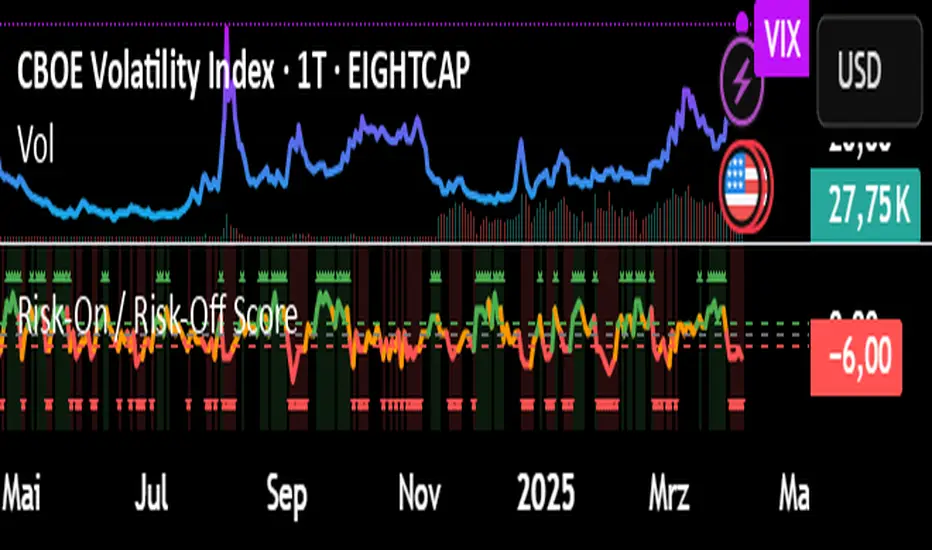

Risk-On / Risk-Off ScoreRisk-On / Risk-Off Score (Macro Sentiment Indicator)

This indicator calculates a custom Risk-On / Risk-Off Score to objectively assess the current market risk sentiment using a carefully selected basket of macroeconomic assets and intermarket relationships.

🧠 What does this indicator do?

The score is based on 14 key components grouped into three categories:

🟢 Risk-On Assets (rising = appetite for risk)

(+1 if performance over X days is positive, otherwise –1)

NASDAQ 100 (NAS100USD)

S&P 500 (SPX)

Bitcoin (BTCUSD)

Copper (HG1!)

WTI Crude Oil (CLK2025)

🔴 Risk-Off Assets (rising = flight to safety)

(–1 if performance is positive, otherwise +1)

Gold (XAUUSD)

US Treasury Bonds (TLT ETF) (TLT)

US Dollar Index (DXY)

USD/CHF

USD/JPY

US 10Y Yields (US10Y) (yields are interpreted inversely)

⚖️ Risk Spreads / Relative Indicators

(+1 if rising, –1 if falling)

Copper/Gold Ratio → HG1! / XAUUSD

NASDAQ/VIX Ratio → NAS100USD / VIX

HYG/TLT Ratio → HYG / TLT

📏 Score Calculation

Total score = sum of all components

Range: from –14 (extreme Risk-Off) to +14 (strong Risk-On)

Color-coded output:

🟢 Score > 2 = Risk-On

🟠 –2 to +2 = Neutral

🔴 Score < –2 = Risk-Off

Displayed as a line plot with background color and signal markers

🧪 Timeframe of analysis:

Default: 5 days (adjustable via input)

Calculated using Rate of Change (% change)

🧭 Use Cases:

Quickly assess macro sentiment

Filter for position sizing, hedging, or intraday bias

Especially useful for:

Swing traders

Day traders with macro filters

Volatility and options traders

📌 Note:

This is not a buy/sell signal indicator, but a contextual sentiment tool designed to help you stay aligned with overall market conditions.

Fundamental Analysis

Metatrader CalculatorThe “ Metatrader Calculator ” indicator calculates the position size, risk, and potential gain of a trade, taking into account the account balance, risk percentage, entry price, stop loss price, and risk/reward ratio. It supports the XAUUSD, XAGUSD, and BTCUSD pairs, automatically calculating the position size (in lots) based on these parameters. The calculation is displayed in a table on the chart, showing the lot size, loss in dollars, and potential gain based on the defined risk.

AltSeasonality - MTFAltSeason is more than a brief macro market cycle — it's a condition. This indicator helps traders identify when altcoins are gaining strength relative to Bitcoin dominance, allowing for more precise entries, exits, and trade selection across any timeframe.

The key for altcoin traders is that the lower the timeframe, the higher the alpha.

By tracking the TOTAL3/BTC.D ratio — a real-time measure of altcoin strength versus Bitcoin — this tool highlights when capital is rotating into or out of altcoins. It works as a bias filter, helping traders avoid low-conviction setups, especially in chop or during BTC-led conditions.

________________________________________________________________________

It works well on the 1D chart to validate swing entries during strong altcoin expansion phases — especially when TOTAL3/BTC.D breaks out while BTCUSD consolidates.

On the 4H or 1D chart, rising TOTAL3/BTC.D + a breakout on your altcoin = high-conviction setup. If BTC is leading, fade the move or reduce size. Consider pairing with the Accumulation - Distribution Candles, optimized for the 1D (not shown).

🔍 Where this indicator really excels, however, is on the 1H and 15M charts, where short-term traders need fast bias confirmation before committing to a move. Designed for scalpers, intraday momentum traders, and tactical swing setups.

Use this indicator to confirm whether an altcoin breakout is supported by broad market flow — or likely to fail due to hidden BTC dominance pressure.

________________________________________________________________________

🧠 How it works:

- TOTAL3 = market cap of altcoins (excl. BTC + ETH)

- BTC.D = Bitcoin dominance as % of total market cap

- TOTAL3 / BTC.D = a normalized measure of altcoin capital strength vs Bitcoin

- BTCUSD = trend baseline and comparison anchor

The indicator compares these forces side-by-side, using a normalized dual-line ribbon. There is intentionally no "smoothing".

When TOTAL3/BTC.D is leading, the ribbon shifts to an “altseason active” phase. When BTCUSD regains control, the ribbon flips back into BTC dominance — signaling defensive posture.

________________________________________________________________________

💡 Strategy Example:

On the 1H chart, a crossover into altseason → check the 15M chart for confirmation. Consider adding the SUPeR TReND 2.718 for confirmation (not shown). If both align, you have trend + flow confluence. If BTCUSD is leading or ribbon is mixed, reduce exposure or wait for confirmation. Further confirmation via Volume breakouts in your specific coin.

⚙️ Features:

• MTF source selection (D, 1H, 15M)

• Normalized ribbon (TOTAL3/BTC.D vs BTCUSD)

• Cross-aware fill shading

• Custom color and transparency controls

• Optional crossover markers

• Midline + zone guides (0.2 / 0.5 / 0.8)

Supertrend + MACD CrossoverKey Elements of the Template:

Supertrend Settings:

supertrendFactor: Adjustable to control the sensitivity of the Supertrend.

supertrendATRLength: ATR length used for Supertrend calculation.

MACD Settings:

macdFastLength, macdSlowLength, macdSignalSmoothing: These settings allow you to fine-tune the MACD for better results.

Risk Management:

Stop-Loss: The stop-loss is based on the ATR (Average True Range), a volatility-based indicator.

Take-Profit: The take-profit is based on the risk-reward ratio (set to 3x by default).

Both stop-loss and take-profit are dynamic, based on ATR, which adjusts according to market volatility.

Buy and Sell Signals:

Buy Signal: Supertrend is bullish, and MACD line crosses above the Signal line.

Sell Signal: Supertrend is bearish, and MACD line crosses below the Signal line.

Visual Elements:

The Supertrend line is plotted in green (bullish) and red (bearish).

Buy and Sell signals are shown with green and red triangles on the chart.

Next Steps for Optimization:

Backtesting:

Run backtests on BTC in the 5-minute timeframe and adjust parameters (Supertrend factor, MACD settings, risk-reward ratio) to find the optimal configuration for the 60% win ratio.

Fine-Tuning Parameters:

Adjust supertrendFactor and macdFastLength to find more optimal values based on BTC's market behavior.

Tweak the risk-reward ratio to maximize profitability while maintaining a good win ratio.

Evaluate Market Conditions:

The performance of the strategy can vary based on market volatility. It may be helpful to evaluate performance in different market conditions or pair it with a filter like RSI or volume.

Let me know if you'd like further tweaks or explanations!

Swing Trade IndicatorThis is a Swing Trade Indicator that combines several technical indicators to analyze market conditions and generate trade signals. I've included two tables that provide real-time information to help you analyze the market and track trades: the Market Status Table and the Trade Tracking Table. These tables are overlaid on the TradingView chart and are customizable in terms of position and visibility.

