for traders and investors seeking a data-driven, multi-factor approach to market valuation. With its combination of momentum, trend, risk-adjusted, and mean-reversion indicators, it provides a robust, adaptable, and statistically sound framework for making informed market decisions.

🔹 Who Should Use Sentival?

✅ Swing Traders & Medium-Term Investors looking for structured valuation metrics.

✅ Quantitative & Systematic Traders incorporating multi-factor models.

✅ Portfolio Managers optimizing exposure to different market regimes.

🔹 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Volatility

AMR-AQR-VolSD-Loc**Dynamic Volatility Bands**

The **Dynamic Volatility Bands** indicator is a powerful tool designed to visualize price volatility and key support/resistance levels based on Average Monthly/Quarterly Range (AMR/AQR) and standard deviation calculations. It plots a base volatility line with customizable upper and lower bands (Vol +1 to +5 and Vol -1 to -5), using a vibrant color progression from blue (#2563EB) to red (#EF4444) for clear visual distinction on dark chart backgrounds like #131722.

**Key Features:**

- **Flexible Volatility Calculation**: Choose between manual standard deviation input or automatic calculation using AMR/AQR ranges, with a scaling factor for fine-tuning.

- **Customizable Levels**: Plot up to 5 upper and 5 lower volatility bands, with options for intermediate (half-step) lines.

- **AMR/AQR Integration**: Displays High, Low, 50% High, 50% Low, and Zero Point levels based on monthly or quarterly ranges, with optional monthly/quarterly open reference.

- **Visual Customization**: Configure line styles, widths, colors, and label positions (right, left, or center). Labels show price levels and can be offset for clarity.

- **Informative Table**: A dynamic table summarizes AMR/AQR levels, volatility settings, and key metrics, with customizable position and appearance.

- **Alerts**: Built-in alerts notify when the price approaches AMR/AQR levels, aiding in timely trading decisions.

**How to Use:**

1. Apply the indicator to your chart and adjust the settings under "Standard Deviation Calculation" to set the volatility source (Manual or AMR/AQR).

2. Customize the number of upper/lower bands and their appearance in the "Volatility Settings" group.

3. Enable the table and alerts to monitor key levels and price movements.

4. Use the vibrant color progression to identify volatility zones: blue for low volatility (Vol ±1) and red for high volatility (Vol ±5).

This indicator is ideal for traders seeking to identify potential support/resistance zones and gauge market volatility dynamically. It’s fully customizable to suit various trading strategies and timeframes.

**Note**: Best viewed on dark chart backgrounds (#131722) for optimal color contrast. Ensure sufficient historical data for accurate AMR/AQR calculations.

Wick Spike 50% Detector (15m & 1h)This script identifies candles with significant upper or lower wicks (spikes) based on a percentage of the total candle range. It helps spot potential reversals, exhaustion moves, or liquidity grabs — especially useful in volatile markets.

📍 Key Features:

15-Minute Timeframe:

Red Triangle Above: Candle range ≥ 0.35% and upper wick ≥ 50% of the range.

Green Triangle Below: Candle range ≥ 0.30% and lower wick ≥ 50% of the range.

1-Hour Timeframe:

Red Circle Above: Candle range ≥ 0.50% and upper wick ≥ 50%.

Green Circle Below: Candle range ≥ 0.50% and lower wick ≥ 50%.

📢 Alerts:

Alerts trigger when the 50% spike condition is met — within the last 60 seconds before candle close — ensuring timely notifications.

🎯 Designed to assist traders in identifying spike-driven opportunities and refining entry/exit strategies.

RDBRB Strategy with Filters + Cooldowns + LabelsRDBRB Strategy with Filters + Cooldowns

This script implements the RDBRB (Rally-Drop-Base-Retest-Breakout) strategy, a classic price action setup designed to identify structured trade opportunities using volume, volatility bands, and trend alignment. It’s ideal for traders looking for clean, rule-based entries across any timeframe.

🧠 Core Components

Rally & Drop Detection

Identifies short-term momentum shifts using moving average crossovers:

✅ Ra = Rally (bullish crossover)

🔻 Dr = Drop (bearish crossunder)

Base Formation

A statistical base is defined using a moving average with a standard deviation envelope (Upper/Lower BB). This forms the foundation for breakout or retest setups.

Retest Zone (RT)

When price returns to the lower band (but stays below the base), it suggests a potential re-accumulation or reaction zone before a breakout.

Breakout Confirmation (BO)

A breakout is validated when:

Price crosses above the upper band

Volume exceeds the 20-bar average by a threshold multiplier

RSI is above a bullish momentum level

Price is trending above the longer-term EMA

⏱️ Smart Cooldown Logic

Each signal (Rally, Drop, Retest, Breakout) has an independent cooldown timer to prevent multiple triggers within a short range, filtering out noise and duplicate signals:

Customizable cooldown periods via input settings

Ensures signals are meaningful and not clustered

💡 Visual Markers

All signals are shown as small, color-coded labels:

Ra : Green label below bar

Dr : Red label above bar

RT : Yellow label below bar

BO : Green breakout label below bar

Bands and base are plotted for structure reference.

🛠️ Customizable Settings

Cooldown periods for each signal type

MA lengths, volume and RSI thresholds

Trend filter and base calculation inputs

This script is ideal for price action traders who want a clean, structured method to trade consolidations and trend continuations while avoiding over-signaling. Use it on any timeframe and combine with higher-timeframe confirmation for best results.

Beyond Insights IndicatorThe Beyond Insights Indicator is a multi-timeframe overlay tool designed for TradingView that displays key Exponential Moving Averages (EMAs) and volatility insights to support various trading strategies. It intelligently adapts its display based on the current chart timeframe to reduce clutter and enhance relevance. Specifically, it shows EMA 6, 18, and 50 when viewing intraday timeframes.

In addition to EMAs, the indicator includes an ATR (Average True Range) calculation with a default length of 14, offering insight into market volatility.

GOD Complex Trading By QTX Algo SystemsGOD Complex Trading by QTX Algo Systems

Overview

GOD Complex Trading is a comprehensive signal engine that combines multiple QTX Algo Systems indicators into a unified framework for identifying high-confluence reversal and continuation setups. It includes dynamic entry detection, adaptive stop loss logic, multi-timeframe analysis, score-based risk scaling, and real-time trade visualization.

This script is designed for discretionary traders who want to see structured trade logic unfold directly on the chart, with visual labeling of entry type, dynamic stop loss placement, exit score computation, and key trade metrics shown in an on-chart table.

How It Works

Each trade is classified into one of four categories:

Reversal Long

Reversal Short

Continuation Long

Continuation Short

Each trade type has a distinct confluence requirement involving real-time and higher-timeframe inputs. The indicator calculates a confluence score out of 200 and determines HTF (high-timeframe) directional bias across three layers (HTF1, HTF2, HTF3), which are configurable.

QTX Indicators Used

This script integrates internal logic from the following proprietary QTX tools:

VBM (Volatility-Based Momentum) – Confirms directional bias using momentum slope and volatility increase.

VBSMI (Volatility-Based SMI) – Detects early momentum shifts via band exits and crossovers of adaptive smoothed SMI values.

SEA (Statistically Extreme Areas) – Highlights exhaustion zones using normalized volatility, smoothed range deviation, and SMI divergence.

SPB (Statistical Price Bands) – Uses volatility and trend-adjusted percentiles to define dynamic overbought/oversold zones.

COI (Continuation Opportunity Indicator) – Validates re-entry opportunities following a pullback during trend continuation.

