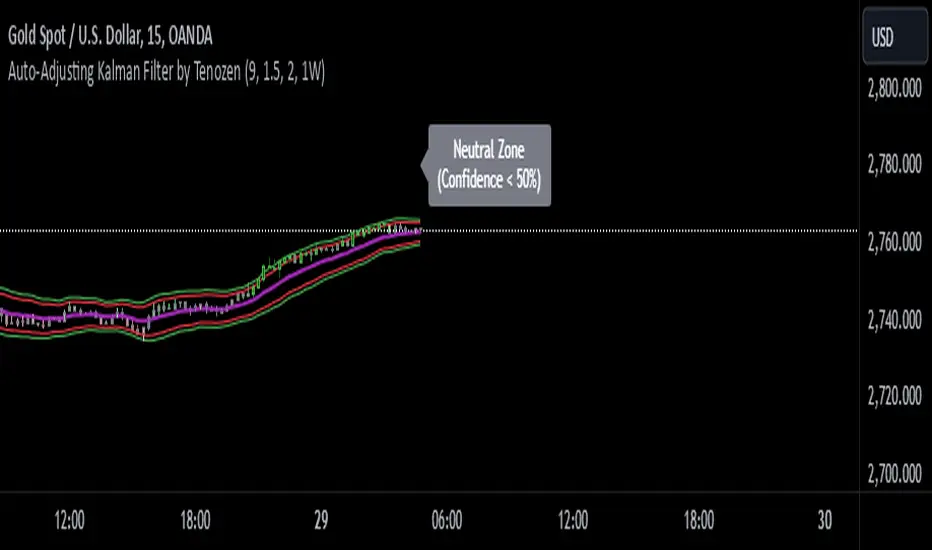

Auto-Adjusting Kalman Filter by TenozenNew year, new indicator! Auto-Adjusting Kalman Filter is an indicator designed to provide an adaptive approach to trend analysis. Using the Kalman Filter (a recursive algorithm used in signal processing), this algo dynamically adjusts to market conditions, offering traders a reliable way to identify trends and manage risk! In other words, it's a remaster of my previous indicator, Kalman Filter by Tenozen.

What's the difference with the previous indicator (Kalman Filter by Tenozen)?

The indicator adjusts its parameters (Q and R) in real-time using the Average True Range (ATR) as a measure of market volatility. This ensures the filter remains responsive during high-volatility periods and smooth during low-volatility conditions, optimizing its performance across different market environments.

The filter resets on a user-defined timeframe, aligning its calculations with dominant trends and reducing sensitivity to short-term noise. This helps maintain consistency with the broader market structure.

A confidence metric, derived from the deviation of price from the Kalman filter line (measured in ATR multiples), is visualized as a heatmap:

Green : Bullish confidence (higher values indicate stronger trends).

Red : Bearish confidence (higher values indicate stronger trends).

Gray : Neutral zone (low confidence, suggesting caution).

This provides a clear, objective measure of trend strength.

How it works?

The Kalman Filter estimates the "true" price by filtering out market noise. It operates in two steps, that is, prediction and update. Prediction is about projection the current state (price) forward. Update is about adjusting the prediction based on the latest price data. The filter's parameters (Q and R) are scaled using normalized ATR, ensuring adaptibility to changing market conditions. So it means that, Q (Process Noise) increases during high volatility, making the filter more responsive to price changes and R (Measurement Noise) increases during low volatility, smoothing out the filter to avoid overreacting to minor fluctuations. Also, the trend confidence is calculated based on the deviation of price from the Kalman filter line, measured in ATR multiples, this provides a quantifiable measure of trend strength, helping traders assess market conditions objectively.

How to use?

Use the Kalman Filter line to identify the prevailing trend direction. Trade in alignment with the filter's slope for higher-probability setups.

Look for pullbacks toward the Kalman Filter line during strong trends (high confidence zones)

Utilize the dynamic stop-loss and take-profit levels to manage risk and lock in profits

Confidence Heatmap provides an objective measure of market sentiment, helping traders avoid low-confidence (neutral) zones and focus on high-probability opportunities

Guess that's it! I hope this indicator helps! Let me know if you guys got some feedback! Ciao!

Statistics

Moon Phases by Shailesh DesaiTrading Strategy Based on Lunar Phases

This custom trading indicator leverages the power of lunar cycles to provide unique market insights based on the four primary moon phases: New Moon, First Quarter, Full Moon, and Third Quarter. By aligning your trades with the natural rhythm of the moon, this strategy offers a different perspective to trading and can help enhance decision-making based on the cyclical nature of the market.

Key Features:

1. Moon Phase Identification:

o The indicator automatically identifies the current moon phase based on the user's selected timeframe and marks it on the chart.

o Each phase is visualized with a specific symbol and color to help traders easily recognize the current moon phase:

New Moon/Waxing Moon: Represented by a circle (colored as per user input).

First Quarter: Represented by a cross (colored as per user input).

Full Moon/Waning Moon: Represented by a circle (colored as per user input).

Third Quarter: Represented by a cross (colored as per user input).

2. Automatic Moon Phase Transition Detection:

o The indicator tracks and highlights when a phase change occurs. This feature ensures you are always aware of when the market moves from one phase to another.

o Moon phase changes are only visualized on the first bar of each new phase to avoid cluttering the chart.

3. Background Color Indicators:

o The background color dynamically changes according to the current moon phase, helping to reinforce the phase context for the trader. This feature makes it easy to see at a glance which phase the market is in.

4. Customizable Appearance:

o Customize the color of each moon phase to suit your preferences. Adjust the colors for the New Moon, First Quarter, Full Moon, and Third Quarter to align with your visual strategy.

5. Avoids Unsupported Timeframes:

o This indicator does not support monthly timeframes, ensuring that it operates smoothly only on timeframes that are compatible with the lunar cycle.

How to Use:

• The moon phases are thought to have an influence on human behavior and the market's psychology, making this indicator useful for traders who wish to integrate lunar cycles into their strategy.

• Traders can use the phase changes as an indicator of potential market momentum or reversal points. For example:

o New Moon may indicate the beginning of a new cycle, signaling a potential upward or downward move.

o Full Moon might suggest a peak or significant shift in market direction.

o First Quarter and Third Quarter phases may represent moments of consolidation or decision points.

Ideal for:

• Traders interested in cycle-based strategies or looking to experiment with new approaches.

• Those who believe in the influence of natural forces, including moon phases, on market movements.

• Technical analysts who want to add another layer of insights to their chart analysis.

Important Notes:

• The indicator uses precise astronomical calculations to identify the correct phase, ensuring accuracy.

• It’s important to understand that moon phase-based trading is not a standalone strategy but should ideally be combined with other technical analysis tools for maximum effectiveness.

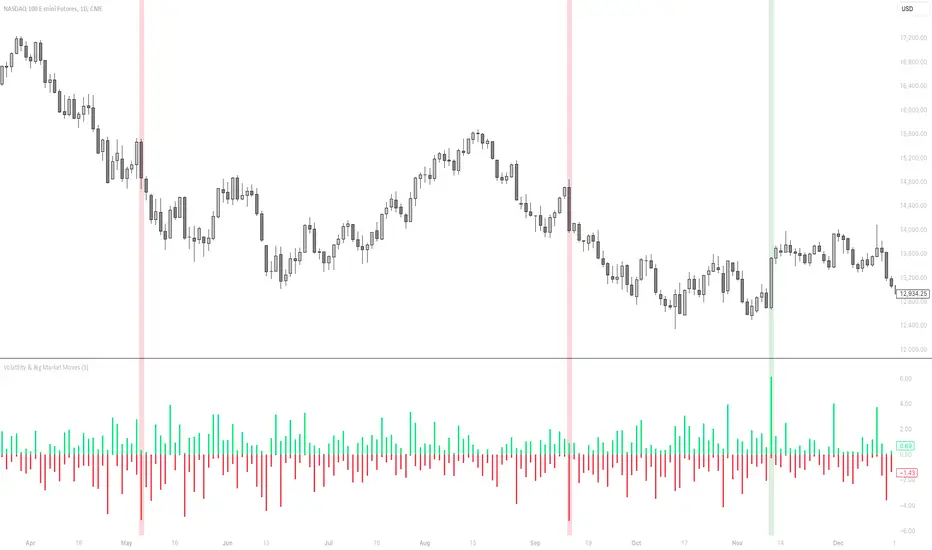

Volatility & Big Market MovesThis indicator shows the volatility per candle, and highlights candles where volatility exceeds a defined threshold.

