Composite Risk IndicatorThe Composite Risk Indicator is a financial tool designed to assess market risk by analyzing the spreads between various asset classes. This indicator synthesizes information across six key spreads, normalizing each on a scale from 0 to 100 where higher values represent higher perceived risk. It provides a single, comprehensive measure of market sentiment and risk exposure.

Key Components of the CRI:

1. Stock Market to Bond Market Spread (SPY/BND): Measures the performance of stocks relative to bonds. Higher values indicate stronger stock performance compared to bonds, suggesting increased market optimism and higher risk.

2. Junk Bond to Treasury Bond Spread (HYG/GOVT): Assesses the performance of high-yield (riskier) bonds relative to government (safer) bonds. A higher ratio indicates increased appetite for risk.

3. Junk Bond to Investment Grade Bond Spread (HYG/LQD): Compares high-yield bonds to investment-grade corporate bonds. This ratio sheds light on the risk tolerance within the corporate bond market.

4. Growth to Value Spread (VUG/VTV): Evaluates the performance of growth stocks against value stocks. A higher value suggests a preference for growth stocks, often seen in risk-on environments.

5. Tech to Staples Spread (XLK/XLP): Measures the performance of technology stocks relative to consumer staples. This ratio highlights the market’s risk preference within equity sectors.

6. Small Cap Growth to Small Cap Value Spread (SLYG/SLYV): Compares small-cap growth stocks to small-cap value stocks, providing insight into risk levels in smaller companies.

Utility:

This indicator is particularly useful for investors and traders looking to gauge market sentiment, identify shifts in risk appetite, and make informed decisions based on a broad assessment of market conditions. The CRI can serve as a valuable addition to investment analysis and risk management strategies.

Statistics

MetaFOX DCA (ASAP-RSI-BB%B-TV)Welcome To ' MetaFOX DCA (ASAP-RSI-BB%B-TV) ' Indicator.

This is not a Buy/Sell signals indicator, this is an indicator to help you create your own strategy using a variety of technical analyzing options within the indicator settings with the ability to do DCA (Dollar Cost Average) with up to 100 safety orders.

It is important when backtesting to get a real results, but this is impossible, especially when the time frame is large, because we don't know the real price action inside each candle, as we don't know whether the price reached the high or low first. but what I can say is that I present to you a backtest results in the worst possible case, meaning that if the same chart is repeated during the next period and you traded for the same period and with the same settings, the real results will be either identical to the results in the indicator or better (not worst). There will be no other factors except the slippage in the price when executing orders in the real trading, So I created a feature for that to increase the accuracy rate of the results. For more information, read this description.

Below I will explain all the properties and settings of the indicator:

A) 'Buy Strategies' Section: Your choices of strategies to Start a new trade: (All the conditions works as (And) not (OR), You have to choose one at least and you can choose more than one).

- 'ASAP (New Candle)': Start a trade as soon as possible at the opening of a new candle after exiting the previous trade.

- 'RSI': Using RSI as a technical analysis condition to start a trade.

- 'BB %B': Using BB %B as a technical analysis condition to start a trade.

- 'TV': Using tradingview crypto screener as a technical analysis condition to start a trade.

B) 'Exit Strategies' Section: Your choices of strategies to Exit the trades: (All the conditions works as (And) not (OR), You can choose more than one, But if you don't want to use any of them you have to activate the 'Use TP:' at least).

- 'ASAP (New Candle)': Exit a trade as soon as possible at the opening of a new candle after opening the previous trade.

- 'RSI': Using RSI as a technical analysis condition to exit a trade.

- 'BB %B': Using BB %B as a technical analysis condition to exit a trade.

- 'TV': Using tradingview crypto screener as a technical analysis condition to exit a trade.

C) 'Main Settings' Section:

- 'Trading Fees %': The Exchange trading fees in percentage (trading Commission).

- 'Entry Price Slippage %': Since real trading differs from backtest calculations, while in backtest results are calculated based on the open price of the candle, but in real trading there is a slippage from the open price of the candle resulting from the supply and demand in the real time trading, so this feature is to determine the slippage Which you think it is appropriate, then the entry prices of the trades will calculated higher than the open price of the start candle by the percentage of slippage that you set. If you don't want to calculate any slippage, just set it to zero, but I don't recommend that if you want the most realistic results.

Note: If (open price + slippage) is higher than the high of the candle then don't worry, I've kept this in consideration.

- 'Use SL': Activate to use stop loss percentage.

- 'SL %': Stop loss percentage.

- 'SL settings options box':

'SL From Base Price': Calculate the SL from the base order price (from the trade first entry price).

'SL From Avg. Price': Calculate the SL from the average price in case you use safety orders.

'SL From Last SO.': Calculate the SL from the last (lowest) safety order deviation.

ex: If you choose 'SL From Avg. Price' and SL% is 5, then the SL will be lower than the average price by 5% (in this case your SL will be dynamic until the price reaches all the safety orders unlike the other two SL options).

Note: This indicator programmed to be compatible with '3COMMAS' platform, but I added more options that came to my mind.

'3COMMAS' DCA bots uses 'SL From Base Price'.

- 'Use TP': Activate to use take profit percentage.

- 'TP %': Take profit percentage.

- 'Pure TP,SL': This feature was created due to the differences in the method of calculations between API tools trading platforms:

If the feature is not activated and (for example) the TP is 5%, this means that the price must move upward by only 5%, but you will not achieve a net profit of 5% due to the trading fees. but If the feature is activated, this means that you will get a net profit of 5%, and this means that the price must move upward by (5% for the TP + the equivalent of trading fees). The same idea is applied to the SL.

Note: '3COMMAS' DCA bots uses activated 'Pure TP,SL'.

- 'SO. Price Deviation %': Determines the decline percentage for the first safety order from the trade start entry price.

- 'SO. Step Scale': Determines the deviation multiplier for the safety orders.

Note: I'm using the same method of calculations for SO. (safety orders) levels that '3COMMAS' platform is using. If there is any difference between the '3COMMAS' calculations and the platform that you are using, please let me know.

'3COMMAS' DCA bots minimum 'SO. Price Deviation %' is (0.21)

'3COMMAS' DCA bots minimum 'SO. Step Scale' is (0.1)

- 'SO. Volume Scale': Determines the base order size multiplier for the safety orders sizes.

ex: If you used 10$ to buy at the trade start (base order size) and your 'SO. Volume Scale' is 2, then the 1st SO. size will be 20, the 2nd SO. size will be 40 and so on.

- 'SO. Count': Determines the number of safety orders that you want. If you want to trade without safety orders set it to zero.

'3COMMAS' DCA bots minimum 'SO. Volume Scale' is (0.1)

- 'Exchange Min. Size': The exchange minimum size per trade, It's important to prevent you from setting the base order Size less than the exchange limit. It's also important for the backtest results calculations.

ex: If you setup your strategy settings and it led to a loss to the point that you can't trade any more due to insufficient funds and your base order size share from the strategy becomes less than the exchange minimum trade size, then the indicator will show you a warning and will show you the point where you stopped the trading (It works in compatible with the initial capital). I recommend to set it a little bit higher than the real exchange minimum trade size especially if you trade without safety orders to not stuck in the trade if you hit the stop loss

- 'BO. Size': The base order size (funds you use at the trade entry).

- 'Initial Capital': The total funds allocated for trading using your strategy settings, It can be more than what is required in the strategy to cover the deficit in case of a loss, but it should not exceed the funds that you actually have for trading using this strategy settings, It's important to prevent you from setting up a strategy which requires funds more than what you have. It's also has other important benefits (refer to 'Exchange Min. Size' for more information).

