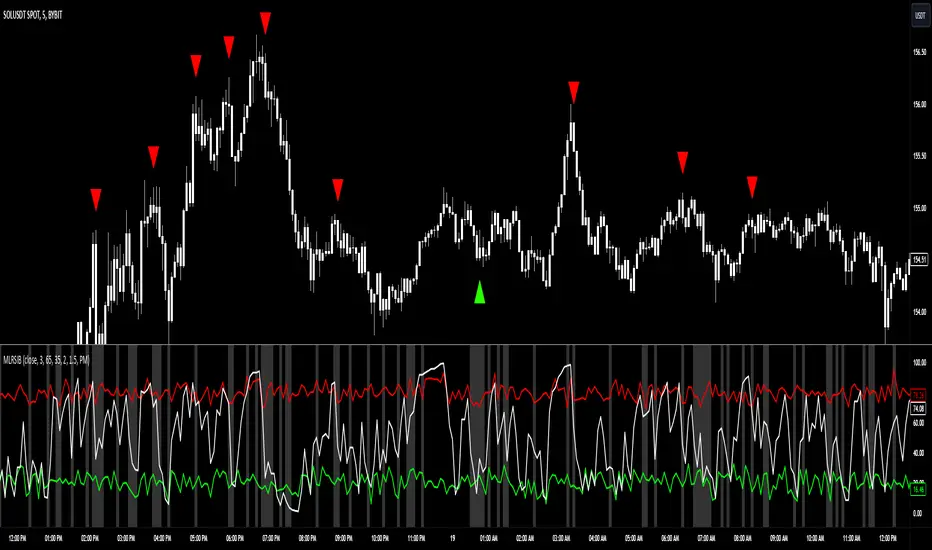

Mean Trend OscillatorMean Trend Oscillator

The Mean Trend Oscillator offers an original approach to trend analysis by integrating multiple technical indicators, using statistic to get a probable signal, and dynamically adapting to market volatility.

This tool aggregates signals from four popular indicators—Relative Strength Index (RSI), Simple Moving Average (SMA), Exponential Moving Average (EMA), and Relative Moving Average (RMA)—and adjusts thresholds using the Average True Range (ATR). By using this, we can use Statistics to aggregate or take the average of each indicators signal. Mathematically, Taking an average of these indicators gives us a better probability on entering a trending state.

By consolidating these distinct perspectives, the Mean Trend Oscillator provides a comprehensive view of market direction, helping traders make informed decisions based on a broad, data-driven trend assessment. Traders can use this indicator to enter long spot or leveraged positions. The Mean Trend Oscillator is intended to be use in long term trending markets. Scalping MUST NOT be used with this indicator. (This indicator will give false signals when the Timeframe is too low. The best intended use for high-quality signals are longer timeframes).

The current price of a beginning trend series may tell us something about the next move. Thus, the Mean Trend Oscillator allows us to spot a high probability trending market and potentially exploit this information enter long or shorts strategy. (again, this indicator will give false signals when the Timeframe is too low. The best intended use for high-quality signals are longer timeframes).

Concept and Calculation and Inputs

The Mean Trend Oscillator calculates a “net trend” score as follows:

RSI evaluates market momentum, identifying overbought and oversold conditions, essential for confirming trend direction.

SMA, EMA, and RMA introduce varied smoothing methods to capture short- to medium-term trends, balancing quick price changes with smoothed averages.

ATR-Enhanced Thresholds: ATR is used as a dynamic multiplier, adjusting each indicator’s thresholds to current volatility levels, which helps reduce noise in low-volatility conditions and emphasizes significant signals when volatility spikes.

Length could be used to adjust how quickly each indicator can more or how slower each indicator can be.

Time Coherency for Inputs: Each indicator must be calculated where each signal is relatively around the same area.

For example:

Simply:

SMA, RMA, EMA, and RSI enters long around each intended trend period. Doesn't have to be perfect, but the indicators all enter long around there.

Each indicator contributes a score (+1 for bullish and -1 for bearish), and these scores are averaged to generate the final trend score:

A positive score, shown as a green line, suggests bullish conditions.

A negative score, indicated by a red line, signifies bearish conditions.

Thus, giving us a signal to long or short.

How to Use the Mean Trend Oscillator

This indicator’s output is straightforward and can fit into various trading strategies:

Bullish Signal: A green line shows that the trend is bullish, based on a positive average score across the indicators, signaling a consideration of longing an asset.

Bearish Signal: A red line indicates bearish conditions, with an overall negative trend score, signaling a consideration to shorting an asset.

By aggregating these indicators, the Mean Trend Oscillator helps traders identify strong trends while filtering out minor fluctuations, making it a versatile tool for both short- and long-term analysis. This multi-layered, adaptive approach to trend detection sets it apart from traditional single-indicator trend tools.

Statistics

Performance Summary and Shading (Offset Version)Modified "Recession and Crisis Shading" Indicator by @haribotagada (Original Link: )

The updated indicator accepts a days offset (positive or negative) to calculate performance between the offset date and the input date.

Potential uses include identifying performance one week after company earnings or an FOMC meeting.

This feature simplifies input by enabling standardized offset dates, while still allowing flexibility to adjust ranges by overriding inputs as needed.

Summary of added features and indicator notes:

Inputs both positive and negative offset.

By default, the script calculates performance from the close of the input date to the close of the date at (input date + offset) for positive offsets, and from the close of (input date - offset) to the close of the input date for negative offsets. For example, with an input date of November 1, 2024, an offset of 7 calculates performance from the close on November 1 to the close on November 8, while an offset of -7 calculates from the close on October 25 to the close on November 1.

Allows user to perform the calculation using the open price on the input date instead of close price

The input format has been modified to allow overrides for the default duration, while retaining the original capabilities of the indicator.

The calculation shows both the average change and the average annualized change. For bar-wise calculations, annualization assumes 252 trading days per year. For date-wise calculations, it assumes 365 days for annualization.

Carries over all previous inputs to retain functionality of the previous script. Changes a few small settings:

Calculates start to end date performance by default instead of peak to trough performance.

Updates visuals of label text to make it easier to read and less transparent.

Changed stat box color scheme to make the text easier to read

Updated default input data to new format of input with offsets

Changed default duration statistic to number of days instead of number of bars with an option to select number of bars.

Potential Features to Add:

Import dataset from CSV files or by plugging into TradingView calendar

Example Input Datasets:

Recessions:

2020-02-01,COVID-19,59

2007-12-01,Subprime mortgages,547

2001-03-01,Dot-com,243

1990-07-01,Oil shock,243

1981-07-01,US unemployment,788

1980-01-01,Volker,182

1973-11-01,OPEC,485

Japan Revolving Door Elections

2006-09-26, Shinzo Abe

2007-09-26, Yasuo Fukuda

2008-09-24, Taro Aso

2009-09-16, Yukio Hatoyama

2010-07-08, Naoto Kan

2011-09-02, Yoshihiko Noda

Hope you find the modified indicator useful and let me know if you would like any features to be added!

Volume StatsDescription:

Volume Stats displays volume data and statistics for every day of the year, and is designed to work on "1D" timeframe. The data is displayed in a table with columns being months of the year, and rows being days of each month. By default, latest data is displayed, but you have an option to switch to data of the previous year as well.

The statistics displayed for each day is:

- volume

- % of total yearly volume

- % of total monthly volume

The statistics displayed for each column (month) is:

- monthly volume

- % of total yearly volume

- sentiment (was there more bullish or bearish volume?)

- min volume (on which day of the month was the min volume)

- max volume (on which day of the month was the max volume)

The cells change their colors depending on whether the volume is bullish or bearish, and what % of total volume the current cell has (either yearly or monthly). The header cells also change their color (based either on sentiment or what % of yearly volume the current month has).

This is the first (and free) version of the indicator, and I'm planning to create a "PRO" version of this indicator in future.

Parameters:

- Timezone

- Cell data -> which data to display in the cells (no data, volume or percentage)

- Highlight min and max volume -> if checked, cells with min and max volume (either monthly or yearly) will be highlighted with a dot or letter (depending on the "Cell data" input)

- Cell stats mode -> which data to use for color and % calculation (All data = yearly, Column = monthly)

- Display data from previous year -> if checked, the data from previous year will be used

- Header color is calculated from -> either sentiment or % of the yearly volume

- Reverse theme -> the table colors are automatically changed based on the "Dark mode" of Tradingview, this checkbox reverses the logic (so that darker colors will be used when "Dark mode" is off, and lighter colors when it's on)

- Hide logo -> hides the cat logo (PLEASE DO NOT HIDE THE CAT)

Conclusion:

Let me know what you think of the indicator. As I said, I'm planning to make a PRO version with more features, for which I already have some ideas, but if you have any suggestions, please let me know.

