Correction TerritoryA simple indicator showing how much percentage has been corrected since a recent highest high.

You can set 3 horizontal line to compare with past correction rates.

直近の最高値からの調整率を表示するインジケーターです。

過去の調整規模との比較のため、3本の水平線も設定可能です。

Breadth Indicators

Trending Bar SRTrending Bar SR is a simple script define a Bar called "Trending Bar".

Depend on direction of Trending Bar, if Trending Bar is UpTrend then this indicator plot Bar's Low Price as Support and if Trending Bar is DownTrend then it plot Bar's High Price as Resistance.

Beside, this indicaor also plot 4 levels retracement of Trending Bar for trading.

1. Define Trending Bar

1.1 Uptrend Bar

+ Close Price higher than previous High Price

+ Body greater than sum of shadows (up and down)

+ Color: A green dot is plotted at bottom chart.

1.2 Downtrend Bar

+ Close Price lower than previous Low Price

+ Body greater than sum of shadows (up and down)

+ Color: A red dot is plotted at bottom chart.

2. Retracement Level

+ Trending Bar Retracement 0.5 is called Equerium.

+ Trending Bar Retracement 0.618 is called Perfect Entry.

+ Trending Bar Retracement 0.705 is called Optimal Entry.

+ Trending Bar Retracement 0.79 is called Max Entry.

3. Trading

+ When Price crossed Equerium, consider open position at Perfect Entry, Optimal Entry with stoploss place at Max Entry.

+ If place order at Max Entry, stoploss can place at Support or Resistance.

VOLD-MarketBreadth-RatioThis script provides NASDAQ and NYSE Up Volume (volume in rising stocks) and Down Volume (volume in falling stocks) ratio. Up Volume is higher than Down Volume, then you would see green label with ratio e.g 3.5:1. This means Up Volume is 3.5 times higher than Down Volume - Positive Market Breadth. If Down Volume is higher than Up Volume, then you would see red label with ratio e.g -4.5:1. This means Down Volume is 4.5 times higher than Up Volume.

For example, ratio is 1:1, then it is considered Market Breadth is Neutral.

PS: Currently TradingView provides only NASDAQ Composite Market volume data. I have requested them to provide Primary NASDAQ volume data. If they respond with new ticket for primary NQ data, I will update the script and publish the updated version. So if you have got similar table on ToS, you would see minor difference in NQ ratio.

Intrabar OBV/PVTI got this idea from @fikira's script Intrabar-Price-Volume-Change-experimental

The indicator calculates OBV and PVT based on ticks. Since, the indicator relies on live ticks, it only starts execution after it is put on the charts. The script can be useful in analysing intraday buy and sell pressure. Details are color coded based on the values.

Data is presented in simple tabular format.

Formula for OBV and PVT can be found here:

www.investopedia.com

www.investopedia.com

Breadth Ratio BubblesBubbles for ADD thats shows ratios between up and down volumes for the NYSE and NASDAQ

Here Is The Bottom(VIX and Its MA Deviation Rate)I found a very interesting article on Bloomberg with the title “JP Morgan Strategists See Sure Fire Sign It Is Time to Buy Stocks”.

It says when VIX index far exceeds its 1 month MA by 50%, then stock prices rise later except recession period. This buying signals are almost 100% accurate and now is the time to buy stocks as the VIX met the condition on Jan25 this year, the article says.

I can’t post the URL of the article here as it violates TradingView house rules, so if you are interested, you just google it with the title.

Anyway, I have developed this indicator to see what JP Morgan says.

It draws VIX, its MA and its MA deviation rate.

You will see the truth.

Enjoy!

World Markets Open/Close BackgroundIndicator fills background color on the chart for different markets around the world.

This can be helpful in some markets to understand after hours and premarket price action. User can study if there is correlation between highs/low in whole session or open/close of different markets.

Tokyo, Hong Kong and Shanghai are Asian Markets in Red are combined

Bombay, London and NYSE are individually plotted.

Times can be changed for each session to include the entire session, or selected block of 15 minutes.

Less than 15 minutes will need to be changed in the default value of the code which is why I'm publishing it open source.