Simple Moving Averages (SMAs):

Determines trend direction (e.g., bullish if fastMA > slowMA).

Calculates the average closing price over a set period:

fastMA: 21-period SMA (short-term trend).

slowMA: 50-period SMA (medium-term trend).

ultraSlowMA: 200-period SMA (long-term trend).

How:

ta.sma(close, fastLength) computes the SMA of the closing price over fastLength bars (similarly for slowLength and ultraSlowLength).

Volume Analysis:

Identifies potential liquidity spikes.

Measures trading volume to detect high activity.

Average volume over liquidityPeriod (20 bars).

Standard deviation of volume to set a dynamic threshold.

How:

avgVolume = ta.sma(volume, liquidityPeriod): Average volume.

volumeStdDev = ta.stdev(volume, liquidityPeriod): Volatility of volume.

highVolume = volume > avgVolume + volumeStdDev * volumeThresholdMultiplier: Flags high volume if it exceeds the average plus a multiplier (default 1.0) times the standard deviation.

Relative Strength Index (RSI):

Filters entries to avoid overextended markets.

Measures momentum and overbought/oversold conditions.

14-period RSI with thresholds at 60 (overbought) and 40 (oversold).

How:

rsiValue = ta.rsi(close, rsiLength) calculates RSI based on price changes over 14 bars.

Average Directional Index (ADX):

Gauges whether the trend is strong enough to trade.

Assesses trend strength.

14-period ADX.

How:

Calculates True Range (tr), Plus Directional Movement (plusDM), and Minus Directional Movement (minusDM).

Smooths these with ta.rma (Running Moving Average) over adxLength (14).

Computes plusDI and minusDI (directional indicators), then dx (difference), and finally adxValue = ta.rma(dx, adxLength) for trend strength.

Classifies as "Strong" (≥40), "Moderate" (≥20), or "Weak" (<20).

Moving Average Convergence Divergence (MACD) (Optional):

Optional filter for entry conditions if useMacdFilter is enabled.

Tracks momentum and trend changes.

Fast EMA (12), Slow EMA (26), Signal Line (9).

How:

= ta.macd(close, macdFastLength, macdSlowLength, macdSignalLength) computes the MACD components.

macdBullish = macdLine > signalLine: Bullish signal.

macdBearish = macdLine < signalLine: Bearish signal.

Liquidity Zones:

Confirms entries near key levels and suggests next trade setups.

Identifies support and resistance levels based on recent price extremes.

Dynamic levels over 20 bars (if useDynamicLevels is true).

How:

highLiquidityLevel1 = ta.highest(high, 20): Highest high in last 20 bars.

highLiquidityLevel2 = ta.highest(high , 20): Highest high from 20 to 40 bars ago.

highLiquidityLevel3 = ta.lowest(low, 20): Lowest low in last 20 bars.

highLiquidityLevel4 = ta.lowest(low , 20): Lowest low from 20 to 40 bars ago.

Upper and lower zones are derived (upperLevel, lowerLevel), with a midpoint between them.

How It Calculates Entries and Exits

Long Entry:

Basic Conditions (longEntry):

close > fastMA: Price is above the 21-period SMA.

fastMA > slowMA: Short-term trend is above medium-term trend (bullish).

rsiValue < rsiOverbought: RSI below 60 (not overbought).

(not useMacdFilter or macdBullish): If MACD filter is off, ignore it; if on, MACD must be bullish.

Confirmed Entry (confirmedLongEntry):

longEntry is true.

close >= highLiquidityLevel3 * 0.95 and close <= highLiquidityLevel3 * 1.05: Price is within 5% of the lower liquidity level (support).

Action: Sets currentPosition = 'long', records entry price and bar, plots a green triangle below the bar.

Short Entry:

Basic Conditions (shortEntry):

close < fastMA: Price is below the 21-period SMA.

fastMA < slowMA: Short-term trend is below medium-term trend (bearish).

rsiValue > rsiOversold: RSI above 40 (not oversold).

(not useMacdFilter or macdBearish): If MACD filter is off, ignore it; if on, MACD must be bearish.

Confirmed Entry (confirmedShortEntry):

shortEntry is true.

close <= highLiquidityLevel1 * 1.05 and close >= highLiquidityLevel1 * 0.95: Price is within 5% of the upper liquidity level (resistance).

Action: Sets currentPosition = 'short', records entry price and bar, plots a red triangle above the bar.

Exit Conditions

Note: The exit logic is defined but commented out in the script (//longExit and //shortExit), meaning it doesn’t automatically exit positions. It calculates stop-loss and take-profit levels for manual use:

Long Exit (if uncommented):

close < stopLossLevelLong: Price falls below stop-loss (entry price × (1 - 1.5%)).

close > takeProfitLevelLong: Price exceeds take-profit (entry price × (1 + 1.5% × 2.0)).

Short Exit (if uncommented):

close > stopLossLevelShort: Price rises above stop-loss (entry price × (1 + 1.5%)).

close < takeProfitLevelShort: Price falls below take-profit (entry price × (1 - 1.5% × 2.0)).

Suggested Levels: The script provides suggestedLongSL, suggestedLongTP, suggestedShortSL, and suggestedShortTP in the Market Status Table, based on liquidity levels rather than entry price, for manual exits.

Users Can Edit Settings:

Market Status Table Position: Dropdown (e.g., "top_right" to "bottom_left").

Trade Tracking Table Position: Dropdown (e.g., "bottom_right" to "middle_center").

Visibility Toggles (checkboxes):

Show Tables: Enable/disable tables (default: true).

Show Liquidity Zones: Not plotted but affects logic (default: true).

Show Entry Points: Show/hide entry triangles (default: true).

Use Dynamic Levels: Enable/disable liquidity zones (default: true).

Use MACD for Entry Filter: Add MACD to entry conditions (default: false).

Show MACD on Chart: Not implemented but reserved (default: false).

Indicator Periods:

Fast MA Length: Integer (default: 21, e.g., change to 10).

Slow MA Length: Integer (default: 50, e.g., change to 30).

Ultra Slow MA Length: Integer (default: 200, e.g., change to 100).

Liquidity Detection Period: Integer (default: 20, e.g., change to 10).

RSI Length: Integer (default: 14, e.g., change to 7).

ADX Length: Integer (default: 14, e.g., change to 20).

MACD Fast/Slow/Signal Length: Integers (default: 12/26/9, e.g., 9/21/5).

Thresholds:

Volume Threshold Multiplier: Float (default: 1.0, e.g., 1.5 for stricter high volume).

RSI Overbought: Integer (default: 60, e.g., 70).

RSI Oversold: Integer (default: 40, e.g., 30).

Stop Loss %: Float (default: 1.5, e.g., 2.0, range 0.1-10).

Take Profit Ratio: Float (default: 2.0, e.g., 3.0, range 1.0-5.0).

Liquidity Threshold (%): Float (default: 2.0, e.g., 1.5, range 0.5-5.0).

Guntavnook Katta - Fair Value PROOverview:

This script is designed to help long-term investors estimate the fair value of a stock using a combination of fundamental financial metrics and a proprietary multi-factor scoring model. It is especially useful for those who wish to assess whether a stock is undervalued or overvalued based on key fundamentals and recent price behavior.

This script is suitable for stocks, and is best applied on the Daily timeframe.

Purpose:

Many investors rely on Price-to-Earnings (PE) ratios, but not all businesses deserve the same PE due to differences in quality, growth visibility, brand strength, and financial health. This tool attempts to automate the estimation of a fair PE ratio for each company, based on key qualitative and quantitative metrics.

Core Logic:

The script takes the EPS (Earnings Per Share) for the recent financial year from TradingView’s built-in fundamental database and multiplies it by a calculated ideal PE ratio, derived from scoring logic applied to the following parameters:

Financial Parameters Considered:

ROCE (Return on Capital Employed): Indicates how efficiently a company is using its capital to generate profits. Higher ROCE generally reflects strong capital allocation.

ROE (Return on Equity): Shows how effectively the company uses shareholders’ equity. A high ROE may imply strong profitability.

Dividend Yield: Companies that share profits with shareholders via dividends are generally viewed favorably, especially if the yield is sustainable.

Promoter Holding: Higher promoter holding reflects confidence of the founders or promoters in the business. Companies with very low promoter holding might raise governance concerns.

Debt to Equity Ratio: Measures financial risk. Companies with low debt are generally safer, except for banks and NBFCs where high debt is normal.

Sales Growth (5 Years): Reflects business expansion. Consistent growth signals strong demand and operational scalability.