Presidential Election Day Projection

This indicator analyzes historical price movements during US Presidential elections from 1972-2020. It provides projected price levels based on normalized percentage moves from the daily open, helping traders understand potential price action on the election day.

Features

Analyzes election day candles from 1972-2020

Filters by Democratic or Republican victories

Shows both average and median projections

Projects high, low, and close levels

Comprehensive statistics table with party-specific analysis

The indicator works exclusively on the daily timeframe and projects price levels based on the current day's open price. It normalizes historical moves as percentages to maintain relevance across different price ranges and time periods.

Key Components

Average projections

Median projections

Election Day High, Low and Close

All data presented in the table, lines filtered according to user input.

Notes

Works only on daily timeframe

Updates projections based on each day's opening price

Historical data covers 13 presidential elections

All projections are based on normalized percentage moves

Trade Manager 2Hi Traders,

this manager will make it easier for you to enter lots into your trading platform. Just go to the indicator settings, set your trading account amount, RRR, % risk and then give ok. If you then know where you want to put the stop loss then reopen, enter the value and hit ok again. The chart will show you exactly the stop loss and take profit as you wanted. The stop loss will always stay where you enter it and the take profit will move with the lot size as the price goes further or closer to the stop loss.

This should help when entering the number of lots, TP, SL into the platform.

Up/Down Volume with Normal DistributionThis indicator analyzes the relationship between price movements and trading volume by distinguishing between "up" and "down" volume. Up volume refers to trading volume occurring during price increases, while down volume refers to trading volume during price decreases. The indicator calculates the mean and standard deviation for both up and down volume over a specified length. This statistical approach enables traders to visualize volume deviations from the average, highlighting potential market anomalies that could signal trading opportunities.

Relationship Between Price and Volume

Volume is a critical metric in technical analysis, often considered a leading indicator of price movements. According to studies in financial economics, significant price changes accompanied by high volume tend to indicate strong market conviction (Wyart et al., 2008). Conversely, price changes on low volume may suggest a lack of interest or conviction, making those moves less reliable.

The relationship between price and volume can be summarized as follows:

Confirmation of Trends: High volume accompanying a price increase often confirms an upward trend. Similarly, high volume during price declines indicates bearish sentiment.

Reversals and Exhaustion: Decreases in volume during price increases may suggest a potential reversal or exhaustion of buying pressure, while increased volume during declines can indicate capitulation.

Breakouts: Price movements that break through significant resistance or support levels accompanied by high volume are typically more significant and suggest stronger follow-through in the new direction.

Developing a Trading Strategy

Traders can leverage the insights gained from this relationship to formulate a trading strategy based on volume analysis:

Entry Signals: Traders can enter long positions when the up volume significantly exceeds the mean by a predefined number of standard deviations. This situation indicates strong buying interest. Conversely, short positions can be initiated when down volume exceeds the mean by a specified standard deviation.

Exit Signals: Exiting positions can be based on changes in volume patterns. If the volume starts to decrease significantly after a price increase, this may signal a potential reversal or the need to lock in profits.

Risk Management: Integrating volume analysis with other technical indicators, such as moving averages or RSI, can provide a more comprehensive risk management framework, enhancing the overall effectiveness of the strategy.

In conclusion, understanding the relationship between price and volume, alongside employing statistical measures like the mean and standard deviation, enables traders to create more robust trading strategies that capitalize on market movements.

References

Wyart, M., Bouchaud, J.-P., & Dacorogna, M. (2008). "Self-organized volatility in a complicated market." European Physical Journal B, 61(2), 195-203. doi:10.1140

Quick scan for drift🙏🏻

ML based algorading is all about detecting any kind of non-randomness & exploiting it, kinda speculative stuff, not my way, but still...

Drift is one of the patterns that can be exploited, because pure random walks & noise aint got no drift.

This is an efficient method to quickly scan tons of timeseries on the go & detect the ones with drift by simply checking wherther drift < -0.5 or drift > 0.5. The code can be further optimized both in general and for specific needs, but I left it like dat for clarity so you can understand how it works in a minute not in an hour

^^ proving 0.5 and -0.5 are natural limits with no need to optimize anything, we simply put the metric on random noise and see it sits in between -0.5 and 0.5

You can simply take this one and never check anything again if you require numerous live scans on the go. The metric is purely geometrical, no connection to stats, TSA, DSA or whatever. I've tested numerous formulas involving other scaling techniques, drift estimates etc (even made a recursive algo that had a great potential to be written about in a paper, but not this time I gues lol), this one has the highest info gain aka info content.

The timeseries filtered by this lil metric can be further analyzed & modelled with more sophisticated tools.

Live Long and Prosper

P.S.: there's no such thing as polynomial trend/drift, it's alwasy linear, these curves you see are just really long cycles

P.S.: does cheer still work on TV? @admin

TradingIQ - Reversal IQIntroducing "Reversal IQ" by TradingIQ

Reversal IQ is an exclusive trading algorithm developed by TradingIQ, designed to trade trend reversals in the market. By integrating artificial intelligence and IQ Technology, Reversal IQ analyzes historical and real-time price data to construct a dynamic trading system adaptable to various asset and timeframe combinations.

Philosophy of Reversal IQ

Reversal IQ integrates IQ Technology (AI) with the timeless concept of reversal trading. Markets follow trends that inevitably reverse at some point. Rather than relying on rigid settings or manual judgment to capture these reversals, Reversal IQ dynamically designs, creates, and executes reversal-based trading strategies.

Reversal IQ is designed to work straight out of the box. In fact, its simplicity requires just one user setting, making it incredibly straightforward to manage.

AI Aggressiveness is the only setting that controls how Reversal IQ works.

Traders don’t have to spend hours adjusting settings and trying to find what works best - Reversal IQ handles this on its own.

Key Features of Reversal IQ

Self-Learning Reversal Detection

Employs AI and IQ Technology to identify trend reversals in real-time.

AI-Generated Trading Signals

Provides reversal trading signals derived from self-learning algorithms.

Comprehensive Trading System

Offers clear entry and exit labels.

AI-Determined Profit Target and Stop Loss

Position exit levels are clearly defined and calculated by the AI once the trade is entered.

Performance Tracking

Records and presents trading performance data, easily accessible for user analysis.

Configurable AI Aggressiveness

Allows users to adjust the AI's aggressiveness to match their trading style and risk tolerance.

Long and Short Trading Capabilities

Supports both long and short positions to trade various market conditions.

IQ Channel

The IQ Channel represents what Reversal IQ considers a tradable long opportunity or a tradable short opportunity. The channel is dynamic and adjusts from chart to chart.

IQMA – Proprietary Moving Average

Introduces the IQ Moving Average (IQMA), designed to classify overarching market trends.

IQCandles – Trend Classification Tool

Complements IQMA with candlestick colors designed for trend identification and analysis.

How It Works

Reversal IQ operates on a straightforward heuristic: go long during an extended downside move and go short during an extended upside move.

What defines an "extended move" is determined by IQ Technology, TradingIQ's exclusive AI algorithm. For Reversal IQ, the algorithm assesses the extent to which historical high and low prices are breached. By learning from these price level violations, Reversal IQ adapts to trade future, similar violations in a recurring manner. It calculates a price area, distant from the current price, where a reversal is anticipated.

In simple terms, price peaks (tops) and troughs (bottoms) are stored for Reversal IQ to learn from. The degree to which these levels are violated by subsequent price movements is also recorded. Reversal IQ continuously evaluates this stored data, adapting to market volatility and raw price fluctuations to better capture price reversals.

What classifies as a price top or price bottom?

For Reversal IQ, price tops are considered the highest price attained before a significant downside reversal. Price bottoms are considered the lowest price attained before a significant upside reversal. The highest price achieved is continuously calculated before a significant counter trend price move renders the high price as a swing high. The lowest price achieved is continuously calculated before a significant counter trend price move renders the low price as a swing low.

The image above illustrates the IQ channel and explains the corresponding prices and levels

The blue lower line represents the Long Reversal Level, with the price highlighted in blue showing the Long Reversal Price.

The red upper line represents the Short Reversal Level, with the price highlighted in red showing the Short Reversal Price.

Limit orders are placed at both of these levels. As soon as either level is touched, a trade is immediately executed.

The image above shows a long position being entered after the Long Reversal Level was reached. The profit target and stop loss are calculated by Reversal IQ

The blue line indicates where the profit target is placed (acting as a limit order).

