Luma DCA Simulator (BTC only)Luma DCA Simulator – Guide

What is the Luma DCA Simulator?

The Luma DCA Tracker shows how regular Bitcoin investments (Dollar Cost Averaging) would have developed over a freely selectable period – directly in the chart, transparent and easy to follow.

Settings Overview

1. Investment amount per interval

Specifies how much capital is invested at each purchase (e.g. 100).

2. Start date

Defines the point in time from which the simulation begins – e.g. 01.01.2020.

3. Investment interval

Determines how frequently investments are made:

– Daily

– Weekly

– Every 14 days

– Monthly

4. Language

Switches the info box display between English and German.

5. Show investment data (optional)

If activated, the chart will display additional values such as total invested capital, BTC amount, current value, and profit/loss.

What the Chart Displays

Entry points: Each DCA purchase is marked as a point in the price chart.

Average entry price: An orange line visualizes the evolving DCA average.

Info box (bottom left) with a live summary of:

– Total invested capital

– Total BTC acquired

– Average entry price

– Current portfolio value

– Profit/loss in absolute terms and percentage

Note on Accuracy

This simulation is for illustrative purposes only.

Spreads, slippage, fees, and tax effects are not included.

Actual results may vary.

Technical Note

For daily or weekly intervals, the chart timeframe should be set to 1 day or lower to ensure all purchases are accurately included.

Larger timeframes (e.g. weekly or monthly charts) may result in missed investments.

Currency Handling

All calculations are based on the selected chart symbol (e.g. BTCUSD, BTCEUR, BTCUSDT).

The displayed currency is automatically determined by the chart used.

Statistics

Adaptive Multi-MA OptimizerAdaptive Multi-MA Optimizer

This indicator provides a powerful, customizable solution for traders seeking dynamically optimized moving averages with precision and control. It integrates multiple custom-built moving average types, applies real-time volatility-based optimization, and includes an optional composite smoothing engine.

🧠 Key Features

Dynamic Optimization:

Automatically selects the optimal lookback length based on market volatility stability using a custom standard deviation differential model.

Multiple Custom MA Types:

Includes fully custom implementations of:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

VWMA (Volume Weighted MA)

DEMA (Double EMA)

TEMA (Triple EMA)

Hull MA

ALMA (Arnaud Legoux MA)

Composite MA Option:

A unique "Composite" mode blends all supported MAs into a single average, then applies optional smoothing for enhanced signal clarity.

Dynamic Smoothing:

The composite mode supports volatility-adjusted smoothing (based on optimized lookback), making it adaptable to different market regimes.

Fully Custom Logic:

No built-in MA functions are used — every moving average is hand-coded for transparency and educational value.

⚙️ How It Works

Optimization:

The script evaluates a range of lengths (minLen to maxLen) using the standard deviation of price returns. It selects the length with the most stable recent volatility profile.

Calculation:

The selected MA type is calculated using that optimized length. If "Composite" is chosen, all MA types are averaged and smoothed dynamically.

Visualization:

The adaptive MA is plotted on the chart, changing color based on its position relative to price.

📌 Use Cases

Trend-following strategies that adapt to different market conditions.

Traders wanting a high-fidelity composite of multiple MAs.

Analysts interested in visualizing market smoothness without lag-heavy signals.

Coders looking to learn how to build custom indicators from scratch.

🧪 Inputs

MA Type: Choose from 8 MA types or a blended Composite.

Lookback Range: Control min/max and step size for optimization.

Source: Choose any price series (e.g., close, hl2).

⚠️ Disclaimer

This indicator is for educational and informational purposes only and does not constitute financial advice, trading advice, or investment recommendations. Use of this script is at your own risk. Past performance does not guarantee future results. Always perform your own analysis and consult with a qualified financial advisor before making trading decisions.

Adaptive Normalized Global Liquidity OscillatorAdaptive Normalized Global Liquidity Oscillator

A dynamic, non-repainting oscillator built on real central bank balance sheet data. This tool visualizes global liquidity shifts by aggregating monetary asset flows from the world’s most influential central banks.

🔍 What This Script Does:

Aggregates Global Liquidity:

Includes Federal Reserve (FED) assets and subtracts liabilities like the Treasury General Account (TGA) and Reverse Repo Facility (RRP), combined with asset positions from the ECB, BOJ, PBC, BOE, and over 10 other central banks. All data is normalized into USD using FX rates.

Adaptive Normalization:

Optimizes the lookback period dynamically based on rate-of-change stability—no fixed lengths, enabling adaptation across macro conditions.

Self-Optimizing Weighting:

Applies inverse standard deviation to balance raw liquidity, smoothed momentum (HMA), and standardized deviation from the mean.

Percentile-Ranked Highlights:

Liquidity readings are ranked relative to history—extremes are visually emphasized using gradient color and adaptive transparency.

Non-Repainting Design:

Data is anchored with bar index awareness and offset techniques, ensuring no forward-looking bias. What you see is what was known at that time.

⚠️ Important Interpretation Note:

This is not a zero-centered oscillator like RSI or MACD. The signal line does not represent neutrality at zero.

Instead, a dynamic baseline is calculated using a rolling mean of scaled liquidity.

0 is irrelevant on its own—true directional signals come from crosses above or below this adaptive baseline.

Even negative values may signal strength if they are rising above the moving average of past liquidity conditions.

✅ What to Watch For:

Crossover Above Dynamic Baseline:

Indicates liquidity is expanding relative to recent conditions—supports a risk-on interpretation.

Crossover Below Dynamic Baseline:

Suggests deteriorating liquidity conditions—may align with risk-off shifts.

Percentile Extremes:

Readings near the top or bottom historical percentiles can act as contrarian or confirmation signals, depending on momentum.

⚙️ How It Works:

Bounded Normalization:

The final oscillator is passed through a tanh function, keeping values within and reducing distortion.

Adaptive Transparency:

The strength of deviations dynamically adjusts plot intensity—visually highlighting stronger liquidity shifts.

Fully Customizable:

Toggle which banks are included, adjust dynamic optimization ranges, and control visual display options for plot and background layers.

🧠 How to Use:

Trend Confirmation:

Sustained rises in the oscillator above baseline suggest underlying monetary support for asset prices.

Macro Turning Points:

Reversals or divergences, especially near OB/OS zones, can foreshadow broader risk regime changes.

Visual Context:

Use the dynamic baseline to see if liquidity is supportive or suppressive relative to its own adaptive history.

📌 Disclaimer:

This indicator is for educational and informational purposes only. It does not constitute financial advice. Past performance is not indicative of future results. Always consult a qualified financial advisor before making trading or investment decisions.

Luma DCA Tracker (BTC)Luma DCA Tracker (BTC) – User Guide

Function

This indicator simulates a regular Bitcoin investment strategy (Dollar Cost Averaging). It calculates and visualizes:

Accumulated BTC amount

Average entry price

Total amount invested

Current portfolio value

Profit/loss in absolute and percentage terms

Settings

Investment per interval

Fixed amount to be invested at each interval (e.g., 100 USD)

Start date

The date when DCA simulation begins

Investment interval

Choose between:

daily, weekly, every 14 days, or monthly

Show investment data

Displays additional chart lines (total invested, value, profit, etc.)

Chart Elements

Orange line: Average DCA entry price

Grey dots: Entry points based on selected interval

Info box (bottom left): Live summary of all key values

Notes

Purchases are simulated at the closing price of each interval

No fees, slippage, or taxes are included

The indicator is a simulation only and not linked to an actual portfolio

GCM Price Based ColorIndicator Name:

GCM Price Based Color Indicator

Detailed Description:

The GCM Price Based Color Indicator is a unique tool designed to help traders spot potential "pump" events in the market. Unlike traditional Volume Rate of Change (VROC) indicators, this script is conditional: it calculates a VROC value only when both the average volume and the price are increasing. This focus helps filter out volume surges that don't accompany immediate price appreciation, highlighting more relevant "pump" signals.

Key Features & Calculation Logic:

Conditional Volume Rate of Change (VROC):

It first calculates a Simple Moving Average (SMA) of the volume over a user-defined length (lookback period).

It then checks two conditions:

Is the current SMA volume greater than the previous bar's SMA volume (i.e., volumeIncreasing)?

Is the current close price greater than the previous bar's close price (i.e., valueIncreasing)?

Only if both volume Increasing AND value Increasing are true, a VROC value is calculated as (current _ MA _ volume - previous _ MA _ volume) * (100 / previous _ MA _ volume). Otherwise, the VROC for that bar is 0.

Historical Normalization:

The raw VROC value is then normalized against its own historical maximum value observed since the indicator was applied. This scaling brings all VROC values into a common 0-100 range.