- 'Accumulative Results': This feature is also called re-invest profits & risk reduction. If it's not activated then you will use the same funds size in each new trade whether you are in profit or loss till the (initial capitals + net results) turns insufficient. If it's activated then you will reuse your profits and losses in each new trade.

ex: The feature is active and your first trade ended with a net profit of 1000$, the next trade will add the 1000$ to the trade funds size and it will be distributed as a percentage to the BO. & SO.s according to your strategy settings. The same idea in case of a loss, the trade funds size will be reduced.

D) 'RSI Strategy' Section:

- 'Buy': RSI technical condition to start a trade. Has no effect if you don't choose 'RSI' option in 'Buy Strategies'.

- 'Exit': RSI technical condition to exit a trade. Has no effect if you don't choose 'RSI' option in 'Exit Strategies'.

E) 'TV Strategy' Section:

- 'Buy': TradingView Crypto Screener technical condition to start a trade. Has no effect if you don't choose 'TV' option in 'Buy Strategies'.

- 'Exit': TradingView Crypto Screener technical condition to exit a trade. Has no effect if you don't choose 'TV' option in 'Exit Strategies'.

F) 'BB %B Strategy' Section:

- 'Buy': BB %B technical condition to start a trade. Has no effect if you don't choose 'BB %B' option in 'Buy Strategies'.

- 'Exit': BB %B technical condition to exit a trade. Has no effect if you don't choose 'BB %B' option in 'Exit Strategies'.

G) 'Plot' Section:

- 'Signals': Plots buy and exit signals.

- 'BO': Plots the trade entry price (base order price).

- 'AVG': Plots the trade average price.

- 'AVG options box': Your choice to plot the trade average price type:

'Avg. With Fees': The trade average price including the trading fees, If you exit the trade at this price the trade net profit will be 0.00

'Avg. Without Fees': The trade average price but not including the trading fees, If you exit the trade at this price the trade net profit will be a loss equivalent to the trading fees.

- 'TP': Plots the trade take profit price.

- 'SL': Plots the trade stop loss price.

- 'Last SO': Plots the trade last safety order that the price reached.

- 'Exit Price': Plots a mark on the trade exit price, It plots in 3 colors as below:

Red (Default): Trade exit at a loss.

Green (Default): Trade exit at a profit.

Yellow (Default): Trade exit at a profit but this is a special case where we have to calculate the profits before reaching the safety orders (if any) on that candle (compatible with the idea of getting strategy results at the worst case).

- 'Result Table': Plots your strategy result table. The net profit percentage shown is a percentage of the 'initial capital'.

- 'TA Values': Plots your used strategies Technical analysis values. (Green cells means valid condition).

- 'Help Table': Plots a table to help you discover 100 safety orders with its deviations and the total funds needed for your strategy settings. Deviations shown in red is impossible to use because its price is <= 0.00

- 'Portfolio Chart': Plots your Portfolio status during the entire trading period in addition to the highest and lowest level reached. It's important when evaluating any strategy not only to look at the final result, but also to look at the change in results over the entire trading period. Perhaps the results were worryingly negative at some point before they rose again and made a profit. This feature helps you to see the whole picture.

- 'Welcome Message': Plots a welcome message and showing you the idea behind this indicator.

- 'Green Net Profit %': It plots the 'Net Profit %' in the result table in green color if the result is equal to or above the value that you entered.

- 'Green Win Rate %': It plots the 'Win Rate %' in the result table in green color if the result is equal to or above the value that you entered.

- 'User Notes Area': An empty text area, Feel free to use this area to write your notes so you don't forget them.

The indicator will take care of you. In some cases, warning messages will appear for you. Read them carefully, as they mean that you have done an illogical error in the indicator settings. Also, the indicator will sometimes stop working for the same reason mentioned above. If that happens then click on the red (!) next to the indicator name and read the message to find out what illogical error you have done.

Please enjoy the indicator and let me know your thoughts in the comments below.

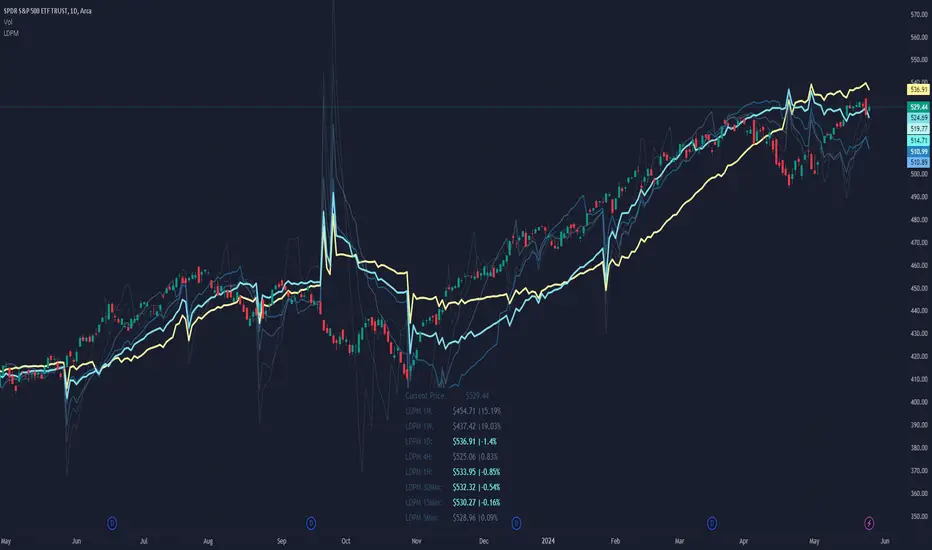

Liquidity Dependent Price Stability AlgorithmThe Liquidity Dependent Price Stability (LDPS) indicator is designed to measure liquidity levels on an equity and, from those measurements, provide Bullish or Bearish outlooks for future price action. These outlooks are given via reporting the equity's Liquidity Condition and Liquidity Flow.

Interpretation

Liquidity Condition (LC) and Liquidity Flow (LF) measurements are displayed with color-specific chart colors and/or with text output.

LC can be reported as "Weak Bullish", "Bullish", or "Strong Bullish" for Bullish outlooks and "Weak Bearish", "Bearish" or "Strong Bearish" for Bearish outlooks. LC can also just be reported as "Bullish" or "Bearish".

Bullish LCs have a statistical correlation with future price appreciation, and Bearish LCs have a statistical correlation with price depreciation. When LC is “Bullish”, the price is likely to go up, and if LC is “Bearish”, the price is likely to go down.

Liquidity Flow (LF) is a measure of how LC is changing. When LC is becoming more bullish, LF is reported as “Improving”. When LC is becoming more bearish, LF is reported as “Worsening”. LF is only displayed via text output.

Settings and Configurations

LDPS Sensitivity and Reactivity: Determines if you want LDPS to be more sensitive to changing conditions or less sensitive. This choice affects how certain LDPS is when forming its future outlooks. LDPS achieves this increase in sensitivity and reactivity by lowering the bar for what LDPS considers a significant change.

Aggressive : LDPS will optimize reporting early changes in LC and LF at the expensive of accuracy. Aggressive is good for low-risk trading styles that prefer to exit a position early rather than deal with increased risk of oppositional movement.

Balanced : LDPS will try to balance reporting changes in LC and LF with maintaining accuracy. Balanced style is a good setting to start out with and is applicable across the widest range of equity’s and timeframes.

Conservative : LDPS will optimize accuracy over being sensitive to changes in LC or LF. Conservative is a good choice for lower timeframes and traders who only want to change or exit positions with the greatest confidence.

LDPS Reporting Style: Determines how you want LC to be reported.

Simplified : LDPS will only report LC as “Bullish” or “Bearish”.

Full : LDPS will increase its reporting details and include the “Strong” and “Weak” pre-fixes, when appropriate.