The red line shows where the stop loss is placed (acting as a stop loss order).

Green arrows indicate that the strategy entered a long position at the highlighted price level.

You can also hover over the trade labels to get more information about the trade—such as the entry price, profit target, and stop loss.

The image above demonstrates the profit target being hit for the trade. All profitable trades are marked by a blue arrow and blue line. Hover over the blue arrow to obtain more details about the trade exit.

The image above depicts a short position being entered after the Short Reversal Level was touched. The profit target and stop loss are calculated by the AI

The blue line indicates where the profit target is placed (acting as a limit order).

The red line shows where the stop loss is placed (acting as a stop loss order).

The image above shows the profit target being hit for the short trade. Profitable trades are indicated by a blue arrow and blue line. Hover over the blue arrow to access more information about the trade exit.

Long Entry: Green Arrow

Short Entry: Red Arrow

Profitable Trades: Blue Arrow

Losing Trades: Red Arrow

IQMA

The IQMA implements a dynamic moving average that adapts to market conditions by adjusting its smoothing factor based on its own slope. This makes it more responsive in volatile conditions (steeper slopes) and smoother in less volatile conditions.

The IQMA is not used by Reversal IQ as a trade condition; however, the IQMA can be used by traders to characterize the overarching trend and elect to trade only long positions during bullish conditions and only short positions during bearish conditions.

The IQMA is an adaptive smoothing function that applies a combination of multiple moving averages to reduce lag and noise in the data. The adaptiveness is achieved by dynamically adjusting the Volatility Factor (VF) based on the slope (derivative) of the price trend, making it more responsive to strong trends and smoother in consolidating markets.

This process effectively makes the moving average a self-adjusting filter, the IQMA attempts to track both trending and ranging market conditions by dynamically changing its sensitivity in response to price movements.

When IQMA is blue, an overarching uptrend is in place. When IQMA is red, an overarching downtrend is in place.

IQ Candles

IQ Candles are price candles color-coordinated with IQMA. IQ Candles help visualize the overarching trend and are not used by Reversal IQ to determine trade entries and trade exits.

AI Aggressiveness

Reversal IQ has only one setting that controls its functionality.

AI Aggressiveness controls the aggressiveness of the AI. This setting has three options: Sniper, Aggressive, and Very Aggressive.

Sniper Mode

In Sniper Mode, Reversal IQ will prioritize trading large deviations from established reversal levels and extracting the largest countertrend move possible from them.

Aggressive Mode

In Aggressive Mode, Reversal IQ still prioritizes quality but allows for strong, quantity-based signals. More trades will be executed in this mode with tighter stops and profit targets. Aggressive mode forces Reversal IQ to learn from narrower raw-dollar violations of historical levels.

Very Aggressive Mode

In Very Aggressive Mode, Reversal IQ still prioritizes the strongest quantity-based signals. Stop and target distances aren't inherently affected, but entries will be aggressive while prioritizing performance. Very Aggressive mode forces Reversal IQ to learn from narrower raw-dollar violations of historical levels and also forces it to embrace volatility more aggressively.

AI Direction

The AI Direction setting controls the trade direction Reversal IQ is allowed to take.

“Both” allows for both long and short trades.

“Long” allows for only long trades.

“Short” allows for only short trades.

Verifying Reversal IQ’s Effectiveness

Reversal IQ automatically tracks its performance and displays the profit factor for the long strategy and the short strategy it uses. This information can be found in a table located in the top-right corner of your chart.

The image above shows the long strategy profit factor and the short strategy profit factor for Reversal IQ.

A profit factor greater than 1 indicates a strategy profitably traded historical price data.

A profit factor less than 1 indicates a strategy unprofitably traded historical price data.

A profit factor equal to 1 indicates a strategy did not lose or gain money when trading historical price data.

Using Reversal IQ

While Reversal IQ is a full-fledged trading system with entries and exits, it was designed for the manual trader to take its trading signals and analysis indications to greater heights - offering numerous applications beyond its built-in trading system.

The hallmark feature of Reversal IQ is its sniper-like reversal signals. While exits are dynamically calculated as well, Reversal IQ simply has a knack for "sniping" price reversals.

When performing live analysis, you can use the IQ Channel to evaluate price reversal areas, whether price has extended too far in one direction, and whether price is likely to reverse soon.

Of course, in times of exuberance or panic, price may push through the reversal levels. While infrequent, it can happen to any indicator.

The deeper price moves into the bullish reversal area (blue) the better chance that price has extended too far and will reverse to the upside soon. The deeper price moves into the bearish reversal area (red) the better chance that price has extended too far and will reverse to the downside soon.

Of course, you can set alerts for all Reversal IQ entry and exit signals, effectively following along its systematic conquest of price movement.

TradingIQ - Impulse IQIntroducing "Impulse IQ" by TradingIQ

Impulse IQ is an exclusive trading algorithm developed by TradingIQ, designed to trade breakouts and established trends. By integrating artificial intelligence and IQ Technology, Impulse IQ analyzes historical and real-time price data to construct a dynamic trading system adaptable to various asset and timeframe combinations.

Philosophy of Impulse IQ

Impulse IQ combines IQ Technology (AI) with the classic principles of trend and breakout trading. Recognizing that markets inherently follow trends that need to persist for significant price movements to unfold, Impulse IQ eliminates the need for rigid settings or manual intervention.

Instead, it dynamically develops, adapts, and executes trend-based trading strategies, enabling a more responsive approach to capturing meaningful market opportunities.

Impulse IQ is designed to work straight out of the box. In fact, its simplicity requires just one user setting, making it incredibly straightforward to manage.

Strategy type is the only setting that controls Impulse IQ’s functionality.

Traders don’t have to spend hours adjusting settings and trying to find what works best - Impulse IQ handles this on its own.

Key Features of Impulse IQ

Self-Learning Breakout Detection

Employs IQ Technology to identify breakouts.

AI-Generated Trading Signals

Provides breakout trading signals derived from self-learning algorithms.

Comprehensive Trading System

Offers clear entry and exit labels.

AI-Determined Trailing Profit Target and Stop Loss

Position exit levels are clearly defined and calculated by the AI once the trade is entered.

Performance Tracking

Records and presents trading performance data, easily accessible for user analysis.

Long and Short Trading Capabilities

Supports both long and short positions to trade various market conditions.

IQ Meter

The IQ Meter details where price is trading relative to a higher timeframe trend and lower timeframe trend. Fibonacci levels are interlaced along the meter, offering unique insights on trend retracement opportunities.

Self Learning, Multi Timeframe IQ Zig Zags

The Zig Zag IQ is a self-learning, multi-timeframe indicator that adapts to market volatility, providing a clearer representation of market movements than traditional zig zag indicators.

Dual Strategy Execution

Impulse IQ integrates two distinct strategy types: Breakout and Cheap (details explained later).

How It Works

Before diving deeper into Impulse IQ, it's essential to understand the core terminology:

Zig Zag IQ : A self-learning trend and breakout identification mechanism that serves as the foundation for Impulse IQ. Although it belongs to the “Zig Zag” class of technical indicators, it's powered by IQ Technology.

Impulse IQ : A self-learning trading strategy that executes trades based on Zig Zag IQ. Zig Zag IQ identifies market trends, while Impulse IQ adapts, learns, and executes trades based on these trend characterizations.

Impulse IQ operates on a simple heuristic: go long during upside volatility and go short during downside volatility, essentially capturing price breakouts.

The definition of a “price breakout” is determined by IQ Technology, TradingIQ's exclusive AI algorithm. In Impulse IQ, the algorithm utilizes two IQ Zig Zags (self-learning, multi-timeframe zig zags) to analyze and learn from market trends.

It identifies breakout opportunities by recognizing violations of established price levels marked by the IQ Zig Zags. Impulse IQ then adapts and evolves to trade similar future violations in a recurring and dynamic manner.

Put simply, IQ Zig Zags continuously learn from both historical and real-time price updates to adjust themselves for an "optimal fit" to price data. The aim is to adapt so that the marked price tops and bottoms, when violated, reveal potential breakout opportunities.

The strategy layer of IQ Zig Zags, known as Impulse IQ, incorporates an additional level of self-learning with IQ Technology. It learns from breakout signals generated by the IQ Zig Zags, enabling it to dynamically identify and signal tradable breakouts. Moreover, Impulse IQ learns from historical price data to manage trade exits.

All positions start with an initial fixed stop loss and a trailing stop target. Once the trailing stop target is reached, the fixed stop loss converts into a trailing stop, allowing Impulse IQ to remain in the breakout/trend until the trailing stop is triggered.

