Relative Strength RatioWhen comparing a stock’s strength against NIFTY 50, the Relative Strength (RS) is calculated to measure how the stock is performing relative to the index. This is different from the RSI but is often used alongside it.

How It Works:

Relative Strength (RS) Calculation:

𝑅

𝑆

=

Stock Price

NIFTY 50 Price

RS=

NIFTY 50 Price

Stock Price

This shows how a stock is performing relative to the NIFTY 50 index.

Relative Strength Ratio Over Time:

If the RS value is increasing, the stock is outperforming NIFTY 50.

If the RS value is decreasing, the stock is underperforming NIFTY 50.

Statistics

Liquidity Depth [AlgoAlpha]OVERVIEW

This script visualizes market liquidity by identifying key price levels where significant volume has transacted. It highlights zones of high buying and selling interest, helping traders understand where liquidity is accumulating and how price may respond to these areas. By dynamically tracking volume at highs and lows, the script builds a real-time liquidity profile, making it a powerful tool for identifying potential support and resistance levels.

CONCEPTS

Liquidity depth analysis helps traders determine how price interacts with supply and demand at different levels. The script processes historical volume data to distinguish between high-liquidity and low-liquidity zones. It assigns transparency levels to plotted lines , ensuring that more relevant liquidity areas stand out visually. The script adds a profile to show the depth of liquidity (derived from historical volume data) for levels above and below the current price

FEATURES

Liquidity Levels: Tracks liquidity levels based on volume concentration at price high and lows.

Volume-Based Transparency: More significant liquidity levels are displayed with higher visibility, showing their significance.

Interpolation: interpolates the bullish and bearish liquidity depth at a user defined range away from the price, helping in comparing the liquidity amounts between bullish and bearish.

Depth Profile: Allows traders to visualize depth of liquidity in a more quantitative and clearer way than the liquidity levels/list]

USAGE

This indicator is best used to track liquidity levels and potential price reaction areas. Traders can adjust the Liquidity Lookback setting to analyze past liquidity levels over different historical periods. The Profile Resolution setting controls the granularity of liquidity depth visualization, with higher values providing more detail. The script can be applied across different timeframes, from intraday scalping to swing trading analysis. The plotted liquidity zones provide traders with insights into where price may encounter strong support, resistance, or potential liquidity-driven reversals.

PnL MonitorThe PnL Monitor is a customizable tool designed to help traders track the Profit and Loss (PnL) of up to 20 currency pairs or assets in real-time. This script provides a clear and organized table that displays the entry price, and PnL percentage for each pair, making it an essential tool for monitoring open positions or tracking potential trades.

Key Features:

Multi-Asset Tracking:

Monitor up to 20 currency pairs or assets simultaneously. Simply input the pair symbol and your entry price, and the script will calculate the PnL in real-time.

Dynamic Table Positioning:

Choose where the table appears on your chart with the Table Position input. Options include:

Top Left

Top Right

Bottom Left

Bottom Right

Real-Time PnL Calculation:

The script fetches the current price of each pair and calculates the PnL percentage based on your entry price. Positive PnL is highlighted in green, while negative PnL is highlighted in red.

Exchange and Pair Separation:

The script automatically separates the exchange name (if provided) from the pair symbol, making it easier to identify the source of the data.

Customizable Inputs:

Add or remove pairs as needed.

Leave the price field blank for pairs you don’t want to track.

How to Use:

Input Your Pairs:

In the script settings, input the symbol of the pair (e.g., NASDAQ:AAPL or BTCUSD) and your entry price. Leave the price field blank for pairs you don’t want to track.

Choose Table Position:

Select where you want the table to appear on your chart.

Monitor PnL:

The table will automatically update with the current price and PnL percentage for each pair.

Why Use This Script?

Efficiency: Track multiple pairs in one place without switching charts.

Clarity: Easily identify profitable and losing positions at a glance.

Flexibility: Customize the table to fit your trading style and preferences.

Ideal For:

Forex, crypto, and stock traders managing multiple positions.

Uptrick: Portfolio Allocation DiversificationIntro

The Uptrick: Portfolio Allocation Diversification script is designed to help traders and investors manage multiple assets simultaneously. It generates signals based on various trading systems, allocates capital using different diversification methods, and displays real-time metrics and performance tables on the chart. The indicator compares active trading strategies with a separate long-term holding (HODL) simulation, allowing you to see how a systematic trading approach stacks up against a simple buy-and-hold strategy.

------------------------------------------------------------------------

Trading System Selection

1. No signals (none)

In this mode, the script does not produce bullish or bearish indicators; every asset stays in a neutral stance. This setup is useful if you prefer to observe how capital might be distributed based solely on the chosen diversification method, with no influence from directional signals.

2. rsi – neutral

This mode uses an index-based measure of whether an asset appears overbought or oversold. It generates a bearish signal if market conditions point to overbought territory, and a bullish signal if they indicate oversold territory. If neither extreme surfaces, it remains neutral. Some traders apply this in sideways or range-bound conditions, where overbought and oversold levels often hint at possible turning points. It does not specifically account for divergence patterns.

3. rsi – long only

In this setting, the system watches for instances where momentum readings strengthen even if the asset’s price is still under pressure or setting new lows. It also considers oversold levels as potential signals for a bullish setup. When such conditions emerge, the script flags a possible move to the upside, ignoring indications that might otherwise suggest a bearish trend. This approach is generally favored by those who want to concentrate exclusively on identifying price recoveries.

4. rsi – short only

Here, the script focuses on spotting signs of deteriorating momentum while an asset’s price remains relatively high or attempts further gains. It also checks whether the market is drifting into overbought territory, suggesting a potential decline. Under such conditions, it issues a bearish signal. It provides no bullish alerts, making it particularly suitable for traders who look to take advantage of overvalued scenarios or protect themselves against sudden downward moves.

5. Deviation from fair value

Under this system, the script judges how far the current price may have strayed from what is considered typical, taking into account normal fluctuations. If the asset appears to be trading at an unusually low level compared to that reference, it is flagged as bullish. If it seems abnormally high, a bearish signal is issued. This can be applied in various market environments to seek opportunities that arise from perceived mispricing.

6. Percentile channel valuation

In this mode, the script determines where an asset's price stands within a historical distribution, highlighting whether it has reached unusually high or low territory compared to its recent past. When the price reaches what is deemed an extreme reading, it may indicate that a reversal is more likely. This approach is often used by traders who watch for statistical outliers and potential reversion to a more typical trading range.

7. ATH valuation

This technique involves comparing an asset's current price with its previously recorded peak values. The script then interprets whether the price is positioned so far below the all-time high that it looks discounted, or so close to that high that it could be overextended. Such perspective is favored by market participants who want to see if an asset still has ample room to climb before matching historic extremes, or if it is nearing a possible ceiling.

8. Z-score system

Here, the script measures how far above or below a standard reference average an asset's price may be, translated into standardized units. Substantial negative readings can suggest a price that might be unusually weak, prompting a bullish indication, while large positive readings could signal overextension and lead to a bearish call. This method is useful for traders watching for abrupt deviations from a norm that often invite a reversion to more balanced levels.

RSI Divergence Period

This input is particularly relevant for the RSI - Long Only and RSI - Short Only modes. The period determines how many bars in the past you compare RSI values to detect any divergences.

------------------------------------------------------------------------

Diversification Method

Once the script has determined a bullish, bearish, or neutral stance for each asset, it then calculates how to distribute capital among all included assets. The diversification method sets the weighting logic.

1. None

Gives each asset an equal weight. For example, if you have five included assets, each might get 20 percent. This is a simple baseline.

2. Risk-Adjusted Expected Return Using Volatility Clustering

Emphasizes each asset’s average returns relative to its observed risk or volatility tendencies. Assets that exhibit good risk-adjusted returns combined with moderate or lower volatility may receive higher weights than more volatile or less appealing assets. This helps steer capital toward assets that have historically provided a better ratio of return to risk.