Profit Growth (5 Years): Indicates the company’s ability to grow net earnings over time. High profit growth with low sales growth can sometimes indicate improved margins.

Brand Value: Users can assign qualitative ratings to the company's brand strength, which significantly affects valuation.

Professional Management: If promoter holding is 0%, the company may be professionally or institutionally managed, which adds value in many sectors.

Special Edge: A user-defined optional scoring input for businesses with a strong moat, monopoly, or hard-to-replicate model.

Each of these parameters contributes positively or negatively to the Ideal PE score, which is then used to compute the Fair Value = EPS × Ideal PE.

Why This Scoring Approach?

In fast-moving and diverse market environments, the concept of fair value cannot be treated as a one-size-fits-all number. Traditional valuation models often apply a static PE ratio across stocks, overlooking the individual nuances that define each business. However, real-world investing calls for a more contextual approach—one that acknowledges the dynamic nature of companies, sectors, and economic cycles.

This script attempts to address that gap by offering a systematic way to estimate the fair price of a stock, based on both qualitative and quantitative parameters. The scoring logic is derived from concepts and patterns observed in popular books on fundamental investing and valuation. It encapsulates capital efficiency, ownership structure, growth performance, and brand power—all of which influence a company’s ability to command a premium valuation. The goal is not to suggest decisions but to enable custom, data-supported valuation assessments.

User Instructions:

Apply the script to a stock chart using Daily timeframe.

Open the indicator Settings Panel.

Choose either:

Auto-calculated PE: Let the script determine Ideal PE from scoring inputs.

Manual PE: If you're confident in the fair PE value, input it directly.

Hover over (i) icons in settings for explanation of each input.

Most inputs like ROE, ROCE, D/E ratio, etc., can be found from official filings, annual reports, or financial platforms.

Overbought & Oversold Signals:

This script also provides technical signals based on price deviation from fair value:

Uses RSI-based crossover logic in combination with user-defined price deviation thresholds.

Users can enable/disable signals independently.

Thresholds define how far above/below fair value the stock should move before a signal is triggered.

For example:

If the price moves above the fair value by a percentage equal to or greater than the Overbought threshold set by the user and the RSI crosses below 70, a red Overbought label appears.

If the price drops below the fair value by a percentage equal to or greater than the Oversold threshold set by the user and the RSI crosses above 30, a green Oversold label appears.

You can use the average deviation values displayed in the info table to determine suitable threshold levels based on historical price behavior.

Why RSI?

The Relative Strength Index (RSI) is a widely accepted momentum indicator used to assess whether a stock is overbought or oversold based on recent price performance. In this script, RSI serves as a reliable trigger mechanism when combined with fair value deviations. While the fair value estimation captures long-term fundamentals, RSI helps identify short-term extremes in price action. By using RSI crossovers, the script ensures signals are technically validated and not triggered solely by deviation, thus improving accuracy.

Visual Aids:

The green line shows the calculated Fair Value.

Candle colors:

Red: RSI ≥ 70

Green: RSI ≤ 30

Yellow: Neutral zone

An info table at the top-right displays:

Ideal PE

Current PE (based on FY EPS)

Calculated Fair Value

Avg Upper and Lower Price Deviation % from Fair Value

Note:

This tool is primarily optimized for evaluating Indian stocks, especially those listed on NSE/BSE, where metrics like promoter holding and ROCE are commonly used.

Disclaimer:

This script is intended for educational and research purposes only. It is not investment advice. The logic is based on publicly available data and scoring heuristics designed for learning and valuation awareness.

Smarter Money Concepts - FVGs [PhenLabs]📊 Smarter Money Concepts - FVGs

Version: PineScript™ v6

📌 Description

Smarter Money Concepts - FVGs is a sophisticated indicator designed to identify and track Fair Value Gaps (FVGs) in price action. These gaps represent market inefficiencies where price moves quickly, creating imbalances that often attract subsequent price action for mitigation. By highlighting these key areas, traders can identify potential zones for reversals, continuations, and price targets.

The indicator employs volume filtering ideology to highlight only the most significant FVGs, reducing noise and focusing on gaps formed during periods of higher relative volume. This combination of price structure analysis and volume confirmation provides traders with high-probability areas of interest that institutional smart money may target during future price movements.

🚀 Points of Innovation

Volume-Filtered Gap Detection : Eliminates low-significance FVGs by requiring a minimum volume threshold, focusing only on gaps formed with institutional participation

Equilibrium Line Visualization : Displays the midpoint of each gap as a potential precision target for trades

Automated Gap Mitigation Tracking : Monitors when price revisits and mitigates gaps, automatically managing visual elements

Time-Based Gap Management : Intelligently filters gaps based on a configurable timeframe, maintaining chart clarity

Dual Direction Analysis : Simultaneously tracks both bullish and bearish gaps, providing a complete market structure view

Memory-Optimized Design : Implements efficient memory management for smooth chart performance even with numerous FVGs

🔧 Core Components

Fair Value Gap Detection : Identifies price inefficiencies where the current candle’s low is higher than the previous candle’s high (bearish FVG) or where the current candle’s high is lower than the previous candle’s low (bullish FVG).

Volume Filtering Mechanism : Calculates relative volume compared to a moving average to qualify only gaps formed during significant market activity.

Mitigation Tracking : Continuously monitors price action to detect when gaps get filled, with options to either hide or maintain visual representation of mitigated gaps.

🔥 Key Features

Customizable Gap Display : Toggle visibility of bullish and bearish gaps independently to focus on your preferred market direction

Volume Threshold Control : Adjust the minimum volume ratio required for gap qualification, allowing fine-tuning between sensitivity and significance

Flexible Mitigation Methods : Choose between “Wick” or “Close” methods for determining when a gap has been mitigated, adapting to different trading styles

Visual Customization : Full control over colors, transparency, and style of gap boxes and equilibrium lines

🎨 Visualization

Gap Boxes : Rectangular highlights showing the exact price range of each Fair Value Gap. Bullish gaps indicate potential upward price targets, while bearish gaps show potential downward targets.

Equilibrium Lines : Dotted lines running through the center of each gap, representing the mathematical midpoint that often serves as a precision target for price movement.

📖 Usage Guidelines

General Settings

Days to Analyze : Default: 15, Range: 1-100. Controls how many days of historical gaps to display, balancing between comprehensive analysis and chart clarity

Visual Settings

Bull Color : Default:(#596fd33f). Color for bullish Fair Value Gaps, typically using high transparency for clear chart visibility

Bear Color : Default:(#d3454575). Color for bearish Fair Value Gaps, typically using high transparency for clear chart visibility

Equilibrium Line : Default: Enabled. Toggles visibility of the center equilibrium line for each FVG

Eq. Line Color : Default: Black with 99% transparency. Sets the color of equilibrium lines, usually kept subtle to avoid chart clutter

Eq. Line Style : Default: Dotted, Options: Dotted, Solid, Dashed. Determines the line style for equilibrium lines

Mitigation Settings

Mitigation Method : Default: Wick, Options: Wick, Close. Determines how gap mitigation is calculated - “Wick” uses high/low values while “Close” uses open/close values for more conservative mitigation criteria

Hide Mitigated : Default: Enabled. When enabled, gaps become transparent once mitigated, reducing visual clutter while maintaining historical context

Volume Filter

Volume Filter : Default: Enabled. When enabled, only shows gaps formed with significant volume relative to recent average

Min Ratio : Default: 1.5, Range: 0.1-10.0. Minimum volume ratio compared to average required to display an FVG; higher values filter out more gaps

Periods : Default: 15, Range: 5-50. Number of periods used to calculate the average volume baseline

✅ Best Use Cases

Identifying potential reversal zones where price may react after extended moves

Finding precise targets for take-profit placement in trend-following strategies

Detecting institutional interest areas for potential breakout or breakdown confirmations

Plotting significant support and resistance zones based on structural imbalances

Developing fade strategies at key market structure points

Confirming trade entries when price approaches significant unfilled gaps

⚠️ Limitations

Works best on higher timeframes where gaps reflect more significant market inefficiencies

Very choppy or ranging markets may produce small gaps with limited predictive value

Volume filtering depends on accurate volume data, which may be less reliable for some symbols

Performance may be affected when displaying a very large number of historical gaps

Some gaps may never be fully mitigated, particularly in strongly trending markets

💡 What Makes This Unique

Volume Intelligence : Unlike basic FVG indicators, this script incorporates volume analysis to identify the most significant structural imbalances, focusing on quality over quantity.

Visual Clarity Management : Automatic handling of mitigated gaps and memory management ensures your chart remains clean and informative even over extended analysis periods.