What Classifies as a Breakout, Price Top, and Price Bottom?

For Impulse IQ:

Price tops are considered the highest price achieved before a price bottom forms.

Price bottoms are the lowest price reached before a price top forms.

For price tops, the highest price continues to be calculated until a significant downside price move occurs. Similarly, for price bottoms, the lowest price is calculated until a significant upside price move happens.

What distinguishes Zig Zag IQ from other zig zag indicators is its unique mechanism for determining a "significant counter-trend price move." Zig Zag IQ evaluates multiple fits to identify what best suits the current market conditions. Consequently, a "significant counter-trend price move" in one market might differ in magnitude from what’s considered "significant" in another, allowing it to adapt to varying market dynamics.

For example, a 1% price move in the opposite direction might be substantial in one market but not in another, and Zig Zag IQ figures this out internally.

The image above illustrates the IQ Zig Zags in action. The solid Zig Zag IQ lines represent the most recent price move being calculated, while the dotted, shaded lines display historical price moves previously analyzed by IQ Zig Zag.

Notice how the green zig zag aligns with a larger trend, while the purple zig zag follows a smaller trend. This mechanism is crucial for generating breakout signals in Impulse IQ: for a position to be entered, the breakout of the smaller trend must occur in the same direction as the larger trend.

The image above depicts the IQ Meters—an exclusive TradingIQ tool designed to help traders evaluate trend strength and retracement opportunities.

When the lower timeframe Zig Zag IQ and the higher timeframe Zig Zag IQ are out of sync (i.e., one is uptrending while the other is downtrending, with no active positions), the meters display a neutral color, as shown in the image.

The key to using these meters is to identify trend unison and pinpoint key trend retracement entry opportunities. Fibonacci retracement levels for the current trend are interlaced along each meter, and the current price is converted to a retracement ratio of the trend.

These meters can mathematically determine where price stands relative to the larger and smaller trends, aiding in identifying entry opportunities.

The top of each meter indicates the highest price achieved during the current price move.

The bottom of each meter indicates the lowest price achieved during the current price move.

When both the larger and smaller trends are in sync and uptrending, or when a long position is active, the IQ meters turn green, indicating uptrend strength.

When both trends are in sync and downtrending, or when a short position is active, the IQ meters turn red, indicating downtrend strength.

The image above shows the Point of Change for both the larger and smaller Zig Zag IQ trends. A distinctive feature of Zig Zag IQ is its ability to calculate these turning points in advance—unlike most traditional zig zag indicators that lack predetermined turning points and often lag behind price movements. In contrast, Zig Zag IQ offers a minimal-lag trend detection capability, providing a more responsive representation of market trends.

Simply put, once the market Zig Zag anchors are touched, the corresponding Zig Zag IQ will change direction.

Trade Signals

Impulse IQ can trade in one of two ways: Entering breakouts as soon as they happen (Breakout Strategy Type) or entering the pullback of a price breakout (Cheap Strategy Type).

Generally, the Breakout Strategy type will take a greater number of trades and enter a breakout quicker. The Cheap Strategy type will usually take less trades, but potentially enter at a better time/price point, prior to the next leg up of a break up, or the next leg down of a break down.

Entry signals are given when price breaks out to the upside or downside for the "Breakout" strategy type, or for the "Cheap" strategy type, when price retraces to the level it broke out from!

Breakout Strategy Example

The image above demonstrates a long position entered and exited using the Breakout strategy. The price breakout level is marked by the dotted, horizontal green line, representing a previously established price high identified by IQ Zig Zag. Once the price breaks and closes above this level, a long position is initiated.

After entering a long position, Impulse IQ immediately displays the initial fixed stop price. As the price moves favorably for the long position, the trailing stop conversion level is reached, and the indicator switches to a trailing stop, as shown in the image. Impulse IQ continues to "ride the trend" for as long as it persists, exiting only when the trailing stop is triggered.

Cheap Strategy Example

The image above shows a short entry executed using the Cheap strategy. The aim of the Cheap strategy is to enter on a pullback before the breakout occurs. While this results in fewer trades if price doesn’t pull back before the breakout, it typically allows for a better entry time and price point when a pullback does happen.

The image above illustrates the remainder of the trade until the trailing stop was hit.

Green Arrow = Long Entry

Red Arrow = Short Entry

Blue Arrow = Trade Exit

Impulse IQ calculates the initial stop price and trailing stop distance before any entry signals are triggered. This means users don’t need to constantly tweak these settings to improve performance—Impulse IQ handles this process internally.

Verifying Impulse IQ’s Effectiveness

Impulse IQ automatically tracks its performance and displays the profit factor for both its long and short strategies, visible in a table located in the top-right corner of your chart.

The image above shows the profit factor for both the long and short strategies used by Impulse IQ.

A profit factor greater than 1 indicates that the strategy was profitable when trading historical price data.

A profit factor less than 1 indicates that the strategy was unprofitable when trading historical price data.

A profit factor equal to 1 indicates that the strategy neither gained nor lost money on historical price data.

Using Impulse IQ

While Impulse IQ functions as a comprehensive trading system with its own entry and exit signals, it was designed for the manual trader to take its trading signals and analysis indications to greater heights - offering numerous applications beyond its built-in trading system.

The standout feature of Impulse IQ is its ability to characterize and capitalize on trends. Keeping a close eye on “Breakout” labels and making use of the IQ meter is the best way to use Impulse IQ.

The IQ Meters can be used to:

Find entry points during trend retracements

Assess trend alignment across higher and lower timeframes

Evaluate overall trend strength, indicating where the price lies on both IQ Meters.

Additionally, "Break Up" and "Break Down" labels can be identified for anticipating breakouts. Impulse IQ self-learns to capture breakouts optimally, making these labels dynamic signals for predicting a breakout.

The Zig Zag IQ indicators are instrumental in characterizing the market's current state. As a self-learning tool, Zig Zag IQ constantly adapts to improve the representation of current price action. The price tops and bottoms identified by Zig Zag IQ can be treated as support/resistance and breakout levels.

Of course, you can set alerts for all Impulse IQ entry and exit signals, effectively following along its systematic conquest of price movement.

TradingIQ - Nova IQIntroducing "Nova IQ" by TradingIQ

Nova IQ is an exclusive Trading IQ algorithm designed for extended price move scalping. It spots overextended micro price moves and bets against them. In this way, Nova IQ functions similarly to a reversion strategy.

Nova IQ analyzes historical and real-time price data to construct a dynamic trading system adaptable to various asset and timeframe combinations.

Philosophy of Nova IQ

Nova IQ integrates AI with the concept of central-value reversion scalping. On lower timeframes, prices may overextend for small periods of time - which Nova IQ looks to bet against. In this sense, Nova IQ scalps against small, extended price moves on lower timeframes.

Nova IQ is designed to work straight out of the box. In fact, its simplicity requires just one user setting, making it incredibly straightforward to manage.

Use HTF (used to apply a higher timeframe trade filter) is the only setting that controls how Nova IQ works.

Traders don’t have to spend hours adjusting settings and trying to find what works best - Nova IQ handles this on its own.

Key Features of Nova IQ

Self-Learning Market Scalping

Employs AI and IQ Technology to scalp micro price overextensions.

AI-Generated Trading Signals

Provides scalping signals derived from self-learning algorithms.

Comprehensive Trading System

Offers clear entry and exit labels.

Performance Tracking

Records and presents trading performance data, easily accessible for user analysis.

Higher Timeframe Filter

Allows users to implement a higher timeframe trading filter.

Long and Short Trading Capabilities

Supports both long and short positions to trade various market conditions.

Nova Oscillator (NOSC)

The Nova IQ Oscillator (NOSC) is an exclusive self-learning oscillator developed by Trading IQ. Using IQ Technology, the NOSC functions as an all-in-one oscillator for evaluating price overextensions.

Nova Bands (NBANDS)

The Nova Bands (NBANDS) are based on a proprietary calculation and serve as a custom two-layer smoothing filter that uses exponential decay. These bands adaptively smooth prices to identify potential trend retracement opportunities.

How It Works

Nova IQ operates on a simple heuristic: scalp long during micro downside overextensions and short during micro upside overextensions.

What constitutes an "overextension" is defined by IQ Technology, TradingIQ's proprietary AI algorithm. For Nova IQ, this algorithm evaluates the typical extent of micro overextensions before a reversal occurs. By learning from these patterns, Nova IQ adapts to identify and trade future overextensions in a consistent manner.

In essence, Nova IQ learns from price movements within scalping timeframes to pinpoint price areas for capitalizing on the reversal of an overextension.

