Volumetric Expansion/Contraction### Indicator Title: Volumetric Expansion/Contraction

### Summary

The Volumetric Expansion/Contraction (PCC) indicator is a comprehensive momentum oscillator designed to identify high-conviction price moves. Unlike traditional oscillators that only look at price, the PCC integrates four critical dimensions of market activity: **Price Change**, **Relative Volume (RVOL)**, **Cumulative Volume Delta (CVD)**, and **Average True Range (ATR)**.

Its primary purpose is to help traders distinguish between meaningful, volume-backed market expansions and noisy, unsustainable price action. It gives more weight to moves that occur in a controlled, low-volatility environment, highlighting potential starts of new trends or significant shifts in market sentiment.

### Key Concepts & Purpose

The indicator's unique formula synthesizes the following concepts:

1. **Price Change:** Measures the magnitude and direction of the primary move.

2. **Relative Volume (RVOL):** Confirms that the move is backed by significant volume compared to its recent average, indicating institutional participation.

3. **Cumulative Volume Delta (CVD):** Measures the underlying buying and selling pressure, confirming that the price move is aligned with the net flow of market orders.

4. **Inverse Volatility (ATR):** This is the indicator's unique twist. It normalizes the signal by the inverse of the Average True Range. This means the indicator's value is **amplified** when volatility (ATR) is low (signifying a controlled, confident expansion) and **dampened** when volatility is high (filtering out chaotic, less predictable moves).

The goal is to provide a single, easy-to-read oscillator that signals when price, volume, and order flow are all in alignment, especially during a breakout from a period of contraction.

### Features

* **Main Oscillator Line:** A single line plotted in a separate pane that represents the calculated strength of the volumetric expansion or contraction.

* **Zero Line:** A dotted reference line to easily distinguish between bullish (above zero) and bearish (below zero) regimes.

* **Visual Threshold Zones:** The background automatically changes color to highlight periods of significant strength:

* **Bright Green:** Indicates a "Strong Up Move" when the oscillator crosses above the user-defined upper threshold.

* **Bright Fuchsia:** Indicates a "Strong Down Move" when the oscillator crosses below the user-defined lower threshold.

### Configurable Settings & Filters

The indicator is fully customizable to allow for extensive testing and adaptation to different assets and timeframes.

#### Main Calculation Inputs

* **Price Change Lookback:** Sets the period for calculating the primary price change.

* **CVD Normalization Length:** The lookback period for normalizing the Cumulative Volume Delta.

* **RVOL Avg Volume Length:** The lookback for the simple moving average of volume, used to calculate RVOL.

* **RVOL Normalization Length:** The lookback period for normalizing the RVOL score.

* **ATR Length & Normalization Length:** Sets the periods for calculating the ATR and its longer-term average for normalization.

#### Weights

* Fine-tune the impact of each core component on the final calculation, allowing you to emphasize what matters most to your strategy (e.g., give more weight to CVD or RVOL).

#### External Market Filter (Powerful Feature)

* **Enable SPY/QQQ Filter for Up Moves?:** A checkbox to activate a powerful regime filter.

* **Symbol:** A dropdown to choose whether to filter signals based on the trend of **SPY** or **QQQ**.

* **SMA Period:** Sets the lookback period for the Simple Moving Average (default is 50).

* **How it works:** When enabled, this filter will **only allow "Strong Up Move" signals to appear if the chosen symbol (SPY or QQQ) is currently trading above its specified SMA**. This is an excellent tool for aligning your signals with the broader market trend and avoiding bullish entries in a bearish market.

#### Visuals

* **Upper/Lower Threshold:** Allows you to define what level the oscillator must cross to trigger the colored background zones, letting you customize the indicator's sensitivity.

***

**Disclaimer:** This tool is designed for market analysis and confluence. It is not a standalone trading system. Always use this indicator in conjunction with your own trading strategy, risk management, and other forms of analysis.

Indicators and strategies

Ultimate Williams %RUltimate Williams %R

The most advanced Williams %R indicator available - featuring multi-timeframe analysis, zero-lag processing, volatility adaptivity, and intelligent extreme zone detection.

Key Improvements Over Standard Williams %R

Multi-Timeframe: Combines short, medium, and long-term Williams %R calculations with Ultimate Oscillator-style weighting for superior signal quality

Zero-Lag Implementation: Utilizes Ehler's Zero-Lag EMA with error correction, eliminating traditional oscillator lag while maintaining smoothness

Volatility Adaptive: Automatically adjusts periods based on ATR volatility analysis for optimal performance in all market conditions

Z-Score Normalization: Provides consistent, statistically-based extreme level detection across different market environments

Perfect For

Overbought/Oversold Identification: Instantly spot extreme market conditions with visual intensity that scales with signal strength

Divergence Analysis: Enhanced responsiveness and smooth operation make divergence patterns clearer and more reliable

Multi-Timeframe Confirmation: Built-in timeframe combination eliminates the need for multiple Williams %R indicators

Entry/Exit Timing: Zero-lag processing provides earlier signals without sacrificing accuracy

Customizable Settings

Timeframe Periods: Adjustable short (7), medium (14), and long (28) periods

Volatility Adaptation: Configurable ATR-based period adjustment

Zero-Lag Processing: Toggle and fine-tune the smoothing system

Z-Score Normalization: Adjustable lookback period for statistical analysis

Extreme Levels: Customizable threshold for extreme signal detection

[FS] Time & Cycles Time & Cycles

A comprehensive trading session indicator that helps traders identify and track key market sessions and their price levels. This tool is particularly useful for forex and futures traders who need to monitor multiple trading sessions.

Key Features:

• Multiple Session Support:

- London Session

- New York Session

- Sydney Session

- Asia Session

- Customizable TBD Session

• Session Visualization:

- Clear session boxes with customizable colors

- Session labels with adjustable visibility

- Support for sessions crossing midnight

- Timezone-aware calculations

• Price Level Tracking:

- Daily High/Low levels

- Weekly High/Low levels

- Previous session High/Low levels

- Customizable history depth for each level type

• Customization Options:

- Adjustable colors for each session

- Customizable border styles

- Label visibility controls

- Timezone selection

- History level depth settings

• Technical Features:

- High-performance calculation engine

- Support for multiple timeframes

- Efficient memory usage

- Clean and intuitive visual display

Perfect for:

• Forex traders monitoring multiple sessions

• Futures traders tracking market hours

• Swing traders identifying key session levels

• Day traders planning their trading hours

• Market analysts studying session patterns

The indicator helps traders:

- Identify active trading sessions

- Track session-specific price levels

- Monitor market activity across different time zones

- Plan trades based on session boundaries

- Analyze price action within specific sessions

Note: This indicator is designed to work across all timeframes and is optimized for performance with minimal impact on chart loading times.

Running Minimum HighThe running minimum high looks at the minimum high from a defined lookback period (default 10 days) and plots that on the price chart. Green arrows signify when the low of the candle is above the running minimum high (suggesting an uptrend), and red arrows signify when the high of the candle is below the running minimum high (suggesting a downtrend).

It is recommended to use this on high timeframes (e.g. 1 hour and above) given the high number of signals it generates on lower timeframes.

Session Range ProjectionsSession Range Projections

Purpose & Concept:

Session Range Projections is a comprehensive trading tool that identifies and analyzes price ranges during user-defined time periods. The indicator visualizes high-probability reversal zones and profit targets by projecting Fibonacci levels from custom session ranges, making it ideal for traders who focus on time-based market structure analysis.