3. Relative Strength

Allocates more capital to assets that show stronger price strength compared to a reference (for example, price above a long-term moving average plus a higher RSI). Assets in clear uptrends may be given higher allocations.

4. Trend-Following Indicators

Examines trend-based signals, like positive momentum measurements or upward-trending strength indicators, to assign more weight to assets demonstrating strong directional moves. This suits those who prefer to latch onto trending markets.

5. Volatility-Adjusted Momentum

Looks for assets that have strong price momentum but relatively subdued volatility. The script tends to reward assets that are trending well yet are not too volatile, aiming for stable upward performance rather than massive swings.

6. Correlation-Based Risk Parity

Attempts to weight assets in such a way that the overall portfolio risk is more balanced. Although it is not an advanced correlation matrix approach in a strict sense, it conceptually scales each asset’s weight so no single outlier heavily dominates.

7. Omega Ratio Maximization

Gives preference to assets with higher omega ratios. This ratio can be interpreted as the probability-weighted gains versus losses. Assets with a favorable skew are given more capital.

8. Liquidity-Weighted Valuation

Considers each asset’s average trading liquidity, such as the combination of volume and price. More liquid assets typically receive a higher allocation because they can be entered or exited with lower slippage. If the trading system signals bullishness, that can further boost the allocation, and if it signals bearishness, the allocation might be set to zero or reduced drastically.

9. Drawdown-Controlled Allocation (DCA)

Examines each asset’s maximum drawdown over a recent window. Assets experiencing lighter drawdowns (thus indicating somewhat less downside volatility) receive higher allocations, aiming for a smoother overall equity curve.

------------------------------------------------------------------------

Portfolio and Allocation Settings

Portfolio Value

Defines how much total capital is available for the strategy-based investment portion. For example, if set to 10,000, then each asset’s monetary allocation is determined by the percentage weighting times 10,000.

Use Fixed Allocation

When enabled, the script calculates the initial allocation percentages after 50 bars of data have passed. It then locks those percentages for the remainder of the backtest or real-time session. This feature allows traders to test a static weighting scenario to see how it differs from recalculating weights at each bar.

------------------------------------------------------------------------

HODL Simulator

The script has a separate simulation that accumulates positions in an asset whenever it appears to be recovering from an undervalued state. This parallel tracking is intended to contrast a simple buy-and-hold approach with the more adaptive allocation methods used elsewhere in the script.

HODL Buy Quantity

Each time an asset transitions from an undervalued state to a recovery phase, the simulator executes a purchase of a predefined quantity. For example, if set to 0.5 units, the system will accumulate this amount whenever conditions indicate a shift away from undervaluation.

HODL Buy Threshold

This parameter determines the level at which the simulation identifies an asset as transitioning out of an undervalued state. When the asset moves above this threshold after previously being classified as undervalued, a buy order is triggered. Over time, the performance of these accumulated positions is tracked, allowing for a comparison between this passive accumulation method and the more dynamic allocation strategy.

------------------------------------------------------------------------

Asset Table and Display Settings

The script displays data in multiple tables directly on your chart. You can toggle these tables on or off and position them in various corners of your TradingView screen.

Asset Info Table Position

This table provides key details for each included asset, displaying:

Symbol – Identifies the trading pair being monitored. This helps users keep track of which assets are included in the portfolio allocation process.

Current Trading Signal – Indicates whether the asset is in a bullish, bearish, or neutral state based on the selected trading system. This assists in quickly identifying which assets are showing potential trade opportunities.

Volatility Approximation – Represents the asset’s historical price fluctuations. Higher volatility suggests greater price swings, which can impact risk management and position sizing.

Liquidity Estimate – Reflects the asset’s market liquidity, often based on trading volume and price activity. More liquid assets tend to have lower transaction costs and reduced slippage, making them more favorable for active strategies.

Risk-Adjusted Return Value – Measures the asset’s returns relative to its risk level. This helps in determining whether an asset is generating efficient returns for the level of volatility it experiences, which is useful when making allocation decisions.

2. Strategy Allocation Table Position

Displays how your selected diversification method converts each asset into an allocation percentage. It also shows how much capital is being invested per asset, the cumulative return, standard performance metrics (for example, Sharpe ratio), and the separate HODL return percentage.

Symbol – Displays the asset being analyzed, ensuring clarity in allocation distribution.

Allocation Percentage – Represents the proportion of total capital assigned to each asset. This value is determined by the selected diversification method and helps traders understand how funds are distributed within the portfolio.

Investment Amount – Converts the allocation percentage into a dollar value based on the total portfolio size. This shows the exact amount being invested in each asset.

Cumulative Return – Tracks the total return of each asset over time, reflecting how well it has performed since the strategy began.

Sharpe Ratio – Evaluates the asset’s return in relation to its risk by comparing excess returns to volatility. A higher Sharpe ratio suggests a more favorable risk-adjusted performance.

Sortino Ratio – Similar to the Sharpe ratio, but focuses only on downside risk, making it more relevant for traders who prioritize minimizing losses.

Omega Ratio – Compares the probability of achieving gains versus losses, helping to assess whether an asset provides an attractive risk-reward balance.

Maximum Drawdown – Measures the largest percentage decline from an asset’s peak value to its lowest point. This metric helps traders understand the worst-case loss scenario.

HODL Return Percentage – Displays the hypothetical return if the asset had been bought and held instead of traded actively, offering a direct comparison between passive accumulation and the active strategy.

3. Profit Table

If the Profit Table is activated, it provides a summary of the actual dollar-based gains or losses for each asset and calculates the overall profit of the system. This table includes separate columns for profit excluding HODL and the combined total when HODL gains are included. As seen in the image below, this allows users to compare the performance of the active strategy against a passive buy-and-hold approach. The HODL profit percentage is derived from the Portfolio Value input, ensuring a clear comparison of accumulated returns.

4. Best Performing Asset Table

Focuses on the single highest-returning or highest-profit asset at that moment. It highlights the symbol, the asset’s cumulative returns, risk metrics, and other relevant stats. This helps identify which asset is currently outperforming the rest.

5. Most Profitable Asset

A simpler table that underscores the asset producing the highest absolute dollar profit across the portfolio.

------------------------------------------------------------------------

Multi Asset Selection

You can include up to ten different assets (such as BTCUSDT, ETHUSDT, ADAUSDT, and so on) in this script. Each asset has two inputs: one to enable or disable its inclusion, and another to select its trading pair symbol. Once you enable an asset, the script requests the relevant market data from TradingView.

------------------------------------------------------------------------

Uniqness and Features

1. Multiple Data Fetches

Each asset is pulled from the chart’s timeframe, along with various metrics such as RSI, volatility approximations, and trend indicators.

2. Various Risk and Performance Metrics

The script internally keeps track of different measures, like Sharpe ratio (a measure of average return adjusted for risk), Sortino ratio (which focuses on downside volatility), Omega ratio, and maximum drawdown. These metrics feed into the strategy allocation table, helping you quickly assess the risk-and-return profile of each asset.

3. Real-Time Tables

Instead of having to set up complex spreadsheets or external dashboards, the script updates all tables on every new bar. The color schemes in these tables are designed to draw attention to bullish or bearish signals, positive or negative returns, and so forth.

4. HODL Comparison

You can visually compare the active strategy’s results to a separate continuous buy-on-dips accumulation strategy. This allows for insight into whether your dynamic approach truly beats a simpler, more patient method.

5. Locking Allocations

The Use Fixed Allocation input is convenient for those who want to see how holding a fixed distribution of capital performs over time. It helps in distinguishing between constant rebalancing vs a fixed, set-and-forget style.

------------------------------------------------------------------------

How to use

1. Add the Script to Your Chart

Once added, open the settings panel to configure your asset list, choose a trading system, and select the diversification approach.

2. Select Assets

Pick up to ten symbols to monitor. Disable any you do not want included. Each included asset is then handled for signals, diversification, and performance metrics.

3. Choose Trading System

Decide if you prefer RSI-based signals, a fair-value approach, or a percentile-based method, among others. The script will then flag assets as bullish, bearish, or neutral according to that selection.