As a trading system, Nova IQ enters all positions using market orders at the bar’s close. Each trade is exited with a profit-taking limit order and a stop-loss order. Thanks to its self-learning capability, Nova IQ determines the most suitable profit target and stop-loss levels, eliminating the need for the user to adjust any settings.

What classifies as a tradable overextension?

For Nova IQ, tradable overextensions are not manually set but are learned by the system. Nova IQ utilizes NOSC to identify and classify micro overextensions. By analyzing multiple variations of NOSC, along with its consistency in signaling overextensions and its tendency to remain in extreme zones, Nova IQ dynamically adjusts NOSC to determine what constitutes overextension territory for the indicator.

When NOSC reaches the downside overextension zone, long trades become eligible for entry. Conversely, when NOSC reaches the upside overextension zone, short trades become eligible for entry.

The image above illustrates NOSC and explains the corresponding overextension zones

The blue lower line represents the Downside Overextension Zone.

The red upper line represents the Upside Overextension Zone.

Any area between the two deviation points is not considered a tradable price overextension.

When either of the overextension zones are breached, Nova IQ will get to work at determining a trade opportunity.

The image above shows a long position being entered after the Downside Overextension Zone was reached.

The blue line on the price scale shows the AI-calculated profit target for the scalp position. The redline shows the AI-calculated stop loss for the scalp position.

Blue arrows indicate that the strategy entered a long position at the highlighted price level.

Yellow arrows indicate a position was closed.

You can also hover over the trade labels to get more information about the trade—such as the entry price and exit price.

The image above depicts a short position being entered after the Upside Overextension Zone was breached.

The blue line on the price scale shows the AI-calculated profit target for the scalp position. The redline shows the AI-calculated stop loss for the scalp position.

Red arrows indicate that the strategy entered a short position at the highlighted price level.

Yellow arrows indicate that NOVA IQ exited a position.

Long Entry: Blue Arrow

Short Entry: Red Arrow

Closed Trade: Yellow Arrow

Nova Bands

The Nova Bands (NBANDS) are based on a proprietary calculation and serve as a custom two-layer smoothing filter that uses exponential decay and cosine factors.

These bands adaptively smooth the price to identify potential trend retracement opportunities.

The image above illustrates how to interpret NBANDS. While NOSC focuses on identifying micro overextensions, NBANDS is designed to capture larger price overextensions. As a result, the two indicators complement each other well and can be effectively used together to identify a broader range of price overextensions in the market.

While the Nova Bands are not part of the core heuristic and do not use IQ technology, they provide valuable insights for discretionary traders looking to refine their strategies.

Use HTF (Use Higher Timeframe) Setting

Nova IQ has only one setting that controls its functionality.

“Use HTF” controls whether the AI uses a higher timeframe trading filter. This setting can be true or false. If true, the trader must select the higher timeframe to implement.

No Higher TF Filter

Nova IQ operates with standard aggression when the higher timeframe setting is turned off. In this mode, it exclusively learns from the price data of the current chart, allowing it to trade more aggressively without the influence of a higher timeframe filter.

Higher TF Filter

Nova IQ demonstrates reduced aggression when the "Use HTF" (Higher Timeframe) setting is enabled. In this mode, Nova IQ learns from both the current chart's data and the selected higher timeframe data, factoring in the higher timeframe trend when seeking scalping opportunities. As a result, trading opportunities only arise when both the higher timeframe and the chart's timeframe simultaneously display overextensions, making this mode more selective in its entries.

In this mode, Nova IQ calculates NOSC on the higher timeframe, learns from the corresponding price data, and applies the same rules to NOSC as it does for the current chart's timeframe. This ensures that Nova IQ consistently evaluates overextensions across both timeframes, maintaining its trading logic while incorporating higher timeframe insights.

AI Direction

The AI Direction setting controls the trade direction Nova IQ is allowed to take.

“Trade Longs” allows for long trades.

“Trade Shorts” allows for short trades.

Verifying Nova IQ’s Effectiveness

Nova IQ automatically tracks its performance and displays the profit factor for the long strategy and the short strategy it uses. This information can be found in a table located in the top-right corner of your chart showing the long strategy profit factor and the short strategy profit factor.

The image above shows the long strategy profit factor and the short strategy profit factor for Nova IQ.

A profit factor greater than 1 indicates a strategy profitably traded historical price data.

A profit factor less than 1 indicates a strategy unprofitably traded historical price data.

A profit factor equal to 1 indicates a strategy did not lose or gain money when trading historical price data.

Using Nova IQ

While Nova IQ is a full-fledged trading system with entries and exits - it was designed for the manual trader to take its trading signals and analysis indications to greater heights, offering numerous applications beyond its built-in trading system.

The hallmark feature of Nova IQ is its to ignore noise and only generate signals during tradable overextensions.

The best way to identify overextensions with Nova IQ is with NOSC.

NOSC is naturally adept at identifying micro overextensions. While it can be interpreted in a manner similar to traditional oscillators like RSI or Stochastic, NOSC’s underlying calculation and self-learning capabilities make it significantly more advanced and useful than conventional oscillators.

Additionally, manual traders can benefit from using NBANDS. Although NBANDS aren't a core component of Nova IQ's guiding heuristic, they can be valuable for manual trading. Prices rarely extend beyond these bands, and it's uncommon for prices to consistently trade outside of them.

NBANDS do not incorporate IQ Technology; however, when combined with NOSC, traders can identify strong double-confluence opportunities.

ShuffleOverview

This TV script is designed to assist traders by visually marking key price levels and identifying potential trading opportunities on their charts. The script highlights the previous day's, week's, and month's highs and lows, as well as hourly fair value gaps. By providing clear visual indicators, traders can make more informed decisions based on significant price movements and gaps in the market.

Features

1. Previous Day Highs and Lows

Highs and Lows: Automatically plots the highest and lowest price points from the previous trading day.

Visual Indicators: Uses distinct colors and lines to differentiate between highs and lows for easy identification.

Alerts: Optional alerts when current price approaches these levels.

2. Weekly Highs and Lows

Weekly Range: Marks the highest and lowest prices of the current week.

Trend Analysis: Helps in identifying the overall trend direction based on weekly extremes.

Support and Resistance: Acts as dynamic support and resistance levels for potential trade setups.

3. Monthly Highs and Lows

Monthly Extremes: Highlights the highest and lowest prices recorded in the current month.

Long-Term Perspective: Provides insights into long-term market sentiment and potential major support/resistance zones.

Investment Decisions: Aids in making strategic investment decisions based on significant monthly price movements.

4. Hourly Fair Value Gaps

Fair Value Gaps (FVG): Identifies gaps between the high of one hour and the low of the next hour where no trading has occurred.

Price Retracement: Marks areas where price is likely to retrace to fill these gaps, offering potential entry points.

Gap Analysis: Assists in understanding market inefficiencies and potential price corrections.

Z-Score Weighted Trend System I [InvestorUnknown]The Z-Score Weighted Trend System I is an advanced and experimental trading indicator designed to utilize a combination of slow and fast indicators for a comprehensive analysis of market trends. The system is designed to identify stable trends using slower indicators while capturing rapid market shifts through dynamically weighted fast indicators. The core of this indicator is the dynamic weighting mechanism that utilizes the Z-score of price , allowing the system to respond effectively to significant market movements.

Dynamic Z-Score-Based Weighting System

The Z-Score Weighted Trend System I utilizes the Z-score of price to assign weights dynamically to fast indicators. This mechanism is designed to capture rapid market shifts at potential turning points, providing timely entry and exit signals.

Traders can choose from two primary weighting mechanisms:

Threshold-Based Weighting: The fast indicators are given weight only when the absolute Z-score exceeds a user-defined threshold. Below this threshold, fast indicators have no impact on the final signal.

Continuous Weighting: By setting the threshold to zero, fast indicators always contribute to the final signal, regardless of Z-score levels. However, this increases the likelihood of false signals during ranging or low-volatility markets

// Calculate weight for Fast Indicators based on Z-Score (Slow Indicator weight is kept to 1 for simplicity)

f_zscore_weights(series float z, simple float weight_thre) =>

float fast_weight = na

float slow_weight = na

if weight_thre > 0

if math.abs(z) <= weight_thre

fast_weight := 0

slow_weight := 1

else

fast_weight := 0 + math.sqrt(math.abs(z))

slow_weight := 1

else

fast_weight := 0 + math.sqrt(math.abs(z))

slow_weight := 1

Choice of Z-Score Normalization

Traders have the flexibility to select different Z-score processing methods to better suit their trading preferences:

Raw Z-Score or Moving Average: Traders can opt for either the raw Z-score or a moving average of the Z-score to smooth out fluctuations.