Signal Logic – Examples

Each entry type is built from layered logic:

Reversal Long (Example)

Triggers when:

VBSMI is in dynamic oversold and crosses up

SEA level is at or below threshold (signaling statistical exhaustion)

SPB confirms recent low percentile hit

VBM and COI do not indicate trend continuation in the opposite direction

Continuation Long (Example)

Triggers when:

No recent extreme zones (SPB or SEA) are present

VBM confirms continued trend momentum

VBSMI crosses up and confirms strength

COI may confirm re-entry conditions

High-timeframe bias scores show alignment

All entries are subject to filter checks, including:

Minimum confluence score

HTF bias thresholds (HTF1, HTF2, HTF3)

Position type and trade history

Key Features

Trade Type Auto-Labeling

Each signal is labeled (“Rev Long”, “Cont Short”, etc.) directly on the chart for instant identification.

Stop Loss Visualization

Stop loss levels are calculated using a weighted average of ATR-based padding and prior swing highs/lows. Ghost lines are drawn for Add trades.

TP1 / TP2 Logic

TP1: Fires on opposite VBSMI crossover (momentum loss).

TP2: Fires when the opposite side’s reversal score exceeds a user-defined threshold.

Position Size & Risk Table

The on-chart table shows estimated trade size (based on max risk input), stop loss price, and calculated exit score. Reversal trades scale based on confluence score, while continuation trades use linear scaling.

Multi-Timeframe Confluence

The script uses three automatic higher timeframes to calculate directional bias and exit score amplification. This allows scoring logic to reflect broader trend alignment.

Add Trade Logic

The indicator detects both same-style and cross-style Add setups. Add signals are labeled and visualized, but should be used cautiously.

Auto-Close on Opposite Signal

When an opposite entry signal is triggered (e.g. Cont Short after Rev Long), the current trade is automatically considered closed, resetting tracking variables and metrics.

Additional Features

Fully bar-closed logic: no repainting or mid-bar recalculation.

High-precision control over alert triggering using bias filters and score ranges.

Dedicated alert conditions for all key trade types and TP/SL events.

Score-based position sizing using dynamic confluence score caps.

Table remains visible for a configurable number of bars after trade close.

Use Cases

Manual discretionary entries with clearly labeled setups and real-time validation

Score-based trade review and journaling using TP1/TP2 and exit score

Optimizing trade filters using alerts with HTF bias and confluence thresholds

Data-driven strategy refinement by observing which trades reach full exits

Disclaimer

This tool is provided for educational and informational purposes only. It does not guarantee any particular outcome or profitability. Always use proper risk management, backtest thoroughly, and consult a financial professional if needed.

Full Day Midpoint Line with Dynamic StdDev Bands (ETH & RTH)A Pine Script indicator designed to plot a midpoint line based on the high and low prices of a user-defined trading session (typically Extended Trading Hours, ETH) and to add dynamic standard deviation (StdDev) bands around this midpoint.

Session Midpoint Line:

The midpoint is calculated as the average of the session's highest high and lowest low during the defined ETH period (e.g., 4:00 AM to 8:00 PM).

This line represents a central tendency or "fair value" for the session, similar to a pivot point or volume-weighted average price (VWAP) anchor.

Interpretation:

Prices above the midpoint suggest bullish sentiment, while prices below indicate bearish sentiment.

The midpoint can act as a dynamic support/resistance level, where price may revert to or react at this level during the session.

Dynamic StdDev Bands:

The bands are calculated by adding/subtracting a multiple of the standard deviation of the midpoint values (tracked in an array) from the midpoint.

The standard deviation is dynamically computed based on the historical midpoint values within the session, making the bands adaptive to volatility.

Interpretation:

The upper and lower bands represent potential overbought (upper) and oversold (lower) zones.

Prices approaching or crossing the bands may indicate stretched conditions, potentially signaling reversals or breakouts.

Trend Identification:

Use the midpoint as a reference for the session’s trend. Persistent price action above the midpoint suggests bullishness, while below indicates bearishness.

Combine with other indicators (e.g., moving averages, RSI) to confirm trend direction.

Support/Resistance Trading:

Treat the midpoint as a dynamic pivot point. Price rejections or consolidations near the midpoint can be entry points for mean-reversion trades.

The StdDev bands can act as secondary support/resistance levels. For example, price reaching the upper band may signal a potential short entry if accompanied by reversal signals.

Breakout/Breakdown Strategies:

A strong move beyond the upper or lower band may indicate a breakout (bullish above upper, bearish below lower). Confirm with volume or momentum indicators to avoid false breakouts.

The dynamic nature of the bands makes them useful for identifying significant price extensions.

Volatility Assessment:

Wider bands indicate higher volatility, suggesting larger price swings and potentially riskier trades.

Narrow bands suggest consolidation, which may precede a breakout. Traders can prepare for volatility expansions in such scenarios.

The "Full Day Midpoint Line with Dynamic StdDev Bands" is a versatile and visually intuitive indicator well-suited for day traders focusing on session-specific price action. Its dynamic midpoint and volatility-adjusted bands provide valuable insights into support, resistance, and potential reversals or breakouts.

SMC ICT – Simplified Daily Trend & Reversal AnalyzerThis Pine Script provides a simplified approach to analyzing daily trends and potential reversals using concepts inspired by Smart Money Concepts (SMC) and ICT (Inner Circle Trader).

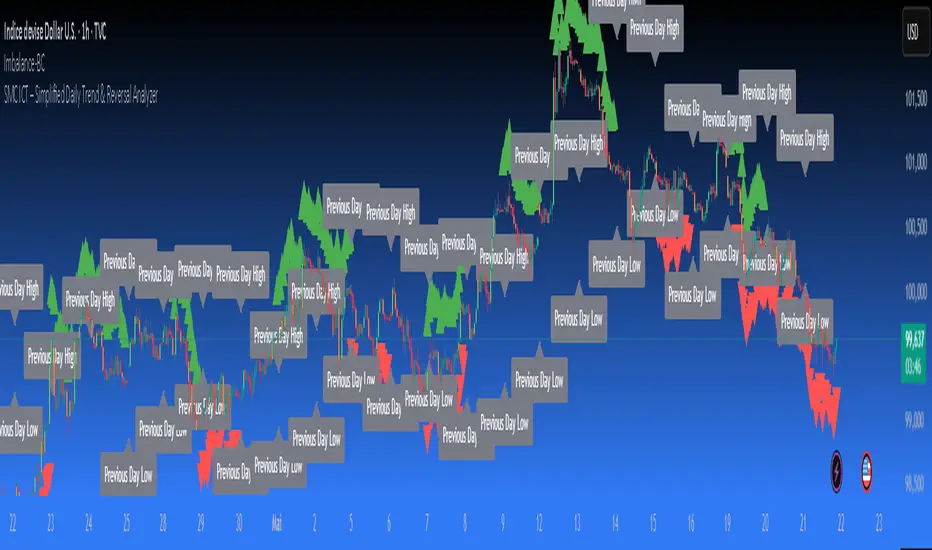

What It Does:

• Detects daily uptrend and downtrend conditions by comparing the current daily high/low to the previous day’s values.

• Highlights potential bullish or bearish reversal zones when price behavior suggests a shift in sentiment.

• Automatically draws dashed lines for the previous day's high and low.

• Labels these high/low levels for quick visual reference.

How to Use:

Apply this indicator to any timeframe chart. Use the plotted trend markers to assess daily direction and potential reversal signals. The dashed lines (previous high/low) can be used as reference points for liquidity zones or break/retest entries.