Data shown:

Furthest %-distance from the previous candle's closing price to the top (positive histogram).

Furthest %-distance from the previous candle's closing price to the bottom (negative histogram).

Asset Rotation System [InvestorUnknown]Overview

This system creates a comprehensive trend "matrix" by analyzing the performance of six assets against both the US Dollar and each other. The objective is to identify and hold the asset that is currently outperforming all others, thereby focusing on maintaining an investment in the most "optimal" asset at any given time.

- - - Key Features - - -

1. Trend Classification:

The system evaluates the trend for each of the six assets, both individually against USD and in pairs (assetX/assetY), to determine which asset is currently outperforming others.

Utilizes five distinct trend indicators: RSI (50 crossover), CCI, SuperTrend, DMI, and Parabolic SAR.

Users can customize the trend analysis by selecting all indicators or choosing a single one via the "Trend Classification Method" input setting.

2. Backtesting:

Calculates an equity curve for each asset and for the system itself, which assumes holding only the asset deemed optimal at any time.

Customizable start date for backtesting; by default, it begins either 5000 bars ago (the maximum in TradingView) or at the inception of the youngest asset included, whichever is shorter. If the youngest asset's history exceeds 5000 bars, the system uses 5000 bars to prevent errors.

The equity curve is dynamically colored based on the asset held at each point, with this coloring also reflected on the chart via barcolor().

Performance metrics like returns, standard deviation of returns, Sharpe, Sortino, and Omega ratios, along with maximum drawdown, are computed for each asset and the system's equity curve.

3 Alerts:

Supports alerts for when a new, confirmed optimal asset is identified. However, due to TradingView limitations, the specific asset cannot be included in the alert message.

- - - Usage - - -

1. Select Assets/Tickers:

Choose which assets or tickers you want to include in the rotation system. Ensure that all selected tickers are denominated in USD to maintain consistency in analysis.

2. Configure Trend Classification:

Decide on the trend classification method from the available options (RSI, CCI, SuperTrend, DMI, or Parabolic SAR, All) and adjust the settings to your preferences. This customization allows you to tailor the system to different market conditions or your specific trading strategy.

3. Utilize Backtesting for Calibration:

Use the backtesting results, including equity curves and performance metrics, to fine-tune your chosen trend indicators.

Be cautious not to overemphasize performance maximization, as this can lead to overfitting. The goal is to achieve a robust system that performs well across various market conditions, rather than just optimizing for past data.

- - - Parameters - - -

Tickers:

Asset 1: Select the symbol for the first asset.

Asset 2: Select the symbol for the second asset.

Asset 3: Select the symbol for the third asset.

Asset 4: Select the symbol for the fourth asset.

Asset 5: Select the symbol for the fifth asset.

Asset 6: Select the symbol for the sixth asset.

General Settings:

Trend Classification Method: Choose from RSI, CCI, SuperTrend, DMI, PSAR, or "All" to determine how trends are analyzed.

Use Custom Starting Date for Backtest: Toggle to use a custom date for beginning the backtest.

Custom Starting Date: Set the custom start date for backtesting.

Plot Perf. Metrics Table: Option to display performance metrics in a table on the chart.

RSI (Relative Strength Index):

RSI Source: Choose the price data source for RSI calculation.

RSI Length: Set the period for the RSI calculation.

CCI (Commodity Channel Index):

CCI Source: Select the price data source for CCI calculation.

CCI Length: Determine the period for the CCI.

SuperTrend:

SuperTrend Factor: Adjust the sensitivity of the SuperTrend indicator.

SuperTrend Length: Set the period for the SuperTrend calculation.

DMI (Directional Movement Index):

DMI Length: Define the period for DMI calculations.

Parabolic SAR:

PSAR Start: Initial acceleration factor for the Parabolic SAR.

PSAR Increment: Increment value for the acceleration factor.

PSAR Max Value: Maximum value the acceleration factor can reach.

Notes/Recommendations:

While this system is operational, it's important to recognize that it relies on "basic" indicators, which may not be ideal for generating trading signals on their own. I strongly suggest that users delve into the code to grasp the underlying logic of the system. Consider customizing it by integrating more sophisticated and higher-quality trend-following indicators to enhance its performance and reliability.

Disclaimer:

This system's backtest results are historical and do not predict future performance. Use for educational purposes only; not investment advice.

[COG] Advanced School Run StrategyAdvanced School Run Strategy (ASRS) – Explanation

Overview: The Advanced School Run Strategy (ASRS) is an intraday trading approach designed to identify breakout opportunities based on specific time and price patterns. This script applies the concepts of the Advanced School Run Strategy as outlined in Tom Hougaard's research, adapted to work seamlessly on TradingView charts. It leverages 5-minute candlestick data to set actionable breakout levels and provides traders with visual cues and alerts to make informed decisions.

Features:

Dynamic Breakout Levels: Automatically calculates high and low levels based on the market's behavior during the initial trading minutes.

Custom Visualization: Highlights breakout zones with customizable colors and transparency, providing clear visual feedback for bullish and bearish breakouts.

Configurable Alerts: Includes alert conditions for both bullish and bearish breakouts, ensuring traders never miss a trading opportunity.

Reset Logic: Resets breakout levels daily at the market open to ensure accurate signal generation for each session.

How It Works:

The script identifies key levels (high and low) after a configurable number of minutes from the market open (default: 25 minutes).

If the price breaks above the high level or below the low level, a corresponding breakout is detected.

The script draws breakout zones on the chart and triggers alerts based on the breakout direction.

All levels and signals reset at the start of each new trading session, maintaining relevance to current market conditions.

Customization Options:

Line and box colors for bullish and bearish breakouts.

Transparency levels for breakout visualizations.

Alert settings to receive notifications for detected breakouts.

Acknowledgment: This script is inspired by Tom Hougaard's Advanced School Run Strategy. The methodology has been translated into Pine Script for TradingView users, adhering to TradingView’s policies and community guidelines. This script does not redistribute proprietary content from the original research but implements the principles for educational and analytical purposes.

Anomaly DetectorPrice Anomaly Detector

This is a script designed to identify unusual price movements. By analyzing deviations from typical price behavior, this tool helps traders spot potential trading opportunities and manage risks effectively.

---

Features

- Anomaly Detection: Flags price points that significantly deviate from the average.

- Visual Indicators: Highlights anomalies with background colors and cross markers.

- Customizable Settings: Adjust sensitivity and window size to match your trading strategy.

- Real-Time Analysis: Continuously updates anomaly signals as new data is received.

---

Usage

After adding the indicator to your chart:

1. View Anomalies: Red backgrounds and cross markers indicate detected anomalies.

2. Adjust Settings: Modify the `StdDev Threshold` and `Window Length` to change detection sensitivity.

3. Interpret Signals:

- Red Background: Anomaly detected on that bar.

- Red Cross: Specific point of anomaly.

---

Inputs

- StdDev Threshold: Higher values reduce anomaly sensitivity. Default: 2.0.

- Window Length: Larger windows smooth data, reducing false positives. Default: 20.

---

Limitations

- Approximation Method: Uses a simple method to detect anomalies, which may not capture all types of unusual price movements.