Normalized Z-Score (ranging from -1 to 1) or Z-Score Percentile: The normalized Z-score is simply the raw Z-score divided by 3, while the Z-score percentile utilizes a normal distribution for transformation.

f_zscore_perc(series float zscore_src, simple int zscore_len, simple string zscore_a, simple string zscore_b, simple string ma_type, simple int ma_len) =>

z = (zscore_src - ta.sma(zscore_src, zscore_len)) / ta.stdev(zscore_src, zscore_len)

zscore = switch zscore_a

"Z-Score" => z

"Z-Score MA" => ma_type == "EMA" ? (ta.ema(z, ma_len)) : (ta.sma(z, ma_len))

output = switch zscore_b

"Normalized Z-Score" => (zscore / 3) > 1 ? 1 : (zscore / 3) < -1 ? -1 : (zscore / 3)

"Z-Score Percentile" => (f_percentileFromZScore(zscore) - 0.5) * 2

output

Slow and Fast Indicators

The indicator uses a combination of slow and fast indicators:

Slow Indicators (constant weight) for stable trend identification: DMI (Directional Movement Index), CCI (Commodity Channel Index), Aroon

Fast Indicators (dynamic weight) to identify rapid trend shifts: ZLEMA (Zero-Lag Exponential Moving Average), IIRF (Infinite Impulse Response Filter)

Each indicator is calculated using for-loop methods to provide a smoothed and averaged view of price data over varying lengths, ensuring stability for slow indicators and responsiveness for fast indicators.

Signal Calculation

The final trading signal is determined by a weighted combination of both slow and fast indicators. The slow indicators provide a stable view of the trend, while the fast indicators offer agile responses to rapid market movements. The signal calculation takes into account the dynamic weighting of fast indicators based on the Z-score:

// Calculate Signal (as weighted average)

float sig = math.round(((DMI*slow_w) + (CCI*slow_w) + (Aroon*slow_w) + (ZLEMA*fast_w) + (IIRF*fast_w)) / (3*slow_w + 2*fast_w), 2)

Backtest Mode and Performance Metrics

The indicator features a detailed backtesting mode, allowing traders to compare the effectiveness of their selected settings against a traditional Buy & Hold strategy. The backtesting provides:

Equity calculation based on signals generated by the indicator.

Performance metrics comparing Buy & Hold metrics with the system’s signals, including: Mean, positive, and negative return percentages, Standard deviations, Sharpe, Sortino, and Omega Ratios

// Calculate Performance Metrics

f_PerformanceMetrics(series float base, int Lookback, simple float startDate, bool Annualize = true) =>

// Initialize variables for positive and negative returns

pos_sum = 0.0

neg_sum = 0.0

pos_count = 0

neg_count = 0

returns_sum = 0.0

returns_squared_sum = 0.0

pos_returns_squared_sum = 0.0

neg_returns_squared_sum = 0.0

// Loop through the past 'Lookback' bars to calculate sums and counts

if (time >= startDate)

for i = 0 to Lookback - 1

r = (base - base ) / base

returns_sum += r

returns_squared_sum += r * r

if r > 0

pos_sum += r

pos_count += 1

pos_returns_squared_sum += r * r

if r < 0

neg_sum += r

neg_count += 1

neg_returns_squared_sum += r * r

float export_array = array.new_float(12)

// Calculate means

mean_all = math.round((returns_sum / Lookback), 4)

mean_pos = math.round((pos_count != 0 ? pos_sum / pos_count : na), 4)

mean_neg = math.round((neg_count != 0 ? neg_sum / neg_count : na), 4)

// Calculate standard deviations

stddev_all = math.round((math.sqrt((returns_squared_sum - (returns_sum * returns_sum) / Lookback) / Lookback)) * 100, 2)

stddev_pos = math.round((pos_count != 0 ? math.sqrt((pos_returns_squared_sum - (pos_sum * pos_sum) / pos_count) / pos_count) : na) * 100, 2)

stddev_neg = math.round((neg_count != 0 ? math.sqrt((neg_returns_squared_sum - (neg_sum * neg_sum) / neg_count) / neg_count) : na) * 100, 2)

// Calculate probabilities

prob_pos = math.round((pos_count / Lookback) * 100, 2)

prob_neg = math.round((neg_count / Lookback) * 100, 2)

prob_neu = math.round(((Lookback - pos_count - neg_count) / Lookback) * 100, 2)

// Calculate ratios

sharpe_ratio = math.round((mean_all / stddev_all * (Annualize ? math.sqrt(Lookback) : 1))* 100, 2)

sortino_ratio = math.round((mean_all / stddev_neg * (Annualize ? math.sqrt(Lookback) : 1))* 100, 2)

omega_ratio = math.round(pos_sum / math.abs(neg_sum), 2)

// Set values in the array

array.set(export_array, 0, mean_all), array.set(export_array, 1, mean_pos), array.set(export_array, 2, mean_neg),

array.set(export_array, 3, stddev_all), array.set(export_array, 4, stddev_pos), array.set(export_array, 5, stddev_neg),

array.set(export_array, 6, prob_pos), array.set(export_array, 7, prob_neu), array.set(export_array, 8, prob_neg),

array.set(export_array, 9, sharpe_ratio), array.set(export_array, 10, sortino_ratio), array.set(export_array, 11, omega_ratio)

// Export the array

export_array

//}

Calibration Mode

A Calibration Mode is included for traders to focus on individual indicators, helping them fine-tune their settings without the influence of other components. In Calibration Mode, the user can visualize each indicator separately, making it easier to adjust parameters.

Alerts

The indicator includes alerts for long and short signals when the indicator changes direction, allowing traders to set automated notifications for key market events.

// Alert Conditions

alertcondition(long_alert, "LONG (Z-Score Weighted Trend System)", "Z-Score Weighted Trend System flipped ⬆LONG⬆")

alertcondition(short_alert, "SHORT (Z-Score Weighted Trend System)", "Z-Score Weighted Trend System flipped ⬇Short⬇")

Important Note:

The default settings of this indicator are not optimized for any particular market condition. They are generic starting points for experimentation. Traders are encouraged to use the calibration tools and backtesting features to adjust the system to their specific trading needs.

The results generated from the backtest are purely historical and are not indicative of future results. Market conditions can change, and the performance of this system may differ under different circumstances. Traders and investors should exercise caution and conduct their own research before using this indicator for any trading decisions.

aPortfolioaPortfolio can be overlayed on any chart with any timeframe. It provides a way to keep track of your portfolio(s) real-time and dynamically. Tool tips provide information about each input item.

Up to 8 customizable assets can be defined using 2 exchanges. The amount owned, the exchange used and the amount spent (in Euro or US Dollar) can be entered per asset.

Furthermore, available Euros and US Dollars can be entered as part of your portfolio.

The output consists of a label and a table , which can both be configured or switched off.

The label is being displayed at the current bar and price on the chart. It can show various totals and a total profit percentage.

The table display position can be set to “AUTO” or to a fixed customizable position. Per used asset, it can show the amount, value in BTC, value in Euro, value in US Dollar and value in a customizable currency. Also, the profit percentage and the percentage of the total portfolio value of an asset can be shown.

The total line shows the values and the profit percentage of the whole portfolio.

In the VIEW options, on the bottom of the settings/inputs window, the coloring can be customized. The profit percentages provide dynamic coloring.

It is also possible to use the EU (#.###,#) format in stead of the US format for numbers.

Although it has its limitations, aPortfolio might be useful and conveniently provides real-time insight.

GuidoN - October 2024

Machine Learning RSI Bands"Machine Learning RSI Bands" Indicator

The "Machine Learning RSI Bands" (MLRSIB) indicator leverages advanced algorithmic analysis to enhance traditional RSI strategies:

RSI Customization: Users can customize the RSI settings including source, length, and thresholds for overbought/oversold conditions.

Innovative Machine Learning Application: The script uses a proprietary function FOUNDATION_400x10x2 from the 'FOUNDATION' library, which analyzes the last 400 occurrences of data points, considering various market dynamics like volume changes or RSI movements based on the selected sampling method. Outputs four optimal outcomes for both upper and lower band conditions, representing the most statistically significant patterns or predictions.

Dynamic Band Visualization: Plots the average of these four outcomes as colored lines (red for the upper band, green for the lower band) on the chart, serving as dynamic support and resistance or overbought/oversold levels.

Signal Plotting: Displays triangles above or below the bars to signal potential short or long entries when the RSI crosses these machine learning-adjusted bands under certain confidence conditions.