User Interface:

The indicator displays labels and shapes in English. This script is intended for educational and trading workflow enhancement purposes.

Note:

This is an open-source tool designed for clarity and basic SMC/ICT application. It is best used in combination with other confluences like FVGs, order blocks, and liquidity sweeps.

Momentum (80) + ATR (14)his indicator combines two essential technical analysis tools in a single panel for enhanced market insight:

🔹 Momentum (80 periods): Measures the difference between the current price and the price 80 bars ago. Displayed as a semi-transparent filled area, it helps to visually identify shifts in price momentum over a longer timeframe.

🔸 ATR (Average True Range, 14 periods): Shown as a fine orange line, the ATR represents average market volatility over 14 periods, highlighting phases of calm or increased price fluctuations.

By viewing both momentum and volatility simultaneously, traders can better assess trend strength and market conditions, improving decision-making across assets such as stocks, forex, and cryptocurrencies.

✅ Suitable for all asset types

✅ Complements other indicators like RSI, MACD, and Bollinger Bands

✅ Categorized under Momentum & Volatility indicators

Candle Range DetectorCandle Range Detector

// Pine Script v6

// Detects candle-based ranges, mitigations, and sweeps with advanced logic

Overview

This indicator automatically detects price ranges based on candle containment, then tracks when those ranges are mitigated (broken) and when a sweep occurs. It is designed for traders who want to identify liquidity events and range breaks with precision.

How It Works

- Range Detection: A range is formed when a candle is fully contained within the previous candle (its high is lower and its low is higher). This marks a potential area of price balance or liquidity.

- Mitigation: A range is considered mitigated when price closes beyond its extension levels (configurable by normal or Fibonacci logic). This signals that the range has been invalidated or "taken out" by price action.

- Sweep Detection: After mitigation, the script watches for a sweep event: a candle that both trades through the range extreme and closes decisively beyond the log-mid of the candle itself. This is a strong sign of a liquidity grab or stop run.

- Alerts & Visuals: You can enable alerts and on-chart labels for sweeps. Only the most recent mitigated range can be swept, and each range can only be swept once.

- Timeframe Sensitivity: On weekly or monthly charts, a candle can both mitigate and sweep a range on the same bar. On lower timeframes, only one event can occur per bar.

Why It Works

- Candle containment is a robust way to identify natural price ranges and liquidity pools, as it reflects where price is consolidating or being absorbed.

- Mitigation marks the moment when a range is no longer defended, often leading to new directional moves.

- Sweeps are powerful signals of stop hunts or liquidity grabs, especially when confirmed by a close beyond the log-mid of the candle, indicating strong intent.

Visual Explanation

Tip: Use this tool to spot high-probability reversal or continuation zones, and to get alerted to key liquidity events in real time.

Grid Trade Helper📌 Grid Trade Helper – Range-Based Grid Planning Tool

This tool is designed for range-based traders and manual grid strategy operators, providing a framework to balance execution efficiency and risk exposure.

By referencing historical weekly volatility, it helps estimate a reasonable grid width, visualizes key levels, and supports position management with quantitative guidance.

🧭 Design Philosophy:

In multi-entry systems like grid trading, there's always a tradeoff:

"Tighter grids improve opportunity density but increase risk; wider grids reduce risk but lower efficiency."

This tool seeks to provide a dynamic equilibrium between the two, using past volatility to determine practical grid intervals and suggest safe leverage thresholds.

✨ Core Features:

Weekly open level tracking (custom time + time zone support)

Volatility-based suggestions for grid width and safe grid count

Visual range plotting with optional stop-line overlay

Compact live table showing key metrics: average range, grid width, grid count, leverage cap

🔧 Customizable Parameters:

Time zone and custom weekly open hour

Max number of visual elements (lines, boxes)

Color and line style options

📈 Suggested Use Cases:

Planning manual grid structures with volatility-adjusted intervals

Visual support for range-bound or sideways market strategies

Estimating leverage exposure and grid density for better position control

⚠️ This indicator is intended as a strategic support tool and does not constitute financial advice. Use according to your own risk framework and market understanding.

Ultimate Scalping Tool[BullByte]Overview

The Ultimate Scalping Tool is an open-source TradingView indicator built for scalpers and short-term traders released under the Mozilla Public License 2.0. It uses a custom Quantum Flux Candle (QFC) oscillator to combine multiple market forces into one visual signal. In plain terms, the script reads momentum, trend strength, volatility, and volume together and plots a special “candlestick” each bar (the QFC) that reflects the overall market bias. This unified view makes it easier to spot entries and exits: the tool labels signals as Strong Buy/Sell, Pullback (a brief retracement in a trend), Early Entry, or Exit Warning . It also provides color-coded alerts and a small dashboard of metrics. In practice, traders see green/red oscillator bars and symbols on the chart when conditions align, helping them scalp or trend-follow without reading multiple separate indicators.

Core Components

Quantum Flux Candle (QFC) Construction

The QFC is the heart of the indicator. Rather than using raw price, it creates a candlestick-like bar from the underlying oscillator values. Each QFC bar has an “open,” “high/low,” and “close” derived from calculated momentum and volatility inputs for that period . In effect, this turns the oscillator into intuitive candle patterns so traders can recognize momentum shifts visually. (For comparison, note that Heikin-Ashi candles “have a smoother look because take an average of the movement”. The QFC instead represents exact oscillator readings, so it reflects true momentum changes without hiding price action.) Colors of QFC bars change dynamically (e.g. green for bullish momentum, red for bearish) to highlight shifts. This is the first open-source QFC oscillator that dynamically weights four non-correlated indicators with moving thresholds, which makes it a unique indicator on its own.

Oscillator Normalization & Adaptive Weights

The script normalizes its oscillator to a fixed scale (for example, a 0–100 range much like the RSI) so that various inputs can be compared fairly. It then applies adaptive weighting: the relative influence of trend, momentum, volatility or volume signals is automatically adjusted based on current market conditions. For instance, in very volatile markets the script might weight volatility more heavily, or in a strong trend it might give extra weight to trend direction. Normalizing data and adjusting weights helps keep the QFC sensitive but stable (normalization ensures all inputs fit a common scale).

Trend/Momentum/Volume/Volatility Fusion

Unlike a typical single-factor oscillator, the QFC oscillator fuses four aspects at once. It may compute, for example, a trend indicator (such as an ADX or moving average slope), a momentum measure (like RSI or Rate-of-Change), a volume-based pressure (similar to MFI/OBV), and a volatility measure (like ATR) . These different values are combined into one composite oscillator. This “multi-dimensional” approach follows best practices of using non-correlated indicators (trend, momentum, volume, volatility) for confirmation. By encoding all these signals in one line, a high QFC reading means that trend, momentum, and volume are all aligned, whereas a neutral reading might mean mixed conditions. This gives traders a comprehensive picture of market strength.

Signal Classification

The script interprets the QFC oscillator to label trades. For example:

• Strong Buy/Sell : Triggered when the oscillator crosses a high-confidence threshold (e.g. breaks clearly above zero with strong slope), indicating a well-confirmed move. This is like seeing a big green/red QFC candle aligned with the trend.

• Pullbacks : Identified when the trend is up but momentum dips briefly. A Pullback Buy appears if the overall trend is bullish but the oscillator has a short retracement – a typical buying opportunity in an uptrend. (A pullback is “a brief decline or pause in a generally upward price trend”.)

• Early Buy/Sell : Marks an initial swing in the oscillator suggesting a possible new trend, before it is fully confirmed. It’s a hint of momentum building (an early-warning signal), not as strong as the confirmed “Strong” signal.

