ATR Stop Loss BandsATR Stop Loss Bands Indicator

Overview

The ATR Stop Loss Bands indicator creates dynamic support and resistance levels based on the Average True Range (ATR), providing traders with volatility-adjusted price bands that can be used for stop loss placement and trend analysis.

How It Works

This indicator calculates two bands around the current closing price using the ATR value:

Upper Band: Close price + ATR value

Lower Band: Close price - ATR value

The bands automatically adjust to market volatility, expanding during volatile periods and contracting during calmer market conditions.

Key Features

Customizable ATR Period: Default 14-period length (adjustable from 1 to any desired value)

Multiple Smoothing Options: Choose from RMA (default), SMA, EMA, or WMA for ATR calculation

Dynamic Volatility Adjustment: Bands automatically adapt to current market volatility

Clean Visual Design: Gray bands that don't clutter your chart

Trading Applications

Stop Loss Placement: Use the bands as dynamic stop loss levels - long positions might use the lower band as a stop, while short positions could use the upper band

Volatility Assessment: Wide bands indicate high volatility periods, narrow bands suggest low volatility

Breakout Identification: Price movements beyond the bands may signal potential breakouts or trend changes

Support/Resistance Levels: The bands can act as dynamic support and resistance zones

Settings

Length: ATR calculation period (default: 14)

Smoothing: Method for ATR smoothing (RMA, SMA, EMA, or WMA)

Best Practices

Use in conjunction with other technical analysis tools for confirmation

Consider the overall trend direction when interpreting band breaks

Adjust the length parameter based on your trading timeframe and strategy

Remember that ATR bands are reactive, not predictive - they respond to price movements rather than forecasting them

This indicator is particularly useful for traders who want to incorporate market volatility into their risk management and entry/exit decisions.

Volatility

CM RSI-Stoch Hybrid D&K%CM RSI-Stoch Hybrid D&K% Indicator

The CM RSI-Stoch Hybrid D&K% Indicator is a sophisticated momentum and trend analysis tool that combines the Relative Strength Index (RSI), Stochastic %K, and %D into a single, cohesive signal, enhanced by dynamic volume weighting and customizable smoothing. Unlike standalone RSI or Stochastic indicators, this hybrid approach integrates multiple data points to reduce noise, filter false signals, and provide traders with a clearer, more actionable view of market dynamics. Designed for versatility, it’s suitable for day trading, swing trading, or long-term investing across stocks, forex, cryptocurrencies, and commodities.

Why This Indicator Is Unique

Traditional RSI measures momentum based on price changes, while Stochastic tracks price cycles relative to highs and lows. However, both can generate conflicting or noisy signals in volatile markets. The CM RSI-Stoch Hybrid D&K% addresses this by:

Merging Complementary Signals: It calculates a composite signal by averaging RSI, Stochastic %K, and %D, balancing momentum and cyclical insights to produce a smoother, more reliable indicator.

Volume-Weighted Context: A dynamic colour system adjusts the composite signal’s appearance based on volume surges, helping traders prioritize moves backed by strong market participation.

Customizable Smoothing: A user-defined moving average (SMA, EMA, or WMA) smooths the composite signal, allowing traders to adapt the indicator to their preferred timeframe or strategy. This unique combination reduces the lag and false positives common in individual indicators, offering a novel perspective on market momentum and reversals.

How It Works

The indicator operates through a multi-layered approach:

Composite Signal Calculation: The core feature is a composite line derived by averaging RSI (based on closing prices), Stochastic %K, and %D (calculated from price highs and lows). This fusion creates a balanced momentum signal that mitigates the limitations of each indicator, such as RSI’s sensitivity to price spikes or Stochastic’s tendency to oscillate in choppy markets.

Volume-Weighted Colouring: The composite line changes colour (navy for high volume, blue for normal) based on a comparison of current trading volume to a user-defined volume moving average. This highlights when momentum aligns with significant market activity, improving trade timing.

Customizable Moving Average: Traders can apply an SMA, EMA, or WMA to the composite signal, adjusting its sensitivity to suit scalping, swing trading, or trend-following strategies.

Overbought/Oversold Zones: User-defined thresholds for overbought and oversold conditions (based on RSI) are visually marked with semi-transparent red (overbought) and green (oversold) backgrounds, making it easy to spot potential reversals or continuation patterns.

Key Features

Hybrid Momentum Signal: Combines RSI, Stochastic %K, and %D into a single, noise-filtered line for enhanced clarity.

Volume-Driven Insights: Dynamically adjusts the composite line’s colour to reflect high-volume conditions, emphasizing significant market moves.

Flexible Smoothing: Choose from SMA, EMA, or WMA to tailor the indicator to your trading style.

Customizable Parameters: Adjust RSI length, Stochastic periods, volume MA length, and overbought/oversold thresholds to match any market or timeframe.

Clear Visuals: Displays RSI, Stochastic %K, %D, composite signal, and moving average in a single panel, with intuitive overbought/oversold zones.

How to Use It

Trend Confirmation: Monitor the composite signal relative to its moving average. A composite line above its MA suggests bullish momentum, while a line below indicates bearish momentum.

Reversal Opportunities: Use the overbought (red background) and oversold (green background) zones to identify potential reversals, especially when confirmed by high-volume signals (navy composite line).

Scalping and Swing Trading: Adjust RSI and Stochastic lengths for faster or slower signals, using the moving average to filter noise for precise entries and exits.

Cross-Market Application: Customize settings to suit the volatility of stocks, forex, crypto, or commodities, ensuring versatility across timeframes.

Hint - watch for the back ground to change colour to reflect oversold or overbought conditions and then watch for the composite signal line to cross the moving average and for the back ground colour to go. High volume (navy blue) would also then add to directional bias.

Why Traders Will Benefit

The CM RSI-Stoch Hybrid D&K% goes beyond traditional indicators by integrating RSI, Stochastic, and volume analysis into a unified system that reduces false signals and enhances decision-making. Its dynamic volume weighting and customizable options make it a powerful tool for traders seeking to navigate complex markets with confidence. Whether you’re scalping intraday moves or tracking long-term trends, this indicator provides a clear, actionable edge.

Note: Combine this indicator with proper risk management and complementary analysis tools. Past performance is not indicative of future results.

Full setup support will be given

Session Range ProjectionsSession Range Projections

Purpose & Concept:

Session Range Projections is a comprehensive trading tool that identifies and analyzes price ranges during user-defined time periods. The indicator visualizes high-probability reversal zones and profit targets by projecting Fibonacci levels from custom session ranges, making it ideal for traders who focus on time-based market structure analysis.

Key Features & Calculations:

1. Custom Time Range Analysis

- Define any time period for range calculation - from traditional sessions (Asian, London, NY) to custom periods like opening ranges, hourly ranges, or 4-hour blocks

- Automatically captures the highest and lowest prices within your specified timeframe

- Supports multiple timezone selections for global market analysis

- Flexible enough for intraday scalping ranges or longer-term swing trading setups

2. Premium & Discount Zones

- Automatically divides the range into premium (above 50%) and discount (below 50%) zones

- Visual differentiation helps identify institutional buying and selling areas

- Color-coded boxes clearly mark these critical price zones

3. Optimal Trade Entry (OTE) Zones

- Highlights the 79-89% retracement zone in premium territory

- Highlights the 11-21% retracement zone in discount territory

- These zones represent high-probability reversal areas based on institutional order flow concepts

4. Fibonacci Projections

- Projects 11 customizable Fibonacci extension levels from the range extremes

- Levels extend both above and below the range for symmetrical analysis

- Each level can be individually toggled and color-customized

- Default levels include common retracement ratios: -0.5, -1.0, -2.0, -2.33, -2.5, -3.0, -4.0, -4.5, -6.0, -7.0, -8.0

How to Use:

Set Your Time Range: Input your desired session start and end times (24-hour format)

Select Timezone: Choose the appropriate timezone for your trading session

Customize Display: Toggle various visual elements based on your preferences

Monitor Price Action: Watch for reactions at projected levels and OTE zones

Set Alerts: Configure sweep alerts for when price breaks above/below range extremes

Input Parameters Explained:

Time Range Settings

Range Start/End Hour & Minute: Define your analysis period

Time Zone: Ensure accurate session timing across different markets

Visual Settings

Range Box: Toggle the premium/discount zone visualization

Horizontal Lines: Customize high/low line appearance

Internal Range Levels: Show/hide equilibrium and OTE zones

Labels: Configure text display for key levels

Fibonacci Projections: Enable/disable extension levels

Display Settings

Historical Ranges: Show up to 10 previous session ranges

Alert Type: Choose between high sweep, low sweep, or both

Trading Applications:

Session-Based Trading: Analyze specific market sessions (Asian, London, New York, opening ranges, hourly ranges)

Reversal Trading: Identify high-probability reversal zones at OTE levels

Breakout/Reversal Trading: Monitor range breaks/reversals with built-in sweep alerts

Risk Management: Use Fibonacci projections as profit targets or rejection areas

Multi-Timeframe Analysis: Apply to any timeframe for various trading styles

Important Notes:

This indicator is for educational purposes only and should not be considered financial advice

Past performance does not guarantee future results

Always use proper risk management when trading

The indicator automatically manages historical data to maintain chart performance

ADR et %+Vol (ADR ou %)This indicator identifies breakout bars based on significant price movements combined with increased trading volume. It allows you to define breakout thresholds in two ways:

Key Features:

Threshold Method: Choose between:

Fixed Percentage (%): Specify an exact percentage move.