Key Features & Calculations:

1. Custom Time Range Analysis

- Define any time period for range calculation - from traditional sessions (Asian, London, NY) to custom periods like opening ranges, hourly ranges, or 4-hour blocks

- Automatically captures the highest and lowest prices within your specified timeframe

- Supports multiple timezone selections for global market analysis

- Flexible enough for intraday scalping ranges or longer-term swing trading setups

2. Premium & Discount Zones

- Automatically divides the range into premium (above 50%) and discount (below 50%) zones

- Visual differentiation helps identify institutional buying and selling areas

- Color-coded boxes clearly mark these critical price zones

3. Optimal Trade Entry (OTE) Zones

- Highlights the 79-89% retracement zone in premium territory

- Highlights the 11-21% retracement zone in discount territory

- These zones represent high-probability reversal areas based on institutional order flow concepts

4. Fibonacci Projections

- Projects 11 customizable Fibonacci extension levels from the range extremes

- Levels extend both above and below the range for symmetrical analysis

- Each level can be individually toggled and color-customized

- Default levels include common retracement ratios: -0.5, -1.0, -2.0, -2.33, -2.5, -3.0, -4.0, -4.5, -6.0, -7.0, -8.0

How to Use:

Set Your Time Range: Input your desired session start and end times (24-hour format)

Select Timezone: Choose the appropriate timezone for your trading session

Customize Display: Toggle various visual elements based on your preferences

Monitor Price Action: Watch for reactions at projected levels and OTE zones

Set Alerts: Configure sweep alerts for when price breaks above/below range extremes

Input Parameters Explained:

Time Range Settings

Range Start/End Hour & Minute: Define your analysis period

Time Zone: Ensure accurate session timing across different markets

Visual Settings

Range Box: Toggle the premium/discount zone visualization

Horizontal Lines: Customize high/low line appearance

Internal Range Levels: Show/hide equilibrium and OTE zones

Labels: Configure text display for key levels

Fibonacci Projections: Enable/disable extension levels

Display Settings

Historical Ranges: Show up to 10 previous session ranges

Alert Type: Choose between high sweep, low sweep, or both

Trading Applications:

Session-Based Trading: Analyze specific market sessions (Asian, London, New York, opening ranges, hourly ranges)

Reversal Trading: Identify high-probability reversal zones at OTE levels

Breakout/Reversal Trading: Monitor range breaks/reversals with built-in sweep alerts

Risk Management: Use Fibonacci projections as profit targets or rejection areas

Multi-Timeframe Analysis: Apply to any timeframe for various trading styles

Important Notes:

This indicator is for educational purposes only and should not be considered financial advice

Past performance does not guarantee future results

Always use proper risk management when trading

The indicator automatically manages historical data to maintain chart performance

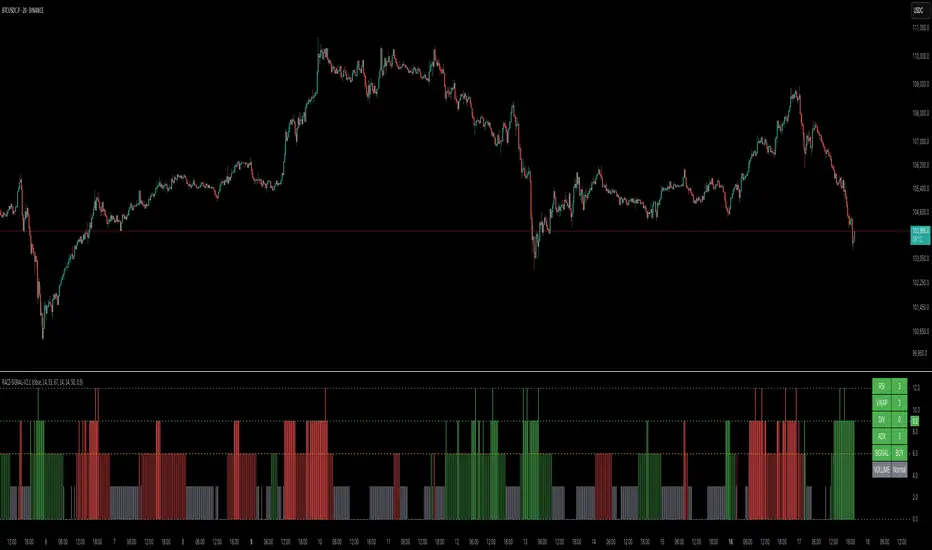

RACZ-SIGNAL-V2.1RACZ-SIGNAL-V2.1 – Reactive Analytical Confluence Zones

Developed by: RACZ Trading

Indicator Type: Multi-Factor Confluence System

Overlay: Off (separate pane)

Purpose: Detect powerful trade opportunities through confluence of technical signals.

⸻

🔍 What is RACZ?

RACZ stands for Reactive Analytical Confluence Zones.

It’s a high-precision trading tool built for traders who rely on multi-signal confirmation, momentum alignment, and market structure awareness.

Rather than relying on a single technical metric, RACZ dynamically combines RSI, VWAP-RSI, Divergence, ADX, and Volume Analytics to produce a composite signal score from 0 to 12 — the higher the score, the stronger the signal.

⸻

🧠 How It Works – Core Components

1. RSI Analysis

• Detects momentum shifts.

• Compares RSI value to overbought (default: 67) and oversold (default: 33) thresholds.

• Adds points to Bullish or Bearish score.

2. VWAP-RSI

• Uses RSI based on VWAP (Volume Weighted Average Price).

• Adds weight to signals influenced by volume-adjusted price movement.

3. Divergence Detection

• Detects potential reversal zones.

• Bullish Divergence: RSI crosses up from low zone.

• Bearish Divergence: RSI crosses down from high zone.

• Strong confluence signal when present.

4. ADX Dynamic Strength Filter

• Custom-calculated ADX (trend strength indicator).

• Uses a dynamic threshold derived from SMA of ADX over a lookback period, scaled by a factor (default 0.9).

• Ensures signals are only validated in strong trend environments.

5. Volume Z-Score

• Detects anomalies in volume behavior.

• Z-score applied to 20-period volume average & deviation.

• Labels spikes, drops, high/low volume conditions.

⸻

📊 Signal Scoring Logic

Each component (RSI, VWAP-RSI, Divergence, ADX) can score up to 3 points each.

• Bullish Score: Total from bullish alignment of each factor.

• Bearish Score: Total from bearish alignment of each factor.

• Signal Power = max(bullish, bearish)

📈 Signal Interpretation

• BUY: Bullish Score > Bearish Score

• SELL: Bearish Score > Bullish Score

• NEUTRAL: Scores are equal

• Signal power is plotted on a 0–12 histogram:

• 0–5 = Weak

• 6–8 = Medium

• 9–12 = Strong (High Confluence Zone)

🖥️ Live Status Panel (Top-Right Corner)

This real-time panel helps you break down the signal:Component

Value Explanation: RSI / VWAP / DIV / ADX

Shows points contributing to signal

SIGNAL: Current market bias (BUY, SELL, NEUTRAL)

VOLUME: Volume classification (Spike, Drop, High, Low, Normal)

Color-coded for quick interpretation.

