Frahm Factor Position Size CalculatorThe Frahm Factor Position Size Calculator is a powerful evolution of the original Frahm Factor script, leveraging its volatility analysis to dynamically adjust trading risk. This Pine Script for TradingView uses the Frahm Factor’s volatility score (1-10) to set risk percentages (1.75% to 5%) for both Margin-Based and Equity-Based position sizing. A compact table on the main chart displays Risk per Trade, Frahm Factor, and Average Candle Size, making it an essential tool for traders aligning risk with market conditions.

Calculates a volatility score (1-10) using true range percentile rank over a customizable look-back window (default 24 hours).

Dynamically sets risk percentage based on volatility:

Low volatility (score ≤ 3): 5% risk for bolder trades.

High volatility (score ≥ 8): 1.75% risk for caution.

Medium volatility (score 4-7): Smoothly interpolated (e.g., 4 → 4.3%, 5 → 3.6%).

Adjustable sensitivity via Frahm Scale Multiplier (default 9) for tailored volatility response.

Position Sizing:

Margin-Based: Risk as a percentage of total margin (e.g., $175 for 1.75% of $10,000 at high volatility).

Equity-Based: Risk as a percentage of (equity - minimum balance) (e.g., $175 for 1.75% of ($15,000 - $5,000)).

Compact 1-3 row table shows:

Risk per Trade with Frahm score (e.g., “$175.00 (Frahm: 8)”).

Frahm Factor (e.g., “Frahm Factor: 8”).

Average Candle Size (e.g., “Avg Candle: 50 t”).

Toggles to show/hide Frahm Factor and Average Candle Size rows, with no empty backgrounds.

Four sizes: XL (18x7, large text), L (13x6, normal), M (9x5, small, default), S (8x4, tiny).

Repositionable (9 positions, default: top-right).

Customizable cell color, text color, and transparency.

Set Frahm Factor:

Frahm Window (hrs): Pick how far back to measure volatility (e.g., 24 hours). Shorter for fast markets, longer for chill ones.

Frahm Scale Multiplier: Set sensitivity (1-10, default 9). Higher makes the score jumpier; lower smooths it out.

Set Margin-Based:

Total Margin: Enter your account balance (e.g., $10,000). Risk auto-adjusts via Frahm Factor.

Set Equity-Based:

Total Equity: Enter your total account balance (e.g., $15,000).

Minimum Balance: Set to the lowest your account can go before liquidation (e.g., $5,000). Risk is based on the difference, auto-adjusted by Frahm Factor.

Customize Display:

Calculation Method: Pick Margin-Based or Equity-Based.

Table Position: Choose where the table sits (e.g., top_right).

Table Size: Select XL, L, M, or S (default M, small text).

Table Cell Color: Set background color (default blue).

Table Text Color: Set text color (default white).

Table Cell Transparency: Adjust transparency (0 = solid, 100 = invisible, default 80).

Show Frahm Factor & Show Avg Candle Size: Check to show these rows, uncheck to hide (default on).

Indicators and strategies

Wyckoff Smart Signals (Long + Short)- Wycoff Smart signals made by Melik

Using Wycoff fundamentals and volume confirmation to form a bias

Position Size CalculatorIt calculates the risk per trade using two methods: Margin-Based (percentage of total Account Balance) or Equity-Based (percentage of Total Balance minus minimum balance). Displayed as a compact, customizable label on the main chart, it’s perfect for traders seeking quick, precise risk calculations.

Key Features

Two Calculation Options:

Margin-Based: Risk as a percentage (0-5%) of your total account balance.

Equity-Based: Risk as a percentage (0-50%) of (Total balance - Minimum balance).

Flexible Risk Input: Manually enter any risk percentage with 0.01% precision (e.g., 1.75%).

Customizable Display:

Repositionable table (9 positions, e.g., top-right, middle-center).

Four table sizes (XL, L, M, S) with text scaling (large, normal, small, tiny).

Adjustable cell color, text color, and transparency

Margin-Based Risk Calculation:

Set “Total Margin” (e.g., $10,000).

Enter “Risk Percentage (%)” (0 to 5%, e.g., 1.75%).

Equity-Based Risk Calculation:

Set “Total Equity” (e.g., $15,000).

Set “Minimum Balance” (e.g., $5,000).

Enter “Equity Risk Percentage (%)” (0 to 50%, e.g., 1.75%).

Display Settings:

Choose “Calculation Method” (Margin-Based or Equity-Based).

Select “Table Position” (e.g., top_right).

Select “Table Size” (XL, L, M, S; default M).

Customize “Table Cell Color”, “Table Text Color”, and “Table Cell Transparency”.

MVWAP 5/21/50 + LWMA 400Moving vwap de 5,21,50 y media movil ponderada de 400

se puede utilizar con cruces

Gattsreal EMASummary

The Gattsreal EMA indicator is a complete technical analysis tool designed to provide a clear and immediate view of the market trend and momentum across multiple timeframes. It combines long-term Exponential Moving Averages (EMAs) with a short-term EMA "ribbon," allowing traders to quickly identify the direction of the main trend and the strength of short-term movements.

Indicator Components

The Gattsreal EMA is composed of two main elements, both fully customizable:

Long-Term EMAs (Thick Lines):

EMA 200 (White): Considered the definitive line between a bull market and a bear market. Prices above the 200 EMA are generally considered to be in a long-term uptrend.

EMA 50 (Blue): An important medium-term trend line, often used as a dynamic level of support or resistance.

Short-Term EMA Ribbon:

Consists of a set of 9 EMAs (periods 9, 10, 15, 20, 25, 30, 35, 40, and 45).

The "ribbon" expands when volatility increases and contracts when volatility decreases.

The color of the ribbon's fill changes to indicate short-term momentum:

Green: The ribbon is in an uptrend (fastest EMA above the slowest), suggesting buying pressure.

Red: The ribbon is in a downtrend (fastest EMA below the slowest), suggesting selling pressure.

How to Use the Indicator

The Gattsreal EMA can be used in various ways to enhance your analysis and decision-making:

Main Trend Identification: The price's position relative to the 200 and 50 EMAs helps define your operational bias. It is preferable to trade in the direction of the main trend.

Entry and Exit Signals: The crossing of the price through the EMA ribbon can be used as a signal. For example, when the price crosses and closes above the entire ribbon and it turns green, it can be a buy signal.

Momentum Confirmation: The color and expansion of the ribbon serve as excellent confirmation of the strength of a move. A green and expanding ribbon confirms strong bullish momentum.

Dynamic Support and Resistance: All 11 EMAs can act as dynamic levels of support (in an uptrend) or resistance (in a downtrend).

This indicator is a powerful tool for traders of all levels looking for a visual and effective way to analyze market trends.