ADR-based (%): Utilize the Average Daily Range (ADR) multiplied by a factor of your choice.

ADR Calculation: Offers two distinct calculation methods to suit your trading style:

True Range (TR): Incorporates overnight gaps, making it ideal for swing trading.

High-Low (H-L): Purely intraday measure, suitable for day trading without gap consideration.

Timeframe Flexibility:

Select the desired timeframe for ADR calculation (e.g., Daily, Weekly, Hourly), providing flexibility to match your specific trading horizon.

Visual Signals:

Blue Bar Coloring: Highlights breakout candles clearly.

Blue Circle Markers: Signals bars with significant price movement accompanied by strong volume.

Information Display:

Shows the ADR percentage, selected timeframe, and calculation method directly on the chart (top-right), providing instant clarity about the current settings.

Usage Recommendations:

Use True Range ADR if you hold positions overnight or trade multi-day swings.

Opt for High-Low ADR if you're trading purely intraday and prefer simpler measures.

This versatile indicator is suited for both swing and intraday traders looking for reliable volatility measures combined with volume confirmation.

Daily ATR TrackerDaily ATR Tracker

The Daily ATR Tracker is a simple yet powerful tool designed to help traders monitor the daily price movement relative to the average daily range (ATR). This indicator provides an objective view of how much price has moved compared to its recent daily volatility.

🔎 Key Features:

Customizable ATR period (default 14 days)

Live calculation of the current day's price range

ATR value displayed in pips for clear reference

Percentage of ATR covered by the current day's range

Color-coded table for quick visual interpretation:

🟢 Green: less than 60% of ATR covered

🟠 Orange: 60% to 100% of ATR covered

🔴 Red: more than 100% of ATR covered

Alert condition when daily range exceeds 100% of the ATR average

Movable table position to fit your chart layout

🎯 Why use Daily ATR Tracker?

✅ Identify exhaustion zones: When price has already covered a large portion of its typical daily range, the odds of further strong movement may diminish, helping you to manage entries, exits, and risk.

✅ Objective daily bias: Get a quantitative sense of how "stretched" the market is in real time.

✅ Works with any timeframe: While designed for daily ranges, you can monitor intraday movements with this context in mind.

⚠️ Usage Note:

This tool does not provide buy or sell signals by itself. It is designed to complement your existing strategies by offering additional context regarding daily range exhaustion.

Rolling Z-Score Trend [QuantAlgo]🟢 Overview

The Rolling Z-Score Trend measures how far the current price deviates from its rolling mean in terms of standard deviations. It transforms price data into standardized scores to identify overbought and oversold conditions while tracking momentum shifts.

The indicator displays a Z-Score line showing price deviation from statistical norms, with background momentum columns showing the rate of change in these deviations. This helps traders and investors identify mean reversion opportunities and momentum shifts across different asset classes and timeframes.

🟢 How It Works

The indicator uses the Z-Score formula: Z = (X - μ) / σ, where X is the current closing price, μ is the rolling mean, and σ is the rolling standard deviation over a user-defined lookback period. This creates a dynamic baseline that adapts to changing market conditions and standardizes price movements for interpretation across different assets and volatility conditions. The raw Z-Score undergoes 3-period EMA smoothing to reduce noise while maintaining responsiveness to market signals.

Beyond the basic Z-Score calculation, the indicator measures the rate of change in Z-Score values between successive bars, displayed as background momentum columns. This momentum component shows acceleration and deceleration of statistical deviations. All calculations are processed through confirmation filters, displaying signals only on confirmed bars to reduce premature signals based on incomplete price action.

🟢 How to Use

1. Z-Score Interpretation and Threshold Zones

Positive Values (Above Zero) : Price trading above statistical mean, suggesting bullish momentum or potential overbought conditions

Negative Values (Below Zero) : Price trading below statistical mean, suggesting bearish momentum or potential oversold conditions

Zero Line Crosses : Signal transitions between statistical regimes and potential trend changes

Upper Threshold Zone : Area above entry threshold (default 1.5) indicating potential overbought conditions

Lower Threshold Zone : Area below negative entry threshold (default -1.5) indicating potential oversold conditions

Extreme Values (±2.0 or higher) : Statistically significant deviations that may indicate reversal opportunities

2. Momentum Background Analysis and Info Table

Green Columns : Accelerating positive momentum in Z-Score values

Red Columns : Accelerating negative momentum in Z-Score values

Column Height : Magnitude of momentum change between bars

Momentum Divergence : When columns contradict primary Z-Score direction, often signals impending reversals

Info Table : Displays real-time numerical values for both Z-Score and momentum, including trend direction indicators and bar-to-bar change calculations for position management

3. Preconfigured Settings

Default : Balanced performance across multiple timeframes and asset classes for general trading and medium-term position management.

Scalping : Responsive setup for ultra-short-term trading on 1-15 minute charts with frequent signals and increased sensitivity to quick price movements.

Swing Trading : Optimized for multi-day positions with noise filtering, focusing on larger price swings. Most effective on 1-4 hour and daily timeframes.

Trend Following : Maximum smoothing that prioritizes established trends over short-term volatility. Generates fewer signals for daily and weekly charts.

Bollinger Band Breakout With Volatility StoplossDetailed Explanation of the Bollinger Band Breakout With Volatility Stoploss System

Introduction

The "Bollinger Band Breakout With Volatility Stoploss" system is a trading strategy designed to exploit price volatility in financial markets using the Bollinger Bands indicator, a widely recognized tool developed by John Bollinger. This system adapts the traditional Bollinger Bands framework into a Volatility Breakout strategy, focusing on capturing significant price movements by leveraging customized parameters and precise trading rules. The system operates exclusively on long positions, employs a daily timeframe, and incorporates dynamic risk management techniques to optimize trade outcomes while preserving capital.

System Parameters

The system modifies the standard Bollinger Bands configuration to suit its breakout methodology:

Standard Deviation (SD): Set to 1x, determining the width of the bands relative to the central moving average. This tighter setting enhances sensitivity to price movements, making the system responsive to smaller volatility shifts compared to the conventional 2x SD.

Period: A 30-day (1-month) lookback period is used to calculate the bands, providing a balance between capturing medium-term price trends and avoiding excessive noise from shorter timeframes.

Moving Average Type: The system uses an Exponential Moving Average (EMA) instead of the Simple Moving Average (SMA). The EMA places greater weight on recent price data, making it more responsive to current market conditions and better suited for detecting breakout opportunities in dynamic markets.

Core Concept

The Bollinger Band Breakout system is built on the principle of Volatility Breakout, which seeks to capitalize on significant price movements when the price breaks out of a defined volatility range. The Bollinger Bands, consisting of an EMA as the central line and two bands (Upper and Lower) calculated as the EMA plus or minus 1x SD, define this range. The system operates on a Daily Chart (D) timeframe, making it suitable for traders who prefer analyzing and executing trades based on daily price action. By focusing solely on Long Positions (buying low and selling high), the system avoids short-selling, aligning with strategies that capitalize on upward price momentum.

The core idea is to use the 1x SD multiplier over a 30-day period to establish a dynamic price range that reflects recent market volatility. Breakouts above the Upper Band signal potential buying opportunities, while penetrations below the Lower Band indicate exits, ensuring trades are aligned with significant price movements.