LDPS Candle Coloring: There are three different ways that LC can be reported on the chart via coloring.

LDPS Candle Replacement: This will replace the chart’s default candles with those created by LDPS. Note: In order to see LDPS’ candles and not the chart’s, you have to disable to chart’s candles. This can be done in Settings -> Symbol and unchecking “Body”, “Borders” and “Wick” boxes.

LDPS Candle Coloring: This will just color the bodies of the chart’s default candles. Note: This setting should not have the chart’s candle’s disabled.

LDPS Background Coloring: This will color the chart’s background rather than any candles.

LDPS Text Output: LC and LF are reported via a text box that can be moved several places on the chart, or the text box can be removed.

LDPS Measurements – Display: When selected, LC and LF will be reported via the text box.

LDPS Measurement – Text Location: Determines where the text box with LC and LF are located.

LDPS Measurement – Text Size: Determines the size of LC and LF within the text box.

LDPS Measurement – Background Color: Determines the background color of the text box with LC and LF.

LDPS Condition Color Selection – Bullish / Bearish: Color selection for each type of LC. Note: If the Simplified reporting style is selected, the “Full Bullish” and “Full Bearish” are the bullish and bearish color choices, respectively.

Frequently Asked Questions:

Where can I get additional Information?

Please check the “Author’s Instructions” section below.

Where can I find the results of the LDPS research?

Please check the “Author’s Instructions” section below.

Help! Something’s not working!

Apologies. Please see the email listed in “Author’s Instructions” below and let’s get started on solving the issue.

Which Sensitivity setting should I use?

The author’s preference is Conservative in most cases, but the answer for you depends on your preferred style.

An analogy might help: the aggressive setting will ensure LDPS is early to the party – every party. Of the parties that really kick off, you can be certain LDPS is there, but they had to visit a several of parties before finding the right one.

The Conservative setting won’t bring LDPS to every party – it will gladly stay at the one it’s at but when it detects the next real big hit, LDPS will move to that party instead. It won’t be the first one there, but it is definitely earlier than most.

Should I use the Full or Simplified reporting style?

Depending on how engaged you are with the particular equity or position, either choice can be beneficial. The Full reporting style will let you detect changes in LC before they might show with the Simplified reporting style. Some enjoy the additional data, some (like the Author) enjoy keeping things simple.

I can see LDPS’ colors in the chart’s candlesticks when the settings are open, but not when the settings are closed. How come?

If you are using the “LDPS Candle Replacement” setting, be sure to turn off the Chart’s default candles by right-clicking on the chart, going to Settings, then Symbol and then un-checking “Body”, “Border” and “Wick”. This should fix the issue.

I think there’s a bug – where do I report it?

Thank you for reaching out about a potential bug or issue! Please see the email below in “Author’s Instructions” to report the issue.

LDPM Crossover Scanner AddonThe LDPM Crossover Scanner is designed to be used in conjunction with the Liquidity Dependent Price Movement Algorithm and is included with LDPM access.

The LDPM Crossover Scanner displays the LDPM status for up to 10 equity's. When conditions are bearish, per LDPM, the equity will light up on the scanner; otherwise, the equity will not light up.

When used in aggregate, this becomes a particularly useful way to measure up-coming market moves (especially when the crossover scanner showcases equities with significant beta to the chart's underlying!).

Liquidity Dependent Price Movement AlgorithmLiquidity-Dependent Price Movement (LDPM) is a metric designed to directly measure liquidity on a equity in real time, and to translate those measurements into signals to provide insights into where the anticipate price-direction is headed.

Liquidity can be characterized as a way of measuring how smoothly things are running in the market. When things are running smoothly – such as when there is good agreement as to the price of an asset, then things are considered liquid. Conversely, when things are not running smoothly, just as when the bid or the ask do not agree with each other, then things are considered not liquid. These different states have different outcome liklihoods.

In a liquid environment, a stock can trade a lot of shares without moving the price. On the other hand, when a stock is not liquid, even small volumes can move the price substantially.

It is therefore helpful to know when a stock is liquid to the upside or to the downside, or even, when a stock is not liquid to the upside or the downside. These data have statistical associations with future price movement and volatility.

The use of LDPM is straightforward:

If the price is above LDPM: bullish outlooks.

If the price is below LDPM: bearish outlooks.

There are a few key differences about LDPM as compared to other indicators, namely that timeframe matters . That means, LDPM will tailor its output to the timeframe selected. The advantage of this is that it allows LDPM to be "tailored" to the specific timeframe as desired, without having to do any conversions or adaptations mentally.

Key Settings and Configurations:

Setting - Smoothing Type of LDPM :

Default: KF.

LDPM can be smoothened if desired. There are 5 different types of smoothing available:

EMA : Exponential Smoothing

SMA : Simple Smoothing

WMA : Weighted Smoothing

RMA : Modified Smoothing

KF : Kellman Smoothing

The default is "KF" for Kellman Smoothing.

Setting - Include LDPM-Granular :

Default: Off.

LDPM-Granular is the more "raw" form of LDPM that displays the candle-specific result, rather than the smoothened result. This can be toggled on or off, if desired. LDPM granular is helpful for looking at candle-specific

Setting - Place LDPM Standard :

Default: Off.

An additional, single, LDPM line can be placed via this toggle. Settings for this LDPM can be configured directly below toggle.

Setting - Place LDPM-Fib :

Default: On.

LDPM-Fib is a default setting for displaying 5 LDPMs (LDPM-13, LDPM-21, LDPM-34, LDPM-55, and LDPM-89) whose lookbacks are spaced via the Fib sequence. Useful for those who enjoy a static relationship between the different "layers" of LDPM.

Setting - Place LDPM-Reference :

Default: Off.

Since LDPM is time-interval dependent, there may be times when a higher-order timeframe is desired to act as a reference. For instance, suppose you want to go long if the 1-Hour LDPM experiences a bullish crossover, but you want to scalp shorts on the 15-minute timeframe until then. Then you could place the chart on the 15-minute interval for your scalping, and then place a 1-Hour reference LDPM that will show you when the 1-Hour LDPM and price experience a crossover.

Note: The reference must be a higher-order timeframe. So if your chart is on the 15-minute, you can only reference timeframes greater than 15.

Setting - LDPM Box Creation :

Default: On.

Instead of implementing a reference LDPM, it is possible to display the other timeframes in a data table with conditional coloring for if the overall LDPM-Price relationship is bullish or bearish.

Why Chose LDPM

There are no other Liquidity-measuring indicators available to the retail investor. Measuring liquidity often requires the use of expensive data and high-throughput computing to be used in real-time. Neither of these requirements apply to utilizing LDPM.

Additionally, the data are supportive that LDPM provides statistically significant, price-direction-correct outlooks.