✅ How to Use

1. Look at Histogram: Bars ≥6 suggest valid setups, especially ≥9.

2. Confirm Panel Agreement: Check which components are supporting the signal.

3. Validate Volume: Unusual spikes/drops often precede strong moves.

4. Follow Direction: Use BUY/SELL signals aligned with signal power and trend.

⸻

⚙️ Customizable Inputs

• RSI period, overbought/oversold levels

• VWAP-RSI period

• ADX period and dynamic threshold settings

• Fully adjustable to fit any trading style

⸻

🚀 Why Choose RACZ?

• Clarity: Scores & signals derived from multiple tools, not just one.

• Confluence Logic: Designed for traders who look for confirmation across indicators.

• Speed: Real-time responsiveness to changing market dynamics.

• Volume Awareness: Integrated volume intelligence gives a deeper edge.

⸻

⚠️ Disclaimer

This indicator is intended strictly for educational and informational purposes only. It is not financial advice and should not be used to make actual investment decisions. Always conduct your own research or consult with a licensed financial advisor before trading or investing. Use of this script is at your own risk.

cd_cisd_market_CxHi Traders,

Overview:

Many traders follow market structure to identify the market direction and seek trade opportunities in line with the trend.

However, markings derived from user-defined inputs can create different structures, depending on personal choices. For instance, choosing a pivot distance of 3 instead of 2 alters the structure, even though the chart remains the same. Ideally, the structure should remain consistent.

"Change in State Delivery" ( CISD ) is a widely accepted concept among traders and is considered a significant indicator of market direction based on the gain/loss of CISD levels.

In this indicator, CISD is selected as the primary criterion for marking market structure, eliminating the influence of user-dependent variations.

Here is a summary of the key logic and rules applied:

• When the price forms a new high/low, that level is only considered a pivot if a CISD has occurred.

• A bullish CISD is always followed by a bearish CISD, and vice versa.

• Pivot points form the internal structure.

• The internal structure is used to interpret the swing structure.

• Probabilities are derived from internal structure patterns.

________________________________________

Details:

How is CISD determined?

As is commonly known:

• When price makes a new high, the opening level of the first candle in the consecutive bullish candle sequence is marked.

• When price makes a new low, the opening of the first candle in the consecutive bearish sequence is marked.

• If there’s only one candle in the sequence, its opening level is used.

In a bullish market, losing a bearish CISD level (i.e., a close below it) or in a bearish market, gaining a bullish CISD level (i.e., a close above it) is interpreted as a potential shift in buyer-seller dominance and a possible market reversal.

________________________________________

How are internal (pivot) levels determined?

• When price closes below a bearish CISD level, the highest candle's high becomes a pivot high (PH).

• When price closes above a bullish CISD level, the lowest candle's low becomes a pivot low (PL).

• If the new PH is above the previous PH, it’s labeled as HH (Higher High); otherwise, LH (Lower High).

• If the new PL is below the previous PL, it’s labeled as LL (Lower Low); otherwise, HL (Higher Low).

________________________________________

Internal Market Structure:

• A series of HHs indicates a bullish internal structure.

• A series of LLs indicates a bearish internal structure.

________________________________________

Swing (Main) Market Structure:

Using internal pivots and previous swing levels, the main market structure is derived.

• A new swing high (SH) requires the price to move above the previous SH.

• A new swing low (SL) requires the price to move below the previous SL.

________________________________________

Probability Calculation:

Pivot levels forming the internal structure are coded as five-element sequences.

There are 64 possible combinations of such sequences made from consecutive PH and PL values.

Each pattern’s frequency from its starting candle is tracked.

To make it more understandable:

For example, after the four-sequence “HH, LL, LH,HL”, either HH or LH might follow.

The table shows the statistical likelihood of both possible outcomes for the most recent four-element sequence on the chart.

________________________________________

How reliable is it?

To assess reliability, results are calculated from the beginning using:

Success Rate (Suc. Rt) = Number of Correct Predictions / Total Predictions

This value is added to the table for reference.

It’s important to note that no statistical outcome guarantees certainty—every result offers a different interpretation. What truly matters is to avoid getting stopped out 😊.

________________________________________

Menu Options:

Show/hide preferences and color selections can be customized via the indicator menu.

________________________________________

What’s Coming in Future Versions?

Features such as FVG (Fair Value Gaps) between swing levels, volume imbalances, order blocks / mitigation blocks, Fibonacci levels, and relevant trade suggestions will be added.

________________________________________

This is a BETA version that I believe will help simplify your market reading. I’d be happy to hear your feedback and suggestions.

Cheerful Trading!

Position Size Calculator v206/17/2025 - Updated to add MGC to list of instruments

Position Size Calculator for Futures Trading

A professional position sizing tool designed specifically for futures traders who want to maintain disciplined risk management. This indicator calculates the optimal number of contracts based on your predefined risk amount and provides instant visual feedback.

Key Features:

• Interactive price selection - simply click on the chart to set entry, stop loss, and take profit levels

• Supports all major futures contracts: ES, NQ, GC, RTY, YM, MNQ, MES with accurate contract specifications

• Customizable risk amount (defaults to $500 but fully adjustable)

• Real-time position size calculations that never exceed your risk tolerance

• Visual risk validation with color-coded header (green = valid risk, red = excessive risk)

• Automatic 2:1 risk/reward ratio calculations

• Compact, non-intrusive table display in top-right corner

• Clean interface with no chart clutter

How to Use:

Select your futures instrument from the dropdown

Set your maximum risk amount (default $500)

Click on the chart to set your Entry Price

Click on the chart to set your Stop Loss Price

Optionally click to set your Take Profit Price

The calculator instantly shows maximum contracts, actual risk, expected profit, and R/R ratio

Risk Management:

The indicator enforces strict risk management by calculating the maximum number of contracts you can trade while staying within your specified risk limit. The header turns green when your trade is within acceptable risk parameters and red when the risk is too high, providing instant visual feedback.

Perfect for day traders, swing traders, and anyone trading futures who wants to maintain consistent position sizing and risk management discipline.

Smarter Money Flow Divergence Detector [PhenLabs]📊 Smarter Money Flow Divergence Detector

Version: PineScript™ v6

📌 Description

SMFD was developed to help give you guys a better ability to “read” what is going on behind the scenes without directly having access to that level of data. SMFD is an enhanced divergence detection indicator that identifies money flow patterns from advanced volume analysis and price action correspondence. The detection portion of this indicator combines intelligent money flow calculations with multi timeframe volume analysis to help you see hidden accumulation and distribution phases before major price movements occur.

The indicator measures institutional trading activity by looking at volume surges, price volume dynamics, and the factors of momentum to construct an overall picture of market sentiment. It’s built to assist traders in identifying high probability entries by identifying if smart money is positioning against price action.