Why is this important? Normalization makes the indicator's readings comparable across different assets (e.g., high-volume vs. low-volume stocks/cryptos) and different timeframes, making it easier to interpret the strength of a "pump" relative to its own past.

Dynamic Plot Color (Price-Based):

The plot line's color itself provides an immediate visual cue about the current bar's price action:

Green: close is greater than close (price is up for the current bar).

Red: close is less than close (price is down for the current bar).

Grey: close is equal to close (price is flat for the current bar).

Important Note: The plot color reflects the price movement of the current bar, not the magnitude of the VROC Normalized value itself. This means you can have a high vrocNormalized value (indicating a strong conditional volume surge) but a red plot color if the very next bar's price closes lower, providing a multi-faceted view.

Thresholds & Alerts:

Two horizontal lines (small Pump Threshold and big Pump Threshold) are plotted to visually mark significant levels of normalized pump strength.

Customizable alerts can be set up to notify you when VROC Normalized reaches or exceeds these thresholds, helping you catch potential pump events in real-time.

How to Use It:

Identify Potential Pumps: Look for upward spikes in the VROC Normalized line. Higher spikes indicate stronger pump signals (i.e., a larger increase in average volume coinciding with an increasing price).

Monitor Thresholds: Pay attention when the VROC Normalized line crosses above your small Pump Threshold or big Pump Threshold. These are configurable levels to suit different assets and trading styles.

Observe Plot Color: The line color provides crucial context. A high VROC Normalized (strong pump signal) with a green line indicates current price momentum is still positive. If VROC Normalized is high but the line turns red, it might suggest the initial pump is losing steam or experiencing a pullback.

Combine with Other Tools: This indicator is best used in conjunction with other technical analysis tools (e.g., support/resistance, trend lines, other momentum indicators) for confirmation and a more holistic trading strategy.

Indicator Inputs:

Lookback period (1 - 4999) (default: 420): This length determines the period for the Simple Moving Average (SMA) of volume. A higher value will smooth the volume average more, reacting slower, while a lower value will make it more reactive. Adjust based on the timeframe and asset volatility.

Big Pump Threshold (0.01 - 99.99) (default: 10.0): The normalized VROC Normalized level that signifies a "Big Pump." When VROC Normalized reaches or exceeds this level, an alert can be triggered.

Small Pump Threshold (0.01 - 99.99) (default: 0.5): The normalized VROC Normalized level that signifies a "Small Pump." This is a lower threshold for earlier or less significant pump activity.

Alerts:

Small Pump: Triggers when VROC Normalized crosses above or equals the small Pump Threshold.

Big Pump: Triggers when VROC Normalized crosses above or equals the big Pump Threshold.

Best Practices & Considerations:

Timeframes: The indicator can be used on various timeframes, but its effectiveness may vary. Experiment to find what works best for your chosen asset and trading style.

Volatility: Highly volatile assets might require different threshold settings compared to less volatile ones.

Lag: Due to the use of a Simple Moving Average (SMA) for volume, there will be some inherent lag in the calculation.

Normalization Start: The historic Max for normalization starts with a default value of 10.0. For the very first bars, or if there hasn't been a significant VROC yet, the VROC Normalized might behave differently until a true historical maximum VROC establishes itself.

Not Financial Advice: This indicator is a tool for analysis and does not constitute financial advice. Always perform your own research and manage your risk.

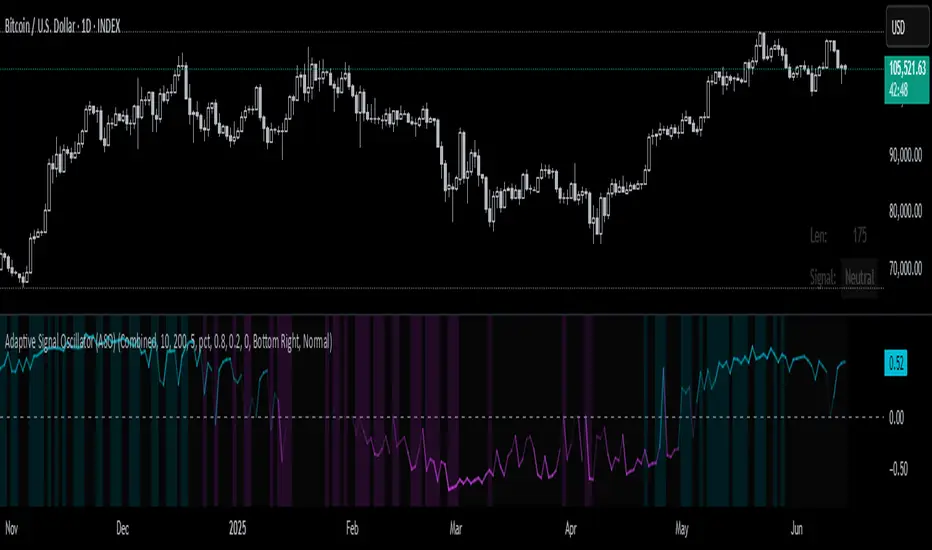

Adaptive Signal Oscillator (ASO)📘 Adaptive Signal Oscillator (ASO)

A fully dynamic, self-calibrating oscillator that adapts to any asset or timeframe by optimizing for real-time signal stability and volatility structure — without relying on static parameters or hardcoded thresholds.

🔍 Overview

The Adaptive Signal Oscillator (ASO) is a next-generation technical analysis tool designed to provide context-aware long/short signals across crypto, equities, or forex markets. Unlike traditional oscillators (RSI, Stochastics, MACD), ASO requires no manual tuning of lookback periods or overbought/oversold zones — it self-optimizes based on current market behavior.

🧠 How It Works

✅ 1. Dynamic Lookback Optimization

ASO evaluates a range of lookback lengths between user-defined minLen and maxLen. For each length, it calculates the standard deviation of returns and finds the one with the least volatility change (i.e., the most stable structure). This length is dynamically assigned as bestLen, recalculated on every bar.

✅ 2. Multi-Layer Signal Composition

Four independent signal layers are computed using bestLen:

RSI Layer: Measures relative price strength via a custom dynamic RSI.

Z-Score Layer: Standardized deviation of price from its mean.

Volatility Layer: Standard deviation of log or percent returns.

Price Position Layer: Current price percentile within the lookback window.

Each of these layers is transformed into a percentile score scaled to the range .

✅ 3. Volatility-Based Weighting

The standard deviation (volatility) of each signal layer is computed. Less volatile layers are weighted more heavily, ensuring the final composite signal prioritizes stable, consistent inputs.

Weights are normalized and combined to form a composite score, representing a dynamically blended, noise-weighted signal across the four layers.

✅ 4. Optional Adaptive Smoothing

A boolean toggle lets users apply smoothing to the final score. The smoothing window scales proportionally to bestLen, preserving adaptiveness even during trend transitions.

✅ 5. Percentile-Based Thresholding

Rather than using arbitrary fixed thresholds, ASO converts the composite score into a ranked percentile. Long/short signals are then generated based on user-defined percentile bands, adapting naturally to each asset’s behavior.

📈 Interpreting ASO

Score > Threshold → Strong long signal (highlighted in aqua).

Score < Threshold → Strong short signal (highlighted in fuchsia).

Crossing h_thresh (e.g., 0) → Neutral-to-bias change; useful for early trend cues.

The background and label update in real time to reflect the current regime and bestLen.

⚙️ Inputs

minLen, maxLen, step: Define the search range for optimal lookback length.

retMethod: Choose between log or percent return calculations.

threshHigh, threshLow: Define signal zones using percentiles.

smooth: Enable dynamic score smoothing.

h_thresh: Midline crossover zone for directional context.

⚠️ Disclaimer

This tool is designed for exploratory and educational purposes only. It does not offer financial advice or trading recommendations. Past performance is not indicative of future results.

Always consult a licensed financial advisor before making investment decisions.

Flux Capacitor (FC)# Flux Capacitor

**A volume-weighted, outlier-resistant momentum oscillator designed to expose hidden directional pressure from institutional participants.**

---

### Why "Flux Capacitor"?

The name pays homage to the fictional energy core in *Back to the Future* — an invisible engine that powers movement. Similarly, this indicator detects whether price movement is being powered by real market participation (volume) or if it's coasting without conviction.

---

### Methodology

The Flux Capacitor fuses three statistical layers:

- **Normalized Momentum**: `(Close – Open) / ATR`

Controls for raw price size and volatility.

- **Volume Scaling**:

Amplifies the effect of price moves that occur with elevated volume.

- **Robust Normalization**:

- *Winsorization* caps outlier spikes.

- *MAD-Z scoring* normalizes the signal across assets (crypto, futures, stocks).

- This produces consistent scaling across timeframes and symbols.

The result is a smooth oscillator that reliably indicates **liquidity-backed momentum** — not just price movement.