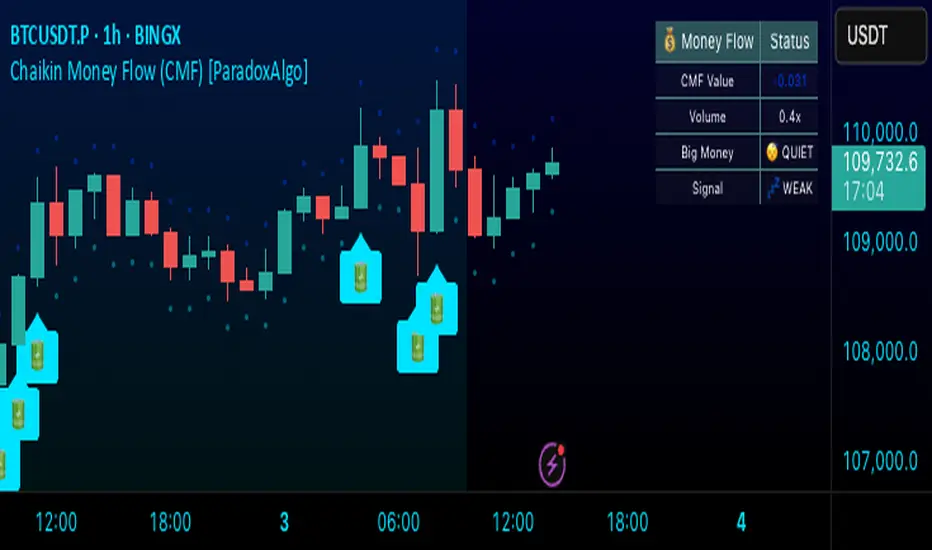

Chaikin Money Flow (CMF) [ParadoxAlgo]OVERVIEW

This indicator implements the Chaikin Money Flow oscillator as an overlay on the price chart, designed to help traders identify institutional money flow patterns. The Chaikin Money Flow combines price and volume data to measure the flow of money into and out of a security, making it particularly useful for detecting accumulation and distribution phases.

WHAT IS CHAIKIN MONEY FLOW?

Chaikin Money Flow was developed by Marc Chaikin and measures the amount of Money Flow Volume over a specific period. The indicator oscillates between +1 and -1, where:

Positive values indicate money flowing into the security (accumulation)

Negative values indicate money flowing out of the security (distribution)

Values near zero suggest equilibrium between buying and selling pressure

CALCULATION METHOD

Money Flow Multiplier = ((Close - Low) - (High - Close)) / (High - Low)

Money Flow Volume = Money Flow Multiplier × Volume

CMF = Sum of Money Flow Volume over N periods / Sum of Volume over N periods

KEY FEATURES

Big Money Detection:

Identifies significant institutional activity when CMF exceeds user-defined thresholds

Requires volume confirmation (volume above average) to validate signals

Uses battery icon (🔋) for institutional buying and lightning icon (⚡) for institutional selling

Visual Elements:

Background coloring based on money flow direction

Support and resistance levels calculated using Average True Range

Real-time dashboard showing current CMF value, volume strength, and signal status

Customizable Parameters:

CMF Period: Calculation period for the money flow (default: 20)

Signal Smoothing: EMA smoothing applied to reduce noise (default: 5)

Big Money Threshold: CMF level required to trigger institutional signals (default: 0.15)

Volume Threshold: Volume multiplier required for signal confirmation (default: 1.5x)

INTERPRETATION

Signal Types:

🔋 (Battery): Indicates strong institutional buying when CMF > threshold with high volume

⚡ (Lightning): Indicates strong institutional selling when CMF < -threshold with high volume

Background color: Green tint for positive money flow, red tint for negative money flow

Dashboard Information:

CMF Value: Current Chaikin Money Flow reading

Volume: Current volume as a multiple of 20-period average

Big Money: Status of institutional activity (BUYING/SELLING/QUIET)

Signal: Strength assessment (STRONG/MEDIUM/WEAK)

TRADING APPLICATIONS

Trend Confirmation: Use CMF direction to confirm price trends

Divergence Analysis: Look for divergences between price and money flow

Volume Validation: Confirm breakouts with corresponding money flow

Accumulation/Distribution: Identify phases of institutional activity

PARAMETER RECOMMENDATIONS

Day Trading: CMF Period 14-21, higher sensitivity settings

Swing Trading: CMF Period 20-30, moderate sensitivity

Position Trading: CMF Period 30-50, lower sensitivity for major trends

ALERTS

Optional alert system notifies users when:

Big money buying is detected (CMF above threshold with volume confirmation)

Big money selling is detected (CMF below negative threshold with volume confirmation)

LIMITATIONS

May generate false signals in low-volume conditions

Best used in conjunction with other technical analysis tools

Effectiveness varies across different market conditions and timeframes

EDUCATIONAL PURPOSE

This open-source indicator is provided for educational purposes to help traders understand money flow analysis. It demonstrates the practical application of the Chaikin Money Flow concept with visual enhancements for easier interpretation.

TECHNICAL SPECIFICATIONS

Overlay indicator (displays on price chart)

No repainting - all calculations are based on closed bar data

Suitable for all timeframes and asset classes

Minimal resource usage for optimal performance

DISCLAIMER

This indicator is for educational and informational purposes only. Past performance does not guarantee future results. Always conduct your own analysis and consider risk management before making trading decisions.

Machine Learning Key Levels [AlgoAlpha]🟠 OVERVIEW

This script plots Machine Learning Key Levels on your chart by detecting historical pivot points and grouping them using agglomerative clustering to highlight price levels with the most past reactions. It combines a pivot detection, hierarchical clustering logic, and an optional silhouette method to automatically select the optimal number of key levels, giving you an adaptive way to visualize price zones where activity concentrated over time.

🟠 CONCEPTS

Agglomerative clustering is a bottom-up method that starts by treating each pivot as its own cluster, then repeatedly merges the two closest clusters based on the average distance between their members until only the desired number of clusters remain. This process creates a hierarchy of groupings that can flexibly describe patterns in how price reacts around certain levels. This offers an advantage over K-means clustering, since the number of clusters does not need to be predefined. In this script, it uses an average linkage approach, where distance between clusters is computed as the average pairwise distance of all contained points.

The script finds pivot highs and lows over a set lookback period and saves them in a buffer controlled by the Pivot Memory setting. When there are at least two pivots, it groups them using agglomerative clustering: it starts with each pivot as its own group and keeps merging the closest pairs based on their average distance until the desired number of clusters is left. This number can be fixed or chosen automatically with the silhouette method, which checks how well each point fits in its cluster compared to others (higher scores mean cleaner separation). Once clustering finishes, the script takes the average price of each cluster to create key levels, sorts them, and draws horizontal lines with labels and colors showing their strength. A metrics table can also display details about the clusters to help you understand how the levels were calculated.

🟠 FEATURES

Agglomerative clustering engine with average linkage to merge pivots into level groups.

Dynamic lines showing each cluster’s price level for clarity.

Labels indicating level strength either as percent of all pivots or raw counts.

A metrics table displaying pivot count, cluster count, silhouette score, and cluster size data.

Optional silhouette-based auto-selection of cluster count to adaptively find the best fit.

🟠 USAGE

Add the indicator to any chart. Choose how far back to detect pivots using Pivot Length and set Pivot Memory to control how many are kept for clustering (more pivots give smoother levels but can slow performance). If you want the script to pick the number of levels automatically, enable Auto No. Levels ; otherwise, set Number of Levels . The colored horizontal lines represent the calculated key levels, and circles show where pivots occurred colored by which cluster they belong to. The labels beside each level indicate its strength, so you can see which levels are supported by more pivots. If Show Metrics Table is enabled, you will see statistics about the clustering in the corner you selected. Use this tool to spot areas where price often reacts and to plan entries or exits around levels that have been significant over time. Adjust settings to better match volatility and history depth of your instrument.

log.info() - 5 Exampleslog.info() is one of the most powerful tools in Pine Script that no one knows about. Whenever you code, you want to be able to debug, or find out why something isn’t working. The log.info() command will help you do that. Without it, creating more complex Pine Scripts becomes exponentially more difficult.

