Will it happen again for S&P500 Future ES using analog from 20088 Apr 2020 recap - S&P500 e-mini futures CME_MINI:ES1! had a strong rally up and closed near the high around 2750. The strong price action has totally ignored the bearish tone set in 7 Apr 2020, where ES was up more than more than 3% but closed down on the day.

In 2008, similar situation had happened a few times, such as on 3, 14, 17 Oct 2008. Every times after the price rejection, ES started a downswing. If we pay close attention to 17-18 Oct 2008, it is similar to ES current situation (7-8 Apr 2020) because the rejection bar was followed by a strong demand bar both in 2008 and 2020. Yet, a down swing was followed in 2008 after the strong demand bar, as shown in the chart as illustrated.

Historical analog is good for reference and keep us to anticipate potential scenarios. However, always trade according to the charts.

So far, ES does not show any emergence of supply., which is a bullish sign. Could it grind higher to stretch to around 2800?

Bias - neutral. A range bound between 2630-2750 can be expected. A break below 2600-2630 will validate the up thrust scenario. A break above 2750 should see a test of 2800.

Key levels - Resistance: 2750-2780 Support: 2700, 2600-2630.

Potential intraday setup - A short entry is preferred. Pay close attention on how the price interacts with the key levels, swing high, swing low, neckline, etc...

Supply and Demand

Up Thrust of ES S&P500 future - What's next move?7 Apr 2020 recap - S&P500 e-mini futures (ES) tested the target around 2700-2770 yesterday and had an up thrust movement on level 2700 before closing below 2650, as per my trading idea yesterday. It had a great run-up during the non regular trading hours (RTH). However, weakness did show up during the US session. ES was rejected from the target 2700-2770 with increasing supply. The down wave is the greatest for the H1 trend started from the low at 2450, suggests a change of character, which means that the up move could stop at least for now, into a trading range or even a reversal to move down.

During today's non-RTH session, ES had a weak rally up, tested only 50% of the last hour bar from yesterday followed by a reversal bar, which could be a sign of weakness. Should ES break below the support levels at 2600-2635, it could test lower targets like 2400-2450 or even the selling climax's low at 2174.

However, if the levels 2600-2635 are defended, with absorption characteristics, ES could test the swing high at around 2750 and possible to grind higher.

Bias - bearish. Expect a break of 2600-2630 to test lower.

Key levels - Resistance: 2650-2700 Support: 2600-2630. Swing high and swing low from lower timeframe.

Potential intraday setup - look for an up thrust or test of swing high at 2658, 2680 and/or key levels followed by a reversal to short. If ES can commit below 2600, I will consider to switch the position to swing trade instead of day-trading.

.WTICrude Demand?This my understanding of the current oil situation. If everything goes good on Thursday USOil can have an extremely bullish daily move. Fundamentally we might not have the right demand conditions to sustain a sentimental boost. If it does boost and if it does not break below 20 it can most likely remain bullish. Recommended to trail SL in profit. SL in profit may also be a good Sell Stop entry if fundamental conditions continue to remain bearish for OIL

GBPUSD 15 min strength example (training)In the circle there is a confluence of criteria:

stopping volume (demand)

extension of price out of demand side of 1 hour Bollinger band with immediate rejection back into channel (multi-time frame Bollinger band indicator)/ also a previous support

diminished supply pressure at automatic rally

Can you tell when/where the buying began activating?

Refer to Wyckoff, VSA, Tom Williams for a more organized explanations/schematics.

Practice*

ES S&P500 future - breakout to start a bull run? Analog inside6 Apr 2020 recap - S&P500 e-mini futures (ES) had a great rally to take out the immediate resistance at 2525 during the non-Regular Trading Hour (RTH) and to further commit above 2600-2635 during the RTH. Since ES broke out the trading range between 2440-2630, it is expected to test the higher target at 2700-2770.

It is worth noting that the upside target at 2700-2770 coincides with :

Fibonacci retracement of around 50% from the top (3397) to the selling climax (SC) low of 2174, as shown in the daily chart.

Axis line or flip zone where there is strong resistance and supply available, as shown in the H4 chart.

During the crash in Jan 2018, ES did up thrust twice before it came down to test the selling climax low. Using Jan 2018's event as an analog, we should be aware that an up thrust is a possible scenario.

Bias - Slightly bullish. Expect ES to test the upside target but also prepare n up thrust bearish scenario similar to 2018.

Key levels - Resistance: 2700-2770 Support: 2600-2635. Swing high and swing low from smaller timeframe

Potential intraday setup - look for an up thrust or test of the key levels / smaller timeframe for a short entry. Possible long entry at the support should it happen.