4. Pick a Diversification Method

For example, you might choose Trend-Following Indicators if you believe momentum stocks or cryptocurrencies will continue their trends. Or you could use the Omega Ratio approach if you want to reward assets that have had a favorable upside probability.

5. Set Portfolio Value and HODL Parameters

Enter how much capital you want to allocate in total (for the dynamic strategy) and adjust HODL buy quantities and thresholds as desired. (HODL Profit % is calculated from the Portfolio Value)

6. Inspect the Tables

On the chart, the script can display multiple tables showing your allocations, returns, risk metrics, and which assets are leading or lagging. Monitor these to make decisions about capital distribution or see how the strategy evolves.

------------------------------------------------------------------------

Additional Remarks

This script aims to simplify multi-asset portfolio management in a single tool. It emphasizes user-friendliness by color-coding the data in tables, so you do not need extra spreadsheets. The script is also flexible in letting you lock allocations or compare dynamic updates.

Always remember that no script can guarantee profitable outcomes. Real markets involve unpredictability, and real trading includes fees, slippage, and liquidity constraints not fully accounted for here. The script uses real-time and historical data for demonstration and educational purposes, providing a testing environment for various systematic strategies.

Performance Considerations

Due to the complexity of this script, users may experience longer loading times, especially when handling multiple assets or using advanced allocation methods. In some cases, calculations may time out if too many settings are adjusted simultaneously. If this occurs, removing and reapplying the indicator to the chart can help reset the process. Additionally, it is recommended to configure inputs gradually instead of adjusting all parameters at once, as excessive changes can extend the script’s loading duration beyond TradingView’s processing limits.

------------------------------------------------------------------------

Originality

This script stands out by integrating multiple asset management techniques within a single indicator, eliminating the need for multiple scripts or external portfolio tools. Unlike traditional single-asset strategies, it simultaneously evaluates multiple assets, applies systematic allocation logic, and tracks risk-adjusted performance in real time. The script is designed to function within TradingView’s script limitations while still allowing for complex portfolio simulations, making it an efficient tool for traders managing diverse holdings. Additionally, its combination of systematic trading signals with allocation-based diversification provides a structured approach to balancing exposure across different market conditions. The dynamic interplay between adaptive trading strategies and passive accumulation further differentiates it from conventional strategy indicators that focus solely on directional signals without considering capital allocation.

Conclusion

Uptrick: Portfolio Allocation Diversification pulls multiple assets into one efficient workflow, where each asset’s signal, volatility, and performance is measured, then assigned a share of capital according to your selected diversification method. The script accommodates both dynamic rebalancing and a locked allocation style, plus an ongoing HODL simulation for passive accumulation comparison. It neatly visualizes the entire process through on-chart tables that are updated every bar.

Traders and investors looking for ways to manage multiple assets under one unified framework can explore the different modules within this script to find what suits their style. Users can quickly switch among trading systems, vary the allocation approach, or review side-by-side performance metrics to see which method aligns best with their risk tolerance and market perspective.

Divergence IQ [TradingIQ]Hello Traders!

Introducing "Divergence IQ"

Divergence IQ lets traders identify divergences between price action and almost ANY TradingView technical indicator. This tool is designed to help you spot potential trend reversals and continuation patterns with a range of configurable features.

Features

Divergence Detection

Detects both regular and hidden divergences for bullish and bearish setups by comparing price movements with changes in the indicator.

Offers two detection methods: one based on classic pivot point analysis and another that provides immediate divergence signals.

Option to use closing prices for divergence detection, allowing you to choose the data that best fits your strategy.

Normalization Options:

Includes multiple normalization techniques such as robust scaling, rolling Z-score, rolling min-max, or no normalization at all.

Adjustable normalization window lets you customize the indicator to suit various market conditions.

Option to display the normalized indicator on the chart for clearer visual comparison.

Allows traders to take indicators that aren't oscillators, and convert them into an oscillator - allowing for better divergence detection.

Simulated Trade Management:

Integrates simulated trade entries and exits based on divergence signals to demonstrate potential trading outcomes.

Customizable exit strategies with options for ATR-based or percentage-based stop loss and profit target settings.

Automatically calculates key trade metrics such as profit percentage, win rate, profit factor, and total trade count.

Visual Enhancements and On-Chart Displays:

Color-coded signals differentiate between bullish, bearish, hidden bullish, and hidden bearish divergence setups.

On-chart labels, lines, and gradient flow visualizations clearly mark divergence signals, entry points, and exit levels.

Configurable settings let you choose whether to display divergence signals on the price chart or in a separate pane.

Performance Metrics Table:

A performance table dynamically displays important statistics like profit, win rate, profit factor, and number of trades.

This feature offers an at-a-glance assessment of how the divergence-based strategy is performing.

The image above shows Divergence IQ successfully identifying and trading a bullish divergence between an indicator and price action!

The image above shows Divergence IQ successfully identifying and trading a bearish divergence between an indicator and price action!

The image above shows Divergence IQ successfully identifying and trading a hidden bullish divergence between an indicator and price action!

The image above shows Divergence IQ successfully identifying and trading a hidden bearish divergence between an indicator and price action!

The performance table is designed to provide a clear summary of simulated trade results based on divergence setups. You can easily review key metrics to assess the strategy’s effectiveness over different time periods.

Customization and Adaptability

Divergence IQ offers a wide range of configurable settings to tailor the indicator to your personal trading approach. You can adjust the lookback and lookahead periods for pivot detection, select your preferred method for normalization, and modify trade exit parameters to manage risk according to your strategy. The tool’s clear visual elements and comprehensive performance metrics make it a useful addition to your technical analysis toolbox.

The image above shows Divergence IQ identifying divergences between price action and OBV with no normalization technique applied.

While traders can look for divergences between OBV and price, OBV doesn't naturally behave like an oscillator, with no definable upper and lower threshold, OBV can infinitely increase or decrease.

With Divergence IQ's ability to normalize any indicator, traders can normalize non-oscillator technical indicators such as OBV, CVD, MACD, or even a moving average.

In the image above, the "Robust Scaling" normalization technique is selected. Consequently, the output of OBV has changed and is now behaving similar to an oscillator-like technical indicator. This makes spotting divergences between the indicator and price easier and more appropriate.

The three normalization techniques included will change the indicator's final output to be more compatible with divergence detection.

This feature can be used with almost any technical indicator.

Stop Type

Traders can select between ATR based profit targets and stop losses, or percentage based profit targets and stop losses.

The image above shows options for the feature.

Divergence Detection Method

A natural pitfall of divergence trading is that it generally takes several bars to "confirm" a divergence. This makes trading the divergence complicated, because the entry at time of the divergence might look great; however, the divergence wasn't actually signaled until several bars later.

To circumvent this issue, Divergence IQ offers two divergence detection mechanisms.

Pivot Detection

Pivot detection mode is the same as almost every divergence indicator on TradingView. The Pivots High Low indicator is used to detect market/indicator highs and lows and, consequently, divergences.

This method generally finds the "best looking" divergences, but will always take additional time to confirm the divergence.

Immediate Detection

Immediate detection mode attempts to reduce lag between the divergence and its confirmation to as little as possible while avoiding repainting.

Immediate detection mode still uses the Pivots Detection model to find the first high/low of a divergence. However, the most recent high/low does not utilize the Pivot Detection model, and instead immediately looks for a divergence between price and an indicator.

Immediate Detection Mode will always signal a divergence one bar after it's occurred, and traders can set alerts in this mode to be alerted as soon as the divergence occurs.

TradingView Backtester Integration

Divergence IQ is fully compatible with the TradingView backtester!

Divergence IQ isn’t designed to be a “profitable strategy” for users to trade. Instead, the intention of including the backtester is to let users backtest divergence-based trading strategies between the asset on their chart and almost any technical indicator, and to see if divergences have any predictive utility in that market.

So while the backtester is available in Divergence IQ, it’s for users to personally figure out if they should consider a divergence an actionable insight, and not a solicitation that Divergence IQ is a profitable trading strategy. Divergence IQ should be thought of as a Divergence backtesting toolkit, not a full-feature trading strategy.