---

### Signal Events

- **Divergence (D)**: Price makes higher highs or lower lows, but Flux does not.

- **Absorption (A)**: Candle shows high volume and small body, while Flux opposes the candle direction — indicates smart money stepping in.

- **Compression (◆)**: High volume with low momentum — potential breakout zone.

- **Zero-Cross**: Indicates directional regime flip.

- **Flux Acceleration**: Histogram shows pressure rate of change.

- **Regime Background**: Color fades with weakening trend conviction.

All signals are color-coded and visually compact for easy pattern recognition.

---

### Interpreting Divergence & Absorption Correctly

Signal strength improves significantly when it appears **in the correct zone**:

#### Divergence:

| Signal | Zone | Meaning | Strength |

|--------|------------|------------------------------------------|--------------|

| Green D | Below 0 | Bullish reversal forming in weakness | **Strong** |

| Green D | Above 0 | Bullish, but less convincing | Moderate |

| Red D | Above 0 | Bearish reversal forming in strength | **Strong** |

| Red D | Below 0 | Bearish continuation — low warning value | Weak |

#### Absorption:

| Signal | Zone | Meaning | Strength |

|--------|------------|-----------------------------------------|--------------|

| Green A | Below 0 | Buyers absorbing panic-selling | **Strong** |

| Green A | Above 0 | Support continuation | Moderate |

| Red A | Above 0 | Sellers absorbing FOMO buying | **Strong** |

| Red A | Below 0 | Trend continuation — not actionable | Weak |

Look for **absorption or divergence signals in “enemy territory”** for the most actionable entries.

---

### Reducing Visual Footprint

If your chart shows a long line of numbers across the top of the Flux Capacitor pane (e.g. "FC 14 20 9 ... Bottom Right"), it’s due to TradingView’s *status line input display*.

**To fix this**:

Right-click the indicator pane → **Settings** → **Status Line** tab → uncheck “Show Indicator Arguments”.

This frees up vertical space so top-edge signals (like red `D` or yellow `◆`) remain visible and unobstructed.

---

### Features

- Original MAD-Z based momentum design

- True volume-based divergence and absorption logic

- Built-in alerts for all signal types

- Works across timeframes (1-min to weekly)

- Minimalist, responsive layout

- 25+ customizable parameters

- No future leaks, no repainting

---

### Usage Scenarios

- **Trend confirmation**: Flux > 0 confirms bullish trend strength

- **Reversal detection**: Divergence or absorption in opposite territory = high-probability reversal

- **Breakout anticipation**: Compression signal inside range often precedes directional move

- **Momentum shifts**: Watch for zero-crosses + flux acceleration spikes

---

### ⚠ Visual Note for BTC, ETH, Crude Oil & Futures

These high-priced or rapidly accelerating instruments can visually compress any linear oscillator. You may notice the Flux Capacitor’s line appears "flat" or muted on these assets — especially over long lookbacks.

> **This does not affect signal validity.** Divergence, absorption, and compression triggers still fire based on underlying logic — only the line’s amplitude appears reduced due to scaling constraints.

---

### Disclaimer

This indicator is for educational purposes only. It is not trading advice. Past results do not guarantee future performance. Use in combination with your own risk management and analysis.

Multi-Period Performance TableHello friends,

I'm returning to the fascinating world of TradingView publications. Over time, I've accumulated many unpublished ideas — both open- and closed-source — that I now plan to share, alternating between the two. It felt like a shame to let so much valuable work remain unseen. The story isn't over yet — so today, we kick off a new series of invite-only scripts, starting with this indicator.

🛠️ How It Works

The script analyzes your selected number of years of price data, calculating returns for each month, quarter, and season

Advanced algorithms compute comprehensive statistics, including the mean, median, standard deviation, and extremes for each period

Data is presented in an intuitive table with optional heatmap coloring that makes patterns immediately stand out

Sorting of any column allows you to quickly identify the best and worst performing periods

🔥 Key Features

Pine Script V6 – leverages the latest version for better performance

Custom number of years to aggregate statistics

Complete breakdown for all 12 months (Jan-Dec)

Quarter (Q1, Q2, Q3, Q4) statistics

Season (Winter, Spring, Summer, Fall) statistics

Year/Year-to-Date (YTD) statistics

Enable/disable Right-side statistics for each row

Enable/disable Bottom statistics for each column

Heatmap mode with 10 palettes

Sortable columns

Customizable table

Optimized performance - efficient calculations for smooth operation

Universal compatibility – runs smoothly across all assets, timeframes, and market conditions — from euphoric peaks to capitulation lows

📸 Visual Examples

Monthly view

Quarterly view

Seasonal view

Clean table mode - without heatmaps

Default heatmap palette

June column sorted in descending order to quickly identify best/worst years

Turbo palette - high contrast

Spectral palette - professional look

Red/Yellow/Blue palette - classic style

My similar indicators that are also worth paying attention to

Still here? Unlock the full potential of multi-period market analysis — and take your trading to the next level today! 🚀

👋Good luck!

Normalized Volume & True RangeThis indicator solves a fundamental challenge that traders face when trying to analyze volume and volatility together on their charts. Traditionally, volume and price volatility exist on completely different scales, making direct comparison nearly impossible. Volume might range from thousands to millions of shares, while volatility percentages typically stay within single digits. This indicator brings both measurements onto a unified scale from 0 to 100 percent, allowing you to see their relationship clearly for the first time.

The core innovation lies in the normalization process, which automatically calculates appropriate scaling factors for both volume and volatility based on their historical statistical properties. Rather than using arbitrary fixed scales that might work for one stock but fail for another, this system adapts to each instrument's unique characteristics. The indicator establishes baseline averages for both measurements and then uses statistical analysis to determine reasonable maximum values, ensuring that extreme outliers don't distort the overall picture.

You can choose from three different volatility calculation methods depending on your analytical preferences. The "Body" option measures the distance between opening and closing prices, focusing on the actual trading range that matters most for price action. The "High/Low" method captures the full daily range including wicks and shadows, giving you a complete picture of intraday volatility. The "Close/Close" approach compares consecutive closing prices, which can be particularly useful for identifying gaps and overnight price movements.

The indicator displays volume as colored columns that match your candlestick colors, making it intuitive to see whether high volume occurred during up moves or down moves. Volatility appears as a gray histogram, providing a clean background reference that doesn't interfere with volume interpretation. Both measurements are clipped at 100 percent, which represents their calculated maximum normal values, so any readings near this level indicate unusually high activity in either volume or volatility.

The baseline reference line shows you what "normal" volume looks like for the current instrument, helping you quickly identify when trading activity is above or below average. Optional moving averages for both volume and volatility are available if you prefer smoothed trend analysis over raw daily values. The entire system updates in real-time as new data arrives, continuously refining its statistical calculations to maintain accuracy as market conditions evolve.

This two-in-one indicator provides a straightforward way to examine how price movements relate to trading volume by presenting both measurements on the same normalized scale, making it easier to spot patterns and relationships that might otherwise remain hidden when analyzing these metrics separately.

Outside Bar Strategy with Multiple Entry ModelsOutside Bar Strategy with Multiple Entry Models

This Pine Script strategy implements a versatile trading system based on the Outside Bar pattern, offering three distinct entry models: Close Entry, High/Low Entry, and Midpoint Entry. Designed for traders seeking flexibility, the strategy includes customizable risk/reward ratios, an optional EMA trend filter, and enhanced visualization with line fills.

Key Features:

Entry Models:

Close Entry: Enters a long position when the current candle closes above the high of the previous outside bullish bar . For short, it enters when the candle closes below the low of the previous outside bearish bar.

High/Low Entry: Enters a long position when the price crosses above the high of the previous outside bullish bar . For short, it enters when the price crosses below the low of the previous outside bearish bar .

Midpoint Entry: Places a limit order at the midpoint of the previous outside bar, entering when the price reaches this level.

EMA Trend Filter: Optionally filters signals based on the alignment of EMAs (7 > 25 > 99 > 200 for long, 7 < 25 < 99 < 200 for short). Can be toggled via the Use EMA Filter input.

Risk/Reward Management: Configurable risk/reward ratio (default 2.0) with stop-loss set at the low/high of the outside bar and take-profit calculated based on the bar's range multiplied by the ratio.

Visualization:

Lines for entry, stop-loss, and take-profit levels (dashed for active trades, solid for pending Midpoint Entry orders).

Line fills: Red between entry and stop-loss, green between entry and take-profit.

Previous lines and fills persist on the chart for historical reference (line deletion disabled).

Pending limit orders for Midpoint Entry extend dynamically to the right until triggered or canceled.

Information Table: Displays real-time trade details (entry model, RR ratio, open trade status, entry/stop/take-profit levels, profit/loss percentage) and strategy statistics (success rate, total trades). For Midpoint Entry, pending order details are shown.