Is the ES rally done yet? What's next?3 Apr 2020 recap - ES did rally to level 2525 and was rejected again. In smaller time frame (M1, M3), it did provide great short entry after the up thrust of the level. However, ES only managed to test 2450 and bounced up from there. The low volume without aggressive demand caused ES to drift down. Should ES still stuck below 2525, it should break down to test 2400 or even lower (i.e. the Selling climax's low), under the background of lacking of demand.

Daily - After a sharp sell off, ES formed a selling climax (SC) low at 2174 followed by an automatic rally (AR). Now, it seems like the rally is coming to and end. The next move would be a secondary test (ST) to test the selling climax's low. It could in a form of a higher low, similar low or even lower low. Oct 2008 global financial crisis could provide a good analog for reference. Could we see a down-sloping accumulation structure similar to 2008?

Weekly - a megaphone structure is formed. ES could potentially test the low as illustrated should a down-sloping structure in progress. This won't surprise me given the COVID-19 situation is getting worse every day and the impact on the businesses.

Bias - bearish. If ES fails to commit above 2525, it should break down to test 2400 or lower, sooner or later.

Key levels - Resistance: 2480, 2525. Support: 2450, 2400.

Potential intraday setup - Look for a test or up thrust of the key levels and/or smaller timeframe to initiate a short entry. Yet, I will pay close attention for long opportunities like a spring of the swing low, shortening of the downward thrusts, etc... should it arise.

Stay safe and happy trading!

NAKED TRADING 15M USD/JPY BACKTEST 1 WEEK WINRATE 80% 👌GREEN: TP HIT (16)

RED: SL HIT (4)

Reward/Risk = 1:1

ES price action analysis for 3 Apr 2020 trading plan

2 Apr 2020 recap - Although yesterday was a bullish day, the character does not confirm this. It started with ugly numbers of jobless claims, which drove ES down to spring the low (around 2433) of the previous day followed by a rally up to test 2525 thanks to a spike up in crude oil.

It was highlighted in M15 chart that the 2 candles tested the 2525 level has volume spike, suggests the demand was met by supply at this level.

On the daily chart, candle b (yesterday) has slight increase of volume compare to candle a, yet the result (to the up side) is mediocre. The rally from yesterday only reached about half way of the previous down candle. This suggests supply was present and managed to stop the up move at level 2525.

Bias - slightly bearish. If ES fails to break above 2525 with aggressive demand, it might break below the swing low at 2425 and test further down.

Potential intraday setup - Look for how ES interacts with 2525 or structures in smaller timeframe. A short entry after a test or up thrust of level 2525 is preferred.

Key levels - Resistance: 2500, 2525 Support: 2450, 2425. Swing high and swing low from lower time frame.

Note: Since yesterday has increase of supply, it is important to see how significant is the reaction. A trading range between 2425-2525 will be neutral. A break above 2525 is bullish and expect continuation of the rally. A break below 2425 should draw out more supply to test 2380 or lower.

ES price action analysis for 2 Apr 2020 trading plan

1 Apr 2020 recap - Major movement of ES happened during non-RTH. Level 2450 was tested from the last 4 H1 bars and defended eventually. The last hour bar did spring the prior swing low and form a demand tail. The magnitude of the down move might be significant but without aggressive supply. Daily volume is slightly lower than the previous day (31 Mar 2020). Result - did not commit below level 2550 and the swing low formed on 30 Mar 2020, suggests a bounce up from here.

A trading range between 2450-2630 is expected. The down-sloping accumulation structure since 12 Mar 2020 is still valid. ES could have gone through a sign of strength (SOS) rally from 24-26 Mar 2020 and currently on a backup action before marking-up higher.

Bias - Break above 2500 to challenge levels 2550, 2600 and the swing high (2630).

Potential intraday setup - look for possible continuation of the rally if committed above 2500. Else, short into an up thrust of level 2500. Pay close attention on how ES interacts with the key levels for reversal trades. It is possible to switch to swing trade should the close is favorable.

Key levels - Resistance: 2500, 2550 Support: 2450 ; Prior day high 2509 and day low 2434; Swing high and swing low from lower time frame.

Note: bullish bias is maintained until emergence of aggressive supply. During the unwinding of the volatility, expects relatively normal session without huge swing (up or down).

Commitment of traders reportWHAT IS IT

The Commitment Of Traders (CoT) is a report issued by the Commodity Futures Trading Commission (CFTC) , one of the most important trading insitutionsof the American government. The report has the purpose of transparently showing market dynamics to the all the people involved or interested in the matter.