The first thing to note is that log.info() only displays strings. So, if you have a variable that is not a string, you must turn it into a string in order for log.info() to work. The way you do that is with the str.tostring() command. And remember, it's all lower case! You can throw in any numeric value (float, int, timestamp) into str.string() and it should work.

Next, in order to make your output intelligible, you may want to identify whatever value you are logging. For example, if an RSI value is 50, you don’t want a bunch of lines that just say “50”. You may want it to say “RSI = 50”.

To do that, you’ll have to use the concatenation operator. For example, if you have a variable called “rsi”, and its value is 50, then you would use the “+” concatenation symbol.

EXAMPLE 1

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

log.info(“RSI= ” + str.tostring(rsi))

Example Output =>

RSI= 50

Here, we use double quotes to create a string that contains the name of the variable, in this case “RSI = “, then we concatenate it with a stringified version of the variable, rsi.

Now that you know how to write a log, where do you view them? There isn’t a lot of documentation on it, and the link is not conveniently located.

Open up the “Pine Editor” tab at the bottom of any chart view, and you’ll see a “3 dot” button at the top right of the pane. Click that, and right above the “Help” menu item you’ll see “Pine logs”. Clicking that will open that to open a pane on the right of your browser - replacing whatever was in the right pane area before. This is where your log output will show up.

But, because you’re dealing with time series data, using the log.info() command without some type of condition will give you a fast moving stream of numbers that will be difficult to interpret. So, you may only want the output to show up once per bar, or only under specific conditions.

To have the output show up only after all computations have completed, you’ll need to use the barState.islast command. Remember, barState is camelCase, but islast is not!

EXAMPLE 2

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

if barState.islast

log.info("RSI=" + str.tostring(rsi))

plot(rsi)

However, this can be less than ideal, because you may want the value of the rsi variable on a particular bar, at a particular time, or under a specific chart condition. Let’s hit these one at a time.

In each of these cases, the built-in bar_index variable will come in handy. When debugging, I typically like to assign a variable “bix” to represent bar_index, and include it in the output.

So, if I want to see the rsi value when RSI crosses above 0.5, then I would have something like

EXAMPLE 3

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,0.5)

if rsiCrossedOver

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

Example Output =>

bix=19964 - RSI=51.8449459867

bix=19972 - RSI=50.0975830828

bix=19983 - RSI=53.3529808079

bix=19985 - RSI=53.1595745146

bix=19999 - RSI=66.6466337654

bix=20001 - RSI=52.2191767466

Here, we see that the output only appears when the condition is met.

A useful thing to know is that if you want to limit the number of decimal places, then you would use the command str.tostring(rsi,”#.##”), which tells the interpreter that the format of the number should only be 2 decimal places. Or you could round the rsi variable with a command like rsi2 = math.round(rsi*100)/100 . In either case you’re output would look like:

bix=19964 - RSI=51.84

bix=19972 - RSI=50.1

bix=19983 - RSI=53.35

bix=19985 - RSI=53.16

bix=19999 - RSI=66.65

bix=20001 - RSI=52.22

This would decrease the amount of memory that’s being used to display your variable’s values, which can become a limitation for the log.info() command. It only allows 4096 characters per line, so when you get to trying to output arrays (which is another cool feature), you’ll have to keep that in mind.

Another thing to note is that log output is always preceded by a timestamp, but for the sake of brevity, I’m not including those in the output examples.

If you wanted to only output a value after the chart was fully loaded, that’s when barState.islast command comes in. Under this condition, only one line of output is created per tick update — AFTER the chart has finished loading. For example, if you only want to see what the the current bar_index and rsi values are, without filling up your log window with everything that happens before, then you could use the following code:

EXAMPLE 4

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

bix = bar_index

if barstate.islast

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

Example Output =>

bix=20203 - RSI=53.1103309071

This value would keep updating after every new bar tick.

The log.info() command is a huge help in creating new scripts, however, it does have its limitations. As mentioned earlier, only 4096 characters are allowed per line. So, although you can use log.info() to output arrays, you have to be aware of how many characters that array will use.

The following code DOES NOT WORK! And, the only way you can find out why will be the red exclamation point next to the name of the indicator. That, and nothing will show up on the chart, or in the logs.

// CODE DOESN’T WORK

//@version=6

indicator("MW - log.info()")

var array rsi_arr = array.new()

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,50)

if rsiCrossedOver

array.push(rsi_arr, rsi)

if barstate.islast

log.info("rsi_arr:" + str.tostring(rsi_arr))

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

// No code errors, but will not compile because too much is being written to the logs.

However, after putting some time restrictions in with the i_startTime and i_endTime user input variables, and creating a dateFilter variable to use in the conditions, I can limit the size of the final array. So, the following code does work.

EXAMPLE 5

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

// CODE DOES WORK

//@version=6

indicator("MW - log.info()")

i_startTime = input.time(title="Start", defval=timestamp("01 Jan 2025 13:30 +0000"))

i_endTime = input.time(title="End", defval=timestamp("1 Jan 2099 19:30 +0000"))

var array rsi_arr = array.new()

dateFilter = time >= i_startTime and time <= i_endTime

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,50) and dateFilter // <== The dateFilter condition keeps the array from getting too big

if rsiCrossedOver

array.push(rsi_arr, rsi)

if barstate.islast

log.info("rsi_arr:" + str.tostring(rsi_arr))

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

Example Output =>

rsi_arr:

bix=20210 - RSI=56.9030578034

Of course, if you restrict the decimal places by using the rounding the rsi value with something like rsiRounded = math.round(rsi * 100) / 100 , then you can further reduce the size of your array. In this case the output may look something like:

Example Output =>

rsi_arr:

bix=20210 - RSI=55.6947486019

This will give your code a little breathing room.

In a nutshell, I was coding for over a year trying to debug by pushing output to labels, tables, and using libraries that cluttered up my code. Once I was able to debug with log.info() it was a game changer. I was able to start building much more advanced scripts. Hopefully, this will help you on your journey as well.

Dynamic VWAP: Fair Value & Divergence SuiteDynamic VWAP: Fair Value & Divergence Suite

Dynamic VWAP: Fair Value & Divergence Suite is a comprehensive tool for tracking contextual valuation, overextension, and potential reversal signals in trending markets. Unlike traditional VWAP that anchors to the start of a session or a fixed period, this indicator dynamically resets the VWAP anchor to the most recent swing low. This design allows you to monitor how far price has extended from the most recent significant low, helping identify zones of potential profit-taking or reversion.

Deviation bands (standard deviations above the anchored VWAP) provide a clear visual framework to assess whether price is in a fair value zone (±1σ), moderately extended (+2σ), or in zones of extreme extension (+3σ to +5σ). The indicator also highlights contextual divergence signals, including slope deceleration, weak-volume retests, and deviation failures—giving you actionable confluence around potential reversal points.

Because the anchor updates dynamically, this tool is particularly well suited for trend-following assets like BTC or stocks in sustained moves, where price rarely returns to deep negative deviation zones. For this reason, the indicator focuses on upside extension rather than symmetrical reversion to a long-term mean.

🎯 Key Features

✅ Dynamic Swing Low Anchoring

Continuously re-anchors VWAP to the most recent swing low based on your chosen lookback period.