Inputs:

Entry Model: Choose between Close Entry, High/Low Entry, or Midpoint Entry (default: Close Entry).

Risk/Reward Ratio: Set the RR ratio (default: 2.0, step: 0.5).

Use EMA Filter: Enable/disable the EMA trend filter (default: true).

Line Colors and Style: Customize colors for entry, stop-loss, and take-profit lines, and select line style (solid or dashed).

Table Settings: Adjust table text color, size (small/normal/large), and position (right top/middle/bottom).

Disclaimer: This strategy is for educational purposes only. Backtest thoroughly and use at your own risk. Past performance is not indicative of future results.

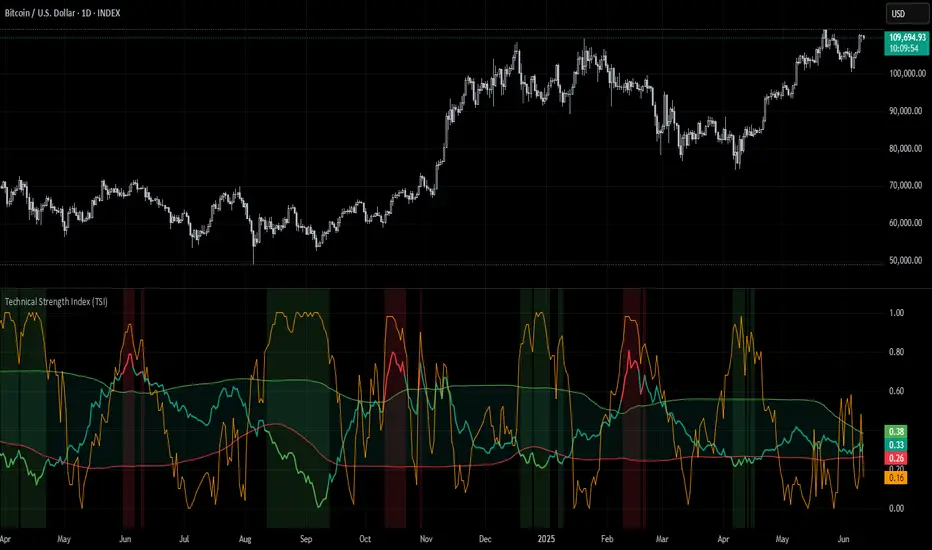

Technical Strength Index (TSI)📘 TSI with Dynamic Bands – Technical Strength Index

The TSI with Dynamic Bands is a multi-factor indicator designed to measure the statistical strength and structure of a trend. It combines several quantitative metrics into a single, normalized score between 0 and 1, allowing traders to assess the technical quality of market moves and detect overbought/oversold conditions with adaptive precision.

🧠 Core Components

This indicator draws from the StatMetrics library, blending:

📈 Trend Persistence: via the Hurst exponent, indicating whether price action is mean-reverting or trending.

📉 Risk-Adjusted Volatility: via the inverted , rewarding smoother, less erratic price movement.

🚀 Momentum Strength: using a combination of directional momentum and Z-score–normalized returns.

These components are normalized and averaged into the TSI line.

🎯 Features

TSI Line: Composite score of trend quality (0 = weak/noise, 1 = strong/structured).

Dynamic Bands: Mean ± 1 standard deviation envelopes provide adaptive context.

Overbought/Oversold Detection: Based on a rolling quantile (e.g. 90th/10th percentile of TSI history).

Signal Strength Bar (optional): Measures how statistically extreme the current TSI value is, helping validate confidence in trade setups.

Dynamic Color Cues: Background and bar gradients help visually identify statistically significant zones.

📈 How to Use

Look for overbought (red background) or oversold (green background) conditions as potential reversal zones.

Confirm trend strength with the optional signal strength bar — stronger values suggest higher signal confidence.

Use the TSI line and context bands to filter out noisy ranges and focus on structured price moves.

⚙️ Inputs

Lookback Period: Controls the smoothing and window size for statistical calculations.

Overbought/Oversold Quantiles: Adjust the thresholds for signal zones.

Plot Signal Strength: Enable or disable the signal confidence bar.

Overlay Signal Strength: Show signal strength in the same panel (compact) or not (cleaner TSI-only view).

🛠 Example Use Cases

Mean reversion traders identifying reversal zones with statistical backing

Momentum/Trend traders confirming structure before entries

Quantitative dashboards or multi-asset screening tools

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any financial instrument.

This AI is not a financial advisor; please consult your financial advisor for personalized advice.

[GetSparx] Lacuna Pro⚡ Lacuna Pro – Institutional Liquidity Framework

This indicator is a premium Smart Money Concepts (SMC) trading toolkit designed to help traders identify high-probability entry and exit zones by visualizing real-time market inefficiencies. It combines Fair Value Gaps (FVGs), Break of Structure (BOS), Change of Character (CHoCH), and Supply & Demand Zones into a unified, configurable framework.

Unlike many public indicators that simply "overlay concepts", this indicator implements strict internal validation to filter out noise and provide only institutional-grade levels — making it a valuable execution layer for SMC-based strategies.

🧠 What the Script Does – and Why the Combination Matters

This is more than just a combination of known SMC tools — it's a complete workflow assistant:

-FVGs highlight where liquidity is likely resting due to institutional imbalance.

-BOS & CHoCH define structural context: whether the market is trending or shifting.

-Supply & Demand Zones show where institutions are likely to react.

-Each component works together to create a layered confluence system:

-FVG inside a Demand Zone after a Bullish CHoCH → High-probability Long Setup

-Bearish BOS into a Supply Zone + fresh Bearish FVG → High-probability Short Setup

📘 Core Concepts Explained

Fair Value Gap (FVG)

FVGs occur when price moves with strong momentum and leaves a gap between candles — suggesting inefficiency. Bullish FVGs lie below price; bearish ones above. Price often returns to these levels before continuing.

An FVG is detected when a three-candle sequence reveals a price imbalance:

- Bullish : Candle 2’s low is higher than Candle 1’s high

- Bearish : Candle 2’s high is lower than Candle 1’s low

These setups indicate a sudden burst of institutional momentum, often causing price to revisit the gap for rebalancing.

Break of Structure (BOS)

A BOS signals trend continuation when price breaks the previous swing high or low in the direction of the current trend.

The script uses a 3-bar pivot system to detect local swing highs and lows — a swing high forms when the highest candle is flanked by two lower highs on each side (and vice versa for swing lows).

A BOS is confirmed when price closes beyond the most recent swing point in alignment with the current trend direction.

Change of Character (CHoCH)

A CHoCH signals a potential trend reversal by breaking a structure level in the opposite direction of the prevailing trend.

It is detected when price breaks the most recent opposing swing and simultaneously flips the internal trend state.

CHoCH events always take precedence over BOS to avoid conflicting signals.

The internal trend engine ensures that these structural shifts are valid and not caused by random volatility.

Supply & Demand Zones

These zones mark institutional interest and are formed using precise price action rules — not arbitrary support/resistance.

A valid zone begins when a small-bodied base candle (such as a star or doji) appears at a local swing point. This candle must be followed by a strong impulse candle — either a bullish engulfing (for demand) or bearish breakout (for supply).

- Demand Zone : From the base candle's low to the impulse candle's high

- Supply Zone : From the base candle's high to the impulse candle's low

These zones represent likely institutional entries or exits, often acting as magnets or rejection areas. Once price decisively breaks through a zone, it is automatically removed — keeping the chart clean and relevant.

Zone Detection Logic – When a Zone Is Drawn or Skipped

Below are the precise rules used to determine whether a Supply or Demand Zone is valid and shown on the chart

A Supply or Demand Zone is only drawn if all of the following conditions are met:

-A small-bodied base candle forms at a local high or low (body size below threshold)

-The base candle is followed by a strong impulse candle (engulfing or breakout)

-The impulse direction matches the expected context (e.g., bearish impulse from swing high = Supply)

-The candle wicks do not invalidate the structure (e.g., no long opposing wick that retraces the move)

-The zone meets the minimum size threshold based on % or ATR filter

If any of these criteria are not satisfied, the zone is skipped to avoid false or weak levels.

This ensures only clean, institutional-grade Supply & Demand Zones are shown on the chart.

(e.g. small-bodied star + bullish engulfing at swing low = Demand Zone, or bearish breakout at swing high = Supply Zone).

🔍 Core Functionality & Original Features

1. 📉 Fair Value Gaps (FVGs) – Dynamic, Validated, and Clean

Unlike scripts that draw every gap, this script applies strict quality control to ensure only meaningful FVGs appear:

Minimum Threshold Filtering

Filters out small or noisy gaps by requiring each FVG to exceed a % or ATR-based size threshold. Prevents micro-gap clutter on lower timeframes.