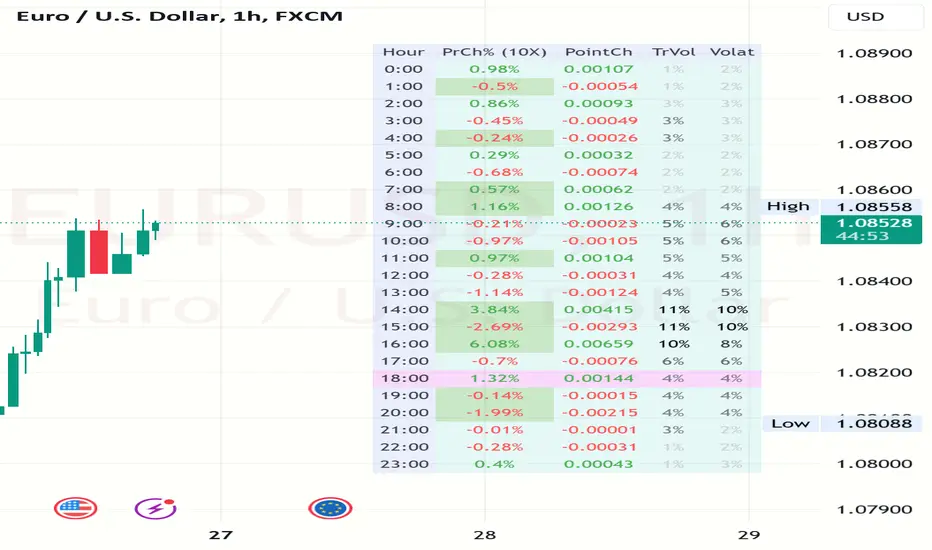

Volatility and Volume by Hour EXT(Extended republication, use this instead of the old one)

The goal of this indicator is to show a “characteristic” of the instrument, regarding the price change and trading volume. You can see how the instrument “behaved” throughout the day in the lookback period. I've found this useful for timing in day trading.

The indicator creates a table on the chart to display various statistics for each hour of the day.

Important: ONLY SHOWS THE TABLE IF THE CHART’S TIMEFRAME IS 1H!

Explanation of the columns:

1. Volatility Percentage (Volat): This column shows the volatility of the price as a percentage. For example, a value of "15%" means the price movement was 15% of the total daily price movement within the hour.

2. Hourly Point Change (PointCh): This column shows the change in price points for each hour in the lookback period. For example, a value of "5" means the price has increased by 5 points in the hour, while "-3" means it has decreased by 3 points.

3. Hourly Point Change Percentage (PrCh% (LeverageX)): This column shows the percentage change in price points for each hour, adjusted with leverage multiplier. Displayed green (+) or red (-) accordingly. For example, a value of "10%" with a leverage of 2X means the price has effectively changed by 5% due to the leverage.

4. Trading Volume Percentage (TrVol): This column shows the percentage of the daily total volume that was traded in a specific hour. For example, a value of "10%" would mean that 10% of the day's total trading volume occurred in that hour.

5. Added New! - Relevancy Check: The indicator checks the last 24 candle. If the direction of the price movement was the same in the last 24 hour as the statistical direction in that hour, the background of the relevant hour in the second column goes green.

For example: if today at 9 o'clock the price went lower, so as at 9 o'clock in the loopback period, the instrument "behaves" according to statistics . So the statistics is probably more relevant for today. The more green background row the more relevancy.

Settings:

1. Lookback period: The lookback period is the number of previous bars from which data is taken to perform calculations. In this script, it's used in a loop that iterates over a certain number of past bars to calculate the statistics. TIP: Select a period the contains a trend in one direction, because an upward and a downward trend compensate the price movement in opposite directions.

2. Timezone: This is a string input that represents the user's timezone. The default value is "UTC+2". Adjust it to your timezone in order to view the hours properly.

3. Leverage: The default value is 10(!). This input is used to adjust the hourly point change percentage. For FOREX traders (for example) the statistics can show the leveraged percentage of price change. Set that according the leverage you trade the instrument with.

Use at your own risk, provided “as is” basis!

Hope you find it useful! Cheers!

trend_switch

█ Description

Asset price data was time series data, commonly consisting of trends, seasonality, and noise. Many applicable indicators help traders to determine between trend or momentum to make a better trading decision based on their preferences. In some cases, there is little to no clear market direction, and price range. It feels much more appropriate to use a shorter trend identifier, until clearly defined market trend. The indicator/strategy developed with the notion aims to automatically switch between shorter and longer trend following indicator. There were many methods that can be applied and switched between, however in this indicator/strategy will be limited to the use of predictive moving average and MESA adaptive moving average (Ehlers), by first determining if there is a strong trend identified by calculating the slope, if slope value is between upper and lower threshold assumed there is not much price direction.

█ Formula

// predictive moving average

predict = (2*wma1-wma2)

trigger = (4*predict+3*predict +2*predict *predict)

// MESA adaptive moving average

mama = alpha*src+(1-alpha)*mama

fama = .5*alpha*mama+(1-.5-alpha)*fama

█ Feature

The indicator will have a specified default parameter of:

source = ohlc4

lookback period = 10

threshold = 10

fast limit = 0.5

slow limit = 0.05

Strategy type can be switched between Long/Short only and Long-Short strategy

Strategy backtest period

█ How it works

If slope between the upper (red) and lower (green) threshold line, assume there is little to no clear market direction, thus signal predictive moving average indicator

If slope is above the upper (red) or below the lower (green) threshold line, assume there is a clear trend forming, the signal generated from the MESA adaptive moving average indicator

█ Example 1 - Slope fall between the Threshold - activate shorter trend

█ Example 2 - Slope fall above/below Threshold - activate longer trend

Normalized Z-ScoreThe Normalized Z-Score indicator is designed to help traders identify overbought or oversold conditions in a security's price. This indicator can provide valuable signals for potential buy or sell opportunities by analyzing price deviations from their average values.

How It Works :

-- Z-Score Calculation:

---- The indicator calculates the Z-Score for both high and low prices over a user-defined period (default is 14 periods).

---- The Z-Score measures how far a price deviates from its average in terms of standard deviations.

-- Average Z-Score:

---- The average Z-Score is derived by taking the mean of the high and low Z-Scores.

-- Normalization:

---- The average Z-Score is then normalized to a range between -1 and 1. This helps in standardizing the indicator's values, making it easier to interpret.

-- Signal Line:

---- A signal line, which is the simple moving average (SMA) of the normalized Z-Score, is calculated to smooth out the data and highlight trends.

-- Color-Coding:

---- The signal line changes color based on its value: green when it is positive (indicating a potential buy signal) and red when it is negative (indicating a potential sell signal). This coloration is also used for the candle/bar coloration.

How to Use It:

-- Adding the Indicator:

---- Add the Normalized Z-Score indicator to your TradingView chart. It will appear in a separate pane below the price chart.

-- Interpreting the Histogram:

---- The histogram represents the normalized Z-Score. High positive values suggest overbought conditions, while low negative values suggest oversold conditions.

-- Using the Signal Line:

---- The signal line helps to confirm the conditions indicated by the histogram. A green signal line suggests a potential buying opportunity, while a red signal line suggests a potential selling opportunity.

-- Adjusting the Period:

---- You can adjust the period for the Z-Score calculation to suit your trading strategy. The default period is 14, but you can change this based on your preference.

Example Scenario:

-- Overbought Condition: If the histogram shows a high positive value and the signal line is green, the security may be overbought. This could indicate that it is a good time to consider selling.

-- Oversold Condition: If the histogram shows a low negative value and the signal line is red, the security may be oversold. This could indicate that it is a good time to consider buying.

By using the Normalized Z-Score indicator, traders can gain insights into price deviations and potential market reversals, aiding in making more informed trading decisions.

TanHef Ranks ScreenerTanHef Ranks Screener: A Numeric Compass to Market Tops and Bottoms

█ Simple Explanation:

The TanHef Ranks Screener illustrates the ‘TanHef Ranks’ indicator, designed to signal 'buy low and sell high' opportunities through numerical rankings. Larger numbers represent stronger signals, with negative numbers indicating potential ‘buy’ opportunities and positive numbers suggesting possible ‘sell’ moments.

█ TanHef Ranks Indicator:

View the TanHef Ranks Indicator description prior to using the screener.

█ Ticker Input Method:

Add tickers to the screener using a text area list in a CSV-styled (comma-separated values) list and/or through individual ticker inputs. The text area supports various delimiters, including commas, spaces, semicolons, apostrophes, and new lines. To ensure the expected exchange is used, the exchange prefix should be included when using a text area list.