Provides context for trend progression and overextension relative to structural lows.

✅ Standard Deviation Bands

Plots up to +5σ deviation bands to visualize levels of overextension.

Extended bands (+3σ to +5σ) can be toggled for simplicity.

✅ Conditional Zone Fills

Colored background fills show when price is inside each valuation zone.

Helps you immediately see if price is in fair value, moderately extended, or highly stretched territory.

✅ Divergence Detection

VWAP Slope Divergence: Flags when price makes a higher high but VWAP slope decelerates.

Low Volume Retest: Highlights weak re-tests of VWAP on low volume.

Deviation Failure: Identifies when price reverts back inside +1σ after closing beyond +3σ.

✅ Volume Fallback

If volume is unavailable, uses high-low range as a proxy.

✅ Highly Customizable

Adjust lookbacks, show/hide extended bands, toggle fills, and enable or disable divergences.

🛠️ How to Use

Identify Buy and Sell Zones

Price in the fair value band (±1σ) suggests equilibrium.

Reaching +2σ to +3σ signals increasing overextension and potential areas to take profits.

+4σ to +5σ zones can be used to watch for exhaustion or mean-reversion setups.

Monitor Divergence Signals

Use slope divergence and deviation failures to look for confluence with overextension.

Low volume retests can flag rallies lacking conviction.

Adapt Swing Lookback

30–50 bars: Faster re-anchoring for swing trading.

75–100 bars: More stable anchors for longer-term trends.

🧭 Best Practices

Combine the anchored VWAP with higher timeframe structure.

Confirm signals with other tools (momentum, volume profiles, or trend filters).

Use extended deviation zones as context, not as standalone signals.

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial professional before making any trading decisions. Past performance does not guarantee future results.

Price Extension from 8 EMAOverview

This indicator can be used to see how far away the price is from the 8 EMA. It compares this to the Average Daily Range % to see if the stock may be overextended. The "Extension Multiplier" represents how far the stock is extended away from the 8 EMA.

Core Concept

This indicator is best used for breakout trades that are trying to make sure they are not chasing the stock.

How to Use This Indicator

This tool is primarily intended for analyzing daily charts of individual stocks and is often used by breakout traders to evaluate potential entry areas.

If the stock is far away from the 8 EMA, it is likely not ready to break out. If it is close to the 8ema, it could be ready to move higher.

This indicator can also be used in the opposite way. For example, shorting or puts.

Understanding the colors

Green (Not Extended): Indicates the price is close to the 8 EMA. This often corresponds to periods of consolidation.

Yellow (Slightly Extended): The price is beginning to move away from the 8 EMA.

Orange (Extended): The price has moved a considerable distance from the 8 EMA.

Red (Very Extended): The price is at an extreme distance from the 8 EMA, historically increasing the likelihood of a pullback or consolidation.

Settings

Info Row Position: Adjusts the vertical position of the display table on the chart. Useful when using other indicators.

ADR Length: Sets the lookback period for calculating the Average Daily Range. Or the average range % for different timeframes.

Timeframe: Determines the timeframe for the EMA and ADR calculation (the default is Daily).

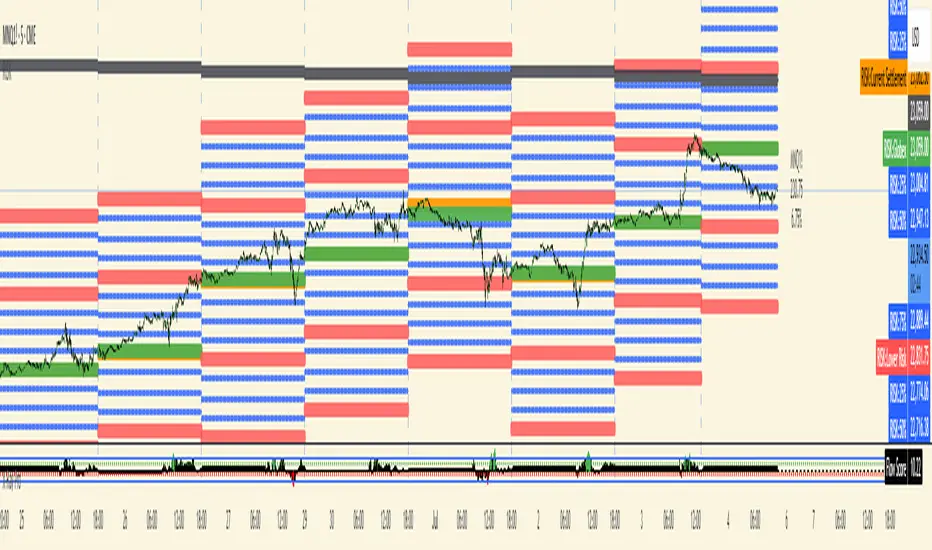

RISK## Main Purpose

The indicator calculates and displays risk levels based on margin requirements and daily settlement prices, helping traders visualize their potential risk exposure.

## Key Features

**Inputs:**

- **Margin for Calculation**: The CME long margin requirement for the asset

- **HTF Margin Line**: An anchor point for higher timeframe margin calculations

**Core Calculations:**

1. **Settlement Price Tracking**: Captures daily settlement prices during specific session times (6:58-6:59 PM ET for close, 6:00-6:01 PM ET for new day open)

2. **Risk Percentage**: Calculates `margin / (point value × settlement price)` - with special handling for Micro contracts (symbols starting with "M") that uses 10× point value

3. **Risk Intervals**: Determines price intervals representing one margin unit of risk

## Visual Display

The indicator plots multiple risk levels on the chart:

- **Settlement price** (orange circles)

- **Globex open** (green circles)

- **Upper/Lower Risk levels** (red circles) - one and two risk intervals away

- **Subdivision levels** (blue crosses) - 25%, 50%, and 75% of each risk interval

- **MHP+ level** (black crosses) - HTF anchor adjusted by risk percentage

- **HTF Anchor** (black crosses)

## Practical Use

This helps futures traders:

- Visualize how far price can move before hitting margin calls

- See risk levels relative to daily settlements

- Plan position sizing and risk management

- Understand exposure in terms of actual margin requirements

The indicator essentially transforms abstract margin numbers into concrete price levels on the chart, making risk management more visual and intuitive.

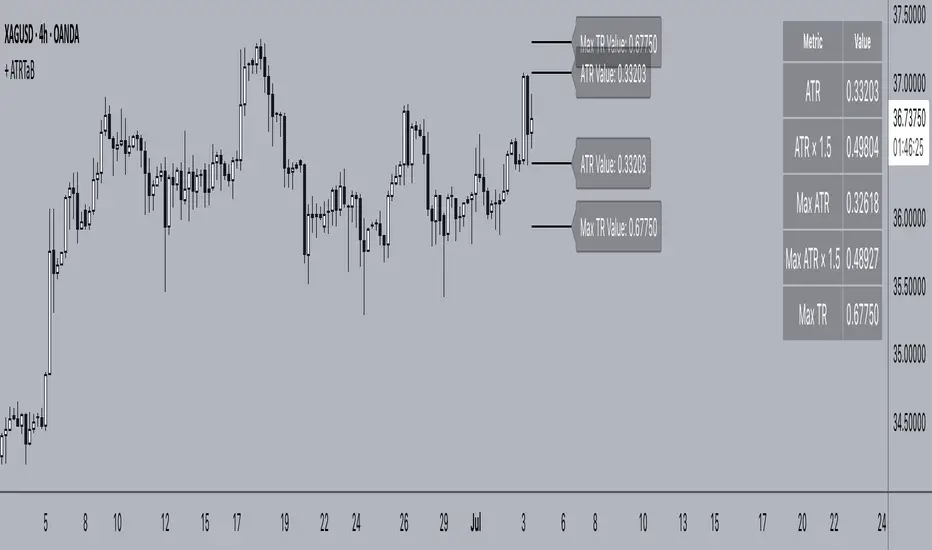

+ ATR Table and BracketsHi, all. I'm back with a new indicator—one I firmly believe could be one of the most valuable indicators you keep in your indicator toolshed—based around true range.