Momentum Candle Verification

Requires a strong middle candle (candle 2) between two extremes. Large opposing wicks invalidate the setup.

Partial Fill Adjustment

When price partially fills a gap, the FVG box automatically shrinks to show only the remaining imbalance. If fully filled, the box is removed.

Multi-Timeframe Overlays

View institutional gaps from 15m, 1H, 4H, or Daily overlaid onto any chart for top-down analysis and entry refinement.

2. 🧱 Structural Shifts – BOS & CHoCH

Structural logic is built around pivot detection with real-time trend state awareness:

Pivot Logic (Customizable Strength)

Local highs/lows are detected using pivot length (default: 3 bars left/right). Breaks are only confirmed if they align with the internal trend state.

BOS = Continuation

Breaks a swing in trend direction (e.g., HL → HH → BOS at previous HH)

CHoCH = Reversal

Breaks a structure against trend (e.g., HH → HL → break of HL = Bearish CHoCH)

Conflict Resolution

If both BOS and CHoCH could trigger, CHoCH takes priority. This avoids false positives and ensures a single, clear structure signal per swing.

Styling & Visibility

All structure lines and labels are customizable — colors, line style (solid/dashed), and which signals to display (BOS/CHoCH/both).

3. 🧠 Supply & Demand Zones – Smart Detection & Maintenance

These zones are generated using strict price action logic, not arbitrary support/resistance lines:

-Formation Conditions

-Small-bodied "base candle" at a local high/low

-Followed by an impulse candle (bullish/bearish engulfing or breakout)

-Zone Bounds

- Demand : From base candle low to impulse high

- Supply : From base candle high to impulse low

Automatic Cleanup

Once price decisively pierces a zone, it’s automatically removed from the chart. This keeps the display relevant and clutter-free.

Multi-Timeframe Zones

Toggle zones from your current timeframe or overlay from 1H, 4H, and Daily — ideal for confluence stacking.

Zone Compression Filtering

Optional compression % ensures overlapping zones are combined logically to reduce redundancy.

🧩 How It Works Together – Practical Usage Flow

This indicator is designed to follow a structured workflow used by institutional-style traders:

Trend Structure

Identify trend using BOS and CHoCH on your timeframe.

Liquidity Zones

Look for supply/demand zones aligning with the structural bias.

Execution Areas

Wait for an unfilled FVG in confluence with the above conditions.

📸 Screenshot Captions

Screenshot 1: CHoCH + Demand Zone + Bullish FVG

📌 Reversal Setup with Confluence

A Bullish CHoCH confirms a structural shift. Price enters a Demand Zone and reacts from an unfilled Bullish FVG, creating a high-probability long opportunity.

Screenshot 2: Bearish BOS + FVG Fill

📌 Trend Continuation Confirmation

Price breaks a swing low, triggering a Bearish BOS. A Bearish FVG forms and price returns to fill it before continuing lower — validating the trend and the gap.

Screenshot 3: Multi-Timeframe Overlay (FVGs from 1H and 4H)

📌 Top-Down Liquidity Mapping

Overlaid 1H and 4H FVGs provide institutional-level insight on lower timeframes. Combined with structure signals, this supports precise entry alignment across timeframes.

As price partially fills a bullish gap, the FVG box auto-adjusts to show only the remaining imbalance. Fully filled zones are automatically removed, keeping the chart clean.

Screenshot 4: Supply Zone Rejection

📌 Institutional Supply in Action

Price enters a Supply Zone formed from a base candle + bearish impulse. A sharp rejection confirms active sell-side interest at this level. Zone opgevuld box verdwijnt

Screenshot 5: Bullish BOS + Internal Trend Logic

📌 Trend Continuation with Structure Awareness

A Higher Low forms, followed by a Higher High, triggering a Bullish BOS. The internal trend engine confirms direction and filters false reversals.

Screenshot 6: Zone Compression Logic

📌 Smart Zone Consolidation

Closely overlapping supply zones are merged using compression logic to prevent clutter. Only the strongest institutional levels remain visible.

⚙ Full Customization Panel

You can configure:

-FVG display per timeframe + color scheme

-BOS/CHoCH styling, label text, and detection toggles

-Zone settings: visibility, compression %, length

-Auto-cleanup behavior for FVGs and zones

🔐 Why Invite-Only?

This indicator contains original logic not available in public indicators, including:

-Momentum-candle verified FVGs

-Real-time partial fill trimming

-Auto-removal of invalidated structure/zones

-Conflict-aware BOS/CHoCH logic

-Multi-timeframe overlays with internal state tracking

-Proprietary compression-based zone filtering

This script is part of a private paid offering. It is not based on reused or repackaged educational code. The logic and structure management are exclusive to this implementation.

⚠ Disclaimer

This tool is for educational and analytical use only. It does not provide financial advice or trading signals. Always use proper risk management and do your own due diligence.

Market Strength Buy Sell Indicator [TradeDots]A specialized tool designed to assist traders in evaluating market conditions through a multifaceted analysis of relative performance, beta-adjusted returns, momentum, and volume—allowing you to identify optimal points for long or short trades. By integrating multiple benchmarks (default S&P 500) and percentile-based thresholds, the script provides clear, actionable insights suitable for both day trading and higher-level timeframe assessments.

📝 HOW IT WORKS

1. Multi-Factor Composite Score

Relative Performance (RS Ratio): Compares your asset’s performance to a chosen benchmark (default: SPY). Values above 1.0 indicate outperformance, while below 1.0 suggest underperformance.

Beta-Adjusted Returns: Checks the ticker’s excess movement relative to expected market-related moves. This helps distinguish pure “alpha” from broad market effects.

Volume & Correlation: Volume spikes often confirm the momentum behind a move, while correlation measures how closely the asset tracks or diverges from its benchmark.

These components merge into a 0–100 composite score. Scores above 50 frequently imply bullish strength; drops below 50 often point to underperformance—potentially flagging short opportunities.

2. Intraday & Day Trading Focus

Monitoring Below 50: During the trading day, the script calculates live data against the benchmark, offering an intraday-sensitive composite score. A dip under 50 may indicate a short bias for that session, especially when accompanied by high volume or momentum shifts.

3. Higher Timeframe Monitoring

Daily Strategies: On daily or weekly charts, the script reveals overall relative strength or weakness compared to the S&P 500. This higher-level perspective helps form broader trading biases—crucial for swing or position trades spanning multiple days.

Long/Short Thresholds: Persistent readings above 50 on a daily chart typically reinforce a long bias, while consistent dips below 50 can sustain a short or cautious outlook.

4. Pair Trading Applications

Custom Benchmark Selection: By setting a specific ticker pair as your benchmark instead of the default S&P 500, you can identify spread trading opportunities between two correlated assets. This allows you to go long the outperforming asset while shorting the underperforming one when the spread reaches extreme levels.

4. Color-Coded Signals & Alerts

Visual Zones (25–75): Color-coded bands highlight strong outperformance (above 75) or pronounced underperformance (below 25).

Alerts on Strong Shifts: Automatic alerts can notify you of sudden entries or exits from bullish or bearish zones, so you can potentially act on new market information without delay.

⚙️ HOW TO USE

1. Select Your Timeframe: For scalping or day trading, lower intervals (e.g., 5-minute) offer immediate data resets at the session’s start. For multi-day insight, daily or weekly charts reveal broader performance trends.

2. Watch Key Levels Around 50: Intraday dips under 50 may be a cue to consider short trades, while bounces above 50 can confirm renewed strength.

3. Assess Benchmark Relationships: Compare your asset’s score and signals to the broader market. A stock falling below its pair’s relative strength line might lag overall market momentum.

4. Combine Tools & Validate: This script excels when integrated with other technical analysis methods (e.g., support/resistance, chart patterns) and fundamental factors for a holistic market view.

❗ LIMITATIONS

No Direction Guarantee: The indicator identifies relative strength but does not guarantee directional price moves.

Delayed Updates: Since calculations update after each bar close, sudden intrabar changes may not immediately reflect.

Market-Specific Behaviors: Some assets or unusual market conditions may deviate from typical benchmarks, weakening signal reliability.

Past ≠ Future: High or low relative strength in the past may not predict continued performance.

RISK DISCLAIMER

All forms of trading and investing involve risk, including the possible loss of principal. This indicator analyzes relative performance but cannot assure profits or eliminate losses. Past performance of any strategy does not guarantee future results. Always combine analysis with proper risk management and your broader trading plan. Consult a licensed financial advisor if you are unsure of your individual risk tolerance or investment objectives.