- Performance: Extremely large window sizes may impact script performance.

- Segment Detection: Does not group consecutive anomalies into segments.

---

Disclaimer : This tool is for educational purposes only. Trading involves risk, and you should perform your own analysis before making decisions. The author is not liable for any losses incurred.

Rolling CAGRRolling CAGR (Compound Annual Growth Rate) Indicator

This indicator calculates and plots the rolling Compound Annual Growth Rate (CAGR) for any selected data source. CAGR represents the mean annual growth rate of an investment over a specified time period, taking into account the effect of compounding.

Features:

• Customizable data source (default: close price)

• Adjustable time period in years

• Configurable trading days per year (252 for stocks, 365 for crypto)

• Results displayed as percentage values

• Works on daily timeframes

Input Parameters:

• Data Source: Select the price or indicator data to analyze

• Number of Years: Set the lookback period for CAGR calculation

• Trading Days in a Year: Adjust based on market type (252 for stocks, 365 for crypto)

Usage:

Perfect for analyzing long-term growth rates and comparing investment performance across different periods. The indicator provides a rolling view of compound growth, helping traders and investors understand the sustained growth rate of an asset over their chosen timeframe.

Note: This indicator is designed for daily timeframes as CAGR calculations are most meaningful over longer periods.

Formula Used:

CAGR = (End Value / Start Value)^(1/number of years) - 1

Quantitative Breakout Bands (AIBitcoinTrend)Quantitative Breakout Bands (AIBitcoinTrend) is an advanced indicator designed to adapt to dynamic market conditions by utilizing a Kalman filter for real-time data analysis and trend detection. This innovative tool empowers traders to identify price breakouts, evaluate trends, and refine their trading strategies with precision.

👽 What Are Quantitative Breakout Bands, and Why Are They Unique?

Quantitative Breakout Bands combine advanced filtering techniques (Kalman Filters) with statistical measures such as mean absolute error (MAE) to create adaptive price bands. These bands adjust to market conditions dynamically, providing insights into volatility, trend strength, and breakout opportunities.

What sets this indicator apart is its ability to incorporate both position (price) and velocity (rate of price change) into its calculations, making it highly responsive yet smooth. This dual consideration ensures traders get reliable signals without excessive lag or noise.

👽 The Math Behind the Indicator

👾 Kalman Filter Estimation:

At the core of the indicator is the Kalman Filter, a recursive algorithm used to predict the next state of a system based on past observations. It incorporates two primary elements:

State Prediction: The indicator predicts future price (position) and velocity based on previous values.

Error Covariance Adjustment: The process and measurement noise parameters refine the prediction's accuracy by balancing smoothness and responsiveness.

👾 Breakout Bands Calculation:

The breakout bands are derived from the mean absolute error (MAE) of price deviations relative to the filtered trendline:

float upperBand = kalmanPrice + bandMultiplier * mae

float lowerBand = kalmanPrice - bandMultiplier * mae

The multiplier allows traders to adjust the sensitivity of the bands to market volatility.

👾 Slope-Based Trend Detection:

A weighted slope calculation measures the gradient of the filtered price over a configurable window. This slope determines whether the market is trending bullish, bearish, or neutral.

👾 Trailing Stop Mechanism:

The trailing stop employs the Average True Range (ATR) to calculate dynamic stop levels. This ensures positions are protected during volatile moves while minimizing premature exits.

👽 How It Adapts to Price Movements

Dynamic Noise Calibration: By adjusting process and measurement noise inputs, the indicator balances smoothness (to reduce noise) with responsiveness (to adapt to sharp price changes).

Trend Responsiveness: The Kalman Filter ensures that trend changes are quickly identified, while the slope calculation adds confirmation.

Volatility Sensitivity: The MAE-based bands expand and contract in response to changes in market volatility, making them ideal for breakout detection.

👽 How Traders Can Use the Indicator

👾 Breakout Detection:

Bullish Breakouts: When the price moves above the upper band, it signals a potential upward breakout.

Bearish Breakouts: When the price moves below the lower band, it signals a potential downward breakout.

The trailing stop feature offers a dynamic way to lock in profits or minimize losses during trending moves.

👾 Trend Confirmation:

The color-coded Kalman line and slope provide visual cues:

Bullish Trend: Positive slope, green line.

Bearish Trend: Negative slope, red line.

👽 Why It’s Useful for Traders

Dynamic and Adaptive: The indicator adjusts to changing market conditions, ensuring relevance across timeframes and asset classes.

Noise Reduction: The Kalman Filter smooths price data, eliminating false signals caused by short-term noise.

Comprehensive Insights: By combining breakout detection, trend analysis, and risk management, it offers a holistic trading tool.

👽 Indicator Settings

Process Noise (Position & Velocity): Adjusts filter responsiveness to price changes.

Measurement Noise: Defines expected price noise for smoother trend detection.

Slope Window: Configures the lookback for slope calculation.

Lookback Period for MAE: Defines the sensitivity of the bands to volatility.

Band Multiplier: Controls the band width.

ATR Multiplier: Adjusts the sensitivity of the trailing stop.

Line Width: Customizes the appearance of the trailing stop line.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

Range Averages [Blu_Ju]Using Ranges

A popular analysis technique among traders is to use statistical price data over a given time range. For example, a trader might want to examine the average price range for the time period of 9:30 am - 10:00 am EST (commonly referred to as the Opening Range), and compare the average range to the current, live range as it forms.

What this Script Does

This script allows a user to monitor the current price range against the average price range of up to six different periods of time (sessions). The data is presented in a table in the chart window, with four stats listed per session:

Range: This is the most recent (or current) price range for the session. This value is updated in real-time as the price range forms.

Avg: This is the average price range for the session. (See below for how this is calculated.)

Diff: This is the price difference between the most recent (or current) price range of the session and the average price range of the session. When the most recent price range is smaller than the average, this will be a negative number. This value is updated in real-time as the price range forms.

Range %: This is the percent value of the most recent (or current) price range of the session compared to the average price range of the session. For example, If the most recent price range was half that of the average price range, the Range % would be 50%. If the most recent price range was twice that of the average price range, the Range % would be 200%. A Range % value of 100% indicates that the most recent price range is equal to the average price range. This value is updated in real-time as the price range forms.

What Makes this Script Unique

While this is not the only publicly available average range script, what makes it unique is the complete user control over up to six sessions (including overlapping sessions) and the display of that data.

Scope of this Script

This script is intended for use on intraday timeframes only. It will not calculate properly on daily or higher timeframes. Additionally, for the calculation to be correct, the input session must be evenly divisible by the chart timeframe. For example, if the user inputs a session that is 30 minutes long (e.g., 9:30 am - 10:00 am), then the calculations would be correct on the 1, 2, 3, 5, 10, 15, and 30-minute timeframes only.

User Inputs

This script was written to provide the user with maximum control over the range data and how that data is displayed. These are the user inputs:

Data - Input the number of days used to calculate the average price range of the sessions. This input is applied to all six sessions. The default value is 10.

Sessions - There are six sessions the user can set. Checking the box next to a session will cause that session data to be calculated and displayed. This allows the user to turn on or off a session at their discretion. The default value are displayed in the chart image above.

Visibility - Checking this box will cause the range data to be displayed only when the range is currently forming (i.e., live price is within the session). This allows the user to display the data from multiple sessions only when needed.

Visual Styles - This section has controls for how the data table is displayed. The user can select the table position, colors and border, and text size.