This is a simple, streamlined indicator utilizing true range and average true range that will help any trader with stoploss, trailing stoploss, and take-profit placement—things that I know many traders use average true range for. It could also be useful for trade entries as well, depending on the trader's style.

Typically, most traders (or at least what I've seen recommended across websites, video tutorials on YouTube, etc.) are taught to simply take the ATR number and use that, and possibly some sort of multiplier, as your stoploss and take-profit. This is fine, but I thought that it might be possible to dive a bit deeper into these values. Because an average is a combination of values, some higher, some lower, and we often see ATR spikes during periods of high volatility, I thought wouldn't it be useful to know what value those ATR spikes are, and how do they relate to the ATR? Then I thought to myself, well, what about the most volatile candle within that ATR (the candle with the greatest true range)? Couldn't knowing that value be useful to a trader? So then the idea of a table displaying these values, along with the ATR and the ATR times some multiplier number, would be a useful, simple way to display this information. That's what we have here.

The table is made up of two columns, one with the name of the metric being measured, and the other with its value. That's it. Simple.

As nice as this was, I thought an additional, great, and perhaps better, way to visualize this information would be in the form of brackets extending from the current bar. These are simply lines/labels plotted at the price values of the ATR, ATR times X, highest ATR, highest ATR times X, and highest TR value. These labels supply the actual values of the ATR, etc., but may also display the price if you should choose (both of these values are toggleable in the 'Inputs' section of the indicator.). Additionally, you can choose to display none of these labels, or all five if you wish (leaves the chart a bit cluttered, as shown in the image below), though I suspect you'll determine your preferences for which information you'd like to see and which not.

Chart with all five lines/labels displayed. I adjusted the ATRX value to 3 just to make the screenshot as legible as possible. Default is set to 1.5. As you can see, the label doesn't show the multiplier number, but the table does.

Here's a screenshot of the labels showing the price in addition to the value of the ATR, set to "Previous Closing Price," (see next paragraph for what that means) and highest TR. Personally, I don't see the value in the displaying the price, but I thought some people might want that. It's not available in the table as of now, but perhaps if I get enough requests for it I will add it.

That's basically it, but one last detail I need to go over is the dropdown box labeled "Bar Value ATR Levels are Oriented To." Firstly, this has no effect on Highest ATR, Highest ATRX, and Highest TR levels. Those are based on the ATR up to the last closed candle, meaning they aren't including the value of the currently open candle (this would be useless). However, knowing that different traders trade different ways it seemed to me prudent to allow for traders to select which opening or closing value the trader wishes to have the ATR brackets based on. For example, as someone who has consumed much No Nonsense Forex content I know that traders are urged to enter their trades in the last fifteen minutes of the trading day because the ATR is unlikely to change significantly in that period (ATR being the centerpiece of NNFX money management), so one of three selections here is to plot the brackets based on the ATR's inclusion of this value (this of course means the brackets will move while the candle is still open). The other options are to set the brackets to the current opening price, or the previous closing price. Depending on what you're trading many times these prices are virtually identical, but sometimes price gaps (stocks in particular), so, wanting your brackets placed relative to the previous close as opposed to the current open might be preferable for some traders.

And that's it. I really hope you guys like this indicator. I haven't seen anything closely similar to it on TradingView, and I think it will be something you all will find incredibly handy.

Please enjoy!

Fibonacci Extension Distance Table## 🧾 **Script Name**: Fibonacci Extension Distance Table

### 🎯 Purpose:

This script helps traders visually track **key Fibonacci extension levels** on any chart and immediately see:

* The **price target** at each extension

* The **distance in percentage** from the current market price

It is especially helpful for:

* **Profit targets in trending trades**

* Monitoring **potential resistance zones** in uptrends

* Planning **entry/exit timing**

---

## 🧮 **How It Works**

1. **Swing Logic (A → B → C)**

* It automatically finds:

* `A`: the **lowest low** in the last `swingLen` bars

* `B`: the **highest high** in that same lookback

* `C`: current bar’s low is used as the **retracement point** (simplified)

2. **Extension Formula**

Using the Fibonacci formula:

```text

Extension Price = C + (B - A) × Fibonacci Ratio

```

The script calculates projected target prices at:

* **100%**

* **127.2%**

* **161.8%** (Golden Ratio)

* **200%**

* **261.8%**

3. **Distance Calculation**

For each level, it calculates:

* The **absolute difference** between current price and the extension level

* The **percentage difference**, which helps quickly assess how close or far the market is from that target

---

## 📋 **Table Output in Top Right**

| Level | Target ₹ | Dist % from current price |

| ------ | ---------- | ------------------------- |

| 100% | Calculated | % Above/Below |

| 127.2% | Calculated | % Above/Below |

| 161.8% | Calculated | % Above/Below |

| 200% | Calculated | % Above/Below |

| 261.8% | Calculated | % Above/Below |

* The table updates **live on each bar**

* It **highlights levels** where price is nearing

* Useful in **any time frame** and **any market** (stocks, crypto, forex)

---

## 🔔 Example Use Case

You bought a stock at ₹100, and recent swing shows:

* A = ₹80

* B = ₹110

* C = ₹100

The 161.8% extension = 100 + (110 − 80) × 1.618 = ₹148.54

If the current price is ₹144, the table will show:

* Golden Ratio Target: ₹148.54

* Distance: −4.54

* Distance %: −3.05%

You now know your **target is near** and can plan your **exit or trailing stop**.

---

## 🧠 Benefits

* No need to draw extensions manually

* Automatically adapts to new swing structures

* Supports **scalping**, **swing**, and **positional** strategies

Pivot Swings w Table Pivot Swings w Table — Intraday Structure & Range Analyzer

This indicator identifies key pivot highs and lows on the chart and highlights market structure shifts using a real-time table display. It helps traders visually confirm potential trade setups by tracking unbroken swing points and measuring the range between the most recent pivots.

🔍 Features:

🔹 Automatic Pivot Detection using configurable left/right bar logic.

🔹 Unbroken Pivot Filtering — only pivots that haven't been invalidated by price are displayed.

🔹 Dynamic Range Table with:

Latest valid Pivot High and Pivot Low

Total Range Width

Upper & Lower 25% range thresholds (useful for value/imbalance analysis)

🔹 Trend-Based Color Coding — the table background changes based on which pivot (high or low) occurred more recently:

🟥 Red: Downward bias (last pivot was a lower high)

🟩 Green: Upward bias (last pivot was a higher low)

🔹 Optional extension of pivot levels to the right of the chart for support/resistance confluence.

⚙️ How to Use:

Adjust the Left Bars and Right Bars inputs to fine-tune how swings are defined.

Look for price reacting near the Upper or Lower 25% zones to anticipate mean reversion or breakout setups.