🚀 Points of Innovation

● Advanced Smart Money Flow algorithm with volume spike detection and large trade weighting

● Multi timeframe volume analysis for enhanced institutional activity detection

● Dynamic overbought/oversold zones that adapt to current market conditions

● Enhanced divergence detection with pivot confirmation and strength validation

● Color themes with customizable visual styling options

● Real time institutional bias tracking through accumulation/distribution analysis

🔧 Core Components

● Smart Money Flow Calculation: Combines price momentum, volume expansion, and VWAP analysis

● Institutional Bias Oscillator: Tracks accumulation/distribution patterns with volume pressure analysis

● Enhanced Divergence Engine: Detects bullish/bearish divergences with multiple confirmation factors

● Dynamic Zone Detection: Automatically adjusts overbought/oversold levels based on market volatility

● Volume Pressure Analysis: Measures buying vs selling pressure over configurable periods

● Multi factor Signal System: Generates entries with trend alignment and strength validation

🔥 Key Features

● Smart Money Flow Period: Configurable calculation period for institutional activity detection

● Volume Spike Threshold: Adjustable multiplier for detecting unusual institutional volume

● Large Trade Weight: Emphasis factor for high volume periods in flow calculations

● Pivot Detection: Customizable lookback period for accurate divergence identification

● Signal Sensitivity: Three tier system (Conservative/Medium/Aggressive) for signal generation

● Themes: Four color schemes optimized for different chart backgrounds

🎨 Visualization

● Main Oscillator: Line, Area, or Histogram display styles with dynamic color coding

● Institutional Bias Line: Real time tracking of accumulation/distribution phases

● Dynamic Zones: Adaptive overbought/oversold boundaries with gradient fills

● Divergence Lines: Automatic drawing of bullish/bearish divergence connections

● Entry Signals: Clear BUY/SELL labels with signal strength indicators

● Information Panel: Real time statistics and status updates in customizable positions

📖 Usage Guidelines

Algorithm Settings

● Smart Money Flow Period

○ Default: 20

○ Range: 5-100

○ Description: Controls the calculation period for institutional flow analysis.

Higher values provide smoother signals but reduce responsiveness to recent activity

● Volume Spike Threshold

○ Default: 1.8

○ Range: 1.0-5.0

○ Description: Multiplier for detecting unusual volume activity indicating institutional participation. Higher values require more extreme volume for detection

● Large Trade Weight

○ Default: 2.5

○ Range: 1.5-5.0

○ Description: Weight applied to high volume periods in smart money calculations. Increases emphasis on institutional sized transactions

Divergence Detection

● Pivot Detection Period

○ Default: 12

○ Range: 5-50

○ Description: Bars to analyze for pivot high/low identification.

Affects divergence accuracy and signal frequency

● Minimum Divergence Strength

○ Default: 0.25

○ Range: 0.1-1.0

○ Description: Required price change percentage for valid divergence patterns.

Higher values filter out weaker signals

✅ Best Use Cases

● Trading with intraday to daily timeframes for institutional position identification

● Confirming trend reversals when divergences align with support/resistance levels

● Entry timing in trending markets when institutional bias supports the direction

● Risk management by avoiding trades against strong institutional positioning

● Multi timeframe analysis combining short term signals with longer term bias

⚠️ Limitations

● Requires sufficient volume for accurate institutional detection in low volume markets

● Divergence signals may have false positives during highly volatile news events

● Best performance on liquid markets with consistent institutional participation

● Lagging nature of volume based calculations may delay signal generation

● Effectiveness reduced during low participation holiday periods

💡 What Makes This Unique

● Multi Factor Analysis: Combines volume, price, and momentum for comprehensive institutional detection

● Adaptive Zones: Dynamic overbought/oversold levels that adjust to market conditions

● Volume Intelligence: Advanced algorithms identify institutional sized transactions

● Professional Visualization: Multiple display styles with customizable themes

● Confirmation System: Multiple validation layers reduce false signal generation

🔬 How It Works

1. Volume Analysis Phase:

● Analyzes current volume against historical averages to identify institutional activity

● Applies multi timeframe analysis for enhanced detection accuracy

● Calculates volume pressure through buying vs selling momentum

2. Smart Money Flow Calculation:

● Combines typical price with volume weighted analysis

● Applies institutional trade weighting for high volume periods

● Generates directional flow based on price momentum and volume expansion

3. Divergence Detection Process:

● Identifies pivot highs/lows in both price and indicator values

● Validates divergence strength against minimum threshold requirements

● Confirms signals through multiple technical factors before generation

💡 Note: This indicator works best when combined with proper risk management and position sizing. The institutional bias component helps identify market sentiment shifts, while divergence signals provide specific entry opportunities. For optimal results, use on liquid markets with consistent institutional participation and combine with additional technical analysis methods.

Wyckoff Entry Times @jqrmThis indicator visually marks two custom time zones on your TradingView chart by drawing vertical lines at the start and end of each zone. The first time zone spans from 9:27 AM to 9:33 AM, highlighted in red, and the second spans from 9:50 AM to 10:10 AM, highlighted in blue. You can enable or disable each zone's lines using the indicator inputs. This helps to quickly spot important intraday sessions or time ranges on your chart.

Stephis Supply & Demand Zones v3

📉 Support

Definition: Support is a price level where a downtrend can be expected to pause or reverse due to a concentration of buying interest.

Why it matters: When the price of an asset falls to a support level, traders expect buyers to step in, preventing the price from falling further.

Visual clue: On a chart, support often appears as a horizontal line where the price has bounced up multiple times.

📈 Demand

Definition: Demand refers to the willingness and ability of buyers to purchase an asset at a given price.

In trading context: High demand typically pushes prices up, while low demand can lead to price drops.

Relation to support: A support level exists because of demand—buyers are willing to buy at that price, creating a floor.

🧠 How They Work Together

When price approaches a support level, traders watch to see if demand increases—if it does, the price may bounce.

If the support level is broken, it may signal that demand has weakened, and the price could fall further.

🔁 Opposite Concept: Resistance & Supply

Resistance is the opposite of support—it's a level where selling pressure (supply) may stop a price from rising.

Just like demand creates support, supply creates resistance.

Advanced Volume Profile Levels (Working)This indicator is a powerful tool for traders who use volume profile analysis to identify significant price levels. It automatically calculates and plots the three most critical levels derived from volume data—the Point of Control (POC), Value Area High (VAH), and Value Area Low (VAL)—for three different timeframes simultaneously: the previous week, the previous day, and the current, live session.

The primary focus of this indicator is unmatched readability. It features dynamic, floating labels that stay clear of price action, combined with a high-contrast design to ensure you can see these crucial levels at a glance without any visual clutter.

Key Features

Multi-Session Analysis: Gain a complete market perspective by viewing levels from different timeframes on a single chart.

Weekly Levels: Identify the long-term areas of value and control from the prior week's trading activity.

Daily Levels: Pinpoint the most significant levels from the previous day's Regular Trading Hours (9:30 AM - 4:00 PM ET).

Current Session Levels: Track the developing value area and POC in real-time with a dynamic profile that updates with every bar.

Advanced Visuals for Clarity:

Floating Labels: The labels for the weekly and daily levels intelligently "float" on the right side of your chart, moving with the price to ensure they are never obscured by candles.

High-Contrast Design: Labels are designed for maximum readability with solid, opaque backgrounds and an automatic text color (black or white) that provides the best contrast against your chosen level color.

Trailing Current Levels: The labels for the current session neatly trail the most recent price action, providing an intuitive view of intra-day developments.

Comprehensive Customization: Tailor the indicator's appearance to your exact preferences.

Toggle each profile (Weekly, Daily, Current) on or off.

Individually set the color, line style (solid, dashed, dotted), and line width for each set of levels.

Adjust the text size, background transparency, and horizontal offset for all on-chart labels.

Information Hub:

On-Chart Price Labels: Each label clearly displays both the level name and its precise price (e.g., "D-POC: 22068.50").

Corner Table: An optional, clean table in the top-right corner provides a quick summary of all active weekly and daily level values.

Built-in Alerts:

Create alerts directly from the script to be notified whenever the price crosses above or below the weekly or daily Point of Control, helping you stay on top of key market movements.