The COT report show all currently open positions (open interest) of the future and options market, where 20 or more traders hold positions for an amount greater or equal to the minimum amount amount established by the CFTC .

The report is issued every Friday at 3:30 P.M. (Eastern Standard Time, hence UTC-5). Each report normally contains data until previous Tuesday. CFTC usually receives data on Wednesday morning from the reporting firms (i.e.: Future Commission Merchants, Financial Insititutions, Brokers or International Stock Exchanges). After some verifications, CFTC publish data the following Friday. For each market, data are provided in terms of existing (still open) LONG and SHORT positions.

TYPES OF REPORTS

There are 4 types of report:

1) Legacy

It contains data split by stock exchange. This report has two different variants: "futures only", that contains data related to the futures market only, and "combined", that contains aggregated data for futures and options market. All the reported positions in this report are split in two main market actors categories: Commercials (or Large Speculators) and Non-Commercials

2) Supplemental

It includes contracts related to 13 selected agricultural market commodities. This kind of report split positions in 3 market actors categories: Commercials (or Large Speculators), Non-Commercials and Index Traders. Differently from Legacy report, the Supplemental is provided in the "combined" format only, hence contains data for both futures and options market

3) Disaggregated

This report contains the same data issued in the Legacy report, but with a more detailed drill down in terms of representation. First of all, it presents data split in 5 macro-categories: Agriculture, Petroleum and Products, Natural Gas and Products, Electricity, Metals and Other. Moreover, the report shows open positions/interests of 4 market actors categories: Producer/Merchant/Processor/User, Swap Dealers, Managed Money e Other Reportables. Aggregating data of this report, it is possible to obtain same data of Legacy report, hence this is a detailed view of data contained in the Legacy report. The Disaggregated, as well as the Legacy one, is available as "futures only" and "combined" variants

4) Traders in Financial Futures (TFF)

This report includes contracts related to currencies, US Treasury Bonds, Eurodollar deposits, VIX shares and Bloomberg Index only. The reports shows open interests of 4 market actors categories: Dealer/Intermediary, Asset Manager/Institutional, Leveraged Funds e Other Reportables. Last, also this report is available as "futures only" and "combined" variants

REPORT FORMATS

Legacy and Disaggregated reports are provided in two formats: short (synthetic) and long (extended). Both these formats contain same data, but long format contains also the concentration of open positions in the hands of the major 4 and 8 market investors at the moment of data collection, while short format does not contains any data about concentration.

TFF report is available in long format only, while the Supplemental is available in the short format only.

Report type Scope Format

Futures Combined Long Short

Legacy ✓ ✓ ✓ ✓

Disaggregated ✓ ✓ ✓ ✓

TTFF ✓ ✓ ✓ X

Supplemental X ✓ X ✓

Legacy report

As said above, market actors in Legacy report are divided in 2 categories:

Non-Commercials , or Large Speculators : they are market speculators as well as hedge funds. This category normally uses financial leverage to amplify variation of derivative asset and has an aggressive behavior in the market. They use rigid stop loss policies and, when the market falls below certain levels, they reverse positions on the other side. The main purpose of Large Speculators is not the asset they buy or sell, but to obtain a net profit from the buy/sell cycle. They normally have a trend following behavior.

Commercials buy futures just because they are interested in the underlying asset and try to hedge their financial exposition related to the commercial activity with the assets they are interested in. These market actors hold more than 50% of open positions in the US futures market and normally they go against the price trend: they sell when the market goes higher and they buy when the market goes lower. Their positions on underlying assets normally anticipate market trend, hence they should be carefully monitored

Non-Reportable : are the open position of small investors/traders that normally are on the wrong side of the market. This investors category is usually confused and not disciplined. They do not follow precise rules and are usually dragged by the trend, but they are slow to reverse positions when the market trend reverses.

The following example contains data about "futures only" market for BUTTER, coming from Chicago Mercantile Exchange.

BUTTER (CASH SETTLED) - CHICAGO MERCANTILE EXCHANGE Code-050642

FUTURES ONLY POSITIONS AS OF 03/17/20 |

----------------------------------------------------------------------------------| NON-REPORTABLE

NON-COMMERCIAL | COMMERCIAL | TOTAL | POSITIONS

--------------------------------|---------------------|--------------------------|-----------------

LONG | SHORT |SPREADS | LONG | SHORT | LONG | SHORT | LONG | SHORT

--------------------------------------------------------------------------------

(CONTRACTS OF 20,000 POUNDS) OPEN INTEREST: 11,597

COMMITMENTS

0 2,473 453 10,401 8,149 10,854 11,075 743 522

CHANGES FROM 03/10/20 (CHANGE IN OPEN INTEREST: 753)

0 -127 101 675 796 776 770 -23 -17

PERCENT OF OPEN INTEREST FOR EACH CATEGORY OF TRADERS

0.0 21.3 3.9 89.7 70.3 93.6 95.5 6.4 4.5

NUMBER OF TRADERS IN EACH CATEGORY (TOTAL TRADERS: 47)

0 12 10 28 22 38 34

It is possible to see as in the report is provided the total amount of LONG and SHORT positions for Non-Commercial, Commercial and Non-Reportable actors. Variations from previous week are moreover reported.