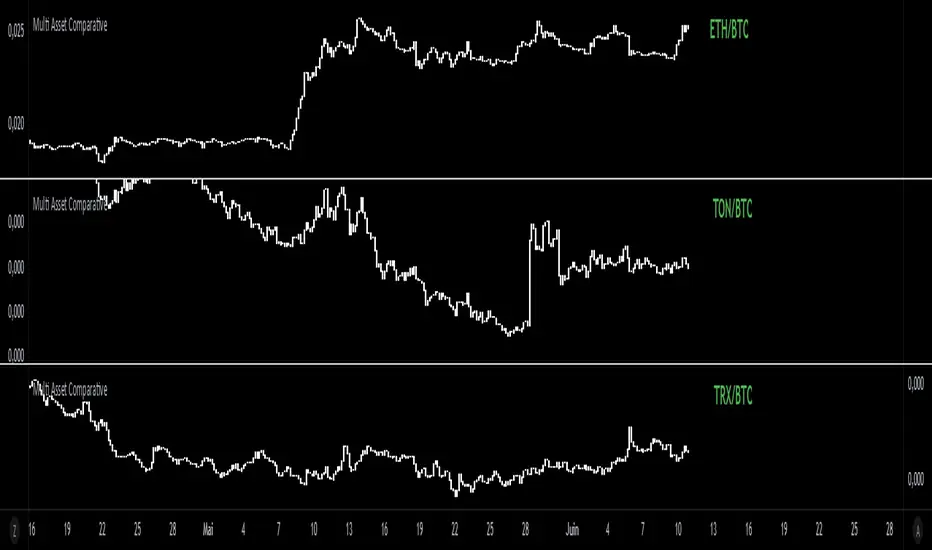

Multi Asset Comparative📊 Multi Asset Comparative – Compare Baskets of Cryptos Visually

This indicator allows you to compare the performance of two groups of cryptocurrencies (or any assets) over time, using a clean and intuitive chart.

Instead of looking at each asset separately, this tool gives you a global view by showing how one group performs relative to another — all displayed in the form of candlesticks.

🧠 What This Tool Is For

Markets constantly shift, and capital rotates between sectors or tokens. This script helps you visually track those shifts by answering a key question:

"Is this group of assets getting stronger or weaker compared to another group?"

For example:

Compare altcoins vs Bitcoin

Track the DeFi sector vs Ethereum

Analyze your custom portfolio vs the market

Spot moments when money flows from majors to smaller caps, or vice versa

🧩 How It Works (Simplified)

You select two groups of assets:

Group 1 (up to 20 assets) — the one you want to analyze

Group 2 (up to 5 assets) — your comparison baseline

The indicator then creates a single line of candles that represents the performance of Group 1 compared to Group 2. If the candles go up, it means Group 1 is gaining strength over Group 2. If the candles go down, it's losing ground.

This lets you see market dynamics in one glance, instead of switching charts or running calculations manually.

🚀 Why It's Unique

Unlike many indicators that just show data from one asset, this one provides a bird's-eye view of multiple assets at once — condensed into a simple visual ratio.

It’s:

Customizable (you choose the assets)

Visual and intuitive (no need to interpret tables or formulas)

Actionable (helps with trend confirmation, macro views, and market rotation)

Whether you're a swing trader, a macro analyst, or building your own strategy, this tool can help you spot opportunities hidden in plain sight.

✅ How to Use It

Choose your two groups of assets (e.g., altcoins vs BTC/ETH)

Watch the direction of the candles:

Uptrend = Group 1 gaining strength over Group 2

Downtrend = Group 1 weakening

Use it to confirm market shifts, anticipate rotations, or analyze sector strength

Approximate Entropy Zones [PhenLabs]Version: PineScript™ v6

Description

This indicator identifies periods of market complexity and randomness by calculating the Approximate Entropy (ApEn) of price action. As the movement of the market becomes complex, it means the current trend is losing steam and a reversal or consolidation is likely near. The indicator plots high-entropy periods as zones on your chart, providing a graphical suggestion to anticipate a potential market direction change. This indicator is designed to help traders identify favorable times to get in or out of a trade by highlighting when the market is in a state of disarray.

Points of Innovation

Advanced Complexity Analysis: Instead of relying on traditional momentum or trend indicators, this tool uses Approximate Entropy to quantify the unpredictability of price movements.

Dynamic Zone Creation: It automatically plots zones on the chart during periods of high entropy, providing a clear and intuitive visual guide.

Customizable Sensitivity: Users can fine-tune the ‘Entropy Threshold’ to adjust how frequently zones appear, allowing for calibration to different assets and timeframes.

Time-Based Zone Expiration: Zones can be set to expire after a specific time, keeping the chart clean and relevant.

Built-in Zone Size Filter: Excludes zones that form on excessively large candles, filtering out noise from extreme volatility events.

On-Chart Calibration Guide: A persistent note on the chart provides simple instructions for adjusting the entropy threshold, making it easy for users to optimize the indicator’s performance.

Core Components

Approximate Entropy (ApEn) Calculation: The core of the indicator, which measures the complexity or randomness of the price data.

Zone Plotting: Creates visual boxes on the chart when the calculated ApEn value exceeds a user-defined threshold.

Dynamic Zone Management: Manages the lifecycle of the zones, from creation to expiration, ensuring the chart remains uncluttered.

Customizable Settings: A comprehensive set of inputs that allow users to control the indicator’s sensitivity, appearance, and time-based behavior.

Key Features

Identifies Potential Reversals: The high-entropy zones can signal that a trend is nearing its end, giving traders an early warning.

Works on Any Timeframe: The indicator can be applied to any chart timeframe, from minutes to days.

Customizable Appearance: Users can change the color and transparency of the zones to match their chart’s theme.

Informative Labels: Each zone can display the calculated entropy value and the direction of the candle on which it formed.

Visualization

Entropy Zones: Shaded boxes that appear on the chart, highlighting candles with high complexity.

Zone Labels: Text within each zone that displays the ApEn value and a directional arrow (e.g., “0.525 ↑”).

Calibration Note: A small table in the top-right corner of the chart with instructions for adjusting the indicator’s sensitivity.

Usage Guidelines

Entropy Analysis

Source: The price data used for the ApEn calculation. (Default: close)

Lookback Length: The number of bars used in the ApEn calculation. (Default: 20, Range: 10-50)

Embedding Dimension (m): The length of patterns to be compared; a standard value for financial data. (Default: 2)

Tolerance Multiplier (r): Adjusts the tolerance for pattern matching; a larger value makes matching more lenient. (Default: 0.2)

Entropy Threshold: The ApEn value that must be exceeded to plot a zone. Increase this if too many zones appear; decrease it if too few appear. (Default: 0.525)

Time Settings

Analysis Timeframe: How long a zone remains on the chart after it forms. (Default: 1D)

Custom Period (Bars): The zone’s lifespan in bars if “Analysis Timeframe” is set to “Custom”. (Default: 1000)

Zone Settings

Zone Fill Color: The color of the entropy zones. (Default: #21f38a with 80% transparency)

Maximum Zone Size %: Filters out zones on candles that are larger than this percentage of their low price. (Default: 0.5)

Display Options

Show Entropy Label: Toggles the visibility of the text label inside each zone. (Default: true)

Label Text Position: The horizontal alignment of the text label. (Default: Right)

Show Calibration Note: Toggles the visibility of the calibration note in the corner of the chart. (Default: true)

Best Use Cases

Trend Reversal Trading: Identifying when a strong trend is likely to reverse or pause.

Breakout Confirmation: Using the absence of high entropy to confirm the strength of a breakout.

Ranging Market Identification: Periods of high entropy can indicate that a market is transitioning into a sideways or choppy phase.

Limitations

Not a Standalone Signal: This indicator should be used in conjunction with other forms of analysis to confirm trading signals.

Lagging Nature: Like all indicators based on historical data, ApEn is a lagging measure and does not predict future price movements with certainty.

Calibration Required: The effectiveness of the indicator is highly dependent on the “Entropy Threshold” setting, which needs to be adjusted for different assets and timeframes.

What Makes This Unique

Quantifies Complexity: It provides a numerical measure of market complexity, offering a different perspective than traditional indicators.

Clear Visual Cues: The zones make it easy to see when the market is in a state of high unpredictability.

User-Friendly Design: With features like the on-chart calibration note, the indicator is designed to be easy to use and optimize.

How It Works

Calculate Standard Deviation: The indicator first calculates the standard deviation of the source price data over a specified lookback period.

Calculate Phi: It then calculates a value called “phi” for two different pattern lengths (embedding dimensions ‘m’ and ‘m+1’). This involves comparing sequences of data points to see how many are “similar” within a certain tolerance (determined by the standard deviation and the ‘r’ multiplier).

Calculate ApEn: The Approximate Entropy is the difference between the two phi values. A higher ApEn value indicates greater irregularity and unpredictability in the data.