Dual-Direction Comprehensive Analysis : Simultaneously tracks both bullish and bearish gaps, providing a complete market structure picture rather than forcing a directional bias.

🔬 How It Works

1. Gap Detection Process :

The indicator examines each candle in relation to previous candles, identifying when a gap forms between the low of candle and high of candle (bearish FVG) or between the high of candle and low of candle (bullish FVG). This specific candle relationship identifies true structural imbalances.

2. Volume Qualification :

For each potential gap, the algorithm calculates the relative volume compared to the configured period average. Only gaps formed with volume exceeding the minimum ratio threshold are displayed, ensuring focus on institutionally significant imbalances.

3. Equilibrium Calculation :

For each qualified gap, the script calculates the precise mathematical midpoint, which becomes the equilibrium line - a key target that price often gravitates toward during mitigation attempts.

4. Mitigation Tracking :

The indicator continuously monitors price action against existing gaps, determining mitigation based on the selected method (wick or close). When price reaches the equilibrium point, the gap is considered mitigated and can be visually updated accordingly.

💡 Note:

Fair Value Gaps represent market inefficiencies that often, but not always, get filled. Use this indicator as part of a complete trading strategy rather than as a standalone system. The most valuable signals typically come from combining FVG analysis with other confirmatory indicators and overall market context. For optimal results, start with the default settings and gradually adjust parameters to match your specific trading timeframe and style.

Imbalance(FVG) DetectorImbalance (FVG) Detector

Overview

The Imbalance (FVG) Detector is a technical analysis tool designed to highlight price inefficiencies by identifying Fair Value Gaps (FVGs). These gaps occur when rapid price movement leaves an area with little to no traded volume, which may later act as a zone of interest. The indicator automatically detects and marks these imbalances on the chart, allowing users to observe historical price behavior more effectively.

Key Features

- Automatic Imbalance Detection: Identifies bullish and bearish imbalances based on a structured three-bar price action model.

- Customizable Sensitivity: Users can adjust the minimum imbalance percentage threshold to tailor detection settings to different assets and market conditions.

- Real-time Visualization: Marked imbalances are displayed as colored boxes directly on the chart.

- Dynamic Box Updates: Imbalance zones extend forward in time until price interacts with them.

- Alert System: Users can set alerts for when new imbalances appear or when price tests an existing imbalance.

How It Works

The indicator identifies market imbalances using a three-bar price structure:

- Bullish Imbalance: Occurs when the high of three bars ago is lower than the low of the previous bar, forming a price gap.

- Bearish Imbalance: Occurs when the low of three bars ago is higher than the high of the previous bar, creating a downward gap.

When an imbalance is detected:

- Green Boxes indicate bullish imbalances.

- Red Boxes indicate bearish imbalances.

- Once price interacts with an imbalance, the box fades to gray, marking it as tested.

! Designed for Crypto Markets

This indicator is particularly useful in crypto markets, where frequent volatility can create price inefficiencies. It provides a structured way to visualize gaps in price movement, helping users analyze historical liquidity areas.

Customization Options

- Min Imbalance Percentage Size: Adjusts the sensitivity of the imbalance detection.

- Alerts: Users can enable alerts to stay notified of new or tested imbalances.

Important Notes

- This indicator is a technical analysis tool and does not provide trading signals or financial advice.

- It does not predict future price movement but highlights historical price inefficiencies.

- Always use this tool alongside other market analysis methods and risk management strategies.

Professional MSTI+ Trading Indicator"Professional MSTI+ Trading Indicator" is a comprehensive technical analysis tool that combines over 20 indicators to generate high-quality trading signals and assess market sentiment. The script integrates standard indicators (MACD, RSI, Bollinger Bands, Stochastic, Simple Moving Averages, and Volume Analysis) with advanced components (Squeeze Momentum, Fisher Transform, True Strength Index, Heikin-Ashi, Laguerre RSI, Hull MA) and further includes metrics such as ADX, Chaikin Money Flow, Williams %R, VWAP, and EMA for in-depth market analysis.

Key Features:

Multiple Presets for Different Trading Styles:

Choose from optimal configurations like Professional, Swing Trading, Day Trading, Scalping, or Reversal Hunter. Note that the presets may not work perfectly on all pairs, and manual calibration might be required. This flexibility allows you to fine-tune the settings to align with your unique strategies and signals.

Multi-Layered Signal Filtering:

Filters based on trend, volume, and volatility help eliminate false signals, enhancing the accuracy of market entries.

Comprehensive Fear & Greed Index:

The indicator aggregates data from RSI, volatility, momentum, trend, and volume to gauge overall market sentiment, providing an additional layer of market context.

Dynamic Information Panel:

Displays detailed status updates for each component (e.g., MACD, RSI, Laguerre RSI, TSI, Fisher Transform, Squeeze, Hull MA, etc.) along with a visual strength bar that represents the intensity of the trading signal.

Signal Generation:

Buy and sell signals are generated when a predefined number of conditions are met and confirmed over multiple bars. These signals are clearly displayed on the chart with arrows, making it easier to spot potential entry and exit points.

Alert Setup:

Built-in alert conditions allow you to receive real-time notifications when trading signals are generated, helping you stay on top of market movements.

"Professional MSTI+ Trading Indicator" is designed to enhance your trading strategy by providing a multi-faceted market analysis and an intuitive visual interface. While the presets offer a robust starting point, they may require manual calibration on certain pairs, giving you the flexibility to configure your own unique strategies and signals.

Global Liquidity Index with Editable DEMA + 107 Day OffsetGlobal Liquidity DEMA (107-Day Lead)

This indicator visualizes a smoothed version of global central bank liquidity with a forward time shift of 107 days. The concept is based on the macroeconomic observation that markets tend to lag changes in global liquidity — particularly from central banks like the Federal Reserve, ECB, BOJ, and PBOC.

The script uses a Double Exponential Moving Average (DEMA) to smooth the combined balance sheets and money supply inputs. It then offsets the result into the future by 107 days, allowing you to visually align liquidity trends with delayed market reactions. A second plot (ROC SMA) is included to help identify liquidity momentum shifts.

🔍 How to Use:

Add this indicator to any chart (S&P 500, BTC, Gold, etc.)

Compare price action to the forward-shifted liquidity trend

Look for divergence, confirmation, or crossovers with price

Use as a macro timing tool for long-term entries/exits

📌 Included Features:

Editable DEMA smoothing length

ROC + SMA overlay for momentum signals

Fixed 107-day forward projection

Includes main DEMA and ROC SMA both real-time and shifted

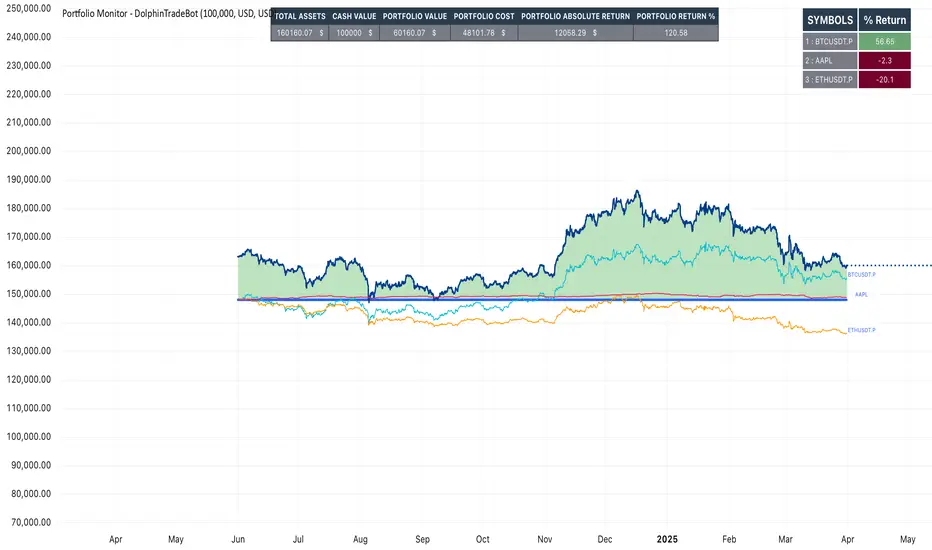

Portfolio Monitor - DolphinTradeBot1️⃣ Overview

▪️This indicator unifies the value of all your investments—whether stocks, currencies, or cryptocurrencies—in your chosen currency. This tool not only provides a clear snapshot of your overall portfolio performance but also highlights the individual growth of each asset with intuitive visualizations and an easy-to-understand performance report.