How to Use

The levels provided by this indicator serve as powerful reference points for market activity:

Point of Control (POC): The price level with the highest traded volume. It acts as a magnet for price and represents the area of "fair value" for that session. Markets often test or revert to the POC.

Value Area High (VAH) & Value Area Low (VAL): These levels define the range where approximately 70% of the session's volume occurred. They are critical support and resistance zones.

Price acceptance above the VAH may signal a bullish breakout.

Price acceptance below the VAL may signal a bearish breakdown.

Rejection at the VAH or VAL often leads to price moving back across the value area towards the POC.

Daily ATR TrackerDaily ATR Tracker

The Daily ATR Tracker is a simple yet powerful tool designed to help traders monitor the daily price movement relative to the average daily range (ATR). This indicator provides an objective view of how much price has moved compared to its recent daily volatility.

🔎 Key Features:

Customizable ATR period (default 14 days)

Live calculation of the current day's price range

ATR value displayed in pips for clear reference

Percentage of ATR covered by the current day's range

Color-coded table for quick visual interpretation:

🟢 Green: less than 60% of ATR covered

🟠 Orange: 60% to 100% of ATR covered

🔴 Red: more than 100% of ATR covered

Alert condition when daily range exceeds 100% of the ATR average

Movable table position to fit your chart layout

🎯 Why use Daily ATR Tracker?

✅ Identify exhaustion zones: When price has already covered a large portion of its typical daily range, the odds of further strong movement may diminish, helping you to manage entries, exits, and risk.

✅ Objective daily bias: Get a quantitative sense of how "stretched" the market is in real time.

✅ Works with any timeframe: While designed for daily ranges, you can monitor intraday movements with this context in mind.

⚠️ Usage Note:

This tool does not provide buy or sell signals by itself. It is designed to complement your existing strategies by offering additional context regarding daily range exhaustion.

Trend Blend

Trend blend is my new indicator. I use it to identify my bias when trading and filter out fake setups that are going in the wrong direction.

Trend blend utilises the 9 EMA (Red), 21 EMA (Black), and if you trade futures or Bitcoin, you can also use the VWAP (Blue).

There is also a table at the top right that displays the chart time frame bias

I prefer to use the 1-hour time frame for bias and execute the trades on 5-minute charts, mainly, and sometimes on the 1-minute for a smaller stoploss.

Here's an example of the trade I took during the London session on XAU/USD

1 hour bias was Bearish

Price broke out of the range

I waited for the London session to open, where I ended up taking a short on the 5-minute time frame as we broke out of the pre-London range

Entry was at the Fair Value Gap (5-minute bias was also Bearish as price traded into the FVG)

Stoploss was at the last high

Take Profit was the next major support level

Another set that I like to trade with the Trend blend is when price is trending bullish and price trades inside the 9 and 21 EMA, and there is a bullish candle closer above the 9 EMA with Stoploss below the low of the bullish candle and Take profit between 1-2 Risk to Reward

Same when there's a bearish trend, I wait for price to trade inside the 9 and 21 EMA, and I'll take sells when a bearish candle closes below the 9 EMA.

This setup works best in strong trends, or it can be used to enter a trade on a pullback or to scale into an existing trade.

Rolling Z-Score Trend [QuantAlgo]🟢 Overview

The Rolling Z-Score Trend measures how far the current price deviates from its rolling mean in terms of standard deviations. It transforms price data into standardized scores to identify overbought and oversold conditions while tracking momentum shifts.

The indicator displays a Z-Score line showing price deviation from statistical norms, with background momentum columns showing the rate of change in these deviations. This helps traders and investors identify mean reversion opportunities and momentum shifts across different asset classes and timeframes.

🟢 How It Works

The indicator uses the Z-Score formula: Z = (X - μ) / σ, where X is the current closing price, μ is the rolling mean, and σ is the rolling standard deviation over a user-defined lookback period. This creates a dynamic baseline that adapts to changing market conditions and standardizes price movements for interpretation across different assets and volatility conditions. The raw Z-Score undergoes 3-period EMA smoothing to reduce noise while maintaining responsiveness to market signals.

Beyond the basic Z-Score calculation, the indicator measures the rate of change in Z-Score values between successive bars, displayed as background momentum columns. This momentum component shows acceleration and deceleration of statistical deviations. All calculations are processed through confirmation filters, displaying signals only on confirmed bars to reduce premature signals based on incomplete price action.

🟢 How to Use

1. Z-Score Interpretation and Threshold Zones

Positive Values (Above Zero) : Price trading above statistical mean, suggesting bullish momentum or potential overbought conditions

Negative Values (Below Zero) : Price trading below statistical mean, suggesting bearish momentum or potential oversold conditions

Zero Line Crosses : Signal transitions between statistical regimes and potential trend changes

Upper Threshold Zone : Area above entry threshold (default 1.5) indicating potential overbought conditions

Lower Threshold Zone : Area below negative entry threshold (default -1.5) indicating potential oversold conditions

Extreme Values (±2.0 or higher) : Statistically significant deviations that may indicate reversal opportunities

2. Momentum Background Analysis and Info Table

Green Columns : Accelerating positive momentum in Z-Score values

Red Columns : Accelerating negative momentum in Z-Score values

Column Height : Magnitude of momentum change between bars

Momentum Divergence : When columns contradict primary Z-Score direction, often signals impending reversals

Info Table : Displays real-time numerical values for both Z-Score and momentum, including trend direction indicators and bar-to-bar change calculations for position management

3. Preconfigured Settings

Default : Balanced performance across multiple timeframes and asset classes for general trading and medium-term position management.

Scalping : Responsive setup for ultra-short-term trading on 1-15 minute charts with frequent signals and increased sensitivity to quick price movements.

Swing Trading : Optimized for multi-day positions with noise filtering, focusing on larger price swings. Most effective on 1-4 hour and daily timeframes.

Trend Following : Maximum smoothing that prioritizes established trends over short-term volatility. Generates fewer signals for daily and weekly charts.

PulseMA + MADescription

The PulseMA + MA indicator is an analytical tool that combines the analysis of the price relationship to a base Exponential Moving Average (EMA) with a smoothed Simple Moving Average (SMA) of this relationship. The indicator helps traders identify the direction and momentum of market trends and generates entry signals, displaying data as lines below the price chart.

Key Features

PulseMA: Calculates trend momentum by multiplying the number of consecutive candles above or below the base EMA by the slope of this average. The number of candles determines trend strength (positive for an uptrend, negative for a downtrend), while the EMA slope reflects the rate of change of the average. The PulseMA value is scaled by multiplying by 100.

Smoothed Average (PulseMA MA): Adds a smoothed SMA, facilitating the identification of long-term changes in market momentum.

Dynamic Colors: The PulseMA line changes color based on the price position relative to the base EMA (green for price above, red for price below).

Zero Line: Indicates the area where the price is close to the base EMA.

Applications

The PulseMA + MA indicator is designed for traders and technical analysts who aim to:

Analyze the direction and momentum of market trends, particularly with higher PulseMA Length values (e.g., 100), which provide a less sensitive EMA for longer-term trends.

Generate entry signals based on the PulseMA color change or the crossover of PulseMA with PulseMA MA.

Anticipate potential price reversals to the zero line when PulseMA is significantly distant from it, which may indicate market overextension.

How to Use

Add the Indicator to the Chart: Search for "PulseMA + MA" in the indicator library and add it to your chart.

Adjust Parameters:

PulseMA Length: Length of the base EMA (default: 50).