Use the trend color of the table to confirm directional bias, especially useful during consolidation or retracement periods.

💡 Best For:

Intraday or short-term swing traders

Traders who use market structure, support/resistance, or trend-based strategies

Those looking to avoid low-quality trades in tight ranges

✅ Built for overlay use on price charts

📈 Works on all symbols and timeframes

🧠 No repainting — pivots are confirmed with completed bars

Momentum Regression [BackQuant]Momentum Regression

The Momentum Regression is an advanced statistical indicator built to empower quants, strategists, and technically inclined traders with a robust visual and quantitative framework for analyzing momentum effects in financial markets. Unlike traditional momentum indicators that rely on raw price movements or moving averages, this tool leverages a volatility-adjusted linear regression model (y ~ x) to uncover and validate momentum behavior over a user-defined lookback window.

Purpose & Design Philosophy

Momentum is a core anomaly in quantitative finance — an effect where assets that have performed well (or poorly) continue to do so over short to medium-term horizons. However, this effect can be noisy, regime-dependent, and sometimes spurious.

The Momentum Regression is designed as a pre-strategy analytical tool to help you filter and verify whether statistically meaningful and tradable momentum exists in a given asset. Its architecture includes:

Volatility normalization to account for differences in scale and distribution.

Regression analysis to model the relationship between past and present standardized returns.

Deviation bands to highlight overbought/oversold zones around the predicted trendline.

Statistical summary tables to assess the reliability of the detected momentum.

Core Concepts and Calculations

The model uses the following:

Independent variable (x): The volatility-adjusted return over the chosen momentum period.

Dependent variable (y): The 1-bar lagged log return, also adjusted for volatility.

A simple linear regression is performed over a large lookback window (default: 1000 bars), which reveals the slope and intercept of the momentum line. These values are then used to construct:

A predicted momentum trendline across time.

Upper and lower deviation bands , representing ±n standard deviations of the regression residuals (errors).

These visual elements help traders judge how far current returns deviate from the modeled momentum trend, similar to Bollinger Bands but derived from a regression model rather than a moving average.

Key Metrics Provided

On each update, the indicator dynamically displays:

Momentum Slope (β₁): Indicates trend direction and strength. A higher absolute value implies a stronger effect.

Intercept (β₀): The predicted return when x = 0.

Pearson’s R: Correlation coefficient between x and y.

R² (Coefficient of Determination): Indicates how well the regression line explains the variance in y.

Standard Error of Residuals: Measures dispersion around the trendline.

t-Statistic of β₁: Used to evaluate statistical significance of the momentum slope.

These statistics are presented in a top-right summary table for immediate interpretation. A bottom-right signal table also summarizes key takeaways with visual indicators.

Features and Inputs

✅ Volatility-Adjusted Momentum : Reduces distortions from noisy price spikes.

✅ Custom Lookback Control : Set the number of bars to analyze regression.

✅ Extendable Trendlines : For continuous visualization into the future.

✅ Deviation Bands : Optional ±σ multipliers to detect abnormal price action.

✅ Contextual Tables : Help determine strength, direction, and significance of momentum.

✅ Separate Pane Design : Cleanly isolates statistical momentum from price chart.

How It Helps Traders

📉 Quantitative Strategy Validation:

Use the regression results to confirm whether a momentum-based strategy is worth pursuing on a specific asset or timeframe.

🔍 Regime Detection:

Track when momentum breaks down or reverses. Slope changes, drops in R², or weak t-stats can signal regime shifts.

📊 Trade Filtering:

Avoid false positives by entering trades only when momentum is both statistically significant and directionally favorable.

📈 Backtest Preparation:

Before running costly simulations, use this tool to pre-screen assets for exploitable return structures.

When to Use It

Before building or deploying a momentum strategy : Test if momentum exists and is statistically reliable.

During market transitions : Detect early signs of fading strength or reversal.

As part of an edge-stacking framework : Combine with other filters such as volatility compression, volume surges, or macro filters.

Conclusion

The Momentum Regression indicator offers a powerful fusion of statistical analysis and visual interpretation. By combining volatility-adjusted returns with real-time linear regression modeling, it helps quantify and qualify one of the most studied and traded anomalies in finance: momentum.

Multi-Timeframe PivotDescription:

This script provides an advanced tool for multi-timeframe pivot point

analysis. It identifies swing points based on a candle's relationship to

its neighbors. The default strength settings of 1 align with the Inner

Circle Trader (ICT) concept of market structure.

The ICT concept defines a swing point based on a simple 3-candle pattern:

- A swing high is a candle where the candles to the immediate left and right

both have lower highs.

- A swing low is a candle where the candles to the immediate left and right

both have higher lows.

A key feature is its ability to accurately calculate and translate pivot

points from up to five higher timeframes (HTFs) and display them

precisely on a lower timeframe (LTF) chart.

NOTE: This indicator is designed to show HTF data on an LTF chart.

If you select a timeframe in the settings that is lower than your

current chart's timeframe, it will show pivots for the chart's

timeframe instead.

Core Features:

- Up to five independent higher timeframes.

- Per-timeframe customization for pivot strength (left/right bars) and color.

- Optional "Watchlines" that project the price of each pivot forward,

complete with a text label identifying the timeframe.

- An optional "Alignment Model" that colors the background when price is

aligned across all active timeframes (requires at least 2 TFs to be enabled).

Default State:

For a clean initial application, the Watchlines and Alignment Model features

are disabled by default but can be enabled in the settings.

Omori Law Recovery PhasesWhat is the Omori Law?

Originally a seismological model, the Omori Law describes how earthquake aftershocks decay over time. It follows a power law relationship: the frequency of aftershocks decreases roughly proportionally to 1/(t+c)^p, where:

t = time since the main shock

c = time offset constant

p = power law exponent (typically around 1.0)

Application to the markets

Financial markets experience "aftershocks" similar to earthquakes:

Market Crashes as Main Shocks: Major market declines (crashes) represent the initial shock event.

Volatility Decay: After a crash, market volatility typically declines following a power law pattern rather than a linear or exponential one.

Behavioral Components: The decay pattern reflects collective market psychology - initial panic gives way to uncertainty, then stabilization, and finally normalization.

The Four Recovery Phases

The Omori decay pattern in markets can be divided into distinct phases:

Acute Phase: Immediately after the crash, characterized by extreme volatility, panic selling, and sharp reversals. Trading is hazardous.

Reaction Phase: Volatility begins decreasing, but markets test previous levels. False rallies and retests of lows are common.

Repair Phase: Structure returns to the market. Volatility approaches normal levels, and traditional technical analysis becomes more reliable.

Recovery Phase: The final stage where market behavior normalizes completely. The impact of the original shock has fully decayed.

Why It Matters for Traders

Understanding where the market stands in this recovery cycle provides valuable context:

Risk Management: Adjust position sizing based on the current phase

Strategy Selection: Different strategies work in different phases

Psychological Preparation: Know what to expect based on the phase

Time Horizon Guidance: Each phase suggests appropriate time frames for trading

Tsallis Entropy Market RiskTsallis Entropy Market Risk Indicator

What Is It?

The Tsallis Entropy Market Risk Indicator is a market analysis tool that measures the degree of randomness or disorder in price movements. Unlike traditional technical indicators that focus on price patterns or momentum, this indicator takes a statistical physics approach to market analysis.