• Exit Warnings : Issued when momentum peaks or reverses. For instance, if the QFC bars reach a high and start turning red/green opposite, the indicator warns that the move may be ending. In other words, a Momentum Peak is the point of maximum strength after which weakness may follow.

These categories correspond to typical trading concepts: Pullback (temporary reversal in an uptrend), Early Buy (an initial bullish cross), Strong Buy (confirmed bullish momentum), and Momentum Peak (peak oscillator value suggesting exhaustion).

Filters (DI Reversal, Dynamic Thresholds, HTF EMA/ADX)

Extra filters help avoid bad trades. A DI Reversal filter uses the +DI/–DI lines (from the ADX system) to require that the trend direction confirms the signal . For example, it might ignore a buy signal if the +DI is still below –DI. Dynamic Thresholds adjust signal levels on-the-fly: rather than fixed “overbought” lines, they move with volatility so signals happen under appropriate market stress. An optional High-Timeframe EMA or ADX filter adds a check against a larger timeframe trend: for instance, only taking a trade if price is above the weekly EMA or if weekly ADX shows a strong trend. (Notably, the ADX is “a technical indicator used by traders to determine the strength of a price trend”, so requiring a high-timeframe ADX avoids trading against the bigger trend.)

Dashboard Metrics & Color Logic

The Dashboard in the Ultimate Scalping Tool (UST) serves as a centralized information hub, providing traders with real-time insights into market conditions, trend strength, momentum, volume pressure, and trade signals. It is highly customizable, allowing users to adjust its appearance and content based on their preferences.

1. Dashboard Layout & Customization

Short vs. Extended Mode : Users can toggle between a compact view (9 rows) and an extended view (13 rows) via the `Short Dashboard` input.

Text Size Options : The dashboard supports three text sizes— Tiny, Small, and Normal —adjustable via the `Dashboard Text Size` input.

Positioning : The dashboard is positioned in the top-right corner by default but can be moved if modified in the script.

2. Key Metrics Displayed

The dashboard presents critical trading metrics in a structured table format:

Trend (TF) : Indicates the current trend direction (Strong Bullish, Moderate Bullish, Sideways, Moderate Bearish, Strong Bearish) based on normalized trend strength (normTrend) .

Momentum (TF) : Displays momentum status (Strong Bullish/Bearish or Neutral) derived from the oscillator's position relative to dynamic thresholds.

Volume (CMF) : Shows buying/selling pressure levels (Very High Buying, High Selling, Neutral, etc.) based on the Chaikin Money Flow (CMF) indicator.

Basic & Advanced Signals:

Basic Signal : Provides simple trade signals (Strong Buy, Strong Sell, Pullback Buy, Pullback Sell, No Trade).

Advanced Signal : Offers nuanced signals (Early Buy/Sell, Momentum Peak, Weakening Momentum, etc.) with color-coded alerts.

RSI : Displays the Relative Strength Index (RSI) value, colored based on overbought (>70), oversold (<30), or neutral conditions.

HTF Filter : Indicates the higher timeframe trend status (Bullish, Bearish, Neutral) when using the Leading HTF Filter.

VWAP : Shows the V olume-Weighted Average Price and whether the current price is above (bullish) or below (bearish) it.

ADX : Displays the Average Directional Index (ADX) value, with color highlighting whether it is rising (green) or falling (red).

Market Mode : Shows the selected market type (Crypto, Stocks, Options, Forex, Custom).

Regime : Indicates volatility conditions (High, Low, Moderate) based on the **ATR ratio**.

3. Filters Status Panel

A secondary panel displays the status of active filters, helping traders quickly assess which conditions are influencing signals:

- DI Reversal Filter: On/Off (confirms reversals before generating signals).

- Dynamic Thresholds: On/Off (adjusts buy/sell thresholds based on volatility).

- Adaptive Weighting: On/Off (auto-adjusts oscillator weights for trend/momentum/volatility).

- Early Signal: On/Off (enables early momentum-based signals).

- Leading HTF Filter: On/Off (applies higher timeframe trend confirmation).

4. Visual Enhancements

Color-Coded Cells : Each metric is color-coded (green for bullish, red for bearish, gray for neutral) for quick interpretation.

Dynamic Background : The dashboard background adapts to market conditions (bullish/bearish/neutral) based on ADX and DI trends.

Customizable Reference Lines : Users can enable/disable fixed reference lines for the oscillator.

How It(QFC) Differs from Traditional Indicators

Quantum Flux Candle (QFC) Versus Heikin-Ashi

Heikin-Ashi candles smooth price by averaging (HA’s open/close use averages) so they show trend clearly but hide true price (the current HA bar’s close is not the real price). QFC candles are different: they are oscillator values, not price averages . A Heikin-Ashi chart “has a smoother look because it is essentially taking an average of the movement”, which can cause lag. The QFC instead shows the raw combined momentum each bar, allowing faster recognition of shifts. In short, HA is a smoothed price chart; QFC is a momentum-based chart.

Versus Standard Oscillators

Common oscillators like RSI or MACD use fixed formulas on price (or price+volume). For example, RSI “compares gains and losses and normalizes this value on a scale from 0 to 100”, reflecting pure price momentum. MFI is similar but adds volume. These indicators each show one dimension: momentum or volume. The Ultimate Scalping Tool’s QFC goes further by integrating trend strength and volatility too. In practice, this means a move that looks strong on RSI might be downplayed by low volume or weak trend in QFC. As one source notes, using multiple non-correlated indicators (trend, momentum, volume, volatility) provides a more complete market picture. The QFC’s multi-factor fusion is unique – it is effectively a multi-dimensional oscillator rather than a traditional single-input one.

Signal Style

Traditional oscillators often use crossovers (RSI crossing 50) or fixed zones (MACD above zero) for signals. The Ultimate Scalping Tool’s signals are custom-classified: it explicitly labels pullbacks, early entries, and strong moves. These terms go beyond a typical indicator’s generic “buy”/“sell.” In other words, it packages a strategy around the oscillator, which traders can backtest or observe without reading code.

Key Term Definitions

• Pullback : A short-term dip or consolidation in an uptrend. In this script, a Pullback Buy appears when price is generally rising but shows a brief retracement. (As defined by Investopedia, a pullback is “a brief decline or pause in a generally upward price trend”.)

• Early Buy/Sell : An initial or tentative entry signal. It means the oscillator first starts turning positive (or negative) before a full trend has developed. It’s an early indication that a trend might be starting.

• Strong Buy/Sell : A confident entry signal when multiple conditions align. This label is used when momentum is already strong and confirmed by trend/volume filters, offering a higher-probability trade.

• Momentum Peak : The point where bullish (or bearish) momentum reaches its maximum before weakening. When the oscillator value stops rising (or falling) and begins to reverse, the script flags it as a peak – signaling that the current move could be overextended.

What is the Flux MA?

The Flux MA (Moving Average) is an Exponential Moving Average (EMA) applied to a normalized oscillator, referred to as FM . Its purpose is to smooth out the fluctuations of the oscillator, providing a clearer picture of the underlying trend direction and strength. Think of it as a dynamic baseline that the oscillator moves above or below, helping you determine whether the market is trending bullish or bearish.

How it’s calculated (Flux MA):

1.The oscillator is normalized (scaled to a range, typically between 0 and 1, using a default scale factor of 100.0).

2.An EMA is applied to this normalized value (FM) over a user-defined period (default is 10 periods).

3.The result is rescaled back to the oscillator’s original range for plotting.