In addiction to LONG and SHORT positions, Legacy report contains also the SPREAD amount, that is available for Non-Commercial only, and refers to contracts that are opened LONG and SHORT at the same time. Normally a growing SPREAD value means a high level of uncertainty.

If we calculate NET POSITIONS (NP) for the 3 actors categories, as it's easy to check, the report show a zero-sum scenario:

NP Non-Comm = 0 – 2,473 = - 2,473

NP Comm = 10,401 – 8,149 = 2,252

NP Non-Rept = 743 – 522 = 221

NP Non-Comm + NP Comm + NP Non-Rept = -2,473 + 2,252 + 221 = 0

OPEN INTEREST value is the grand total resulting as the sum of LONG, SHORT and SPREAD positions:

Open Interest = 0 + 453 + 10,401 + 743 = 11,597

Supplemental report

Even the Supplemental report (called also Commodity Index Traders - CIT) shows data in the same manner of Legacy report, but the market actors are 3: Non-Commercial, Commercial and Index Traders.

Non-Commercial and Commercial actors are the same, while Index Traders category has appeared for the first time in January 2007. Before that date, investors that are now reported in this category were scattered in the two existing categories (Non-Commercial and mostly in the Commercial). The creation of Index Traders category has had the purpose to separate that category from Commercials, because Index Traders are not involved in the buy/sell cycle of underlying assets, and are usually managed funds, institutional investors or swap dealers. Index traders are normally interested in passive and longstanding LONG positions, while are not interested in the short-term price fluctuations. It's not unusual that this category start buying when price is falling and technical analysis says that the price falling will be even more deep. Index Traders are hence a counter-part of speculators, who have usually a contrarian habit.

Supplemental report is provided for 13 commodities:

• WHEAT-SRW - CHICAGO BOARD OF TRADE

• WHEAT-HRW - CHICAGO BOARD OF TRADE

• CORN - CHICAGO BOARD OF TRADE

• SOYBEANS - CHICAGO BOARD OF TRADE

• SOYBEAN OIL - CHICAGO BOARD OF TRADE

• SOYBEAN MEAL - CHICAGO BOARD OF TRADE

• COTTON NO. 2 - ICE FUTURES U.S.

• LEAN HOGS - CHICAGO MERCANTILE EXCHANGE

• LIVE CATTLE - CHICAGO MERCANTILE EXCHANGE

• FEEDER CATTLE - CHICAGO MERCANTILE EXCHANGE

• COCOA - ICE FUTURES U.S.

• SUGAR NO. 11 - ICE FUTURES U.S.

• COFFEE C - ICE FUTURES U.S.

Disaggregated report

Market actors of Disaggregated report are:

Producer/Merchant/Processor/User : they are involved in production, handling, packaging or transport of physical assets that is underlying to the future instrument or option. These actors use futures to cover/hedge risks associated to the activities they are involved in that are strictly related to the production of the assets

Swap Dealers : they are subjects that are involved in trading swap contracts related to the commodity and uses futures market to cover/hedge risks associated with swap transactions. The counterpart of a Swap dealer could be a speculative traders, as well as an hedge fund, or a more traditional Commercial subject that is interested in managing risks associated with the commerce activities of the asset

Money manager : to this category belong Commodity Trading Advisor (CTA), Commodity Pool Operator (CPO) or an unregistered fund identified by the CFTC. These subjects are delegated from their clients to do financial operations in their behalf

Other Reportable : all speculative traders that are not belonging in the three previous category are included in this category

Even in this case, the report shows LONG, SHORT and SPREAD positions.

Comparing this kind of report with Legacy, we can see that:

COMMERCIAL = PRODUCER/MERCHANT/PROCESSOR/USER + SWAP DEALERS

NON-COMMERCIAL = MONEY MANAGER + OTHER REPORTABLE

This explains why the report is called "disaggregated". It shows the same data but with a more level of detail especially regarding the actors that hold open positions.