PulseMA Smoothing Length: Length of the smoothed SMA (default: 20).

Interpretation:

Green PulseMA Line: Price is above the base EMA, suggesting an uptrend.

Red PulseMA Line: Price is below the base EMA, indicating a downtrend.

PulseMA Color Change: May signal an entry point (recommended to wait for 2 candles to reduce noise).

PulseMA Crossing PulseMA MA from Below: May indicate a buy signal in an uptrend.

Zero Line: Indicates the area where the price is close to the base EMA.

Significant Deviation of PulseMA from the Zero Line: Suggests a potential price reversal to the zero line, indicating possible market overextension.

Notes

The indicator generates trend signals and can be used to independently identify entry points, e.g., on PulseMA color changes (waiting 2 candles is recommended to reduce noise) or when PulseMA crosses PulseMA MA from below.

In sideways markets, it is advisable to use the indicator with a volatility filter to limit false signals.

Adjusting the lengths of the averages to suit the specific instrument can improve signal accuracy.

True High/Low RSI for DivergenceThis Pine Script creates a highly specialized RSI (Relative Strength Index) indicator designed to provide a more accurate signal for divergence trading. Its official title is "True High/Low RSI for Divergence."

Here is a breakdown of its core features:

1. Dual RSI Calculation based on Highs and Lows:

Unlike a standard RSI that typically uses the closing price of a candle, this indicator calculates two separate RSI lines:

A "High RSI" : This line calculates the RSI based on the high price of each candle. It is intended to track momentum peaks more accurately.

A "Low RSI" : This line calculates the RSI based on the low price of each candle. It is designed to track momentum troughs more accurately.

The main purpose of this separation is to avoid the potential errors that can occur when using an average price (like the close or hl2) during periods of high volatility. By using the true extremes of the price candles, the indicator aims to show a more "true" representation of momentum for identifying divergences between price and the indicator.

2. Dynamic Transparency:

This is a key visual feature. The RSI lines are not always fully visible. They dynamically fade into view as they enter significant overbought or oversold zones:

The Low RSI line (red by default) is invisible when above a value of 50. As it drops from 49 towards 30, it becomes progressively more opaque (more visible). It reaches full opacity at an RSI value of 30, visually alerting the user to strengthening oversold conditions.

The High RSI line (blue by default) is invisible when below a value of 50. As it rises from 51 towards 70, it also becomes progressively more opaque. It is fully opaque at an RSI value of 70, highlighting strengthening overbought conditions.

3. User Customization:

The script allows for user flexibility. You can change:

The colors for both the High and Low RSI lines.

The RSI calculation length (default is 14).

The price source for each RSI line (though they are specifically designed to use high and low).

In summary, this indicator is a purpose-built tool for traders who rely on divergence. It provides a more precise and visually intuitive way to track momentum at its true peaks and troughs, helping to make more informed trading decisions.

SMT DivergenceSMT Divergence Indicator

This powerful indicator identifies high-probability reversal points by detecting SMT (Smart Money Technique) divergences between two correlated assets. It spots subtle shifts in market momentum, revealing when one asset fails to confirm the price action of another—often signaling an impending trend change.

Key Features:

Inter-Market Divergence Detection: Automatically compares the price action of the main symbol with a second user-defined asset.

Identifies Key Reversals: Pinpoints both bullish and bearish SMT divergences, highlighting hidden strength in downtrends and underlying weakness in uptrends.

Customizable Pivot Detection: Allows fine-tuning of the pivot length to adjust sensitivity for different market conditions and timeframes.

Flexible Display Modes: Choose between clean 'Lines' connecting the diverging pivots or precise 'Labels' marking the exact high/low points.

Full Visual Customization: Complete control over the colors and line thickness for seamless integration with your existing chart layout.

Built-in Alerts: Stay notified of every potential opportunity with alerts for both bullish and bearish signals.

Settings:

Core Parameters:

Comparison Symbol: Select the second asset to compare against for divergence analysis (e.g., NQ1! if you are charting ES1!).

Pivot Length: Defines the number of bars to the left and right required to confirm a pivot high or low.

Visual Settings:

Display Style: Choose to visualize divergences as 'Lines' or 'Labels'.

Bearish/Bullish Color: Set custom colors for bearish and bullish divergence indicators.

Line Width: Adjust the thickness of the divergence lines for optimal visibility.

Perfect for traders who utilize inter-market analysis to confirm trade ideas. The SMT Divergence indicator provides a crucial edge by exposing non-confirmations between related assets, allowing for earlier and more confident entries into potential market reversals.

Big Move Follow-Through Tracker🚀 What This Indicator Does

Ever wondered if that sudden 5% pump in your favorite crypto will continue or just fade away? This powerful indicator automatically tracks every significant price move and tells you exactly what happened next - momentum continuation or mean reversion.

🎯 Key Features

📊 Smart Move Detection

Automatically identifies "big moves" based on your custom threshold (default 3%)

Uses ATR filtering to ensure moves are truly significant, not just normal volatility

Works on ANY timeframe and ANY crypto pair

🔍 Follow-Through Analysis

Tracks each big move for your specified number of bars (default 5)

Classifies outcomes as either Follow-Through (momentum continues) or Mean Reversion (price reverses)

Uses intelligent 2% thresholds to avoid noise and focus on meaningful moves

📈 Real-Time Statistics Dashboard

Live statistics table showing historical performance

Separate analysis for UP moves vs DOWN moves (crypto often behaves differently!)

Percentage breakdowns of follow-through vs reversion rates

Track total moves detected vs analyzed over time

🎨 Visual Clarity

Clear arrow signals when big moves are detected

Background highlighting during significant moves

Customizable display options - show/hide signals and stats as needed

🛠️ How to Use

Add to any crypto chart (works on BTC, ETH, altcoins, etc.)

Adjust the move threshold (3% for major coins, higher for smaller caps)

Set analysis timeframe (how many bars to track each move)

Watch the statistics build over time to understand your asset's behavior

💡 Trading Applications

For Momentum Traders:

High follow-through rates? → Consider riding the momentum

Trade in direction of big moves when statistics support it

For Mean Reversion Traders:

High reversion rates? → Look for fade opportunities

Counter-trade big moves when they historically reverse

For Risk Management:

Understand typical behavior after significant moves

Size positions based on historical follow-through probabilities

📋 Customizable Settings

Big Move Threshold: Adjust sensitivity (0.5% - 10%)

Analysis Period: How long to track each move (3-20 bars)

Display Options: Toggle signals and statistics table

Alert System: Get notified when big moves occur

🎲 What Makes This Different

Unlike simple momentum indicators, this tool:

✅ Quantifies actual outcomes with real statistics

✅ Adapts to each asset's unique volatility profile

✅ Separates up and down move behavior

✅ Provides actionable probability data

📊 Perfect For

Crypto day traders looking for edge identification

Swing traders wanting to understand momentum vs reversion tendencies

Risk managers needing probability-based position sizing

Strategy developers building data-driven trading systems

⚡ Quick Setup Tips

For Major Cryptos (BTC, ETH): Use 2-4% threshold

For Altcoins: Use 4-8% threshold

For Scalping: Use lower timeframes with 1-2% threshold

For Swing Trading: Use higher timeframes with 5%+ threshold

Yelober_Momentum_BreadthMI# Yelober_Momentum_BreadthMI: Market Breadth Indicator Analysis

## Overview

The Yelober_Momentum_BreadthMI is a comprehensive market breadth indicator designed to monitor market internals across NYSE and NASDAQ exchanges. It tracks several key metrics including up/down volume ratios, TICK readings, and trend momentum to provide traders with real-time insights into market direction, strength, and potential turning points.