Trading Signals

The system generates clear entry and exit signals based on price interactions with the Bollinger Bands:

Buy Signal: A buy signal is triggered when the closing price of a daily candle exceeds the Upper Bollinger Band (EMA + 1x SD over 30 days). The trade is entered at the opening price of the subsequent candle, ensuring the breakout is confirmed by the close of the prior day. This approach minimizes false signals by waiting for a definitive breach of the volatility threshold.

Sell Signal: A sell signal occurs when the closing price falls below the Lower Bollinger Band (EMA - 1x SD over 30 days). The position is exited at the opening price of the next candle, allowing the trader to lock in profits or limit losses when the price reverses or loses momentum.

Risk Management

Risk management is a cornerstone of the system, ensuring capital preservation and disciplined trade execution:

Initial Stoploss: The stoploss is set at the Lower Bollinger Band of the candle that triggered the buy signal. This level acts as a volatility-based threshold, below which the trade is deemed invalid, prompting an immediate exit to protect capital. Traders have two options for implementing the stoploss:

Pending Stoploss: A predefined stoploss order placed at the Lower Band level.

Conditional Exit: Using the sell signal condition (price closing below the Lower Band) as the exit trigger, effectively aligning the stoploss with the system’s exit rules.

Position Sizing: The system employs Fixed Fractional Position Sizing with a risk per trade capped at 3% of the account balance. The position size is calculated based on the distance between the entry price and the Initial Stoploss, incorporating Volatility Position Sizing. This method adjusts the trade size according to the market’s volatility, ensuring that risk remains consistent across varying market conditions. Two options are available for managing capital:

Gear Up Option: Profits from previous trades are reinvested into the account’s capital, increasing the base for calculating the next position size. This compounding approach can amplify returns but also increases risk exposure.

Fixed Equity Option: Profits from previous trades are withdrawn, and only the remaining capital is used for calculating the next position size. This conservative approach prioritizes capital preservation by not compounding gains.

Trailing Stop: The system uses the Lower Bollinger Band as a dynamic trailing stop, which adjusts with price movements and volatility. This ensures that profits are protected during favorable trends while allowing the trade to remain open as long as the price stays above the Lower Band. The trailing stop aligns with the sell signal condition, maintaining consistency in the system’s exit strategy.

Supporting Indicators

The system incorporates two additional indicators to enhance market analysis and decision-making:

Bollinger Band Width (BBW): BBW measures the distance between the Upper and Lower Bollinger Bands relative to the EMA, serving as a proxy for market volatility.

A high BBW indicates significant price volatility, often associated with strong trends or large price movements, which may confirm the strength of a breakout.

A low BBW suggests low volatility, potentially signaling a period of consolidation or "squeeze" that could precede a breakout. This can help traders anticipate potential trade setups.

The BBW calculation uses the EMA to maintain consistency with the system’s core parameters.

Bollinger Band Ratio (BBR) or %B: BBR measures the price’s position relative to the Bollinger Bands, providing insight into market conditions.

BBR > 1: The price is above the Upper Band, indicating potential overbought conditions or strong upward momentum, which aligns with the system’s buy signal.

BBR < 0: The price is below the Lower Band, suggesting oversold conditions or downward momentum, corresponding to the sell signal or stoploss trigger.

BBR between 0 and 1: The price is within the bands, indicating a neutral state where no immediate action is required.

Like BBW, BBR is calculated using the EMA for consistency.

Backtesting and Implementation

To evaluate the system’s performance, traders can utilize the Backtest Parameter function, which allows for testing the strategy across user-defined time periods. This feature enables traders to assess the system’s effectiveness under various market conditions, optimize parameters, and refine their approach based on historical data.

Conclusion

The Bollinger Band Breakout With Volatility Stoploss system is a robust, volatility-driven trading strategy that combines the predictive power of Bollinger Bands with disciplined risk management. By focusing on long positions, using a 1x SD multiplier, and incorporating EMA-based calculations, the system is designed to capture significant price breakouts while minimizing risk through dynamic stoplosses and volatility-adjusted position sizing. The inclusion of BBW and BBR indicators provides additional context for assessing market conditions, enhancing the trader’s ability to make informed decisions. With its structured approach and backtesting capabilities, this system is well-suited for traders seeking a systematic, data-driven method to trade in volatile markets.

Liquidity Hunter HeatmapLiquidity Hunter (GPS Companion Tool)

Liquidity Hunter is a specialized script designed to help traders visualize and track potential liquidation zones, clusters, and imbalance traps in real-time. It is particularly useful for scalpers and short-term traders who rely on liquidity sweeps, stop hunts, and reversion plays.

This tool does not replicate open-source liquidation trackers. Instead, it uses a proprietary combination of volume surges, candle displacement, VWAP deviation, and high-timeframe wicks to infer areas of trapped traders and display them with clear, color-coded markers.

Key Features:

• Real-Time Liquidation Estimates: Detects where major stop losses (and potential liquidations) may have occurred, based on proprietary volume + price action logic.

• Cluster Strength Bubbles: Visual bubbles (scaled by cluster size) show where liquidations are stacking. Purple for bearish, white for bullish — intensity reflects strength.

• Pre-Liquidation Warning Zones: Highlights areas where price is likely to sweep liquidity before reversing, helping traders avoid chasing moves.

• Dollar-Based Labels (Optional): Displays the estimated value liquidated, helping traders size the significance of a move (e.g., $8.4M).

• Minimal Clutter Mode: Designed for intraday clarity — hides excess lines and uses bubbles, not shapes, for cleaner visualization.

Consolidation Zones[RanaAlgo]Overview

This indicator helps traders identify price consolidation zones (ranges) and potential breakouts in the market. It is useful for spotting periods of low volatility before significant price movements.

How It Works

Detects Consolidation Zones

Uses the ADX (Average Directional Index) to determine when the market is in a consolidation phase .

When ADX is below the threshold , the indicator marks the start of a consolidation zone.

Draws a semi-transparent box around the price range, adjusting its height as new highs/lows form.

Tracks Breakouts

When price breaks above/below the consolidation box, it signals a potential trend continuation.

Displays breakout arrows/labels (configurable shape & style) when price exits the range.

Visual Features

Boxes highlight consolidation areas (customizable color, border, and style).

Labels show real-time status ("CONSOLIDATING" or "TRENDING").

Breakout signals appear as arrows or shapes (up/down).

Usefulness in Trading

Range Trading: Helps traders identify sideways markets for buying low and selling high.

Breakout Trading: Signals potential trend entries when price exits consolidation.

Trend Confirmation: Low ADX + consolidation box = weak trend; breakout = possible trend start.

Example: If price stays in a blue box (consolidation) and then breaks above with an arrow, it suggests a bullish move.

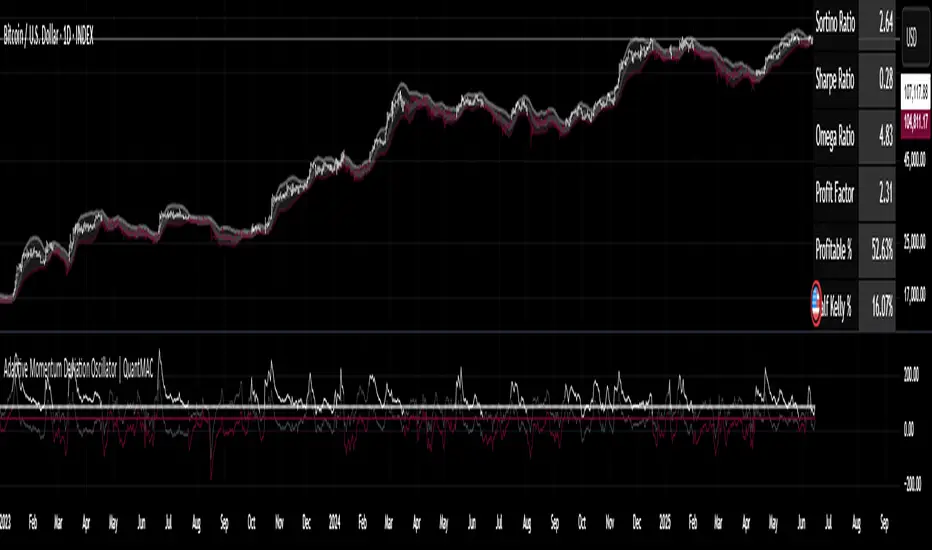

Adaptive Momentum Deviation Oscillator | QuantMACAdaptive Momentum Deviation Oscillator | QuantMAC 📊

Overview 🎯

The Adaptive Momentum Deviation Oscillator (AMDO) is an advanced technical analysis indicator that combines the power of Bollinger Bands with adaptive momentum calculations to identify optimal entry and exit points in financial markets. This sophisticated oscillator creates dynamic bands that adapt to market volatility while providing clear visual signals for both trending and ranging market conditions.