All coded default times for each market are in CST.

Background color can be turned off individually under the Style tab, and can also be unchecked under Inputs and can just be used for source for further coding.

My intentions for this script is to use it and its variable value to plot the highs and lows just in the specific times in a session and to more easily visualize those sessions with color coding.

I hope this is useful

Cheers!

S&P Sector Advance/Decline Weighted -Tom1traderEnjoy, enhance your trading (I hope), copy or adapt to your needs and keep smiling!

Thanks to @MartinShkreli. The sector variables and the "repaint" option (approx lines 20 through 32 of this script) are used directly from your script "Sectors"

RECOMMENDATION: Update the sector weightings -inputs are provided. They change as often as monthly and the

annual changes are certainly significant. When updating weighting percentages use the decimal value. I.E. 29% is .29

Good on any time frame. Especially SPY, SPX and ES scalpers and 0DTE options traders may like this a lot.

This gives good signals on S & P and related (ES, SPY) and indicates / plots differently than the AD line or ratio.

Each sector's entire % weight is added or subtracted depending of whether that sector advanced or declined.

Example: Information Tech weight at 29% so that % of 500 (145) is added if InfoTech is up a penny and subtracted if it is

down a penny. All sectors processed the same way so that for a given bar/candle the value will be between +500 (all

sectors up) and -500 (all sectors down). This weighted AD line of sectors is scaled to +/- 350 and plotted as a red/green line

along with aqua/fuchsia columns of its 5 period ema. The line is actual sector behavior and the columns seem to make a

good signal with column zero crosses standing out.

The columns aqua / fuchsia are a 5 period ema of the Sector AD line and give pretty good signals at

zero cross for SPX. I colored the AD red green line also to emphasize the times it opposes the ema

for example the histo/colums zero cross signal is NOT true when the AD line is showing all or most sectors

going the other way.

For readability, the AD line itself is scaled to 350. This lets the columns of the ema stand out better. The hlines at

350 and at 175 give an idea for the AD green red line how much of the sector's weight is up or down.

350 is all sectors up (advancing) and -350 is all sectors down (declining). The hlines at +/- 175 seem to outline

a more or less "neutral" zone. For example in an uptrend with most of the AD level positive and the columns positive;

a negative spike that does not pass the -175 line and returns positive does not seem to impact the price as much as

a deeper negative spike.

IB + ExtensionsInitial Balance with Extensions.

Other traders have posted similar indicators. I wrote my own because I wanted additional features.

Features:

Supports up to 9 extensions. Default = 3.

Each extension is filled using an automatic gradient. Fill can be disabled if you like.

IB levels extend into the future to the end of the current session.

By default only the current IB levels are shown, but you can enable past IB's as well.

When showing past IB's, each session has a clean break - no awkward lines connecting one session to the other (this really annoyed me about other IB indicators!)

The IB midpoint is also supported. It is on by default, but can be disabled.

You may notice the midpoint of past IB's looks different than the current IB . There is a technical reason for this that I won't go into here. Ask if you want the full explanation.

NOTE: This indicator was designed for the crypto charts. It may have some rendering issues when used with other markets.

TL Data PanelIntroducing the TraderLion Data Panel

Features

1. Plot Quarterly EPS & Sales in a table. Disclaimer | TradingView data for EPS & Sales can be highly inaccurate in some cases.

2. U/D Ratio - Calculates the Up/Down Volume Ratio on a 50 Day Average or 20 Day Average. A number above 1.5 will show in green.

3. DCR - Calculates the Daily Closing Range for the stock. It's green when the DCR is greater than your benchmark (set in indicator settings) and greater than 50%.

4. WCR - Calculates the Weekly Closing Range for the stock. It's green when the DCR is greater than your benchmark (set in indicator settings) and greater than 50%.

5. Extended - Calculates if the stock is extended vs the 10DMA and 10WMA. The output will be Yes or No.

6. RSNHBP Count - Counts the number of RSNHBP in the past 30 sessions. Higher the count the better the odds of a stock performing well in the markets.