Strategy Properties Used For Backtest

Initial Capital: $1000 - a realistic amount of starting capital that will resonate with many traders

Amount Per Trade: 5% of equity - a realistic amount of capital to invest relative to portfolio size

Commission: 0.02% - a conservative amount of commission to pay for trade that is standard in crypto trading, and very high for other markets.

Slippage: 1 tick - appropriate for liquid markets, but must be increased in markets with low activity.

Once more, the backtester is meant for traders to personally figure out if divergences are actionable trading signals on the market they wish to trade with the indicator they wish to use.

And that's all!

If you have any cool features you think can benefit Divergence IQ - please feel free to share them!

Thank you so much TradingView community!

Destroyer LifeDestroyer Life Strategy - High-Frequency Long & Short Trading

Overview:

The Destroyer Life strategy is an advanced cryptocurrency trading algorithm designed for high-frequency execution on the 15-second timeframe. It combines CRT (Candle Range Trend) and Turtle Soup trading logic with multi-timeframe analysis to optimize entries and exits for both long and short trades. This strategy is specifically optimized for high-volatility crypto pairs, such as SOL/USD on MEXC, ensuring precise execution with minimal drawdown.

Key Features:

15-Second Timeframe Execution: Optimized for ultra-short-term trading.

Long & Short Strategy: Simultaneously identifies profitable buy and sell opportunities.

CRT & Turtle Soup Logic: Leverages price action patterns for enhanced trade accuracy.

Higher Timeframe Analysis (HTF): Incorporates liquidity zones, fair value gaps (FVG), and breaker blocks for context-aware trading.

Dynamic Position Sizing: Uses an adjustable leverage multiplier for risk-controlled trade sizing.

Commission Optimization: Ensures profitability even with trading fees.

Strict Risk Management: Implements exit conditions based on liquidity structure and trend reversals.

Strategy Performance (Backtested on SOL/USD - MEXC):

Overall Profitability: ~80% win rate in backtesting.

Net Profit: $3,151.12 (6.30% ROI).

Gross Profit: $3,795.68 (7.59%).

Gross Loss: $644.56 (1.29%).

Long Trades Profit: $1,459.05 (2.92%).

Short Trades Profit: $1,692.07 (3.38%).

Commission Paid: $924.82.

Minimum Trade Holding Period: 1-minute cooldown between trades.

Trading Logic:

Entry Conditions:

Long Trades: Triggered when the price enters a liquidity void and aligns with higher timeframe bullish bias.

Short Trades: Triggered when price approaches a resistance level with bearish higher timeframe confluence.

CRT & Turtle Soup Patterns: Identifies reversals by analyzing breakout and fake-out structures.

Exit Conditions:

Long Positions Close: Upon price exceeding a 3.88% profit threshold or reversing below an HTF structure.

Short Positions Close: Upon reaching a similar 3.88% threshold or showing strong bullish signals.

Dynamic Position Sizing:

Uses a leverage-based calculation that adapts trade size based on volatility.

Liquidity Awareness:

Tracks Mitigation Blocks (MB), Fair Value Gaps (FVG), Buy/Sell-Side Liquidity (BSL/SSL) to determine optimal execution.

Best Use Cases:

Scalpers & High-Frequency Traders: Those looking for rapid trade execution with short holding periods.

Crypto Traders Focused on Low Timeframes: Optimized for 15-second price action.

Traders Utilizing Liquidity Concepts: Built to exploit liquidity traps and inefficiencies.

Risks & Considerations:

High-Frequency Execution Requires Low Latency: Ensure your broker or exchange supports fast order execution.

Backtested Results May Vary: Real-time performance depends on market conditions.

Commission & Fees Impact Profits: Consider exchanges with low fees to maximize strategy efficiency.

Final Thoughts:

The Destroyer Life Strategy is designed for serious traders looking to take advantage of high-volatility markets with a structured, liquidity-based approach. By combining price action, liquidity concepts, and adaptive risk management, it provides a solid framework for executing high-probability trades on crypto markets.

🚀 Ready to take your trading to the next level? Try Destroyer Life today and dominate the markets!

OHLC LoggerOHLC OG - 10 Candles

The OHLC OG - 10 Candles indicator provides a clear visualization of price action by analyzing the Open, High, Low, and Close (OHLC) data of the last 10 candles. Designed for traders who rely on structured price patterns, this indicator helps in identifying market trends, key support and resistance zones, and potential breakout points.

Features:

✅ Tracks the last 10 candles to highlight significant price movements.

✅ Visualizes Open, High, Low, and Close levels for improved market analysis.

✅ Customizable settings for enhanced adaptability to different strategies.

✅ Works across all timeframes and assets (forex, stocks, crypto, etc.).

✅ Ideal for price action traders looking for structured market insights.

This indicator is perfect for traders who prefer clean and reliable price action analysis without unnecessary complexity. Whether you trade breakouts, trend reversals, or continuation patterns, OHLC OG - 10 Candles helps you stay ahead of the market.

🔹 How to Use:

Apply the indicator to your chart and observe how the OHLC levels react to price movements.

Use it to confirm trends, identify potential breakout zones, or refine entry/exit points.

Combine it with other indicators or strategies for a more comprehensive trading approach.

📌 Disclaimer: This indicator is for educational purposes only. Always conduct proper risk management before trading.

QSL Upside/DownsideThe QSL Upside/Downside Indicator helps traders estimate potential gains and losses using Conditional Value at Risk (cVaR), a statistical measure that assesses both downside risk and upside potential beyond standard volatility. Instead of fixed timeframes (daily, weekly, etc.), traders can set a custom lookback period (in days) to analyze market behavior over their preferred time frame.

How It Works

The indicator calculates cVaR over the chosen period to determine how much an investment could move up or down based on past price behavior. It does this by:

• Mean Return – The average price movement over the period.

• Standard Deviation – Measures price fluctuations from the average.

• cVaR Confidence Interval (95%) – Estimates worst-case losses, meaning the downside projection reflects the worst 5% of expected losses.

• Upside Potential (Best 5%) – Instead of only considering risk, this indicator also calculates the potential upside by measuring returns in the top 5% of past price movements.

This provides a more complete view of what traders can expect—both in terms of risk and potential reward.

Key Features

✅ Custom Lookback Period – Set any number of days to analyze.

✅ cVaR Calculation (95% Confidence Interval) – Identifies extreme downside risks.

✅ Upside Potential (Best 5%) – Estimates how much an investment could rise in a best-case scenario.

✅ Clear Table Display – Quickly see projected best and worst-case portfolio values.

Understanding Probabilities: Upside & Downside Potential

Most traders focus on risk, but it’s equally important to understand potential gains. This indicator provides a probability-based view of expected market moves:

• 95% Confidence Interval (Downside cVaR) – There’s a 5% chance that losses could exceed this level.

• 95% Confidence Interval (Upside cVaR) – There’s a 5% chance that gains could be greater than this level.

• The remaining 90% of expected returns fall between these two extremes.

By knowing both potential losses and gains, traders can make more balanced, data-driven decisions rather than only focusing on worst-case scenarios.

Why Use This Indicator?

🔹 Better Risk & Reward Assessment – Understand both downside risk and upside potential.

🔹 More Realistic Market Projections – Uses probabilities instead of simple historical averages.

🔹 Flexible & Customizable – Works with any asset and any time period.