## Indicator Components

This indicator displays a table with data for:

- NYSE breadth metrics

- NASDAQ breadth metrics

- NYSE TICK data and trends

- NASDAQ TICK (TICKQ) data and trends

## Table Columns and Interpretation

### Column 1: Market

Identifies the data source:

- **NYSE**: New York Stock Exchange data

- **NASDAQ**: NASDAQ exchange data

- **Tick**: NYSE TICK index

- **TickQ**: NASDAQ TICK index

### Column 2: Ratio

Shows the current ratio values with different calculations depending on the row:

- **For NYSE/NASDAQ rows**: Displays the up/down volume ratio

- Positive values (green): More up volume than down volume

- Negative values (red): More down volume than up volume

- The magnitude indicates the strength of the imbalance

- **For Tick/TickQ rows**: Shows the ratio of positive to negative ticks plus the current TICK reading in parentheses

- Format: "Ratio (Current TICK value)"

- Positive values (green): More stocks ticking up than down

- Negative values (red): More stocks ticking down than up

### Column 3: Trend

Displays the directional trend with both a symbol and value:

- **For NYSE/NASDAQ rows**: Shows the VOLD (volume difference) slope

- "↗": Rising trend (positive slope)

- "↘": Falling trend (negative slope)

- "→": Neutral/flat trend (minimal slope)

- **For Tick/TickQ rows**: Shows the slope of the ratio history

- Color-coding: Green for positive momentum, Red for negative momentum, Gray for neutral

The trend column is particularly important as it shows the current momentum of the market. The indicator applies specific thresholds for color-coding:

- NYSE: Green when normalized value > 2, Red when < -2

- NASDAQ: Green when normalized value > 3.5, Red when < -3.5

- TICK/TICKQ: Green when slope > 0.01, Red when slope < -0.01

## How to Use This Indicator

### Basic Interpretation

1. **Market Direction**: When multiple rows show green ratios and upward trends, it suggests strong bullish market internals. Conversely, red ratios and downward trends indicate bearish internals.

2. **Market Breadth**: The magnitude of the ratios indicates how broad-based the market movement is. Higher absolute values suggest stronger market breadth.

3. **Momentum Shifts**: When trend arrows change direction or colors shift, it may signal a potential reversal or change in market momentum.

4. **Divergences**: Look for divergences between different markets (NYSE vs NASDAQ) or between ratios and trends, which can indicate potential market turning points.

### Advanced Usage

- **Volume Normalization**: The indicator includes options to normalize volume data (none, tens, thousands, millions, 10th millions) to handle different exchange scales.

- **Trend Averaging**: The slope calculation uses an averaging period (default: 5) to smooth out noise and identify more reliable trend signals.

## Examples for Interpretation

### Example 1: Strong Bullish Market

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 1.75 | ↗ 2.85 |

| NASDAQ | 2.10 | ↗ 4.12 |

| Tick | 2.45 (485) | ↗ 0.05 |

| TickQ | 1.95 (320) | ↗ 0.03 |

```

**Interpretation**: All metrics are positive and trending upward (green), indicating a strong, broad-based rally. The high ratio values show significant bullish dominance. This suggests continuation of the upward move with good momentum.

### Example 2: Weakening Market

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 0.45 | ↘ -1.50 |

| NASDAQ | 0.85 | → 0.30 |

| Tick | 0.95 (105) | ↘ -0.02 |

| TickQ | 1.20 (160) | → 0.00 |

```

**Interpretation**: The market is showing mixed signals with positive but low ratios, while NYSE and TICK trends are turning negative. NASDAQ shows neutral to slightly positive momentum. This divergence often occurs near market tops or during consolidation phases. Traders should be cautious and consider reducing position sizes.

### Example 3: Negative Market Turning Positive

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | -1.25 | ↗ 1.75 |

| NASDAQ | -0.95 | ↗ 2.80 |

| Tick | -1.35 (-250) | ↗ 0.04 |

| TickQ | -1.10 (-180) | ↗ 0.02 |

```

**Interpretation**: This is a potential bottoming pattern. Current ratios are still negative (red) showing overall negative breadth, but the trends are all positive (green arrows), indicating improving momentum. This divergence often occurs at market bottoms and could signal an upcoming reversal. Look for confirmation with price action before establishing long positions.

### Example 4: Mixed Market with Divergence

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 1.45 | ↘ -2.25 |

| NASDAQ | -0.85 | ↘ -3.80 |

| Tick | 1.20 (230) | ↘ -0.03 |

| TickQ | -0.75 (-120) | ↘ -0.02 |

```

**Interpretation**: There's a significant divergence between NYSE (positive ratio) and NASDAQ (negative ratio), while all trends are negative. This suggests sector rotation or a market that's weakening but with certain segments still showing strength. Often seen during late-stage bull markets or in transitions between leadership groups. Consider reducing risk exposure and focusing on relative strength sectors.

## Practical Trading Applications

1. **Confirmation Tool**: Use this indicator to confirm price movements. Strong breadth readings in the direction of the price trend increase confidence in trade decisions.

2. **Early Warning System**: Watch for divergences between price and breadth metrics, which often precede market turns.

3. **Intraday Trading**: The real-time nature of TICK and volume data makes this indicator valuable for day traders to gauge intraday momentum shifts.

4. **Market Regime Identification**: Sustained readings can help identify whether the market is in a trend or chop regime, allowing for appropriate strategy selection.

This breadth indicator is most effective when used in conjunction with price action and other technical indicators rather than in isolation.

Yelober - Sector Rotation Detector# Yelober - Sector Rotation Detector: User Guide

## Overview

The Yelober - Sector Rotation Detector is a TradingView indicator designed to track sector performance and identify market rotations in real-time. It monitors key sector ETFs, calculates performance metrics, and provides actionable stock recommendations based on sector strength and weakness.

## Purpose

This indicator helps traders identify when capital is moving from one sector to another (sector rotation), which can provide valuable trading opportunities. It also detects risk-off conditions in the market and highlights sectors with abnormal trading volume.

## Table Columns Explained

### 1. Sector

Displays the sector name being monitored. The indicator tracks six primary sectors plus the S&P 500:

- Energy (XLE)

- Financial (XLF)

- Technology (XLK)

- Consumer Staples (XLP)

- Utilities (XLU)

- Consumer Discretionary (XLY)

- S&P 500 (SPY)

### 2. Perf %

Shows the daily percentage performance of each sector ETF. Values are color-coded:

- Green: Positive performance

- Red: Negative performance

Positive values display with a "+" sign (e.g., +1.25%)

### 3. RSI

Displays the Relative Strength Index value for each sector, which helps identify overbought or oversold conditions:

- Values above 70 (highlighted in red): Potentially overbought

- Values below 30 (highlighted in green): Potentially oversold

- Values between 30-70 (highlighted in blue): Neutral territory

### 4. Vol Ratio

Shows the volume ratio, which compares today's volume to the average volume over the lookback period:

- Values above 1.5x (highlighted in yellow): Indicates abnormally high trading volume

- Values below 1.5x (highlighted in blue): Normal trading volume

This helps identify sectors with unusual activity that may signal important price movements.