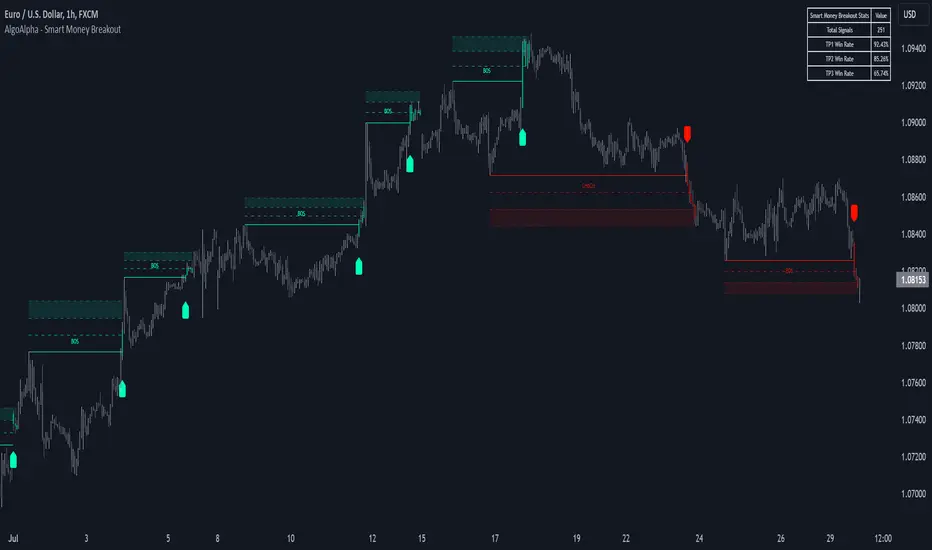

Smart Money Breakout Signals [AlgoAlpha]Introducing the Smart Money Breakout Signals, a cutting-edge trading indicator designed to identify key structural shifts and breakout opportunities in the market. This tool leverages a blend of smart money concepts like Break of Structure (BOS) and Change of Character (CHoCH) to provide traders with actionable insights into market direction and potential entry or exit points.

Key Features :

✨ Market Structure Analysis : Automatically detects and labels BOS and CHoCH for trend confirmation and reversals.

🎨 Customizable Visualization : Tailor bullish and bearish colors for breakout lines and signals to suit your preferences.

📊 Dynamic Take-Profit Targets : Displays three tiered take-profit levels based on breakout volatility.

🔔 Real-Time Alerts : Stay ahead of the game with notifications for bullish and bearish breakouts.

📋 Performance Dashboard : Monitor signal statistics, including win rates and total signals, directly on your chart.

How to Use :

Add the Indicator : Add the script to your favourites ⭐ and customize settings like market structure horizon and confirmation type.

Monitor Breakouts : Observe BOS and CHoCH labels to identify potential trend shifts. Use the breakout lines and tiered take-profit levels to plan trades effectively.

Set Alerts : Enable alerts for bullish or bearish breakouts to act on opportunities without constant monitoring.

How It Works :

The indicator identifies market structure by analyzing pivot highs and lows over a user-defined time horizon. A breakout is confirmed based on either candle closes or wicks surpassing previous pivot points. Upon detection, the script generates signals with breakout lines and calculates take-profit targets based on the distance from the breakout level. A built-in dashboard tracks performance metrics like total signals and win rates, giving traders real-time feedback on strategy effectiveness.

200 EMA Breakout & Retest Strategy200 EMA Breakout & Retest Strategy

This script is designed for traders who rely on the 200 EMA as a key indicator for trend direction and trade setups. The strategy identifies potential buy and sell opportunities based on breakouts and subsequent retests of the 200 EMA.

How It Works

EMA Breakout Detection:

The script monitors when the price crosses and closes above or below the 200 EMA.

No signal is generated immediately upon the breakout.

Retest Confirmation:

After the breakout, the price must retrace to touch the 200 EMA.

A valid signal occurs only when the price touches the EMA and the candle closes above (for buy) or below (for sell).

Trade Signal Generation:

Once the retest is confirmed:

A Buy Signal is generated if the price closes above the 200 EMA after the retest.

A Sell Signal is generated if the price closes below the 200 EMA after the retest.

The script calculates:

Stop Loss: Placed at the low of the candle for a buy signal and at the high of the candle for a sell signal.

Take Profit: Based on a customizable Risk-Reward Ratio (default is 1:2).

Visual Indicators:

The 200 EMA is plotted on the chart for reference.

Buy/Sell signals are displayed as labels on the chart.

Stop loss and take profit levels are drawn using dotted lines.

Customization Options

EMA Length: Adjustable (default is 200).

Risk-Reward Ratio: Customizable to suit different trading styles.

Who Is This For?

This strategy is ideal for traders who:

Prefer trading with the trend using EMA-based strategies.

Look for precise entry points with confirmation from retests.

Require automated calculation of risk-reward levels.

CAD CHF JPY (Index) vs USDDescription:

Analyze the combined performance of CAD, CHF, and JPY against the USD with this customized Forex currency index. This tool enables traders to gain a broader perspective of how these three currencies behave relative to the US Dollar by aggregating their movements into a single index. It’s a versatile tool designed for traders seeking actionable insights and trend identification.

Core Features:

Flexible Display Options:

Choose between Line Mode for a simplified view of the index trend or Candlestick Mode for detailed analysis of price action.

Custom Weight Adjustments:

Fine-tune the weight of each currency pair (USD/CAD, USD/CHF, USD/JPY) to better reflect your trading priorities or market expectations.

Moving Average Integration:

Add a moving average to smooth the data and identify trends more effectively. Choose your preferred type: SMA, EMA, WMA, or VWMA, and configure the number of periods to suit your strategy.

Streamlined Calculation:

The index aggregates data from USD/CAD, USD/CHF, and USD/JPY using a weighted average of their OHLC (Open, High, Low, Close) values, ensuring accuracy and adaptability to different market conditions.

Practical Applications:

Trend Identification:

Use the Line Mode with a moving average to confirm whether CAD, CHF, and JPY collectively show strength or weakness against the USD. A rising trendline signals currency strength, while a declining line suggests USD dominance.

Weight-Based Analysis:

If CAD is expected to lead, adjust its weight higher relative to CHF and JPY to emphasize its influence in the index. This customization makes the indicator adaptable to your market outlook.

Actionable Insights:

Identify key reversal points or breakout opportunities by analyzing the interaction of the index with its moving average. Combined with other technical tools, this indicator becomes a robust addition to any trader’s toolkit.

Additional Notes:

This indicator is a valuable resource for comparing the collective behavior of CAD, CHF, and JPY against the USD. Pair it with additional oscillators or divergence tools for a comprehensive market overview.

Perfect for both intraday analysis and swing trading strategies. Combine it with EUR GPB AUD (Index) indicator.

Good Profits!

Futuristic Indicator v3 - Enhanced Glow & Strength MetersTo ensure candles are display by script go to trading view settings and uncheck default Candle, Body and Wick to prevent them from plotting over your modified candles.

Futuristic Indicator v3 - Enhanced Glow & Strength Meters: Detailed Breakdown

This Modern styled Pine Script indicator is designed to enhance technical analysis by providing a visually striking OLED-style dashboard with multiple market insights. It integrates trend detection, momentum analysis, volatility tracking, and strength meters into a single, streamlined interface for traders.

1️⃣ Customizable Features for Flexibility

The indicator offers multiple user-configurable settings, allowing traders to adjust the display based on their trading strategy and preferences. Users can toggle elements such as strength meters, volatility indicators, trend arrows, moving averages, and buy/sell alerts. Additionally, background and candle colors can be customized for better readability.

🔹 Why is this useful?

Traders can customize their charts to focus on the data they care about.

Reduces chart clutter by allowing users to toggle features on or off.

2️⃣ Trend Detection Using EMAs

This indicator detects market trends using two Exponential Moving Averages (EMA):

A "Fast" EMA (shorter period) for quick trend shifts.

A "Slow" EMA (longer period) to confirm trends.

Comparison of the two EMAs determines if the trend is bullish (uptrend) or bearish (downtrend).