With this tool, QSL members can strategically plan trades, knowing the expected best and worst-case outcomes with a 95% probability range. 🚀

Date Display with Bar Counter and EMA===== ENGLISH DESCRIPTION =====

OVERVIEW:

This is a multi-function indicator that combines three useful tools in one script:

1. Date Display - Shows current date and symbol information in a customizable table

2. Bar Counter - Displays sequential bar numbers at specified intervals

3. EMA (Exponential Moving Average) - Plots an EMA line with customizable settings

FEATURES:

1. DATE DISPLAY:

- Shows date in full format (e.g., "Mon ∙ January 1, 2023") or short format (e.g., "Mon ∙ 01.01.23")

- Option to show/hide day of week

- Option to show/hide symbol and timeframe information

- Customizable table position (top/middle/bottom, left/center/right)

- Automatic color adjustment based on chart background

2. BAR COUNTER:

- Displays sequential bar numbers below price bars

- Customizable display frequency (every X bars)

- Special handling for Hong Kong futures (resets at market open)

- Different reset logic based on timeframe (daily, weekly, monthly)

- Customizable text size and color

3. EMA INDICATOR:

- Customizable period length (default: 20)

- Option to use different timeframe for calculation

- Option to wait for timeframe close for more stable signals

- Customizable line color

USAGE INSTRUCTIONS:

- After adding the indicator to your chart, customize settings in the "Format" panel

- The Date Display table will appear at your chosen position on the chart

- Bar numbers will appear below price bars at your specified frequency

- The EMA line will be plotted on the chart with your chosen settings

- Colors automatically adjust to light/dark chart themes

===== 中文说明 =====

概述:

这是一个多功能指标,将三个实用工具合并为一个脚本:

1. 日期显示 - 在可自定义的表格中显示当前日期和交易品种信息

2. K线计数器 - 按指定间隔显示K线序号

3. EMA指数移动平均线 - 绘制可自定义设置的EMA线

功能特点:

1. 日期显示:

- 支持完整格式(如"Mon ∙ January 1, 2023")或简短格式(如"Mon ∙ 01.01.23")

- 可选择显示/隐藏星期几

- 可选择显示/隐藏交易品种和时间周期信息

- 可自定义表格位置(顶部/中部/底部,左侧/中间/右侧)

- 根据图表背景自动调整颜色

2. K线计数器:

- 在价格K线下方显示序号

- 可自定义显示频率(每X根K线)

- 对香港期货有特殊处理(在开市时重置)

- 根据时间周期(日线、周线、月线)使用不同的重置逻辑

- 可自定义文字大小和颜色

3. EMA指标:

- 可自定义周期长度(默认:20)

- 可选择使用不同的时间周期进行计算

- 可选择等待时间周期结束以获得更稳定的信号

- 可自定义线条颜色

使用说明:

- 将指标添加到图表后,在"格式"面板中自定义设置

- 日期显示表格将出现在您选择的图表位置

- K线序号将按您指定的频率显示在价格K线下方

- EMA线将根据您选择的设置绘制在图表上

- 颜色会根据浅色/深色图表主题自动调整

*/

Machine Learning + Geometric Moving Average 250/500Indicator Description - Machine Learning + Geometric Moving Average 250/500

This indicator combines password-protected market analysis levels with two powerful Geometric Moving Averages (GMA 250 & GMA 500).

🔒 Password-Protected Custom Levels

Access pre-defined long and short price levels for select assets (crypto, stocks, and more) by entering the correct password in the indicator settings.

Once the correct password is entered, the indicator automatically displays:

Green horizontal lines for long entry zones.

Red horizontal lines for short entry zones.

If the password is incorrect, a warning label will appear on the chart.

📈 Geometric Moving Averages (GMA)

This indicator calculates GMA 250 and GMA 500, two long-term trend-following tools.

Unlike traditional moving averages, GMAs use logarithmic smoothing to better handle exponential price growth, making them especially useful for assets with strong trends (e.g., crypto and tech stocks).

GMA 250 (white line) tracks the medium-term trend.

GMA 500 (gold line) tracks the long-term trend.

⚙️ Customizable & Flexible

Works on multiple assets, including cryptocurrencies, equities, and more.

Adaptable to different timeframes and trading styles — ideal for both swing traders and long-term investors.

This indicator is ideal for traders who want to blend custom support/resistance levels with advanced geometric trend analysis to better navigate both volatile and trending markets.

MacroJP: US Macro Conditions & Forward GuidanceMacroJP is a comprehensive, free-to-use TradingView indicator designed to provide a clear snapshot of the US macroeconomic environment. It consolidates key economic metrics into a single, interactive dashboard, allowing traders and investors to quickly assess current conditions and adjust their portfolio biases accordingly.

How It Works:

• Data Aggregation:

The indicator pulls monthly data from reputable free economic sources—specifically, ISM Manufacturing PMI, US CPI YoY, US M2 Money Supply, and US Treasury yields (10-year and 2-year). This robust dataset forms the backbone of the analysis.

• Composite Calculations:

By calculating a Composite Inflation Indicator (the average of CPI YoY and the yield spread) and evaluating the year-over-year change in M2, MacroJP gauges both the inflationary pressures and liquidity trends in the economy. These composite metrics offer a nuanced view that goes beyond single-indicator analysis.

Regime Classification:

The core strength of MacroJP lies in its quadrant classification system. It categorises the macro environment into four distinct regimes based on the direction of economic growth (derived from PMI) and inflation (from the Composite Inflation Indicator):

• Expansion (Reflation): Indicative of a recovering economy with rising production and moderate inflation—ideal for a bullish equity bias.

• Stagflation Risk: A scenario of weak growth coupled with high inflation, where a defensive posture is recommended.

• Slowdown (Deflationary): Characterised by contracting economic activity and falling prices, suggesting a move towards cash or high-quality bonds.

• Disinflationary Boom: Reflects strong growth with stable or falling inflation—an optimal environment for equities with some bond diversification.

Forward Guidance:

To enhance its predictive capability, MacroJP incorporates leading indicators by shifting key data points. For instance, it uses a forward-shifted M2 YoY value and a one-month shifted CPI proxy to offer insights into near-term trends. This approach helps in anticipating changes, providing a sort of “forward guidance” that can inform strategic asset allocation.

User Education:

The indicator features an intuitive table with on-hover tooltips that explain each metric, its relevance, and recommended investment biases. This educational layer is designed to empower users to not only monitor the economic pulse but also to understand the ‘why’ behind each reading, making it a valuable tool for both novice and experienced investors.

MacroJP brings clarity to complex macroeconomic dynamics, allowing users to make more informed decisions in volatile markets. Its seamless integration of free public data and detailed on-chart annotations makes it an indispensable tool for anyone looking to understand the broader economic context impacting their investments.

— Jaroslav

Pearson Correlation Best MA [victhoreb]Pearson Correlation Best MA is an innovative indicator designed to dynamically select the moving average that best aligns with price action based on the Pearson correlation coefficient. Here’s what it does:

- Multiple MA Evaluation: The indicator computes eight different moving averages — SMA, EMA, DEMA, TEMA, LSMA, RMA, WMA, and VWMA — using a user-defined period.

- Correlation Analysis: For each moving average, it calculates the Pearson correlation with the price (using the average of high and low) over a specified correlation length, then identifies the one with the highest correlation.

- Optional Smoothing: Users can opt to further smooth the selected best moving average for an even more refined signal.

- Visual Cues: The indicator plots the “Best MA” on the chart, colors it based on its direction (bullish or bearish), and also displays the correlation value. Additionally, it can color the price candles to reflect the trend indicated by the best moving average.

- Customizability: All key parameters such as moving average length, correlation length, smoothing options, and color settings are fully customizable.

This tool helps traders by automatically adapting to market conditions—highlighting the moving average that is most in sync with current price trends, potentially improving trade timing and decision-making.

ALN Sessions - for NQ2/24/25 - v1

This script does not calculate any stats.

It uses the sessions and stats from NQStats/ALNSessions

Option to draw boxes around the session times.

Options to adjust the table text/background colors/position.

The logic will determine how the Asia and London sessions interact.

Once the New York session starts (8am), it will then display the appropriate stats.

Script quirk...fyi. The script removes the stats table at 6PM.

That's just how it works. I used grok to assist with the code, and it got funky. It works, so I left it that way.

The appropriate stats table will then be displayed when the next New York session begins.

---

There is another table I used just for troubleshooting to show the values of the Asia/London session highs/lows. This can just be ignored.

3/3/25 - republished.