7. HV Stats - This shows if a stock meets the HVE/HV1/HVIPO criteria. HVE - Highest Volume Ever. HV1 - Highest Volume in One Year. HVIPO - Highest Volume Since IPO.

Customizations

Up Down Volume Length - Toggle between 50 Day or 20 Day.

Average $ Volume Length - Toggle between 50 Day or 20 Day.

Closing Range Benchmark - Set your benchmark vs any index.

RS Benchmark - Calculate RSNHBP benchmark vs any index.

Table Size - Tweak table size on personal preference.

Table Position - Tweak table position to top right, bottom left, bottom right, or top left.

Margins vs ROE - Toggle this setting to display Margins or ROE.

Color Theme - Toggle between Light or Dark Theme.

If you have any questions, please post them in the comments below!

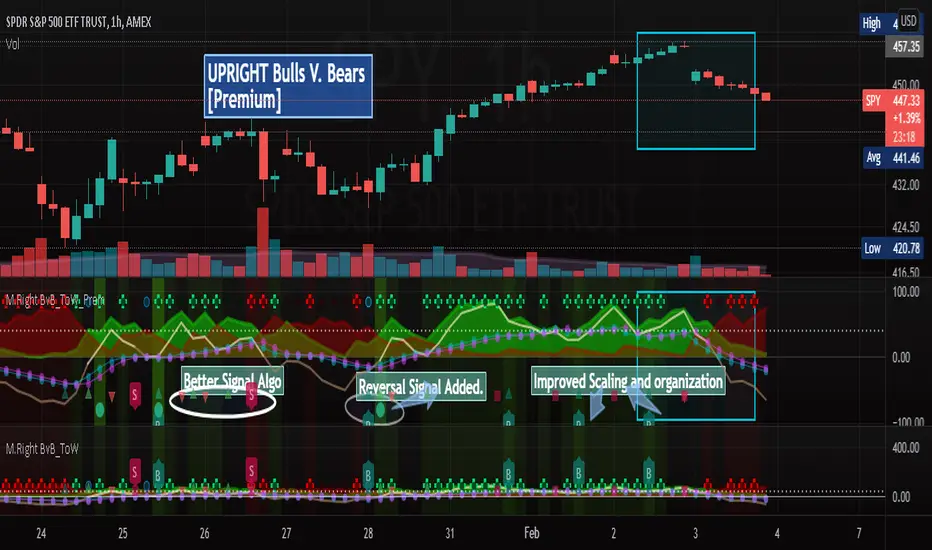

[UPRIGHT] Bulls-V-Bears Tug-of-War SquidGame [Premium] (cc)Hello Traders,

Today I'm updating the Bull V. Bears with a Premium version. (Note: the other version is shown below the Premium on the chart above)

……"The game is Tug of War, the side that pulls the rope from the middle to their side wins. Let the game begin."……

How it works:

This indicator is not a typical one.

1) It shows visually when Bull volume or Bear volume is ‘pulling the rope to their side’.

2) It uses several different formulas to get an accurate read on the level of volume , but still keeps peaks and troughs within 100 for easy reading.

3) Update: It was originally meant to be used strictly with other indicators, but it can now be used as a standalone indicator.

__________________________________

Legend:

1) The top line signals give the major signals –

a. Red cross = Bearish volume strength and continuation.

b. Green cross = Bullish volume strength and continuation.

i. + Green Dot inside enhances signal.

ii. + Red Dot inside weakens signal.

c. Blue circle = Can indicate the beginning of a reversal to the upside or downside.

d. Pink circle = Can indicate the beginning of a reversal to the downside.

2) The Bottom signals are triggered when one circle-rope crosses over the other, these signals give confirmation to the top line signals – Red bearish / Green bullish .

3) As shown on the chart, the Reversal setup usually consists of a blue circle, followed by a red or green cross, then confirmation from the bottom signal.

4) Without the signals: green obviously is Bullish especially above the threshold set --Red bearish . The regular rope gives trend indication.

I've added tooltips to make it easy to understand, feel free to leave a comment if you still have a question!