If we take the Disaggregated report about BUTTER for the "futures only" market coming from Chicago Mercantile Exchange (equivalent to the previous example that is showed under the Legacy report section, we see:

:------------------------------------------------------------------------------------------------------------------------------------------------------ :

: Producer/Merchant : : : :

: Processor/User : Swap Dealers : Managed Money : Other Reportables :

: Long : Short : Long : Short : Spreading : Long : Short : Spreading : Long : Short : Spreading :

--------------------------------------------------------------------------------------------------------------------------------------------------------

BUTTER (CASH SETTLED) - CHICAGO MERCANTILE EXCHANGE (CONTRACTS OF 20,000 POUNDS) :

CFTC Code #050642 Open Interest is 11,597 :

: Positions :

: 8,893 6,326 1,048 1,363 460 0 301 180 0 2,172 273 :

: :

: Changes from: March 10, 2020 :

: 244 648 324 41 107 0 -12 -8 0 -115 109 :

: :

: Percent of Open Interest Represented by Each Category of Trader :

: 76.7 54.5 9.0 11.8 4.0 0.0 2.6 1.6 0.0 18.7 2.4 :

: :

: Number of Traders in Each Category Total Traders: 47 :

: 24 18 . . 4 0 . . 0 10 9 :

---------------------------------------------------------------------------------------------------------------------------------------------------------

If we take the categories Producer/Merchant/Processor/User and Swap Dealers and we sum all LONG positions and then subtract all SHORT positions, we obtain an overall NET positions like this:

NP = (8,893 +1,048 + 0 + 0) - (6,326 + 1,363) = 2,252

Now, if we do the same calculation for Commercial category of the correspondent Legacy report (see above) we obtain:

NP = 10,401 - 8,149 = 2,252

This is the confirmation that Disaggregated report contains the split of data reported in the Legacy report, where Commercial category is divided in Producer/Merchant/Processor/User and Swap Dealers. Same calculation would demonstrate that Non-Commercial category in the Legacy report is spitted here in Managed Money and Other Reportable categories.

If we now consider the Disaggregated report and we sum all LONG positions and then we subtract all SHORT positions for each actors category, we obtain:

(8,893 + 1,048 + 0 + 0) – (6,326 + 1,363 + 301 + 2,172) = 9941 - 10162 = -221

Given that the grand total should represent a zero-sum scenario, e can deduce from Disaggregated report that net position of Non-Reportable subjects should be +221, hence a net LONG of 221 contracts, and that is correct, in fact it is possible to obtain the same result from correspondent Legacy report (see above) by subtracting net SHORT position for Non-Reportable actors to the amount of net LONG positions for the same actors. Hence Disaggregated report allow us to calculato also net position of Non-Reportable, even if the data do not explicitly report the value.

Traders in financial futures report

This report is a further view on the market and split market actors in two sides (SELL and BUY) and 4 categories:

SELL SIDE

Dealer/Intermediary : are financial intermediaries who earn by the commissions related to the sell of financial products. Big banks and other financial entities are involved in this activities

BUY SIDE

Asset Manager/Institutional : they are insitutional investors, including pension funds, insurance companies and investment portfolio managers whose clients are mainly institutional entities

Leveraged funds : these are typically speculative funds (hedge funds) and various types of money managers, including the Commodity Trading Advisors (CTA) and the Commodity Pool Operators (CPO) not necessarily registered by CFTC. These subjects can be involved in hedging strategies and arbitrages on their own capital, or even third parties capital

Other reportable : these are all the traders that are not included in previous categories

Differently from Disaggregated report, the TFF report the positions of the mentioned actors categories are not an exact disaggregation of Commercial and Non-Commercial positions reported in the Legacy report. Here each actor belonging to one of the categories mentioned above could belong to the Commercial or the Non-Commercial category in the Legacy report, basing on the decision that CFTC takes during the report creation, that can be different time after time (i.e.: a subject that has already been considered a Commercial one in the beginning, can be shifted to Non-Commercial after a while, depending on the specific activities he is involved during the time, that can change as well). The TFF report is moreover available only in the LONG format

REPORT ANALYSIS

If we properly analyze data in the Commitment of Traders legacy report, we can determine the expectations of each market actor category regarding the market future.

The possibility to know the net positions of Commercial subjects (institutional investors) is the basis to understand the market sentiment. Their influence is, in fact, between 50% and 75% of the entire futures market of S&P500 and from 40% and 60% of Nasdaq100.