Exchange and Symbol by BULL┃NETThe B | N EXSY (Exchange and Symbol by BULL | NET)

indicator provides traders using CFD brokers with the most significant price and time events from the stock exchange of the underlying original index or security. For example traders are able to easily identify the price at the Daily Open and Close time of up to three additional stock exchanges. Traders can choose from a huge list of options including the values from the current and previous Day, Week, Month and Year. In addition traders can enable the display of the Expected Move by either implied or historical volatility. The indicator can show Open Gaps (gap between close and open of two trading sessions) also which traders would usually see only on the original chart of an index or security.

The B | N EXSY indicator can help traders to make better entry decisions based on the real market sessions.

█ ⚠️ DISCLAIMER – READ BEFORE YOU USE ⚠️

█ CONCEPTS

CFD Brokers allow you to trade many indices, securities and assets up to 24 hours per day and 7 days per week (24/7). Other than Crypto Assets indices and securities get the highest transaction volume during the session of a stock market. Most importantly while its “Home Stock Market” is open.

For example the NASDAQ or S&P500 will see the highest volume during the business hours of the New York Stock Exchange (NYSE) between 9:30am and 4:00pm (America New York Time). Most CFD Providers however will open their Trading session approximately 9.5 hours before the NYSE opens and even 2 hours before Japan and Australia open the markets.

The German DAX on the other hand is listed on the Deutsche Börse Xetra which is open from 9:00 to 17:00 (Europe Berlin Time). CFD Brokers will open the DAX for trading differently between 9 and 5.5 hours before the XETRA opens.

Therefore most available indicators for visualizing the day open will show different results. Traders at Broker A will tell a totally different story than traders at Broker B who opened 3 hours later.

Furthermore people trading the NASDAQ often keep an eye on the London Stock Exchange (LSE) as well and those trading the NIKKEI often watch the NYSE besides its home at the Japan Exchange Group (JPX).

Advanced traders know about the importance of those information and I have seen thousands of charts where people draw horizontal lines to mark the open and closing prices as well as the session highs and lows. They do it every day and often for different indices and securities. A time consuming job.

Here is where B | N EXSY steps in to give traders objective information for Intraday trading (Daily timeframe and below). More or less automatically. Choose your primary stock exchange (e.g. the NYSE if you trade the NASDAQ) and optionally a second and third stock exchange you are interested in. Individually select the price events you like to see or keep the defaults. Make your own cosmetic decision on how you want the data to be displayed. Save your chart and you will never have to draw a horizontal line again to see the High of the current session, the Low of last week, the monthly Open or yesterdays Close. Sharing ideas with other traders in the chat groups will be easy because everyone is relying on the same information. Even across different CFD Brokers (with slightly different prices of course). Your Technical Analysis can become much more efficient.

█ FEATURES

B | N EXSY is highly customizable. The default settings are optimized for the NASDAQ during the NYSE session. Following you get an overview of all options in the settings menu.

— LOWER TIMEFRAME

The “Lower Timeframe in Minutes” defaults to 30 minutes and should work with most CFD Brokers and stock exchanges. If not you will get a huge warning on the chart suggesting different settings. If e.g. a CFD Broker opens the Dax session at 3:15 but the XETRA opens at 9:00 you have to change the setting to 15.

— STOCK EXCHANGE

Primary is mandatory and defaults to NYSE (New York Stock Exchange) which is the home of the NASDAQ, the S&P 500, the Dow Jones and many others. Usually you select the home stock exchange of the instrument you trade. E.g. XETRA for the DAX, JPX for the NIKKEI or HKEX for the HANG SENG.

The Second and Third stock exchange is optional and defaults to NONE. If e.g. you trade Nvidia with NYSE as the primary stock exchange and you are interested in the High and Low of the European Session select LSE (London Stock Exchange) or XETRA (Deutsche Börse Xetra) as the second stock exchange. By default the indicator will show only information about the current day and week for the second and third stock exchange but you can change that later.

— VISUALIZE SESSIONS

Beginners and less advanced traders sometimes want to see the time span of a session. By default this feature is disabled because it adds more noise to the chart. You can select each of the three stock exchanges individually and select your preferred color.

— CUSTOM STOCK EXCHANGE

Whether your preferred Stock Exchange is missing in the dropdowns or you have a special purpose (see the HOW TO USE section) you can add your own ”Stock Exchange” to the chart.

Name and Country are optional and get displayed in tooltips only. Opening, Closing and Timezone are important. Enter the Open and Close time as HOUR:MINUTE in 24 hour notation (22:00 instead of 10:00pm). The timezone can be provided as time offset in GMT or UTC notation (e.g. GMT+2 or UTC-5) or as a time zone name listed in the IANA Time Zone Database ( e.g. "America/New_York" or “Europe/Berlin”). If you do it wrong the indicator will give wrong results or don’t work at all.

— EXPECTED MOVE IMPLIED VOLATILITY

With this setting you can enable the calculation and display of the Expected Move (EM). Option and Future traders should be familiar with this feature. Those who never heard about should read about it on the internet. Your favorite search engine will provide you with lots of information about it.

After enabling the feature you have to select a source to calculate the EM. The drop down menu contains popular sources and are named after the indices they are based on. It is crucial that the setting match the index, symbol or asset you are trading. If e.g. you are trading a CFD for the NASDAQ you have to select Nasdaq as source. Wrong settings will lead to wrong calculations.

If the source you need is missing you select manually and enter the implied Volatility in the field “Value for manual calculation”. If e.g. you trade the Nikkei you have to enter the current value of the JNIV manually because it is not listed at TradingView so I can’t add it.

The other settings control the Line Color and Style, the Label Color and Size as well as the Text Color.

The indicator will display the EM+ and EM- as well as the 2 and 3 Sigma EM +/-. On the Daily Chart it will display the Weekly Expected Moves. On any timeframe below you will get the Daily Expected Moves.

— EXPECTED MOVE HISTORICAL VOLATILITY

Other than the feature above, this one calculates the EM based on historical volatility.

After enabling the feature you have to enter the amount of days to look back to calculate volatility. Like you would do for a SMA, EMA or RSI. The default is 10 days. Depending on what asset you trade you might play a little with this setting.

The other settings control the Line Color and Style, the Label Color and Size as well as the Text Color.

Like with the Expected Move Implied Volatility this setting will show weekly data on the daily timeframe and daily information on intraday timeframes.

— LABEL AND LINE COSMETICS

The settings in this section control how lines and labels get positioned on the chart and which information the labels show.

● Bar Offset

The bar offset controls the horizontal distance to the last bar on the chart where lines end. By default it is “2” bars to the right. If you use other indicators which show information on the right side you can increase this value to avoid overlapping.

● Bar Anchor

The bar anchor controls where lines start. Default is “lastbar”.

Lastbar sets the start of lines to the last bar of the chart. This provides a very clean chart without lines crossing bars to the left.

Moving sets lines to start at the bar at which the price event occurred. The line for the daily open (DO) price will stay at the opening bar of the stock market and it will do so when it becomes the previous day open (PDO) the next day. The line that marks the session High (DH) will be anchored to the highest bar while the stock market is open. Therefore it might be moving with the advancing chart. The same counts for the session Low (DL). The next day these lines become the previous day high or low (PDH / PDL) and stay at the highest/lowest bar from the day before. This logic is forwarded to all other lines (weekly, monthly, yearly). This gives traders a quick orientation on which bar a price event occurred but a less clean chart.

If you choose Day as bar anchor all lines will start at the beginning of the Brokers trading session in which the price event took place. This is also true for the roll over event when e.g. the Week Open (WO) will become the Previous Week Open (PWO) next Week. Unlike the “moving” setting the new WO and PWO will be anchored to the beginning of the Week. Traders will have a box like view into the past.

● Label Distance Divisor

This setting is used to calculate the minimum vertical distance of labels in means of price points. The internal formular takes the day close price and divides it by the number entered in this field. If e.g. the daily closing price was 5000 the minimum vertical distance would become 1 price point if you enter 5000 for this setting. If the price difference of two events would then be less than 1 the labels would be positioned higher and lower to prevent overlapping. The default value is fine for the Nasdaq (~ 19000 / 5000 = 3.8 at the time of writing). For other indices, securities and assets you should change the divider to your likings or as needed to set the trigger for repositioning labels.