__________________________________

Features:

-Tooltips (hover over - Info) for understanding.

-Works well on all timeframes; even 5min, I made a tooltip for recommended lengths.

-Customizable Signals; with the ability to turn on and off.

-Reversal signals: Pink and Blue circles can indicate reversals coming.

-Works well as a leading standalone indicator.

-Adjustable top signal row.

-Background Highlights.

-Alerts

-Rules added (hover over).

__________________________________

Premium :

-Better signal algo (will likely be updated again soon)

-Reversal Signal added (Large Circle)

-Improved Scaling and Organization - Now easier to see large moves/signals on Multiple timeframes.

Chart should look like:

Cheers,

Mike

(UPRIGHT Trading)

Federal Funds Rate and Overnight Bank Fund RateAMEX:SPY

Comparison of the Overnight Bank Fund Rate and the Effective Federal Funds Rate.

The Fed sets a discount rate of 100 basis points above the effective federal funds rate to discourage ("penalize") banks from borrowing from its reserves. If lending banks have excess in their reserves, the borrowing banks have ease in negotiating a lower rate overnight to maintain its requirements. For this reason its a good indicator of the economy. If it becomes more difficult for banks to maintain the required reserve amount they may charge borrowing banks higher rates.

Both the Effective Federal Funds Rate and Overnight Bank Fund Rate use the same data. Except, the OBFR includes overnight Eurodollar transaction data and certain overnight “selected deposit” transactions that are placed at domestic bank branches controlled by a U.S. banking office.

The indicator includes the lower and upper bound target rate set by the Federal Reserve.

An interesting note:

Notice the jump in the Overnight Bank Rate followed by Fed buying to provide liquidity and lower rates in Sept 2019.

Fibonacci Ghost CloudHello my nocturnal minions.... This is your dark knight in the crypto light.... your alpha and omega, your crypto king reigning wisdom down from my gilded throne of code!

Enjoy the spooky Fibonacci Ghost Cloud. Shadows of previous Fibonacci look-back levels provide possible entries, stop losses, and take profit levels for intrepid crypto travelers.

DESCRIPTION

This indicator is front weighted by using the Fibonacci integer sequence..... 2,3,5,8,13. Each green and red "ghost" is a reflection of the highest highs and lowest lows of a given FIB lookback. The guide lines, red and green, are averages of the highs (green) and the lows (red).

USAGE

The "ghosts" can be used as possible support and resistance levels. They diminish in intensity (they become more transparent) as these ghosts move back further in time. When multiple greens overlap it is an indicator of a lot of recent price action at that level. The same is true of overlapping red.

In addition, the amount of ghosts above and/or below are indicative of recent price action taking place at a higher or a lower level

CURRENT PRICE IS LOWER THAN RECENT PA - There will be many green ghosts above, but few or no red ghosts below.

CURRENT PRICE IS HIGHER THAN RECENT PA- There will be many red ghosts below, but few or no green above

TAKE PROFIT - Possible take profit targets could be on the approach to a previous green level

STOP LOSS - Possible stop losses could be at lower red level

Like Bollinger bands, the green and red "average" lines can help to indicate that a security is oversold or underbought according to how close it is to a recent average. Nearing the red line can indicate that the security is oversold - and the converse is also true.

DERIVATIONS

Within the code is additional greyed-out lines which could be activated allowing you to target the open or close, instead of the High-Low - the current settings

SETTINGS:

You can change the FIB levels and substitute your own integer sequence to use as the lookback.

Feel free to offer feedback and/or suggest features you would like to have added.

SPX DivergenceScript plots divergence of SPX sectors and world markets based on 3 months return of various ETF's.

Excessive divergence in returns typically preceeds strong market downturns 1-2 weeks ahead of time.

Goethe A - Multiple Leading Indicator PackageGoethe A is an Indicator Package that contains multiple leading and lagging indicators.

The background is that shows the local trend is calculated by either two Moving Averages or by a Kumo Cloud. By default the Kumo Cloud calculation is used.

What are those circles?

-These are OBV (or VPT, can be set in the options) Divergences. Red for Regular-Bearish. Orange for Hidden-Bearish. Green for Regular-Bullish. Aqua for Hidden-Bullish.