2️⃣ What sets this indicator apart

▪️is its ability to convert values from various currency pairs into any currency you choose. This means you can monitor your portfolio's performance against any currency pair you prefer, offering a flexible and comprehensive view of your investments.

3️⃣ How Is It Work ?

🔍The indicator can be analyzed under two main categories: visual representations and tables.

1- Visual representations ;

The indicator includes three different types of lines:

1. 1 - Reference Line → This represents the cost of all assets we hold, based on the selected date.

1. 2 - Total Assets Line → Displays the real-time value of all assets in our possession, including cash value, in the selected trading pair.

The area between the reference line is filled with green and red. The section above the reference line is represented in green, while the section below is shown in red.

1. 3 - Performance Lines → These visualize the performance of the assets, starting from the reference line and taking into account their weights in the portfolio. (Note: The lines are scaled for visualization purposes, so their absolute values should not be considered.)

"The names of the lines are shown in the image below."⤵️

2- Tables

The indicator includes three different types of tables:

2. 1 - Analysis Table : It provides a superficial overview of wallet statistics and values.

▪️TOTAL ASSETS → The current equivalent of all assets in the target currency

▪️CASH VALUE → The current value of the amount "Cash Value", in the target currency.

▪️PORTFOLIO VALUE → The total value of assets excluding Cash, in the target currency.

▪️POSTFOLIO COST → The cost of assets excluding Cash, in the target currency.

▪️PORTFOLIO ABSOLUTE RETURN → It shows the profit or loss relative to the cost of assets

▪️PORTFOLIO RETURN % →It shows the profit or loss relative to the cost of assets on a percentage basis

2. 2 - Performance Table : It displays the names of assets excluding Cash and their profit amounts, sorted from highest to lowest profit. If "Show as Percentage" is selected in the settings, it shows the percentage profit or loss relative to the cost. Profits are represented in green, while losses are represented in red.

"You can see the visual showing the tables below"⤵️

4️⃣How to Use ?

1- Choose the date on which the visualization will begin (📌The start date only affects the exchange rate used for calculating the reference line in the target currency.)

2- If you have cash holdings, enter the amount and specify the currency.

3- Select the currency in which your portfolio value will be displayed.(Default value is USD)

4- To set up your portfolio;

SYMBOLS - QUANTITY - PURCHASE PRICE

Enter the symbols of your assets - the number of units you hold - and their cost levels.

5- If you have cash, be sure to include your cash balance. If you also hold other currencies, enter them as separate assets with their corresponding quantities and purchase prices.

6- If you want to see the percentage returns of the assets in the performance table relative to their cost, select the "Show as Percent" option.

7- If you want to see the performance visuals of the assets, click on the "Show Asset Performance" option.

You can find an image of the settings section where the numbers above are used as references below.⤵️

📌 NOTE → By default, a few assets and their values have been pre-added in the initial settings. This is to ensure that you don’t see an empty screen when adding the indicator to the chart. Please remember to enter your own assets and values. The default settings are only provided as an example.

ICT IPDA Lookback / Cast-forwardThis script automatically displays 20/40/60 daily range highs and lows.

Known as IPDA ranges, a term popularised by Inner Circle Trader (ICT). IPDA = Interbank Price Delivery Algorithm.

You can also add 80 day lines (my own addition) . IPDA labels are shown for Daily highs, and an equivalent line is drawn at IPDA Daily lows - but without the label to keep your chart as clean as possible. You can use this on hourly timeframes as well.

ICT is "flexible" on IPDA data ranges in his mentorship regarding whether you should use the first day of each month, or go recalculate day by day, and that's why this script lets you do both + also has an option to set a hard specified date - useful for more advanced purposes.

You can also Cast-forward the displayed 20/40/60 (+80) IPDA ranges with this tool.

You can use IPDA ranges to forecast Highs and Lows that price will be attracted to on a Daily timeframe and where price is in its P/D range, being in a discount or premium. You can also use this knowledge to help guide lower timeframe scalps.

Longer term traders can reference the 40 and 60 Day Look Back lines for an indication of current market conditions.

Econometrica by [SS]This is Econometrica, an indicator that aims to bridge a big gap between the resources available for analysis of fundamental data and its impact on tickers and price action.

I have noticed a general dearth of available indicators that offer insight into how fundamentals impact a ticker and provide guidance on how they these economic factors influence ticker behaviour.

Enter Econometrica. Econometrica is a math based indicator that aims to co-integrate and model indicator price action in relation to critical economic metrics.

Econometrica supports the following US based economic data:

CPI

Non-Farm Payroll

Core Inflation

US Money Supply

US Central Bank Balance Sheet

GDP

PCE

Let's go over the functions of Econometrica.

Creating a Regression Cointegrated Model

The first thing Econometrica does is creates a co-integrated regression, as you see in the main chart, predicting ticker value ranges from fundamental economic data.

You can visualize this in the main chart above, but here are some other examples:

SPY vs Core Inflation:

BA vs PCE:

QQQ vs US Balance Sheet:

The band represents the anticipated range the ticker should theoretically fall in based on the underlying economic value. The indicator will breakdown the relationship between the economic indicator and the ticker more precisely. In the images above, you can see how there are some metrics provided, including Stationairty, lagged correlation, Integrated Correlation and R2. Let's discuss these very briefly:

Stationarity: checks to ensure that the relationship between the economic indicator and ticker is stationary. Stationary data is important for making unbiased inferences and projections, so having data that is stationary is valuable.

Lagged Correlation: This is a very interesting metric. Lagged correlation means whether there is a delay in the economic indicator and the response of the ticker. Typically, you will observed a lagged correlation between an economic indicator and price of a ticker, as it can take some time for economic changes to reach the market. This lagged correlation will provide you with how long it takes for the economic indicator to catch up with the ticker in months.

Integrated Correlation: This metric tells you how good of a fit the regression bands are in relation to the ticker price. A higher correlation, means the model is better at consistent and accurate information about the anticipated range for the ticker in relation to the economic indicator.

R2: Provides information on the variance and degree of model fit. A high R2 value means that the model is capable of explaining a large amount of variance between the economic indicator and the ticker price action.

Explaining the Relationship

Owning to the fact that the indicator is a bit on the mathy side (it has to be to do this kind of task), I have included ability for the indicator to explain and make suggestions based on the underlying data. It can assess the model's fit and make suggestions for tweaking. It can also explain the implications of the data being presented in the model.

Here is an example with QQQ and the US Balance Sheet:

This helps to simplify and interpret the results you are looking at.

Forecasting the Economic Indicator

In addition to assessing the economic indicator's impact on the ticker, the indicator is also capable of forecasting out the economic indicator over the next 25 releases.

Here is an example of the CPI forecast:

Overall use of the indicator

The indicator is meant to bridge the gap between Technical Analysis and Fundamental Analysis.

Any trader who is attune to fundamentals would benefit from this, as this provides you with objective data on how and to what extent fundamental and economic data impacts tickers.

It can help affirm hypothesis and dispel myths objectively.

It also omits the need from having to perform these types of analyses outside of Tradingview (i.e. in excel, R or Python), as you can get the data in just a few licks of enabling the indicator.

Conclusion

I have tried to make this indicator as user friendly as possible. Though it uses a lot of math, it is fairly straight forward to interpret.

The band plotted can be considered the fair market value or FMV of the ticker based on the underlying economic data, provided the indicator tells you that the relationship is significant (and it will blatantly give you this information verbatim, you don't have to interpret the math stuff).

This is US economic data only. It does not pull economic data from other countries. You can absolutely see how US economic data impacts other markets like the TSX, BANKNIFTY, NIFTY, DAX etc. but the indicator is only pulling US economic data.

That is it!

I hope you enjoy it and find this helpful!

Thanks everyone and safe trades as always 🚀🚀🚀

Advanced Swing High/Low Trend Lines with MA Filter# Advanced Swing High/Low Trend Lines Indicator

## Overview

This advanced indicator identifies and draws trend lines based on swing highs and lows across three different timeframes (large, middle, and small trends). It's designed to help traders visualize market structure and potential support/resistance levels at multiple scales simultaneously.