Why it matters : The Flux MA acts like a support or resistance level for the oscillator, making it easier to spot trend shifts.

Color of the Flux Candle

The Quantum Flux Candle visualizes the normalized oscillator (FM) as candlesticks, with colors that indicate specific market conditions based on the relationship between the FM and the Flux MA. Here’s what each color means:

• Green : The FM is above the Flux MA, signaling bullish momentum. This suggests the market is trending upward.

• Red : The FM is below the Flux MA, signaling bearish momentum. This suggests the market is trending downward.

• Yellow : Indicates strong buy conditions (e.g., a "Strong Buy" signal combined with a positive trend). This is a high-confidence signal to go long.

• Purple : Indicates strong sell conditions (e.g., a "Strong Sell" signal combined with a negative trend). This is a high-confidence signal to go short.

The candle mode shows the oscillator’s open, high, low, and close values for each period, similar to price candlesticks, but it’s the color that provides the quick visual cue for trading decisions.

How to Trade the Flux MA with Respect to the Candle

Trading with the Flux MA and Quantum Flux Candle involves using the MA as a trend indicator and the candle colors as entry and exit signals. Here’s a step-by-step guide:

1. Identify the Trend Direction

• Bullish Trend : The Flux Candle is green and positioned above the Flux MA. This indicates upward momentum.

• Bearish Trend : The Flux Candle is red and positioned below the Flux MA. This indicates downward momentum.

The Flux MA serves as the reference line—candles above it suggest buying pressure, while candles below it suggest selling pressure.

2. Interpret Candle Colors for Trade Signals

• Green Candle : General bullish momentum. Consider entering or holding a long position.

• Red Candle : General bearish momentum. Consider entering or holding a short position.

• Yellow Candle : A strong buy signal. This is an ideal time to enter a long trade.

• Purple Candle : A strong sell signal. This is an ideal time to enter a short trade.

3. Enter Trades Based on Crossovers and Colors

• Long Entry : Enter a buy position when the Flux Candle turns green and crosses above the Flux MA. If it turns yellow, this is an even stronger signal to go long.

• Short Entry : Enter a sell position when the Flux Candle turns red and crosses below the Flux MA. If it turns purple, this is an even stronger signal to go short.

4. Exit Trades

• Exit Long : Close your buy position when the Flux Candle turns red or crosses below the Flux MA, indicating the bullish trend may be reversing.

• Exit Short : Close your sell position when the Flux Candle turns green or crosses above the Flux MA, indicating the bearish trend may be reversing.

•You might also exit a long trade if the candle changes from yellow to green (weakening strong buy signal) or a short trade from purple to red (weakening strong sell signal).

5. Use Additional Confirmation

To avoid false signals, combine the Flux MA and candle signals with other indicators or dashboard metrics (e.g., trend strength, momentum, or volume pressure). For example:

•A yellow candle with a " Strong Bullish " trend and high buying volume is a robust long signal.

•A red candle with a " Moderate Bearish " trend and neutral momentum might need more confirmation before shorting.

Practical Example

Imagine you’re scalping a cryptocurrency:

• Long Trade : The Flux Candle turns yellow and is above the Flux MA, with the dashboard showing "Strong Buy" and high buying volume. You enter a long position. You exit when the candle turns red and dips below the Flux MA.

• Short Trade : The Flux Candle turns purple and crosses below the Flux MA, with a "Strong Sell" signal on the dashboard. You enter a short position. You exit when the candle turns green and crosses above the Flux MA.

Market Presets and Adaptation

This indicator is designed to work on any market with candlestick price data (stocks, crypto, forex, indices, etc.). To handle different behavior, it provides presets for major asset classes. Selecting a “Stocks,” “Crypto,” “Forex,” or “Options” preset automatically loads a set of parameter values optimized for that market . For example, a crypto preset might use a shorter lookback or higher sensitivity to account for crypto’s high volatility, while a stocks preset might use slightly longer smoothing since stocks often trend more slowly. In practice, this means the same core QFC logic applies across markets, but the thresholds and smoothing adjust so signals remain relevant for each asset type.

Usage Guidelines

• Recommended Timeframes : Optimized for 1 minute to 15 minute intraday charts. Can also be used on higher timeframes for short term swings.

• Market Types : Select “Crypto,” “Stocks,” “Forex,” or “Options” to auto tune periods, thresholds and weights. Use “Custom” to manually adjust all inputs.

• Interpreting Signals : Always confirm a signal by checking that trend, volume, and VWAP agree on the dashboard. A green “Strong Buy” arrow with green trend, green volume, and price > VWAP is highest probability.

• Adjusting Sensitivity : To reduce false signals in fast markets, enable DI Reversal Confirmation and Dynamic Thresholds. For more frequent entries in trending environments, enable Early Entry Trigger.

• Risk Management : This tool does not plot stop loss or take profit levels. Users should define their own risk parameters based on support/resistance or volatility bands.

Background Shading

To give you an at-a-glance sense of market regime without reading numbers, the indicator automatically tints the chart background in three modes—neutral, bullish and bearish—with two levels of intensity (light vs. dark):

Neutral (Gray)

When ADX is below 20 the market is considered “no trend” or too weak to trade. The background fills with a light gray (high transparency) so you know to sit on your hands.

Bullish (Green)

As soon as ADX rises above 20 and +DI exceeds –DI, the background turns a semi-transparent green, signaling an emerging uptrend. When ADX climbs above 30 (strong trend), the green becomes more opaque—reminding you that trend-following signals (Strong Buy, Pullback) carry extra weight.

Bearish (Red)

Similarly, if –DI exceeds +DI with ADX >20, you get a light red tint for a developing downtrend, and a darker, more solid red once ADX surpasses 30.

By dynamically varying both hue (green vs. red vs. gray) and opacity (light vs. dark), the background instantly communicates trend strength and direction—so you always know whether to favor breakout-style entries (in a strong trend) or stay flat during choppy, low-ADX conditions.

The setup shown in the above chart snapshot is BTCUSD 15 min chart : Binance for reference.

Disclaimer

No indicator guarantees profits. Backtest or paper trade this tool to understand its behavior in your market. Always use proper position sizing and stop loss orders.

Good luck!

- BullByte

Value Scanner | QuantEdgeB📡 Value Scanner | QuantEdgeB

🔍 What is the Value Scanner?

The Value Scanner by QuantEdgeB is a volatility-adaptive valuation framework that dynamically evaluates where price sits relative to a custom “Fair Value” zone. It combines your choice of moving average engine (SMA, WMA, VIDYA, etc.) with multi-layered standard deviation or ATR-based bands to highlight extreme conditions, reversal zones, and statistical overextensions in real time.

💡 Think of Value Scanner as a radar grid, continuously scanning market terrain and painting a full spectrum from balance to extreme disequilibrium.

⚙️ Core Components

✅ Customizable Moving Average Core

At the heart of the scanner lies a flexible moving average engine:

• Choose from 12+ advanced types: 𝓦𝓜𝓐, 𝓥𝓦𝓜𝓐, 𝓥𝓘𝓓𝓨𝓐, 𝓢𝓜𝓜𝓐, 𝓐𝓛𝓜𝓐, 𝓛𝓢𝓜𝓐, and more.

• Fair Value is derived from this base and acts as the center of the statistical zones.

✅ Volatility-Driven Band Construction

Two volatility methods power the adaptive zones:

• Average True Range (ATR): Ideal for reactive, price-based spreads.

• Standard Deviation (SD): Better for modeling reversion and deviation symmetry.

The scanner builds up to ±5σ zones, dynamically updating in real time.