Market Volatility Indicator: Adjusts the chart's background color based on volatility, using an average deviation analysis to gauge market calmness or agitation.

Alert System: Provides alert conditions for when these sophisticated signals are triggered, allowing for timely trading actions.

This indicator is designed for traders interested in combining traditional technical analysis with machine learning to refine their market entry and exit strategies, focusing on patterns identified from recent market behavior.

Keltner Channel Strategy by Kevin DaveyKeltner Channel Strategy Description

The Keltner Channel Strategy is a volatility-based trading approach that uses the Keltner Channel, a technical indicator derived from the Exponential Moving Average (EMA) and Average True Range (ATR). The strategy helps identify potential breakout or mean-reversion opportunities in the market by plotting upper and lower bands around a central EMA, with the channel width determined by a multiplier of the ATR.

Components:

1. Exponential Moving Average (EMA):

The EMA smooths price data by placing greater weight on recent prices, allowing traders to track the market’s underlying trend more effectively than a simple moving average (SMA). In this strategy, a 20-period EMA is used as the midline of the Keltner Channel.

2. Average True Range (ATR):

The ATR measures market volatility over a 14-period lookback. By calculating the average of the true ranges (the greatest of the current high minus the current low, the absolute value of the current high minus the previous close, or the absolute value of the current low minus the previous close), the ATR captures how much an asset typically moves over a given period.

3. Keltner Channel:

The upper and lower boundaries are set by adding or subtracting 1.5 times the ATR from the EMA. These boundaries create a dynamic range that adjusts with market volatility.

Trading Logic:

• Long Entry Condition: The strategy enters a long position when the closing price falls below the lower Keltner Channel, indicating a potential buying opportunity at a support level.

• Short Entry Condition: The strategy enters a short position when the closing price exceeds the upper Keltner Channel, signaling a potential selling opportunity at a resistance level.

The strategy plots the upper and lower Keltner Channels and the EMA on the chart, providing a visual representation of support and resistance levels based on market volatility.

Scientific Support for Volatility-Based Strategies:

The use of volatility-based indicators like the Keltner Channel is supported by numerous studies on price momentum and volatility trading. Research has shown that breakout strategies, particularly those leveraging volatility bands such as the Keltner Channel or Bollinger Bands, can be effective in capturing trends and reversals in both trending and mean-reverting markets  .

Who is Kevin Davey?

Kevin Davey is a highly respected algorithmic trader, author, and educator, known for his systematic approach to building and optimizing trading strategies. With over 25 years of experience in the markets, Davey has earned a reputation as an expert in quantitative and rule-based trading. He is particularly well-known for winning several World Cup Trading Championships, where he consistently demonstrated high returns with low risk.

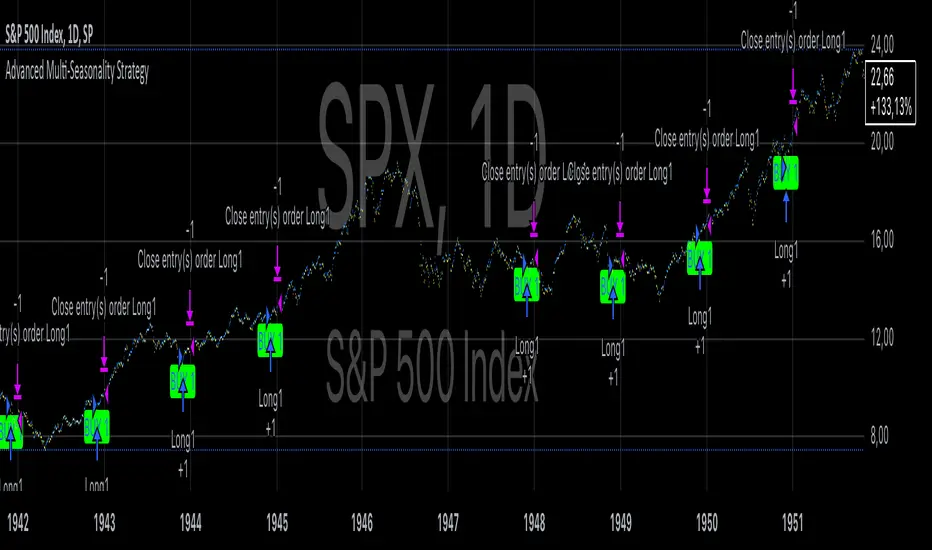

Advanced Multi-Seasonality StrategyThe Multi-Seasonality Strategy is a trading system based on seasonal market patterns. Seasonality refers to recurring market trends driven by predictable calendar-based events. These patterns emerge due to economic cycles, corporate activities (e.g., earnings reports), and investor behavior around specific times of the year. Studies have shown that such effects can influence asset prices over defined periods, leading to opportunities for traders who exploit these patterns (Hirshleifer, 2001; Bouman & Jacobsen, 2002).

How the Strategy Works:

The strategy allows the user to define four distinct periods within a calendar year. For each period, the trader selects:

Entry Date (Month and Day): The date to enter the trade.

Holding Period: The number of trading days to remain in the trade after the entry.

Trade Direction: Whether to take a long or short position during that period.

The system is designed with flexibility, enabling the user to activate or deactivate each of the four periods. The idea is to take advantage of seasonal patterns, such as buying during historically strong periods and selling during weaker ones. A well-known example is the "Sell in May and Go Away" phenomenon, which suggests that stock returns are higher from November to April and weaker from May to October (Bouman & Jacobsen, 2002).

Seasonality in Financial Markets:

Seasonal effects have been documented across different asset classes and markets:

Equities: Stock markets tend to exhibit higher returns during certain months, such as the "January effect," where prices rise after year-end tax-loss selling (Haugen & Lakonishok, 1987).

Commodities: Agricultural commodities often follow seasonal planting and harvesting cycles, which impact supply and demand patterns (Fama & French, 1987).

Forex: Currency pairs may show strength or weakness during specific quarters based on macroeconomic factors, such as fiscal year-end flows or central bank policy decisions.

Scientific Basis:

Research shows that market anomalies like seasonality are linked to behavioral biases and institutional practices. For example, investors may respond to tax incentives at the end of the year, and companies may engage in window dressing (Haugen & Lakonishok, 1987). Additionally, macroeconomic factors, such as monetary policy shifts and holiday trading volumes, can also contribute to predictable seasonal trends (Bouman & Jacobsen, 2002).

Risks of Seasonal Trading:

While the strategy seeks to exploit predictable patterns, there are inherent risks:

Market Changes: Seasonal effects observed in the past may weaken or disappear as market conditions evolve. Increased algorithmic trading, globalization, and policy changes can reduce the reliability of historical patterns (Lo, 2004).

Overfitting: One of the risks in seasonal trading is overfitting the strategy to historical data. A pattern that worked in the past may not necessarily work in the future, especially if it was based on random chance or external factors that no longer apply (Sullivan, Timmermann, & White, 1999).

Liquidity and Volatility: Trading during specific periods may expose the trader to low liquidity, especially around holidays or earnings seasons, leading to slippage and larger-than-expected price swings.

Economic and Geopolitical Shocks: External events such as pandemics, wars, or political instability can disrupt seasonal patterns, leading to unexpected market behavior.

Conclusion:

The Multi-Seasonality Strategy capitalizes on the predictable nature of certain calendar-based patterns in financial markets. By entering and exiting trades based on well-established seasonal effects, traders can potentially capture short-term profits. However, caution is necessary, as market dynamics can change, and seasonal patterns are not guaranteed to persist. Rigorous backtesting, combined with risk management practices, is essential to successfully implementing this strategy.

References:

Bouman, S., & Jacobsen, B. (2002). The Halloween Indicator, "Sell in May and Go Away": Another Puzzle. American Economic Review, 92(5), 1618-1635.

Fama, E. F., & French, K. R. (1987). Commodity Futures Prices: Some Evidence on Forecast Power, Premiums, and the Theory of Storage. Journal of Business, 60(1), 55-73.

Haugen, R. A., & Lakonishok, J. (1987). The Incredible January Effect: The Stock Market's Unsolved Mystery. Dow Jones-Irwin.

Hirshleifer, D. (2001). Investor Psychology and Asset Pricing. Journal of Finance, 56(4), 1533-1597.

Lo, A. W. (2004). The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective. Journal of Portfolio Management, 30(5), 15-29.

Sullivan, R., Timmermann, A., & White, H. (1999). Data-Snooping, Technical Trading Rule Performance, and the Bootstrap. Journal of Finance, 54(5), 1647-1691.

This strategy harnesses the power of seasonality but requires careful consideration of the risks and potential changes in market behavior over time.