## Key Features

- *Multi-Timeframe Analysis*: Simultaneously tracks trends at large (200-bar), middle (100-bar), and small (50-bar) scales

- *Customizable Visualization*: Different colors, widths, and styles for each trend level

- *Trend Confirmation System*: Requires minimum consecutive pivot points to validate trends

- *Trend Filter Option*: Can align trends with 200 EMA direction for consistency

## Recommended Settings

### For Long-Term Investors:

- Large Swing Length: 200-300

- Middle Swing Length: 100-150

- Small Swing Length: 50-75

- Enable Trend Filter: Yes

- Confirmation Points: 4-5

### For Swing Traders:

- Large Swing Length: 100

- Middle Swing Length: 50

- Small Swing Length: 20-30

- Enable Trend Filter: Optional

- Confirmation Points: 3

### For Day Traders:

- Large Swing Length: 50

- Middle Swing Length: 20

- Small Swing Length: 5-10

- Enable Trend Filter: No

- Confirmation Points: 2-3

## How to Use

### Identification:

1. *Large Trend Lines* (Red/Green): Show major market structure

2. *Middle Trend Lines* (Purple/Aqua): Intermediate levels

3. *Small Trend Lines* (Orange/Blue): Short-term price action

### Trading Applications:

- *Breakout Trading*: Watch for price breaking through multiple trend lines

- *Bounce Trading*: Look for reactions at confluence of trend lines

- *Trend Confirmation*: Aligned trends across timeframes suggest stronger moves

### Best Markets:

- Works well in trending markets (forex, indices)

- Effective in higher timeframes (1H+)

- Can be used in ranging markets to identify boundaries

## Customization Tips

1. For cleaner charts, reduce line widths in congested markets

2. Use dotted styles for smaller trends to reduce visual clutter

3. Adjust confirmation points based on market volatility (higher for noisy markets)

## Limitations

- May repaint on current swing points

- Works best in trending conditions

- Requires sufficient historical data for longer swing lengths

This indicator provides a comprehensive view of market structure across multiple timeframes, helping traders make more informed decisions by visualizing the hierarchy of support and resistance levels.

Spot - Fut spread v2"Spot - Fut Spread v2"

indicator is designed to track the difference between spot and futures prices on various exchanges. It automatically identifies the corresponding instrument (spot or futures) based on the current symbol and calculates the spread between the prices. This tool is useful for analyzing the delta between spot and futures markets, helping traders assess arbitrage opportunities and market sentiment.

Key Features:

- Automatic detection of spot and futures assets based on the current chart symbol.

- Flexible asset selection: the ability to manually choose the second asset if automatic selection is disabled.

- Spread calculation between futures and spot prices.

- Moving average of the spread for smoothing data and trend analysis.

Flexible visualization:

- Color indication of positive and negative spread.

- Adjustable background transparency.

- Text label displaying the current spread and moving average values.

- Error alerts in case of invalid data.

How the Indicator Works:

- Determines whether the current symbol is a futures contract.

- Based on this, selects the corresponding spot or futures symbol.

- Retrieves price data and calculates the spread between them.

- Displays the spread value and its moving average.

- The chart background color changes based on the spread value (positive or negative).

- In case of an error, the indicator provides an alert with an explanation.

Customization Parameters:

-Exchange selection: the ability to specify a particular exchange from the list.

- Automatic pair selection: enable or disable automatic selection of the second asset.

- Moving average period: user-defined.

- Colors for positive and negative spread values.

- Moving average color.

- Background transparency.

- Background coloring source (based on spread or its moving average).

Application:

The indicator is suitable for traders who analyze the difference between spot and futures prices, look for arbitrage opportunities, and assess the premium or discount of futures relative to the spot market.

NUPL Z-Score | Vistula LabsWhat is NUPL?

NUPL (Net Unrealized Profit/Loss) is a fundamental on-chain metric used to evaluate the profit or loss state of a cryptocurrency's market participants, such as Bitcoin (BTC) and Ethereum (ETH). It compares the current market capitalization—the total value of all coins at their current price—to the realized capitalization, which represents the average price at which all coins were last transacted on-chain.

Market Capitalization: Current price × circulating supply.

Realized Capitalization: The sum of the value of all coins based on the price at their last on-chain movement.

For Bitcoin (BTC):

NUPL = (Market Cap - Realized Cap) / Market Cap * 100

For Ethereum (ETH):

NUPL = (Market Cap - Realized Cap) / Market Cap

A positive NUPL indicates that the market holds unrealized profits, meaning the current value exceeds the price at which coins were last moved. A negative NUPL signals unrealized losses. Extreme NUPL values—high positives or low negatives—can suggest overvaluation (potential market tops) or undervaluation (potential market bottoms), respectively.

How NUPL is Calculated for BTC & ETH

This indicator calculates NUPL using data sourced from Glassnode and CoinMetrics:

For Bitcoin:

Market Cap: GLASSNODE:BTC_MARKETCAP

Realized Cap: COINMETRICS:BTC_MARKETCAPREAL

Formula: ((btc_market_cap - btc_market_cap_real) / btc_market_cap) * 100

For Ethereum:

Market Cap: GLASSNODE:ETH_MARKETCAP

Realized Cap: COINMETRICS:ETH_MARKETCAPREAL

Formula: ((eth_market_cap - eth_market_cap_real) / eth_market_cap) * 100

The indicator then transforms these NUPL values into a Z-Score, which measures how many standard deviations the current NUPL deviates from its historical average. The Z-Score calculation incorporates:

A customizable moving average of NUPL (options: SMA, EMA, DEMA, RMA, WMA, VWMA) over a user-defined length (default: 220 periods).

The standard deviation of NUPL over a specified lookback period (default: 200 periods).

Z-Score Formula:

Z-Score = (Current NUPL - Moving Average of NUPL) / Standard Deviation of NUPL

This normalization allows the indicator to highlight extreme market conditions regardless of the raw NUPL scale.

How This Indicator Can Be Used

Trend Following

The NUPL Z-Score indicator employs a trend-following system with adjustable thresholds to generate trading signals:

Long Signals: Triggered when the Z-Score crosses above the Long Threshold (default: 0.26).

Short Signals: Triggered when the Z-Score crosses below the Short Threshold (default: -0.62).

Visual Representations:

Green up-triangles: Indicate long entry points (plotted below the bar).

Red down-triangles: Indicate short entry points (plotted above the bar).

Color-coded elements:

Candles and Z-Score plot turn teal (#00ffdd) for long positions.

Candles and Z-Score plot turn magenta (#ff00bf) for short positions.

These signals leverage historical NUPL trends to identify potential momentum shifts, aiding traders in timing entries and exits.

Overbought/Oversold Conditions

The indicator flags extreme market states using additional thresholds:

Overbought Threshold (default: 3.0): When the Z-Score exceeds this level, the market may be significantly overvalued, hinting at potential selling pressure. Highlighted with a light magenta background (#ff00bf with 75% transparency).

Oversold Threshold (default: -2.0): When the Z-Score drops below this level, the market may be significantly undervalued, suggesting buying opportunities. Highlighted with a light teal background (#00ffdd with 75% transparency).

These extreme Z-Score levels have historically aligned with major market peaks and troughs, making them useful for medium- to long-term position management.

Customization Options

Traders can tailor the indicator to their preferences:

Cryptocurrency Source: Choose between BTC or ETH.

Moving Average Type: Select from SMA, EMA, DEMA, RMA, WMA, or VWMA.

Moving Average Length: Adjust the period for the NUPL moving average (default: 220).

Z-Score Lookback Period: Set the historical window for Z-Score calculation (default: 200).

Thresholds: Fine-tune values for: Long Threshold (default: 0.26), Short Threshold (default: -0.62), Overbought Threshold (default: 3.0), Oversold Threshold (default: -2.0)

These options enable users to adapt the indicator to various trading strategies and risk profiles.

Alerts

The indicator supports four alert conditions to keep traders informed:

NUPL Long Opportunity: Alerts when a long signal is triggered.

NUPL Short Opportunity: Alerts when a short signal is triggered.

NUPL Overbought Condition: Alerts when the Z-Score exceeds the overbought threshold.

NUPL Oversold Condition: Alerts when the Z-Score falls below the oversold threshold.

These alerts allow traders to monitor key opportunities without constantly watching the chart.

Earnings Trading StrategyThe Earnings Trade Strategy automates the process of entering and exiting trades based on earnings announcements for Apple (AAPL). It allows users to take a position—either long (buy) or short (sell short)—on the trading day before an earnings announcement and close that position on the trading day after the announcement. By leveraging TradingView’s Paper Trading environment, the strategy enables users to simulate trades and collect performance data over a 6-month period in a risk-free setting.

Dynamic Support and Resistance ### Indicator: Dynamic Support and Resistance

#### Overview:

The *Dynamic Support and Resistance* indicator is a powerful tool designed to help traders identify key price levels on a chart. It dynamically calculates support and resistance levels based on pivot points and the Average True Range (ATR). The indicator also highlights broken support and resistance zones, providing visual cues for potential trend reversals or continuations.

---

### Key Features:

1. *Dynamic Support and Resistance Levels*:

- The indicator identifies support and resistance levels using pivot highs and lows within a user-defined range.