It is useful to point out that Commercial subjects, as well as the Non-Commercial, can take arbitrage or hedging positions, or, alternatively, put in place an active management of their portfolios by buying or selling futures on foreign (not US) markets, or, again, have open position on the futures' underlying assets and protect themselves from risks of price variations by taking opposite positions on the futures market. Hence the Commitment of Traders Report is an important thermometer to measure US stock exchange sentiment, but it isn't a tool that, alone, can allow us to predict how financial markets will move. It should be used (as usual) together with other indicators, tools, analysis and perspectives to have a better understanding of what is happening and a good approximation of what is going to happen (most likely).

Commercial subjects are active actors in the futures' underlying asset market and generally sell when the market (price) grows and buy when the price is more convenient (low), hence their activities are contrarian to the logic of speculators. For this reason the Commercial actors are often responsible of market moves and trends. They drag prices and the market with their activities, hence they anticipate and determine the market trends.

Non-Commercial subjects, viceversa, have opposite interests. They want to make money by price variations, hence they buy when the market shows growing prices and sell in the opposite conditions. This behavior is what we call "trend following" approach.

Here are some typical scenarios that we can find by analyzing the Commitment of Traders report:

1) If Non-Reportable actors (small/retail traders) are LONG and Commercial are SHORT, the Non-Reportable actors are most likely going to loose money because the price will go to to the side where Commercial are pushing it (down)

2) On the maximum levels of an asset price (i.e. near significant RESITANCE levels), Non-Reportable are likely pushed to SELL their positions. Then stop loss levels are likely hit and only after the price starts his falling stage

3) If Non-Commercial are LONG and Non-Reportable are SHORT, we are likely in the middle of an UPTREND and there is more space for the price to gro further

4) If Non-Commercial are LONG and also Non-Reportable are LONG, we are likely in the "euphoric" phase of the trend, hence the trend is going to finish soon

5) If Non-Commercial are SHORT, Non-Reportable are upgrading their SHORT positions and Comemrcial slow down their LONG positions, e re likely in the terminal phase of a downtrend

If we accept the hypothesis that Commercial traders hold better information on the market than the others just because they are active actors of the futures' underlying assets (it's their own business!), it is very important to monitor their behaviour in order to understand how they are evaluating the situation related to the specific commodity that is at the center of our interest.

Commitment of Traders Index

An interesting approach to have effective insights from the Commitment of Traders report can be obtained by calculating an index using the report data. Normally Comemrcial net positions are used to calculate the index as follows:

NP (Net Position) = Long Positions – Short Positions

Usually, an interval of 26 periods (weeks) is selected and the calculation to determine the index value is:

COT Index = * 100

The index, expressed as a pecentage value from 0 to 100, reflects net position of Commercials on the basis of last 26 periods. It can be used as an indicator of overbought and oversold zones and can be a good tool to understand where investors are moving.

The index can be also calculated for Non-Commercial or Non-Reportable positions.

Last, but not least, remember that Commitment Of Traders report is released every Friday evening, but contains data up until previous Tuesday, hence a "lagging" effect should be seriously considered in all the analysis that involves it.

The content of this article has solely education purposes and should be not considered trading or investement advise.

ES Price action analysis for 30 Mar 2020 trading plan

27 Mar 2020 - last hour sell off with big spread looks threatening. Yet, it still formed a higher low and within the H1 up channel. Expect a test of the bearish last hour bar during non-RTH on Monday. A break of the up channel and 2500 should send ES to test 2400-2450.

Overall H1 structure - potential up thrust of 2550 level followed by a test (last hour bar on 27 Mar). Confirmation is via a break of 2500.

Potential intraday setup during non-RTH - look for a test of the last hour bar followed by a reversal.

Key levels - First support 2500, 2nd support 2400-2450, resistance at 2550-2600

Commitment above 2600 will violate bearish scenario.