█ Pair Configuration:

Quickly set up specific trading pairs by comparing tickers to the chart’s symbol or a specified input. This feature is useful for identifying opportunities in obscure trading pairs.

█ Total Combined Average Rank:

Compute the average rank of all tickers to highlighting overall market opportunities. When combined with the 'Pair Configuration' settings, it allows for identifying specific opportunities where one ticker may present a better trading opportunity relative to others.

█ Screener Display Settings:

Customize color-coded rank thresholds, text details, toggle visibility of numerical rankings, and other display settings. Hover over tickers for tooltips with full ticker names and rankings, ideal for small fonts or screens.

█ Alerts:

Set up alerts for individual ticker ranks or total average ranks. To avoid inconsistent or excessive alerts within a short period of time due to TradingView's alert frequency limits, it is recommended to use alerts set to occur at bar close to guarantee alerts. For immediate alerts, consider configuring them directly within the ‘TanHef Ranks’ indicator for better reliability. For the most up-to-date suggestions, hover the tooltips within the indicator’s alert settings.

█ Additional Clarity:

All the settings and functionality are described in detail within the tooltips beside each setting in the indicator’s settings. Hover over each tooltip for comprehensive explanations and guidance on how to configure and use the screener effectively.

█ How To Access:

Follow the Author's Instructions below to get access.

Global Financial IndexIntroducing the "Global Financial Index" indicator on TradingView, a meticulously crafted tool derived from extensive research aimed at providing the most comprehensive assessment of a company's financial health, profitability, and valuation. Developed with the discerning trader and investor in mind, this indicator amalgamates a diverse array of financial metrics, meticulously weighted and balanced to yield optimal results.

Financial Strength:

Financial strength is a cornerstone of a company's stability and resilience in the face of economic challenges. It encompasses various metrics that gauge the company's ability to meet its financial obligations, manage its debt, and generate sustainable profits. In our Global Financial Index indicator, the evaluation of financial strength is meticulously crafted to provide investors with a comprehensive understanding of a company's fiscal robustness. Let's delve into the key components and the rationale behind their inclusion:

1. Current Ratio:

The Current Ratio serves as a vital indicator of a company's liquidity position by comparing its current assets to its current liabilities.

A ratio greater than 1 indicates that the company possesses more short-term assets than liabilities, suggesting a healthy liquidity position and the ability to meet short-term obligations promptly.

By including the Current Ratio in our evaluation, we emphasize the importance of liquidity management in sustaining business operations and weathering financial storms.

2. Debt to Equity Ratio:

The Debt to Equity Ratio measures the proportion of a company's debt relative to its equity, reflecting its reliance on debt financing versus equity financing.

A higher ratio signifies higher financial risk due to increased debt burden, potentially leading to liquidity constraints and solvency issues.

Incorporating the Debt to Equity Ratio underscores the significance of balancing debt levels to maintain financial stability and mitigate risk exposure.

3. Interest Coverage Ratio:

The Interest Coverage Ratio assesses a company's ability to service its interest payments with its operating income.

A higher ratio indicates a healthier financial position, as it implies that the company generates sufficient earnings to cover its interest expenses comfortably.

By evaluating the Interest Coverage Ratio, we gauge the company's capacity to manage its debt obligations without compromising its profitability or sustainability.

4. Altman Z-Score:

The Altman Z-Score, developed by Edward Altman, is a composite metric that predicts the likelihood of a company facing financial distress or bankruptcy within a specific timeframe.

It considers multiple financial ratios, including liquidity, profitability, leverage, and solvency, to provide a comprehensive assessment of a company's financial health.

The Altman Z-Score categorizes companies into distinct risk groups, allowing investors to identify potential warning signs and make informed decisions regarding investment or credit exposure.

By integrating the Altman Z-Score, we offer a nuanced perspective on a company's financial viability and resilience in turbulent market conditions.

Profitability Rank:

Profitability rank is a crucial aspect of investment analysis that evaluates a company's ability to generate profits relative to its peers and industry benchmarks. It involves assessing various profitability metrics to gauge the efficiency and effectiveness of a company's operations and management. In our Global Financial Index indicator, the profitability rank segment is meticulously designed to provide investors with a comprehensive understanding of a company's profitability dynamics. Let's delve into the key components and rationale behind their inclusion:

1. Return on Equity (ROE):

Return on Equity measures a company's net income generated relative to its shareholders' equity.

A higher ROE indicates that a company is generating more profits with its shareholders' investment, reflecting efficient capital utilization and strong profitability.

By incorporating ROE, we assess management's ability to generate returns for shareholders and evaluate the overall profitability of the company's operations.

2. Gross Profit Margin:

Gross Profit Margin represents the percentage of revenue retained by a company after accounting for the cost of goods sold (COGS).

A higher gross profit margin indicates that a company is effectively managing its production costs and pricing strategies, leading to greater profitability.

By analyzing gross profit margin, we evaluate a company's pricing power, cost efficiency, and competitive positioning within its industry.

3. Operating Profit Margin:

Operating Profit Margin measures the percentage of revenue that remains after deducting operating expenses, such as salaries, rent, and utilities.

A higher operating profit margin signifies that a company is efficiently managing its operating costs and generating more profit from its core business activities.

By considering operating profit margin, we assess the underlying profitability of a company's operations and its ability to generate sustainable earnings.

4. Net Profit Margin:

Net Profit Margin measures the percentage of revenue that remains as net income after deducting all expenses, including taxes and interest.

A higher net profit margin indicates that a company is effectively managing its expenses and generating greater bottom-line profitability.

By analyzing net profit margin, we evaluate the overall profitability and financial health of a company, taking into account all expenses and income streams.

Valuation Rank:

Valuation rank is a fundamental aspect of investment analysis that assesses the attractiveness of a company's stock price relative to its intrinsic value. It involves evaluating various valuation metrics to determine whether a stock is undervalued, overvalued, or fairly valued compared to its peers and the broader market. In our Global Financial Index indicator, the valuation rank segment is meticulously designed to provide investors with a comprehensive perspective on a company's valuation dynamics. Let's explore the key components and rationale behind their inclusion:

1. Price-to-Earnings (P/E) Ratio:

The Price-to-Earnings ratio is a widely used valuation metric that compares a company's current stock price to its earnings per share (EPS).

A lower P/E ratio may indicate that the stock is undervalued relative to its earnings potential, while a higher ratio may suggest overvaluation.

By incorporating the P/E ratio, we offer insight into market sentiment and investor expectations regarding a company's future earnings growth prospects.

2. Price-to-Book (P/B) Ratio:

The Price-to-Book ratio evaluates a company's market value relative to its book value, which represents its net asset value per share.

A P/B ratio below 1 may indicate that the stock is trading at a discount to its book value, potentially signaling an undervalued opportunity.

Conversely, a P/B ratio above 1 may suggest overvaluation, as investors are paying a premium for the company's assets.

By considering the P/B ratio, we assess the market's perception of a company's tangible asset value and its implications for investment attractiveness.

3. Dividend Yield:

Dividend Yield measures the annual dividend income received from owning a stock relative to its current market price.

A higher dividend yield may indicate that the stock is undervalued or that the company is returning a significant portion of its profits to shareholders.

Conversely, a lower dividend yield may signal overvaluation or a company's focus on reinvesting profits for growth rather than distributing them as dividends.

By analyzing dividend yield, we offer insights into a company's capital allocation strategy and its implications for shareholder returns and valuation.

4. Discounted Cash Flow (DCF) Analysis:

Discounted Cash Flow analysis estimates the present value of a company's future cash flows, taking into account the time value of money.

By discounting projected cash flows back to their present value using an appropriate discount rate, DCF analysis provides a fair value estimate for the company's stock.