The indicator colors the trend lines accordingly and adds a trend arrow 📈📉 for quick visual cues.

🔹 Why is this useful?

EMA crossovers are widely used to identify trend reversals.

Provides clear visual cues for traders to confirm entry & exit points.

3️⃣ RSI-Based Momentum Analysis

The indicator integrates the Relative Strength Index (RSI) to gauge market momentum. The momentum value changes color dynamically based on whether it's in bullish (>50) or bearish (<50) territory.

🔹 Why is this useful?

RSI helps identify overbought and oversold conditions.

Detects trend strength by measuring the speed of price movements.

4️⃣ Bullish & Bearish Strength Meters

The indicator quantifies bullish and bearish market strength based on RSI and converts it into a percentage-based meter:

Bullish Strength (Long Strength)

Bearish Strength (Short Strength)

Strength meters are displayed using OLED-styled bars, dynamically changing in real-time.

🔹 Why is this useful?

Allows traders to visually gauge market sentiment at a glance.

Helps confirm if a trend has strong momentum or is losing strength.

5️⃣ Market Volatility Indicator (ATR-Based)

The indicator includes a volatility tracker using the Average True Range (ATR):

ATR is scaled up to provide easier readability.

Higher ATR values indicate higher market volatility.

🔹 Why is this useful?

Helps traders identify potential breakout or consolidation phases.

Allows better risk management by understanding price fluctuations.

6️⃣ Trend Strength Calculation

The indicator calculates trend strength based on the difference between the EMAs:

A higher trend strength value suggests a stronger directional trend.

Displayed as a percentage for better clarity.

🔹 Why is this useful?

Helps traders differentiate between strong and weak trends.

Reduces the likelihood of entering weak or choppy markets.

7️⃣ OLED-Style Dashboard for Market Data

A futuristic OLED-styled table is used to display critical market data in a visually appealing way:

Trend direction (Bullish/Bearish with an arrow 📈📉).

Current price.

Momentum value.

Strength meters (Bullish/Bearish).

Trend strength percentage.

Volatility Meter

The dashboard uses high-contrast colors and neon glow effects, making it easier to read against dark backgrounds.

🔹 Why is this useful?

Provides a centralized view of key trading metrics.

Eliminates the need to manually calculate trend strength.

8️⃣ Modern Style Neon Glow Effects

To enhance visibility, the indicator applies glowing effects to:

Moving Averages (EMAs): Highlighted with layered glow effects.

Candlesticks: Borders and wicks dynamically change color based on trend direction.

🔹 Why is this useful?

Improves readability in low-contrast or dark-mode charts.

Helps traders spot trends faster without reading numerical data.

9️⃣ Automated Buy & Sell Alerts

The script triggers alerts when momentum crosses key levels:

Above 55 → Potential Long Setup

Below 45 → Potential Short Setup.

🔹 Why is this useful?

Alerts help traders react quickly without constantly monitoring the chart.

Reduces the risk of missing critical trade opportunities.

🔹 Final Summary: Why is This Indicator Useful?

This futuristic cyberpunk-styled trading tool enhances traditional market analysis by combining technical indicators with high-visibility visuals.

🔹 Key Benefits:

✅ Customizable Display – Toggle elements based on trading needs.

✅ Trend Detection – EMAs highlight uptrends & downtrends.

✅ Momentum Tracking – RSI-based momentum gauge identifies strong moves.

✅ Strength Meters – Bullish/Bearish power is clearly visualized.

✅ Volatility Insights – ATR-based metric highlights market turbulence.

✅ Trend Strength Analysis – Quantifies trend intensity.

✅ Dashboard – Provides a centralized, easy-to-read data panel.

✅ Cyberpunk Neon Glow – Enhances clarity with stylish aesthetics.

✅ Real-Time Alerts – Helps traders react to key opportunities.

This indicator is designed to be both functional and visually appealing, making market analysis more intuitive and efficient. 🚀

Multiple Values TableThis Pine Script indicator, named "Multiple Values Table," provides a comprehensive view of various technical indicators in a tabular format directly on your trading chart. It allows traders to quickly assess multiple metrics without switching between different charts or panels.

Key Features:

Table Position and Size:

Users can choose the position of the table on the chart (e.g., top left, top right).

The size of the table can be adjusted (e.g., tiny, small, normal, large).

Moving Averages:

Calculates the 5-day Exponential Moving Average (5DEMA) using daily data.

Calculates the 5-week and 20-week EMAs (5WEMA and 20WEMA) using weekly data.

Indicates whether the current price is above or below these moving averages in percentage terms.

Drawdown and Williams VIX Fix:

Computes the drawdown from the 365-day high to the current close.

Calculates the Williams VIX Fix (WVF), which measures the volatility of the asset.

Shows both the current WVF and a 2% drawdown level.

Relative Strength Index (RSI):

Displays the current RSI and compares it to the RSI from 14 days ago.

Indicates whether the RSI is increasing, decreasing, or flat.

Stochastic RSI:

Computes the Stochastic RSI and compares it to the value from 14 days ago.

Indicates whether the Stochastic RSI is increasing, decreasing, or flat.

Normalized MACD (NMACD):

Calculates the Normalized MACD values.

Indicates whether the MACD is increasing, decreasing, or flat.

Awesome Oscillator (AO):

Calculates the AO on a daily timeframe.

Indicates whether the AO is increasing, decreasing, or flat.

Volume Analysis:

Displays the average volume over the last 22 days.

Shows the current day's volume as a percentage of the average volume.

Percentile Calculations:

Calculates the current percentile rank of the WVF and ATH over specified periods.

Indicates the percentile rank of the current volume percentage over the past period.

Table Display:

All these values are presented in a neatly formatted table.

The table updates dynamically with the latest data.

Example Use Cases:

Comprehensive Market Analysis: Quickly assess multiple indicators at a glance.

Trend and Momentum Analysis: Identify trends and momentum changes based on various moving averages and oscillators.

Volatility and Drawdown Monitoring: Track volatility and drawdown levels to manage risk effectively.

This script offers a powerful tool for traders who want to have a holistic view of various technical indicators in one place. It provides flexibility in customization and a user-friendly interface to enhance your trading experience.

Trading IQ - Razor IQIntroducing TradingIQ's first dip buying/shorting all-in-one trading system: Razor IQ.

Razor IQ is an exclusive trading algorithm developed by TradingIQ, designed to trade upside/downside price dips of varying significance in trending markets. By integrating artificial intelligence and IQ Technology, Razor IQ analyzes historical and real-time price data to construct a dynamic trading system adaptable to various asset and timeframe combinations.

Philosophy of Razor IQ

Razor IQ operates on a single premise: Trends must retrace, and these retracements offer traders an opportunity to join in the overarching trend. At some point traders will enter against a trend in aggregate and traders in profitable positions entered during the trend will scale out. When occurring simultaneously, a trend will retrace against itself, offering an opportunity for traders not yet in the trend to join in the move and continue the trend.

Razor IQ is designed to work straight out of the box. In fact, its simplicity requires just a few user settings to manage output, making it incredibly straightforward to manage.

Long Limit Order Stop Loss and Minimum ATR TP/SL are the only settings that manage the performance of Razor IQ!

Traders don’t have to spend hours adjusting settings and trying to find what works best - Razor IQ handles this on its own.

Key Features of Razor IQ

Self-Learning Retracement Detection

Employs AI and IQ Technology to identify notable price dips in real-time.

AI-Generated Trading Signals

Provides retracement trading signals derived from self-learning algorithms.

Comprehensive Trading System

Offers clear entry and exit labels.

Performance Tracking

Records and presents trading performance data, easily accessible for user analysis.

Self-Learning Trading Exits

Razor IQ learns where to exit positions.

Long and Short Trading Capabilities

Supports both long and short positions to trade various market conditions.