What this middle line?

-The middle line is calculated by a smoothed Heikin-Ashi indicator. I can be used as a dynamic zone of support and resistance. Many times this indicator is used as entry signal giver in trend following strategies.

What are those background lines?

-The background contains a simple Daily Pivots indicator. This indicator can be read as zones of Support and Resistance that updated based on the used timeframe.

What is this smaller thin grey line?

-This is a very simple Stoploss indicator based on Donchian Channels. The trade direction is based and calculated by the local trend (background color)

What are those small orange or aqua triangles?

- These are Pivots . They show when the OBV or wolfpack oscillators (or a double confirmation of both) might reverse, this is important to know because many times the price action follows this move.

What are those purple triangles?

- These are Pivots . They show when the PVT oscillator might reverse, this is important to know because many times the price action follows this move.

What are those big orange or aqua triangles?

- These are TSI (true strength indicator) entry signals . They are calculated by the TSI entry signal, the TSI oscillator treshold and in conjunction with the overall local trend (background color).

What are those white squares?

- These are Overbought or Oversold regions of the build-in RSI bands indicator. Every time the price crosses one of the RSI bands those squares are printed. Most of the time this happens after a move and indicates that this strong move has come to an end.

Most settings of the indicator package can be modified to your liking and based on your chosen strategy might have to be modified. Please keep in mind that this indicator is a tool and not a strategy, do not blindly trade signals, do your own research first! Use this indicator in conjunction with other indicators to get multiple confirmations.

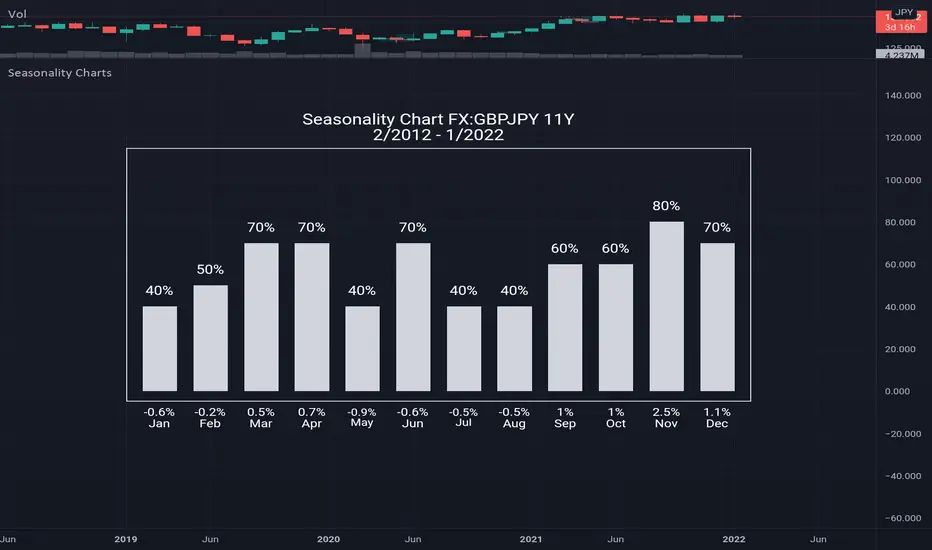

Seasonality ChartsHow to use: open monthly chart

What this chart show: The seasonality tool calculates two numbers: the percentage of time that the month is positive above histogram and the average gain/loss for the month below histogram

Seasonality tells us what has happened in the past, which is the historical tendency. There is certainly no guarantee that past performance will equal future performance, but traders can look for above average tendencies to complement other signals. On the face of it, a bullish bias is present when a security shows gains more than 50% of the time for a particular month. Conversely, a bearish bias is present when a security rises less than 50% of the time. While 50% represents the exact middle, chartists should look for more extreme readings that suggest a relatively strong tendency.