How It Works 🔧

Core Methodology

The AMDO employs a sophisticated multi-layered approach to market analysis through four distinct phases:

Bollinger Band Foundation : The indicator begins by establishing a volatility baseline using traditional Bollinger Bands. These bands are calculated using a simple moving average as the center line, with upper and lower bands positioned at a specific number of standard deviations away from this centerline. The distance between these bands expands and contracts based on market volatility, creating a dynamic envelope around price action.

BB% Normalization Process : The raw price data is then transformed into a normalized percentage format that represents where the current price sits within the Bollinger Band envelope. When price is at the lower band, this percentage reads 0%; at the upper band, it reads 100%. This normalization allows for consistent comparison across different timeframes and price levels, creating a standardized oscillator that oscillates between extreme values.

Adaptive Momentum Band Construction : The normalized BB% values undergo a secondary volatility analysis where their own standard deviation is calculated over a specified period. This creates "bands around the bands" - upper and lower boundaries that adapt to the volatility of the normalized price position itself. These adaptive bands expand during periods of high momentum volatility and contract during consolidation phases.

Intelligent Signal Synthesis : The final layer combines the adaptive momentum bands with user-defined threshold levels to create a sophisticated trigger system. The indicator monitors when the dynamic bands cross above or below these thresholds, filtering out noise while capturing significant momentum shifts. This creates a dual-confirmation system where both volatility adaptation and threshold breaches must align for signal generation.

Key Components 🛠️

Adaptive Momentum Bands 📈

Dynamic Volatility Response : These bands automatically widen during periods of high momentum volatility and narrow during consolidation phases. Unlike fixed oscillator boundaries, they continuously recalibrate based on recent price behavior within the Bollinger Band framework.

Dual-Layer Calculation : The bands are derived from the volatility of the normalized price position itself, creating a "volatility of volatility" measurement. This provides early warning signals when momentum characteristics are changing, even before price breakouts occur.

State-Aware Visualization : The bands employ intelligent color coding that transitions between active and neutral states based on their interaction with threshold levels. Active states indicate high-probability momentum conditions, while neutral states suggest consolidation or indecision.

Momentum Persistence Tracking : The bands maintain memory of recent momentum characteristics, allowing them to distinguish between genuine momentum shifts and temporary price spikes or dips.

Threshold Levels 🎚️

Statistical Significance Boundaries : The threshold levels (default 83 for long, 40 for short) are positioned to capture statistically significant momentum events while filtering out market noise. These levels represent points where momentum probability shifts meaningfully in favor of directional moves.

Asymmetric Design Philosophy : The intentional asymmetry between long and short thresholds (83 vs 40) reflects the natural upward bias of many financial markets and the different risk/reward profiles of long versus short positions.

Contextual Sensitivity : The thresholds work in conjunction with the adaptive bands to create context-sensitive triggers. A threshold breach is only meaningful when it occurs in the proper sequence with band interactions.

Risk-Adjusted Positioning : The threshold levels are calibrated to provide favorable risk-adjusted entry points, considering both the probability of success and the potential magnitude of subsequent moves.

Bollinger Bands Overlay 📊

Multi-Timeframe Context : The price chart overlay provides essential context by showing traditional Bollinger Bands alongside the oscillator. This dual perspective allows traders to see both the absolute price position and the momentum characteristics simultaneously.

Support/Resistance Identification : The filled band area creates a visual representation of dynamic support and resistance levels. Price interaction with these bands provides additional confirmation for oscillator signals.

Volatility Environment Assessment : The width and slope of the bands offer immediate visual feedback about the current volatility environment, helping traders adjust their expectations and risk management accordingly.

Confluence Analysis : The overlay enables traders to identify confluence between price action at Bollinger Band levels and oscillator signals, creating higher-probability trade setups.

Signal Generation ⚡

The AMDO generates signals through precise mathematical crossover events:

Long Signals 🟢

Momentum Accumulation Detection : Long signals are generated when the lower adaptive momentum band crosses above the 83 threshold, indicating that downside momentum has exhausted and bullish momentum is beginning to accumulate. This represents a shift from defensive to offensive market posture.

Statistical Edge Confirmation : The crossing event occurs only when momentum characteristics have shifted sufficiently to provide a statistical edge for long positions. The adaptive nature ensures the signal quality remains consistent across different market volatility regimes.

Visual State Synchronization : Upon signal generation, the entire indicator ecosystem shifts to a bullish state - bar colors change, band states update, and the visual hierarchy emphasizes the long bias until conditions change.

Momentum Persistence Validation : The signal incorporates momentum persistence analysis to distinguish between genuine trend starts and false breakouts, reducing whipsaw trades in choppy market conditions.

Short Signals 🔴

Momentum Exhaustion Recognition : Short signals trigger when the upper adaptive momentum band crosses below the 40 threshold, signaling that bullish momentum has peaked and bearish momentum is emerging. This asymmetric threshold reflects the different dynamics of bullish versus bearish market phases.

Volatility-Adjusted Timing : The adaptive band system ensures that short signals are generated with appropriate timing regardless of the underlying volatility environment, maintaining signal quality in both high and low volatility conditions.

Regime-Aware Activation : Short signals are only active in Long/Short trading mode, recognizing that not all trading strategies benefit from short positions. The indicator adapts its behavior based on the selected trading approach.

Risk-Calibrated Thresholds : The 40 threshold is specifically calibrated to capture meaningful bearish momentum shifts while accounting for the higher risk typically associated with short positions.

Cash Signals 💰

Defensive Positioning Logic : In Long/Cash mode, cash signals are generated when short conditions are met, allowing traders to move to a defensive cash position rather than taking on short exposure. This preserves capital during unfavorable market conditions.

Risk Mitigation Strategy : Cash signals represent a risk-off approach that removes market exposure when momentum conditions favor the short side, protecting long-biased portfolios from adverse market movements.

Opportunity Cost Optimization : The cash position allows traders to avoid negative returns while maintaining flexibility to re-enter long positions when momentum conditions improve, optimizing the risk-adjusted return profile.

Features & Customization ⚙️

Color Schemes 🎨

9 pre-built color schemes (Classic through Classic9)

Custom color override option

Dynamic color changes based on signal states

Trading Modes 📈

Long/Short : Full bidirectional trading capability

Long/Cash : Long-only strategy with cash positions

Performance Metrics 📊

The indicator includes a comprehensive suite of advanced performance analytics that provide deep insights into strategy effectiveness:

Risk-Adjusted Return Metrics

Sortino Ratio : Measures returns relative to downside deviation only, providing a more accurate assessment of risk-adjusted performance by focusing on harmful volatility rather than total volatility. This metric is particularly valuable for asymmetric return distributions.

Sharpe Ratio : Calculates excess return per unit of total risk, offering a standardized measure of risk-adjusted performance that allows for comparison across different strategies and timeframes.

Omega Ratio : Employs probability-weighted analysis to compare the likelihood and magnitude of gains versus losses, providing insights into the overall shape of the return distribution and tail risk characteristics.

Drawdown and Risk Analysis

Maximum Drawdown : Tracks the largest peak-to-trough equity decline, providing crucial information about the worst-case scenario and helping traders understand the emotional and financial stress they might encounter.

Dynamic Drawdown Monitoring : Continuously updates drawdown calculations in real-time, allowing traders to monitor current drawdown levels relative to historical maximums.

Trade Statistics and Profitability

Profit Factor Analysis : Compares gross profits to gross losses, revealing the efficiency of the trading approach and the relationship between winning and losing trades.

Win Rate Calculation : Provides the percentage of profitable trades, which must be interpreted in conjunction with profit factor and average trade size for meaningful analysis.

Trade Frequency Tracking : Monitors total trade count to assess strategy turnover and transaction cost implications.

Position Sizing Guidance

Half Kelly Percentage : Calculates optimal position sizing based on Kelly Criterion methodology, then applies a conservative 50% reduction to account for parameter uncertainty and reduce volatility. This provides mathematically-based position sizing guidance that balances growth with risk management.