Scientific Foundation

The indicator is based on Tsallis entropy, a generalization of traditional Shannon entropy developed by physicist Constantino Tsallis. The Tsallis entropy is particularly effective at analyzing complex systems with long-range correlations and memory effects—precisely the characteristics found in crypto and stock markets.

The indicator also borrows from Log-Periodic Power Law (LPPL).

Core Concepts

1. Entropy Deficit

The primary measurement is the "entropy deficit," which represents how far the market is from a state of maximum randomness:

Low Entropy Deficit (0-0.3): The market exhibits random, uncorrelated price movements typical of efficient markets

Medium Entropy Deficit (0.3-0.5): Some patterns emerging, moderate deviation from randomness

High Entropy Deficit (0.5-0.7): Strong correlation patterns, potentially indicating herding behavior

Extreme Entropy Deficit (0.7-1.0): Highly ordered price movements, often seen before significant market events

2. Multi-Scale Analysis

The indicator calculates entropy across different timeframes:

Short-term Entropy (blue line): Captures recent market behavior (20-day window)

Long-term Entropy (green line): Captures structural market behavior (120-day window)

Main Entropy (purple line): Primary measurement (60-day window)

3. Scale Ratio

This measures the relationship between long-term and short-term entropy. A healthy market typically has a scale ratio above 0.85. When this ratio drops below 0.85, it suggests abnormal relationships between timeframes that often precede market dislocations.

How It Works

Data Collection: The indicator samples price returns over specific lookback periods

Probability Distribution Estimation: It creates a histogram of these returns to estimate their probability distribution

Entropy Calculation: Using the Tsallis q-parameter (typically 1.5), it calculates how far this distribution is from maximum entropy

Normalization: Results are normalized against theoretical maximum entropy to create the entropy deficit measure

Risk Assessment: Multiple factors are combined to generate a composite risk score and classification

Market Interpretation

Low Risk Environments (Risk Score < 25)

Market is functioning efficiently with reasonable randomness

Price discovery is likely effective

Normal trading and investment approaches appropriate

Medium Risk Environments (Risk Score 25-50)

Increasing correlation in price movements

Beginning of trend formation or momentum

Time to monitor positions more closely

High Risk Environments (Risk Score 50-75)

Strong herding behavior present

Market potentially becoming one-sided

Consider reducing position sizes or implementing hedges

Extreme Risk Environments (Risk Score > 75)

Highly ordered market behavior

Significant imbalance between buyers and sellers

Heightened probability of sharp reversals or corrections

Practical Application Examples

Market Tops: Often characterized by gradually increasing entropy deficit as momentum builds, followed by extreme readings near the actual top

Market Bottoms: Can show high entropy deficit during capitulation, followed by normalization

Range-Bound Markets: Typically display low and stable entropy deficit measurements

Trending Markets: Often show moderate entropy deficit that remains relatively consistent

Advantages Over Traditional Indicators

Forward-Looking: Identifies changing market structure before price action confirms it

Statistical Foundation: Based on robust mathematical principles rather than empirical patterns

Adaptability: Functions across different market regimes and asset classes

Noise Filtering: Focuses on meaningful structural changes rather than price fluctuations

Limitations

Not a Timing Tool: Signals market risk conditions, not precise entry/exit points

Parameter Sensitivity: Results can vary based on the chosen parameters

Historical Context: Requires some historical perspective to interpret effectively

Complementary Tool: Works best alongside other analysis methods

Enjoy :)

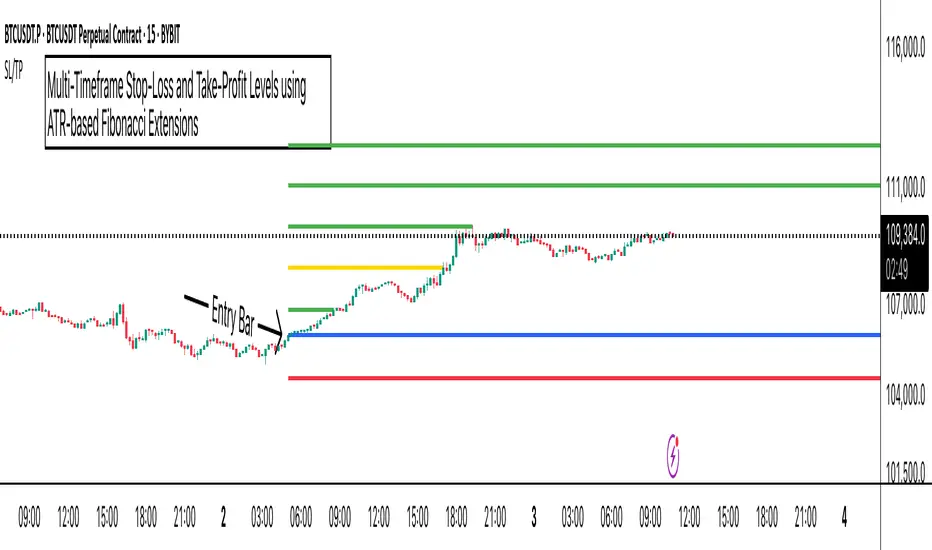

ATR Stop-Loss with Fibonacci Take-Profit [jpkxyz]ATR Stop-Loss with Fibonacci Take-Profit Indicator

This comprehensive indicator combines Average True Range (ATR) volatility analysis with Fibonacci extensions to create dynamic stop-loss and take-profit levels. It's designed to help traders set precise risk management levels and profit targets based on market volatility and mathematical ratios.

Two Operating Modes

Default Mode (Rolling Levels)

In default mode, the indicator continuously plots evolving stop-loss and take-profit levels based on real-time price action. These levels update dynamically as new bars form, creating rolling horizontal lines across the chart. I use this mode primarily to plot the rolling ATR-Level which I use to trail my Stop-Loss into profit.

Characteristics:

Levels recalculate with each new bar

All selected Fibonacci levels display simultaneously

Uses plot() functions with trackprice=true for price tracking

Custom Anchor Mode (Fixed Levels)

This is the primary mode for precision trading. You select a specific timestamp (typically your entry bar), and the indicator locks all calculations to that exact moment, creating fixed horizontal lines that represent your actual trade levels.

Characteristics:

Entry line (blue) marks your anchor point

Stop-loss calculated using ATR from the anchor bar

Fibonacci levels projected from entry-to-stop distance

Lines terminate when price breaks through them

Includes comprehensive alert system

Core Calculation Logic

ATR Stop-Loss Calculation:

Stop Loss = Entry Price ± (ATR × Multiplier)

Long positions: SL = Entry - (ATR × Multiplier)

Short positions: SL = Entry + (ATR × Multiplier)

ATR uses your chosen smoothing method (RMA, SMA, EMA, or WMA)

Default multiplier is 1.5, adjustable to your risk tolerance

Fibonacci Take-Profit Projection:

The distance from entry to stop-loss becomes the base unit (1.0) for Fibonacci extensions:

TP Level = Entry + (Entry-to-SL Distance × Fibonacci Ratio)

Available Fibonacci Levels:

Conservative: 0.618, 1.0, 1.618

Extended: 2.618, 3.618, 4.618

Complete range: 0.0 to 4.764 (23 levels total)

Multi-Timeframe Functionality

One of the indicator's most powerful features is timeframe flexibility. You can analyze on one timeframe while using stop-loss and take-profit calculations from another.