How It Works

Razor IQ operates on a straightforward heuristic: go long during the retracement of significant upside price moves and go short during the retracement of significant downside price moves.

IQ Technology, TradingIQ's proprietary AI algorithm, defines what constitutes a “trend” and a “retracement” and what’s considered a tradable dip buying/shorting opportunity. For Razor IQ, this algorithm evaluates all historical trends and retracements, how much trends generally retrace and how long trends generally persist. For instance, the "dip" following an uptrend is measured and learned from, including the significance of the identified trend level (how long it has been active, how much price has increased, etc). By analyzing these patterns, Razor IQ adapts to identify and trade similar future retracements and trends.

In simple terms, Razor IQ clusters previous trend and retracement data in an attempt to trade similar price sequences when they repeat in the future. Using this knowledge, it determines the optimal, current price level where joining in the current trend (during a retracement) has a calculated chance of not stopping out before trend continuation.

For long positions, Razor IQ enters using a market order at the AI-identified long entry price point. If price closes beneath this level a market order will be placed and a long position entered. Of course, this is how the algorithm trades, users can elect to use a stop-limit order amongst other order types for position entry. After the position is entered TP1 is placed (identifiable on the price chart). TP1 has a twofold purpose:

Acts as a legitimate profit target to exit 50% of the position.

Once TP1 is achieved, a stop-loss order is immediately placed at breakeven, and a trailing stop loss controls the remainder of the trade. With this, so long as TP1 is achieved, the position will not endure a loss. So long as price continues to uptrend, Razor IQ will remain in the position.

For short positions, Razor IQ provides an AI-identified short entry level. If price closes above this level a market order will be placed and a short position entered. Again, this is how the algorithm trades, users can elect to use a stop-limit order amongst other order types for position entry. Upon entry Razor IQ implements a TP order and SL order (identifiable on the price chart).

Downtrends, in most markets, usually operate differently than uptrends. With uptrends, price usually increases at a modest pace with consistency over an extended period of time. Downtrends behave in an opposite manner - price decreases rapidly for a much shorter duration.

With this observation, the long dip entry heuristic differs slightly from the short dip entry heuristic.

The long dip entry heuristic specializes in identifying larger, long-term uptrends and entering on retracement of the uptrends. With a dedicated trailing stop loss, so long as the uptrend persists, Razor IQ will remain in the position.

The short dip entry heuristic specializes in identifying sharp, significant downside price moves, and entering short on upside volatility during these moves. A fixed stop loss and profit target are implemented for short positions - no trailing stop is used.

As a trading system, Razor IQ exits all TP orders using a limit order, with all stop losses exited as stop market orders.

What Classifies As a Tradable Dip?

For Razor IQ, tradable price dips are not manually set but are instead learned by the system. What qualifies as an exploitable price dip in one market might not hold the same significance in another. Razor IQ continuously analyzes historical and current trends (if one exists), how far price has moved during the trend, the duration of the trend, the raw-dollar price move of price dips during trends, and more, to determine which future price retracements offer a smart chance to join in any current price trend.

The image above illustrates the Razor Line Long Entry point.

The green line represents the Long Retracement Entry Point.

The blue upper line represents the first profit target for the trade.

The blue lower line represents the trailing stop loss start point for the long position.

The position is entered once price closes below the green line.

The green Razor Lazor long entry point will only appear during uptrends.

The image above shows a long position being entered after the Long Razor Lazor was closed beneath.

Green arrows indicate that the strategy entered a long position at the highlighted price level.

Blue arrows indicate that the strategy exited a position, whether at TP1, the initial stop loss, or at the trailing stop.

Blue lines above the entry price indicate the TP1 level for the current long trade. Blue lines below the current price indicate the initial stop loss price.

If price reaches TP1, a stop loss will be immediately placed at breakeven, and the in-built trailing stop will determine the future exit price.

A blue line (similar to the blue line shown for TP1) will trail price and correspond to the trailing stop price of the trade.

If the trailing stop is above the breakeven stop loss, then the trailing stop will be hit before the breakeven stop loss, which means the remainder of the trade will be exited at a profit.

If the breakeven stop loss is above the trailing stop, then the breakeven stop loss will be hit first. In this case, the remainder of the position will be exited at breakeven.

The image above shows the trailing stop price, represented by a blue line, and the breakeven stop loss price, represented by a pink line, used for the long position!

You can also hover over the trade labels to get more information about the trade—such as the entry price and exit price.

The image above exemplifies Razor IQ's output when a downtrend is active.

When a downtrend is active, Razor IQ will switch to "short mode". In short mode, Razor IQ will display a neon red line. This neon red line indicates the Razor Lazor short entry point. When price closes above the red Razor Lazor line a short position is entered.

The image above shows Razor IQ during an active short position.

The image above shows Razor IQ after completing a short trade.

Red arrows indicate that the strategy entered a short position at the highlighted price level.

Blue arrows indicate that the strategy exited a position, whether at the profit target or the fixed stop loss.

Blue lines indicate the profit target level for the current trade when below price. and blue lines above the current price indicate the stop loss level for the short trade.

Short traders do not utilize a trailing stop - only a fixed profit target and fixed stop loss are used.

You can also hover over the trade labels to get more information about the trade—such as the entry price and exit price.

Minimum Profit Target And Stop Loss

The Minimum ATR Profit Target and Minimum ATR Stop Loss setting control the minimum allowed profit target and stop loss distance. On most timeframes users won’t have to alter these settings; however, on very-low timeframes such as the 1-minute chart, users can increase these values so gross profits exceed commission.

After changing either setting, Razor IQ will retrain on historical data - accounting for the newly defined minimum profit target or stop loss.

AI Direction

The AI Direction setting controls the trade direction Razor IQ is allowed to take.

“Trade Longs” allows for long trades.

“Trade Shorts” allows for short trades.

Verifying Razor IQ’s Effectiveness

Razor IQ automatically tracks its performance and displays the profit factor for the long strategy and the short strategy it uses. This information can be found in the table located in the top-right corner of your chart showing.

This table shows the long strategy profit factor and the short strategy profit factor.

The image above shows the long strategy profit factor and the short strategy profit factor for Razor IQ.

A profit factor greater than 1 indicates a strategy profitably traded historical price data.

A profit factor less than 1 indicates a strategy unprofitably traded historical price data.

A profit factor equal to 1 indicates a strategy did not lose or gain money when trading historical price data.

Using Razor IQ

While Razor IQ is a full-fledged trading system with entries and exits - manual traders can certainly make use of its on chart indications and visualizations.

The hallmark feature of Razor IQ is its ability to signal an acceptable dip entry opportunity - for both uptrends and downtrends. Long entries are often signaled near the bottom of a retracement for an uptrend; short entries are often signaled near the top of a retracement for a downtrend.

Razor IQ will always operate on exact price levels; however, users can certainly take advantage of Razor IQ's trend identification mechanism and retracement identification mechanism to use as confluence with their personally crafted trading strategy.

Of course, every trend will reverse at some point, and a good dip buying/shorting strategy will often trade the reversal in expectation of the prior trend continuing (retracement). It's important not to aggressively filter retracement entries in hopes of avoiding an entry when a trend reversal finally occurs, as this will ultimately filter out good dip buying/shorting opportunities. This is a reality of any dip trading strategy - not just Razor IQ.

Of course, you can set alerts for all Razor IQ entry and exit signals, effectively following along its systematic conquest of price movement.

Crodl Position Size CalculatorThe Crodl Size Position Calculator is a powerful and intuitive tool designed for traders to calculate their position size, risk, and reward before entering a trade. This indicator simplifies trade planning by providing clear calculations of key metrics such as risk-to-reward ratio, position size, expected profit, and current PnL (Profit and Loss).

Features:

Dynamic Input Fields: Customize your trade parameters, including risk loss, leverage, entry price, stop loss, and take profit.