- These levels are adjusted using the ATR to account for market volatility, making them more responsive to changing market conditions.

2. *Support and Resistance Zones*:

- The indicator draws boxes around the support and resistance levels, with customizable colors and widths.

- The width of the zones is determined by the ATR and a user-defined multiplier, allowing traders to adjust the sensitivity of the zones.

3. *Broken Zones*:

- When price breaks through a support or resistance zone, the zone is highlighted with a distinct color to indicate a potential shift in market sentiment.

- Traders can limit the number of broken zones displayed on the chart to avoid clutter.

4. *Customizable Inputs*:

- *Range Candle Count*: Defines the number of candles analyzed to determine pivot points. Increasing this value will result in fewer but more significant levels, while decreasing it will produce more levels that are sensitive to shorter-term price movements.

- *ATR Period*: Controls the sensitivity of the ATR calculation. A shorter period makes the ATR more responsive to recent price changes, while a longer period smooths it out.

- *Box Width Multiplier*: Adjusts the width of the support and resistance zones. A higher multiplier creates wider zones, which may be useful in more volatile markets.

- *Max Broken Zones*: Limits the number of broken zones displayed on the chart. This helps keep the chart clean and focused on the most recent breaks.

---

### How It Works:

1. *Pivot Points*:

- The indicator identifies pivot highs and lows within the specified range. These pivots serve as the basis for calculating support and resistance levels.

2. *ATR Adjustment*:

- The ATR is used to adjust the support and resistance levels, making them more dynamic and responsive to market volatility.

3. *Zone Creation*:

- Support and resistance zones are drawn as boxes around the pivot levels. The width of these zones is determined by the ATR and the box width multiplier.

4. *Zone Breaks*:

- When price breaks through a zone, the zone is highlighted with a distinct color, and the broken zone is added to an array. If the number of broken zones exceeds the user-defined limit, the oldest broken zone is removed from the chart.

---

### How to Use:

1. *Trend Identification*:

- Use the support and resistance levels to identify key price levels where the market may reverse or consolidate.

- Broken zones can signal potential trend reversals or continuations.

2. *Entry and Exit Points*:

- Traders can use the support and resistance zones as potential entry or exit points. For example, buying near support or selling near resistance.

- Broken zones can be used as confirmation for breakout strategies.

3. *Risk Management*:

- The width of the zones can help traders set stop-loss levels. For example, placing a stop-loss just outside a support or resistance zone.

4. *Customization*:

- Adjust the input parameters to suit your trading style and the specific market conditions. For example, increase the range candle count for longer-term analysis or decrease it for shorter-term trading.

---

### Who Should Use This Indicator?

- *Swing Traders*: Can use the indicator to identify key levels for potential reversals or breakouts.

- *Day Traders*: Can benefit from the dynamic levels and zones, especially in volatile markets.

- *Position Traders*: Can use the indicator to identify long-term support and resistance levels.

- *Breakout Traders*: Can use the broken zones to confirm breakouts and plan their trades accordingly.

---

### Input Parameters and Their Effects:

1. *Range Candle Count*:

- *Increase*: Produces fewer but more significant levels, suitable for longer-term analysis.

- *Decrease*: Produces more levels, sensitive to shorter-term price movements.

2. *ATR Period*:

- *Increase*: Smoothens the ATR, making the levels less sensitive to recent price changes.

- *Decrease*: Makes the ATR more responsive to recent price changes, resulting in more dynamic levels.

3. *Box Width Multiplier*:

- *Increase*: Creates wider zones, suitable for more volatile markets.

- *Decrease*: Creates narrower zones, suitable for less volatile markets.

4. *Max Broken Zones*:

- *Increase*: Displays more broken zones on the chart, providing more historical context.

- *Decrease*: Keeps the chart clean by displaying only the most recent broken zones.

---

### Conclusion:

The *Dynamic Support and Resistance* indicator is a versatile tool that can be adapted to various trading styles and market conditions. By dynamically adjusting to market volatility and highlighting key price levels, it provides traders with valuable insights into potential support and resistance areas. Whether you're a swing trader, day trader, or position trader, this indicator can help you make more informed trading decisions.

---

### Publishing on TradingView:

- *Title*: Dynamic Support and Resistance

- *Description*: A dynamic support and resistance indicator that uses pivot points and ATR to identify key price levels. Includes customizable support/resistance zones and highlights broken zones for breakout trading.

- *Tags*: support, resistance, ATR, pivot points, breakout, trading, indicator

- *Access*: Public or Invite-only, depending on your preference.

This indicator is ready to be published on TradingView, and the detailed description above will help users understand its functionality and how to use it effectively.

Fibonacci RangeFibonacci Range 50 Indicator

The Fibonacci Range 50 indicator is designed to help traders identify potential price reversal zones and breakout levels by utilizing the 50% Fibonacci retracement level as a key reference point. This indicator is particularly useful for traders who rely on technical analysis and price action to make informed trading decisions.

How It Works:

Identifies the Range – The indicator automatically detects a significant price range, typically based on the highest and lowest points of a given session (e.g., Asian session, previous day’s range, or a custom timeframe).

Plots Fibonacci Levels – The key 50% Fibonacci retracement level is calculated within this range, acting as a dynamic midpoint that often serves as a pivot zone for price movements.

Breakout & Reversal Signals –

If the price rejects the 50% level, it may indicate a trend continuation or range-bound movement.

If the price breaks above or below the range with momentum, it may signal a potential breakout trade opportunity.

Key Features:

✅ Automatic Fibonacci Level Calculation – No manual drawing required.

✅ Customizable Time Ranges – Allows traders to adjust the indicator based on their preferred trading session.

✅ Works Across Different Markets – Effective for Forex, Crypto, and Stock trading.

✅ Breakout & Reversal Strategy Integration – Can be used in conjunction with other indicators such as Moving Averages, RSI, and MACD.

Ideal For:

Intraday traders looking for high-probability setups.

Swing traders identifying potential turning points.

Traders using breakout strategies based on price action.

This indicator provides traders with clear and actionable insights to improve their trade entries, stop-loss placements, and profit targets. 🚀

Market Structure Break with Volume & ATR#### Indicator Overview:

The *Market Structure Break with Volume & ATR (MSB+VolATR)* indicator is designed to identify significant market structure breakouts and breakdowns using a combination of price action, volume analysis, and volatility (ATR). It is particularly useful for traders who rely on higher timeframes for swing trading or positional trading. The indicator highlights bullish and bearish breakouts, retests, fakeouts, and potential buy/sell signals based on RSI overbought/oversold conditions.

---

### Key Features:

1. *Market Structure Analysis*:

- Identifies swing highs and lows on a user-defined higher timeframe.

- Detects breakouts and breakdowns when price exceeds these levels with volume and ATR validation.

2. *Volume Validation*:

- Ensures breakouts are accompanied by above-average volume, reducing the likelihood of false signals.

3. *ATR Filter*:

- Filters out insignificant breakouts by requiring the breakout size to exceed a multiple of the ATR.

4. *RSI Integration*:

- Adds a momentum filter by considering overbought/oversold conditions using RSI.

5. *Visual Enhancements*:

- Draws colored boxes to highlight breakout zones.

- Labels breakouts, retests, and fakeouts for easy interpretation.

- Displays stop levels for potential trades.

6. *Alerts*:

- Provides alert conditions for buy and sell signals, enabling real-time notifications.

---

### Input Settings and Their Effects:

1. **Timeframe (tf):

- Determines the higher timeframe for market structure analysis.

- *Effect*: A higher timeframe (e.g., 1D) reduces noise and provides more reliable swing points, while a lower timeframe (e.g., 4H) may generate more frequent but less reliable signals.

2. **Lookback Period (length):

- Defines the number of historical bars used to identify significant highs and lows.

- *Effect*: A longer lookback period (e.g., 50) captures broader market structure, while a shorter period (e.g., 20) reacts faster to recent price action.

3. **ATR Length (atr_length):

- Sets the period for ATR calculation.

- *Effect*: A shorter ATR length (e.g., 14) reacts faster to recent volatility, while a longer length (e.g., 21) smooths out volatility spikes.

4. **ATR Multiplier (atr_multiplier):

- Filters insignificant breakouts by requiring the breakout size to exceed ATR × multiplier.

- *Effect*: A higher multiplier (e.g., 0.2) reduces false signals but may miss smaller breakouts.

5. **Volume Multiplier (volume_multiplier):

- Sets the volume threshold for breakout validation.

- *Effect*: A higher multiplier (e.g., 1.0) ensures stronger volume confirmation but may reduce the number of signals.