Plot Zones: If the calculated ApEn exceeds the user-defined ‘Entropy Threshold’, a zone is plotted on the chart.

Note: The “Entropy Threshold” is the most important setting to adjust. If you see too many zones, increase the threshold. If you see too few, decrease it.

SmartPhase Analyzer📝 SmartPhase Analyzer – Composite Market Regime Classifier

SmartPhase Analyzer is an adaptive regime classification tool that scores market conditions using a customizable set of statistical indicators. It blends multiple normalized metrics into a composite score, which is dynamically evaluated against rolling statistical thresholds to determine the current market regime.

✅ Features:

Composite score calculated from 13+ toggleable statistical indicators:

Sharpe, Sortino, Omega, Alpha, Beta, CV, R², Entropy, Drawdown, Z-Score, PLF, SRI, and Momentum Rank

Uses dynamic thresholds (mean ± std deviation) to classify regime states:

🟢 BULL – Strongly bullish

🟩 ACCUM – Mildly bullish

⚪ NEUTRAL – Sideways

🟧 DISTRIB – Mildly bearish

🔴 BEAR – Strongly bearish

Color-coded histogram for composite score clarity

Real-time regime label plotted on chart

Benchmark-aware metrics (Alpha, Beta, etc.)

Modular design using the StatMetrics library by RWCS_LTD

🧠 How to Use:

Enable/disable metrics in the settings panel to customize your composite model

Use the composite histogram and regime background for discretionary or systematic analysis

⚠️ Disclaimer:

This indicator is for educational and informational purposes only. It does not constitute financial advice or a trading recommendation. Always consult your financial advisor before making investment decisions.

StatMetricsLibrary "StatMetrics"

A utility library for common statistical indicators and ratios used in technical analysis.

Includes Z-Score, correlation, PLF, SRI, Sharpe, Sortino, Omega ratios, and normalization tools.

zscore(src, len)

Calculates the Z-score of a series

Parameters:

src (float) : The input price or series (e.g., close)

len (simple int) : The lookback period for mean and standard deviation

Returns: Z-score: number of standard deviations the input is from the mean

corr(x, y, len)

Computes Pearson correlation coefficient between two series

Parameters:

x (float) : First series

y (float) : Second series

len (simple int) : Lookback period

Returns: Correlation coefficient between -1 and 1

plf(src, longLen, shortLen, smoothLen)

Calculates the Price Lag Factor (PLF) as the difference between long and short Z-scores, normalized and smoothed

Parameters:

src (float) : Source series (e.g., close)

longLen (simple int) : Long Z-score period

shortLen (simple int) : Short Z-score period

smoothLen (simple int) : Hull MA smoothing length

Returns: Smoothed and normalized PLF oscillator

sri(signal, len)

Computes the Statistical Reliability Index (SRI) based on trend persistence

Parameters:

signal (float) : A price or signal series (e.g., smoothed PLF)

len (simple int) : Lookback period for smoothing and deviation

Returns: Normalized trend reliability score

sharpe(src, len)

Calculates the Sharpe Ratio over a period

Parameters:

src (float) : Price series (e.g., close)

len (simple int) : Lookback period

Returns: Sharpe ratio value

sortino(src, len)

Calculates the Sortino Ratio over a period, using only downside volatility

Parameters:

src (float) : Price series

len (simple int) : Lookback period

Returns: Sortino ratio value

omega(src, len)

Calculates the Omega Ratio as the ratio of upside to downside return area

Parameters:

src (float) : Price series

len (simple int) : Lookback period

Returns: Omega ratio value

beta(asset, benchmark, len)

Calculates beta coefficient of asset vs benchmark using rolling covariance

Parameters:

asset (float) : Series of the asset (e.g., close)

benchmark (float) : Series of the benchmark (e.g., SPX close)

len (simple int) : Lookback window

Returns: Beta value (slope of linear regression)

alpha(asset, benchmark, len)

Calculates rolling alpha of an asset relative to a benchmark

Parameters:

asset (float) : Series of the asset (e.g., close)

benchmark (float) : Series of the benchmark (e.g., SPX close)

len (simple int) : Lookback window

Returns: Alpha value (excess return not explained by Beta exposure)

skew(x, len)

Computes skewness of a return series

Parameters:

x (float) : Input series (e.g., returns)

len (simple int) : Lookback period

Returns: Skewness value

kurtosis(x, len)

Computes kurtosis of a return series

Parameters:

x (float) : Input series (e.g., returns)

len (simple int) : Lookback period

Returns: Kurtosis value

cv(x, len)

Calculates Coefficient of Variation

Parameters:

x (float) : Input series (e.g., returns or prices)

len (simple int) : Lookback period

Returns: CV value

autocorr(x, len)

Calculates autocorrelation with 1-lag

Parameters:

x (float) : Series to test

len (simple int) : Lookback window

Returns: Autocorrelation at lag 1

stderr(x, len)

Calculates rolling standard error of a series

Parameters:

x (float) : Input series

len (simple int) : Lookback window

Returns: Standard error (std dev / sqrt(n))

info_ratio(asset, benchmark, len)

Calculates the Information Ratio

Parameters:

asset (float) : Asset price series

benchmark (float) : Benchmark price series

len (simple int) : Lookback period

Returns: Information ratio (alpha / tracking error)

tracking_error(asset, benchmark, len)

Measures deviation from benchmark (Tracking Error)

Parameters:

asset (float) : Asset return series

benchmark (float) : Benchmark return series

len (simple int) : Lookback window

Returns: Tracking error value

max_drawdown(x, len)

Computes maximum drawdown over a rolling window

Parameters:

x (float) : Price series

len (simple int) : Lookback window

Returns: Rolling max drawdown percentage (as a negative value)

zscore_signal(z, ob, os)

Converts Z-score into a 3-level signal

Parameters:

z (float) : Z-score series

ob (float) : Overbought threshold

os (float) : Oversold threshold

Returns: -1, 0, or 1 depending on signal state

r_squared(x, y, len)

Calculates rolling R-squared (coefficient of determination)

Parameters:

x (float) : Asset returns

y (float) : Benchmark returns

len (simple int) : Lookback window

Returns: R-squared value (0 to 1)

entropy(x, len)

Approximates Shannon entropy using log returns

Parameters:

x (float) : Price series

len (simple int) : Lookback period

Returns: Approximate entropy

zreversal(z)

Detects Z-score reversals to the mean

Parameters:

z (float) : Z-score series

Returns: +1 on upward reversal, -1 on downward

momentum_rank(x, len)

Calculates relative momentum strength

Parameters:

x (float) : Price series

len (simple int) : Lookback window

Returns: Proportion of lookback where current price is higher

normalize(x, len)

Normalizes a series to a 0–1 range over a period

Parameters:

x (float) : The input series

len (simple int) : Lookback period

Returns: Normalized value between 0 and 1

composite_score(score1, score2, score3)

Combines multiple normalized scores into a composite score

Parameters:

score1 (float)

score2 (float)

score3 (float)

Returns: Average composite score

Customizable Time DisplayA simple indicator that display the current time on the chart, I find this to be very useful in playback, I know the time is just below but this one give you a quick look on the exact minutes to 30s so you don't have to mouse over the chart to find out the exact time... so this can be very helpful in replay when you want to rewind a few minutes.

It is also very customizable, you can select if you want to display the year, date or minutes or not.. you can also customze colors and location of this display anywhere on the chart.

Time Specific Standard Deviation Zones(10 am - 4hr candle)This indicator is designed for intraday traders who want to visualize volatility-based zones around the 10:00 AM New York session open, plotted precisely from 10:00 AM to 2:00 PM EST.

✅ Key Features:

📦 Automatically draws mirrored Standard Deviation (SD) zones:

0.5 SD, 1 SD, 1.5 SD above and below the 10AM open

Open Line reference for mean reversion tracking

📐 Internal Fibonacci Levels within each zone:

0.236, 0.382, 0.5, 0.618, 0.786

⏱️ Works across any timeframe

📊 Ideal for:

Breakout traders

Volatility compression strategies

Statistical mean reversion models

🔧 Built using precise New York session timestamps, ensuring accuracy across time zones and resolutions.

Uptrick: Mean ReversionOverview

Uptrick: Mean Reversion is a technical indicator designed to identify statistically significant reversal opportunities by monitoring market extremes. It presents a unified view of multiple analytical layers—momentum shifts, extreme zones, divergence patterns, and a multi-factor bias dashboard—within a single pane. By translating price momentum into a normalized framework, it highlights areas where prices are likely to revert to their average range.

Introduction

Uptrick: Mean Reversion relies on several core concepts:

Volatility normalization

The indicator rescales recent market momentum into a common scale so that extreme readings can be interpreted consistently across different assets and timeframes.