### 5. Trend

Displays the current price trend direction with symbols:

- ▲ (green): Uptrend (today's close > yesterday's close)

- ▼ (red): Downtrend (today's close < yesterday's close)

- ◆ (gray): Neutral (today's close = yesterday's close)

## Summary & Recommendations Section

The summary section provides:

1. **Sector Rotation Detection**: Identifies when there's a significant performance gap (>2%) between the strongest and weakest sectors.

2. **Risk-Off Mode Detection**: Alerts when defensive sectors (Consumer Staples and Utilities) are positive while Technology is negative, which often signals investors are moving to safer assets.

3. **Strong Volume Detection**: Indicates when any sector shows abnormally high trading volume.

4. **Stock Recommendations**: Suggests specific stocks to consider for long positions (from the strongest sectors) and short positions (from the weakest sectors).

## Example Interpretations

### Example 1: Sector Rotation

If you see:

- Technology: -1.85%

- Financial: +2.10%

- Summary shows: "SECTOR ROTATION DETECTED: Rotation from Technology to Financial"

**Interpretation**: Capital is moving out of tech stocks and into financial stocks. This could be due to rising interest rates, which typically benefit banks while pressuring high-growth tech companies. Consider looking at financial stocks like JPM, BAC, and WFC for potential long positions.

### Example 2: Risk-Off Conditions

If you see:

- Consumer Staples: +0.80%

- Utilities: +1.20%

- Technology: -1.50%

- Summary shows: "RISK-OFF MODE DETECTED"

**Interpretation**: Investors are seeking safety in defensive sectors while selling growth-oriented tech stocks. This often occurs during market uncertainty or ahead of economic concerns. Consider reducing exposure to high-beta stocks and possibly adding defensive names like PG, KO, or NEE.

### Example 3: Volume Spike

If you see:

- Energy: +3.20% with Volume Ratio 2.5x (highlighted in yellow)

- Summary shows: "STRONG VOLUME DETECTED"

**Interpretation**: The energy sector is making a strong move with significantly higher-than-average volume, suggesting conviction behind the price movement. This could indicate the beginning of a sustained trend in energy stocks. Consider names like XOM, CVX, and COP.

## How to Use the Indicator

1. Apply the indicator to any chart (works best on daily timeframes).

2. Customize settings if needed:

- Timeframe: Choose between intraday (60 or 240 minutes), daily, or weekly

- Lookback Period: Adjust the historical comparison period (default: 20)

- RSI Period: Modify the RSI calculation period (default: 14)

3. To refresh the data: Click the settings icon, increase the "Click + to refresh data" counter, and click "OK".

4. Identify opportunities based on sector performance, RSI levels, volume ratios, and the summary recommendations.

This indicator helps traders align with market rotation trends and identify which sectors (and specific stocks) may outperform or underperform in the near term.

The Butterfly [theUltimator5]This is a technical analysis tool designed to automatically detect and visualize Butterfly harmonic patterns based on recent market pivot structures. This indicator uses a unique plotting and detection algorithm to find and display valid Butterfly patterns on the chart.

The indicator works in real-time and historically by identifying major swing highs and lows (pivots) based on a user-defined ZigZag length. It then evaluates whether the most recent price structure conforms to the ideal proportions of a bullish or bearish Butterfly pattern. If the ratios between price legs XA, AB, BC, and projected CD meet defined tolerances, the pattern is plotted on the chart along with a projected D point for potential reversal.

Key Features:

Automatic Pivot Detection: The script analyzes recent price action to construct a ZigZag pattern, identifying swing points as potential X, A, B, and C coordinates.

Butterfly Pattern Validation: The pattern is validated against traditional Fibonacci ratios:

--AB should be approximately 78.6% of XA.

--BC must lie between 38.2% and 88.6% of AB.

--CD is projected as a multiple of BC, with user control over the ratio (e.g., 1.618–2.24).

Bullish and Bearish Recognition: The pattern logic detects both bullish and bearish Butterflies, automatically adjusting plotting direction and color themes.

Custom Ratio Tolerance: Users can define how strictly the AB/XA and BC/AB legs must adhere to ideal ratios, using a percentage-based tolerance slider.

Fallback Detection Logic: If a new pattern is not identified in recent bars, the script performs a backward search on the last four pivots to find the most recent valid pattern.

Force Mode: A toggle allows users to force the drawing of a Butterfly pattern on the most recent pivot structure, regardless of whether the ideal Fibonacci rules are satisfied.

Dynamic Visualization:

--Clear labeling of X, A, B, C, and D points.

--Colored connecting lines and filled triangles to visualize structure.

--Optional table displaying key Fibonacci ratios and how close each leg is to ideal values.

Inputs:

Length: Controls the sensitivity of the ZigZag pivots. Smaller values result in more frequent pivots.

Tolerance (%): Adjustable threshold for acceptable deviation in AB/XA and BC/AB ratios.

CD Length Multiplier: Projects point D by multiplying the BC leg using a value between 1.618 and 2.24.

Force New Pattern: Overrides validation checks to display a Butterfly structure on recent pivots regardless of ratio accuracy.

Show Table: Enables a table showing calculated ratios and deviations from the ideal.

MC Geopolitical Tension Events📌 Script Title: Geopolitical Tension Events

📖 Description:

This script highlights key geopolitical and military tension events from 1914 to 2024 that have historically impacted global markets.

It automatically plots vertical dashed lines and labels on the chart at the time of each major event. This allows traders and analysts to visually assess how markets have responded to global crises, wars, and significant political instability over time.

🧠 Use Cases:

Historical backtesting: Understand how market responded to past geopolitical shocks.

Contextual analysis: Add macro context to technical setups.

🗓️ List of Geopolitical Tension Events in the Script

Date Event Title Description

1914-07-28 WWI Begins Outbreak of World War I following the assassination of Archduke Franz Ferdinand.

1929-10-24 Wall Street Crash Black Thursday, the start of the 1929 stock market crash.

1939-09-01 WWII Begins Germany invades Poland, starting World War II.

1941-12-07 Pearl Harbor Japanese attack on Pearl Harbor; U.S. enters WWII.

1945-08-06 Hiroshima Bombing First atomic bomb dropped on Hiroshima by the U.S.

1950-06-25 Korean War Begins North Korea invades South Korea.

1962-10-16 Cuban Missile Crisis 13-day standoff between the U.S. and USSR over missiles in Cuba.

1973-10-06 Yom Kippur War Egypt and Syria launch surprise attack on Israel.

1979-11-04 Iran Hostage Crisis U.S. Embassy in Tehran seized; 52 hostages taken.

1990-08-02 Gulf War Begins Iraq invades Kuwait, triggering U.S. intervention.

2001-09-11 9/11 Attacks Coordinated terrorist attacks on the U.S.

2003-03-20 Iraq War Begins U.S.-led invasion of Iraq to remove Saddam Hussein.

2008-09-15 Lehman Collapse Bankruptcy of Lehman Brothers; peak of global financial crisis.

2014-03-01 Crimea Crisis Russia annexes Crimea from Ukraine.

2020-01-03 Soleimani Strike U.S. drone strike kills Iranian General Qasem Soleimani.

2022-02-24 Ukraine Invasion Russia launches full-scale invasion of Ukraine.

2023-10-07 Hamas-Israel War Hamas launches attack on Israel, sparking war in Gaza.

2024-01-12 Red Sea Crisis Houthis attack ships in Red Sea, prompting Western naval response.