6. **RSI Length (rsi_length):

- Defines the period for RSI calculation.

- *Effect*: A shorter RSI length (e.g., 10) makes the indicator more sensitive to recent price changes, while a longer length (e.g., 20) smooths out RSI fluctuations.

7. *RSI Overbought/Oversold Levels*:

- Sets the thresholds for overbought (default: 70) and oversold (default: 30) conditions.

- *Effect*: Adjusting these levels can make the indicator more or less conservative in generating signals.

8. **Stop Loss Multiplier (SL_Multiplier):

- Determines the distance of the stop-loss level from the entry price based on ATR.

- *Effect*: A higher multiplier (e.g., 2.0) provides wider stops, reducing the risk of being stopped out prematurely but increasing potential losses.

---

### How It Works:

1. *Breakout Detection*:

- A bullish breakout occurs when the close exceeds the highest high of the lookback period, with volume above the threshold and breakout size exceeding ATR × multiplier.

- A bearish breakout occurs when the close falls below the lowest low of the lookback period, with similar volume and ATR validation.

2. *Retest Logic*:

- After a breakout, if price retests the breakout zone without closing beyond it, a retest label is displayed.

3. *Fakeout Detection*:

- If price briefly breaks out but reverses back into the range, a fakeout label is displayed.

4. *Buy/Sell Signals*:

- A sell signal is generated when price reverses below a bullish breakout zone and RSI is overbought.

- A buy signal is generated when price reverses above a bearish breakout zone and RSI is oversold.

5. *Stop Levels*:

- Stop-loss levels are plotted based on ATR × SL_Multiplier, providing a visual guide for risk management.

---

### Who Can Use It and How:

1. *Swing Traders*:

- Use the indicator on daily or 4-hour timeframes to identify high-probability breakout trades.

- Combine with other technical analysis tools (e.g., trendlines, Fibonacci levels) for confirmation.

2. *Positional Traders*:

- Apply the indicator on weekly or daily charts to capture long-term trends.

- Use the stop-loss levels to manage risk over extended periods.

3. *Algorithmic Traders*:

- Integrate the buy/sell signals into automated trading systems.

- Use the alert conditions to trigger trades programmatically.

4. *Risk-Averse Traders*:

- Adjust the ATR and volume multipliers to filter out low-probability trades.

- Use wider stop-loss levels to avoid premature exits.

---

### Where to Use It:

- *Forex*: Identify breakouts in major currency pairs.

- *Stocks*: Spot trend reversals in high-volume stocks.

- *Commodities*: Trade breakouts in gold, oil, or other commodities.

- *Crypto*: Apply to Bitcoin, Ethereum, or other cryptocurrencies for volatile breakout opportunities.

---

### Example Use Case:

- *Timeframe*: 1D

- *Lookback Period*: 50

- *ATR Length*: 14

- *ATR Multiplier*: 0.1

- *Volume Multiplier*: 0.5

- *RSI Length*: 14

- *RSI Overbought/Oversold*: 70/30

- *SL Multiplier*: 1.5

In this setup, the indicator will:

1. Identify significant swing highs and lows on the daily chart.

2. Validate breakouts with volume and ATR filters.

3. Generate buy/sell signals when price reverses and RSI confirms overbought/oversold conditions.

4. Plot stop-loss levels for risk management.

---

### Conclusion:

The *MSB+VolATR* indicator is a versatile tool for traders seeking to capitalize on market structure breakouts with added confirmation from volume and volatility. By customizing the input settings, traders can adapt the indicator to their preferred trading style and risk tolerance. Whether you're a swing trader, positional trader, or algorithmic trader, this indicator provides actionable insights to enhance your trading strategy.

Earnings Date and CountdownOverview:

The Earnings Date & Countdown (EDC) Indicator displays the next earnings date for a stock and a countdown of days remaining until the earnings announcement. This helps traders stay informed about upcoming earnings events and adjust their strategies accordingly.

Features:

- Displays the next earnings date in a customizable format.

- Accurate countdown of days remaining until the earnings event (optional).

- Automatically adjusts for time zones and ensures the correct number of full calendar days.

- Customizable display position for easy visibility on the chart.

Settings:

- Show day of the week: option to toggle the day of the week.

- Date Format: choose between dd mmm, mmm dd, dd/mm or mm/dd.

- Show year: option to toggle the year display.

- Show (countdown): option to toggle the countdown display.

- Indicator position: adjusts the location of the display on the chart.

Why use this indicator?

Earnings reports often cause significant price movements.

This indicator helps traders plan ahead by keeping earnings dates visible and tracking the countdown with precision directly on the chart.

Daily Open Rangethis indicator draw the open of the day with a box of high and low ( +1 and -1 ) automatically , you have the ability to select which hour you want to to draw from the inputs and you have the ability to change the style of the range as well

OANDA:XAUUSD

FVG Visual Trading ToolHow to Use the FVG Tool

1. Identify the FVG Zone

Bullish FVG: Look for green boxes that represent potential support zones. These are areas where price is likely to retrace before continuing upward.

Bearish FVG: Look for red boxes that represent potential resistance zones. These are areas where price is likely to retrace before continuing downward.

2. Set Up Your Trade

Entry: Place a limit order at the retracement zone (inside the FVG box). This ensures you enter the trade when the price retraces into the imbalance.

Stop-Loss (SL): Place your stop-loss just below the FVG box for bullish trades or just above the FVG box for bearish trades. The tool provides a suggested SL level.

Take-Profit (TP): Set your take-profit level at a 2:1 risk-reward ratio (or higher). The tool provides a suggested target level.

3. Let the Trade Run

Once your trade is set up, let it play out. Avoid micromanaging the trade unless market conditions change drastically.

Step-by-Step Example

Bullish FVG Trade

Identify the FVG:

A green box appears, indicating a bullish FVG.

The tool provides the target price (e.g., 0.6371) and the stop-loss level (e.g., 0.6339).

Set Up the Trade:

Place a limit buy order at the retracement zone (inside the green box).

Set your stop-loss just below the FVG box (e.g., 0.6339).

Set your take-profit at a 2:1 risk-reward ratio or the suggested target (e.g., 0.6371).

Monitor the Trade:

Wait for the price to retrace into the FVG zone and trigger your limit order.

Let the trade run until it hits the take-profit or stop-loss.

Bearish FVG Trade

Identify the FVG:

A red box appears, indicating a bearish FVG.

The tool provides the target price and the stop-loss level.

Set Up the Trade:

Place a limit sell order at the retracement zone (inside the red box).

Set your stop-loss just above the FVG box.

Set your take-profit at a 2:1 risk-reward ratio or the suggested target.

Monitor the Trade:

Wait for the price to retrace into the FVG zone and trigger your limit order.

Let the trade run until it hits the take-profit or stop-loss.

Key Features of the Tool in Action

Visual Clarity:

The green and red boxes clearly show the FVG zones, making it easy to identify potential trade setups.

Labels provide the target price and stop-loss level for quick decision-making.

Risk-Reward Management:

The tool encourages disciplined trading by providing predefined SL and TP levels.

A 2:1 risk-reward ratio ensures that profitable trades outweigh losses.

Hands-Off Execution:

By placing limit orders, you can let the trade execute automatically without needing to monitor the market constantly.

Best Practices

Trade in the Direction of the Trend:

Use higher timeframes (e.g., 4-hour or daily) to identify the overall trend.

Focus on bullish FVGs in an uptrend and bearish FVGs in a downtrend.

Combine with Confirmation Signals:

Look for additional confirmation, such as candlestick patterns (e.g., engulfing candles) or indicator signals (e.g., RSI, MACD).

Adjust Parameters for Volatility:

For highly volatile markets, consider increasing the stop-loss percentage to avoid being stopped out prematurely.

Avoid Overtrading:

Not every FVG is a good trading opportunity. Be selective and only trade setups that align with your strategy.

Backtest and Optimize:

Use historical data to test the tool and refine your approach before trading live.

Common Mistakes to Avoid

Entering Without Confirmation:

Wait for price to retrace into the FVG zone before entering a trade.

Avoid chasing trades that have already moved away from the zone.

Ignoring Risk Management:

Always use a stop-loss to protect your account.

Stick to a consistent risk-reward ratio.

Trading Against the Trend:

Avoid taking trades that go against the prevailing market trend unless there is strong evidence of a reversal.

Final Thoughts

The FVG Visual Trading Tool is a powerful aid for identifying high-probability trade setups. By following the steps outlined above, you can use the tool to trade with confidence and discipline. Remember, no tool guarantees success, so always combine it with sound trading principles and proper risk management