● Distance Modifier

This setting is used to control the vertical shift of the label. The default of Zero disables the setting and activates an internal function which makes a decision based on the used timeframe on the chart (0.1 less than m30, 0.5 from m30 to h4, 0.75 above h4 and 1 for daily). The logic takes the minimum vertical distance and multiplies it by the distance modifier.

In the example above for the label distance divider a label would shift by 1.9 price points on a 30 minute chart if two lines trigger the minimum vertical distance. On the upper line the label moves up and on the lower line it moves down. If three lines are too close to each other the label in the middle does not get moved. If more lines break the minimum distance some labels will overlap until the price is advancing. Those events happen most likely during the opening of a stock exchange.

Price events with equal price, e.g. Day and Week Open at the start of a new week or Day, Week, Month, Year High in the event of a new ATH will get lined up (stacked) horizontally.

While this cosmetic corrections have limits overlapping can be reduced to a minimum.

● Show Price

● Show Exchange

Labels can show up to three information. The price, the stock exchange and the event. The event however can’t be disabled. If you select both options you will see something like

5347.84 for the Day Close of the S&P 500 on the New York Stock Exchange

With this two settings you can disable the display of price and/or stock exchange.

If you have chosen to use more than one stock exchange the setting for “Show Exchange” will be ignored. Otherwise you would not know which Day Close (DC) or Day High (DH) belongs to which stock exchange

● Enable Tooltip

If you decide to hide the price and/or exchange on the label it can be useful to get this information in a tooltip while hovering with the mouse over the label. On the contrary it might become annoying with labels popping up if you have a nervous mouse finger. The feature is disabled by default.

● Equalize Label Size

The size of labels is one of the most discussed issues. Some say it is too small other say it is too big. Label size matters on different devices. “Normal” labels can be too large on a smartphone and too small on a 4k display. And the size is crucial for the automatic horizontal stacking of labels. You simply can’t line up a small, normal and large label in Pine Script (the programming language at TradingView). The stacking is done by prepending labels with spaces to shift them to the right.

This setting overloads all individual size settings for the price events below and activates the automatic horizontal stacking of labels with equal price. It is a convenient way to change the size of all labels with one click in case you have different layouts for different devices.

If you disable this feature you can set the label size individually but you lose the horizontal stacking. This can be useful for traders who display only a few price events or for educational purpose where you want to point out a special event.

— CURRENT DAY

This setting controls which price events of the current day (current session) get displayed and how they appear.

Primary O/C

Enable the Day Open (DO) and Close (DC) for the primary stock exchange. Enabled by default.

Primary H/L

Enable the Day High (DH) and Low (DL) for the primary stock exchange. Enabled by default.

Other O/C

Enable the Day Open (DO) and Close (DC) for the second and third stock exchange. Enabled by default.

Other H/L

Enable the Day High (DH) and Low (DL) for the second and third stock exchange. Enabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— PREVIOS DAY

This setting controls which price events of the previous day get displayed and how they appear.

Primary O/C

Enable the Previous Day Open (PDO) and Close (PDC) for the primary stock exchange. Enabled by default.

Primary H/L

Enable the Previous Day High (PDH) and Low (PDL) for the primary stock exchange. Enabled by default.

Other O/C

Enable the Previous Day Open (PDO) and Close (PDC) for the second and third stock exchange. Disabled by default.

Other H/L

Enable the Previous Day High (PDH) and Low (PDL) for the second and third stock exchange. Disabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— OPENING HOUR

This setting controls whether and how to display the famous opening hour (High and Low within the first 60 minutes after stock market opens)

Primary Cur

Display the Current Day Opening Hour High (OH) and Low (OL) for the primary stock exchange. Enabled by default.

Primary Pre

Display the Previous Day Opening Hour High (POH) and Low (POL) for the primary stock exchange. Enabled by default.

Other Cur

Display the Current Day Opening Hour High (OH) and Low (OL) for the second and third stock exchange. Disabled by default.

Other Pre

Display the Previous Day Opening Hour High (POH) and Low (POL) for the second and third stock exchange. Disabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— CURRENT WEEK

This setting controls which price events of the current week get displayed and how they appear.

Primary O/C

Enable the Week Open (WO) and Close (WC) for the primary stock exchange. Enabled by default.

Primary H/L

Enable the Week High (WH) and Low (WL) for the primary stock exchange. Enabled by default.

Other O/C

Enable the Week Open (WO) and Close (WC) for the second and third stock exchange. Enabled by default.

Other H/L

Enable the Week High (WH) and Low (WL) for the second and third stock exchange. Enabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— PREVIOUS WEEK

This setting controls which price events of the previous week get displayed and how they appear.

Primary O/C

Enable the Previous Week Open (PWO) and Close (PWC) for the primary stock exchange. Enabled by default.

Primary H/L

Enable the Previous Week High (PWH) and Low (PWL) for the primary stock exchange. Enabled by default.

Other O/C

Enable the Previous Week Open (PWO) and Close (PWC) for the second and third stock exchange. Disabled by default.

Other H/L

Enable the Previous Week High (PWH) and Low (PWL) for the second and third stock exchange. Disabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— CURRENT MONTH

This setting controls which price events of the current month get displayed and how they appear.

Primary O/C

Enable the Month Open (MO) and Close (MC) for the primary stock exchange. Enabled by default.

Primary H/L

Enable the Month High (MH) and Low (ML) for the primary stock exchange. Enabled by default.

Other O/C

Enable the Month Open (MO) and Close (MC) for the second and third stock exchange. Disabled by default.

Other H/L

Enable the Month High (MH) and Low (ML) for the second and third stock exchange. Disabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— PREVIOUS MONTH

This setting controls which price events of the previous month get displayed and how they appear.

Primary O/C

Enable the Previous Month Open (PMO) and Close (PMC) for the primary stock exchange. Enabled by default.

Primary H/L

Enable the Previous Month High (PMH) and Low (PML) for the primary stock exchange. Enabled by default.

Other O/C

Enable the Previous Month Open (PMO) and Close (PMC) for the second and third stock exchange. Disabled by default.

Other H/L

Enable the Previous Month High (PMH) and Low (PML) for the second and third stock exchange. Disabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— CURRENT YEAR

This setting controls which price events of the current year get displayed and how they appear.

Primary O/C

Enable the Year Open (YO) and Close (YC) for the primary stock exchange. Enabled by default.

Primary H/L

Enable the Year High (YH) and Low (YL) for the primary stock exchange. Enabled by default.

Other O/C

Enable the Year Open (YO) and Close (YC) for the second and third stock exchange. Disabled by default.

Other H/L

Enable the Year High (YH) and Low (YL) for the second and third stock exchange. Disabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— PREVIOUS YEAR

This setting controls which price events of the previous year get displayed and how they appear.

Primary O/C

Enable the Previous Year Open (PYO) and Close (PYC) for the primary stock exchange. Enabled by default.

Primary H/L

Enable the Previous Year High (PYH) and Low (PYL) for the primary stock exchange. Enabled by default.

Other O/C

Enable the Previous Year Open (PYO) and Close (PYC) for the second and third stock exchange. Disabled by default.

Other H/L

Enable the Previous Year High (PYH) and Low (PYL) for the second and third stock exchange. Disabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— ALL TIME HIGH

This setting controls whether the All Time High gets displayed on the daily chart and how it appears. See the limitations section (Amount of data) for details why the ATH will be displayed in the daily timeframe only.

Primary ATH

Enable the All Time High (ATH) for the primary stock exchange. Enabled by default.

OTHER ATH

Enable the All Time High (ATH) for the second and third stock exchange. Enabled by default.

The settings below control the Line Color and Style, the Label Color and Size as well as the Text Color.