Mean reversion principle

Markets often oscillate around an average level. When values stray too far beyond typical ranges, a return toward the mean is likely. Uptrick: Mean Reversion detects when these extremes occur.

Momentum inflection

Sharp changes in momentum direction frequently presage turning points. The indicator watches for shifts from upward momentum to downward momentum (and vice versa) to help time entries and exits.

Divergence

When price trends and internal momentum readings move in opposite directions, it can signal weakening momentum and an impending reversal. Uptrick: Mean Reversion flags such divergence conditions directly on the indicator pane.

Multi-factor sentiment

No single metric tells the entire story. By combining several independent sentiment measures—price structure, momentum, oscillators, and external market context—Uptrick: Mean Reversion offers a more balanced view of overall market bias.

Purpose

Uptrick: Mean Reversion was created for traders who focus on countertrend opportunities rather than simply following established trends. Its main objectives are:

Spot extreme conditions

By normalizing momentum into a standardized scale, the indicator clearly marks when the market is in overbought or oversold territory. These conditions often align with points where a snapback toward average is more probable.

Provide reversal signals

Built-in logic detects when momentum shifts direction within extreme zones and displays clear buy or sell markers to guide countertrend entries and exits.

Highlight hidden divergences

Divergence between price and internal momentum can suggest underlying weakness or strength ahead of actual price moves. Uptrick: Mean Reversion plots these divergences directly, allowing traders to anticipate reversals earlier.

Offer contextual bias

A dynamic dashboard aggregates multiple independent indicators—based on recent price action, momentum readings, common oscillators, and broader market context—to produce a single sentiment label. This helps traders determine whether mean reversion signals align with or contradict overall market conditions.

Cater to lower timeframes

Mean reversion tends to occur more frequently and reliably on shorter timeframes (for example, 5-minute, 15-minute, or 1-hour charts). Uptrick: Mean Reversion is optimized for these nimble environments, where rapid reversals can be captured before a larger trend takes hold.

Originality and Uniqueness

Uptrick: Mean Reversion stands out for several reasons:

Proprietary normalization framework

Instead of relying on raw oscillator values, it transforms momentum into a standardized scale. This ensures that extreme readings carry consistent meaning across different assets and volatility regimes.

Inflection-based signals

The indicator waits for a clear shift in momentum direction within extreme zones before plotting reversal markers. This approach reduces false signals compared to methods that rely solely on fixed threshold crossings.

Embedded divergence logic

Divergence detection is handled entirely within the same pane. Rather than requiring a separate indicator window, Uptrick: Mean Reversion identifies instances where price and internal momentum readings do not align and signals those setups directly on the chart.

Adjustable sensitivity profiles

Traders can choose from predefined risk profiles—ranging from very conservative to very aggressive—to automatically adjust how extreme a reading must be before triggering a signal. This customization helps balance between capturing only the most significant reversals or generating more frequent, smaller opportunities.

Multi-factor bias dashboard

While many indicators focus on a single metric, Uptrick: Mean Reversion aggregates five distinct sentiment measures. By balancing price-based bias, momentum conditions, and broader market context, it offers a more nuanced view of when to take—or avoid—countertrend trades.

Why Indicators Were Merged

Proprietary momentum oscillator

A custom-built oscillator rescales recent price movement into a normalized range. This core component underpins all signal logic and divergence checks, allowing extreme readings to be identified consistently.

Inflection detection

By comparing recent momentum values over a configurable lookback interval, the indicator identifies clear shifts from rising to falling momentum (and vice versa). These inflection points serve as a prerequisite for reversal signals when combined with extreme conditions.

Divergence framework

Local peaks and troughs are identified within the normalized oscillator and compared to corresponding price highs and lows. When momentum peaks fail to follow price to new extremes (or vice versa), a divergence alert appears, suggesting weakening momentum ahead of a price turn.

Classic price bias

Recent bar structures are examined to infer whether the immediate past price action was predominantly bullish, bearish, or neutral. This provides one piece of the overall sentiment picture.

Smoothed oscillator bias

A secondary oscillator reading is smoothed and compared to a central midpoint to generate a simple bullish or bearish reading.

Range-based oscillator bias

A familiar range-bound oscillator is used to detect oversold or overbought readings, contributing to the sentiment score.

Classic momentum crossover bias

A traditional momentum check confirms whether momentum currently leans bullish or bearish.

External market trend bias

The indicator monitors a major currency’s short-term trend to gauge broader market risk appetite. A falling currency—often associated with higher risk tolerance—contributes a bullish bias point, while a rising currency adds a bearish point.

All these elements run concurrently. Each piece provides a “vote” toward an overall sentiment reading. At the same time, the proprietary momentum oscillator drives both extreme-zone detection and divergence identification. By merging these inputs, the final result is a single pane showing both precise reversal signals and a unified market bias.

How It Works

At runtime, the indicator proceeds through the following conceptual steps:

Read user inputs (risk profile, lookback index, visual mode, color scheme, background highlighting, bias table display, divergence toggles).

Fetch the latest price data.

Process recent price movement through a proprietary normalization engine to produce a single, standardized momentum reading for each bar.

Track momentum over a configurable lookback interval to detect shifts in direction.

Compare the current momentum reading to dynamically determined extreme thresholds (based on the chosen risk profile).

If momentum has flipped from down to up within an oversold area, display a discrete buy marker. If momentum flips from up to down within an overbought area, display a sell marker.

Identify local peaks and troughs in the proprietary momentum series and compare to price highs and lows over a configurable range. When divergence criteria are met, display bullish or bearish divergence labels

Evaluate five independent sentiment measures—price bar bias, smoothed oscillator bias, range oscillator bias, traditional momentum crossover bias, and an external market trend bias—and assign each a +1 (bullish), –1 (bearish), or 0 (neutral) vote.

Average the five votes to produce an overall sentiment score. If the average exceeds a positive threshold, label the bias as bullish; if it falls below a negative threshold, label it as bearish; otherwise label it neutral.

Update the on-screen bias table at regular intervals, showing each individual metric’s value and vote, as well as the combined sentiment label.

Apply color fills to highlight extreme zones in the background and draw horizontal guideline bands around those extremes.

In complex visual mode, draw a cloud-like band that instantly changes color when momentum shifts. In simple mode, plot only a clean line of the normalized reading in a contrasting color.

Expose alert triggers whenever a buy/sell signal, divergence confirmation, or bias flip occurs, for use in automated notifications.

Inputs

Here is how each input affects the indicator:

Trading Style (very conservative / conservative / neutral / aggressive / very aggressive)

Determines how sensitive the indicator is to extreme readings. Conservative settings require more pronounced market deviations before signaling a reversal; aggressive settings signal more frequently at smaller deviations.

Slope Detection Index (integer)

Controls how many bars back the indicator looks to compare momentum for inflection detection. Lower numbers respond more quickly but can be noisy; higher numbers smooth out short-term fluctuations.

Visual Mode (simple / complex)

Simple mode plots only the normalized momentum line, colored according to the chosen palette. Complex mode draws a candle-style block for each bar—showing the range of momentum movement within that bar—with colored fills that switch instantly when momentum direction changes.

Color Scheme (multiple themes)

Select from preset color palettes to style bullish vs. bearish elements (fills, lines, labels). Options include bright neon tones, classic contrasting pairs, dark-mode palettes, and more, ensuring signals stand out against any chart background.

Enable Background Highlighting (true / false)

When true, extreme overbought or oversold zones are shaded in a semi-transparent color behind the main pane. This helps traders “see” when the market is in a normalized extreme state without relying solely on lines or markers.

Show Helper Scale Lines (true / false)

When true, hidden horizontal lines force the vertical scale to include a fixed range of extreme values—even if the indicator rarely reaches them—so traders always know where the most extreme limits lie.

Enable Divergence Detection (true / false)

Toggles whether the script looks for divergences between price and the proprietary momentum reading. When enabled, bullish/bearish divergence markers appear automatically whenever defined conditions are met.

Pivot Lookback Left & Pivot Lookback Right (integers)

Define how many bars to the left and right the indicator examines when identifying a local peak or trough in the momentum reading. Adjust these to capture divergences on different swing lengths.

Minimum and Maximum Bars Between Pivots (integers)

Set the minimum and maximum number of bars allowed between two identified peaks or troughs for a valid divergence. This helps filter out insignificant or overly extended divergence patterns.

Show Bias Table (true / false)

When enabled, displays a small table in the upper-right corner summarizing five independent sentiment votes and the combined bias label. Disable to keep the pane focused on only the momentum series and signals.

Features

1. Extreme-zone highlighting

Overbought and oversold areas appear as colored backgrounds when the proprietary momentum reading crosses dynamically determined thresholds. This gives an immediate visual cue whenever the market moves into a highly extreme condition.

2. Discrete reversal markers