Position Size Calculation: Automatically calculate the number of units to trade based on your risk tolerance and leverage.

Risk/Reward Ratio: See the ratio of potential profit to risk for informed decision-making.

Real-Time PnL Tracking: Monitor your current profit or loss directly on the chart.

Expected Profit Projection: Displays the profit potential based on your risk-to-reward ratio.

Position Plotting: Visualize your entry, stop loss, and take profit levels directly on the chart with color-coded lines and zones.

User-Friendly Table: A detailed table provides clear visibility of all trade metrics, including:

Risk Loss

Leverage

Entry Price

Stop Loss

Take Profit

Risk/Reward Ratio

Bet Amount

Crypto Units

Real-Time PnL

Expected Profit

How It Works:

Set Your Parameters: Input your desired risk loss, leverage, entry price, stop loss, and take profit levels in the settings.

Get Instant Results: The indicator calculates position size, PnL, expected profit, and other key metrics.

Visualize on the Chart: See your entry, stop loss, and take profit levels plotted on the chart for clarity.

Review the Trade Table: A table at the bottom-right of the screen summarizes all calculations and updates dynamically as the market price changes.

Who is it for? This indicator is ideal for traders of all experience levels, whether you're a beginner learning risk management or a professional looking for efficient trade planning tools.

Customization Options:

Adjust the size of the plotted position zones.

Enable or disable zone plotting for a cleaner chart.

Tailor inputs to match your trading strategy.

Note: Always use proper risk management and ensure your trading parameters align with your personal trading goals and strategy. Use at Own Risk

Closing Prices for Indices AMMOthe "Closing Prices for Indices" indicator displays the daily closing prices of four major stock indices: FTSE 100, DAX 40, Dow Jones Industrial Average, and NASDAQ Composite. The indicator updates the prices based on their respective market closing times:

FTSE 100 and DAX 40: Updates at 4:30 PM UK time.

Dow Jones and NASDAQ Composite: Updates at 9:00 PM UK time.

Key features:

Customizable Labels: Option to display labels showing the closing prices directly on the chart.

Color-Coded Lines: Plots each index's closing price using distinct, customizable colors for easy differentiation.

User-Friendly Settings: Includes options for customizing line and label colors.

This indicator is perfect for traders and analysts looking to monitor and compare key index closing prices visually on their charts.

Best Buffett Ratio w/ Std-Dev Offset + Conditional PlotSummary:

This script provides a visually clear way to track the so-called “Buffett Ratio,”

a popular market valuation gauge which compares the total US stock market cap

to the country’s GDP. In addition, it plots a “hardcoded” long-term trend line,

along with fixed standard-deviation bands (in log space), and uses background colors

to signal potentially overvalued or undervalued zones.

What Is the Buffett Ratio?

Often credited to Warren Buffett, the Buffett Ratio (or Buffett Indicator) measures:

(Total US Stock Market Capitalization) / (US GDP)

• A higher ratio typically means equities are more expensive relative to the size of the economy.

• A lower ratio suggests equities may be more attractively valued compared to GDP.

Historically, the ratio has tended to drift upward over many decades,

as the US economy and stock markets grow, but it still oscillates around some trend over time.

How to Use

1) Add to Chart:

- In TradingView, simply apply the indicator (it internally fetches CRSPTM1 & GDP data).

2) Tweak Inputs:

- Log Offset for 1σ: Adjust how wide the ±1σ/±2σ bands appear around the trend.

- Anchor Points: Edit startYear , endYear , startRatio , endRatio

if you want a different slope or different “fair value” anchors.

3) Interpretation:

- If the indicator is above +2σ (red line) , it’s historically “very expensive,”

often leading to lower future returns over the long term.

- If it’s below –2σ (green line) , it’s historically “deep undervaluation,”

often pointing to better future returns over time.

- The intermediate zones show degrees of mild over- or undervaluation.

How This Script Works

1) Buffett Ratio Calculation:

- The script requests data from TradingView’s built-in CRSPTM1 index (total US market cap).

- It also requests US GDP data via request.economic("US", "GDP") .

- If GDP data is missing, the ratio becomes na on that bar.

2) Hardcoded Trend Line:

- Rather than a rolling average, the script uses two “anchors” (e.g. 1950 → 0.30 ratio, 2024 → 1.25 ratio)

and solves for a single log-growth rate to produce a steady upward slope.

3) Fixed Standard Deviations in Log Space:

- The script takes the log of the trend line, then applies a fixed offset for ±1σ and ±2σ,

creating proportional bands that do not “expand/contract” from a rolling window.

4) Conditional Plotting:

- The script only begins plotting once the Buffett Ratio actually has data (around 2011).

5) Color-Coded Zones:

- Above +2σ: red background (historically very expensive)

- Between +1σ and +2σ: yellow background (moderately expensive)

- Between –1σ and +1σ: no background color (around normal)

- Between –2σ and –1σ: aqua background (moderately undervalued)

- Below –2σ: green background (historically deep undervaluation)

Final Notes

• Data Limitations: US GDP data and CRSPTM1 only go back so far, so this starts around 2011.

• Long-Term vs. Short-Term: Best viewed on monthly/quarterly charts and interpreted over years.

• Tuning: If you believe structural changes have shifted the ratio’s fair slope,

adjust the code’s anchors or log offsets.

Enjoy, and use responsibly!

Countdown Candle RRS// Countdown Candle RRS Indicator

//

// This indicator displays a countdown timer for the current candle on the chart.

// It shows the remaining time until the current candle closes, providing traders

// with a visual reference for time-based decision making.

//

// Features:

// - Customizable countdown display (size, position, and color)

// - Adapts to different timeframes (daily, hourly, and minute-based)

// - Displays time in appropriate format based on the chart timeframe

// - Daily or higher: XdHH:MM:SS (e.g., 2d05:30:15)

// - Hourly: HH:MM:SS

// - Minute or lower: MM:SS

// - Updates in real-time on the last candle

//

// Usage:

// - Add this indicator to your chart to see the countdown timer

// - Use the input options to customize the appearance and position of the timer

// - The timer will update on each tick, showing the time remaining until the current candle closes

//

// Note: This indicator is particularly useful for traders who need precise timing

// for entry or exit decisions, especially in fast-moving markets or when using

// specific time-based strategies.

//

// Author: reza rashidi

// Version: 1.0

Comprehensive Volume and Metrics with Pre-Market Volume Data

This script is designed for traders who want a detailed view of market activity, including regular market and pre-market volume, dollar volume, relative volume (RVOL), average daily range (ADR), average true range (ATR), relative strength index (RSI), and the QQQ’s percentage change.

The script includes customizable metrics displayed in tables on the chart for easy analysis, with the option to toggle the visibility of each metric.

Key Features:

Volume and Dollar Volume:

Displays the volume of shares traded during the current day (or pre-market, if enabled).

Includes a calculation of dollar volume, representing the total dollar amount of trades (Volume × Close Price).

Relative Volume (RVOL):

Displays RVOL Day, which is the relative volume of the current day compared to the 2-day moving average.

Shows RVOL 90D, indicating relative volume over the past 90 days.

Both RVOL metrics are calculated as percentages and display the percentage change compared to the standard (100%).

Pre-Market Data:

Includes pre-market volume (PVOL) and pre-market dollar volume (P$ VOL) which are displayed only if pre-market data is enabled.

Tracks volume and dollar volume during pre-market hours (4:00 AM to 9:30 AM Eastern Time) for more in-depth analysis.

Optionally, shows pre-market RSI based on volume-weighted close prices.

Average Daily Range (ADR):

Displays the percentage change between the highest and lowest prices over the defined ADR period (default is 20 days).

Average True Range (ATR):

Shows the ATR, a popular volatility indicator, for a given period (default is 14 bars).

RSI (Relative Strength Index):

Displays RSI for the given period (default is 14).