🎯 Signal and Zone Identification

🧭 Deviation Labels

The system assigns a statistical label at every candle:

• From +0.5σ to +5σ for increasing levels of overextension upward.

• From -0.5σ to -5σ for oversold and undervalued conditions.

🌐 Market Stage Detection

Each deviation zone is translated into an intuitive market phrase such as:

• “𝓔𝔁𝓽𝓻𝓮𝓶𝓮𝓵𝔂 𝓞𝓿𝓮𝓻𝓫𝓸𝓾𝓰𝓱𝓽”

• “𝓜𝓲𝓭 𝓥𝓪𝓵𝓾𝓮 / 𝓑𝓪𝓵𝓪𝓷𝓬𝓮𝓭”

• “𝓜𝓪𝔁𝓲𝓶𝓾𝓶 𝓔𝔁𝓽𝓮𝓷𝓼𝓲𝓸𝓷 𝓓𝓸𝔀𝓷”

These phrases help you intuitively gauge risk, reward, and imbalance without needing to study a chart for long.

🔺 Signal Mechanics

📌 Reversal Signals (Optional)

• Automatic buy signals when price crosses above key lower deviation levels.

• Sell signals when price crosses below upper deviation bands.

• Ideal for mean-reversion setups or high-probability reversal plays.

🖼️ Visual Overlay Engine

• Beautifully shaded volatility bands with decreasing opacity as they move away from fair value.

• Background coloring highlights extreme price zones for fast visual alerts.

• Built-in "table display" summarizing the current base, volatility method, direction, fair value, and deviation stage.

📊 Table Overlay Features

The live diagnostic table (position adjustable) displays:

• 📈 Current Base MA Type

• 🌡️ Volatility Method in use (ATR or SD)

• 🧭 Trend direction (rising/falling/neutral)

• 🧮 Current Deviation Label (+2σ, -3σ, etc.)

• 🚦 Interpretive Stage Phrase ("Strongly Overbought", etc.)

• 📍 Real-Time Fair Value

• 🚨 Upper & Lower Extremes

🧠 Why Use the Value Scanner?

This tool is designed for traders who want to:

• Identify price extremes relative to statistical norms.

• Time entries and exits based on price's relationship to value zones.

• Visualize volatility structure without clutter.

• Combine trend-following or mean-reversion logic with elegant overlays and table analytics.

💼 Ideal Use Cases

• Swing trading: Spot overextensions or returns to mean.

• Options traders: Gauge volatility compression or expansion.

• Reversion systems: Generate contrarian signals at edge zones.

• Trend continuation: Use +1σ or -1σ as breakout validation levels.

🧬 Default Settings

• Base Type: 𝓦𝓜𝓐

• Length: 21

• Volatility Type: 𝓐𝓿𝓰. 𝓣𝓻𝓾𝓮 𝓡𝓪𝓷𝓰𝓮

•. Volatility Lengths: ATR 14 / Stdev 30

🧬 In Summary

Value Scanner | QuantEdgeB is not just a volatility band indicator — it’s a contextual market scanner that combines price equilibrium theory with precision deviation mapping. It adds statistical insight, color-coded extremes, and narrative stage identification — all in real time.

Whether you’re trend-following or fading extremes, this system helps you locate value, measure dislocation, and trade with mathematical confidence.

📌 Trade with Statistical Precision | Powered by QuantEdgeB

🔹 Disclaimer: Past performance is not indicative of future results.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Z-Score IndicatorWhat it does:

Calculates the Z-Score: (Current Price - Average Price) / Standard Deviation

Plots the Z-Score in a separate panel below your main chart.

Allows you to customize the Lookback Period (default is 30 bars) to suit your trading style and the asset's characteristics. A shorter period is more sensitive, while a longer period provides a smoother output.

Key Features:

Clear Z-Score Line: Visualizes the current Z-Score value.

Reference Lines:

Zero Line (Gray, Dotted): Indicates the price is at its average for the lookback period.

+2 Standard Deviations (Red, Dotted): Highlights when the price is significantly above its recent average. Often interpreted as potentially overbought.

-2 Standard Deviations (Red, Dotted): Highlights when the price is significantly below its recent average. Often interpreted as potentially oversold.

How to use it:

Look for Z-Score values moving towards or beyond the +2 or -2 standard deviation lines. These extremes can signal that the price has moved unusually far from its mean and might be due for a reversion or a pause.

Use it in conjunction with other indicators and your overall market analysis to make more informed trading decisions.

Experiment with the "Lookback Period" setting to find what works best for different assets and timeframes.

Filtered DTR Table📊 Filtered Daily True Range (DTR) Indicator

This indicator calculates and displays a filtered version of the Daily True Range (DTR) over the last 14 trading days, using high and low prices of each day.

It filters out extreme values by excluding any daily range that is:

Less than 0.5× the average range

Greater than 2× the average range

The indicator shows a table in the bottom-right corner of the main chart, containing:

Filtered ATR – The average of valid (filtered) daily ranges over the past 14 days, based on the high-low difference.

Current Day's Range – The high-low range of the current trading day.

% of ATR – How much of the filtered ATR has been covered by today's range, expressed as a whole number percentage.

PhenLabs - Market Fluid Dynamics📊 Market Fluid Dynamics -

Version: PineScript™ v6

📌 Description

The Market Fluid Dynamics - Phen indicator is a new thinking regarding market analysis by modeling price action, volume, and volatility using a fluid system. It attempts to offer traders control over more profound market forces, such as momentum (speed), resistance (thickness), and buying/selling pressure. By visualizing such dynamics, the script allows the traders to decide on the prevailing market flow, its power, likely continuations, and zones of calmness and chaos, and thereby allows improved decision-making.

This measure avoids the usual difficulty of reconciling multiple, often contradictory, market indications by including them within a single overarching model. It moves beyond traditional binary indicators by providing a multi-dimensional view of market behavior, employing fluid dynamic analogs to describe complex interactions in an accessible manner.

🚀 Points of Innovation

Integrated Fluid Dynamics Model: Combines velocity, viscosity, pressure, and turbulence into a single indicator.

Normalized Metrics: Uses ATR and other normalization techniques for consistent readings across different assets and timeframes.

Dynamic Flow Visualization: Main flow line changes color and intensity based on direction and strength.

Turbulence Background: Visually represents market stability with a gradient background, from calm to turbulent.

Comprehensive Dashboard: Provides an at-a-glance summary of key fluid dynamic metrics.

Multi-Layer Smoothing: Employs several layers of EMA smoothing for a clearer, more responsive main flow line.

🔧 Core Components

Velocity Component: Measures price momentum (first derivative of price), normalized by ATR. It indicates the speed and direction of price changes.

Viscosity Component: Represents market resistance to price changes, derived from ATR relative to its historical average. Higher viscosity suggests it’s harder for prices to move.

Pressure Component: Quantifies the force created by volume and price range (close - open), normalized by ATR. It reflects buying or selling pressure.

Turbulence Detection: Calculates a Reynolds number equivalent to identify market stability, ranging from laminar (stable) to turbulent (chaotic).

Main Flow Indicator: Combines the above components, applying sensitivity and smoothing, to generate a primary signal of market direction and strength.

🔥 Key Features

Advanced Smoothing Algorithm: Utilizes multiple EMA layers on the raw flow calculation for a fluid and responsive main flow line, reducing noise while maintaining sensitivity.

Gradient Flow Coloring: The main flow line dynamically changes color from light to deep blue for bullish flow and light to deep red for bearish flow, with intensity reflecting flow strength. This provides an immediate visual cue of market sentiment and momentum.