Parameters & Settings 🔧

BMD Settings

- Base Length : Period for Bollinger Band calculation (default: 10)

- Source : Price data source (default: close)

- Standard Deviation Length : Period for volatility calculation (default: 35)

- SD Multiplier : Bollinger Band width multiplier (default: 1.0)

- BB% Multiplier : Scaling factor for BB% calculation (default: 100)

BMD Settings

Base Length : Period for Bollinger Band calculation (default: 10)

Source : Price data source (default: close)

Standard Deviation Length : Period for volatility calculation (default: 35)

SD Multiplier : Bollinger Band width multiplier (default: 1.0)

BB% Multiplier : Scaling factor for BB% calculation (default: 100)

Signal Thresholds 🎯

Long Threshold : Trigger level for long signals (default: 83)

Short Threshold : Trigger level for short signals (default: 40)

Display Options 🖥️

Toggleable metrics table with 6 position options

Customizable date range limiter

Multiple visual elements for comprehensive analysis

Use Cases & Applications 💡

Trend Following

Identifies momentum shifts in trending markets

Provides early entry signals during trend continuations

Adaptive bands adjust to changing volatility conditions

Mean Reversion

Detects oversold/overbought conditions

Signals potential reversal points

Works effectively in ranging markets

Risk Management

Built-in performance metrics for strategy evaluation

Half Kelly percentage for position sizing guidance

Maximum drawdown monitoring

Advantages ✅

Adaptive Nature : Automatically adjusts to market volatility

Dual Display : Oscillator and price chart components work together

Comprehensive Metrics : Built-in performance analysis

Flexible Trading Modes : Supports different trading strategies

Visual Clarity : Color-coded signals and states

Customizable : Extensive parameter adjustment options

Important Considerations ⚠️

This indicator is designed for educational and analysis purposes

Should be used in conjunction with other technical analysis tools

Proper risk management is essential when trading

Backtest thoroughly before implementing in live trading

Market conditions can change rapidly, affecting indicator performance

Disclaimer ⚠️

Past performance is not indicative of future results. Trading involves substantial risk of loss and is not suitable for all investors. The information provided by this indicator should not be considered as financial advice. Always conduct your own research.

No indicator guarantees profitable trades - Always use proper risk management! 🛡️

Daily Bias on 5 minutes Reversal StrategyThis strategy combines higher-timeframe bias (daily and 1-hour) with 5-minute reversal signals to identify intraday trades. It aims to capitalize on false breakouts of the previous day's high/low, with strict risk management (Strict position sizing, max risk cap, and R:R enforcement), Avoids Over-Trading (1 trade/day rule prevents chasing), SL buffer adapts to volatility.

#1. This strategy does not utilize indicators. We will use the daily (D) price range and look for breakout attempts and rejections at the extreme points on the lower time frame (1h). If rejection occurs, it establishes our bias (bullish or bearish). For final confirmation, we move to the 5-minute timeframe to observe attempts to retest that daily price range. If significant rejection occurs again, that becomes our entry point.

#2. When rejection occurs, the 1-hour candle may form a new extreme point (low/high). Therefore, we will no longer use the daily price range as our trade exit point but instead the new extreme level established after the breakout attempt and price rejection.

To prevent premature trade exits, we also add an SL buffer using ATR while still capping the maximum acceptable risk per trade (as a percentage). Take profit is calculated using a risk-to-reward ratio, with a default setting of 1.5x.

#3. Key Input Parameters

a. Timeframes :

1. Daily TF ((Anchor for daily high/low (default: D).)

2. 1H Bias TF (Bias confirmation timeframe (default: 60))

3. Execution TF (Entry signal timeframe (default: 5, should match chart).

b. Trade Management

1. SL Buffer ATR Multiplier (Buffer beyond swing low/high (default: 6.0))

2. Min ATR Threshold (Minimum buffer size (default: 1.0))

3. Risk Reward Ratio (TP distance multiplier (default: 1.5))

4. Max Risk Allowed (Max risk % of entry (default: 3.0%))

Lookback Bars for SL Bars for swing low/high (default: 60))

c. Break Thresholds

1. 1H Candle Break Threshold (ATR multiplier for 1H break (default: 0.75))

2. 5M Candle Break Threshold (ATR multiplier for 5M break (default: 0.5))

Improved Historical Volatility Calculator (No Options)Improved Historical Volatility Calculator (No Options)

Description

The "Improved Historical Volatility Calculator (No Options)" is a Pine Script indicator designed to calculate the historical volatility (HV) of assets without relying on options data. This tool is particularly useful for markets like forex, indices, or stocks where options trading might be limited or unavailable. It provides a customizable way to measure volatility based on historical price movements, with options to adjust the calculation period, trading days per year, and use an exponentially weighted moving average (EWMA) for enhanced sensitivity to recent data.

This indicator can be used standalone to visualize volatility trends or integrated with other scripts (e.g., option pricing models) to provide a manual input for implied volatility (IV).

Features

Customizable Period: Adjust the number of days (5 to 365) for volatility calculation.

Flexible Annualization: Set the number of trading days per year (default 252) to suit different markets (e.g., 365 for forex).

EWMA Option: Toggle between standard deviation and EWMA for a more responsive volatility measure.

Trend Adjustment: Removes the influence of price trends using an EMA-based detrending method.

Visual Output: Displays volatility as a histogram and labels the latest value on the chart.

How to Use

Add the Indicator: Load the indicator onto your chart via the Pine Script editor or the Indicators menu.

Configure Settings:

Period for Calculation: Set the lookback period (e.g., 30 days) to calculate volatility.

Trading Days per Year: Adjust for your market (e.g., 252 for stocks, 365 for continuous markets).

Use EWMA: Enable for a weighted approach focusing on recent volatility.

Interpret the Results: The histogram shows volatility in decimal form (e.g., 0.03136 = 3.136%), and the label displays the percentage on the last bar.

Integration: Use the calculated volatility value (in decimal form) as a manual IV input in other scripts, such as option pricing models.

Example

For the DXY index, with a 60-day period and 252 trading days per year, the indicator might output a volatility of 0.03136 (3.136%). You can input this value into an options model to estimate standard deviation levels, adjusting for the days to expiry.

Notes

Accuracy: The indicator provides a reliable estimate of historical volatility, with improvements like trend removal and EWMA. For precision, use a period that matches your trading horizon (e.g., 30-90 days).

Limitations: Volatility is based on historical data and may not reflect future market conditions or implied volatility from options.

Compatibility: Tested on TradingView as of June 16, 2025. Ensure sufficient historical data is available for the chosen period.

Suggestions

Increase the period for volatile assets to smooth out noise.

Share feedback or request enhancements in the comments!

Momentum Candle by Sekolah Trading## 🔷 Introduction

**Momentum Candle by Sekolah Trading** is a proprietary price action tool that identifies high-conviction candles with large bodies and minimal wicks, based on dynamically adjusted thresholds tailored to each pair and timeframe. This script helps traders recognize moments of price acceleration that often precede breakouts, trend continuation, or sharp reversals.

---

## 🔷 What Makes This Script Unique (Originality & Utility)

Unlike traditional candle filters that rely on static size comparisons, this indicator uses:

- **Instrument-specific pip sensitivity**: Automatically detects if the pair is XAUUSD, JPY-based, or other Forex instruments.

- **Timeframe-based calibration**: Adjusts body size thresholds dynamically for 5m, 15m, 30m, and 1h.

- **Wick ratio control**: Validates only candles with short wicks (<30%), filtering indecisive moves.

- **Non-repainting logic**: Signals appear after candle close, with no future data lookahead.

This logic has been tested and refined internally by **Sekolah Trading**, designed for scalpers and intraday traders who rely on clean price action structure.

---

## 🔷 How It Works

1. **Pair & Timeframe Detection**

Adjusts `minRange` dynamically based on:

- Gold (XAUUSD), JPY pairs, or other Forex

- Timeframe: 5m to 1h

2. **Candle Structure Analysis**

- Calculates body = `abs(open - close)`

- Wick = `upper + lower shadows`

- Valid only if wick is under 30% of total candle

3. **Conditions for Signal**

- Body ≥ minRange

- Wick ≤ 30%

- Clear bullish or bearish direction

4. **Plots**

- 🔺 Blue triangle = Bullish momentum candle

- 🔻 Red triangle = Bearish momentum candle

---

## 🔷 How to Use

1. **Add to any 5m–1h chart**, ideally on XAUUSD or major Forex pairs

2. **Wait for signal triangle** to appear at the close of a candle

3. Use with:

- Trend indicators (MA, Supertrend, etc.)