RSI is calculated using pre-market data when available.

QQQ:

Shows the percentage change of the QQQ ETF from the previous day’s close.

The QQQ percentage change is color-coded: green for positive, red for negative, and gray for no change.

Customizable Inputs:

Visibility Options: Toggle the visibility of each metric, such as volume, dollar volume, RVOL, ADR, ATR, RSI, and QQQ.

Pre-Market Data: Enable or disable the display of pre-market data for volume and dollar volume.

Table Positioning: Adjust the position of tables displaying the metrics either at the bottom-left or bottom-right of the chart.

Text Color and Table Background: Choose between white or black text for the tables and customize the background color.

Tables:

The script utilizes tables to display multiple metrics in an organized and easy-to-read format.

The values are updated dynamically, reflecting real-time data as the market moves.

Pre-Market Data:

The script calculates pre-market volume and dollar volume, along with other key metrics like RSI and RVOL, to help assess market sentiment before the market officially opens.

The pre-market data is accumulated from 4:00 AM to 9:30 AM ET, allowing for pre-market analysis and comparison to regular market hours.

User-Friendly and Flexible:

This script is designed to be highly customizable, giving you the ability to toggle which metrics to display and where they appear on the chart. You can easily focus on the data that matters most to your trading strategy.

DCA Simulation for CryptoCommunity v1.1Overview

This script provides a detailed simulation of a Dollar-Cost Averaging (DCA) strategy tailored for crypto traders. It allows users to visualize how their DCA strategy would perform historically under specific parameters. The script is designed to help traders understand the mechanics of DCA and how it influences average price movement, budget utilization, and trade outcomes.

Key Features:

Combines Interval and Safety Order DCA:

Interval DCA: Regular purchases based on predefined time intervals.

Safety Order DCA: Additional buys triggered by percentage price drops.

Interactive Visualization:

Displays buy levels, average price, and profit-taking points on the chart.

Allows traders to assess how their strategy adapts to price movements.

Comprehensive Dashboard:

Tracks money spent, contracts acquired, and budget utilization.

Shows maximum amounts used if profit-taking is active.

Dynamic Safety Orders:

Resets safety orders when a new higher high is established.

Customizable Parameters:

Adjustable buy frequency, safety order settings, and profit-taking levels.

Suitable for traders with varying budgets and risk tolerances.

Default Strategy Settings:

Account Size: Default account size is set to $10,000 to represent a realistic budget for the average trader.

Commission & Slippage: Includes realistic trading fees and slippage assumptions to ensure accurate backtesting results.

Risk Management: Defaults to risking no more than 5% of the account balance per trade.

Sample Size: Optimized to generate a minimum of 100 trades for meaningful statistical analysis. Users can adjust parameters to fit longer timeframes or different datasets.

Usage Instructions:

Configure Your Strategy: Set the base order, safety order size, and buy frequency based on your preferred DCA approach.

Analyze Historical Performance: Use the chart and dashboard to understand how the strategy performs under different market conditions.

Optimize Parameters: Adjust settings to align with your risk tolerance and trading objectives.

Important Notes:

This script is for educational and simulation purposes. It is not intended to provide financial advice or guarantee profitability.

If the strategy's default settings do not meet your needs, feel free to adjust them while keeping risk management in mind.

TradingView limits the number of open trades to 999, so reduce the buy frequency if necessary to fit longer timeframes.

Price Move DetectorThe Price Move Detector is a powerful technical analysis tool that automatically detects and highlights significant price movements over a user-defined time frame. This indicator allows traders to quickly identify instances where an asset has experienced a large price change, making it easier to spot potential trading opportunities.

Key Features

Customizable Parameters: Adjust the percentage change and time period (bars or sessions) to define what qualifies as a "significant" price move.

Automatic Highlighting: The indicator overlays a background highlight on the chart whenever the price moves by the specified percentage within the chosen time period.

Flexible Time Frame: Use this indicator across various timeframes and adjust the settings to suit your trading strategy, such as detecting 100% price moves over 20 sessions.

Ideal for Historical Analysis: Perfect for backtesting and screening for past price surges, helping traders spot explosive price action and market trends.

Use Cases

Spot Potential Breakouts: Use the detector to identify stocks or assets that have made significant moves, potentially signaling the start of a breakout or new trend.

Quickly Identify Major Market Moves: Scan historical data to pinpoint times when an asset experienced substantial price changes, providing insight into past performance and future potential.

How to Use

Customize the Settings

Percentage Threshold: Set the minimum percentage increase (e.g., 50%, 100%) that qualifies as a significant move. You can experiment with different percentages to suit your analysis.

Time Period (Bars): Define the lookback period (in bars/sessions) over which the price move should be measured. For example, set it to 20 bars for a one-month time frame on a daily chart.

Analyze the Highlights

Whenever the price increases by the defined percentage over the set period, the indicator will highlight that section of the chart with a background color.

The highlighted sections will make it easy to identify historical periods of large price movements, which can be useful for spotting trends, potential breakouts, or other market behaviors.

Adjust the Parameters for Your Strategy

You can fine-tune the settings to detect smaller or larger price moves depending on your trading goals.

The indicator is flexible enough for use on different timeframes and assets, providing valuable insights across various markets.

Codi's Perp-Spot Basis# Perp-Spot Basis Indicator

This indicator calculates the percentage basis between perpetual futures and spot prices for crypto assets. It is inspired by the original concept from **Krugermacro**, with the added improvement of **automatic detection of the asset pairs** based on the current chart symbol. This enhancement makes it faster and easier to apply across different assets without manual configuration.

## How It Works

The indicator compares the perpetual futures price (e.g., `BTCUSDT.P`) to the spot price (e.g., `BTCUSDT`) on Binance. The difference is expressed as a percentage: (Perp - Spot) / Spot * 100

The results are displayed in a color-coded graph:

- **Blue (Positive Basis):** Perpetual futures are trading at a premium, indicating **bullish sentiment** among derivatives traders.

- **Red (Negative Basis):** Perpetual futures are trading at a discount, indicating **bearish sentiment** among derivatives traders.

This percentage basis is a core component in understanding funding rates and derivatives market dynamics. It serves as a faster proxy for funding rates, which typically lag behind real-time price movements.

---

## How to Use It

### General Concept

- **Red (Negative Basis):** Ideal to execute **longs** when derivatives traders are overly bearish.

- **Blue (Positive Basis):** Ideal to execute **shorts** when derivatives traders are overly bullish.

### Pullback Sniping

1. During an **uptrend**:

- If the basis turns **red** temporarily, it can signal an opportunity to **buy the dip**.

2. During a **downtrend**:

- If the basis turns **blue** temporarily, it can signal an opportunity to **sell the rip**.

3. Wait for the basis to **pop back** (higher in uptrend, lower in downtrend) to time entries more effectively—this often coincides with **stop runs** or **liquidations**.

### Intraday Execution

- **When price is falling**:

- If the basis is **red**, the move is derivatives-led (**normal**).

- If the basis is **blue**, spot traders are leading, and perps are offside—wait for **price dumps** before longing.

- **When price is rising**:

- If the basis is **blue**, the move is derivatives-led (**normal**).

- If the basis is **red**, spot traders are leading, and perps are offside—wait for **price pops** before shorting.

### Larger Time Frames

- **Consistently Blue Basis:** Indicates a **bull market** as derivatives traders are bullish over the long term.

- **Consistently Red Basis:** Indicates a **bear market** as derivatives traders are bearish over the long term.

---

## Improvements Over the Original

This version of the Perp-Spot Basis indicator **automatically detects the Binance perpetual futures and spot pairs** based on the current chart symbol. For example:

- If you are viewing `ETHUSDT`, it automatically references `ETHUSDT.P` for the perpetual futures pair and `ETHUSDT` for the spot pair in BINANCE.