Turbulence Level Background: The chart background changes color based on calculated turbulence (from calm gray to vibrant orange), offering an intuitive understanding of market stability and potential for erratic price action.

Informative Dashboard: A customizable on-screen table displays critical metrics like Flow State, Flow Strength, Market Viscosity, Turbulence, Pressure Force, Flow Acceleration, and Flow Continuity, allowing traders to quickly assess current market conditions.

Configurable Lookback and Sensitivity: Users can adjust the base lookback period for calculations and the sensitivity of the flow to viscosity, tailoring the indicator to different trading styles and market conditions.

Alert Conditions: Pre-defined alerts for flow direction changes (positive/negative crossover of zero line) and detection of high turbulence states.

🎨 Visualization

Main Flow Line: A smoothed line plotted below the main chart, colored blue for bullish flow and red for bearish flow. The intensity of the color (light to dark) indicates the strength of the flow. This line crossing the zero line can signal a change in market direction.

Zero Line: A dotted horizontal line at the zero level, serving as a baseline to gauge whether the market flow is positive (bullish) or negative (bearish).

Turbulence Background: The indicator pane’s background color changes based on the calculated turbulence level. A calm, almost transparent gray indicates low turbulence (laminar flow), while a more vibrant, semi-transparent orange signifies high turbulence. This helps traders visually assess market stability.

Dashboard Table: An optional table displayed on the chart, showing key metrics like ‘Flow State’, ‘Flow Strength’, ‘Market Viscosity’, ‘Turbulence’, ‘Pressure Force’, ‘Flow Acceleration’, and ‘Flow Continuity’ with their current values and qualitative descriptions (e.g., ‘Bullish Flow’, ‘Laminar (Stable)’).

📖 Usage Guidelines

Setting Categories

Show Dashboard - Default: true; Range: true/false; Description: Toggles the visibility of the Market Fluid Dynamics dashboard on the chart. Enable to see key metrics at a glance.

Base Lookback Period - Default: 14; Range: 5 - (no upper limit, practical limits apply); Description: Sets the primary lookback period for core calculations like velocity, ATR, and volume SMA. Shorter periods make the indicator more sensitive to recent price action, while longer periods provide a smoother, slower signal.

Flow Sensitivity - Default: 0.5; Range: 0.1 - 1.0 (step 0.1); Description: Adjusts how much the market viscosity dampens the raw flow. A lower value means viscosity has less impact (flow is more sensitive to raw velocity/pressure), while a higher value means viscosity has a greater dampening effect.

Flow Smoothing - Default: 5; Range: 1 - 20; Description: Controls the length of the EMA smoothing applied to the main flow line. Higher values result in a smoother flow line but with more lag; lower values make it more responsive but potentially noisier.

Dashboard Position - Default: ‘Top Right’; Range: ‘Top Right’, ‘Top Left’, ‘Bottom Right’, ‘Bottom Left’, ‘Middle Right’, ‘Middle Left’; Description: Determines the placement of the dashboard on the chart.

Header Size - Default: ‘Normal’; Range: ‘Tiny’, ‘Small’, ‘Normal’, ‘Large’, ‘Huge’; Description: Sets the text size for the dashboard header.

Values Size - Default: ‘Small’; Range: ‘Tiny’, ‘Small’, ‘Normal’, ‘Large’; Description: Sets the text size for the metric values in the dashboard.

✅ Best Use Cases

Trend Identification: Identifying the dominant market flow (bullish or bearish) and its strength to trade in the direction of the prevailing trend.

Momentum Confirmation: Using the flow strength and acceleration to confirm the conviction behind price movements.

Volatility Assessment: Utilizing the turbulence metric to gauge market stability, helping to adjust position sizing or avoid choppy conditions.

Reversal Spotting: Watching for divergences between price and flow, or crossovers of the main flow line above/below the zero line, as potential reversal signals, especially when combined with changes in pressure or viscosity.

Swing Trading: Leveraging the smoothed flow line to capture medium-term market swings, entering when flow aligns with the desired trade direction and exiting when flow weakens or reverses.

Intraday Scalping: Using shorter lookback periods and higher sensitivity to identify quick shifts in flow and turbulence for short-term trading opportunities, particularly in liquid markets.

⚠️ Limitations

Lagging Nature: Like many indicators based on moving averages and lookback periods, the main flow line can lag behind rapid price changes, potentially leading to delayed signals.

Whipsaws in Ranging Markets: During periods of low volatility or sideways price action (high viscosity, low flow strength), the indicator might produce frequent buy/sell signals (whipsaws) as the flow oscillates around the zero line.

Not a Standalone System: While comprehensive, it should be used in conjunction with other forms of analysis (e.g., price action, support/resistance levels, other indicators) and not as a sole basis for trading decisions.

Subjectivity in Interpretation: While the dashboard provides quantitative values, the interpretation of “strong” flow, “high” turbulence, or “significant” acceleration can still have a subjective element depending on the trader’s strategy and risk tolerance.

💡 What Makes This Unique

Fluid Dynamics Analogy: Its core strength lies in translating complex market interactions into an intuitive fluid dynamics framework, making concepts like momentum, resistance, and pressure easier to visualize and understand.

Market View: Instead of focusing on a single aspect (like just momentum or just volatility), it integrates multiple factors (velocity, viscosity, pressure, turbulence) to provide a more comprehensive picture of market conditions.

Adaptive Visualization: The dynamic coloring of the flow line and the turbulence background provide immediate, adaptive visual feedback that changes with market conditions.

🔬 How It Works

Price Velocity Calculation: The indicator first calculates price velocity by measuring the rate of change of the closing price over a given ‘lookback’ period. The raw velocity is then normalized by the Average True Range (ATR) of the same lookback period. Normalization enables comparison of momentum between assets or timeframes by scaling for volatility. This is the direction and speed of initial price movement.

Viscosity Calculation: Market ‘viscosity’ or resistance to price movement is determined by looking at the current ATR relative to its longer-term average (SMA of ATR over lookback * 2). The further the current ATR is above its average, the lower the viscosity (less resistance to price movement), and vice-versa. The script inverts this relationship and bounds it so that rising viscosity means more resistance.

Pressure Force Measurement: A ‘pressure’ variable is calculated as a function of the ratio of current volume to its simple moving average, multiplied by the price range (close - open) and normalized by ATR. This is designed to measure the force behind price movement created by volume and intraday price thrusts. This pressure is smoothed by an EMA.

Turbulence State Evaluation: A equivalent ‘Reynolds number’ is calculated by dividing the absolute normalized velocity by the viscosity. This is the proclivity of the market to move in a chaotic or orderly fashion. This ‘reynoldsValue’ is smoothed with an EMA to get the ‘turbulenceState’, which indicates if the market is laminar (stable), transitional, or turbulent.

Main Flow Derivation: The ‘rawFlow’ is calculated by taking the normalized velocity, dampening its impact based on the ‘viscosity’ and user-input ‘sensitivity’, and orienting it by the sign of the smoothed ‘pressureSmooth’. The ‘rawFlow’ is then put through multiple layers of exponential moving average (EMA) smoothing (with ‘smoothingLength’ and derived values) to reach the final ‘mainFlow’ line. The extensive smoothing is designed to give a smooth and clear visualization of the overall market direction and magnitude.

Dashboard Metrics Compilation: Additional metrics like flow acceleration (derivative of mainFlow), and flow continuity (correlation between close and volume) are calculated. All primary components (Flow State, Strength, Viscosity, Turbulence, Pressure, Acceleration, Continuity) are then presented in a user-configurable dashboard for ease of monitoring.