- Support/resistance zones

- Breakout levels

4. **Set alerts** using:

`Momentum Candle (Body)`

---

## 🔷 Why This Script is Closed-Source

This indicator includes proprietary logic created by **Sekolah Trading** for professional and community use:

- Original dynamic pip sensitivity calibration

- Custom multi-condition filtering

- Non-reused, non-public logic with adaptive precision

The source is protected to prevent unauthorized duplication. However, all relevant logic and intent have been clearly explained above as required by TradingView’s House Rules.

---

## 🔷 Disclaimer

This indicator does not provide financial advice or guaranteed signals. Always combine with your own analysis and risk management. Historical performance does not guarantee future results.

---

## 🔷 Suggested Tags

`momentum`, `price action`, `breakout`, `forex`, `xauusd`, `jpy`, `scalping`, `candle`, `non-repainting`, `trend confirmation`

Adaptive Multi-MA OptimizerAdaptive Multi-MA Optimizer

This indicator provides a powerful, customizable solution for traders seeking dynamically optimized moving averages with precision and control. It integrates multiple custom-built moving average types, applies real-time volatility-based optimization, and includes an optional composite smoothing engine.

🧠 Key Features

Dynamic Optimization:

Automatically selects the optimal lookback length based on market volatility stability using a custom standard deviation differential model.

Multiple Custom MA Types:

Includes fully custom implementations of:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

VWMA (Volume Weighted MA)

DEMA (Double EMA)

TEMA (Triple EMA)

Hull MA

ALMA (Arnaud Legoux MA)

Composite MA Option:

A unique "Composite" mode blends all supported MAs into a single average, then applies optional smoothing for enhanced signal clarity.

Dynamic Smoothing:

The composite mode supports volatility-adjusted smoothing (based on optimized lookback), making it adaptable to different market regimes.

Fully Custom Logic:

No built-in MA functions are used — every moving average is hand-coded for transparency and educational value.

⚙️ How It Works

Optimization:

The script evaluates a range of lengths (minLen to maxLen) using the standard deviation of price returns. It selects the length with the most stable recent volatility profile.

Calculation:

The selected MA type is calculated using that optimized length. If "Composite" is chosen, all MA types are averaged and smoothed dynamically.

Visualization:

The adaptive MA is plotted on the chart, changing color based on its position relative to price.

📌 Use Cases

Trend-following strategies that adapt to different market conditions.

Traders wanting a high-fidelity composite of multiple MAs.

Analysts interested in visualizing market smoothness without lag-heavy signals.

Coders looking to learn how to build custom indicators from scratch.

🧪 Inputs

MA Type: Choose from 8 MA types or a blended Composite.

Lookback Range: Control min/max and step size for optimization.

Source: Choose any price series (e.g., close, hl2).

⚠️ Disclaimer

This indicator is for educational and informational purposes only and does not constitute financial advice, trading advice, or investment recommendations. Use of this script is at your own risk. Past performance does not guarantee future results. Always perform your own analysis and consult with a qualified financial advisor before making trading decisions.

Dynamic Laguerre Filter Bands | OttoThis indicator combines trend-following and volatility analysis by enhancing the traditional Laguerre filter with a dynamic, volatility-adjusted band system. Instead of using fixed thresholds, the bands adapt in real-time to changing market conditions by applying smoothed standard deviation calculations. This design keeps the indicator responsive to significant price movements while effectively filtering out short-term market noise, resulting in more accurate trend identification and breakout signals.

Core Concept

The indicator is built around the following key components:

Laguerre Filter:

The Laguerre filter is designed to smooth out price data by reducing market noise while still being quick enough to detect real changes in price direction. Its goal is to create a clear, smooth trend line that helps traders/investors focus on the overall market trend without getting distracted by small, random price swings.

It uses a parameter called gamma to control how it balances smoothness and responsiveness:

A lower gamma gives more weight to recent price data, making the filter react faster to new price changes. This means the trend line is more sensitive but may also be less smooth and more prone to small fluctuations.

A higher gamma gives more weight to past price data, making the filter smoother and less sensitive to quick changes. This helps reduce noise and produces a steadier trend line, but it also introduces more lag, meaning the filter reacts slower to new price moves.

By adjusting gamma, the Laguerre filter lets you choose the balance between following price changes quickly and having a stable, noise-free trend signal.

Standard Deviation:

shows how much price varies from the mean. In this indicator, it’s used to measure market volatility.

Volatility Bands: The upper and lower bands are based on an EMA-smoothed standard deviation of price. The EMA reduces sudden jumps in volatility, creating smoother and more stable bands that still respond to changing market conditions. These bands are plotted around the Laguerre filter line, expanding and contracting in a controlled way to stay aligned with real market movement while avoiding short-term noise.

Signal Logic:

A long signal is triggered when the close price crosses above the upper band.

A short signal occurs when the close price falls below the lower band.

⚙️ Inputs

Source: Price source used in calculations

Gamma: Adjusts how much the Laguerre filter responds to price changes. Lower gamma values make the filter react more to recent prices, while higher values give more influence to older data, making the line smoother but slower to respond.

Volatility Length: Period used to calculate standard deviation

Volatility Smoothing Length: EMA smoothing length for standard deviation

Multiplier: Scales the width of the bands based on volatility

📈 Visual Output

Laguerre Filter Line: Plots the laguerre filter line, colored dynamically based on signal direction (green for bullish, purple for bearish)

Upper & Lower Bands: Volatility-based bands that adjust with market conditions. (green for bullish, purple for bearish)

Glow Effect: Optional glow layer to enhance visibility of the laguerre filter trend line (green for bullish, purple for bearish)

Bar Coloring: Candlesticks and bar colors reflect the active signal state for fast visual interpretation (green for bullish, purple for bearish)

How to Use

Apply the indicator to your chart and monitor for signal events:

Long Signal: When price closes above the upper band

Short Signal: When price closes below the lower band

🔔 Alerts

This indicator supports optional alert conditions you can enable for:

Long Signal: Close price crossing above the upper band

Short Signal: Close price crossing below the lower band

⚠️ Disclaimer:

This indicator is intended for educational and informational purposes only. Trading/investing involves risk, and past performance does not guarantee future results. Always test and evaluate indicators/strategies before applying them in live markets. Use at your own risk.

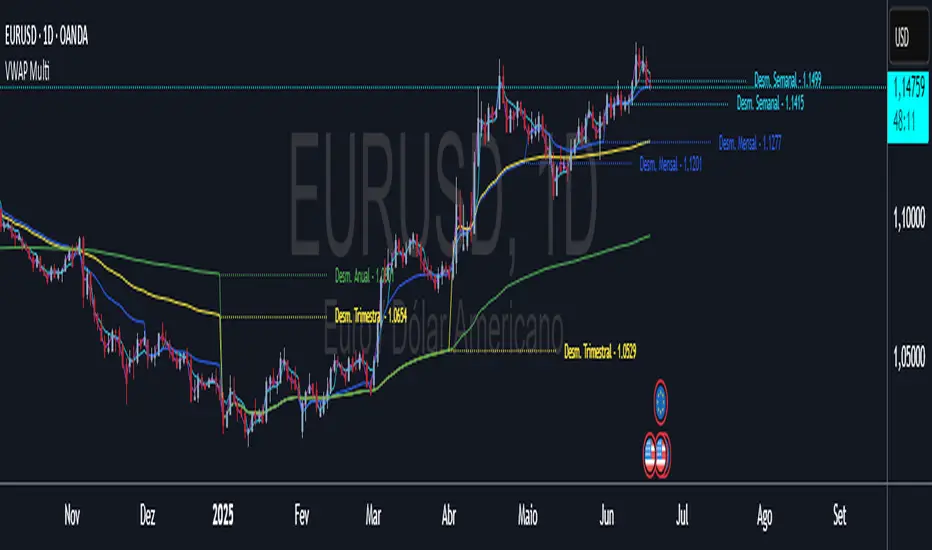

VWAP Multi-Timeframe VWAP Multi-Timeframe - Complete Professional Indicator

🚀 WHAT IS IT?

The VWAP Multi-Timeframe is an advanced indicator that combines 5 different VWAP periods in a single tool, providing a complete view of market fair value levels across multiple time scales.