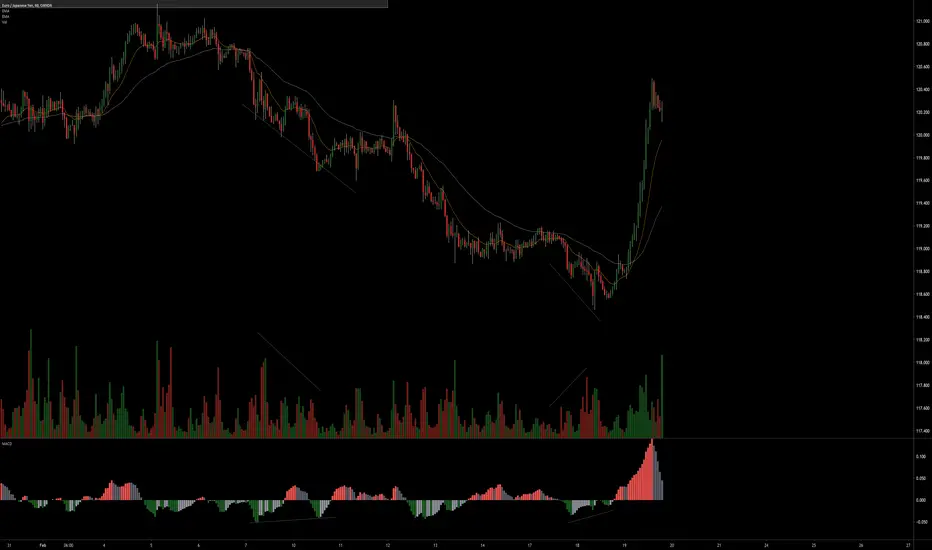

EURJPY 1 Hr MACD histogram positive divergence key ingredientIn this example there I have pointed out 2 MACD histogram positive divs.

Can you spot a key difference?

If using divergences, it is not a bad idea to utilize your volume. Notice the increase in demand, into new low ground, with the accommodating MACD positive divergence (example to the right).

Although there is a positive divergence (to the left of the chart) notice how the increase in demand is not as high. A counter trend situation did occur, but was rapidly met with enough supply to cancel the mark-up attempt (upthrust on high volume).

MACD histogram may be another useful confirmation tool. Not only for divergences, but it can also help one to identify accumulation and distribution areas above or below zero line ( for another time).

Hope this helps.

Practice*

ES Price action analysis with key levels & what to expect

25 Mar 2020 - Climatic run up with increasing volume followed by biggest down wave with highest supply. Bearish reaction with slow grinding down move during non-regular trading hour (RTH). Could it be preliminary supply?

26 Mar 2020 - Another climatic run up after shocking number of jobless claim (think this ugly number will pressure the House to approve the bill?) ES broke above 2550 with fading volume. Possible exhaustive demand?

Key levels to watch - First line of support - 2550, 2nd support- 2400, If stays above 2550, should challenge 2700.

GBPUSD Variations 1/2 Wyckoff accumulation schematicThe example here is using the 1 hour. The higher the times frame the less the detail if using wyckoff methodology. From a day traidng perspective the 5 and 15 minute provides closer detail which enables you to break down the actual phases within the TR. Obviously these are fractal in nature. I think you can point these out on any time frame of course. Te difficulty, for me at least, is getting the time componet down. The price levels (support and resistance) is less hard to plot and predict but the time component is a bit tricky for me. I used to not use the session dividers, but I think they are very helpful. The take some of the noise out. There are also some fib tools that appear to be more time oriented but I haven't found anyone that teaches that area of the art and its probably not necessary .

I came across this while practicing and I thought it might be useful if you are trying to associate what you see on the wyckoff schematic to how it transfers over to a candle chart. Again, the 5 and 15 do help bring the patterns out even further. The schematics are easy to find if you g it.

There are 2 variants according to stockcharts. V. 1 shows you the fake out/spring. V. 2 shows the LPS w/o a spring. The live example here more closely resembles V.2 as you can see.. no fake out before the positive impulse/ mark-up attempt etc.

Also note the W pattern (double bottom?).

Note the apex of the w or the number 4 on the schematic. Notice the low supply pressure. It didn't even need to touch resistance to test it.

Then look at the left and right base and the high volume demand.

Increased demand with decreased supply... what does that mean?.. Higher prices.

Invert the chart (in the settings menu) and its basically the same in reverse.

... some quarantine ranting for anyone who gives a beep.

Practice*

USOil May Reverse Like This - Exercise PatienceFor educational and demonstration purposes. Currently in bear trend; when watching for possible reversal it may not be an aggressive spike but it could look more like this. Just something to consider and study.

EURUSD - Wyckoff and Market PhasesHello Traders !

Today I would like to share with you an addition confirmation why I shorted EURUSD. I used Wyckoff Market Phases

Market Phase:

- Accumulation Phase: During a bull market, the accumulation phase begins when the informed investors usually enter their positions.

- Re-Accumulation Phase: As soon as the price leaves the accumulation phase and the new trend becomes visible, the phase of Re-Accumulation begins. Here, more and more investors are joining

the trend and ensuring higher prices

- Distribution Phase: We are currently in the Distribution Phase. At this stage, the market is often overbought, although the uninformed traders still believe that more bullish pressure is coming.

Afterwards the price will drop .

Wyckoff:

- This analysis clearly shows Wyckoff Theory.

1) Accumulation: The big players buy carefully

2) Mark Up: classic Up Trend

3) Distribution: Up Trend runs out of the steam and the market goes down or into a sideways trading range. The big players starts shorting the price.