Comparing the calculated fair value to the current market price allows investors to assess whether the stock is undervalued, overvalued, or fairly valued.

By integrating DCF analysis, we offer a rigorous framework for valuing stocks based on their underlying cash flow generation potential.

Earnings Transparency:

Mitigating the risk of fraudulent financial reporting is crucial for investors. The indicator incorporates the Beneish M-Score, a robust model designed to detect earnings manipulation or financial irregularities. By evaluating various financial ratios and metrics, this component provides valuable insights into the integrity and transparency of a company's financial statements, aiding investors in mitigating potential risks.

Overall Score:

The pinnacle of the "Global Financial Index" is the Overall Score, a comprehensive amalgamation of financial strength, profitability, valuation, and manipulation risk, further enhanced by the inclusion of the Piotroski F-Score. This holistic score offers investors a succinct assessment of a company's overall health and investment potential, facilitating informed decision-making.

The weighting and balancing of each metric within the indicator have been meticulously calibrated to ensure accuracy and reliability. By amalgamating these diverse metrics, the "Global Financial Index" empowers traders and investors with a powerful tool for evaluating investment opportunities with confidence and precision.

This indicator is provided for informational purposes only and does not constitute financial advice, investment advice, or any other type of advice. The information provided by this indicator should not be relied upon for making investment decisions. Trading and investing in financial markets involves risk, and you should carefully consider your financial situation and consult with a qualified financial advisor before making any investment decisions. Past performance is not necessarily indicative of future results. The creator of this indicator makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the indicator or the information contained herein. Any reliance you place on such information is therefore strictly at your own risk. By using this indicator, you agree to assume full responsibility for any and all gains and losses, financial, emotional, or otherwise, experienced, suffered, or incurred by you.

Alert Before Bar Closei.imgur.com

Alert Before Bar Close

==========================

Example Figure

Originality and usefulness

This indicator/alert mechanism is unique in two ways. First, it provides alerts before the close of a candlestick, allowing time-based traders to prepare early to determine if the market is about to form a setup. Second, it introduces an observation time mechanism, enabling time-based traders to observe when the market is active, thereby avoiding too many false signals during electronic trading or when trading is light.

Detail

Regarding the settings (Arrow 1). The first input is to select the candlestick period you want to observe. The second is to notify a few seconds in advance. The third input sets the observation time. For example, if you set "1,2,3,4,5," the alert mechanism will only be activated during the period from 01:00:00 to 05:59:59, consistent with the time zone you set in TradingView. Additionally, I have set it so that the alert will only trigger once per candlestick, so don't worry about repeated alerts.

The alert setup is very simple, too. Follow the steps (Arrow 2, 3) to complete the setup. I have tested several periods and successfully received alerts on both mobile and computer. If anyone encounters any issues, feel free to let me know.

Buffett Quality Score [Communication Services]Buffett Quality Score "Communication Services": Analyzing Communication Companies with Precision

The communication services sector encompasses a diverse range of companies involved in telecommunications, media, and entertainment. To assess the financial strength and performance of companies within this sector, the Buffett Quality Score employs a tailored set of financial metrics. This scoring system, inspired by the Piotroski F-Score methodology, assigns points based on specific financial criteria to provide a comprehensive quality assessment.

Scoring Methodology

The Buffett Quality Score is designed to evaluate the overall financial health and quality of companies operating within the communication services sector. Each selected financial metric is chosen for its relevance and importance in evaluating a company's performance and potential for sustainable growth. The score is computed by assigning points based on the achievement of specific thresholds for each indicator, with the total points determining the final score. This methodology ensures a nuanced analysis that captures the unique dynamics of the communication services industry.

Selected Financial Metrics and Criteria

1. Return on Invested Capital (ROIC) > 10.0%

Relevance: ROIC measures a company's efficiency in allocating capital to profitable investments. For communication companies, a ROIC above 10.0% indicates effective capital utilization, crucial for sustaining growth and innovation.

2. Return on Equity (ROE) > 15.0%

Relevance: ROE evaluates the return generated on shareholders' equity. A ROE exceeding 15.0% signifies robust profitability and effective management of shareholder funds, essential for investor confidence in communication companies.

3. Revenue One-Year Growth > 10.0%

Relevance: High revenue growth indicates strong market demand and successful business strategies. For communication services, where innovation and content delivery are paramount, growth exceeding 10.0% reflects market leadership and competitive positioning.

4. Gross Margin > 40.0%

Relevance: Gross margin measures profitability after accounting for production costs. In the communication services sector, a gross margin above 40.0% demonstrates efficient operations and high-value content offerings, critical for maintaining competitive advantage.

5. Net Margin > 10.0%

Relevance: Net margin assesses overall profitability after all expenses. A net margin exceeding 10.0% indicates effective cost management and operational efficiency, fundamental for sustained profitability in communication companies.

6. EPS One-Year Growth > 10.0%

Relevance: EPS growth reflects the company's ability to increase earnings per share. For communication firms, where content monetization and subscription models are prevalent, EPS growth above 10.0% signals successful business expansion and value creation.

7. Piotroski F-Score > 6.0

Relevance: The Piotroski F-Score evaluates fundamental strength across various financial metrics. A score above 6.0 suggests strong financial health and operational efficiency, crucial for navigating competitive pressures in the communication services industry.

8. Price/Earnings Ratio (Forward) < 25.0

Relevance: The forward P/E ratio compares current share price to expected future earnings. A ratio below 25.0 indicates reasonable valuation relative to growth prospects, important for investors seeking value opportunities in communication stocks.

9. Current Ratio > 1.5

Relevance: The current ratio assesses short-term liquidity by comparing current assets to current liabilities. In communication companies, a ratio above 1.5 ensures financial flexibility and the ability to meet short-term obligations, vital for operational stability.

10. Debt to Equity Ratio < 1.0

Relevance: A lower debt to equity ratio indicates prudent financial management and reduced reliance on debt financing. For communication firms, maintaining a ratio below 1.0 signifies a healthy balance sheet and lower financial risk.

Interpreting the Buffett Quality Score

0-4 Points: Indicates potential weaknesses across multiple financial areas, suggesting higher risk.

5 Points: Represents average performance, warranting further analysis to understand underlying factors.

6-10 Points: Reflects strong financial health and quality, positioning the company favorably within the competitive communication services industry.

Conclusion

The Buffett Quality Score provides a robust framework for evaluating communication companies, emphasizing critical financial indicators tailored to industry dynamics. By leveraging these insights, investors and analysts can make informed decisions, identifying companies poised for sustainable growth and performance in the ever-evolving communication services landscape.

Disclaimer: The Buffett Quality Score serves as a tool for financial analysis and should not replace professional advice or comprehensive due diligence. Investors should conduct thorough research and consult with financial experts based on individual investment objectives.

Buffett Quality Score [Information Technology]Buffett Quality Score 'Information Technology': Assessing Tech Companies with Precision

The information technology sector is characterized by rapid innovation, high growth potential, and significant competition. To evaluate the financial health and performance of companies within this dynamic industry, the Buffett Quality Score employs a tailored set of financial metrics. This scoring system, inspired by the Piotroski F-Score methodology, assigns points based on specific financial criteria to provide a comprehensive quality assessment.

Scoring Methodology

The Buffett Quality Score is designed to assess the overall financial strength and quality of companies within the tech sector. Each selected financial metric is chosen for its relevance and importance in evaluating a company's performance and potential for sustainable growth. The score is computed by assigning points based on the achievement of specific thresholds for each indicator, with the total points determining the final score. This methodology ensures a nuanced analysis that captures the unique dynamics of the information technology industry.