💡 Note:

The “Market Fluid Dynamics - Phen” indicator is designed to offer a unique perspective on market behavior by applying principles from fluid dynamics. It’s most effective when used to understand the underlying forces driving price rather than as a direct buy/sell signal generator in isolation. Experiment with the settings, particularly the ‘Base Lookback Period’, ‘Flow Sensitivity’, and ‘Flow Smoothing’, to find what best suits your trading style and the specific asset you are analyzing. Always combine its insights with robust risk management practices.

Filt ADR🟠 Script Name: Filtered Average Daily Range (Filt ADR)

This script calculates a filtered version of the Average Daily Range (ADR) based on the last 14 daily candles. It's designed to reduce the influence of unusually high or low daily ranges (outliers) by applying a filter before calculating the average.

🔧 How It Works — Step by Step

1. Calculate Daily Ranges (High - Low)

It retrieves the daily price ranges (difference between daily high and low) for the last 14 days using request.security() with the "D" (daily) timeframe.

pinescript

Копировать

Редактировать

high - low // today's daily range

high - low // yesterday's daily range

...

These values are stored into individual variables dr0 to dr13.

2. Build an Array of Daily Ranges

An array named ranges is used to store the 14 daily ranges, but only if they are not na (missing data). This avoids errors during processing.

3. Calculate the Initial (Unfiltered) Average Range

The script sums all values in the ranges array and calculates their average:

pinescript

Копировать

Редактировать

avg_all = total sum of ranges / number of valid entries

4. Filter Out Outliers

Now it filters the values in ranges:

Only keeps the ranges that are between 0.5×avg_all and 2×avg_all.

This is to remove abnormally small or large daily ranges that could distort the average.

The filtered values are added to a second array called filtered.

5. Calculate the Filtered ADR

Finally, it calculates the average of the filtered daily ranges:

pinescript

Копировать

Редактировать

avg_filt = sum of filtered ranges / number of filtered values

This is the Filtered ADR.

6. Plot the Result

The result (avg_filt) is plotted as an orange line on the chart. It updates on each bar (depending on the current timeframe you're viewing) but the underlying data is based on the last 14 daily candles.

pinescript

Копировать

Редактировать

plot(avg_filt, title="Filtered ADR", color=color.orange, linewidth=2)

✅ Use Case

This script is useful for traders who use the Average Daily Range (ADR) to:

Estimate expected price movement during a day

Set volatility-based stop-loss or take-profit levels

Identify days with unusually high or low volatility

By filtering out extreme values, it provides a more stable and reliable estimate of daily volatility.

GOYD📊 GOYD (Daily Average Percentage Change) Indicator

Created by: Emre Yavuz - @emreyavuz84

This indicator calculates and displays the average daily percentage change for each day of the week. It helps traders identify which days tend to be more volatile, offering valuable insights for timing strategies and market behavior analysis.

=================================================================================

🔧 How It Works

Daily Percentage Change Calculation:

For each candle, the indicator calculates the percentage change using the formula:

Percentage Change = (High - Low) / Low * 100

=================================================================================

Day-Based Data Collection:

The script stores the daily percentage changes in separate arrays for each day of the week:

Monday → mondayChanges

Tuesday → tuesdayChanges

...

Sunday → sundayChanges

================================================================================

Average Calculation:

For each day, the script calculates the average of all recorded percentage changes. This gives a historical view of how volatile each weekday tends to be.

=================================================================================

Visual Table Display:

A table is displayed in the top-right corner of the chart, showing:

Column 1: Day of the week

Column 2: Average percentage change for that day

=================================================================================

🎯 Use Cases

This indicator is useful for:

Weekly Volatility Analysis: Identify which days are historically more volatile.

Timing Strategies: Optimize entry/exit points based on day-specific behavior.

Data-Driven Decisions: Make informed choices using historical volatility trends.

================================================================================

🎨 Customization

The table color can be customized via the _tc input parameter.

The indicator is set to display directly on the chart (overlay=true).

If you find this indicator helpful, feel free to like, comment, or add it to your favorites. Your feedback is always appreciated! 📈

CCT Volatility Index📘 CCT Volatility Index

The CCT Volatility Index is a refined adaptation of the LS Volatility Index , originally presented by Brazilian traders Alexandre Wolwacz (Stormer), Fabrício Lorenz, and Fábio Figueiredo (Vlad) . This implementation respects the core logic of the original concept but introduces two important enhancements:

Bollinger Band Width Percentage (BBWP)

Average True Range (ATR)

These are incorporated into the traditional formula (price deviation from a moving average divided by historical volatility), producing a normalized and responsive oscillator.

🧠 Conceptual Summary

This is a volatility indicator, not a directional trend tool. It measures the degree of price dispersion and tension in the market. It can be applied in two primary contexts:

🔁 Reversal Scenarios

When the index approaches extreme levels (near 100), it may signal exhaustion of volatility and potential mean reversion, especially if price is far from the moving average (SMA21 by default).

📈 Trend Continuation

If price stays near the average and the index maintains an elevated or rising profile, it may suggest trend acceptance with ongoing momentum. In this case, volatility expansion aligns with continuation.

🎯 Strategy Guidelines

Trigger points may come from the index crossing its own moving average (white line), either as a breakout or via retest confirmation.

Overlay colors identify BBWP compression/expansion zones:

- Blue: BBWP is 2% above its historical mean.

- Red: BBWP is 98% above.

These zones can help identify breakout setups or mean-reverting conditions.

📊 Info Panel

The indicator includes a dynamic panel showing:

The current price

The moving average used as reference

The percentage deviation between them

This allows you to evaluate if the asset is currently "stretched" or "fair" under current volatility.

⚠️ Disclaimer

This tool is for educational and informational purposes only. It does not constitute investment advice and should not be used in isolation. Always combine it with other tools, market context, and proper risk management.

Killzones (UTC+3) by Roy⏰ Time-Based Division – Trading Quarters:

The trading day is divided into four main quarters, each reflecting distinct market behaviours:

Opo Finance Blog

Quarter Time (Israel Time) Description

Q1 16:30–18:30 Wall Street opening; highest volatility.

Q2 18:30–20:30 Continuation or correction of the opening move.

Q3 20:30–22:30 Quieter market; often characterized by consolidation.

Q4 22:30–24:00 Preparation for market close; potential breakouts or sharp movements.

This framework assists traders in anticipating market dynamics within each quarter, enhancing decision-making by aligning strategies with typical intraday patterns.

Dynamic Volatility EnvelopeDynamic Volatility Envelope: Indicator Overview

The Dynamic Volatility Envelope is an advanced, multi-faceted technical indicator designed to provide a comprehensive view of market trends, volatility, and potential future price movements. It centers around a customizable linear regression line, enveloped by dynamically adjusting volatility bands. The indicator offers rich visual feedback through gradient coloring, candle heatmaps, a background volatility pulse, and an on-chart trend strength meter.

Core Calculation Mechanism

Linear Regression Core :

-A central linear regression line is calculated based on a user-defined source (e.g., close, hl2) and lookback period.

-The regression line can be optionally smoothed using an Exponential Moving Average (EMA) to reduce noise.

-The slope of this regression line is continuously calculated to determine the current trend direction and strength.

Volatility Channel :

-Dynamic bands are plotted above and below a central basis line. This basis is typically the calculated regression line but shifts to an EMA in Keltner mode.

-The width of these bands is determined by market volatility, using one of three user-selectable modes:

ATR Mode : Bandwidth is a multiple of the Average True Range (ATR).