⭐ KEY FEATURES

📊 5 Configurable VWAPs:

🟡 Daily VWAP - Ideal for day trading and intraday operations

🟠 Weekly VWAP - Perfect for swing trading

🔵 Monthly VWAP - Excellent for medium-term analysis

🔴 Quarterly VWAP - Essential for quarterly strategies

🟢 Yearly VWAP - Fundamental for long-term investments

🎯 Multiple Price Sources:

Choose the source that best fits your strategy:

Close - Closing price (most common)

OHLC4 - Complete average (smoother)

HLC3 - Typical price (default)

HL2 - Period midpoint

Open/High/Low - Specific prices

💡 HOW TO USE

For Day Traders:

Use Daily VWAP as main fair value reference

Prices above = buying pressure / Prices below = selling pressure

For Swing Traders:

Combine Weekly and Monthly VWAP to identify trends

Look for confluences between different timeframes

For Investors:

Quarterly and Yearly VWAP show long-term value levels

Excellent for identifying entry points in investments

🔧 TECHNICAL FEATURES

✅ Pine Script v6 - Latest and optimized version

✅ Clean Interface - User-friendly design

Adaptive Normalized Global Liquidity OscillatorAdaptive Normalized Global Liquidity Oscillator

A dynamic, non-repainting oscillator built on real central bank balance sheet data. This tool visualizes global liquidity shifts by aggregating monetary asset flows from the world’s most influential central banks.

🔍 What This Script Does:

Aggregates Global Liquidity:

Includes Federal Reserve (FED) assets and subtracts liabilities like the Treasury General Account (TGA) and Reverse Repo Facility (RRP), combined with asset positions from the ECB, BOJ, PBC, BOE, and over 10 other central banks. All data is normalized into USD using FX rates.

Adaptive Normalization:

Optimizes the lookback period dynamically based on rate-of-change stability—no fixed lengths, enabling adaptation across macro conditions.

Self-Optimizing Weighting:

Applies inverse standard deviation to balance raw liquidity, smoothed momentum (HMA), and standardized deviation from the mean.

Percentile-Ranked Highlights:

Liquidity readings are ranked relative to history—extremes are visually emphasized using gradient color and adaptive transparency.

Non-Repainting Design:

Data is anchored with bar index awareness and offset techniques, ensuring no forward-looking bias. What you see is what was known at that time.

⚠️ Important Interpretation Note:

This is not a zero-centered oscillator like RSI or MACD. The signal line does not represent neutrality at zero.

Instead, a dynamic baseline is calculated using a rolling mean of scaled liquidity.

0 is irrelevant on its own—true directional signals come from crosses above or below this adaptive baseline.

Even negative values may signal strength if they are rising above the moving average of past liquidity conditions.

✅ What to Watch For:

Crossover Above Dynamic Baseline:

Indicates liquidity is expanding relative to recent conditions—supports a risk-on interpretation.

Crossover Below Dynamic Baseline:

Suggests deteriorating liquidity conditions—may align with risk-off shifts.

Percentile Extremes:

Readings near the top or bottom historical percentiles can act as contrarian or confirmation signals, depending on momentum.

⚙️ How It Works:

Bounded Normalization:

The final oscillator is passed through a tanh function, keeping values within and reducing distortion.

Adaptive Transparency:

The strength of deviations dynamically adjusts plot intensity—visually highlighting stronger liquidity shifts.

Fully Customizable:

Toggle which banks are included, adjust dynamic optimization ranges, and control visual display options for plot and background layers.

🧠 How to Use:

Trend Confirmation:

Sustained rises in the oscillator above baseline suggest underlying monetary support for asset prices.

Macro Turning Points:

Reversals or divergences, especially near OB/OS zones, can foreshadow broader risk regime changes.

Visual Context:

Use the dynamic baseline to see if liquidity is supportive or suppressive relative to its own adaptive history.

📌 Disclaimer:

This indicator is for educational and informational purposes only. It does not constitute financial advice. Past performance is not indicative of future results. Always consult a qualified financial advisor before making trading or investment decisions.

Adaptive RSI Oscillator📌 Adaptive RSI Oscillator

This indicator transforms the classic RSI into a fully adaptive, self-optimizing oscillator — normalized between -1 and 1, dynamically smoothed, and enhanced with divergence detection.

🔧 Key Features

Self-Optimizing RSI: Automatically selects the optimal RSI lookback length based on return stability (no hardcoded periods).

Dynamic Smoothing: Adapts to market conditions using a fraction of the optimized length.

Normalized Output : Converts traditional RSI to a consistent scale across all assets and timeframes.

Divergence Detection: Compares RSI behavior vs. price percentile ranks and scales the signal accordingly.

Gradient Visualization: Color-coded background and plot lines reflect the strength and direction of the signal with soft transitions.

Neutral Zone Adaptation: Dynamically widens or narrows the zone of inaction based on volatility, reducing noise.

🎯 Use Cases

Identify extreme momentum zones without relying on fixed 70/30 RSI levels

Detect divergences early with adaptive filtering

Highlight potential exhaustion or continuation

⚠️ Disclaimer: This indicator is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security. Always conduct your own research and consult a licensed financial advisor before making investment decisions. Use at your own risk.

ATR % Line from Day LowHow can you make sure that you're not buying a stock that is too extended?

By limiting your buys to within a certain percentage of either the low-of-the-day (LoD) if you're going long, or to the high-of-the-day (HoD) if you're shorting a stock. This script will help you do just that.

Limiting stock purchases to within a certain percentage of the Average True Range (ATR) from the day's low or high is a risk management technique that offers several key benefits:

Risk Control and Position Sizing

By using ATR as a boundary, you're essentially creating a volatility-adjusted buffer. Since ATR measures recent price volatility, this approach prevents you from buying into stocks that have already moved significantly beyond their normal trading range. This helps avoid entering positions when the stock might be overextended and due for a pullback.

Improved Entry Timing

This strategy encourages patience and discipline. Rather than chasing a stock that's already run up substantially from its low, you wait for better entry points. For example, if you set a limit of 50% of ATR from the day's low, you're only buying when the stock hasn't moved more than half its typical daily range from the bottom.

Volatility Awareness

ATR naturally adjusts for each stock's individual volatility characteristics. A high-volatility stock might have an ATR of $2, while a low-volatility stock might have an ATR of $0.50. This approach scales your entry criteria appropriately for each security rather than using arbitrary dollar amounts.

Reduced Emotional Trading

Having a systematic rule removes the temptation to chase momentum or buy at poor technical levels. It forces you to wait for the stock to come back to more reasonable levels relative to its recent trading behavior.

Better Risk-Reward Ratios

By entering closer to the day's low (within your ATR percentage), you're typically getting a better risk-reward setup. Your stop loss (often placed below the day's low) will be tighter, while your potential upside remains intact.

This approach works particularly well for swing traders and those looking to enter positions on pullbacks or during consolidation periods rather than breakout scenarios.

To save valuable real estate on your chart, there's also an option that can give you a compact version of this indicator which will show only the "Current Day's Low/High" and "Target Price". "Target Price" being the price at which your max buy limit is based on the % ATR you choose in settings.

X-Day Capital Efficiency ScoreThis indicator helps identify the Most Profitable Movers for Your fixed Capital (ie, which assets offer the best average intraday profit potential for a fixed capital).

Unlike traditional volatility indicators (like ATR or % change), this script calculates how much real dollar profit you could have made each day over a custom lookback period — assuming you deployed your full capital into that ticker daily.

How it works:

Calculates the daily intraday range (high − low)

Filters for clean candles (where body > 60% of the candle range)

Assumes you invested the full amount of capital ($100K set as default) on each valid day

Computes an average daily profit score based on price action over the selected period (default set to 20 days)

Plots the score in dollars — higher = more efficient use of capital

Why It’s Useful:

Compare tickers based on real dollar return potential — not just % volatility

Spot low-priced, high-volatility stocks that are better suited for intraday or momentum trading

Inputs:

Capital ($): Amount you're hypothetically deploying (e.g., 100,000)

Look Back Period: Number of past days to average over (e.g., 20)

Haven Average Daily RangeOverview

This indicator is an enhanced version of the traditional ADR tool that adapts to intraday price movements. Unlike static ADR levels, this indicator dynamically adjusts its range boundaries based on real-time price action while maintaining the original ADR calculation framework.

Key Features

ADR calculation based on multiple periods (5, 10, and 20 days)

ADR levels displayed with automatic style changes upon range reach

Customizable display settings (color, line style)

Price labels for better visualization

The indicator helps traders assess the instrument's volatility, identify potential reversal zones, and plan daily trading targets.

Suitable for all timeframes up to D1 and any trading instrument.