Selected Financial Metrics and Criteria

1. Return on Invested Capital (ROIC) > 10.0%

Relevance: ROIC measures a company's efficiency in allocating capital to profitable investments. For tech companies, a ROIC above 10.0% indicates effective use of investment capital to generate strong returns, crucial for sustaining innovation and growth.

2. Return on Assets (ROA) > 5.0%

Relevance: ROA assesses how efficiently a company utilizes its assets to generate earnings. A ROA above 5.0% signifies that the company is effectively leveraging its assets, which is vital in the capital-intensive tech sector.

3. Revenue One-Year Growth > 10.0%

Relevance: High revenue growth indicates robust market demand and successful product or service offerings. For tech companies, where rapid scalability is common, growth exceeding 10.0% demonstrates significant market traction and expansion potential.

4. Gross Margin > 40.0%

Relevance: Gross margin reflects the proportion of revenue remaining after accounting for the cost of goods sold. In the tech sector, a gross margin above 40.0% indicates efficient production and high-value offerings, essential for maintaining competitive advantage.

5. Net Margin > 15.0%

Relevance: Net margin measures overall profitability after all expenses. A net margin above 15.0% demonstrates strong financial health and the ability to convert revenue into profit, highlighting the company's operational efficiency.

6. EPS One-Year Growth > 10.0%

Relevance: Earnings per share (EPS) growth indicates the company's ability to increase profitability per share. For tech firms, EPS growth above 10.0% signals positive earnings momentum, reflecting successful business strategies and market adoption.

7. Piotroski F-Score > 6.0

Relevance: The Piotroski F-Score assesses fundamental strength, including profitability, leverage, liquidity, and operational efficiency. A score above 6.0 suggests solid financial fundamentals and resilience in the competitive tech landscape.

8. Price/Earnings Ratio (Forward) < 25.0

Relevance: The forward P/E ratio compares current share price to expected future earnings. A ratio below 25.0 indicates reasonable valuation relative to growth expectations, important for identifying undervalued opportunities in the fast-paced tech sector.

9. Current Ratio > 1.5

Relevance: The current ratio evaluates short-term liquidity by comparing current assets to current liabilities. In the tech industry, a ratio above 1.5 ensures the company can meet its short-term obligations, essential for operational stability.

10. Debt to Equity Ratio < 1.0

Relevance: A lower debt to equity ratio signifies prudent financial management and reduced reliance on debt. For tech companies, which often require significant investment in R&D, a ratio below 1.0 highlights a strong financial structure.

Interpreting the Buffett Quality Score

0-4 Points: Indicates potential weaknesses across multiple financial areas, suggesting higher risk.

5 Points: Represents average performance, warranting further analysis to understand underlying factors.

6-10 Points: Reflects strong financial health and quality, positioning the company favorably within the competitive tech industry.

Conclusion

The Buffett Quality Score provides a strategic framework for evaluating tech companies, emphasizing critical financial indicators tailored to industry dynamics. By leveraging these insights, investors and analysts can make informed decisions, identifying companies poised for sustainable growth and performance in the ever-evolving tech landscape.

Disclaimer: The Buffett Quality Score serves as a tool for financial analysis and should not replace professional advice or comprehensive due diligence. Investors should conduct thorough research and consult with financial experts based on individual investment objectives.

Buffett Quality Score [Financials]Evaluating Financial Companies with the Buffett Quality Score 'Financials'

The financial sector, with its unique regulatory environment and market dynamics, requires a tailored approach to financial evaluation. The Buffett Quality Score is meticulously designed to assess the financial robustness and quality of companies within this sector. By focusing on industry-specific financial metrics, this scoring system provides valuable insights for investors and analysts navigating the complexities of the financial industry.

Scoring Methodology

Each selected financial metric contributes a point to the overall score if the specified condition is met. The combined score is a summation of points across all criteria, providing a comprehensive assessment of financial health and quality.

Selected Financial Metrics and Criteria

1. Altman Z-Score > 2.0

Relevance: The Altman Z-Score evaluates bankruptcy risk based on profitability, leverage, liquidity, solvency, and activity. In the financial sector, where market stability and solvency are critical, a score above 2.0 signifies a lower risk of financial distress.

2. Debt to Equity Ratio < 2.0

Relevance: A lower Debt to Equity Ratio signifies prudent financial management and reduced reliance on debt financing. This is particularly important for financial companies, which need to manage leverage carefully to avoid excessive risk.

3. Interest Coverage > 3.0

Relevance: The Interest Coverage Ratio measures a company's ability to meet its interest obligations from operating earnings. A ratio above 3.0 indicates that the company can comfortably cover its interest expenses, reducing the risk of default.

4. Return on Equity (ROE) > 10.0%

Relevance: ROE indicates the company's ability to generate profits from shareholder equity. An ROE above 10.0% suggests efficient use of capital and strong returns for investors, which is a key performance indicator for financial companies.

5. Return on Assets (ROA) > 1.0%

Relevance: ROA measures the company's ability to generate earnings from its assets. In the financial sector, where asset management is crucial, an ROA above 1.0% indicates effective use of assets to generate profits.

6. Net Margin > 10.0%

Relevance: Net Margin measures overall profitability after all expenses. A margin above 10.0% demonstrates strong financial performance and the ability to convert revenue into profit effectively.

7. Revenue One-Year Growth > 5.0%

Relevance: Revenue growth reflects market demand and company expansion. In the financial sector, where growth can be driven by new products and services, revenue exceeding 5.0% indicates successful market penetration and business expansion.

8. EPS One-Year Growth > 5.0%

Relevance: EPS growth reflects the company's ability to increase earnings per share over the past year. For financial companies, growth exceeding 5.0% signals positive earnings momentum and potential market strength.

9. Price/Earnings Ratio (Forward) < 20.0

Relevance: The Forward P/E Ratio reflects investor sentiment and earnings expectations. A ratio below 20.0 suggests reasonable valuation relative to earnings projections, which is important for investors seeking value and growth opportunities in the financial sector.

10. Piotroski F-Score > 6.0

Relevance: The Piotroski F-Score assesses fundamental strength, emphasizing profitability, leverage, liquidity, and operating efficiency. For financial companies, a score above 6.0 indicates strong financial health and operational efficiency.

Interpreting the Buffett Quality Score

0-4 Points: Indicates potential weaknesses across multiple financial areas, warranting careful consideration and risk assessment.

5 Points: Suggests average performance based on sector-specific criteria, requiring further analysis to determine investment viability.

6-10 Points: Signifies strong financial health and quality, positioning the company favorably within the competitive financial industry.

Conclusion

The Buffett Quality Score offers a strategic framework for evaluating financial companies, emphasizing critical financial indicators tailored to industry dynamics. By leveraging these insights, stakeholders can make informed decisions and identify companies poised for sustainable growth and performance in the evolving financial landscape.

Disclaimer: The Buffett Quality Score serves as a tool for financial analysis and should not replace professional advice or comprehensive due diligence. Investors should conduct thorough research and consult with financial experts based on individual investment objectives.

Buffett Quality Score [Health Care]Evaluating Health Care Companies with the Buffett Quality Score "Health Care"

The health care sector presents unique challenges and opportunities, demanding a specialized approach to financial evaluation. The Buffett Quality Score is meticulously designed to assess the financial robustness and quality of companies within this dynamic industry. By focusing on industry-specific financial metrics, this scoring system provides valuable insights for investors and analysts navigating the complexities of the health care sector.

Scoring Methodology

Each selected financial metric contributes a point to the overall score if the specified condition is met. The combined score is a summation of points across all criteria, providing a comprehensive assessment of financial health and quality.

Selected Financial Metrics and Criteria

1. Altman Z-Score > 2.0

Relevance: The Altman Z-Score evaluates bankruptcy risk based on profitability, leverage, liquidity, solvency, and activity. In the health care sector, where regulatory changes and technological advancements can impact financial stability, a score above 2.0 signifies a lower risk of financial distress.