Statistical ArbitrageThe Statistical Arbitrage Strategy, also known as pairs trading, is a quantitative trading method that capitalizes on price discrepancies between two correlated assets. The strategy assumes that over time, the prices of these two assets will revert to their historical relationship. The core idea is to take advantage of mean reversion, a principle suggesting that asset prices will revert to their long-term average after deviating significantly.

Strategy Mechanics:

1. Selection of Correlated Assets:

• The strategy focuses on two historically correlated assets (e.g., equity index futures like Dow Jones Mini and S&P 500 Mini). These assets tend to move in the same direction due to similar underlying fundamentals, such as overall market conditions. By tracking their relative prices, the strategy seeks to exploit temporary mispricings.

2. Spread Calculation:

• The spread is the difference between the prices of the two assets. This spread represents the relationship between the assets and serves as the basis for determining when to enter or exit trades.

3. Mean and Standard Deviation:

• The historical average (mean) of the spread is calculated using a Simple Moving Average (SMA) over a chosen period. The strategy also computes the standard deviation (volatility) of the spread, which measures how far the spread has deviated from the mean over time. This allows the strategy to define statistically significant price deviations.

4. Entry Signal (Mean Reversion):

• A buy signal is triggered when the spread falls below the mean by a multiple (e.g., two) of the standard deviation. This indicates that one asset is temporarily undervalued relative to the other, and the strategy expects the spread to revert to its mean, generating profits as the prices converge.

5. Exit Signal:

• The strategy exits the trade when the spread reverts to the mean. At this point, the mispricing has been corrected, and the profit from the mean reversion is realized.

Academic Support:

Statistical arbitrage has been widely studied in finance and economics. Gatev, Goetzmann, and Rouwenhorst’s (2006) landmark study on pairs trading demonstrated that this strategy could generate excess returns in equity markets. Their research found that by focusing on historically correlated stocks, traders could identify pricing anomalies and profit from their eventual correction.

Additionally, Avellaneda and Lee (2010) explored statistical arbitrage in different asset classes and found that exploiting deviations in price relationships can offer a robust, market-neutral trading strategy. In these studies, the strategy’s success hinges on the stability of the relationship between the assets and the timely execution of trades when deviations occur.

Risks of Statistical Arbitrage:

1. Correlation Breakdown:

• One of the primary risks is the breakdown of correlation between the two assets. Statistical arbitrage assumes that the historical relationship between the assets will hold in the future. However, market conditions, company fundamentals, or external shocks (e.g., macroeconomic changes) can cause these assets to deviate permanently, leading to potential losses.

• For instance, if two equity indices historically move together but experience divergent economic conditions or policy changes, their prices may no longer revert to the expected mean.

2. Execution Risk:

• This strategy relies on efficient execution and tight spreads. In volatile or illiquid markets, the actual price at which trades are executed may differ significantly from expected prices, leading to slippage and reduced profits.

3. Market Risk:

• Although statistical arbitrage is designed to be market-neutral (i.e., not dependent on the overall market direction), it is not entirely risk-free. Systematic market shocks, such as financial crises or sudden shifts in market sentiment, can affect both assets simultaneously, causing the spread to widen rather than revert to the mean.

4. Model Risk:

• The assumptions underlying the strategy, particularly regarding mean reversion, may not always hold true. The model assumes that asset prices will return to their historical averages within a certain timeframe, but the timing and magnitude of mean reversion can be uncertain. Misestimating this timeframe can lead to extended drawdowns or unrealized losses.

5. Overfitting:

• Over-reliance on historical data to fine-tune the strategy parameters (e.g., the lookback period or standard deviation thresholds) may result in overfitting. This means that the strategy works well on past data but fails to perform in live markets due to changing conditions.

Conclusion:

The Statistical Arbitrage Strategy offers a systematic and quantitative approach to trading that capitalizes on temporary price inefficiencies between correlated assets. It has been proven to generate returns in academic studies and is widely used by hedge funds and institutional traders for its market-neutral characteristics. However, traders must be aware of the inherent risks, including correlation breakdown, execution risks, and the potential for prolonged deviations from the mean. Effective risk management, diversification, and constant monitoring are essential for successfully implementing this strategy in live markets.

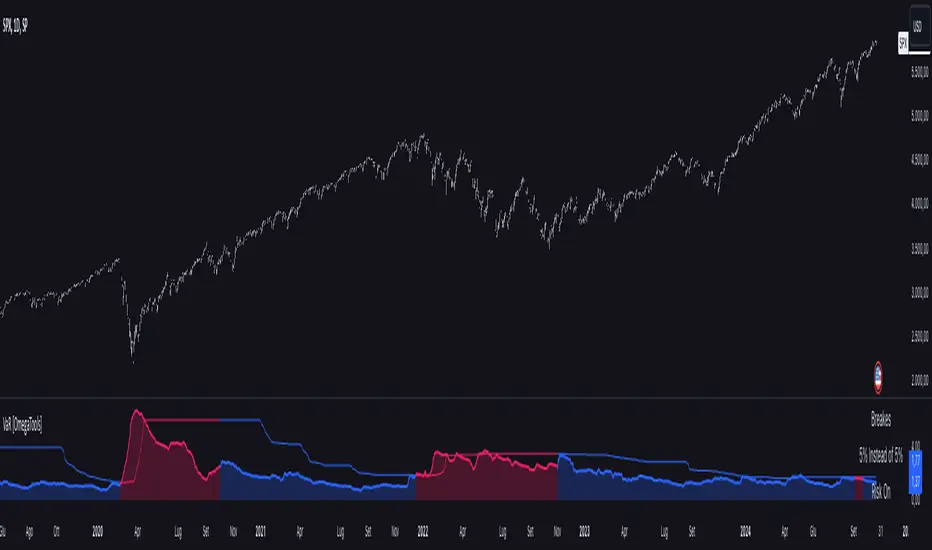

Value at Risk [OmegaTools]The "Value at Risk" (VaR) indicator is a powerful financial risk management tool that helps traders estimate the potential losses in a portfolio over a specified period of time, given a certain level of confidence. VaR is widely used by financial institutions, traders, and risk managers to assess the probability of portfolio losses in both normal and volatile market conditions. This TradingView script implements a comprehensive VaR calculation using several models, allowing users to visualize different risk scenarios and adjust their trading strategies accordingly.

Concept of Value at Risk

Value at Risk (VaR) is a statistical technique used to measure the likelihood of losses in a portfolio or financial asset due to market risks. In essence, it answers the question: "What is the maximum potential loss that could occur in a given portfolio over a specific time horizon, with a certain confidence level?" For instance, if a portfolio has a one-day 95% VaR of $10,000, it means that there is a 95% chance the portfolio will not lose more than $10,000 in a single day. Conversely, there is a 5% chance of losing more than $10,000. VaR is a key risk management tool for portfolio managers and traders because it quantifies potential losses in monetary terms, allowing for better-informed decision-making.

There are several ways to calculate VaR, and this indicator script incorporates three of the most commonly used models:

Historical VaR: This approach uses historical returns to estimate potential losses. It is based purely on past price data, assuming that the past distribution of returns is indicative of future risks.

Variance-Covariance VaR: This model assumes that asset returns follow a normal distribution and that the risk can be summarized using the mean and standard deviation of past returns. It is a parametric method that is widely used in financial risk management.

Exponentially Weighted Moving Average (EWMA) VaR: In this model, recent data points are given more weight than older data. This dynamic approach allows the VaR estimation to react more quickly to changes in market volatility, which is particularly useful during periods of market stress. This model uses the Exponential Weighted Moving Average Volatility Model.

How the Script Works

The script starts by offering users a set of customizable input settings. The first input allows the user to choose between two main calculation modes: "All" or "OCT" (Only Current Timeframe). In the "All" mode, the script calculates VaR using all available methodologies—Historical, Variance-Covariance, and EWMA—providing a comprehensive risk overview. The "OCT" mode narrows the calculation to the current timeframe, which can be particularly useful for intraday traders who need a more focused view of risk.

The next input is the lookback window, which defines the number of historical periods used to calculate VaR. Commonly used lookback periods include 21 days (approximately one month), 63 days (about three months), and 252 days (roughly one year), with the script supporting up to 504 days for more extended historical analysis. A longer lookback period provides a more comprehensive picture of risk but may be less responsive to recent market conditions.

The confidence level is another important setting in the script. This represents the probability that the loss will not exceed the VaR estimate. Standard confidence levels are 90%, 95%, and 99%. A higher confidence level results in a more conservative risk estimate, meaning that the calculated VaR will reflect a more extreme loss scenario.