4) Mark Down: classic Down Trend after distribution

Proof for Wyckoff: The market is ranging now for a while which clearly proofs the Distribution Phase on GBPJPY . Afterwards of a Distribution the Mark Down is following and the price will drop a lot.

I hope you guys could learn something out of it. Very important and nice theory.

Thank you and we will see next time

- Darius.

How to invest your money(CORONA VIRUS) Current Situation MY VIEWHello Traders !

SPX500 Good price to buy? : TVC:SPX

The question is yes on both sides. Whether you are trading or you would like to invest your money. The price is so low right now and thinking long term the price will go up the next years.

SPX500 represents the 500 biggest US Companies. The chance that these companies will lose their value over the next few years is not really possible. If this will happen then our world will have a big problem and you loosing your investment will be the smallest problem.

Investing: Always a got way right now because of the Corona Virus. But think longterm. Of course we could see SPX500 dropping more. Therefore I would split my investment and purchase at different prices. For example now. If we will see the price dropping more than buy again and so on. On the long rung(5-10years) you will make nice profits. #thinklongterm

Trading: If you consider only scalping it a little bit I would wait for price to go down retesting the Demand Zone before entering the trade. Make sure to keep an eye on Price Action in order to know where to close your trade. Stocks are very violent some time and they react pretty well on Price Action Candle Sticks. So keep that in mind.

Corona Virus: What impact will have the Corona Virus on the long run for us? Actually Corona Virus is not that dangerous like we all "think". Of course it is a serious problem but we do not need to make the problem bigger than it is. You as a person need to decide if you can do something against it. For example doctor, researcher, ... But you as a normal person can do 1 important thing. To not spread panic! The crash on SPX, Dow, ... is the sum of the panic reaction of all people. Simply.

Our luck is that the Corona Virus based of facts will not affect our world much. Therefore the whole economy will recover. This is why I recommend investing your money.

That was my View of the current situation of Corona Virus and the impact on our economy and I hope you did like it. Please leave a LIKE if you like my Content that I share with you. In the comment section you can tell my your view and ask questions.

Thank you and we will see next time

- Darius.

Best Trade Of the month = Buy KTC near the FloorOpened position at 25.00 after the reversal from 24.7.

The floor is at 24 so I risk 1. I sold all the positions at 26.75 and 28.25.

What's A Bear Market? Most Define It As a 20% DrawdownThis chart shows the Dow Jones Industrial Average after today's sell-off. In this published idea, we want to take a second to write about bear markets and what they mean.

In the media, bear markets are officially defined as a 20% drawdown from a prior peak. Today, the Dow Jones Industrial Average closed down 20% from its prior peak. Technically, this means the market is officially in a bear market. There are some interesting stats, however, that show this definition has its flaws. For example, since the 1940s, the stock markets has dropped 20% or more 16 times and only 7 of those have turned into recessions. Sometimes, a 20% drawdown is just that... a 20% drawdown without a prolonged bear market that eventually leads to a full on recession.

This post is not making any assumptions or directional predictions. Instead, we wanted to share a chart with everyone showing the official 20% drawdown in the Dow Jones Industrial Average while also providing more context about market panics and crashes.

Thanks for reading and press Like if you enjoyed this or leave a comment with your thoughts.

The power of supply and demand imbalancesIt never ceases to amaze me how powerful bigger timeframe imbalances are and how price can react to them no matter how old these imbalances are. There is a clear example of a very strong supply imbalance on the British Pound versus New Zealand Dollar (GBPNZD) Forex cross pair.

There is a very strong monthly supply imbalance created around 2.09 price level last May 2016. It took 44 months for price to retrace to it, that’s quite a lot of time. This is the type of imbalance you don’t want to trade against. These imbalances are not support and resistance, supply and demand imbalances have nothing to do with support and resistance even though some times imbalances contain classic support and resistance prive levels used by so many traders.

Take a look at GBPNZD Forex cross pair monthly timeframe supply and demand technical analysis below. If you are trading intraday or even scalping Forex cross pairs, you will be losing all of your trades since you won’t be aware of the strength of the imbalance that took control.

Taking a look at the bigger timeframe imbalances will add extra context to Forex trading strategy and will keep you alerted of such strong imbalances that could cause havoc in your trading account.

Trading intraday and scalping Forex is fine for those doing it, there is no doubt that trading lower timeframes can be profitable, but we highly recommend you to keep track of strong imbalances on the bigger timeframes because if you do, you will be avoiding many losses. If you were long biased on GBP/NZD Forex cross and you had some losses, now you know why you had those losses.