2. Piotroski F-Score > 6.0

Relevance: The Piotroski F-Score assesses fundamental strength, emphasizing profitability, leverage, liquidity, and operating efficiency. For health care companies, which often face regulatory challenges and R&D expenses, a score above 6.0 indicates strong financial health and operational efficiency.

3. Current Ratio > 1.5

Relevance: The Current Ratio evaluates short-term liquidity by comparing current assets to current liabilities. In the health care sector, where cash flow stability is essential for ongoing operations, a ratio above 1.5 ensures the company's ability to meet near-term obligations.

4. Debt to Equity Ratio < 1.0

Relevance: A lower Debt to Equity Ratio signifies prudent financial management and reduced reliance on debt financing. This is critical for health care companies, which require significant investments in research and development without overleveraging.

5. EBITDA Margin > 15.0%

Relevance: The EBITDA Margin measures operating profitability, excluding non-operating expenses. A margin above 15.0% indicates efficient operations and the ability to generate substantial earnings from core activities.

6. EPS One-Year Growth > 5.0%

Relevance: EPS growth reflects the company's ability to increase earnings per share over the past year. For health care companies, which often face pricing pressures and regulatory changes, growth exceeding 5.0% signals positive earnings momentum and potential market strength.

7. Net Margin > 10.0%

Relevance: Net Margin measures overall profitability after all expenses. A margin above 10.0% demonstrates strong financial performance and the ability to convert revenue into profit effectively.

8. Return on Equity (ROE) > 15.0%

Relevance: ROE indicates the company's ability to generate profits from shareholder equity. An ROE above 15.0% suggests efficient use of capital and strong returns for investors.

9. Revenue One-Year Growth > 5.0%

Relevance: Revenue growth reflects market demand and company expansion. In the health care sector, where innovation drives growth, revenue exceeding 5.0% indicates successful market penetration and product adoption.

10. Price/Earnings Ratio (Forward) < 20.0

Relevance: The Forward P/E Ratio reflects investor sentiment and earnings expectations. A ratio below 20.0 suggests reasonable valuation relative to earnings projections, which is important for investors seeking value and growth opportunities in the health care sector.

Interpreting the Buffett Quality Score

0-4 Points: Indicates potential weaknesses across multiple financial areas, warranting careful consideration and risk assessment.

5 Points: Suggests average performance based on sector-specific criteria, requiring further analysis to determine investment viability.

6-10 Points: Signifies strong financial health and quality, positioning the company favorably within the competitive health care industry.

Conclusion

The Buffett Quality Score offers a strategic framework for evaluating health care companies, emphasizing critical financial indicators tailored to industry dynamics. By leveraging these insights, stakeholders can make informed decisions and identify companies poised for sustainable growth and performance in the evolving health care landscape.

Disclaimer: The Buffett Quality Score serves as a tool for financial analysis and should not replace professional advice or comprehensive due diligence. Investors should conduct thorough research and consult with financial experts based on individual investment objectives.

Buffett Quality Score [Consumer Discretionary]Evaluating Consumer Discretionary Companies with the Buffett Quality Score

The consumer discretionary sector, characterized by its sensitivity to economic cycles and consumer spending patterns, demands a robust framework for financial evaluation. The Buffett Quality Score offers a comprehensive assessment of financial health and performance specifically tailored to this dynamic industry. This scoring system combines critical financial ratios uniquely relevant to consumer discretionary companies, providing investors and analysts with a reliable tool for evaluation.

Selected Financial Metrics and Criteria

1. Altman Z-Score > 2.0

Relevance: The Altman Z-Score assesses bankruptcy risk, combining profitability, leverage, liquidity, solvency, and activity ratios. For consumer discretionary companies, which often face volatile market conditions, a score above 2.0 indicates financial stability and the ability to withstand economic downturns. This metric is particularly important in this sector due to the high variability in consumer spending.

2. Piotroski F-Score > 6.0

Relevance: The Piotroski F-Score evaluates fundamental strength based on profitability, leverage, liquidity, and operating efficiency. In the consumer discretionary sector, where rapid changes in consumer preferences can impact performance, a score above 6.0 highlights strong fundamental performance and resilience. This score is crucial for identifying companies with robust financial foundations in a highly competitive environment.

3. Asset Turnover > 1.0

Relevance: Asset Turnover measures the efficiency of asset use in generating sales. For consumer discretionary companies, a ratio above 1.0 signifies effective utilization of assets to drive revenue growth. Given the sector's reliance on high sales volumes and rapid inventory turnover, this metric is key to assessing operational efficiency.

4. Current Ratio > 1.5

Relevance: The Current Ratio assesses liquidity by comparing current assets to current liabilities. A ratio above 1.5 ensures that consumer discretionary companies can meet short-term obligations. This liquidity is essential for maintaining operational stability and flexibility to adapt to market changes, especially during economic fluctuations.

5. Debt to Equity Ratio < 1.0

Relevance: A lower Debt to Equity Ratio indicates prudent financial management and reduced reliance on debt. This is particularly important for consumer discretionary companies, which need to maintain financial flexibility to invest in new trends and innovations without overleveraging. Lower debt levels also reduce risk during economic downturns.

6. EBITDA Margin > 15.0%

Relevance: The EBITDA Margin measures operating profitability. A margin above 15.0% indicates efficient operations and the ability to generate sufficient earnings before interest, taxes, depreciation, and amortization. This is crucial for sustaining profitability in a competitive and fluctuating market, ensuring the company can reinvest in growth and innovation.

7. EPS One-Year Growth > 5.0%

Relevance: EPS growth reflects the company’s ability to increase earnings per share over the past year. For consumer discretionary companies, growth exceeding 5.0% signals positive earnings momentum, which is vital for investor confidence and the ability to fund future growth initiatives. This metric highlights companies that are successfully increasing profitability.

8. Gross Margin > 25.0%

Relevance: Gross Margin represents the profitability of sales after production costs. A margin exceeding 25.0% indicates strong pricing power and effective cost management, crucial for maintaining profitability while adapting to changing consumer demands. High gross margins are indicative of a company’s ability to control costs and price products competitively.

9. Net Margin > 10.0%

Relevance: Net Margin measures overall profitability after all expenses. A margin above 10.0% highlights the company’s ability to maintain strong profit levels, ensuring financial health and stability. This is essential for sustaining operations and investing in new opportunities, reflecting the company's efficiency in converting revenue into actual profit.

10.Return on Equity (ROE) > 15.0%

Relevance: ROE indicates how effectively a company uses equity to generate profits. An ROE above 15.0% signifies strong shareholder value creation. This metric is key for evaluating long-term performance in the consumer discretionary sector, where investor returns are closely tied to the company’s ability to innovate and grow. High ROE demonstrates effective management and profitable use of equity capital.

Interpreting the Buffett Quality Score

0-4 Points: Indicates potential weaknesses across multiple financial areas, warranting further investigation and risk assessment.

5 Points: Suggests average performance based on sector-specific criteria, indicating a need for cautious optimism.

6-10 Points: Signifies strong financial health and quality, meeting or exceeding most performance thresholds, making the company a potentially attractive investment.

Conclusion

The Buffett Quality Score provides a structured approach to evaluating financial health and performance. By focusing on these essential financial metrics, stakeholders can make informed decisions, identifying companies that are well-positioned to thrive in the competitive and economically sensitive consumer discretionary sector.

Disclaimer: The Buffett Quality Score serves as a tool for financial evaluation and analysis. It is not a substitute for professional financial advice or investment recommendations. Investors should conduct thorough research and seek personalized guidance based on individual circumstances.