Best Practices:

Identify your entry point on execution timeframe

Enable "Custom Anchor" mode

Set anchor timestamp to your entry bar

Select appropriate analysis timeframe

Choose relevant Fibonacci levels

Enable alerts for automated notifications

Example Scenario:

Analyse trend on 4-hour chart

Execute entry on 5-minute chart for precision

Set custom anchor to your 5-minute entry bar

Configure timeframe setting to "4h" for swing-level targets

Select appropriate Fibonacci Extension levels

Result: Precise entry with larger timeframe risk management

Visual Intelligence System

Line Behaviour in Custom Anchor Mode:

Active levels: Lines extend to the right edge

Hit levels: Lines terminate at the breaking bar

Entry line: Always visible in blue

Stop-loss: Red line, terminates when hit

Take-profits: Green lines (1.618 level in gold for emphasis)

Customisation Options:

Line width (1-4 pixels)

Show/hide individual Fibonacci levels

ATR length and smoothing method

ATR multiplier for stop-loss distance

Rolling Log Returns [BackQuant]Rolling Log Returns

The Rolling Log Returns indicator is a versatile tool designed to help traders, quants, and data-driven analysts evaluate the dynamics of price changes using logarithmic return analysis. Widely adopted in quantitative finance, log returns offer several mathematical and statistical advantages over simple returns, making them ideal for backtesting, portfolio optimization, volatility modeling, and risk management.

What Are Log Returns?

In quantitative finance, logarithmic returns are defined as:

ln(Pₜ / Pₜ₋₁)

or for rolling periods:

ln(Pₜ / Pₜ₋ₙ)

where P represents price and n is the rolling lookback window.

Log returns are preferred because:

They are time additive : returns over multiple periods can be summed.

They allow for easier statistical modeling , especially when assuming normally distributed returns.

They behave symmetrically for gains and losses, unlike arithmetic returns.

They normalize percentage changes, making cross-asset or cross-timeframe comparisons more consistent.

Indicator Overview

The Rolling Log Returns indicator computes log returns either on a standard (1-period) basis or using a rolling lookback period , allowing users to adapt it to short-term trading or long-term trend analysis.

It also supports a comparison series , enabling traders to compare the return structure of the main charted asset to another instrument (e.g., SPY, BTC, etc.).

Core Features

✅ Return Modes :

Normal Log Returns : Measures ln(price / price ), ideal for day-to-day return analysis.

Rolling Log Returns : Measures ln(price / price ), highlighting price drift over longer horizons.

✅ Comparison Support :

Compare log returns of the primary instrument to another symbol (like an index or ETF).

Useful for relative performance and market regime analysis .

✅ Moving Averages of Returns :

Smooth noisy return series with customizable MA types: SMA, EMA, WMA, RMA, and Linear Regression.

Applicable to both primary and comparison series.

✅ Conditional Coloring :

Returns > 0 are colored green ; returns < 0 are red .

Comparison series gets its own unique color scheme.

✅ Extreme Return Detection :

Highlight unusually large price moves using upper/lower thresholds.

Visually flags abnormal volatility events such as earnings surprises or macroeconomic shocks.

Quantitative Use Cases

🔍 Return Distribution Analysis :

Gain insight into the statistical properties of asset returns (e.g., skewness, kurtosis, tail behavior).

📉 Risk Management :

Use historical return outliers to define drawdown expectations, stress tests, or VaR simulations.

🔁 Strategy Backtesting :

Apply rolling log returns to momentum or mean-reversion models where compounding and consistent scaling matter.

📊 Market Regime Detection :

Identify periods of consistent overperformance/underperformance relative to a benchmark asset.

📈 Signal Engineering :

Incorporate return deltas, moving average crossover of returns, or threshold-based triggers into machine learning pipelines or rule-based systems.

Recommended Settings

Use Normal mode for high-frequency trading signals.

Use Rolling mode for swing or trend-following strategies.

Compare vs. a broad market index (e.g., SPY or QQQ ) to extract relative strength insights.

Set upper and lower thresholds around ±5% for spotting major volatility days.

Conclusion

The Rolling Log Returns indicator transforms raw price action into a statistically sound return series—equipping traders with a professional-grade lens into market behavior. Whether you're conducting exploratory data analysis, building factor models, or visually scanning for outliers, this indicator integrates seamlessly into a modern quant's toolbox.

X ORTX ORT — Opening Range & Time Reference Tool

Overview

The X ORT indicator is a precision tool designed for intraday traders seeking to anchor their trading decisions to high-probability price levels. It captures key market reference points including Opening Ranges, Settlement Prices, and Time-Specific Opens, all based on New York time, to help identify potential pivots and directional bias in the market.

Key Features & Usage

🔹 Opening Range Boxes (ORs)

The indicator defines up to two customizable Opening Ranges (e.g., 9:30–9:59 and 8:20–8:49 ET). Each range dynamically tracks the high, low, and midpoint price as the session unfolds, and continues to extend those levels forward throughout the day.

Use as Pivots: The high and low of the Opening Range often act as intraday support and resistance zones. A breakout above the ORH (Opening Range High) may signal bullish intent, while a drop below the ORL (Opening Range Low) may suggest bearish momentum.

Use for Directional Bias: If price remains above or below the range after completion, it may indicate a continuation in that direction. The midpoint (dashed line) serves as a mean-reversion or fair value pivot.

🔸 Settlement Price Anchors

The indicator optionally plots Daily, Weekly, and Monthly Settlement Prices, which are significant institutional reference points.

Use as Market Anchors: Settlement prices are often used by professionals to gauge positioning. Price acceptance above or below settlement can signal strength or weakness and guide directional trades.

Historical weekly and monthly settlements help define multi-day or swing levels for broader context.

🔹 Time-Based Open Levels

X ORT also draws horizontal lines at the open price of specific time points: Midnight, 8:30 AM, 9:30 AM, and 1:30 PM ET.

Use for Session Anchors: These reference opens are useful for understanding session shifts, aligning with key economic releases (like 8:30 AM), and gauging session-to-session continuity.

Why Use X ORT?

Objective Structure: Provides rule-based levels to avoid emotional trading.

Visual Clarity: Transparent, extendable boxes and labeled lines help traders focus on key decision zones.

Multi-Time Context: Blends intraday and higher timeframe levels to support short-term and swing traders.

Whether you're breakout trading, fading range extremes, or gauging market bias, X ORT offers a reliable structural foundation that aligns with how professionals track price behavior throughout the trading day.

Liquidity Zone IndicatorLiquidity Zone Indicator

This PineScript indicator for TradingView identifies liquidity zones in the market where significant trading activity occurs, based on volume spikes and price levels. It highlights areas where large orders may be filled, useful for day traders and scalpers.

Features:

Detects bullish and bearish liquidity zones using a lookback period (default: 50 bars) and volume threshold (default: 1.5x average volume).

Displays zones as shaded boxes or diamond markers above/below bars, customizable by color.

Option to extend zones until price breaks through, with dynamic transparency for better visualization.

Includes an alert for when a liquidity zone is hit.

Settings:

Liquidity Lookback: Number of bars to analyze for high/low price levels.

Volume Threshold: Multiplier for detecting volume spikes.

Display as Zone: Toggle between zone boxes or markers.

Extend Zone: Keep zones active until price crosses them.

Zone Color: Customize the color of zones or markers.

Ideal for traders looking to spot potential reversal or breakout areas driven by liquidity.