— GAPFINDER

If you look at the original charts of an index (not the CFD Broker chart) you will see mostly every day a price difference between the closing price of the last session and the opening price of the current session. There are many names for those gaps. I call them Open Gaps or Kassa Gaps. Advanced traders know the market tends to close those gaps more or less quickly. Which is one more reason to know where the real previous day close was.

There are market conditions where those gaps are not closed within the new session. Those gap leftovers will usually be closed in the future. Some earlier, some later. If those gaps get more and more you quickly lose track and if the time comes to close one of the gaps you might not remember or recognize the price has reached an old gap. The charts of CFDs don’t even show such gaps due to the fact they trade nearly 24 hours per day.

The Gapfinder will display such leftovers after the end of the next session. If e.g. the previous day close was at 18000 and the market opens the next session at 18200 we have an Open Gap of 200 price points. If the Low of this session is 18100 after the session closes there would be rest gap of 100 price points. The Gapfinder then would mark it with a rectangle colored according to the direction of the Gap.

Bullish gaps result from an opening price (DO) and the current Day Low (DL) being higher than the previous day close (PDC).

Bearish gaps arise from an opening price (DO) and the current Day High (DH) being lower than the previous day closing price (PDC).

If you like you can change the color for the gaps and the text color.

— MISCELLANEOUS

To streamline the appearance of prices they are set to display two decimals only. Numbers get rounded! However, trading currency pairs or crypto assets might need to display the full amount of decimals. In that case simply disable the setting “2 Decimals”.

By default the indicator will display a small table in the lower right corner of the chart. It contains information about the current symbol, the selected primary stock exchange and the volatility. If you don’t like or need it you can disable it.

The “Unreliable Data” checkbox usually should not affect you. But if it does it can be really helpful. The B | N EXSY indicator uses Lower Timeframe Data to match CFD Broker and Stock Exchange opening times. If e.g. a CFD Broker opens at 0:00 and the stock exchange at 9:30 the script uses data from the 30 Minutes timeframe if you view the chart at any timeframe higher than 30 Minutes. Why? Because if you chose a four hours timeframe there is simply no bar that starts at 9:30 in this case. The CFD brokers h4 bars will start at 0:00, 4:00, 8:00, 12:00 and so on.

Sometimes the data stream of the Broker and TradingView get out of sync and a 4 hour bar eventually returns just 6x 30 Minutes instead of 8. During development of the indicator I came across of at least two brokers with such an issue. Only in one time frame and a specific period of time. If this happens the price information might be wrong. A Day High might be to low, a Day Close missing or the Day Open not be found. In such cases your trade might fail. To prevent such situations the indicator performs a daily consistency check at 12:00 during the session for an exchange in its time zone if this option is enabled.

In case the data are found unreliable you will see a label above the bar with further information in the tooltip of the label. You should than compare the information from this timeframe with the lower timeframe selected in the field below. Anway, it is a rare issue and if you, like me, work on multiple timeframes in parallel this bug probably won’t affect you.

— HOLIDAYS

● Holidays

If there is a holiday on a stock market the original chart of an index will simply show no bars for that day. CFD Broker charts will only show no bars if it is an international holiday or the broker itself is affected by the holiday. Take for example Memorial Day in the U.S. Although the NYSE is closed you can trade e.g. the NASDAQ until around 17:30 European Time which is the closing time of the LSE and XETRA. Unfortunately the closing time in Europe is after the opening time in the U.S. If the price goes up in the overlapping time you eventually see a new Weekly High (WH) if you rely on the chart of the CFD Broker. To avoid such misleading information the B | N EXSY indicator allows you to enter holidays for each stock market individually. If the indicator finds a holiday it will not store or add data for this day.

By default there are already the market holidays entered for the NYSE, XETRA, FSX and LSE in 2024. If you want to add your own holidays you have to follow some simple rules:

1. The entry must start in a new line below existing entries (carriage return)

2. The entry starts with the shortcut of the stock exchange exactly as you see them in the dropdown menu.

3. The stock exchange gets separated from the holidays with a colon (:)

4. Each holiday is entered as YYYY-MM-DD

5. Holidays get separated with a single whitespace

The entry for the Japan Exchange Group (JPX) in 2025 would start with:

JPX: 2025-01-01, 2025-01-02, 2025-01-03, 2025-01-08

Completed by the rest of the holiday.

If you make your own entries please keep a copy of the line you added because it will be replaced by the defaults if the indicator gets an update. Best practices would be to provide your holiday string in the comment section and I add it as a default.

● Early Close

Some stock exchanges close the market early before some holidays. In that case the indicator won’t be able to fetch the closing price for that day and the daily roll over won’t work for the day after the holiday. To prevent chaos you can enter the days with early close in this field.

By default the early closing days of the NYSE are already entered. If you want to add your own early closing days you have to follow some simple rules:

1. The entry must start in a new line below existing entries (carriage return)

2. The entry starts with the shortcut of the stock exchange exactly as you see them in the dropdown menu.

3. The stock exchange gets separated from the days with a colon (:)

4. Each early closing day is entered as YYYY-MM-DD-HH-MM where HH-MM is the closing time of this day entered in 24 hours format in the timezone of the stock exchange

5. Days get separated with a single whitespace

The entry for the day before Thanksgiving at the NYSE in 2025 would be:

NYSE:2025-11-25-13-00

This is because the market will close early at 1:00 PM on November 25, 2025, the day before Thanksgiving. The time is provided in 24-hour format as 13:00.

-------------------------------------------------------

Disclaimer BullNet: The information provided in this document is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Any use of the content is at your own risk. No liability is assumed for any losses or damages resulting from reliance on this information. Trading financial instruments involves significant risks, including the potential loss of all invested capital. There is no guarantee of profits or specific outcomes. Please conduct your own research and consult a professional financial advisor if needed.

Disclaimer TradingView: According to the www.tradingview.com

Copyright: 2025-BULLNET - All rights reserved.

Roadmap:

Version 1.0 03.03.2025

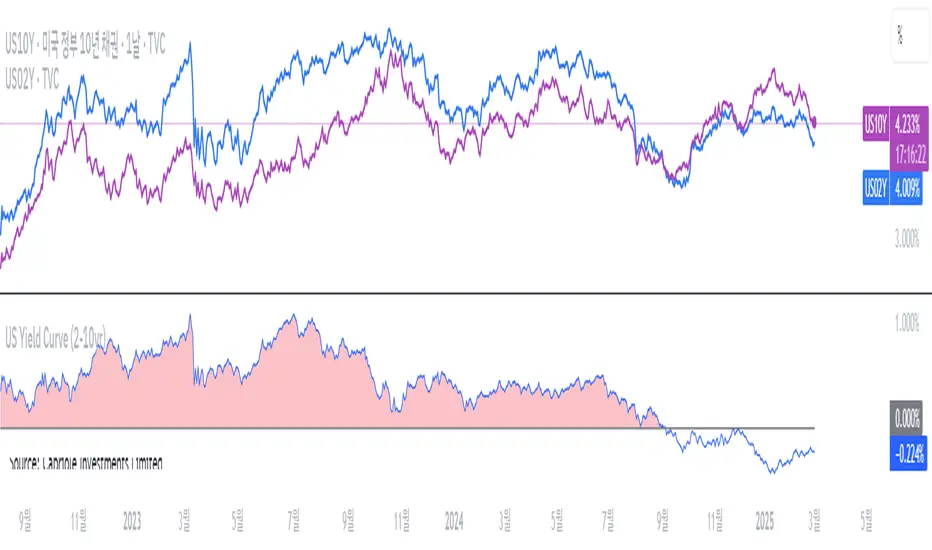

US Yield Curve (2-10yr)US Yield Curve (2-10yr) by oonoon

2-10Y US Yield Curve and Investment Strategies

The 2-10 year US Treasury yield spread measures the difference between the 10-year and 2-year Treasury yields. It is a key indicator of economic conditions.

Inversion (Spread < 0%): When the 2-year yield exceeds the 10-year yield, it signals a potential recession. Investors may shift to long-term bonds (TLT, ZROZ), gold (GLD), or defensive stocks.