How It Works

Session Start (UTC+0): Calculates ADR based on historical data and sets initial High/Low levels

Dynamic Phase: Monitors price action and adjusts the opposite boundary (ADR Low or High) when new extremes are reached.

When price creates new Day high price above the opening price, the ADR Low level moves upward proportionally.

When price creates new Day low price below the opening price, the ADR High level moves downward proportionally.

Completion Phase: Stops adjustments and highlights breach when price reaches either boundary

Trading Application

Entry and Exit Signals

The ADR boundaries serve as key decision points for trade execution. When price approaches the upper ADR boundary, it often signals a potential selling zone, particularly when confluence exists with other overbought indicators such as RSI divergence or resistance levels. Conversely, price reaching the lower ADR boundary frequently indicates potential buying opportunities, especially when supported by oversold conditions or support confluences.

Trend Continuation Assessment

One of the most valuable applications is gauging the probability of continued directional movement. When the current session's price action has not yet reached either ADR boundary, statistical probability favors trend continuation in the established direction. This information helps traders stay with profitable positions longer rather than exiting prematurely.

Reversal and Consolidation Zones

The visual color change to orange when ADR boundaries are reached provides immediate feedback that the normal daily range has been exhausted. At this point, the probability of trend reversal or sideways consolidation increases significantly. This signal helps traders prepare for potential position adjustments or new counter-trend opportunities.

[Smith] VWAP Deviation + VWAP Deviation +

Short Description:

Advanced VWAP indicator with deviation bands, smart signal filtering, and session-based performance tracking. Features log-space scaling, RSI confirmation, volume filters, and market regime detection.

Full Description:

The VWAP Deviation + is a comprehensive trading indicator that combines Volume Weighted Average Price (VWAP) analysis with advanced signal filtering to identify high-probability trade opportunities. This indicator goes beyond basic VWAP by incorporating multiple confirmation layers and intelligent market analysis.

🎯 Key Features

Core VWAP Analysis:

- Custom volume-weighted mean calculation with deviation bands (2σ and 3σ)

- Optional log-space scaling for proportional price movements

- Real-time VWAP line with customizable visibility

Smart Signal Detection:

- RSI confirmation for all trade signals

- Volume filter requiring above-average trading activity

- Market regime detection (trending vs ranging markets)

- Optional RSI divergence analysis

Advanced Filtering:

- Multi-condition signal validation

- Session-based performance tracking (Asian, London, NY)

- Real-time win rate calculation

- Strong vs regular signal classification

Visual Features:

- Clean, professional interface with customizable colors

- Optional signal shapes and annotations

- Performance statistics table

- Filled deviation bands for easy visualization

📊 How It Works

The indicator identifies trade opportunities when:

1. Price touches VWAP deviation bands (2σ or 3σ)

2. RSI confirms oversold/overbought conditions

3. Volume exceeds the specified threshold

4. Market regime conditions are favorable

Signal Types:

- LONG : Price at lower bands + RSI oversold + volume confirmation

- SHORT : Price at upper bands + RSI overbought + volume confirmation

- STRONG : Same conditions but at 3σ bands for higher conviction trades

⚙️ Customization Options

Core Settings:

- VWAP length and source selection

- Adjustable deviation multipliers

- Log-space scaling toggle

Signal Filters:

- RSI length and threshold levels

- Volume filter with customizable multiplier

- Market type filtering options

Advanced Features:

- Session statistics tracking

- RSI divergence detection

- Market regime analysis

Visual Controls:

- Show/hide individual components

- Custom color schemes

- Signal display toggles

🔔 Alert System

Built-in alerts for:

- Long and short trade opportunities

- Strong signal confirmations

- RSI divergence signals

💡 Best Practices

- Use higher timeframes (15m+) for more reliable signals

- Combine with additional confirmation indicators

- Pay attention to session statistics for timing optimization

- Monitor market regime indicators for context

This indicator is suitable for day traders, swing traders, and anyone looking to improve their VWAP-based trading strategies with advanced filtering and market analysis.

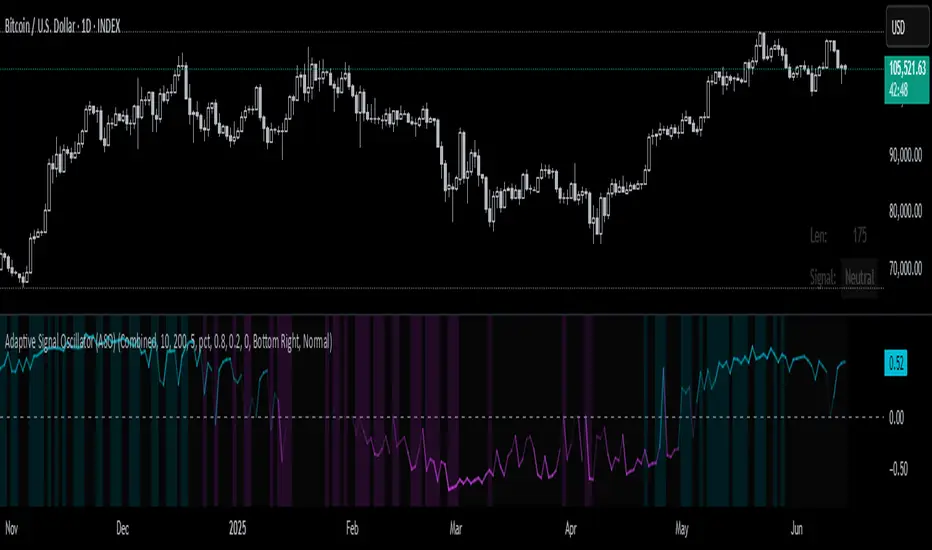

Adaptive Signal Oscillator (ASO)📘 Adaptive Signal Oscillator (ASO)

A fully dynamic, self-calibrating oscillator that adapts to any asset or timeframe by optimizing for real-time signal stability and volatility structure — without relying on static parameters or hardcoded thresholds.

🔍 Overview

The Adaptive Signal Oscillator (ASO) is a next-generation technical analysis tool designed to provide context-aware long/short signals across crypto, equities, or forex markets. Unlike traditional oscillators (RSI, Stochastics, MACD), ASO requires no manual tuning of lookback periods or overbought/oversold zones — it self-optimizes based on current market behavior.

🧠 How It Works

✅ 1. Dynamic Lookback Optimization

ASO evaluates a range of lookback lengths between user-defined minLen and maxLen. For each length, it calculates the standard deviation of returns and finds the one with the least volatility change (i.e., the most stable structure). This length is dynamically assigned as bestLen, recalculated on every bar.

✅ 2. Multi-Layer Signal Composition

Four independent signal layers are computed using bestLen:

RSI Layer: Measures relative price strength via a custom dynamic RSI.

Z-Score Layer: Standardized deviation of price from its mean.

Volatility Layer: Standard deviation of log or percent returns.

Price Position Layer: Current price percentile within the lookback window.

Each of these layers is transformed into a percentile score scaled to the range .

✅ 3. Volatility-Based Weighting

The standard deviation (volatility) of each signal layer is computed. Less volatile layers are weighted more heavily, ensuring the final composite signal prioritizes stable, consistent inputs.

Weights are normalized and combined to form a composite score, representing a dynamically blended, noise-weighted signal across the four layers.

✅ 4. Optional Adaptive Smoothing

A boolean toggle lets users apply smoothing to the final score. The smoothing window scales proportionally to bestLen, preserving adaptiveness even during trend transitions.

✅ 5. Percentile-Based Thresholding

Rather than using arbitrary fixed thresholds, ASO converts the composite score into a ranked percentile. Long/short signals are then generated based on user-defined percentile bands, adapting naturally to each asset’s behavior.

📈 Interpreting ASO

Score > Threshold → Strong long signal (highlighted in aqua).

Score < Threshold → Strong short signal (highlighted in fuchsia).

Crossing h_thresh (e.g., 0) → Neutral-to-bias change; useful for early trend cues.

The background and label update in real time to reflect the current regime and bestLen.

⚙️ Inputs

minLen, maxLen, step: Define the search range for optimal lookback length.

retMethod: Choose between log or percent return calculations.

threshHigh, threshLow: Define signal zones using percentiles.

smooth: Enable dynamic score smoothing.

h_thresh: Midline crossover zone for directional context.

⚠️ Disclaimer

This tool is designed for exploratory and educational purposes only. It does not offer financial advice or trading recommendations. Past performance is not indicative of future results.

Always consult a licensed financial advisor before making investment decisions.