Intraday Price change in Top 5 stocksFixed some code from a script I found online

This tracks intrday price % movement of 5 stocks in S&P500 & NASDAQ 100

Wolf TradeWolf Trade indicator designed to help you develop your own trading strategy and give you that extra confirmation on your trade ideas. This indicator helps you to identify the right buying or selling opportunity. Examines several items to issue a buying or selling position. For example, it checks the status of the RSI , as well as the status of the MACD , as well as the status of the stochastic . Checks the order of placement of the EMA and the condition of their cross with ATR. And uses the ATR for stop loss.

Wolf Trade indicator commodities on all timeframes including 1m, 3m , 5m, 15m, 30m, 1H, 2H, 4H, 1D, 1W, etc. Definitely, the performance of this indicator is much better in 1, 2, 4 hours and daily timeframes, but that does not mean you can not use it in shorter time frames.

This indicator is does not repaint and works on any market internationally including crypto, stocks, forex, futures and currencies. You can utilize our indicator for scalping, swing trading, holding or even for trading options as well.

Fusion: Monster Breakout IndexThis indicator is designed to display on both the main chart and a separate chart area. If you want to display it on the main chart then flip the 4 display options. Well... you might want to:

Disable it first

Move it

Flip the display options

and then show it so the move doesn't look ugly.

Display options:

On a separate chart it will display red and lime bars showning potential breakouts.

On the main chart it will show a channel.

Personally like to see it both ways so I generally have two copies of it with one on the main chart.

The " Bar back marker " option is a tiny down arrow at the top of the chart showing where the length of the lookback starts from the current bar. So, if you set the length to 10 then this will be 10 bars back from the current bar. You can show it on or off the main chart but it's not all that visually tasteful off the main chart.

The length is certainly not some optimized setting so set to whatever suits your needs.

The source I set at hl2 which makes more sense to me than the default most people use of close so again, don't assume the settings are correct for your environment... play with it.

Credit:

Modified from the "Monster Breakout Index" by racer8 under the licence of: This source code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

The code is structured to easily drop into a bigger system so use it as a lone indicator or add the code to some bigger project you are creating. If you do, send me a note, it would be nice to know it's being well used.

Finally, if you find value please do make a comment, give a thumbs up etc.

Enjoy and good luck!

OBV+OBV with an extra twist.

Add up to 4 moving averages and choose from simple, exponential, smoothed, etc.

Choose to display a trend fill. Fill will be green when above the MA4 or red when below it. If the difference between the MA1 and MA4 is growing, the trend fill will be a more solid color indicating a strengthening trend. If the gap is lessening, it will gradually get more transparent indicating a weakening trend.

Finally, options to display bullish and bearish regular and hidden divergences are included.

Breadth Bottom Visualized (Breadth.app) Plots R3k stocks above 20d SMA and Total % of stocks above 20 day

Crypto EMA Breadth (ST)Crypto EMA Breadth (ST) represents the breadth in the "Short Term".

It uses DEMA (Double Exponential Moving Average) instead of EMA to reduce lag.

This indicator returns the percentage of crypto coins that satisfy the following criteria:

Uptrend is defined as: DEMA 10 >DEMA 20 > DEMA 50.

Downtrend is defined as: DEMA 10 < DEMA 20 < DEMA 50.

Range = not uptrend and not downtrend

A time frame for computing market breadth can be specified.

For example, 1 = 1 min, 5 = 5 min, 30 = 30 min, 60 = 1 hr , 240 = 4 hrs , D = 1 day.

Additionally, irregular time frames (e.g. 37 = 37 minutes) can be selected.

TradingView allows for a maximum of 40 names in a single indicator.

The market breadth index is calculated using the top 40 cryptocurrencies (market cap):

btc , eth, bnb,sol, ada, xrp, luna, avax, dot, doge, shib, matic

ltc, algo, near, mana, sand, axs , atom, gala, link, xlm ,

xmr, vet, ftt , hbar, egld , ftm , hnt , eos , lrc , one, enj , zec,

dash, celo, fil, icp , xtz, theta

3commas GRID bot VisualisationHello everyone

This is a grid display indicator for a 3-comma grid bot.

Just enter the upper and lower borders of your grid and the number of grid cells in the indicator settings.

It's simple!